Sample Category Title

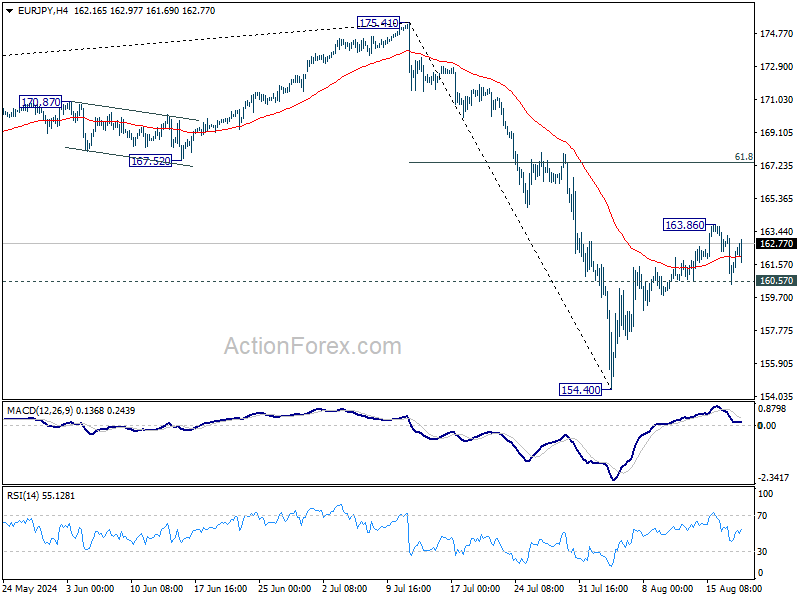

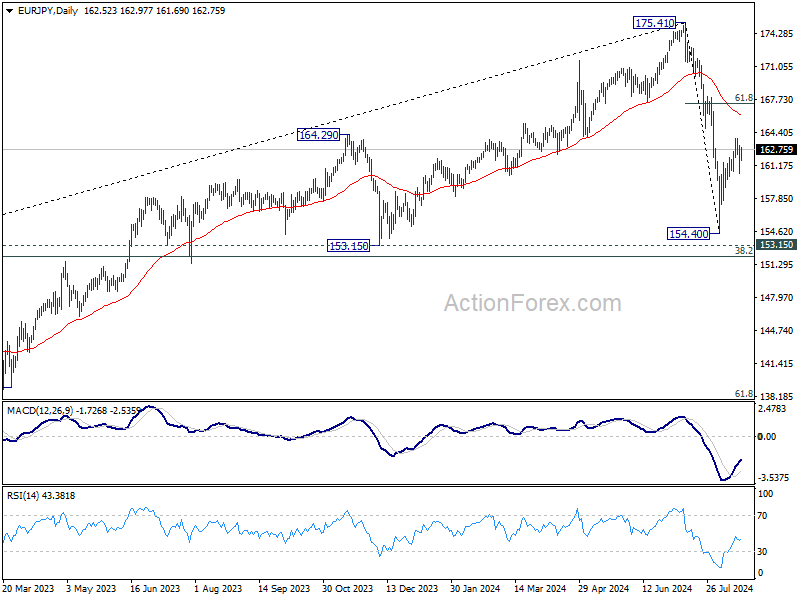

EURJPY’s Rebound Falters Ahead of 200-SMA

- EURJPY recovers from its 2024 low posted on August 6

- But the rebound stumbles before testing 200-day SMA

- Oscillators are skewed to the downside

EURJPY experienced a vast selloff in July, dropping from a 32-year peak of 175.41 to as low as 154.34 on August 6, which is also the pair’s 2024 bottom. Since then, the pair has been in a recovery mode, but its rebound seems to have paused for now ahead of the 200-day simple moving average (SMA).

Should the bears attempt to erase the latest uptick, the recent support of 160.40 could prove to be the first obstacle for them to overcome. Further declines may then cease at the February low of 158.06. Failing to halt there, the price may challenge the January bottom of 155.05 ahead of the 2024 low of 154.34, registered on August 6.

Alternatively, if the rebound resumes, initial resistance could be found at the recent rejection region of 163.87, which lies very close to the 200-day SMA. A break above that zone could open the door for the March resistance of 165.34. Conquering this barricade, the bulls might attack the June support of 167.50, which could serve as resistance in the future.

In brief, EURJPY has been attempting to erase its recent slump, but its efforts have met strong resistance near the 200-day SMA. Hence, a break above that crucial hurdle is needed for the bulls to regain confidence for a full-scale recovery.

Pound Near July Highs: What Could Trigger a Breakout?

The slowdown in U.S. inflation and a cooling labour market have rekindled investor confidence that the Federal Reserve may soon begin cutting interest rates. As bearish sentiment towards the dollar dominates the market, key currency pairs have approached critical levels, the breach of which could spark new medium-term trends.

GBP/USD

Technical analysis of GBP/USD suggests the possibility of a retest of the July high at 1.3050, as a strong upward momentum has developed on the daily timeframe following a bullish engulfing pattern. If buyers manage to secure a hold above 1.3000, the price could extend towards last year's highs around 1.3140-1.3100. Conversely, a rejection from 1.3000 might lead to a corrective decline towards 1.2900-1.2800.

Key events for GBP/USD pricing include:

- Today at 20:35 (GMT +3:00): Speech by FOMC member Bostic

- Tomorrow at 09:00 (GMT +3:00): UK Public Sector Net Borrowing data

- Tomorrow at 21:00 (GMT +3:00): FOMC meeting minutes release

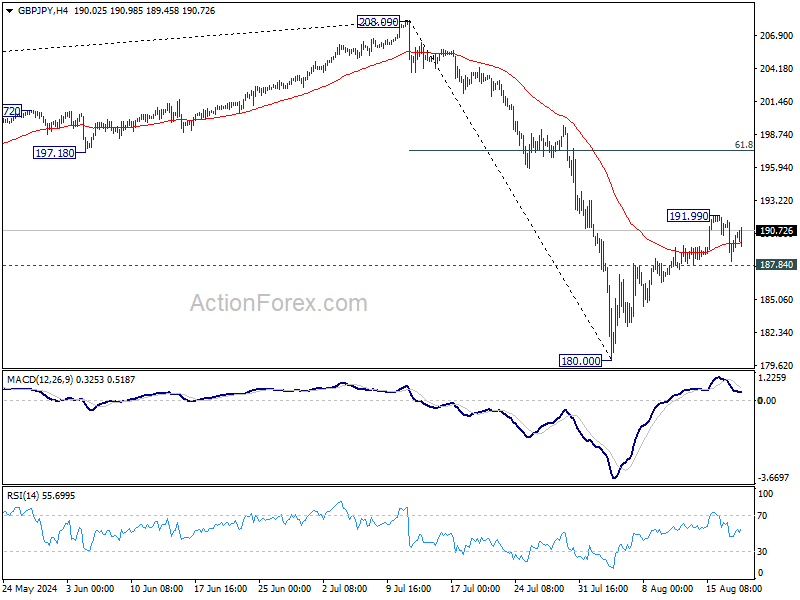

GBP/JPY

Volatility in yen pairs remains high. After a sharp rise in July, yen sellers have managed to regain some losses. Technical analysis of GBP/JPY indicates the potential for further decline, as a bearish harami pattern has formed following a bounce from 192.00. If yesterday's low at 188.30 is breached, the downtrend may continue towards 186.00-184.00. Should the price rise above 192.00, a deeper upward correction is possible.

Key news impacting GBP/JPY includes:

- Tomorrow at 02:50 (GMT +3:00): Japan’s Trade Balance (seasonally adjusted)

- Tomorrow at 02:50 (GMT +3:00): Japan’s Import and Export figures for July

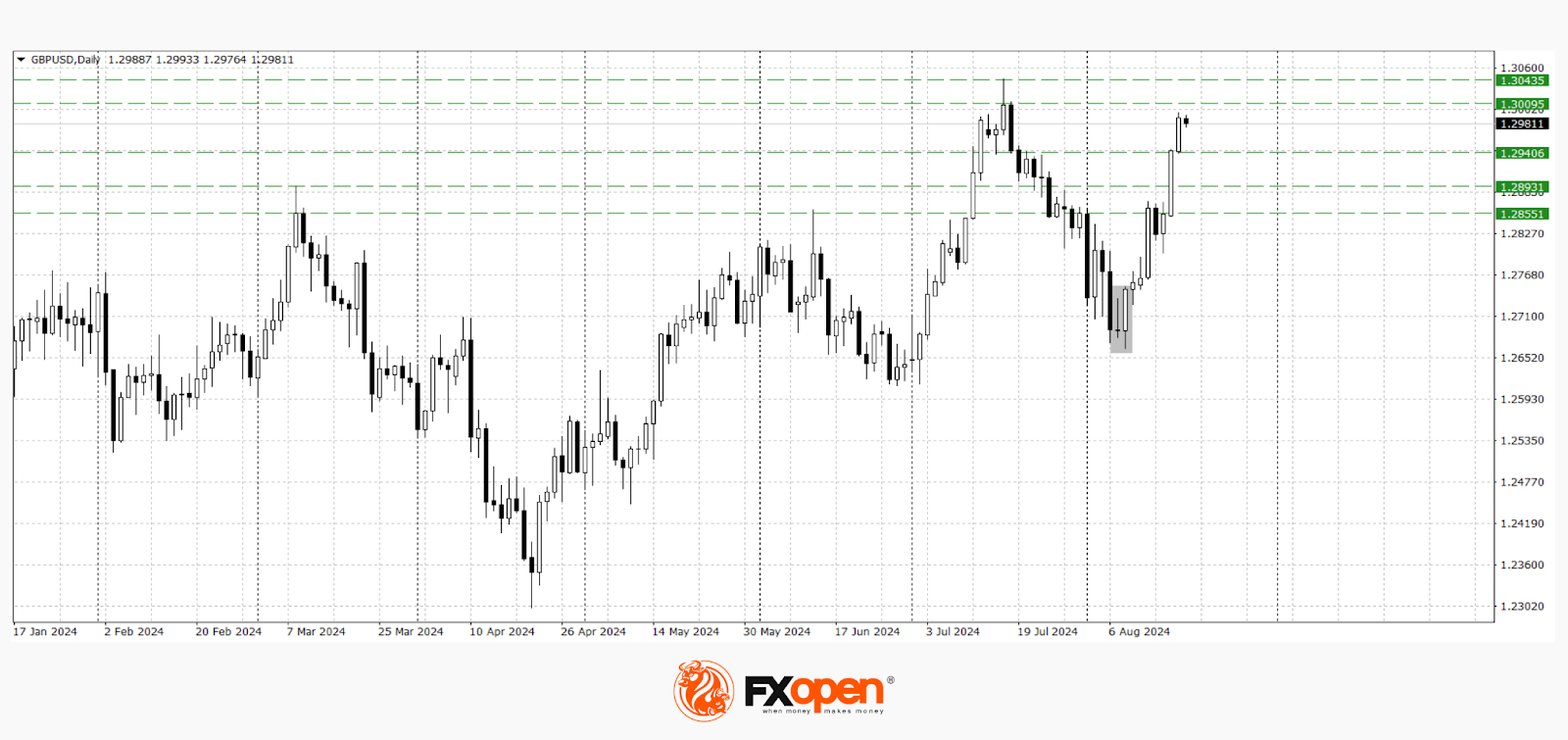

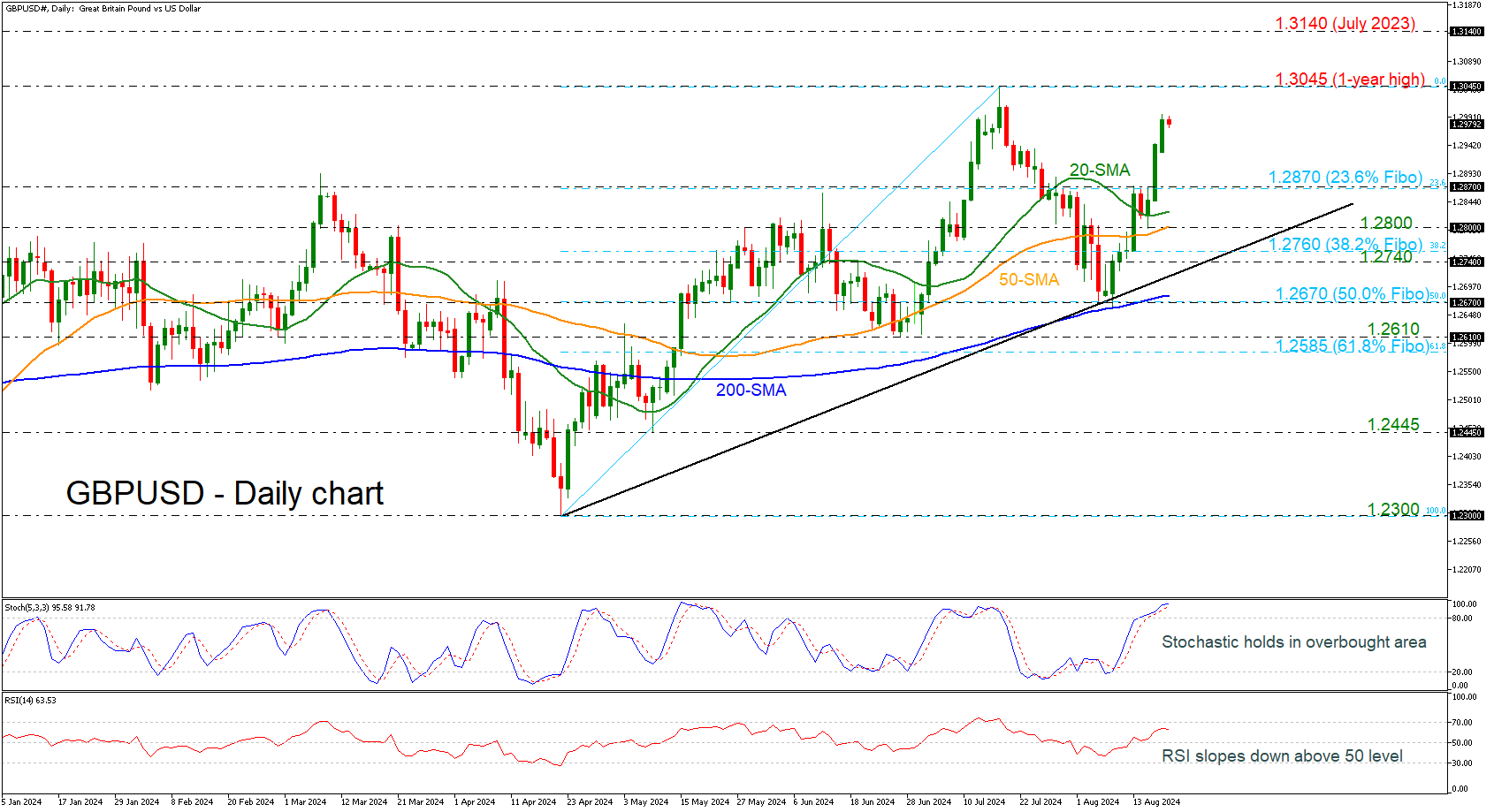

GBPUSD Awaits Strong Resistance Near 1-Year High

- GBPUSD’s rebound off 200-day SMA still holds

- Stochastic in overbought area

- RSI ticks south above 50 level

GBPUSD continues last week's rebound off the 200-day SMA and the 50.0% Fibonacci retracement level of the up leg from 1.2300 to 1.3045 at 1.2670, but with some weakness today. The intraday bias looks neutral to negative, as the stochastic is still standing above the 80 level but is losing some steam, while the RSI, although above 50, seems to be making its way down.

If the pair manages to head higher, the one-year high of 1.3045 could serve as a trigger point for steeper bullish action. Further north, cable could run toward the 1.3140 level, a strong barrier from last year.

However, if the pair reverses to the downside, investors could move first at the 23.6% Fibonacci of 1.2870 before meeting the 20- and then the 50-day simple moving averages (SMAs) at 1.2825 and 1.2800 respectively. If the price continues to drop, support could next come somewhere between the uptrend line and the 38.2% Fibonacci of 1.2760.

In the medium-term picture, the bounce off 1.2300 turned the outlook from neutral to bullish. Chances for another bullish move are still rising as the 200-day SMA keeps rising.

A Softer Dollar Remains the Way to Go

Market Commentary

Markets

Last week’s directional moves on key markets were extended yesterday in absence of any guidance coming from eco data or central bankers. Core bond yields fail to recover from the early August setback with daily changes in the US ranging between -1.8 bps (30-yr) and +1.6 bps (2-yr). German yields closed almost unchanged. Especially US money markets keep banking on significant Fed rate cuts to come. Apart from the magnitude of the lift-off (25 bps being our preferred scenario), especially the 2025 path will be challenged in the updated September FOMC dot plot. Markets currently discount a 3.25% policy rate by the end of 2025 compared with a median Fed view of 4%-4.25% back in June. Aggressive rate cut bets keep the dollar in the defensive. EUR/USD yesterday closed at its best level YTD (1.1085 from 1.1014) with resistance levels lining up: 1.1139 (December top) and 1.1276 (2023 top). A softer dollar remains the way to go. The less restrictive monetary policy where money markets are hoping for should help accommodate the US soft landing and especially rule out the downside recession risk. It’s what helped US stock markets stage an impressive comeback since the August 5 market meltdown. Key benchmarks yesterday rallied another 0.6% (Dow) to 1.4% (Nasdaq), lifting them to this month’s best levels. On commodity markets, gold closed at an all-time high of $2548.3/ounce. Brent crude remains under selling pressure ($77/b) both because of global demand concerns and as the US indicated that Israel accepted a cease-fire proposal in Gaza.

Asian stock markets join yesterday’s positive momentum with China underperforming. Chinese banks kept their benchmark lending rates unchanged (1y: 3.35% & 5y: 3.85%) after cutting them by 10 bps each only a month ago. ECB governing council member Rehn said that the recent increase in negative EMU growth risks reinforced the case for a September policy rate cut (provided that disinflation remains on track). He sees no clear signs of a pick-up in the manufacturing sector even though the energy cost drivers seem to have largely faded away. Today’s eco calendar remains extremely thin with only final July EMU CPI data on tap. The Swedish Riksbank is expected to lower its policy rate for a 2nd time by 25 bps (to 3.5%) with the Turkish central bank forecast to hold rates steady at 50%.

News & Views

The NY Fed’s SCE labour market survey showed a mixed picture. It recorded a sharp increase in the proportion of job seekers compared to a year ago. Among those employed four months ago, 88% were still with the same employer, a low since the start of the series in July2014 as the transition rate rose sharply. Looking forward, the expected likelihood of moving to a new employer increased to 11.6% from 10.6% in July 2023. At the same time, the average expected likelihood of becoming unemployed rose to 4.4% from 3.9% also a new high. Satisfaction with wage compensation as well as with nonwage benefits and promotion opportunities all deteriorated. Conditional on expecting an offer, the average expected annual salary of job offers in the next four months declined to $65,272 from $67,416, though it remains significantly higher than pre-pandemic levels. The average reservation wage—the lowest wage respondents would be willing to accept for a new job—increased to $81,147 from $78,645. The average expected likelihood of working beyond age 62 increased to 48.3% from 47.7. The average expected likelihood of working beyond age 67 increased to 34.2% from 32.

The Minutes of the 5-6 August meeting of the Reserve bank of Australia showed that the central bank discussed a further rate hike, but concluded that the stronger case was for leaving the policy rate unchanged at 4.35%. Members noted that developments over preceding months supported the view that inflation would be slow to decline. Underlying inflation had fallen very little over the prior year in quarterly terms and inflation was still some way above target. Members also saw the gap between aggregate demand and supply being somewhat larger than previously assessed. Holding the cash rate target steady at its current level for a longer period than currently implied by market pricing may be sufficient to return inflation to target in a reasonable timeframe. The Board will need to reassess this at future meetings. Still it guided that it was not possible to either rule in or rule out future changes in the cash rate target.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June. Stubborn inflation (core, services) make follow-up moves less evident. Markets nevertheless price in two to three more cuts for 2024 as disappointing US and unconvincing EMU activity data rolled in, dragging the long end of the curve down. The move accelerated during the early August market meltdown.

US 10y yield

The Fed in its July meeting paved the way for a first cut in September. It turned attentive to risks to the both sides of its dual mandate as the economy is continuing to move better in to balance. Money markets tend to err in favour of a 50 bps lift-off. The pivot weakened the technical picture in US yields with another batch of weak eco data pushing the 10-yr sub 4%.

EUR/USD

EUR/USD moved above the 1.09 resistance area as the dollar lost interest rate support at stealth pace. US recession risks and bets on fast and large (50 bps) rate cuts trumped traditional safe haven flows into USD. EUR/USD 1.1139 (Dec 2023 high) and 1.1276 (2023 top) serve as next technical references.

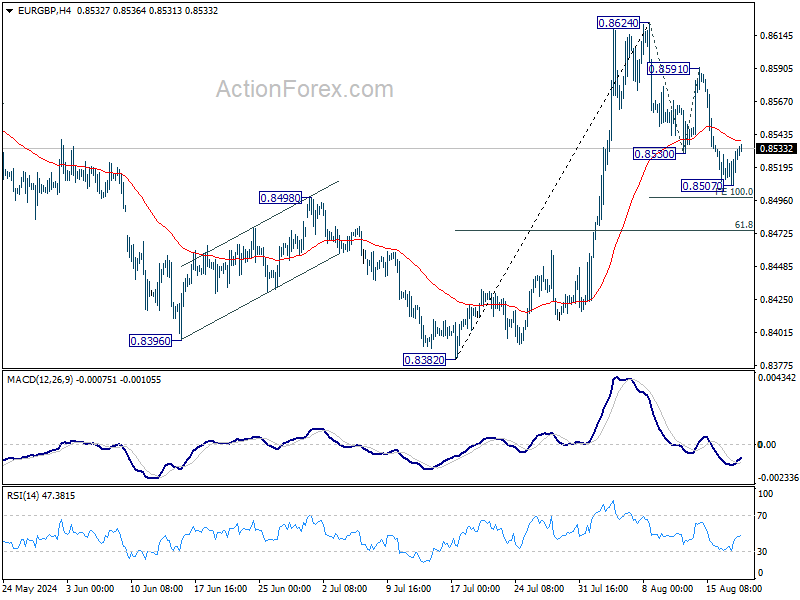

EUR/GBP

The BoE delivered a hawkish cut in August. Policy restrictiveness will be further unwound gradually 0on a pace determined by a broad range of data. The strategy similar to the ECB’s balances out EUR/GBP in a monetary perspective. Risk-off proved a more important driver of GBP recently, triggering a return from 0.84 towards 0.86.

The Sweet Soft-Landing Spot

The week kicked off on a positive note on expectation that when Federal Reserve (Fed) Chair Jerome Powell speaks at the Jackson Hole meeting on Friday, he will deliver a strong hint that the rate cuts will begin soon in the US. How soon ? Probably in September? By how much? Probably a reasonable 25bp? Would the markets be upset with the idea of a 25bp cut instead of a 50bp? Probably not, because a 50bp cut would require a severe economic slowdown, a crisis or a panic mode, which is not good for risk appetite. Therefore, the best of both worlds would be the hint of a 25bp cut that would keep the market mood in the sweet soft-landing spot. And this is what investors hope to hear.

And that hope has pushed the S&P500 up for the 8th straight session on Monday. The index added another 1% yesterday and is now just 1% below its ATH level. Nasdaq 100 jumped 1.30% and above its 50-DMA for the first time in almost more than a month. Roundhill’s Magnificent 7 ETF advanced more than 1.60% while the Russell 2000 gained 1.20%. In summary, both the Big Tech and small companies in the US gained with the thought of an approaching rate cut in the US. Even the energy stocks had a good session despite a heavy selloff in crude oil, which was triggered by the news that Israel accepted a ceasefire proposal in Gaza if Gaza says yes. US crude fell more than 2.5% to below $75pb yesterday and remains under pressure this morning but could – once the geopolitical factors are priced in – see the support of the Fed optimism and rebound back to $78/80pb range. Zooming out, what I want to say is that both the big and small stocks gained yesterday, and the S&P500’s equal-weighted index neared an ATH level as the market rally of today isn’t boosted by AI – but by the Fed expectations – and the latter benefit to other sectors than only the ones that see the direct benefits of AI investments.

AMD steps up efforts to offer something more than just, chips

AMD announced to buy ZT Systems to increase ‘its capabilities and expertise to optimise solutions at the systems, rack and the data center levels’ because customers no longer want only chips, but it want ready-to-use AI solutions - a thing that Nvidia does better than the rivals with its ecosystem and the others should improve at. AMD plans to sell ZT System’s data center infrastructure manufacturing unit and keep its system-design business and hope to compete with Nvidia in offering fast and at-scale AI solutions. AMD jumped 4.5%.

The news didn’t tame appetite for Nvidia, which also rallied more than 4% and closed the session at $130 per share. Even Intel gained yesterday.

Overall, the chipmakers are doing better now than a month ago, but the Fed optimism should enhance rotation toward the non-tech pockets of the market that were left behind over the past year-and-a-half and provide only a limited upside potential to the Big Tech.

Elsewhere

The European Stoxx 600 also opened the ween on a positive note and jumped above the 50 and 100-DMA, and the Japanese Nikkei 225 is better bid today after a moody Monday on a yen rebound. I expect the market mood to remain mainly optimistic into the Jackson Hole meeting with no major data points to hamper optimism. We will have a glance on the European and Canadian inflation numbers today, FOMC minutes tomorrow and flash manufacturing numbers for August on Thursday. I guess that the US weekly jobless claims will also be watched more seriously than usual, but all in all there should be nothing major to change the week’s focus until the Powell speaks.

The US dollar remains weak – too weak – into that speech, the EURUSD consolidates gains near 1.1080 before today’s CPI read and Cable tests the 1.30 offers supported by relatively strong fundamentals. The UK has been the best performing economy among major peers in the first half of the year. Despite political shenanigans, the Brexit pain and the cost-of-living crisis, the British economy grew more than its major peers in the first two quarters of the year – even better than the US. Germany has ranked at the bottom of the range after France and Italy. And the surprisingly good performance of the British economy keeps the Bank of England (BoE) doves more contained than their Fed peers, and gives support to the pound against the greenback. But again, I still think that the US dollar’s weakness has gone a bit too far and we shall see some downside correction before an eventual rise above the 1.30 mark. If nothing, the US economy is doing better than most peers and that alone should give the Fed doves less reason to believe that the Fed will cut more than the peers in the coming months.

Still in the UK, while the British economy and Cable outperformed peers over the past months, the British blue-chip index, the FTSE 100 – which is more concerned about the global economic health than the UK’s own matters due to its high exposure to energy – didn’t do better than the others. But the energy-heavy index should continue to see the benefits of reflation flows, if the rate cuts start while we are still in the soft-landing zone.

Rate Cut from Riksbank Should be a Done Deal

In focus today

In Sweden, the Riksbank's rate decision, a policy statement and a shorter policy report will be published at 09.30 CET. A press conference follows at 11.00 CET. There will be no new macro forecasts and no new rate path. A 25bp rate cut is - or should be - a done deal. Instead, market focus will be on communication. We expect that they will guide toward two more cuts this year, which is slightly more dovish than in June, though less dovish than market is pricing (three more cuts).

In the euro area, we will get final inflation figures for July. The final HICP data allow us to see how the important domestic inflation indicator ('LIMI') fared in May, see Research Euro Area - The importance of domestic inflation guiding ECB policies, 6 August. The preliminary figures showed that service price pressures eased to around 0.3% m/m, which is still too high, but lower than a couple of months ago.

In Denmark, we get national accounts data for Q2. We expect 1% GDP growth in Q2. GDP declined 1.4% q/q in Q1 on the back of a very strong fourth quarter in 2023. This leaves room for growth in Q2. For more details, see Danish section in Weekly Focus - From fear of inflation to fear of slowdown, 16 August.

In Turkey, the central bank will announce its rate decisions at 13.00 CET. The Central Bank of Turkey has concluded its hiking cycle and is expected to keep the policy rate unchanged at 50%. Since the July meeting, inflation has developed largely in line with their forecasts, as headline inflation in month-on-month terms increased temporarily in July, while the rise in underlying inflation was limited.

Fed's Bostic will be on the wire in the evening at 19.35 CET.

Economic and market news

What happened overnight

Peoples Bank of China (PBOC) left loan prime rates unchanged as expected in the market, after interest rates were lowered in July. More easing is expected later in Q3 as the economy is struggling and PBOC has been waiting for the Fed to start easing before cutting rates (to avoid downward pressure on the renminbi).

What happened yesterday

In the euro area, ECB's Rehn (voting member) spoke about monetary policy. He said that ECB may need to lower interest rates at the September meeting, due to negative growth risks arising, while inflation is on the right track in his eyes. Markets price in a 90% probability of a rate cut in September. We, however, still stick to our call of no cut in September.

Market movements

Equities: Global equities were higher yesterday, and this morning's post might start to sound like a broken record with the MSCI World Index gaining for its eighth consecutive day. Equities were up, volatility was lower (VIX below 15), and cyclicals outperformed defensives. As US stocks rallied into the cash close, all 25 industries finished higher on a day that saw virtually no headline news to drive the market. FOMO is back, and all the fear about a recession among equity investors seems to have gone. Please remember, this is typically how investor behaviour appears when we are very late in the cycle. In the US yesterday, Dow +0.6%, S&P 500 +0.97%, Nasdaq +1.4%, and Russell 2000 +1.2%. This morning, most Asian markets are higher, led by Japanese markets, which are up more than 2%, while Chinese stocks are moving in the opposite direction. Futures in Europe are mixed, while in the US, futures are marginally stronger.

FI: Markets waiting for the important ECB data and Jackson Hole speech later this week resulted in a tight trading range. Markets are also waiting for toda'’s supply with an expected 5y Finland deal and a 10y and long-end German bond tap. 10y Bunds ended virtually unchanged at 2.45%. Key events this week are the EA and US PMIs on Thursday, EA negotiated wage data on Thursday as well as Powel'’s speech in Jackson Hole on Friday. Lane speaks on Saturday.

FX: JPY was the top performer among G10 currencies yesterday, were the USD stay on a weak footing. EUR/SEK declined below 11.50 before the Riksbank rate decision today.

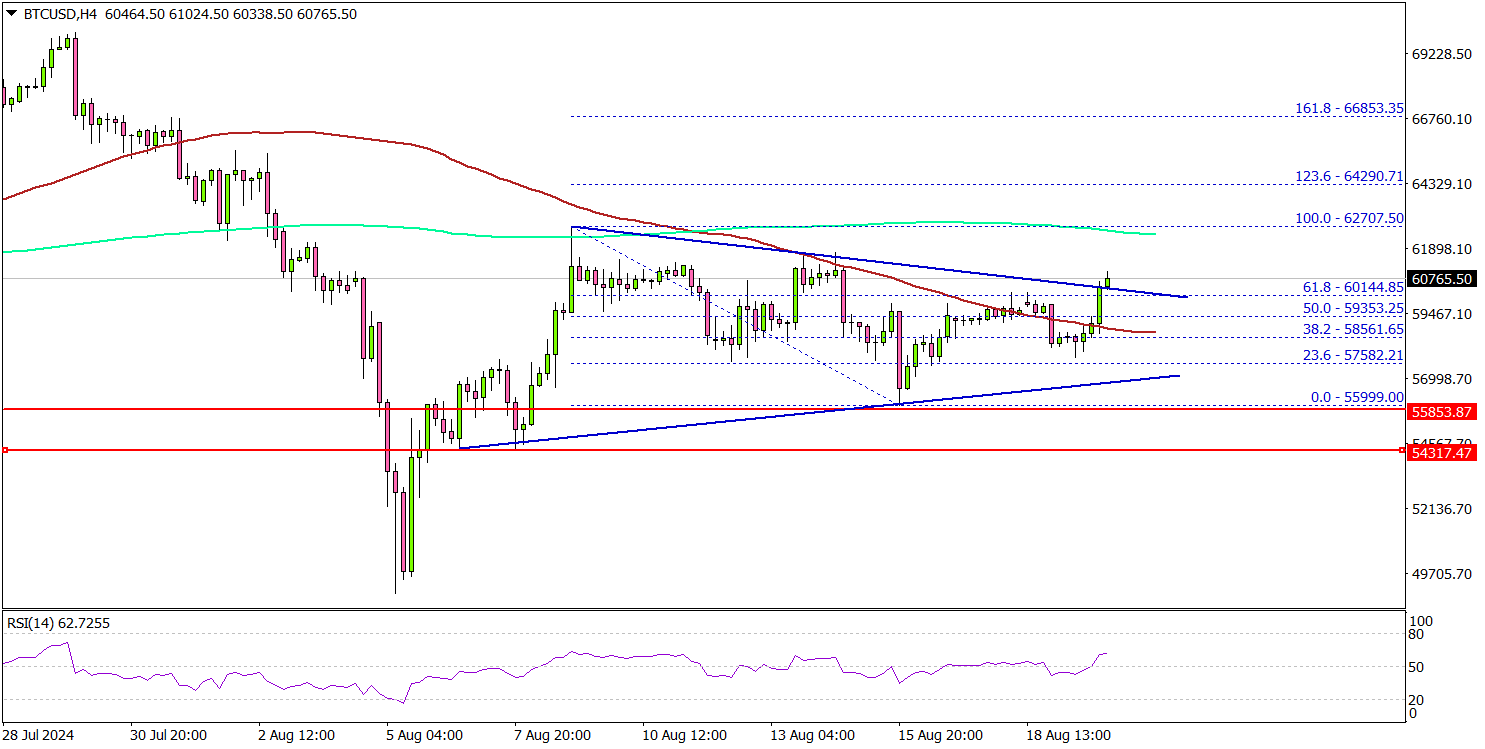

Bitcoin Price Breakout: Could It Lead To Bigger Gains?

Key Highlights

- Bitcoin price is aiming for a decent increase above the $60,000 resistance.

- BTC cleared a key contracting triangle with resistance at $60,800 on the 4-hour chart.

- Gold bulls pushed the price above the $2,500 resistance zone.

- GBP/USD is showing positive signs and aiming for a move above 1.3000.

Bitcoin Price Technical Analysis

Bitcoin price formed a base above the $56,000 level and started a fresh increase. BTC/USD climbed above the $58,000 resistance to start a decent increase.

Looking at the 4-hour chart, the price gained pace for a move above the 50% Fib retracement level of the downward move from the $62,707 swing high to the $55,999 low. It cleared a key contracting triangle with resistance at $60,800.

The price is now trading above the 61.8% Fib retracement level of the downward move from the $62,707 swing high to the $55,999 low, and the 100 simple moving average (red, 4 hours).

On the upside, the price might struggle to clear the $62,500 resistance and the 200 simple moving average (green, 4 hours). A successful close above $62,500 might start another steady increase. In the stated case, the price may perhaps rise toward the $65,000 level.

Immediate support is near the $59,500 level. The next key support sits at $58,500. A downside break below $58,500 might send Bitcoin toward the $55,000 support. Any more losses might send the price toward the $52,500 support zone.

Looking at gold, the price is rising and there could be more upsides above the $2,500 level in the near term.

Today’s Economic Releases

- US Goods and Services Trade Balance for June 2024 - Forecast $-72.4B, versus $-75.1B previous.

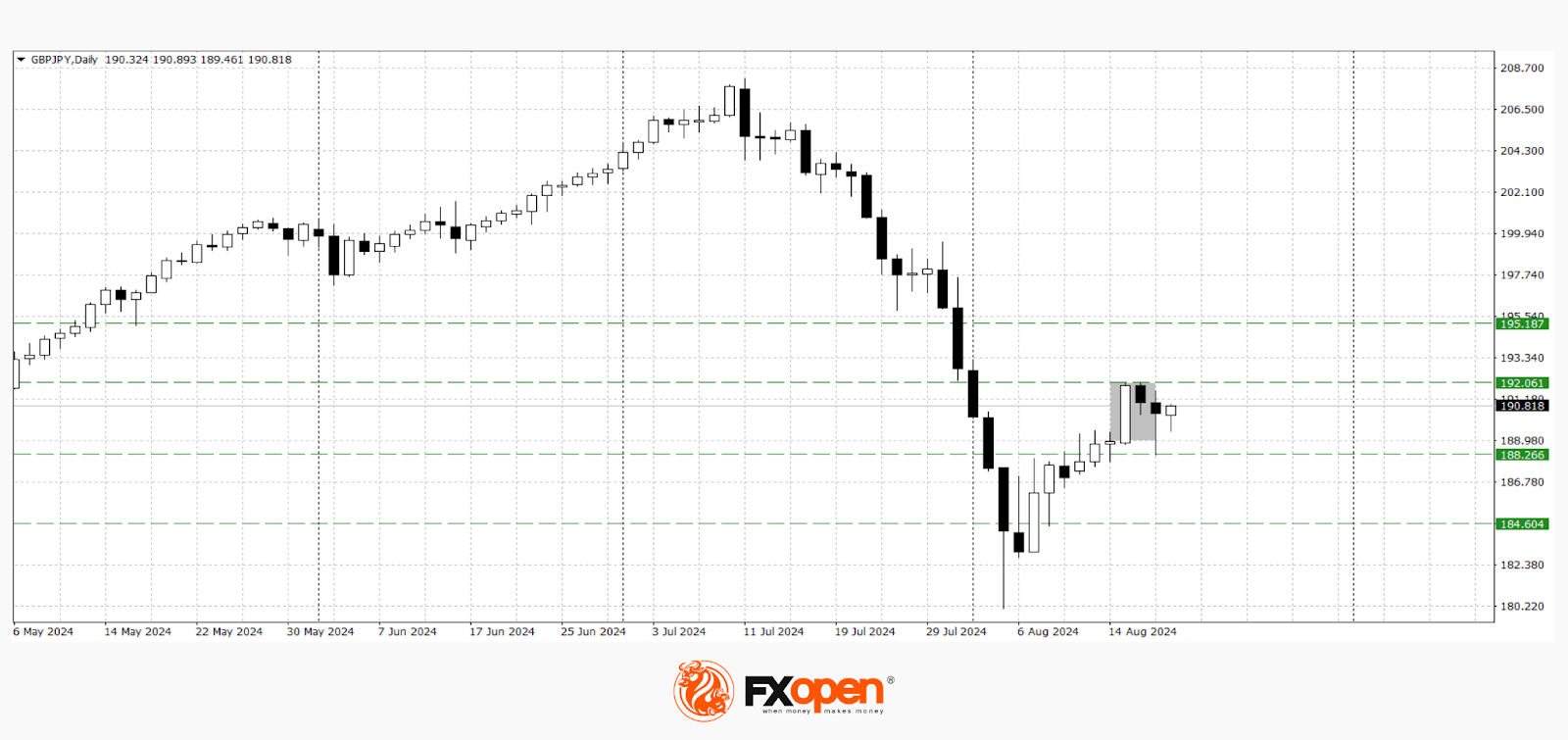

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.58; (P) 190.11; (R1) 191.97; More...

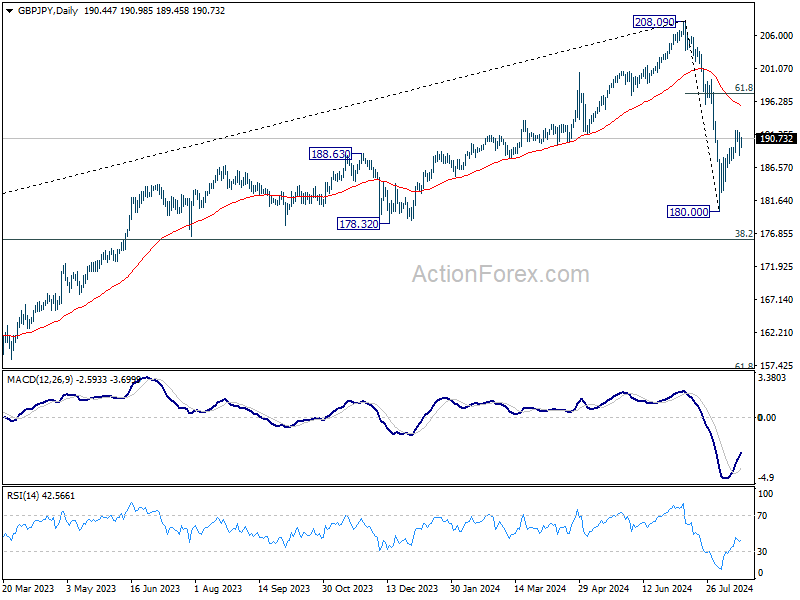

GBP/JPY is staying in range of 187.84/191.99 and intraday bias remains neutral first. On the upside, above 191.99 will target 61.8% retracement of 208.09 to 180.00 at 197.35, as the second leg of the corrective pattern from 208.09. On the downside, however, firm break of 187.84 support will turn bias back to the downside for retesting 180.00 instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). Current development suggests that the first leg has completed and the range of medium term consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09.

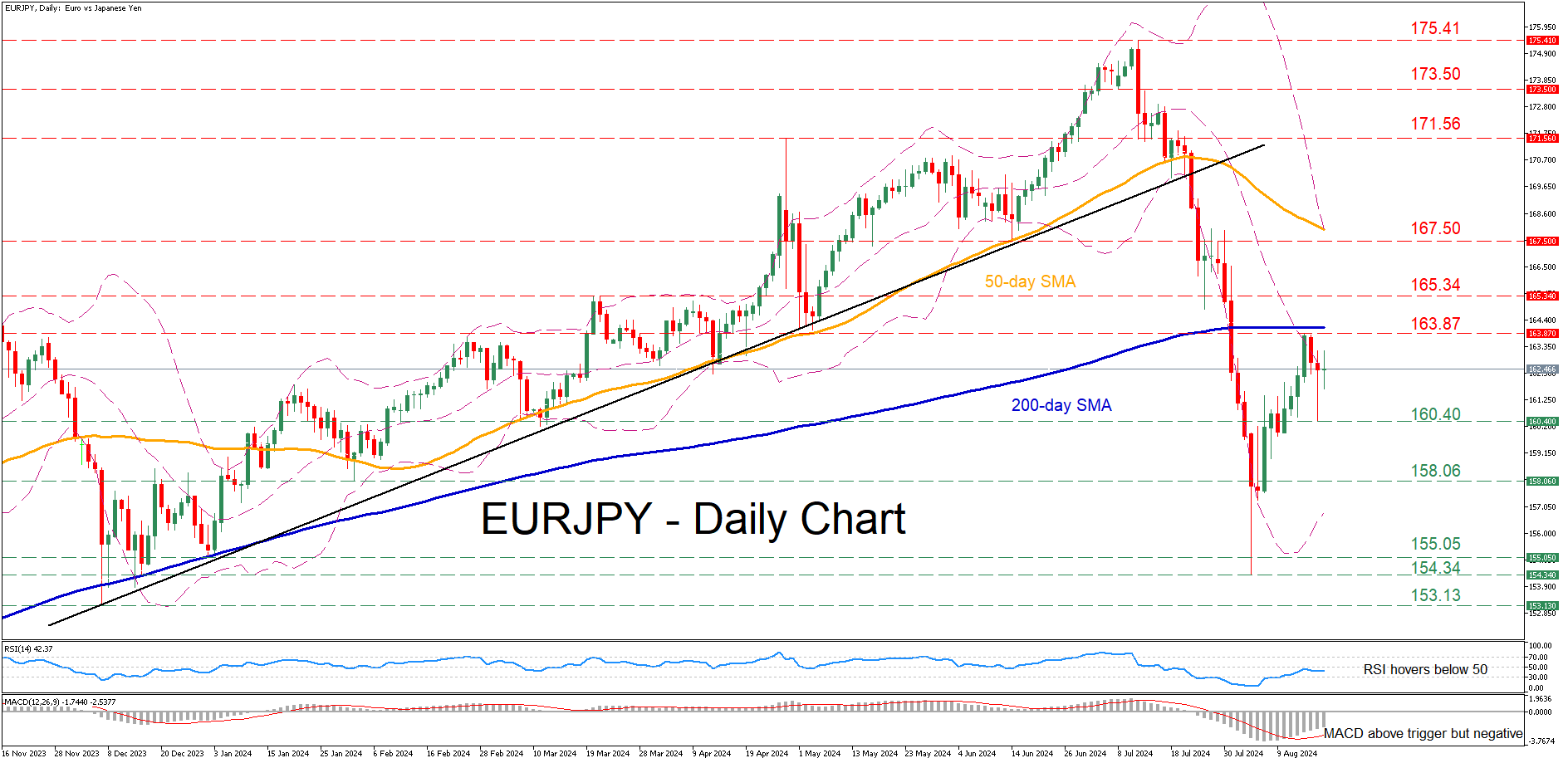

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.88; (P) 162.04; (R1) 163.67; More...

EUR/JPY recovered after drawing support from 160.57, but stays below 163.86 resistance. Intraday bias remains neutral at this point. On the upside, break of 163.86 will target 61.8% retracement of 175.41 to 154.40 at 167.38, as the second leg of the corrective pattern from 175.41. On the downside, however, firm break of 160.57 support will turn bias back to the downside for 154.40 instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Current development suggests that the first leg has completed. The range of consolidation should be seen between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high.

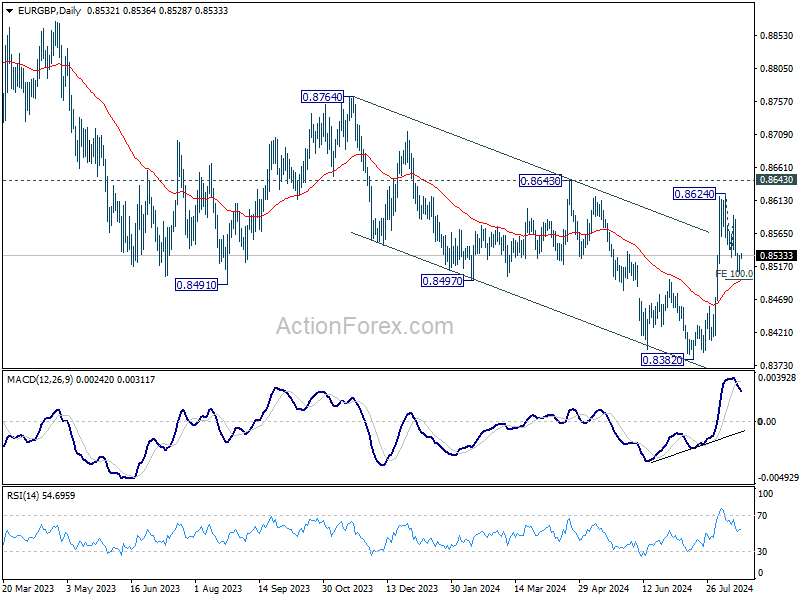

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8517; (P) 0.8525; (R1) 0.8542; More....

Intraday bias in EUR/GBP is turned neutral with current recovery. IN case of another fall, strong support should be seen from 100% projection of 0.8624 to 0.8530 from 0.8591 at 0.8497, which is close to 55 D EMA (now at 0.8494), to complete the correction from 0.8624. Break of 0.8591 resistance will argue that rise from 0.8382 is ready to resume through 0.8624.

In the bigger picture, while the rebound from 0.8382 is strong, there is no confirmation of trend reversal yet. As long as 0.8643 resistance holds, down trend from 0.9267 could still resume through 0.8382 at a later stage. However, firm break of 0.8643 will indicate that such down trend has completed, and turn outlook bullish for 0.8764 resistance next.