Sample Category Title

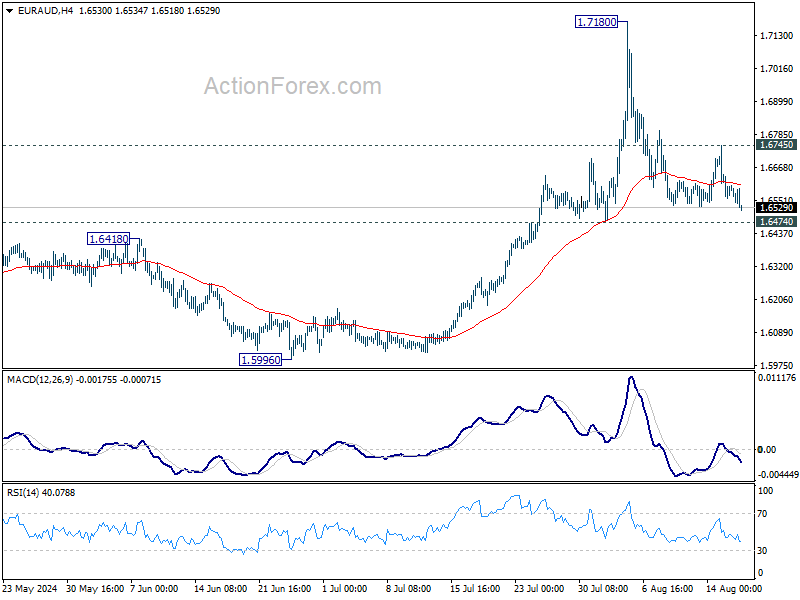

EUR/AUD Weekly Outlook

EUR/AUD's correction from 1.7180 short term top continued last week, but downside is contained above 1.6474 support so far. Initial bias remains neutral this week first, and further rally is in favor. On the upside, above 1.6745 will argue that the pullback has completed, and turn bias back to the upside for retesting 1.7180. However, firm break of 1.6474 will dampen the bullish view and bring deeper pullback towards 1.5996 support.

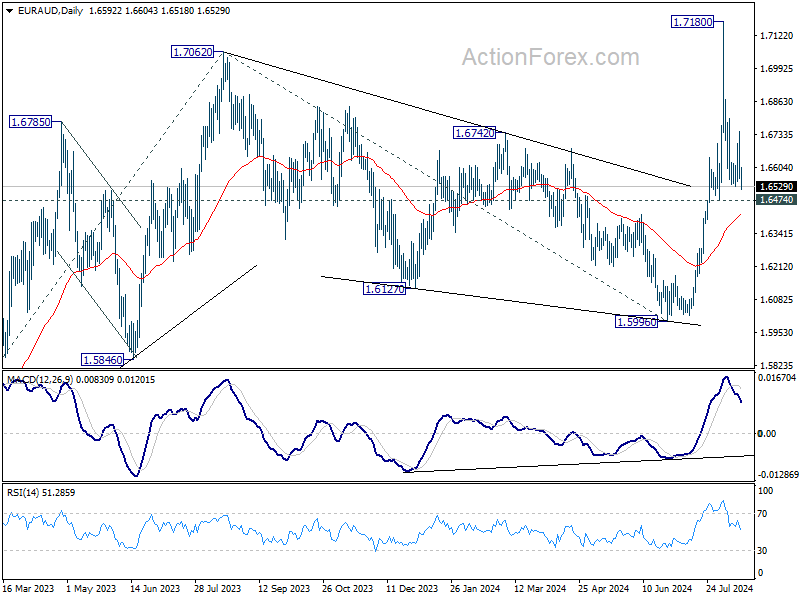

In the bigger picture, corrective fall from 1.7062 medium term top should have completed at 1.5996. Larger up trend from 1.4281 (2022 low) is resuming. Next target is 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715. This will now remain the favored case as long as 1.6474 support holds.

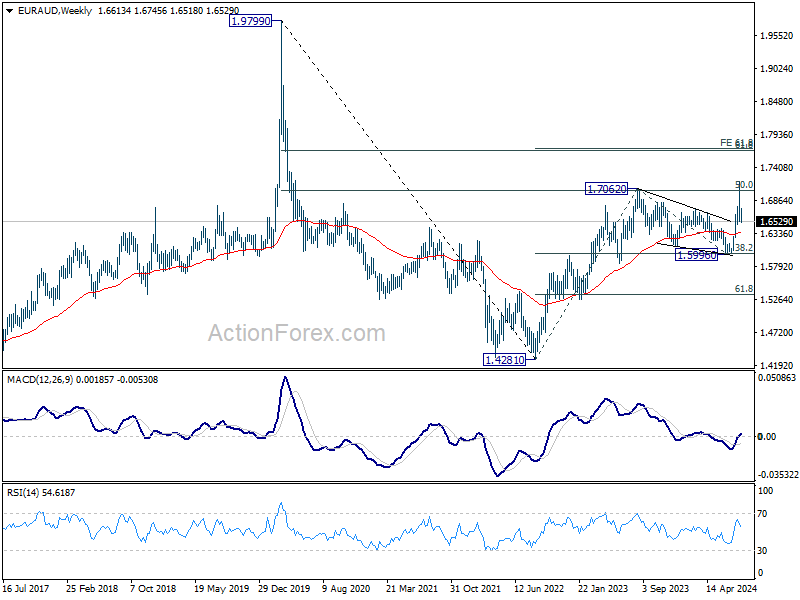

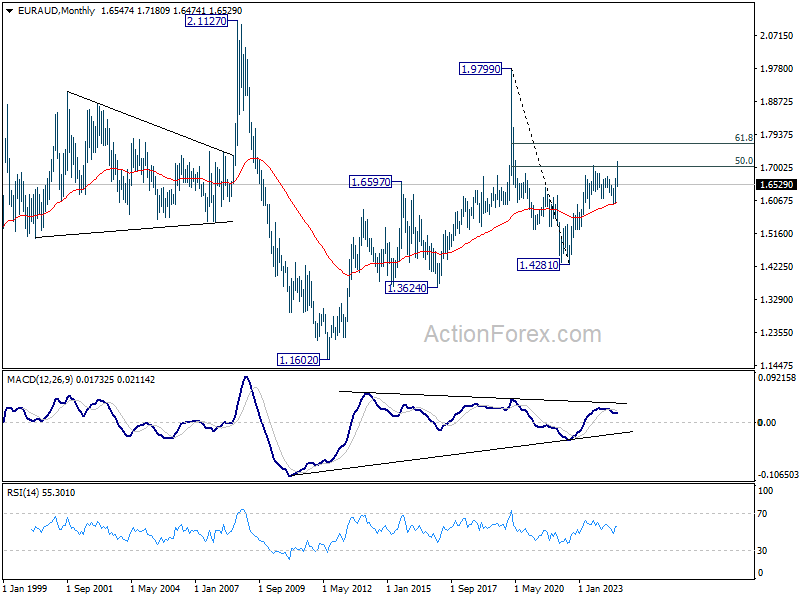

In the longer term picture, price actions from 1.9799 (2020 high) are seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.6006) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

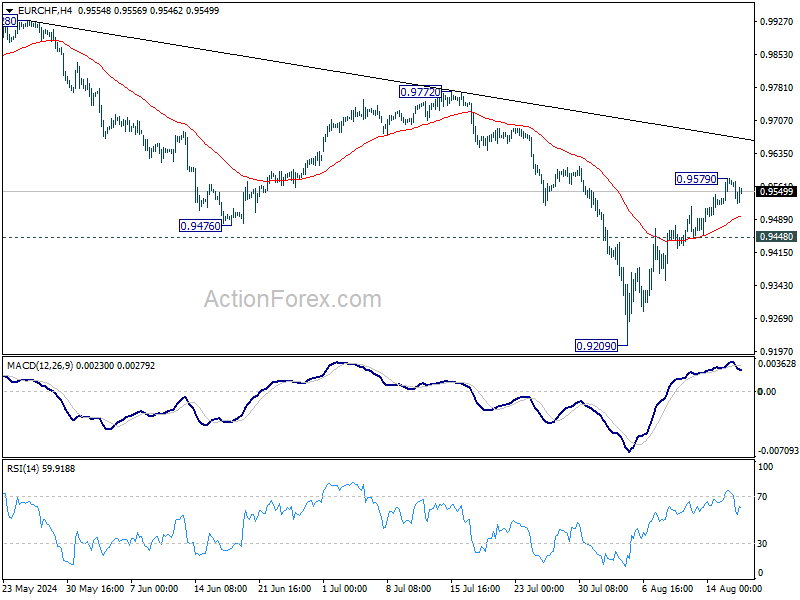

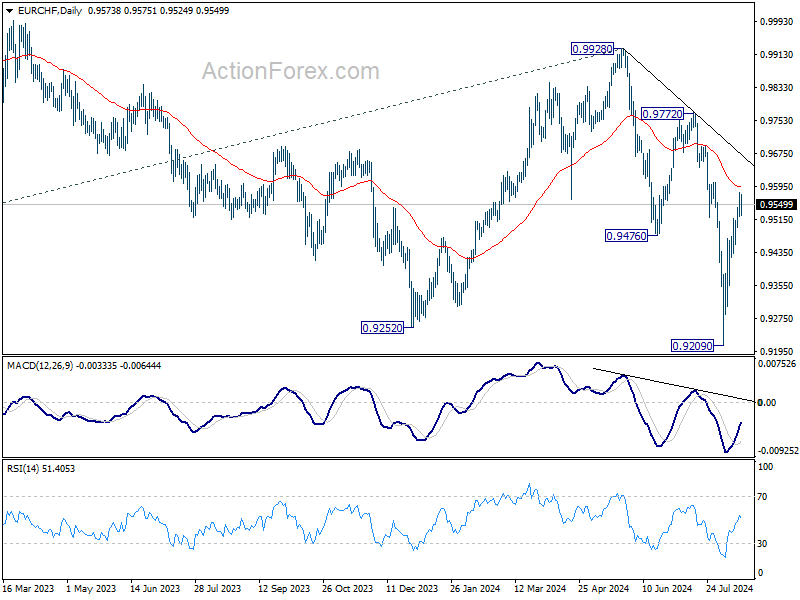

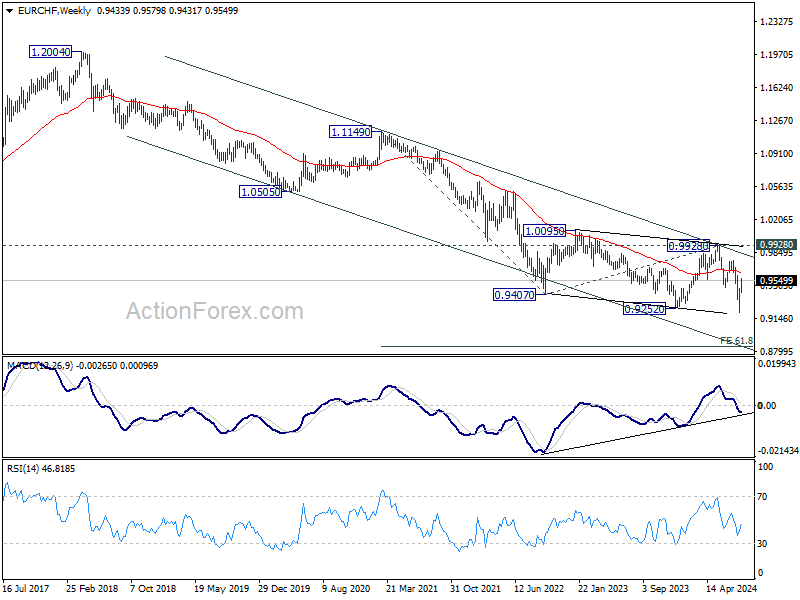

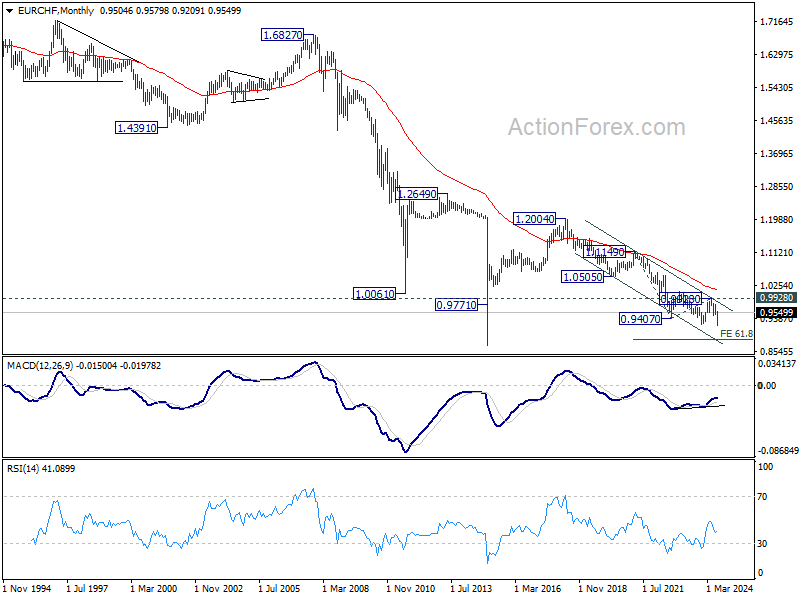

EUR/CHF Weekly Outlook

EUR/CHF's rebound from 0.9209 extended to as high as 0.9579 last week before retreating. Initial bias is turned neutral this week first for some consolidations. Further rally is expected as long as 0.9448 support holds. Sustained break of 55 D EMA (now at 0.9593) will pave the way back to 0.9972/0.9928 resistance zone. However, decisive break of 0.9448 will suggest rejection by 55 D EMA, and turn bias back to the downside for 0.9209 low.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 0.9928 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

Summary 8/19 – 8/23

Monday, Aug 19, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Jul | 40.2 | |

| 23:50 | JPY | Machinery Orders M/M Jun | 0.90% | -3.20% |

| 22:45 | NZD | Trade Balance (NZD) Jul | 331M | 699M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Jul | |

| Forecast: | Previous: 40.2 | ||

| 23:50 | JPY | Machinery Orders M/M Jun | |

| Forecast: 0.90% | Previous: -3.20% | ||

| 22:45 | NZD | Trade Balance (NZD) Jul | |

| Forecast: 331M | Previous: 699M | ||

Tuesday, Aug 20, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:15 | CNY | PBoC 1-Y Loan Prime Rate | 3.35% | 3.35% |

| 01:15 | CNY | PBoC 5-Y Loan Prime Rate | 3.85% | 3.85% |

| 01:30 | AUD | RBA Meeting Minutes | ||

| 06:00 | CHF | Trade Balance (CHF) Jul | 5.44B | 6.18B |

| 06:00 | EUR | Germany PPI M/M Jul | 0.30% | 0.20% |

| 06:00 | EUR | Germany PPI Y/Y Jul | -1.60% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Jun | 36.7B | |

| 09:00 | EUR | Eurozone CPI Y/Y Jul F | 2.60% | 2.60% |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jul F | 2.90% | 2.90% |

| 12:30 | CAD | New Housing Price Index M/M Jul | 0.00% | -0.20% |

| 12:30 | CAD | CPI M/M Jul | 0.30% | -0.10% |

| 12:30 | CAD | CPI Y/Y Jul | 2.70% | |

| 12:30 | CAD | CPI Median Y/Y Jul | 2.50% | 2.60% |

| 12:30 | CAD | CPI Trimmed Y/Y Jul | 2.70% | 2.90% |

| 12:30 | CAD | CPI Common Y/Y Jul | 2.20% | 2.30% |

| 23:50 | JPY | Trade Balance (JPY) Jul | -0.76T | -0.82T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:15 | CNY | PBoC 1-Y Loan Prime Rate | |

| Forecast: 3.35% | Previous: 3.35% | ||

| 01:15 | CNY | PBoC 5-Y Loan Prime Rate | |

| Forecast: 3.85% | Previous: 3.85% | ||

| 01:30 | AUD | RBA Meeting Minutes | |

| Forecast: | Previous: | ||

| 06:00 | CHF | Trade Balance (CHF) Jul | |

| Forecast: 5.44B | Previous: 6.18B | ||

| 06:00 | EUR | Germany PPI M/M Jul | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 06:00 | EUR | Germany PPI Y/Y Jul | |

| Forecast: | Previous: -1.60% | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Jun | |

| Forecast: | Previous: 36.7B | ||

| 09:00 | EUR | Eurozone CPI Y/Y Jul F | |

| Forecast: 2.60% | Previous: 2.60% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Jul F | |

| Forecast: 2.90% | Previous: 2.90% | ||

| 12:30 | CAD | New Housing Price Index M/M Jul | |

| Forecast: 0.00% | Previous: -0.20% | ||

| 12:30 | CAD | CPI M/M Jul | |

| Forecast: 0.30% | Previous: -0.10% | ||

| 12:30 | CAD | CPI Y/Y Jul | |

| Forecast: | Previous: 2.70% | ||

| 12:30 | CAD | CPI Median Y/Y Jul | |

| Forecast: 2.50% | Previous: 2.60% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Jul | |

| Forecast: 2.70% | Previous: 2.90% | ||

| 12:30 | CAD | CPI Common Y/Y Jul | |

| Forecast: 2.20% | Previous: 2.30% | ||

| 23:50 | JPY | Trade Balance (JPY) Jul | |

| Forecast: -0.76T | Previous: -0.82T | ||

Wednesday, Aug 21, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M Jul | 0.00% | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jul | 0.5B | 13.6B |

| 12:30 | CAD | Industrial Product Price M/M Jul | -0.50% | 0.00% |

| 12:30 | CAD | Raw Material Price Index Jul | -0.90% | -1.40% |

| 12:30 | CAD | New Housing Price Index Y/Y Jul | -0.20% | |

| 14:30 | USD | Crude Oil Inventories | 1.4M | |

| 18:00 | USD | FOMC Minutes | ||

| 23:00 | AUD | Manufacturing PMI Aug P | 47.5 | |

| 23:00 | AUD | Services PMI Aug P | 50.4 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M Jul | |

| Forecast: | Previous: 0.00% | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jul | |

| Forecast: 0.5B | Previous: 13.6B | ||

| 12:30 | CAD | Industrial Product Price M/M Jul | |

| Forecast: -0.50% | Previous: 0.00% | ||

| 12:30 | CAD | Raw Material Price Index Jul | |

| Forecast: -0.90% | Previous: -1.40% | ||

| 12:30 | CAD | New Housing Price Index Y/Y Jul | |

| Forecast: | Previous: -0.20% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 1.4M | ||

| 18:00 | USD | FOMC Minutes | |

| Forecast: | Previous: | ||

| 23:00 | AUD | Manufacturing PMI Aug P | |

| Forecast: | Previous: 47.5 | ||

| 23:00 | AUD | Services PMI Aug P | |

| Forecast: | Previous: 50.4 | ||

Thursday, Aug 22, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Aug P | 49.8 | 49.1 |

| 00:30 | JPY | Services PMI Aug P | 53.7 | |

| 07:15 | EUR | France Manufacturing PMI Aug P | 44.6 | 44 |

| 07:15 | EUR | France Services PMI Aug P | 50.5 | 50.1 |

| 07:30 | EUR | Germany Manufacturing PMI Aug P | 43.5 | 43.2 |

| 07:30 | EUR | Germany Services PMI Aug P | 52.4 | 52.5 |

| 08:00 | EUR | Eurozone Manufacturing PMI Aug P | 46.1 | 45.8 |

| 08:00 | EUR | Eurozone Services PMI Aug P | 52.2 | 51.9 |

| 08:30 | GBP | Manufacturing PMI Aug P | 52.2 | 52.1 |

| 08:30 | GBP | Services PMI Aug P | 52.8 | 52.5 |

| 11:30 | EUR | ECB Meeting Accounts | ||

| 12:30 | USD | Initial Jobless Claims (Aug 16) | 230K | 227K |

| 13:45 | USD | Manufacturing PMI Aug P | 49.4 | 49.6 |

| 13:45 | USD | Services PMI Aug P | 54.2 | 55.0 |

| 14:00 | USD | Existing Home Sales Jul | 3.89M | 3.89M |

| 14:00 | EUR | Eurozone Consumer Confidence Aug P | -11 | -13 |

| 14:30 | USD | Natural Gas Storage | -6B | |

| 22:45 | NZD | Retail Sales Q/Q Q2 | 0.50% | 0.50% |

| 22:45 | NZD | Retail Sales ex Autos Q/Q Q2 | 0.50% | 0.40% |

| 23:01 | GBP | GfK Consumer Confidence Aug | -11 | -13 |

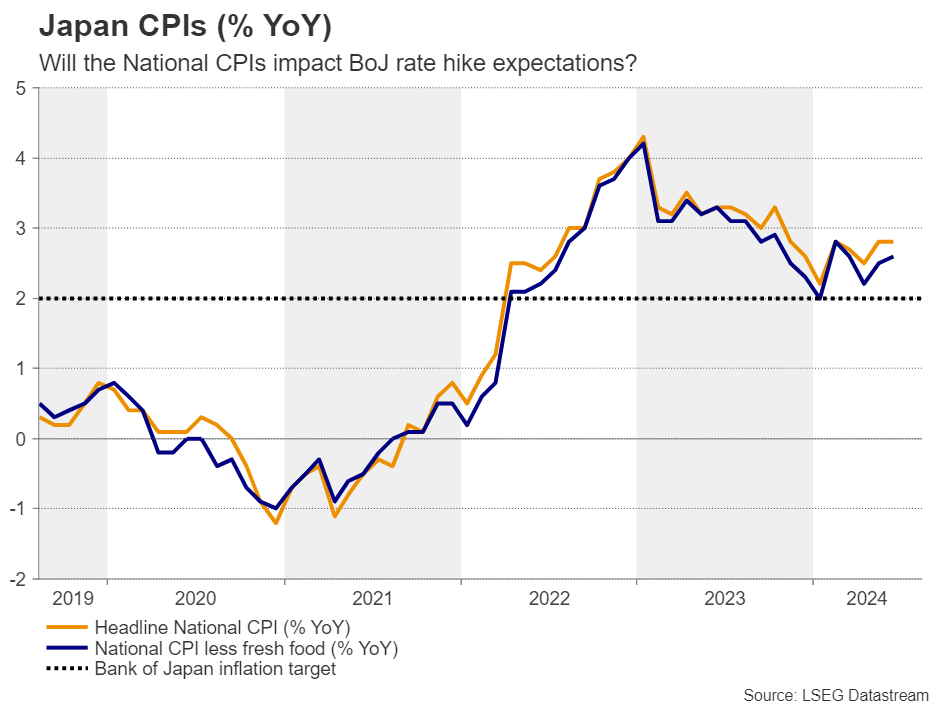

| 23:30 | JPY | National CPI Y/Y Jul | 2.80% | |

| 23:30 | JPY | National CPI Core Y/Y Jul | 2.70% | 2.60% |

| 23:30 | JPY | National CPI Core-Core Y/Y Jul | 2.20% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Aug P | |

| Forecast: 49.8 | Previous: 49.1 | ||

| 00:30 | JPY | Services PMI Aug P | |

| Forecast: | Previous: 53.7 | ||

| 07:15 | EUR | France Manufacturing PMI Aug P | |

| Forecast: 44.6 | Previous: 44 | ||

| 07:15 | EUR | France Services PMI Aug P | |

| Forecast: 50.5 | Previous: 50.1 | ||

| 07:30 | EUR | Germany Manufacturing PMI Aug P | |

| Forecast: 43.5 | Previous: 43.2 | ||

| 07:30 | EUR | Germany Services PMI Aug P | |

| Forecast: 52.4 | Previous: 52.5 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Aug P | |

| Forecast: 46.1 | Previous: 45.8 | ||

| 08:00 | EUR | Eurozone Services PMI Aug P | |

| Forecast: 52.2 | Previous: 51.9 | ||

| 08:30 | GBP | Manufacturing PMI Aug P | |

| Forecast: 52.2 | Previous: 52.1 | ||

| 08:30 | GBP | Services PMI Aug P | |

| Forecast: 52.8 | Previous: 52.5 | ||

| 11:30 | EUR | ECB Meeting Accounts | |

| Forecast: | Previous: | ||

| 12:30 | USD | Initial Jobless Claims (Aug 16) | |

| Forecast: 230K | Previous: 227K | ||

| 13:45 | USD | Manufacturing PMI Aug P | |

| Forecast: 49.4 | Previous: 49.6 | ||

| 13:45 | USD | Services PMI Aug P | |

| Forecast: 54.2 | Previous: 55.0 | ||

| 14:00 | USD | Existing Home Sales Jul | |

| Forecast: 3.89M | Previous: 3.89M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Aug P | |

| Forecast: -11 | Previous: -13 | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -6B | ||

| 22:45 | NZD | Retail Sales Q/Q Q2 | |

| Forecast: 0.50% | Previous: 0.50% | ||

| 22:45 | NZD | Retail Sales ex Autos Q/Q Q2 | |

| Forecast: 0.50% | Previous: 0.40% | ||

| 23:01 | GBP | GfK Consumer Confidence Aug | |

| Forecast: -11 | Previous: -13 | ||

| 23:30 | JPY | National CPI Y/Y Jul | |

| Forecast: | Previous: 2.80% | ||

| 23:30 | JPY | National CPI Core Y/Y Jul | |

| Forecast: 2.70% | Previous: 2.60% | ||

| 23:30 | JPY | National CPI Core-Core Y/Y Jul | |

| Forecast: | Previous: 2.20% | ||

Friday, Aug 23, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 12:30 | CAD | Retail Sales M/M Jun | -0.30% | -0.80% |

| 12:30 | CAD | Retail Sales ex Autos M/M Jun | -0.40% | -1.30% |

| 14:00 | USD | New Home Sales Jul | 630K | 617K |

| GMT | Ccy | Events | |

|---|---|---|---|

| 12:30 | CAD | Retail Sales M/M Jun | |

| Forecast: -0.30% | Previous: -0.80% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Jun | |

| Forecast: -0.40% | Previous: -1.30% | ||

| 14:00 | USD | New Home Sales Jul | |

| Forecast: 630K | Previous: 617K | ||

Markets Weekly Outlook – Gold Hits New ATH Ahead of Jackson Hole Symposium

- Gold reaches a new all-time high as markets reassess rate cut expectations after evaluating resilient US data.

- The Jackson Hole Symposium will be a key event next week, with central bankers discussing strategies for growth and monetary policy.

- It’s a data-heavy week in Europe and the US, with the release of FOMC minutes, PMI data, and speeches from Fed Chair Powell and BoE Governor Bailey.

Week in Review: Data Heavy Week Leaves more Questions Than Answers

As the week draws to a close, many market participants who had anticipated clarity are left with more questions after evaluating resilient US data.

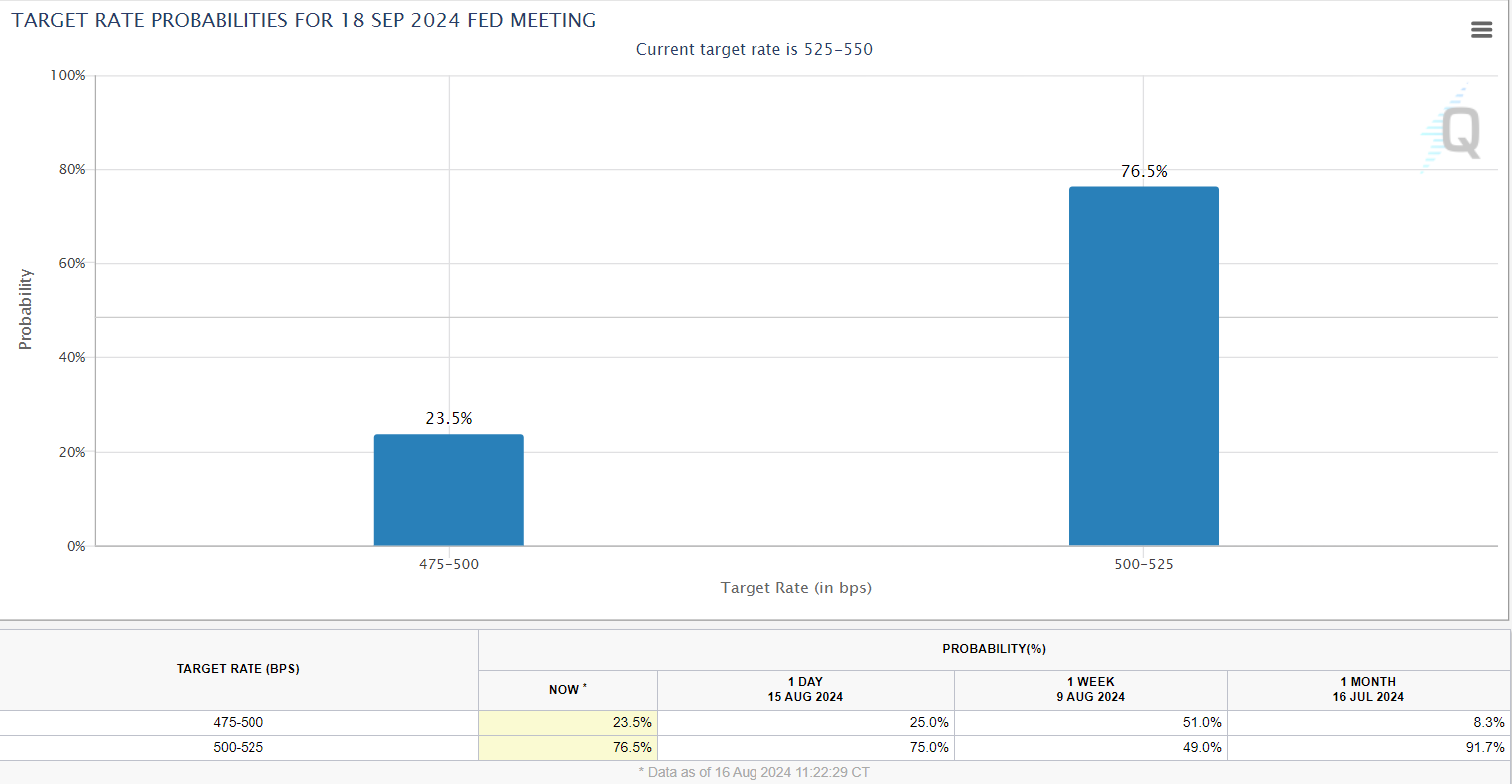

This data has led to a reassessment of rate cut expectations. Previously, markets were pricing in a 51% chance of a 50bps cut, which has now been drastically reduced to 23.5%. Despite this, gold reached a new all-time high of $2500/oz, while both the Euro and GBP made significant gains against the USD.

Source: CME FedWatch Tool

The GBP notably gained from a series of positive data releases, with Friday’s GDP figures surpassing expectations. This propelled Cable into the 1.2900s, with the key psychological level of 1.3000 now within reach as we head into next week.

Oil prices struggled to maintain last week’s rally, ending the week on a bearish note and resulting in a doji weekly candle that could indicate either a bullish or bearish trend.

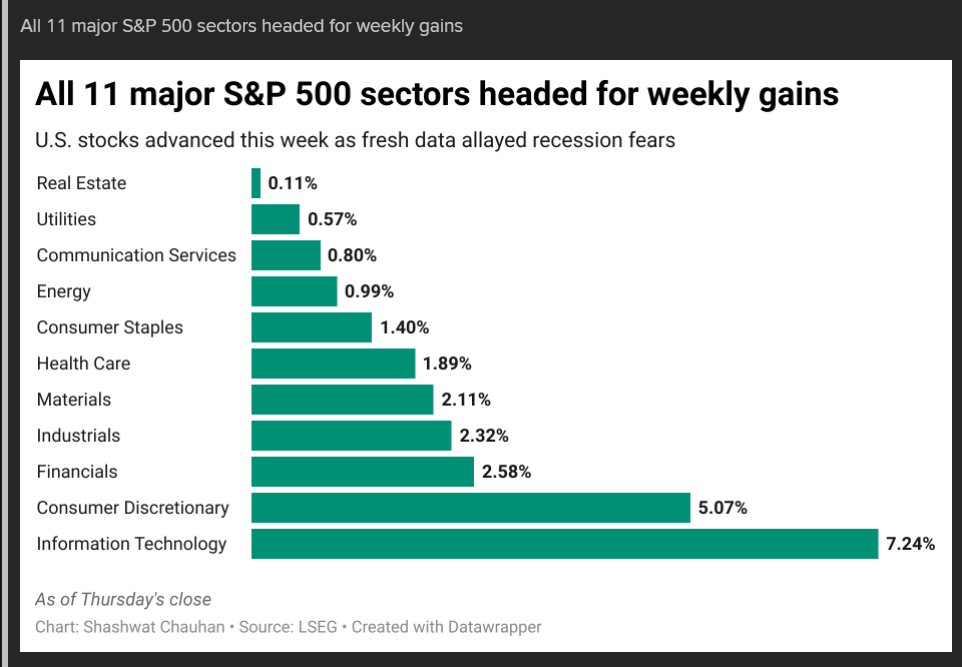

In contrast, US indices had an exceptional week, rallying significantly. The S&P 500 is poised for a 3.2% gain, while the Nasdaq 100 is on track for even stronger gains of around 5.2% at the time of writing.

This sharp shift in market sentiment was driven by a series of positive US data releases, which continued on Friday with improved consumer sentiment data and stable inflation expectations for the next 12 months.

Source: LSEG

The Week Ahead: Jackson Hole and PMI data at the forefront

The Jackson Hole Symposium this year holds significant importance as a gathering of global central bankers, economists, and financial market participants. This year, the symposium’s focus is once again on navigating the post-pandemic economic recovery and addressing the challenges posed by higher interest rates and geopolitical tensions.

Key topics include strategies for sustainable growth, monetary policy adjustments, and the implications of digital currencies on the global financial system. Notable speakers at this year’s event include Federal Reserve Chair Jerome Powell, European Central Bank President Christine Lagarde, and Bank of England Governor Andrew Bailey. Their insights are anticipated to shape market expectations and policy directions for the coming year

The Symposium could stoke volatility across a host of currency pairs and will need to be monitored closely.

Asia Pacific Markets

In Asia, the upcoming week looks quiet for China, having just wrapped up its significant monthly data releases. On Tuesday, an announcement regarding the loan prime rates is anticipated. No changes are expected, given that the MLF and 7-day reverse repo rates have remained steady throughout August.

Looking at Japan and the flash PMIs are expected to improve, driven by a positive outlook for service activity, despite recent fluctuations in the JPY and a significant drop in equity markets. Increased semiconductor and auto exports, along with core machine orders data, also indicate a boost in manufacturers’ sentiment. Additionally, inflation is anticipated to pick up again in July, as previously indicated by Tokyo’s earlier inflation figures.

Europe + UK + US

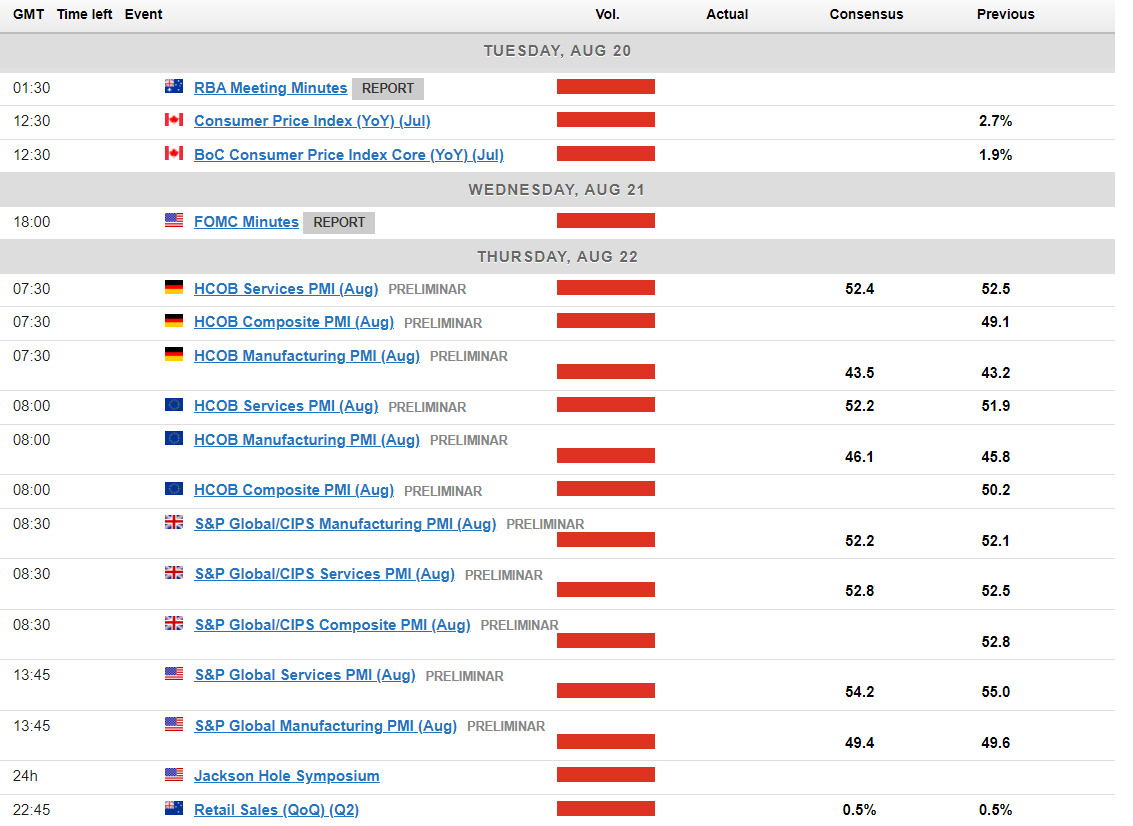

In Europe and the US, it’s another data-heavy week. Beyond Jackson Hole, the week starts with the RBA minutes and Canadian inflation data on Tuesday.

On Wednesday, the FOMC minutes will be released, potentially offering more clarity on Fed policymakers’ stance concerning a possible rate cut in September. Thursday is particularly busy with PMI data coming from the EU, UK, and US.

The week concludes on Friday with speeches from Fed Chair Powell at Jackson Hole and BoE Governor Andrew Bailey.

Chart of the Week

This week’s highlighted chart is the US Dollar Index (DXY), which continues to play a crucial role in the financial markets.

The DXY revisited last week’s lows but experienced a rebound on Thursday, resulting in a morning star pattern on the candlestick chart, suggesting a potential deeper recovery. However, sellers dominated on Friday, driving the DXY back towards last week’s lows around the 102.00 level.

Currently, the DXY is positioned just below a key resistance level at 102.64. A daily close at this level would mark the lowest daily close since January 2024.

If the index moves downward from its current position, it would likely find support around the 102.00 level, with attention then shifting to the significant psychological level of 100.00.

On the upside, immediate resistance is at 102.64, followed by the 103.00 and 103.65 levels as the next focal points.

US Dollar Index (DXY) Daily Chart – June 28, 2024

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support:

- 102.00

- 101.50

- 100.00

Resistance:

- 102.64

- 103.00

- 103.65

The Weekly Bottom Line: Inching Towards a Pivot

U.S. Highlights

- The July report for the Consumer Price Index showed headline inflation fell below 3% for the first time since March 2021.

- U.S. retail sales surpassed expectations in July, rising 1.0% month-on-month.

- Federal Reserve Chair Jerome Powell’s remarks during next week’s Jackson Hole Symposium will headline the week.

Canadian Highlights

- Bad news for Canada’s international trade this week, as the U.S. hiked softwood lumber duties and Canada’s two major rail lines halted shipments of certain goods ahead of a potential lockout.

- Housing activity took a breather in July after a strong showing in June. Still, the soft patch will likely prove to be temporary amid falling interest rates and a resilient economy.

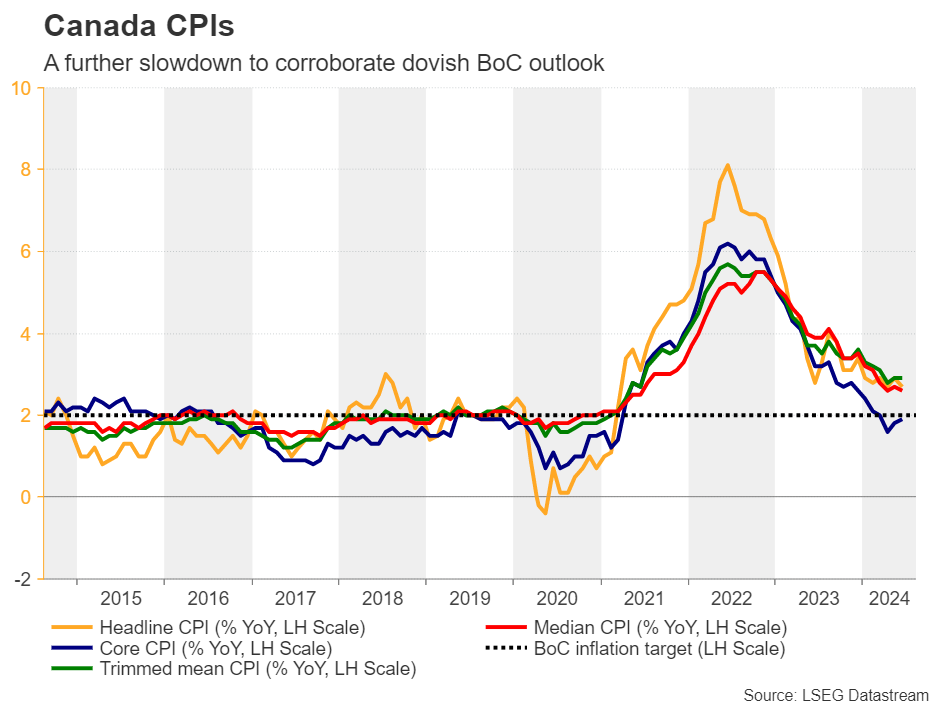

- The marquee event on next week’s data calendar is the July inflation report. We expect core inflation to have eased, leaving the door wide open for a September rate cut.

U.S. – Inching Towards a Pivot

A relative state of calm presided over financial markets this week as incoming economic data continued to support the case for the first Federal Reserve rate cut in September. Inflation data for July showed that the annual change in prices fell below 3% for the first time since March 2021, while retail sales for the month came in above expectations. In response, equity markets rose on the week with the S&P 500 up 3.7% as of the time of writing, while U.S. Treasury yields steadied with the two-year yield roughly unchanged at 4.08%.

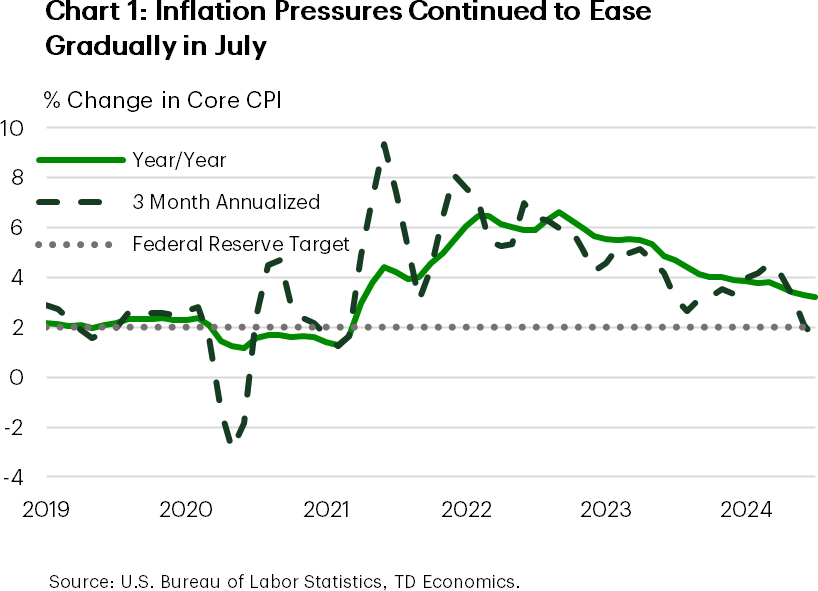

The Consumer Price Index (CPI) report for July showed that inflation picked up slightly relative to June in monthly terms, primarily driven by an uptick in shelter costs. However, the monthly increase in headline and core inflation was still below the level consistent with the Federal Reserve’s 2% target. As a result, the 3-month annualized percentage change in core CPI fell to its lowest level since early 2021 (Chart 1). While the Fed’s preferred inflation metric, core PCE, sat at 2.6% in June, momentum in CPI inflation continues to indicate that inflation pressures will likely ease further moving forward.

This was also evidenced by the Producer Price Index (PPI) report released this week, which showed that upstream production costs decelerated in July. Annual growth in producer prices had been rising through the first half of the year, which contributed to the slowing in the disinflation progress as these costs were likely passed on to consumers. Therefore, the reversal in this trend in July, especially if sustained, would likely provide further relief to consumer price growth moving forward. Taken together the trends in the July reports for PPI and CPI inflation support the case for the Federal Reserve to begin to gradually reduce interest rates at their next meeting in September.

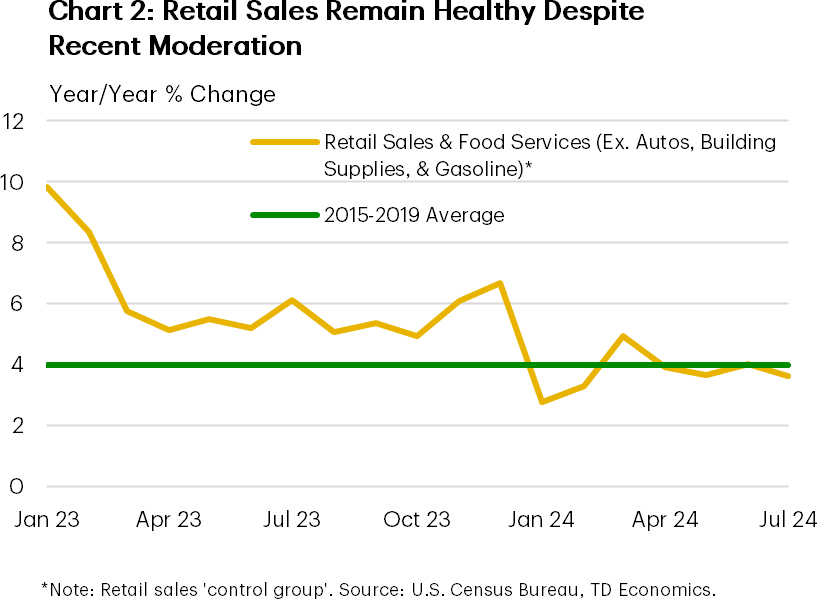

Fortunately, the moderation in price growth seen recently has not required a decline in consumer demand. As indicated by July retail sales, spending rose more than expected to start the second half of the year. This was in part driven by a rebound in auto sales after a cyber attack against a dealership software firm depressed sales in June. Still, sales in the ‘control group’, which excludes the more volatile spending categories, remained healthy in July (Chart 2). The economy has exited a period of exceptionally strong demand and maintained stable momentum, but the Federal Reserve will be cognizant of the balance of risks moving forward.

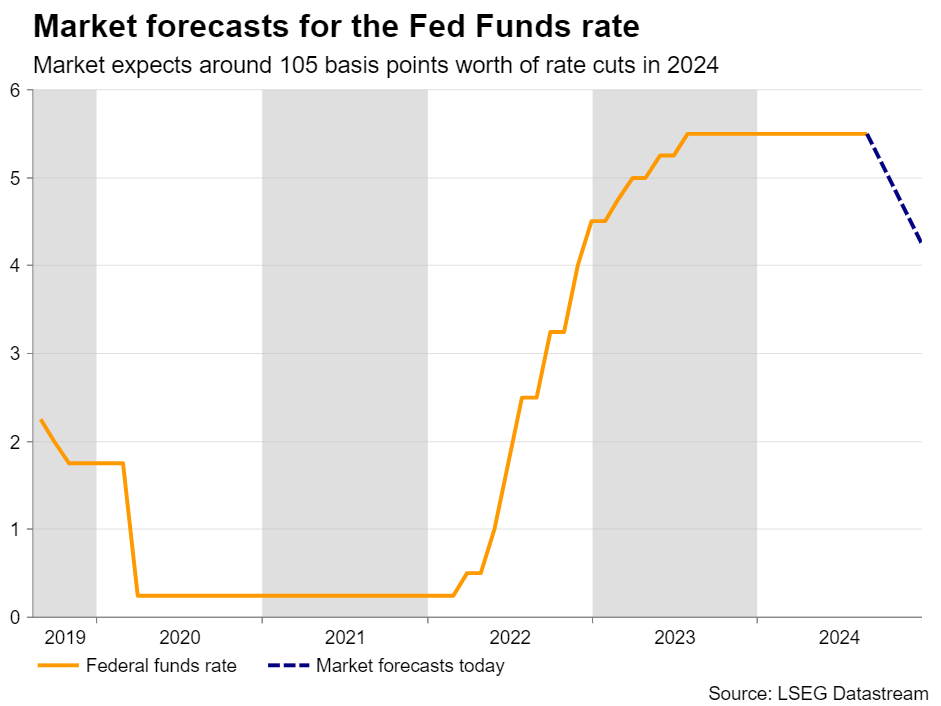

In the leadup to the Federal Reserve’s annual Jackson Hole Symposium next week, the slate of Fed speakers was relatively light this week. Governor Bowman, who is the only voting member of the FOMC who spoke this week, noted that upside risks to inflation remain and that caution would be warranted in considering future policy adjustments. Fed Presidents Bostic (Atlanta) and Musalem (St. Louis) broadly echoed these concerns, although both noted that interest rates would likely be lower in the second half of the year. Financial markets pared back their expectations for an outsized 50 basis-point (bps) cut in September this week, converging closer to our expectation for a 25bps cut, while they await further guidance from Chair Powell’s remarks scheduled for next Friday.

Canada – Housing Data Caps Eventful Week

This week’s data calendar was somewhat limited, but bad news for Canada on softwood lumber and rail shipments is likely to impact the international trade picture. Financial markets largely took their cues from developments south of the border, as a pair of generally soft U.S. inflation reports reinforced that Fed rate cuts were coming. This sentiment kept yields lower in the U.S. and Canada. Meanwhile, solid U.S. retail spending and labour market data injected some optimism about the economy, lifting equities in both countries.

Softwood lumber was back in the headlines. In the latest salvo in a longstanding dispute, the United States hiked its duty on Canadian softwood lumber entering its borders to 14.54% from 8.05%. This change will mark the first increase in some time, although is unlikely to meaningfully swing the overall export outlook given that lumber accounts for less than 2% of total Canadian international merchandise exports. Still, B.C. and New Brunswick (where lumber makes up a higher share of total exports) will feel an outsized impact. It’s also worth noting that that lumber shipments plunged in the wake of the 2017 Trump tariffs on softwood lumber, and volumes have yet to re-gain this lost ground.

Elsewhere, Canada’s two main railways began halting shipments of certain goods this week ahead of a potential lockout of over 9k engineers, conductors, and yard workers on August 22nd. There is still time to strike a deal, although a work stoppage wouldn’t be unfamiliar terrain, as there have been several in the past. A few common threads emerge when these periods are examined: GDP gets directly impacted by a decline in rail transportation, which is quickly recouped when the stoppage ends. Industries like manufacturing and agriculture feel an impact given these goods get shipped on rail lines, and the federal government can and will step in to legislate parties back to work.

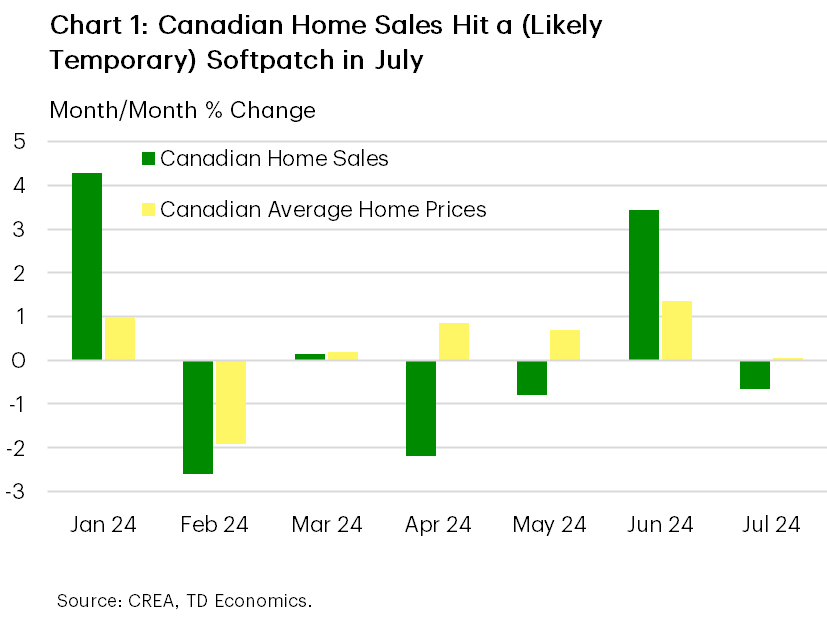

This week also offered a glimpse on how housing markets performed in July. As it turns out, last month was fairly subdued for resale activity, with sales dipping month-on-month and prices flat (Chart 1). This is despite another Bank of Canada rate cut in July, and a significant drop in bond yields during the month. Of course, even with these declines, interest rates were hovering around multi-year highs. Notably, July’s sales decline only gave back a small portion of June’s hefty gain, and nowhere is it said that home sales had to go up in a straight line after rates began dropping. We view July’s soft patch for housing as temporary, with firm gains in home sales and prices likely in the second half.

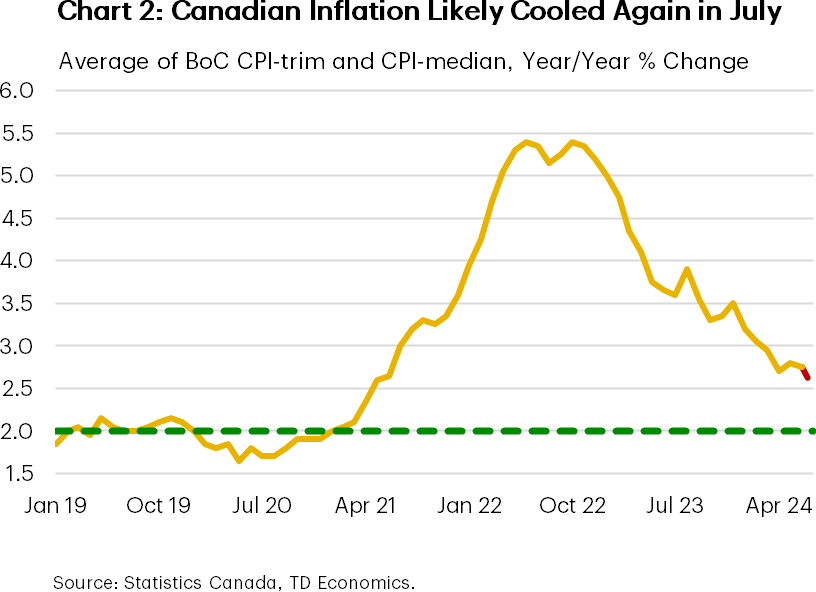

Next week’s data slate will be highlighted by the July inflation (CPI) report (Chart 2). We expect it will show continued progress towards the Bank of Canada’s 2% inflation target. Both headline and the average of the Bank’s preferred core measures could tick lower to around 2.5%, marking the softest reading since 2021. This would leave the door wide open for another Bank of Canada rate cut on September 4th.

Weekly Economic & Financial Commentary: Fishing in Jackson Hole for Clues About the Fed Rate Path

Summary

United States: Solid Activity Raises Questions About the Degree of Policy Easing

- Financial markets were volatile last week as they digested a troubling rise in the unemployment rate in July. The economic calendar this week was packed with solid data that helped quell recession jitters. Inflation continues its gradual descent, and small business optimism has trended higher amid cooler input price growth and steady consumer spending.

- Next week: Leading Economic Index (Mon.), Existing Home Sales (Thu.), New Home Sales (Fri.)

International: Steady U.K. Growth, Gradual Inflation Slowdown Mean Measured Central Bank Easing

- This week's U.K. data were mixed, which we believe keeps the Bank of England on track for a pause in September before resuming rate cuts in November. Q2 GDP grew a respectable 0.6% quarter-over-quarter, employment growth was solid and private sector regular pay growth slowed moderately. We think these factors will keep the Bank of England on hold next month, even as the July CPI showed services and core inflation decelerating a bit more than expected.

- Next week: Riksbank Policy Rate (Tue.), Canada CPI (Tue.), Eurozone PMIs (Thu.)

Interest Rate Watch: Fishing in Jackson Hole for Clues About the Fed Rate Path

- Chair Powell's highly-anticipated annual speech at Jackson Hole is likely to emphasize how much the inflation and labor market picture have changed in the year since the FOMC took the fed funds target range to 5.00%–5.25%, laying the groundwork for a rate cut at the FOMC's September meeting.

Topic of the Week: Lower Income Household Liquidity Crunch

- Amid a slowdown in the labor market, the staying power of the consumer is once again central to the economic outlook. However, consumer purchasing power may be dwindling for lower income households as they face an increasingly constrained availability of liquid assets.

Steady Inflation Shouldn’t Prevent Another BoC Rate Cut

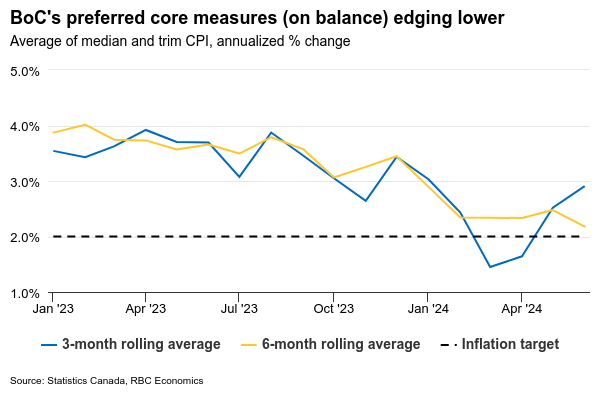

The easing of Canadian inflation pressures has slowed in recent months. On Tuesday, we expect annual price growth for both the headline and excluding food & energy measures to hold steady at 2.7% and 2.9%, respectively, in July. Shelter inflation still accounts for a disproportionate share of the increase, but that has been slowing with lower interest rates leading to a deceleration in mortgage interest costs (MIC). Consumer price index readings, excluding MIC, have been trending around the 2% inflation target since January.

The Bank of Canada is focused on where inflation is going rather than where it has just been. The closely watched three-month rolling average in the BoC’s preferred median and trim core inflation measures (designed to look through monthly volatility and provide a better gauge of underlying price growth trends) likely ticked higher for a second straight month as a meagre monthly increase in April drops out of that calculation. But earlier softer readings mean that annual growth rates in those measures should continue to edge lower. There was concern that initial interest rate cuts from the BoC could reignite rapid house price growth, but the response in housing markets to the 25 basis point cuts in June and July has been muted with signs that rent price growth has also begun to slow.

More importantly, a still weakening economic and labour market backdrop should suggest inflation pressures in Canada will further unwind. Per-capita gross domestic product is continuing to decline in Q2 this year. The unemployment rate is up almost a percentage point from a year ago in July as job openings fall, and wage growth is easing as a result. BoC Governor Tiff Macklem reiterated that confidence has increased that inflation will continue to drift lower even if “there could be setbacks along the way” after cutting rates in July. That means a low hurdle against the BoC cutting rates from levels that are still sharply above what it views as normal in the long run. We think the BoC will cut rates by 25 bps in each of the upcoming meetings in September and October.

Week ahead data watch:

Canadian retail sales likely dropped by 0.3% in June, driven by a price-related sales decline at gas stations. That was partially offset by higher auto sales that edged higher by 0.7% on a seasonally adjusted basis.

A potential rail strike or lockout at both of Canada’s major rail companies could begin as early as August 22 if an agreement isn’t reached with the union. Historically, there have not been disruptions from both major rail companies at the same time. Rail shipping accounts for about 0.5% of GDP. Trucking activity would rise in the event of a strike, but it cannot replace rail shipments, particularly for products like grains. Relatively high levels of inventories in the manufacturing sector could blunt the immediate downstream impact of transportation disruptions, but a shutdown of any significant length (e.g., more than a week) could have a substantial impact on the broader macroeconomy.

Week Ahead – Jackson Hole and PMIs Enter the Spotlight

- As recession fears ease, investors lock gaze on Jackson Hole

- Eurozone and UK PMIs to affect ECB and BoE expectations

- Canadian inflation could back third consecutive BoC cut

- Japan’s Nationwide CPI data also on the agenda

Jackson Hole to test overly dovish Fed cut bets

Following the unjustified panic triggered by the weaker-than-expected NFP report for July, investors have taken a calmer stance, thereafter, reevaluating their aggressive Fed rate cut bets as the incoming data suggested that the US economy is not faring as badly as initially feared.

That said, from penciling as many as 125bps worth of rate cuts by the end of the year at the start of last week, investors lifted their implied path only slightly. They are now expecting rates to be lowered by closer to 100bps, which remains an overly dovish bet as it means a reduction at each of the remaining decisions for 2024, including a 50bps cut.

The probability of a double cut at the upcoming meeting in September currently stands at about 25%, while such action is almost fully priced in for December. With that in mind, next week, investors will lock their gaze on the Fed’s Jackson Hole Economic Symposium, which will be held on August 22-24.

The theme will be “Reassessing the Effectiveness and Transmission of Monetary Policy”, suggesting that investors may have to digest a lot of commentary, not only from Fed Chair Powell and his colleagues, but from other major central bankers as well.

With inflation remaining close to 3%, it will be interesting to see whether Powell and other Fed members maintained their confidence about a downward trajectory in price pressures, and if so, how they are planning to move forward. Even if Powell repeats that the door to a September cut remains open, he is unlikely to satisfy those expecting hints about a double rate cut, which means that Treasury yields and the US dollar could still edge up.

Equity traders may be more eager to hear Powell’s take on the US economy, especially after the latest turmoil. Further reassurance that the risk of a recession is not elevated may allow Wall Street to march further north, even if expectations of very low borrowing costs are scaled back.

The minutes of the latest meeting are due to be released on Wednesday, but investors may prefer to pay more attention to the Jackson Hole symposium for more updated information and signals. The preliminary S&P Global PMIs for August on Thursday may also attract attention as investors remain eager to find out how the world’s largest economy is faring.

PMIs also on the front page of investors’ agenda

The preliminary S&P Global PMIs from the Eurozone and the UK are also due to be released that day.

Getting the ball rolling with the Eurozone, at its latest meeting, the ECB decided to keep interest rates unchanged, and although President Lagarde did not commit to a September cut, she sounded downbeat about the Eurozone’s growth outlook.

This allowed investors to nearly fully price in another 25bps reduction in September, and a set of downbeat PMIs may validate that view. That said, market participants may also dig into the minutes of the latest decision, due out the same day, for hints on how policymakers are planning to move forward.

In the UK, the Bank of England lowered interest rates on August 1 but signaled it will be ‘careful’ about cutting again. This week’s data revealed that the unemployment rate dropped to 4.2% from 4.4%, and that headline inflation rebounded somewhat to 2.2% y/y from 2.0%, even though the core rate slipped to 3.3% from 3.5%.

The data corroborated the BoE’s view, but still, there is around a 30% chance that policymakers will opt for a back-to-back reduction on September 19. For that probability to go higher, the PMIs may need to point to a significant deterioration in business activity.

Will CPI data halt the loonie’s recovery?

The Canadian CPI figures are scheduled to be released on Tuesday and the nation’s retail sales on Friday. The BoC cut interest rates by 25bps at each of the last two decisions, keeping the door open for more action down the line.

Investors are convinced that the Bank will continue cutting at each of the remaining decisions of the year and a further slowdown in inflation may add credence to that view, thereby weighing on the loonie at the time of the release.

However, currently, the oil-linked currency seems to be mainly driven by the rebound in oil prices, which is the result of supply concerns due to the increasing tensions in the Middle East, as well as easing demand worries as recession fears abate. Therefore, given that a dovish path is already priced in for the BoC, a further slowdown in inflation is unlikely to alter much the current outlook.

Japan’s CPI inflation also on tap

Finally, during the Asian session Friday, Japan releases its own Nationwide CPI numbers for July and according to the Tokyo prints for the month, headline inflation slowed but underlying prices continued to accelerate. If this is reflected on the national prints, then the probability for another BoJ hike by the end of the year may increase.

Nevertheless, even if this translates into a stronger yen, the latest relief in investors’ appetite is unlikely to allow the currency to stage a rally similar to that of the past few weeks. Interest rates in Japan remain very low compared to other major central banks, allowing some market participants to reuse the yen as a funding currency while increasing their risk exposures.

Weekly Focus – From Fear of Inflation to Fear of Slowdown

Over the summer, we have seen big moves in financial markets largely reflecting conflicting views of the US economy. During the first half of 2024, markets were often driven by concerns about persistently high US inflation and the implication that it would be difficult for the Fed to reduce interest rates. However, the last three inflation prints now show core inflation in line with or below the 2% annual target, making it much easier for the Fed to cut (although some concerns about service prices remain). Attention has instead shifted to whether there is not only room but also a need for rate cuts to support the economy. Not least a jump in the unemployment rate to 4.3% in July triggered fears that the US is nearing or already in recession, and market pricing shifted to include quite aggressive rate cuts this year. Earlier this year equity markets reacted very positively to prospects of rate cuts, but in early August, that was overshadowed by a negative reaction to fears of weakness in the economy.

Over the last two weeks, markets have calmed down and expectations for rate cuts have partially reversed. Even though unemployment and other indicators of slack in the US labour market have increased, many other indicators still point to robust economic growth, such as this week's retail sales data for July. Higher unemployment can also be largely explained by growth in the labour force due to immigration rather than by weak demand, which makes it less of an obvious trigger for recession dynamics. We agree that low inflation has cleared the path for "normalisation" of interest rates from current high levels and for the Fed to consider the labour market and not only inflation, but the process of rate cuts is still likely to be gradual and cautious, with large reactions in interest rate markets to economic news.

As often before, lower bond yields in the US have been reflected in Europe. However, euro area inflation is still clearly above target, and we have not really had signs of cooling labour markets. A lot depends on data, not least upcoming wage data for Q2, but it seems to us that the ECB is more likely than not to wait before cutting rates further.

The recovery in global manufacturing seems to have stalled somewhat, which is also part of the backdrop for increased economic concerns in markets. We continue to see signs of weak growth in China where it seems that initiatives to stimulate demand have not been very successful so far, and more is likely to be needed.

Japan delivered a surprisingly early rate hike in July, and we have seen a strong rally in the JPY in connection with the market turbulence over the last month. After three disappointing quarters, GDP increased 0.8% in Q2, and further rate hikes are likely.

We will get PMI data for most major economies in the coming week. If we see some reversal of weak indicators for manufacturing that we saw in July, that could further dampen recession fears in the market. It is also time for the annual Jackson Hole Economic Policy Symposium which has often been used by the Fed (and occasionally the ECB) in the past to influence market expectations.

XAUUSD: Formation of Bullish Pattern: Signs of Trend Continuation

- Bearish Scenario: Sell positions below 2470 with TP1: 2463, TP2: 2460, TP3: 2456 intraday, with a stop loss above 2473 or at least 1% of the account capital.

- Bullish Scenario: Buy positions after a pullback above 2460 with TP1: 2470, TP2: 2480, and TP3: 2490 in extension. Stop loss below 2450 or at least 1% of the account capital. Apply Trailing Stop.

Technical Analysis

XAUUSD, Daily

On this timeframe, price consolidation is observed below the July resistance and current all-time high, forming a bullish cup and handle structure. This suggests a continuation of buying pressure in the short term with profit targets at 2500, 2600, and 2609 at 100%.

XAUUSD, H1

Supply Zones (Sell): 2473

Demand Zones (Buy): 2455.18, 2428.49, and 2423.80

The price shows signs of recovery after breaking local resistances at 2460 and 2470, suggesting a continuation of the macro bullish trend with a target at 2500 intraday and the potential for new all-time highs in the short term.

In this context, the breakout of a previous session’s resistance activates a corrective scenario, with targets at 2462, 2460, 2458, and 2456 in extension.

All these levels represent demand zones that could trigger buys towards 2473, 2480, 2483, and the average daily bullish range at 2492.81.

*Uncovered POC: POC = Point of Control: This is the level or zone where the highest volume concentration occurred. If a downward move follows this level, it is considered a sell zone and forms a resistance area. Conversely, if an upward move follows it, it is considered a buy zone, usually located at lows, forming support zones.