Sample Category Title

RBA Minutes: No near-term rate cut expected, nothing ruled in or out

RBA's August meeting minutes revealed a thorough discussion on the merits of both a rate hike and a rate hold, ultimately leading to the decision to keep interest rates unchanged at 4.35%. The minutes reiterated that it is "unlikely that the cash rate target would be reduced in the short term." The minutes also noted that it is "not possible to either rule in or rule out" future changes in the cash rate

The decision to hold rates steady was seen as the best way to "balance the risks" to both inflation and the labor market, especially given the "prevailing uncertainties, market volatility, and market expectations."

RBA members emphasized the importance of placing "greater-than-usual weight on the flow of data" rather than relying solely on forecasts, due to the uncertainties surrounding the persistence of supply shocks. They noted that the data since the previous meeting had "not been sufficient to warrant a change in the stance of monetary policy."

Additionally, the minutes suggested that holding the cash rate target steady for a "longer period" than currently implied by market expectations could be enough to bring inflation back to target within a reasonable timeframe. However, the Board acknowledged that this approach would need to be reassessed at future meetings based on incoming data and evolving economic conditions.

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Sydney – 5 and 6 August 2024

Members present

Michele Bullock (Governor and Chair), Andrew Hauser (Deputy Governor), Ian Harper AO, Carolyn Hewson AO, Steven Kennedy PSM, Iain Ross AO, Elana Rubin AM, Alison Watkins AM

Members had granted leave of absence to Carol Schwartz AO, in accordance with section 18A of the Reserve Bank Act 1959.

Others present

Sarah Hunter (Assistant Governor, Economic), Christopher Kent (Assistant Governor, Financial Markets)

Anthony Dickman (Secretary), David Norman (Deputy Secretary)

Meredith Beechey Osterholm (Future Hub), Sally Cray (Chief Communications Officer), Natasha Cassidy (Deputy Head, Economic Analysis Department), Carl Schwartz (Acting Head, Domestic Markets Department), Penelope Smith (Head, International Department)

Economic conditions

Members began their discussion by considering developments in aggregate demand. Domestic demand had been a little stronger in early 2024 than had been expected in May, driven by household and public consumption. That said, household consumption growth remained well below pre-pandemic averages, even after the upward revisions to consumption from mid-2022 to the end of 2023, as discussed at the June meeting. The upside surprise in domestic demand had also occurred alongside robust growth in imports, leaving GDP growth somewhat lower than expected in the March quarter.

The available data suggested that household consumption had declined further on a per capita basis in the June quarter, but that the pre-conditions for a gradual pick-up in consumption growth remained in place. Real disposable incomes had stabilised earlier in the year and were expected to increase; prior strong growth in household net wealth would also provide some support to household consumption. There had been limited and preliminary indications that consumer confidence had increased a little in July following the implementation of the Stage 3 tax cuts. However, some households remained under significant financial pressure, particularly those with limited or no financial buffers. Members discussed the potential implications of varying trends in income and wealth.

Conditions in residential construction remained challenging. New dwelling supply had weakened, and ongoing cost pressures and labour shortages were constraining how quickly the pipeline of residential projects could be worked through. The shortage of labour was due, in part, to competition for workers from high levels of non-residential building activity. Liaison contacts expected activity on both detached homes and new apartments to slow over the year ahead, given the ongoing cost pressures and the subdued flow of new dwelling approvals. While there was still strong growth in underlying demand for housing, this had diminished slightly as the average household size had increased, possibly in response to higher rents and housing prices.

Labour market conditions in the June quarter had continued to ease gradually. The unemployment rate had increased a little but remained only modestly above its late-2022 trough. Members noted that the rise in the unemployment rate owed more to reduced flows of workers into employment than an increase in layoffs, which remained very low. Both the participation rate and the employment-to-population ratio remained high, and average hours worked had been a little higher than previously expected. Members also observed that the level of job vacancies remained well above both its pre-pandemic average and outcomes in other advanced economies, despite falling significantly from its peak. Many firms continued to report that finding suitable labour is an ongoing challenge.

Members discussed the June quarter inflation data, which were broadly in line with the forecast in May. Underlying inflation had eased a little, but in quarterly terms the outcome was not much lower than it was a year earlier. Inflation in prices of market services had eased in the June quarter but remained high, given persistently strong growth in both labour and domestic non-labour costs. Members discussed trends in inflation for items whose prices are either regulated or partially indexed to past inflation, which collectively account for about one-quarter of the CPI basket. They noted that while overall inflation in these items had been high, this was consistent with historical experience. By contrast, inflation in the remainder of the CPI basket had been well above its historical average.

Members discussed the degree of spare capacity in the economy, which was a key judgement underpinning the staff forecasts. Based on the data and evidence over a period of time, the staff had assessed that the economy had less spare capacity than previously assumed. This reflected higher inflation outcomes over the preceding 12–18 months than could be explained by previous estimates of excess demand, and signals from labour market indicators and survey measures of capacity utilisation. Members discussed the considerable uncertainty around estimates of spare capacity and the need to reassess this judgement regularly as the data evolve.

Economic outlook

Members noted that the staff forecast for GDP growth over the year ahead had been revised higher. This was driven by an upward revision to the forecast for domestic final demand as the outlook for both household consumption and public demand had strengthened. Household consumption growth was expected to pick up in the second half of 2024, supported by an increase in real income growth from the Stage 3 tax cuts and declining inflation, as well as higher wealth. By contrast, the expected recovery in dwelling investment was now forecast to occur a little later than previously assumed. Despite the upward revisions, growth in GDP was still projected to remain below growth in aggregate supply for a period, bringing the economy to a more balanced state and thereby reducing inflationary pressure. However, considerable uncertainty around this judgement remained.

The labour market was expected to continue to ease gradually before stabilising in early 2026, consistent with the signal from leading indicators of labour demand such as job vacancies and hiring intentions. The forecast increase in the unemployment rate was consistent with the anticipated mildness of the downturn. The staff expected that the adjustment to slowing demand would continue to occur, in part, through lower average hours. Members discussed a scenario prepared by the staff in which the unemployment rate picked up more sharply, as had been the case in some peer economies, returning inflation to target sooner. They noted that this would be more likely to occur if businesses were currently hoarding labour. While the evidence that this was occurring seemed limited, members were alert to the possibility that labour demand could soften, perhaps quite rapidly.

Wages growth was judged to be past its peak and was expected to slow gradually as the labour market eased. Members debated how far – and how rapidly – wages growth would slow, and the implications of this for inflation, given the easing in the labour market, the structure of recent enterprise bargaining agreements and the declines in real wages since 2021. They also noted the need for productivity growth to recover in order to help reduce growth in unit labour costs. Members discussed the potential causes of the weakness in productivity growth since the pandemic, the impact of changes to industry composition and explanations for why productivity outcomes had been much stronger in the United States than elsewhere.

The forecast for underlying inflation had been revised higher since May. This reflected the stronger forecast for aggregate demand and the staff’s judgement that potential supply in the economy was less than previously assessed. As such, the forecast return to the inflation target range of 2–3 per cent was expected to be a little later than anticipated in May, and the central forecast had inflation approaching the midpoint in 2026. Headline inflation was expected to dip temporarily below 3 per cent in the year ahead, owing to new and extended electricity rebates and rent assistance, but then rebound following the legislated unwinding of some of these policies in mid-2025.

Members observed that a range of uncertainties could influence the outlook for inflation, including the evolution of the labour market, household saving behaviour and the extent of spare capacity, as well as global geopolitical developments. Members also noted the uncertainty surrounding future population growth. While requirements for offshore student visa applications had been tightened and the government had proposed caps on international student numbers, past population growth had surprised on the upside. Members noted, however, that the impact of population growth on inflation is not straightforward as it affects both aggregate demand and supply capacity.

Financial conditions

Members discussed developments in global financial markets and the significant bout of volatility prevailing at the time of the meeting.

Members noted that several advanced economy central banks – including the Bank of Canada, the Bank of England, the European Central Bank and the Sveriges Riksbank – had lowered their policy rates in recent months. Market participants expected other central banks – including the US Federal Reserve and the Reserve Bank of New Zealand – to do likewise at coming meetings. This reflected progress on returning inflation to central banks’ targets and a softening in labour market conditions in several advanced economies. By contrast, the Bank of Japan had increased its policy rate and accelerated the process of balance sheet reduction, citing greater confidence that it would sustainably achieve its 2 per cent inflation target.

Members observed that the publication of weaker-than-expected US payroll data for July had triggered significant volatility in global financial markets. These data had caused market participants to expect a much faster pace of policy easing by the US Federal Reserve and some other central banks. Market sentiment had also been affected by a range of other factors, including US corporate financial results, questions about the optimistic valuations of some large technology companies, concerns about rising geopolitical tensions and investors’ portfolio adjustments. Government bond yields in most advanced economies had declined in response to the revised expectations for central bank policy rates. Risk asset prices, including for equities, had also fallen as markets reassessed the outlook for growth in advanced economies; this had followed a period of strong appetite for risk in financial markets, which had prompted increases in equity prices in May and June, in some cases to record highs.

The declines in global equity prices had been most notable in Japan. In large part, this reflected the significant appreciation of the yen in response to a narrowing of interest rate differentials between Japan and the rest of the world, which was weighing on the earnings outlook for Japanese exporters. It had also reflected an associated unwinding of so-called ‘carry trades’, whereby market participants borrow in yen at low interest rates to invest in higher yielding assets denominated in other currencies. The unwinding of yen carry trades was likely to be amplifying the decline in riskier asset prices globally.

Members noted that, at the time of the meeting, it was too soon to tell where financial markets would eventually settle. Most markets had continued to function well, and there were early indications that conditions had begun to stabilise.

In China, authorities had eased monetary policy modestly amid weak demand for credit, slowing economic activity and an uncertain economic outlook. Chinese Government bond yields had declined to historical lows and credit demand had eased further, particularly from households, as the protracted contraction in the property sector continued to weigh on the sentiment of consumers and home buyers. The authorities had continued to direct lending towards priority sectors – such as science, technology and manufacturing – which had helped to offset some of the impact of the property sector contraction on commodity prices.

The Australian dollar had depreciated on a trade-weighted basis since the previous meeting but remained within the range of recent years. A widening of interest rate differentials between Australia and other major advanced economies had supported the Australian dollar in early July. However, the appreciation had unwound amid the more recent deterioration in risk sentiment, liquidation of Australian dollar positions related to Japanese yen carry trades and declines in some key commodity prices. Members discussed the materiality of these recent market movements and observed that, if sustained, they could limit the pace of disinflation.

For Australia, members observed that financial conditions appeared to be less restrictive than had previously been the case. While the cash rate remained above estimates of the neutral rate, market participants had lowered their expectations for the path of the cash rate and there had been associated declines in bond yields. Housing credit growth had gradually increased, suggesting households had been more willing to borrow. Meanwhile, business credit growth had picked up and was well above its average since the global financial crisis. Funding conditions more generally for Australian financial and non-financial corporations remained favourable.

Members discussed conditions facing smaller businesses, including information from the Bank’s 32nd annual Small Business Finance Advisory Panel in July. When combined with information from the liaison program and from economic indicators and surveys, it was affirmed that conditions for small businesses were somewhat weaker than those for larger firms. Business insolvencies had increased, including for medium-sized enterprises, though were still below their pre-pandemic trend. Panellists reported that financial conditions generally had tightened over the prior year, mainly because of stricter lending standards. Bank lending to small businesses had not increased for some years.

Market expectations for the cash rate had moved materially in the run-up to the meeting, including falling in response to the June quarter CPI release and the shift in expectations for US monetary policy. Market pricing implied an expectation that the cash rate would be reduced by the end of the year.

Considerations for monetary policy

Turning to considerations for the policy decision, members noted that several developments over preceding months had supported the view that inflation would be slow to decline. Underlying inflation had fallen very little over the prior year in quarterly terms and, while the June quarter outcome had been in line with the staff’s forecast, inflation was still some way above target. The revised forecast was for inflation to take a little longer than previously thought to return sustainably to target. Members noted that there had also been a pattern since early 2023 of both Bank and market-implied forecasts modestly underpredicting inflation a few quarters in advance.

GDP growth remained weak, especially in per capita terms, and the labour market had continued to ease over prior months. Even so, domestic final demand had been stronger than expected over the year to the March quarter, employment growth was still strong and some firms continued to report that labour shortages were a constraint on output. The staff’s forecast for GDP growth had been revised higher since May. Members observed that two key judgements underpinned the forecast: that consumption growth would recover in line with its historical relationships with income and wealth; and that the labour market would continue to ease gradually but stabilise as GDP growth picks up. Members also discussed a third key judgement: that the gap between aggregate demand and supply was somewhat larger than previously assessed. They observed that the outlook for inflation and conditions in the labour market could be materially different if any of these judgements proved to be mistaken.

Members noted that the volatility in financial markets prevailing at the time of the meeting appeared to reflect a combination of market participants reassessing the outlook for US (and hence global) demand, and a partial unwinding of asset valuations that, for certain sectors, had been viewed as optimistic. Whether the adjustments in market prices would persist, however, and their implications for financial conditions were unclear.

In light of these developments, members assessed that the risk of inflation not returning to target within a reasonable timeframe had increased. This reflected the slow pace of disinflation over the preceding year, the staff’s judgement that the gap between aggregate demand and supply was larger than previously assessed, and the upward revision to the forecast for final demand. Members affirmed that their strategy was still to bring inflation back to target within a reasonable timeframe and their tolerance for this timeframe being pushed out further was limited. That said, members noted that the forecasts were uncertain. Importantly, they were also based on a conditioning assumption, derived from market expectations, that the cash rate would be lowered several times in the coming year, beginning later in 2024. Based on what they knew at the time of the meeting, members agreed that monetary policy would need to be tighter than this implied path in order to bring inflation sustainably back to target within a reasonable timeframe.

Given these observations, members considered their decision on the cash rate.

Raising the cash rate target at this meeting could be appropriate if members judged that the risk that inflation would not return to target in a reasonable timeframe had materially increased, either because of economic developments or because financial conditions were insufficiently tight.

Members discussed several developments that could suggest the risk of inflation not returning to the target range by late 2025 had risen materially. Underlying inflation was proving persistent and the central projection was now for inflation to return to target somewhat later than previously forecast. Members also noted that the persistence of cost pressures was a key theme reported by firms in liaison discussions. In addition, the staff’s assessment was that the gap between aggregate demand and supply would be wider than previously judged throughout the forecast period, because of both a stronger outlook for demand and a reassessment of the economy’s current spare capacity. Members noted that judgements about this gap were highly uncertain. However, they observed that both model- and survey-based estimates pointed to the level of aggregate demand exceeding supply, and that some estimates implied that the gap was larger than currently assessed. Given members’ agreed commitment to prioritise returning inflation to target, these observations could justify an immediate increase in the cash rate.

The case to raise the cash rate could be further supported by developments in financial conditions over preceding months. Members noted that financial conditions appeared to have eased modestly, as housing prices and credit growth had picked up and bond yields had declined. The staff’s forecasts also implied that the future path for the cash rate inferred from market pricing was not sufficient to return inflation to the midpoint of the target range in 2026. The volatility in financial markets complicated this assessment, but members’ judgement at the time of the meeting was that the volatility would not have a material effect. Collectively, these considerations could be taken to imply that monetary policy should be tighter to achieve the Board’s inflation objective.

By contrast, holding the cash rate steady at this meeting – and possibly for an extended period – would be appropriate if members assessed that inflation was still broadly on track to return to target within a reasonable timeframe. It could also be appropriate if the current level of the cash rate was judged to be appropriate to balance the prevailing risks to inflation with those surrounding the outlook for the labour market.

Members observed that while underlying inflation was still too high and had fallen only slightly over the prior year, the disinflation in the June quarter had been broadly based across price categories. Inflation was still forecast to decline further as conditions in the labour market eased, and the pace of disinflation would be faster if the staff had overestimated the extent of excess demand. Members observed that there was considerable uncertainty about the inflation outlook and that inflation was forecast to return to the target range even in scenarios that incorporated a stronger outlook for consumption than in the central forecast. In addition, the forecast for when inflation would return to target was conditioned on the cash rate being reduced several times over coming years, including later this year. Members observed that it was possible to achieve a comparable degree of tightening in financial conditions as an increase in the cash rate by holding the cash rate at its current level for longer than the technical conditioning assumption underpinning the forecasts.

The case to hold the cash rate steady at this meeting was further supported by the need to balance the risks to the inflation forecast with those surrounding the outlook for full employment. Members noted that it was uncertain whether the forecast pick-up in domestic demand would materialise, given uncertainty around the staff’s judgements on consumption and the outlook for the labour market. Members noted that scenarios in which either consumption per capita did not grow or in which the unemployment rate increases by more than expected would see inflation return to target sooner than in the central forecast (though possibly still quite gradually). Given this, and the high degree of uncertainty surrounding both the forecasts and the implications of the volatility in financial markets prevailing at the time of the meeting, it could be that holding the cash rate steady best balanced the risks surrounding the outlook for both inflation and the labour market.

After weighing up these alternatives, members decided that the case to leave the cash rate target unchanged at this meeting was the stronger one. They agreed that doing so would best balance the risks to both inflation and the labour market, particularly in light of the prevailing uncertainties, market volatility and market expectations. Members noted that it was appropriate to continue placing somewhat greater-than-usual weight on the flow of data, relative to the forecasts, when there were uncertainties about the persistence of supply shocks. In addition, the flow of data since the previous meeting had not been sufficient to warrant a change in the stance of monetary policy. Members also observed that holding the cash rate target steady at its current level for a longer period than currently implied by market pricing may be sufficient to return inflation to target in a reasonable timeframe, but that the Board will need to reassess this possibility at future meetings.

In finalising the Board’s statement, members agreed that it was important to convey that the information received since the previous meeting had reinforced the need to remain vigilant to upside risks to inflation and that monetary policy will need to be sufficiently restrictive until members are confident that inflation is moving sustainably towards the target range. They also agreed that, based on the information available at the time of the meeting, it was unlikely that the cash rate target would be reduced in the short term, and that it was not possible to either rule in or rule out future changes in the cash rate target. Members will rely upon the data and the evolving assessment of risks to guide the Board’s decisions. Returning inflation to target remains the Board’s highest priority and it will do what is necessary to achieve that outcome.

The decision

The Board decided to leave the cash rate target unchanged at 4.35 per cent, and the interest rate on Exchange Settlement balances unchanged at 4.25 per cent.

New Zealand’s goods export rises 14% yoy in Jul, imports up 8.5% yoy

New Zealand's goods exports saw a robust increase of 14% yoy in July, reaching NZD 6.1B. Goods imports also rose by 8.5% yoy to NZD 7.1B, leading to a trade deficit of NZD -963m, a stark contrast to the expected surplus of NZD 331m.

Breaking down the export data, the strongest growth came from Australia, with total exports up by 19% (NZD 135m), followed by the EU, where exports surged by 30% (NZD 114m). Exports to China increased by 8.5% (NZD 107m), while exports to the US and Japan rose by 4.7% (NZD 35m) and 5.3% (NZD 17m), respectively.

On the import side, the largest increase was from South Korea, where imports more than doubled, rising by 103% (NZD 480m). Imports from China also saw significant growth, up 18% (NZD 233m). In contrast, imports from the US and the EU declined sharply, with drops of -30% (NZD -255m) and -14% (NZD -147m), respectively. Imports from Australia showed a modest increase of 0.82% (NZD 6.3m).

ECB’s Rehn flags September rate cut amid growing growth risks

ECB Governing Council member Olli Rehn highlighted growing concerns about Eurozone's economic outlook, stating that the "recent increase in negative growth risks" has strengthened the case for a rate cut at the next monetary policy meeting in September, assuming disinflation remains on course.

Rehn acknowledged that while inflation is expected to continue its path towards the 2% target, the journey is likely to be "bumpy" throughout the year. The real challenge, however, lies in the growth outlook.

He pointed out that there are still "no clear signs of a pick-up in the manufacturing sector," despite the fading impact of high energy costs that had previously weighed on the sector.

Rehn further cautioned that if investments in the manufacturing sector fail to recover and growth continues to rely heavily on the services sector, the "projected pick-up in productivity growth may be jeopardized."

He also warned that the slowdown in industrial production "may not be as temporary as assumed," suggesting that Eurozone could face prolonged economic challenges if the manufacturing sector does not regain momentum.

BTCUSD Completes Death Cross

- BTCUSD trades sideways in the past few sessions

- Sentiment deteriorates after multiple rejections at 50-day SMA

- Momentum indicators are skewed to the downside

BTCUSD (Bitcoin) has been losing ground in August, experiencing a strong selloff on the back of a downbeat July NFP report. In contrast to stocks, Bitcoin has failed to recover notable ground as the 50-day simple moving average (SMA) has repeatedly repelled any upside attempts.

Should the recent rangebound movement break to the downside, immediate support could be found at the April bottom of 56,483. A violation of that territory could pave the way for the July low of 53,250. Even lower, the six-month low of 49,450, registered in August, could provide downside protection.

On the flipside, bullish actions could send the price to test the recent rejection region of 61,850, which lies very close to the 50-day SMA. If that barricade fails, there is no prominent resistance until the April hurdle of 67,270. Further advances could then cease around the July peak of 70,015.

In brief, BTCUSD has been trading sideways in the past few sessions, but the death cross between 50- and 200-day SMAs has further deteriorated the already bearish short-term picture. For that to alter, the price needs to jump back above its 200-day SMA.

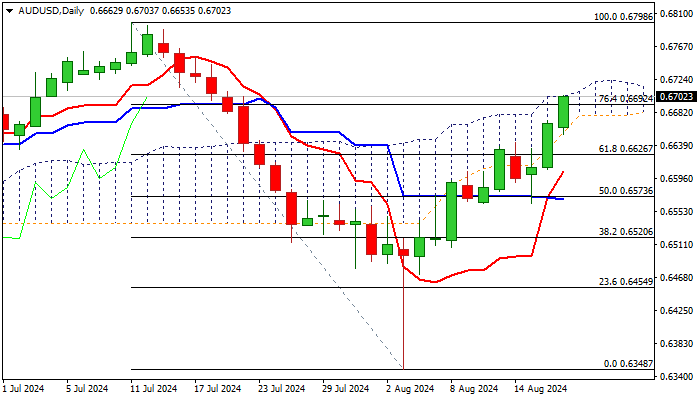

AUD/USD Outlook: Continues to Trend Higher Ahead of FOMC Minutes, Powell’s Speech in Jackson Hole

AUDUSD rose to the highest levels in almost one month on Monday, in extension of almost 0.9% daily advance on Friday and 1.5% gains last week

The pair enters the third consecutive week of strong gains, with the latest acceleration being boosted by revived risk appetite and hopes of September Fed rate cut (with renewed talks about 50 basis points cut).

Investors still need more evidence and await release of FOMC July meeting minutes and more significant speech of Fed Chair Powell in Jackson Hole symposium, which will shed more light on Fed’s next steps.

Widely expected dovish stance of the US central bank will further deflate the US dollar, though disappointing comments from Powell cannot be ruled out, and dollar would receive fresh support in such scenario.

Monday’s rally broke above Fibo barrier at 0.6692 (76.4% of 0.6798/0.6348 downtrend) and cracked pivotal resistance at 0.6701 (daily cloud top).

Firm break here to open way for push towards target at 0.6798 (2024 high, posted on July 11).

However, overbought daily studies may slow bulls, with limited dips (ideally to be contained by 55DMA at 0.6638) to provide better buying opportunities.

Res: 0.6714; 0.6750; 0.6798; 0.6839.

Sup: 0.6653; 0.6638; 0.6600; 0.6570.

Sunset Market Commentary

Markets

Markets took a slow start to the new trading week which looks more enticing later on. In the absence of high profile headlines today, softer yields and a weaker dollar initially proved the to be the path of least resistance, even as the momentum of this trade eased as US traders joined. German/EMU yields reversed small declines to currently trade up to 1.5 bps higher. US yields show a similar picture. Still, any sustained rebound in yields looks difficult for now. US inflation, while still well above the 2% target, has softened enough for the Fed to give more weight to growing signs of a cooling of activity and, in particular, a slowdown in job creation. Last week’s US data (retail sales) suggest that the US economy is heading for a soft landing, rather than an outright recession. Still markets see room for the Fed to ‘substantially’ scale back policy tightening in order to prevent an unnecessary slowdown in activity/rise in unemployment. This week, the (US) PMI’s, comments at the Fed Jackson Hole symposium, the minutes of the July Fed meeting and the annual revision of the BLS’ US payrolls data might help markets to make up their mind on the pace of Fed easing. The debate remains open (and that probably remains the case after Jackson Hole), but markets continue to err on the side of the Fed being behind the curve. Fear for a sharp US downturn triggered a wild risk-off correction early August, but stocks in the meantime rebounded on the hope of easier (global) financial conditions. However, with especially US markets having reversed course, the risk rebound is shifting into a lower gear. Europe now outperforms the US (Eurostoxx 50 + 0.5%, S&P 500 +0.1%). Oil (Brent $79.2/b) still struggles to hold the $80/b reference despite ongoing geopolitical tensions in the Middle East region as uncertainty on global demand lingers.

Anticipation of easier financial conditions keep the dollar in the defensive. USD/JPY this morning tested the 145.20 area (compared to a 147.63 close on Friday) but the USD selling gradually eased intraday (146.15 currently). EUR/USD (1.1035) regained the 1.10 barrier. The EMU eco picture remains uninspiring, but high wage growth (Q2 ECB negotiated wages to be published on Thursday) might force the ECB to take a guarded approach on further easing. The December EUR/USD 1.1139 top is within reach with the 2023 top at 1.1276. Sterling initially tried to extend its post-CPI comeback from end last week, but EUR/GBP 0.85 support holds (currently 0.852).

News & Views

Bulgarian president Radev unexpectedly declined to approve a new interim cabinet, adding he will delay snap elections until after October 20. His decision deepens the political turmoil in the country, which will head to the ballot for the seventh time in less than four years. President Radev, whose powers have already been clipped by the government following several unilateral decisions to form governments over the past years, said that interior minister Stoyanov wouldn’t be able to guarantee fair elections if he continues in his role. The current political crisis delays Bulgarian efforts to join the euro. The middle of 2025 target date (already delay from 1/1/2025) is on a slippery slope. Apart from politics, the country has difficulties meeting the price stability criterion for joining EMU with average inflation rates well above the ECB’s June 2024 convergence report reference value (3.3%).

Rating agency Fitch this weekend confirmed the Czech Republic’s AA- rating with a stable outlook. It is underpinned by a record of credible macroeconomic and monetary policies, and a robust institutional framework. Fitch has revised down this year's real GDP growth forecast to 0.9%, from 1.2% expected in February, given the weak start to the year and subdued external demand, but puts forward an average 2.4% growth rate in 2025-2026. Headline inflation has been moving close to the central bank's target of 2% and is set to average 2.2% in 2024-2026, allowing the CNB to continue its easing cycle bringing the key rate at 3.75% by end-2024 (in line with our forecast) and 3.5% by end-2025. Fitch expects the budget deficit to narrow to 2.5% of GDP in 2024 and 2.2% in 2025 from 3.5% in 2023. The debt/GDP ratio is set to increase to 43.7% in 2025, from 42.4% in 2023 and to gradually decline to 42.9% in 2028 driven by the narrowing of primary budget deficits and recovering economic growth.

Graphs

DXY (trade-weighted USD index) testing 102 big figure as easing of global financial conditions continues to pressure the dollar

Brent oil struggles to hold the $80/b reference as uncertainty on global demand persists

Eurostoxx 50 reversing early month risk-off repositioning

EUR/SEK holding near 11.50 pivot as Riksbank is expected to further scale back policy restriction.

Could Eurozone PMI Surveys Cement September ECB Rate Cut?

- Markets are preparing for the Jackson Hole Symposium

- Eurozone data supports another ECB rate cut

- PMI surveys for the euro area will be published on Thursday

- Euro remains on the back foot against the pound

The Jackson Hole gathering to break the summer lull

Whilst ECB members are probably enjoying their hard-earned holiday break, the countdown to the Jackson Hole Symposium and the crucial September central banks’ meetings has already started. The RBNZ is the latest central bank to ease its monetary policy stance and, interestingly, the first one to openly talk about a recession in the latter part of the year.

Expectations of an imminent recession in the US were the main reason for the recent market rout that scared investors, ignoring the fact that the US data has been relatively satisfactory lately, as portrayed by our custom-made surprise indices. The same cannot be said for eurozone data and especially the German economic releases.

Euro area data remains mixed, rate cut expected

The preliminary GDP prints for the second quarter of 2024 created a sense of optimism in the hawks. Interestingly, the July CPI report for the euro area managed to surprise to the upside with the headline figure printing at 2.6% and the core indicator showing a 2.9% year-on-year increase. In addition, at the July ECB meeting, President Lagarde tried to dent expectations for another rate cut in September.

However, all these are probably not enough to change the current momentum in the ECB council with the market firmly confident that at least 65 bps of extra easing will be announced until year-end on the back of weak economic momentum and the Fed commencing its easing cycle in September.

For the ECB to disappoint the market, two conditions have to be met: (1) the Fed to avoid making a dovish shift at the Jackson Hole Symposium, thus falling shorting from pre-announcing the much talked about rate cut, and (2) the euro area data to show a miraculous improvement.

Euro area PMI surveys in the spotlight this week

Chances of these two events happening simultaneously are rather slim but a strong set of PMI survey prints this week could be a good start. Interestingly, the PMI surveys for the manufacturing and services sectors tell a different story for the eurozone.

The manufacturing PMI surveys for both Germany and France are stuck below 50 for a considerable amount of time. Both countries continue to suffer from the consequences of the Ukraine-Russia conflict, the associated competitiveness loss and the lower demand, both from China and domestically.

On the other hand, the PMI services surveys continue to hover above 50 and thus portray a sector in modest expansion. Services inflation has been a key discussion point in the last ECB meetings, appearing in the official ECB press statement, and thus being as the few reasons that inflation remains elevated.

The market is forecasting another mixed set of PMIs. The manufacturing surveys are expected to edge slightly higher, but remain in contractionary territory, while the PMI services figures could weaken a tad. Such an outcome is unlikely to affect the chances of another ECB rate cut in September.

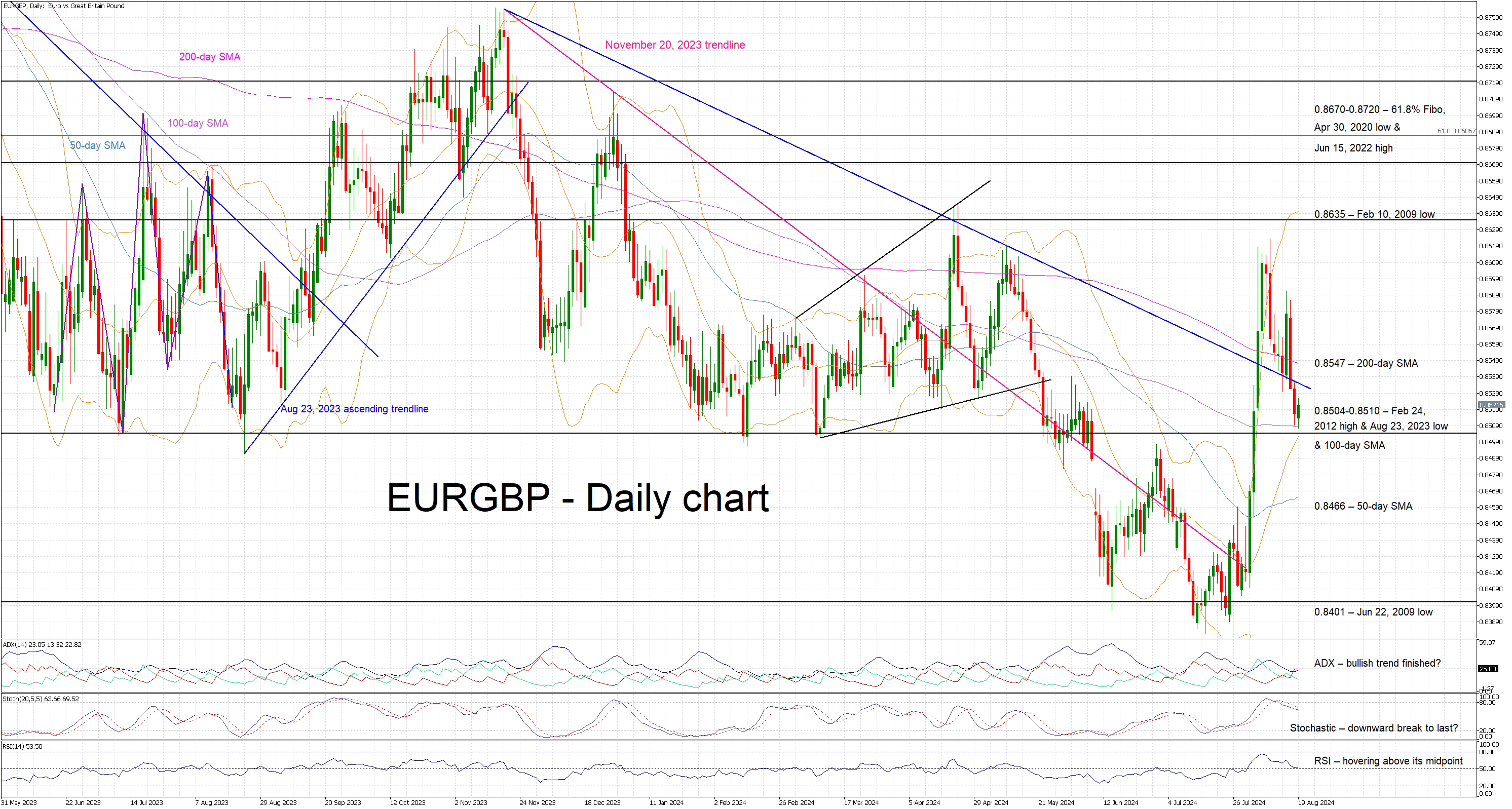

Euro is losing ground against the pound

Following the late July BoE rate cut, euro/pound managed to rally considerably higher, negating most of the April-July 2024 downward move. However, mostly on the back of the overall negative outlook for the eurozone, the euro has been losing ground against the pound lately.

Market expectations for aggressive ECB easing are unlikely to be dented by a strong set of PMI surveys but the euro could benefit by climbing above the 200-day simple moving average at 0.8547. On the flip side, weak PMI survey figures are unlikely to prove significantly market-moving as the market is preparing for the all-important Jackson Hole Symposium.

News of the Week (August 19— August 23): GBPCAD Detailed Analysis

Keep your eyes on GBPCAD—new trading prospects are emerging!

The GBPCAD currency pair, representing the exchange rate between the British pound and the Canadian dollar, is the most critical indicator of economic interaction between the UK and Canada. The Canadian dollar is heavily influenced by fluctuations in commodity prices, particularly oil, due to Canada's status as a major exporter. Economic policy decisions and indicators such as employment levels, GDP growth, and trade balance are also important. On the other hand, the British Pound is influenced by factors such as changes in UK monetary policy, as well as economic reports such as inflation, employment, and consumer spending data.

Canada Consumer Price Index (CPI) MoM, Aug 20, 14:30 (GMT+2)

Canada's Consumer Price Index (CPI) is forecast to rise by 0.2%, recovering from a previous decline of -0.1%. If the CPI exceeds this forecast, indicating an increase in inflationary pressures, this could cause the Bank of Canada to consider tightening monetary policy. This would likely lead to a stronger Canadian Dollar and a decline in the GBPCAD pair. Conversely, the Canadian Dollar could weaken if the CPI exceeds the expected 0.2%, indicating less inflationary pressure than expected. This would potentially lead to a rise in the GBPCAD pair, reflecting lower confidence in the strength of the Canadian economy.

Last time on April 16, 2024, Canadian CPI came in below expectations, causing GBPCAD to surge!

UK Manufacturing Purchasing Managers Index (PMI), Aug 22, 10:30 (GMT+2)

The UK manufacturing PMI is forecast to decline slightly to 51.5 from 52.1. If the PMI beats expectations, demonstrating the resilience of the manufacturing sector, this could boost investor confidence in the UK economy and strengthen the Pound. A stronger Pound is likely to lead to a higher GBPCAD exchange rate. On the other hand, if the PMI falls short of expectations, indicating a weakening manufacturing sector, this could undermine confidence in the Pound. Such a scenario will likely lead to a fall in the GBPCAD pair, as the pound will lose ground.

In the Daily timeframe, GBPCAD, in a long-term uptrend, formed a rising channel pattern. The price bounced off the trend line and is consolidating near 161.8 Fibonacci, creating two possible scenarios.

- If the bulls push the price above 1.7630, the target will be 1.7820. However, if the price bounces off the resistance, it could fall to the trend line and then rally upwards;

- Otherwise, if GBPCAD breaks the trend line and falls below 1.7560, it will reach the support at 1.7450;