Sample Category Title

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0942; (P) 1.0980; (R1) 1.1010; More.....

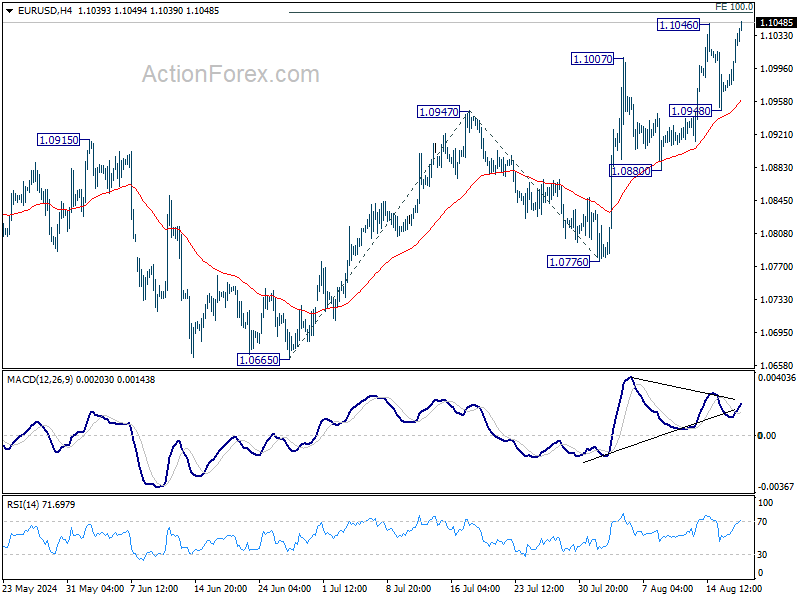

Intraday bias in EUR/USD is back on the upside as rise from 1.0665 is resuming through 1.1046. Firm break of 100% projection of 1.0665 to 1.0947 from 1.0776 at 1.1058 could prompt upside acceleration through 1.1138 resistance to 161.8% projection at 1.1232. However, considering bearish divergence condition in 4H MACD, break of 1.948 support will suggest near term reversal and turn bias to the downside for 1.0880 support and below.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's could still extend. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0776 support will extend the correction with another falling leg back towards 1.0447 support.

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.00; (P) 148.20; (R1) 148.83; More...

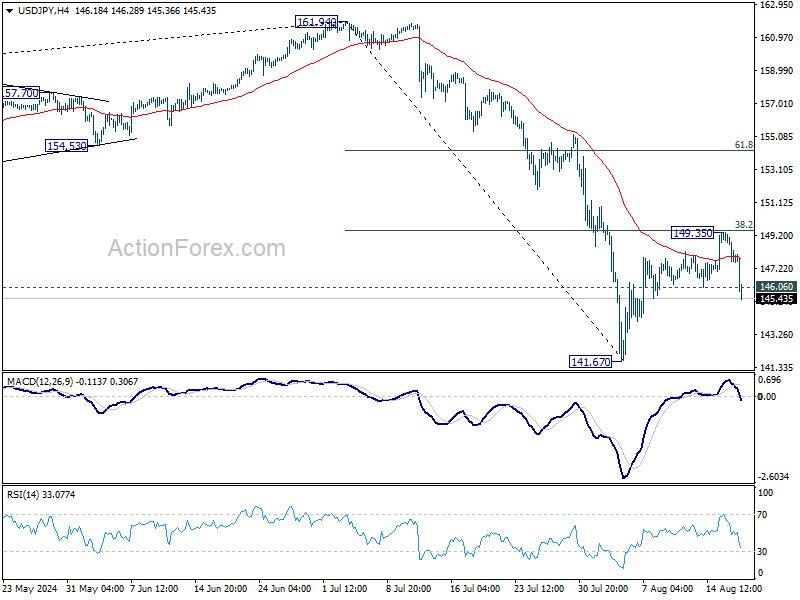

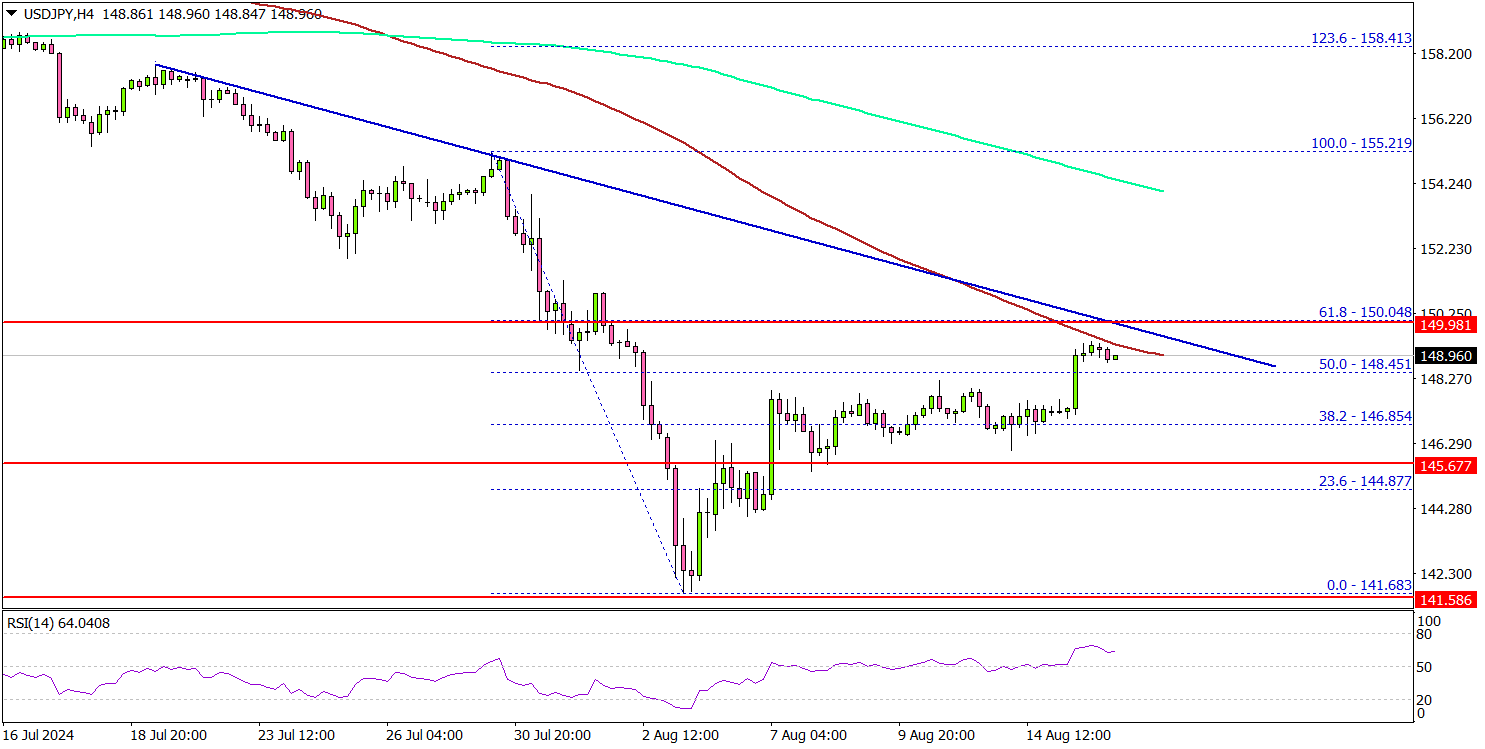

USD/JPY's break of 146.06 support argues that rebound from 141.67 has completed at 149.35 already, after rejection by 38.2% retracement of 161.94 to 141.67 at 149.41. Intraday bias is back on the downside for retesting 141.67. Firm break there will resume the whole fall from 161.94 to 139.26 fibonacci level next. For now, risk will stay on the downside as long as 149.35 resistance holds, in case of recovery.

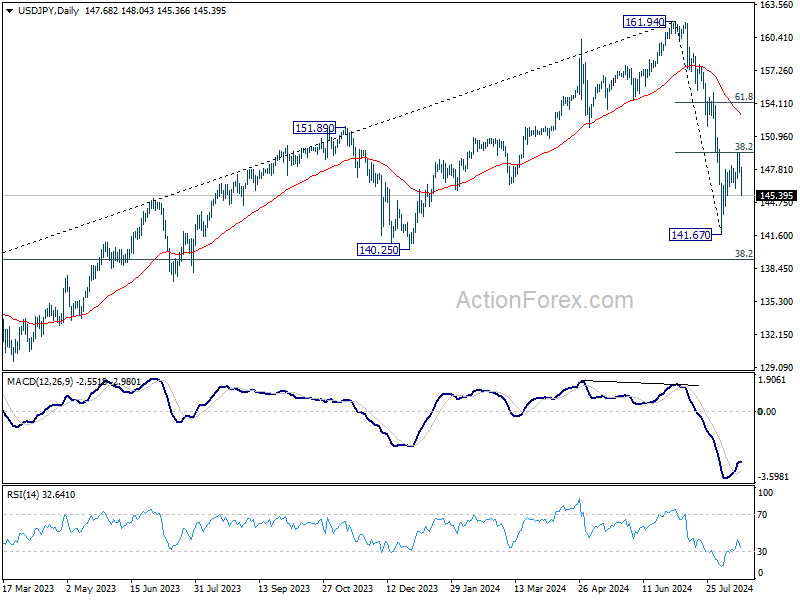

In the bigger picture, fall from 161.94 medium term is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.63) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

Yen Gains Ground as Dollar Weakens, Focus on Fed Powell’s Jackson Hole Speech This Week

Yen is showing broad-based strength in today’s Asian session, particularly against the generally weakening Dollar. This move has also put pressure on the Nikkei, which turned lower as Yen gained momentum. While there’s no clear catalyst for these movements, it appears that Yen’s recent pullback may have run its course. Meanwhile, Dollar continues to extend its decline from last week, driven by risk-on sentiment and falling treasury yields. With Fed Chair Jerome Powell’s upcoming speech at Jackson Hole this week, traders are also likely positioning themselves in anticipation of his remarks.

As we approach the final third of August, Yen stands out as the strongest currency of the month, followed at a distance by Australian Dollar and New Zealand Dollar. In contrast, Dollar has been the worst performer, while European currencies and Loonie are mixed, with the Euro holding a slight edge.

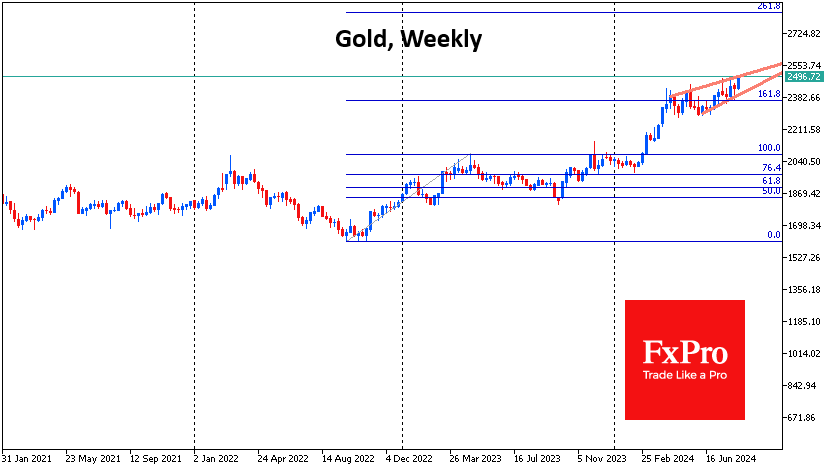

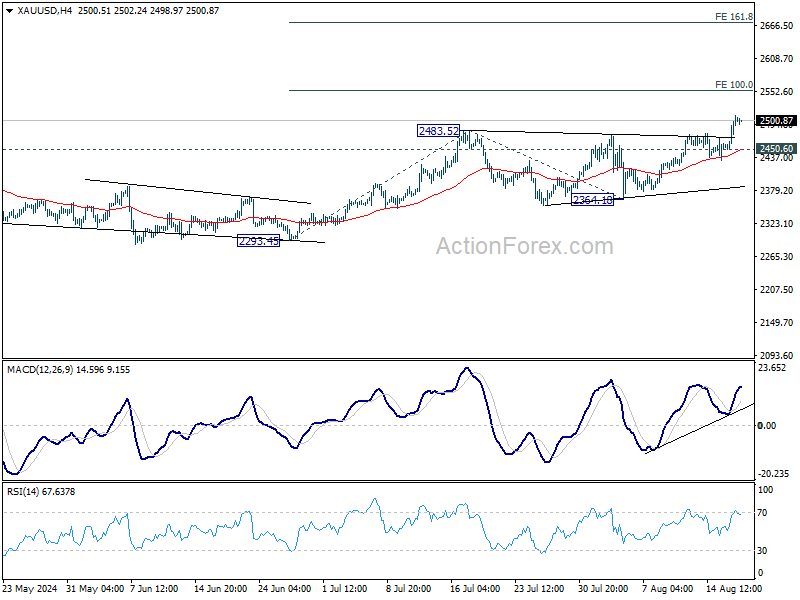

On the technical front, Gold capitalized on the Dollar’s weakness last week, surging to a new record high. Further rally is now expected as long as 2450.60 support holds. Next target is 100% projection of 2293.45 to 2483.52 from 2364.10 at 2554.17. The question is whether Dollar's selloff would intensify and prompt upside acceleration in Gold to 161.8% projection at 2671.63.

In Asia, at the time of writing, Nikkei is down -1.79%. Hong Kong HSI is up 0.89%. China Shanghai SSE is up 0.42%. Singapore Strait Times is down -0.10%. Japan 10-year JGB yield is up 0.0127 at 0.888.

Fed's Daly advocates for gradual rate cuts to avoid overtightening

San Francisco Fed President Mary Daly said in an FT interview that it's time to consider lowering interest rate from the current level gradually. She emphasized, "Gradualism is not weak, it's not slow, it's not behind, it’s just prudent,"

Daly said the Fed wanted to loosen the “restrictiveness” of its policy, while still maintaining some restraint to “fully get the job done” on inflation. The Fed did not “want to overtighten into a slowing economy”, she said.

Fed’s Goolsbee cautions against prolonged tightness in monetary policy

Chicago Fed President Austan Goolsbee stated in a CBS interview that a rate cut in September is not a foregone conclusion. But he pointed out that current economic conditions differ significantly from when Fed initially set rates at their present levels.

Goolsbee highlighted the impact of maintaining high rates while inflation decreases, noting that this approach effectively tightens monetary policy further. He warned that "if you keep too tight for too long, you will have a problem on the employment side of the Fed's mandate."

NZ BNZ services rises to 44.6, modest improvement, but remains under pressure

New Zealand BNZ Performance of Services Index saw a modest rise in July, climbing from 40.7 to 44.6. However, the PSI has averaged only 46.5 for 2024, a stark contrast to its historical average of 53.2.

Breaking down the details, there were slight improvements across most categories. Activity/sales increased from 36.2 to 39.1, and employment ticked up from 45.7 to 46.6. New orders/business rose from 38.9 to 45.3, and stock/inventories edged higher from 43.9 to 45.1. On the downside, supplier deliveries slipped slightly from 41.4 to 41.0.

Despite these gains, the overall sentiment remains cautious, with 67.0% of respondents expressing negative views about the current economic climate, unchanged from June. High living costs and rising interest rates were frequently cited as significant challenges.

BNZ’s Senior Economist Doug Steel provided a sobering perspective, noting that "the increase in the PSI does not even get the index back to the level it was during the depths of the GFC back in 2008/09."

Powell’s upcoming address to clarify Fed’s stance on rate cuts and recession risks

This week’s spotlight will be on Fed Chair Jerome Powell as he prepares to deliver his highly anticipated speech at the annual Jackson Hole Symposium. Markets are already expecting Powell to set the stage for a September interest rate cut, a move that has been largely priced in. However, investors are looking beyond the expected cut and focusing on several pressing concerns that could shape Fed's future actions.

A key concern of investors is the risk for a sudden and severe deterioration in the employment market, which could tip the US economy into a recession. Powell's speech will be closely watched for his view on the issue, and indication of how Fed plans to respond if such a downturn materializes.

Another critical issue is Fed's approach if inflation remains persistently high while the economy shows signs of significant weakness. This scenario would put the Fed in a difficult position, balancing the need to control inflation with the risk of exacerbating an economic slowdown. Powell’s views on this potential dilemma will be of great interest to market participants.

In addition to Powell’s speech, the release of monetary policy meeting minutes from key central banks will provide further insights into the global economic outlook. The minutes from the FOMC are expected to reveal a cautious stance, with Fed signaling that while a rate cut is likely on the horizon, policymakers are waiting for more data to confirm the timing.

Meanwhile, RBA is expected to reiterate its stance that a rate cut is not on the immediate agenda, while keeping the option open for further hikes if necessary. ECB minutes will be closely watched for any signs that the ECB is considering another rate cut in September, following its decision to pause in July.

On the economic data front, inflation reports from Canada and Japan will be in focus, alongside PMI data from several major economies.

Here are some highlights for the week:

- Monday: New Zealand BusinessNZ services index

- Tuesday: New Zealand trade balance; RBA minutes; Swiss trade balance; Germany PPI; Eurozone CPI final, current account; Canada CPI, new housing price index.

- Wednesday: Japan trade balance; Canada IPPI and RMPI; FOMC minutes.

- Thursday: Australia PMIs; Japan PMIs; Eurozone PMIs, ECB accounts; UK PMIs; US jobless claims, PMIs, existing home sales.

- Friday: New Zealand retail sales; Japan CPI; Canada retail sales; US new home sales.

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.00; (P) 148.20; (R1) 148.83; More...

USD/JPY's break of 146.06 support argues that rebound from 141.67 has completed at 149.35 already, after rejection by 38.2% retracement of 161.94 to 141.67 at 149.41. Intraday bias is back on the downside for retesting 141.67. Firm break there will resume the whole fall from 161.94 to 139.26 fibonacci level next. For now, risk will stay on the downside as long as 149.35 resistance holds, in case of recovery.

In the bigger picture, fall from 161.94 medium term is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.63) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Jul | 44.6 | 40.2 | 40.7 | |

| 23:50 | JPY | Machinery Orders M/M Jun | 2.10% | 0.90% | -3.20% |

USD/JPY On The Brink: A Surge Awaits If Resistance Falls

Key Highlights

- USD/JPY started a fresh increase above the 146.00 resistance.

- A major bearish trend line is forming with resistance at 150.00 on the 4-hour chart.

- Gold prices could again aim for a move above the $2,480 resistance.

- EUR/USD surged toward the 1.1040 level before the bears emerged.

USD/JPY Technical Analysis

The US Dollar started a fresh upward move above the 144.50 and 145.00 levels against the Japanese Yen. USD/JPY cleared the 146.50 level to enter a positive zone.

Looking at the 4-hour chart, the pair climbed above the 50% Fib retracement of the downward move from the 155.21 swing high to the 141.68 low. The pair showed positive signs and cleared the 148.00 resistance.

However, the pair is now facing many hurdles on the upside. The first key resistance sits near the 149.20 zone and the 100 simple moving average (red, 4-hour).

There is also a major bearish trend line forming with resistance at 150.00 on the same chart. The trend line is near the 61.8% Fib retracement of the downward move from the 155.21 swing high to the 141.68 low.

A clear move above the trend line might send the pair higher toward the 152.00 resistance or the 200 simple moving average (green, 4-hour).

Any more gains could send the pair toward the 155.00 level. Immediate support is near the 147.50 level. The next major support is near the 146.80 level. A downside break and close below the 146.80 support zone could open the doors for more losses. In the stated case, USD/JPY might decline toward the 145.50 level.

Looking at Gold, the price started a fresh increase and there are chances that the bulls might aim for a move above the $2,480 level.

Economic Releases

- US Housing Starts for July 2024 (MoM) – Forecast 1.330M, versus 1.353M previous.

- US Building Permits for July 2024 (MoM) – Forecast 1.430M, versus 1.454M previous.

NZ BNZ services rises to 44.6, modest improvement, but remains under pressure

New Zealand BNZ Performance of Services Index saw a modest rise in July, climbing from 40.7 to 44.6. However, the PSI has averaged only 46.5 for 2024, a stark contrast to its historical average of 53.2.

Breaking down the details, there were slight improvements across most categories. Activity/sales increased from 36.2 to 39.1, and employment ticked up from 45.7 to 46.6. New orders/business rose from 38.9 to 45.3, and stock/inventories edged higher from 43.9 to 45.1. On the downside, supplier deliveries slipped slightly from 41.4 to 41.0.

Despite these gains, the overall sentiment remains cautious, with 67.0% of respondents expressing negative views about the current economic climate, unchanged from June. High living costs and rising interest rates were frequently cited as significant challenges.

BNZ’s Senior Economist Doug Steel provided a sobering perspective, noting that "the increase in the PSI does not even get the index back to the level it was during the depths of the GFC back in 2008/09."

Fed’s Goolsbee cautions against prolonged tightness in monetary policy

Chicago Fed President Austan Goolsbee stated in a CBS interview that a rate cut in September is not a foregone conclusion. But he pointed out that current economic conditions differ significantly from when Fed initially set rates at their present levels.

Goolsbee highlighted the impact of maintaining high rates while inflation decreases, noting that this approach effectively tightens monetary policy further. He warned that "if you keep too tight for too long, you will have a problem on the employment side of the Fed's mandate."

Fed’s Daly advocates for gradual rate cuts to avoid overtightening

San Francisco Fed President Mary Daly indicated in an interview with the Financial Times that the time has come to consider gradually lowering interest rates from their current levels. Daly emphasized the importance of a cautious approach, stating, "Gradualism is not weak, it's not slow, it's not behind, it’s just prudent."

She explained that while Fed aims to reduce the “restrictiveness” of its policy, it intends to maintain a level of restraint necessary to “fully get the job done” on inflation. Daly underscored the Fed's focus on avoiding the risk of "overtightening into a slowing economy."

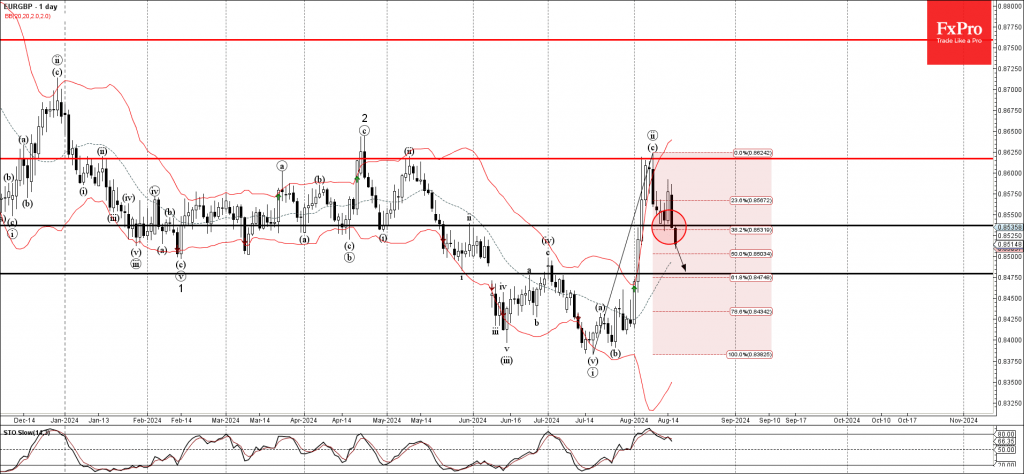

EURGBP Wave Analysis

- EURGBP broke support area

- Likely to fall to support level 0.8475

EURGBP currency pair just broke the support area set between the support level 0.8535 (which reversed the price twice earlier this week) and the 38.2% Fibonacci correction of the earlier sharp upward impulse from July.

The breakout of this support area is aligned with the clear multi-month downtrend seen on the daily EURGBP charts.

Given the strongly bullish sterling sentiment seen across the FX markets today, EURGBP currency pair can be expected to fall further toward the next support level 0.8475.

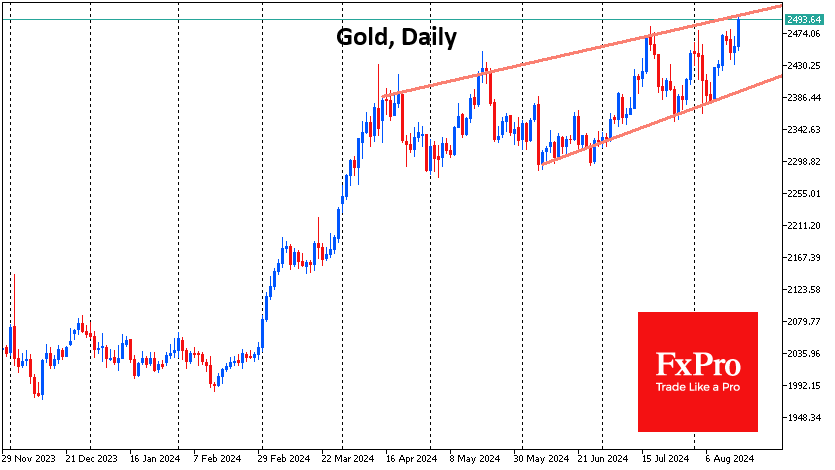

Gold: Third Time Lucky?

Gold has been rising steadily since the end of last week and is attempting to consolidate above $2470 per troy ounce on the spot market for the third time in the last 30 days. Gold has moved in tandem with equities this month, but it is worth noting that it fell less aggressively during the panic and outpaced the rally.

So, gold is riding on a global recovery in demand for risk assets, but it has the fundamental support in its arsenal that has pushed the price to repeated all-time highs since March.

A trend line can be drawn across the local lows of May from which gold rallied in the early days of August. Combined with local resistance at $2475, this forms a bullish triangle with a high probability of a breakout.

The next upside target is $2500. This is the psychologically important round level and the resistance line of the uptrend drawn by the April, May and July highs.

As far as more distant growth targets are concerned, the $2800-2900 area is worth mentioning. The upper boundary of this range is the 261.8% Fibonacci level of growth from the September-October 2022 lows to the April 2023 highs.

The lower boundary of the range is formed by the 161.8% level of the growth impulse from the October lows to the April-May highs. This rally began with the first signs of a shift in the Fed’s monetary policy, supported by tensions in the Middle East and the desire of some central banks to diversify their reserves away from the dollar.