Sample Category Title

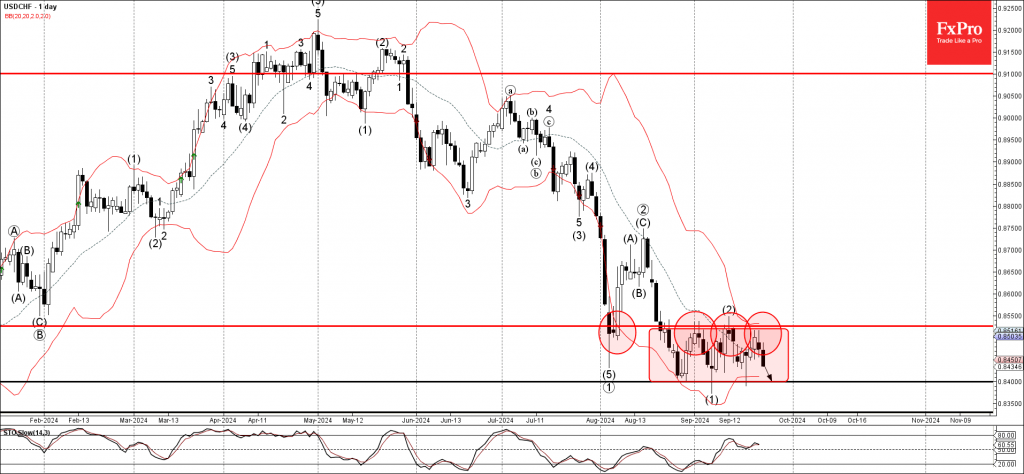

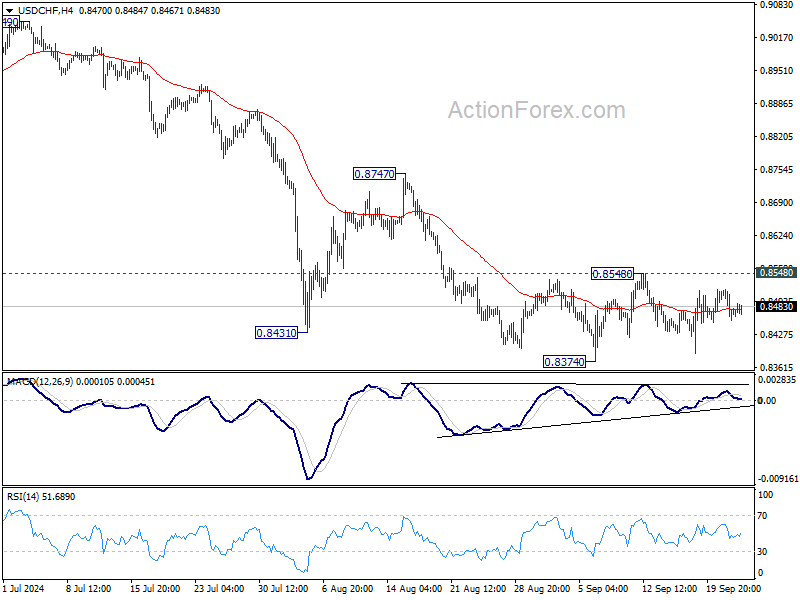

USDCHF Wave Analysis

- USDCHF reversed from resistance area

- Likely to fall to support level 0.8400

USDCHF currency pair recently reversed down from the resistance area located at the intersection of the key resistance level 0.8525 (upper border of the narrow sideways price range inside which the pair is moving from August) and the upper daily Bollinger Band.

The downward reversal from this resistance area is likely to form the daily Evening Star – if the pair closes today near the current levels.

Given the clear daily downtrend, USCHF can be expected to fall further to the next support level 0.8400 (lower boundary of the active sideways price range).

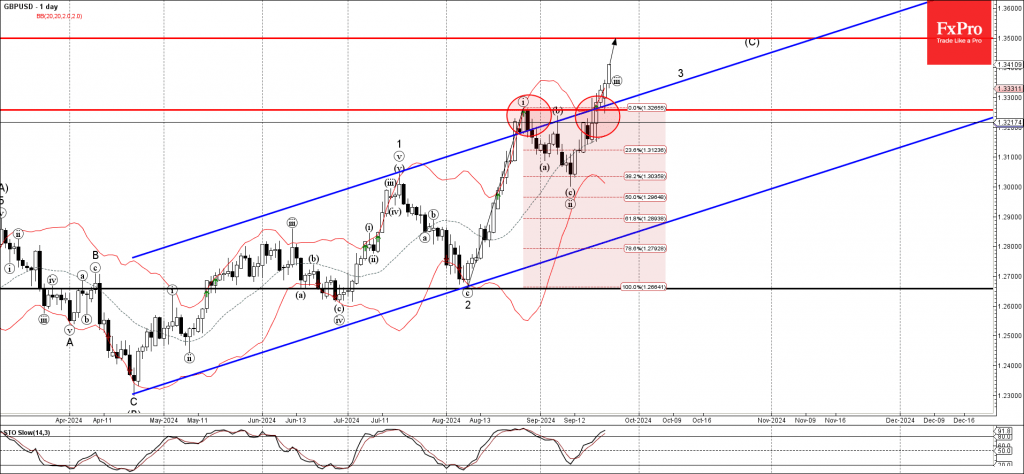

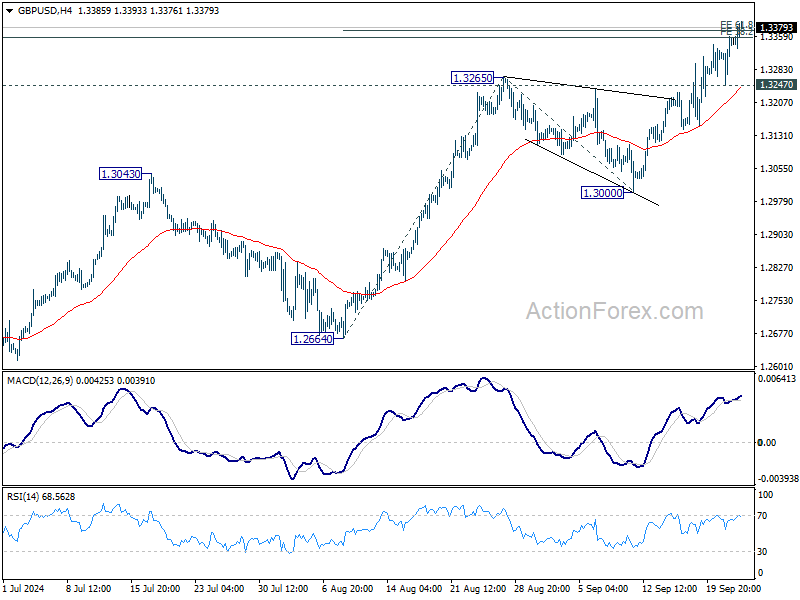

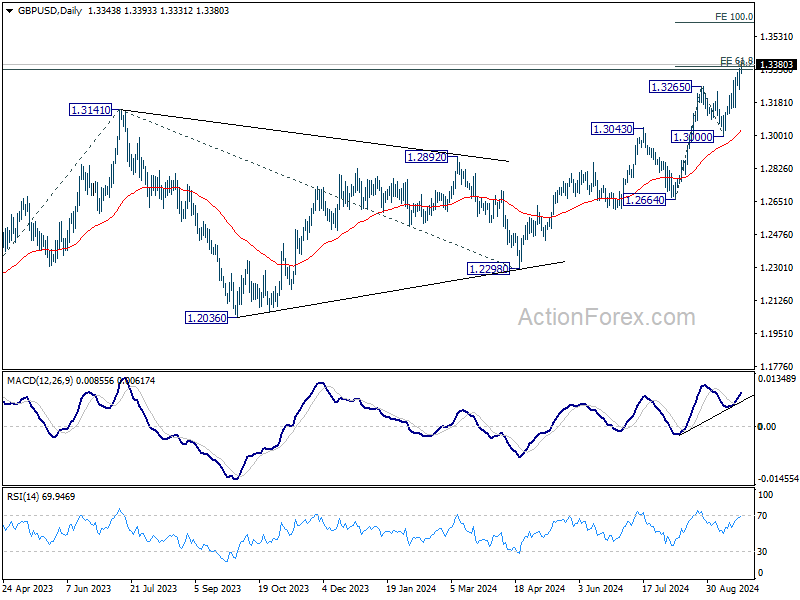

GBPUSD Wave Analysis

- GBPUSD broke resistance area

- Likely to rise to resistance level 1.3500

GBPUSD recently broke the resistance area located at the intersection of the key resistance level 1.3255 (former monthly high from August) and the resistance trendline of the daily up channel from April.

The breakout of this resistance area accelerated the active impulse waves iii and 3 – which belong to the multi-month upward impulse sequence (C) from April.

Given the clear daily uptrend and the strongly bearish US dollar sentiment, GBPUSD can be expected to rise further to the next resistance level 1.3500, target for the completion of wave (C).

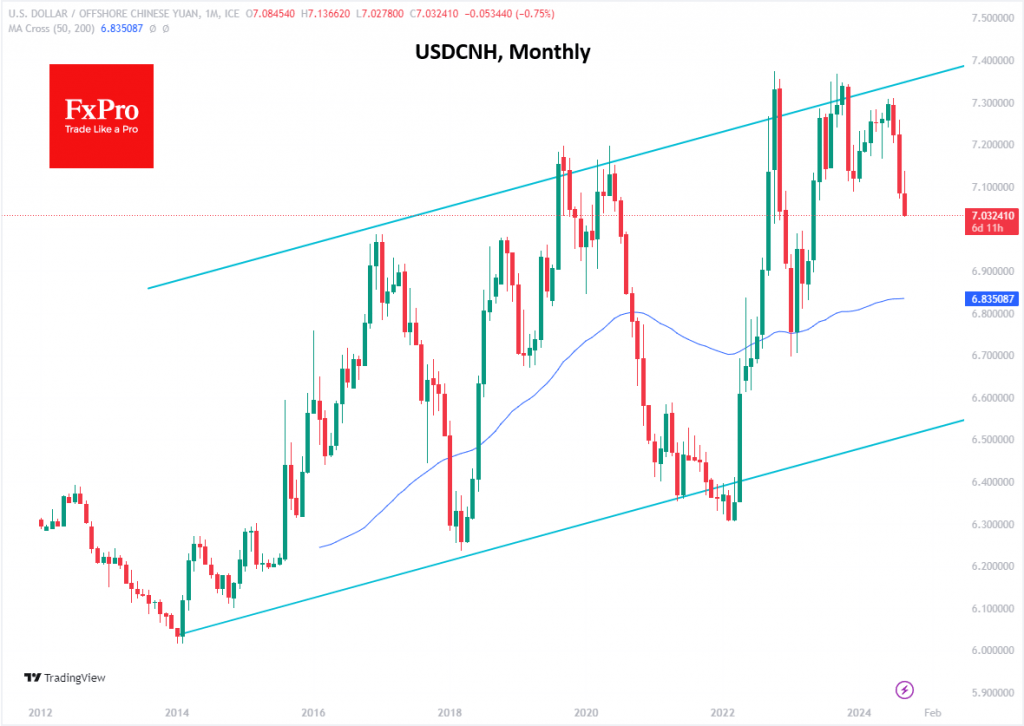

China’s Stimulus Boosts Yuan and Shares

China has unveiled stimulus measures to boost the economy. The scale is not impressive – it is not an all-out crisis salvo but rather an attempt to stop a slide here and there. The People’s Bank of China announced a 0.2 percentage point cut in benchmark interest rates and a 0.25-0.50 percentage point cut in the reserve requirement ratio, freeing up 1 trillion yuan ($142 billion) and easing the burden of mortgage payments.

Financial markets welcomed the move, which was larger than expected. The Hang Seng Index rose 4% on Tuesday, taking the rally from September lows to 13%. However, unlike the S&P500, which has stormed to all-time highs, this is only a four-month high and about 42% below the 2018 peak. China’s blue-chip index is about the same distance from its highs, highlighting the impact of trade wars on the country’s financial market.

The opposite is true for bonds, where low interest rates and chronically low inflation have led to historically low government bond yields, meaning their prices have risen.

The yuan has gained 3.7% against the dollar over the past three months, not much by forex standards but impressive for the USDCNH. The pair has pulled back to 7.03, the low since May 2023, and has reversed from the area of long-term highs at 7.30.

The strengthening of the yuan is an interesting market reaction, suggesting capital inflows from external markets. It won’t help competitiveness, but it could boost economic activity through investment.

In our view, despite the rate cut, the yuan could strengthen further, possibly towards the cyclical support level around 6.50.

The announced stimulus could bring some capital back into Chinese markets, especially if the Politburo sees an opportunity to support the economy and the struggling construction industry.

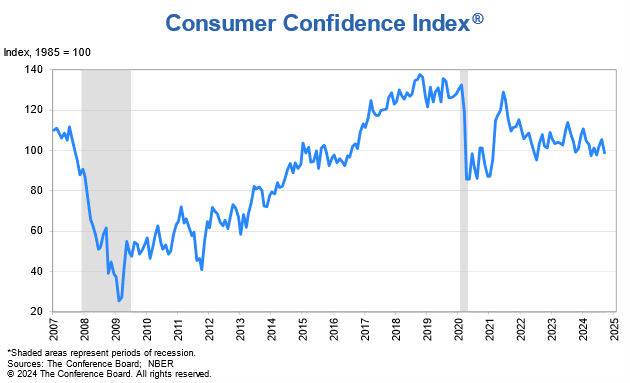

US consumer confidence falls to 98.7, largest slump since 2021

US Conference Board Consumer Confidence Index experienced a sharp drop in September, falling from 103.3 to 98.7, significantly below market expectations of 103.5. This marks the largest decline in consumer confidence since August 2021. Present Situation Index, which assesses current economic conditions, plunged by -10.3 points to 124.3, while Expectations Index, which gauges consumers’ outlook on future conditions, also dropped by -4.6 points to 81.7.

Dana M. Peterson, Chief Economist at The Conference Board, commented, “Consumer confidence dropped in September to near the bottom of the narrow range that has prevailed over the past two years.” She further highlighted that the decline affected all five components of the Index, with consumers’ outlook on current business conditions turning negative. Furthermore, views on the labor market continued to soften, with growing pessimism about both future employment prospects and income expectations.

Sunset Market Commentary

Markets

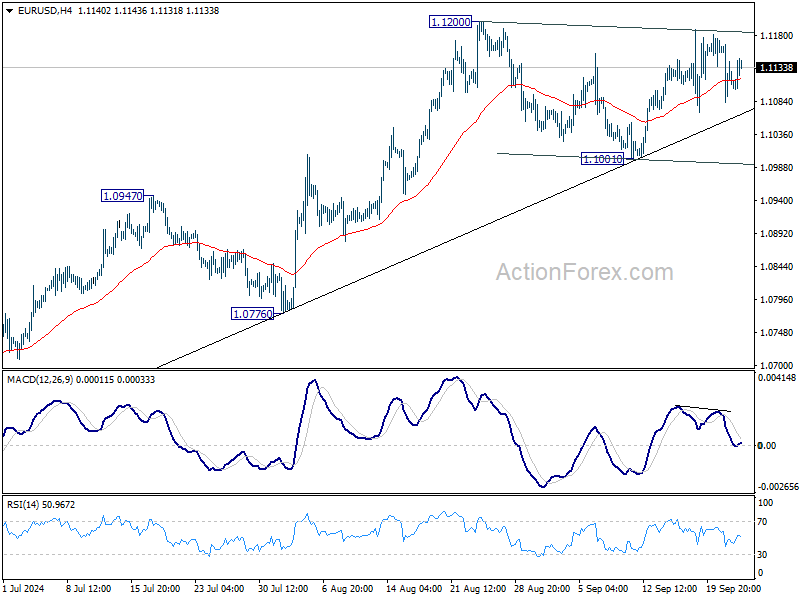

A barrage of Chinese monetary stimulus measures lifted the likes of the CSI 300 with more than 4% and jumpstarted European dealings too. The EuroStoxx50 rose as much as 1.4%, lead by consumer discretionary/luxury sector, before paring gains to around 1% currently. WS opened slightly higher. The risk-on environment leaves some traces on bond markets as well with core bonds losing marginal ground. US Treasuries underperform Bunds, with net daily changes ranging between +1.2 (2-yr) to +4.5 bps (30-yr). The US 10-yr yield (+4.2 bps) tries to recoup first minor resistance of 3.78% (December 2023 low) with the bottoming out at the long end of the curve now firmly taking shape. German rate changes vary from -1.9 bps (2-yr) to 3 bps (30-yr). The German Ifo sentiment indicator undershot analyst estimates but that shouldn’t surprise much after yesterday’s disastrous PMIs. The combined reading fell from 86.6 to 85.4, matching the post-pandemic lows of 85.3. The indicator was lower only during the GFC and pandemic year 2020. Especially the current assessment (84.4, down from 86.4, new post-pandemic low) is in distress territory. The expectations gauge fell to 86.3, from 86.8. The darkening European economic outlook reopened the debate on an October rate cut. Lagarde and many of her colleagues dismissed it shortly after the September meeting but Estonian governing council member Muller is the first since the PMIs to not “totally” rule it out. He did add it would be easier to decide in December. European money markets give it a probability just short of 60%. Sticking to central bank speech, Fed’s Bowman explained her dissenting 25 bps rate cut vote last week. She said she still sees greater risks to price stability, “especially when the labour market continues to be near estimates of full employment.” A 25 bps move “would have better reinforced the strength in economic conditions, while also confidently recognizing progress toward our goals,” Bowman said, adding that she preferred a “measured” approach going forward. It’s classic risk-on in other markets as well, including commodities. Oil prices rise 2.2% (Brent $75.5/b), buoyed by elevated tensions in the Middle East as well after another major Israeli strike on Hezbollah targets in Lebanon. Iron adds about 2%. The FX space is a similar story with safe havens including the Japanese yen suffering. USD/JPY – though off intraday highs – fills bids around 144.1. Cyclical sensitive currencies such as the Aussie (also helped by the RBA’s status quo this morning) and kiwi dollar are among the best performers, together with the NOK and SEK. The euro has a slight edge over the dollar, allowing EUR/USD to recoup a good chunk of yesterday’s damage. The pair is changing hands around 1.114. Sterling holds on to yesterday’s impressive gains against the euro. EUR/GBP hovers around Monday’s closing levels of 0.832. Cable (GBP/USD) is readying an attack of the 1.34 big figure.

News & Views

Belgium business confidence continued to deteriorate in September, sliding from -12.6 to -13.3 (vs -12.4 expected). The fourth consecutive decline bring business confidence to the lowest level since January. Details showed weakness in manufacturing (-17.7 from -16.5) and building (-11.7 from -7.5) more than offsetting improvements in trade (-6.9 from -16.6) and business services (1.9 from 0.4). Manufacturing businesses assessed stock levels less favorably and also expressed much more demand expectations. Building business leaders indicated that they expect a slight decline in demand but were mainly more negative in their assessment of recent developments in both equipment use and orders books. Last week, Belgian consumer confidence fell from -3 to -7, matching the 2024 low set in May.

Czech economic sentiment improved from 93.7 to 97 in September, while consensus only expected a stabilization. It is the best outcome since June and carried by a broad-based improvement in business confidence (96.8 from 93). Confidence increased by 5.1 points in selected services, 3 in construction, 2.9 in industry and 1.3 in trade. Consumer confidence more or less stabilized (97.9 from 97.3) with subcomponents measuring overall economic & personal financial expectations over the next 12 months showing no meaningful direction neither. The share of consumers who believe that the current period is not conducive to making large purchases fell for the second consecutive month. The Czech koruna didn’t respond to the release with EUR/CZK testing this month’s high at 25.17 going into tomorrow’s central bank meeting where the CNB is expected to deliver a 25 bps rate cut to 4.25%.

Graphs

EUR/HUF: forint ekes out slight gain after MNB cut as expected (-25 bps to 6.5%) but sticks a cautious and data-driven approach

AUD/USD: Aussie dollar tests January top after RBA keeps rates steady as inflation is not expected to return to 2% before 2026

Spread between 10-yr and 2-yr EMU swap recently turned positive for first time since 2022 as ECB easing bets rise on darkening outlook

Oil (Brent, $/b) rises on hopes of a Chinese revival after the recent string of monetary measures

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1073; (P) 1.1121; (R1) 1.1158; More....

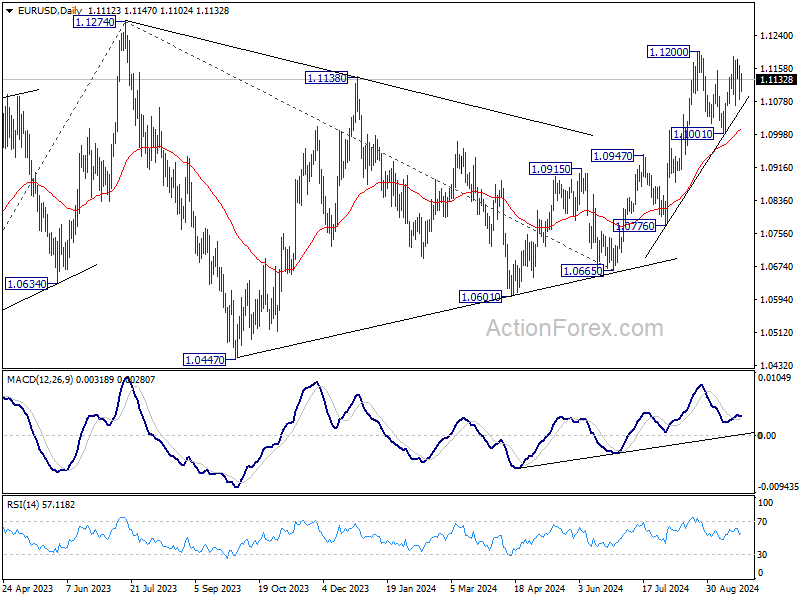

No change in EUR/USD's outlook as range trading continues. Intraday bias remains neutral. Further rally is expected as long as 1.1001 support holds. On the upside, above 1.1200 will target 1.1274 high. Firm break there will resume larger up trend. However, firm break of 1.1001 will indicate near term bearish reversal.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 might have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm resumption of whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3278; (P) 1.3318; (R1) 1.3389; More...

Intraday bias in GBP/USD stays on the upside. Decisive break of 61.8% projection of 1.2664 to 1.3265 from 1.3000 at 1.3371 will pave the way to 100% projection at 1.3601 next. On the downside, below 1.3247 minor support will turn intraday bias neutral and bring consolidations first. But outlook will stay bullish as long as 1.3000 support holds.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. Decisive break there will target 61.8% projection at 1.4022. For now, outlook will stay bullish as long as 1.2892 resistance turned support holds, even in case of deep pullback.

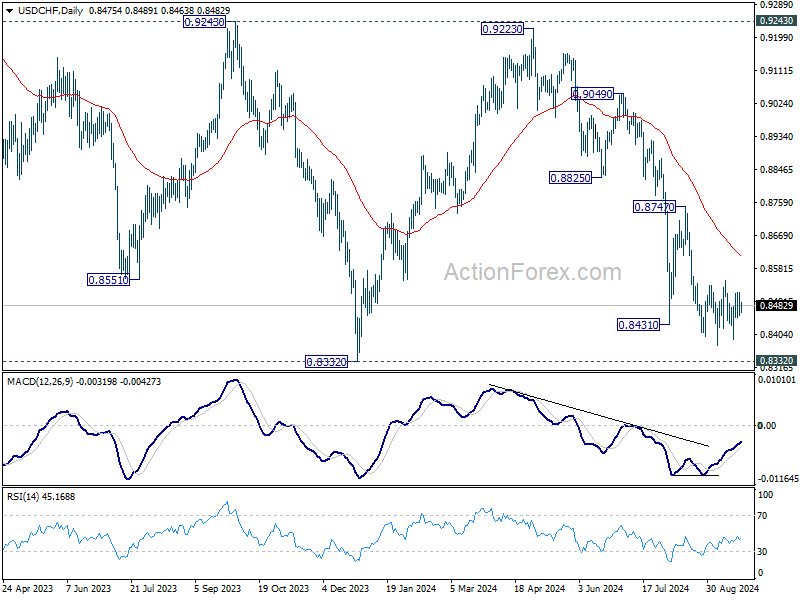

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8449; (P) 0.8484; (R1) 0.8510; More…

USD/CHF is still extending range trading from 0.8374 and intraday bias remains neutral. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. However, considering bullish convergence condition in 4H MACD, break of 0.8548 resistance will confirm short term bottoming, and turn bias back to the upside for 0.8747 resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

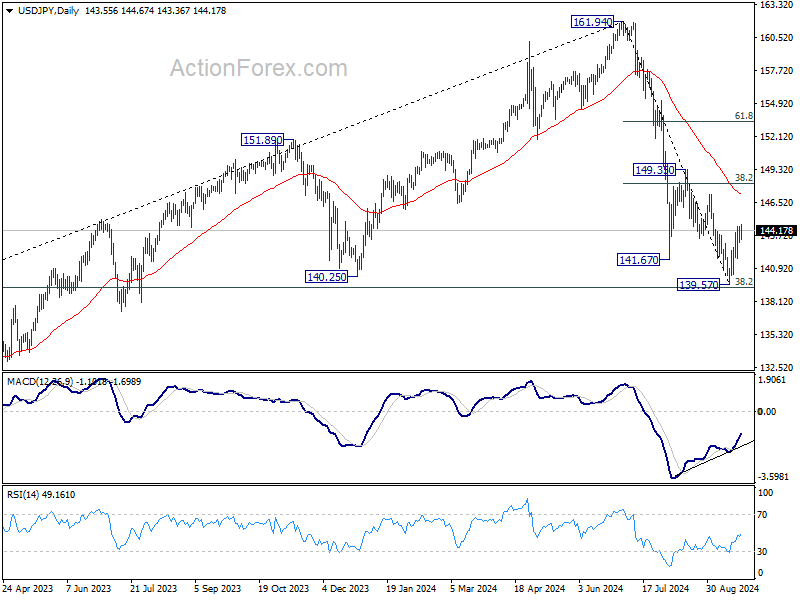

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.02; (P) 143.74; (R1) 144.32; More...

Despite loss of upside momentum as seen in 4H MACD, further rise is still in favor in USD/JPY with 141.73 minor support intact. Rebound from 139.57 short term bottom should extend to 38.2% retracement of 161.94 to 139.57 at 148.11. On the downside, below 141.73 will turn bias to the downside for retesting 139.57 instead.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Strong support could be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to contain downside, at least on first attempt. But in any case, risk will stay on the downside as long as 149.35 resistance holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.