Sample Category Title

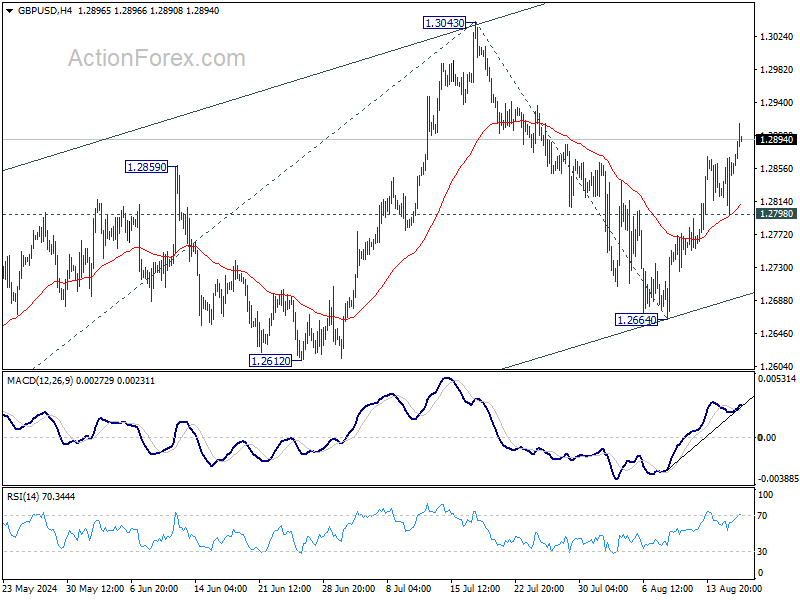

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2811; (P) 1.2841; (R1) 1.2884; More...

Intraday bias in GBP/USD remains on the upside for retesting 1.3043 high. Decisive break there will resume whole rally from 1.2998 to 61.8% projection of 1.2298 to 1.3043 from 1.2664 at 1.3124, which is close to 1.3141 high. On the downside, however, break of 1.2798 support will turn bias back to the downside for 1.2664 support instead.

In the bigger picture, as long as 1.3141 resistance holds (2023 high), medium term corrective pattern from there could still extend with another falling leg. But even in that case, downside should be contained by 1.2036/2298 support zone. Meanwhile, decisive break of 1.3141 will confirm resumption of whole up trend from 1.0351 (2022 low).

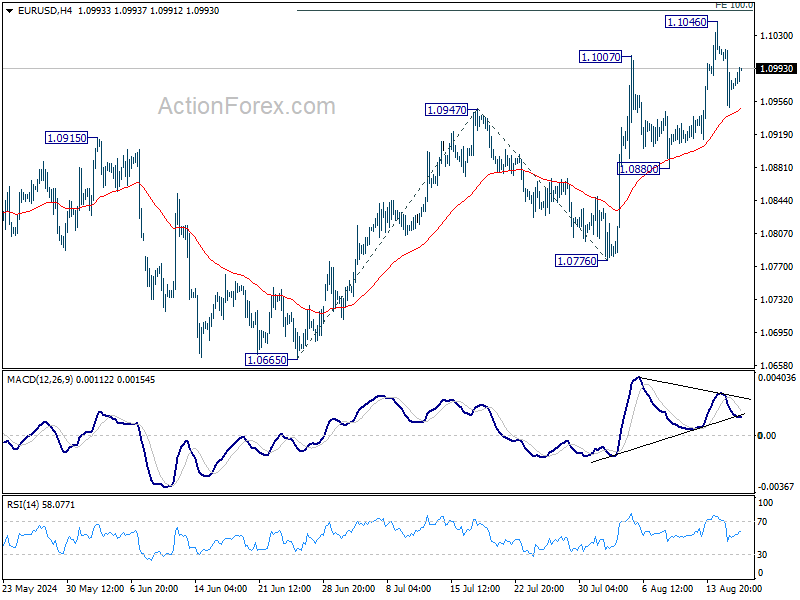

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0942; (P) 1.0980; (R1) 1.1010; More.....

EUR/USD is staying in consolidation below 1.1046 and intraday bias remains neutral. Another rally is in favor as long as 1.0880 support holds. Firm break of 100% projection of 1.0665 to 1.0947 from 1.0776 at 1.1058 could prompt upside acceleration through 1.1138 resistance to 161.8% projection at 1.1232. However, considering bearish divergence condition in 4H MACD, break of 1.0880 will suggest near term reversal and turn bias to the downside for 1.0776 support and below.

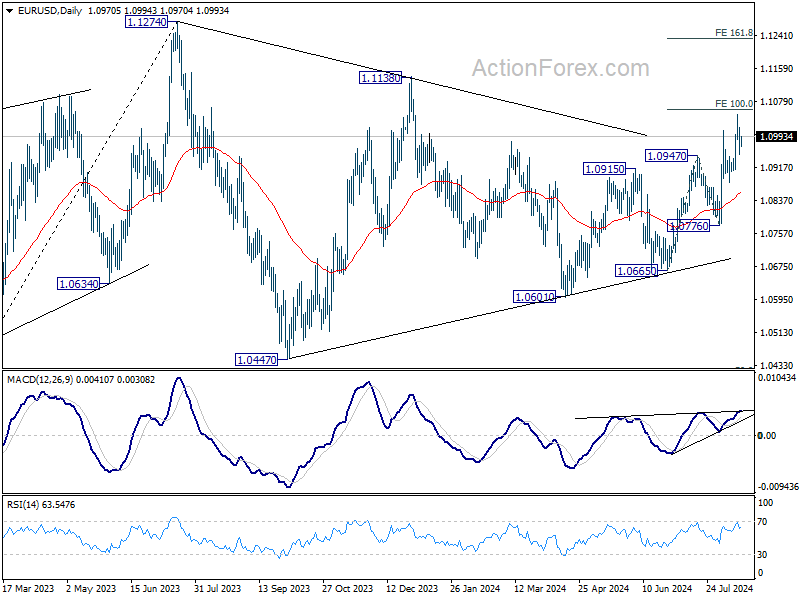

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's could still extend. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0776 support will extend the correction with another falling leg back towards 1.0447 support.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8666; (P) 0.8707; (R1) 0.8768; More….

Intraday bias in USD/CHF is turned neutral first as it retreated after hitting 0.8747. On the upside, sustained break of 38.2% retracement of 0.9223 to 0.8431 at 0.8734 will extend the rebound from 0.8431 to 61.8% retracement at 0.8920, even as a corrective move. On the downside, break of 0.8616 support will indicate rejection by 0.8734, and turn bias back to the downside for retesting 0.8431 low.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

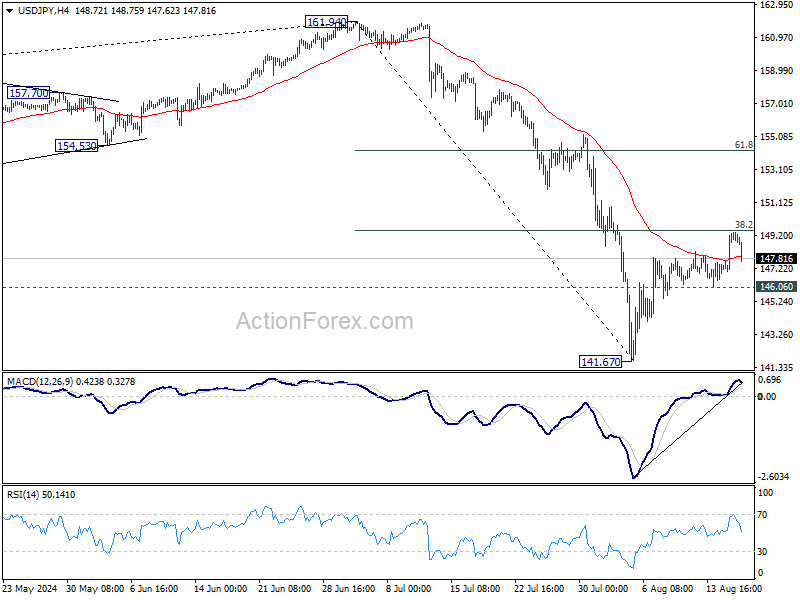

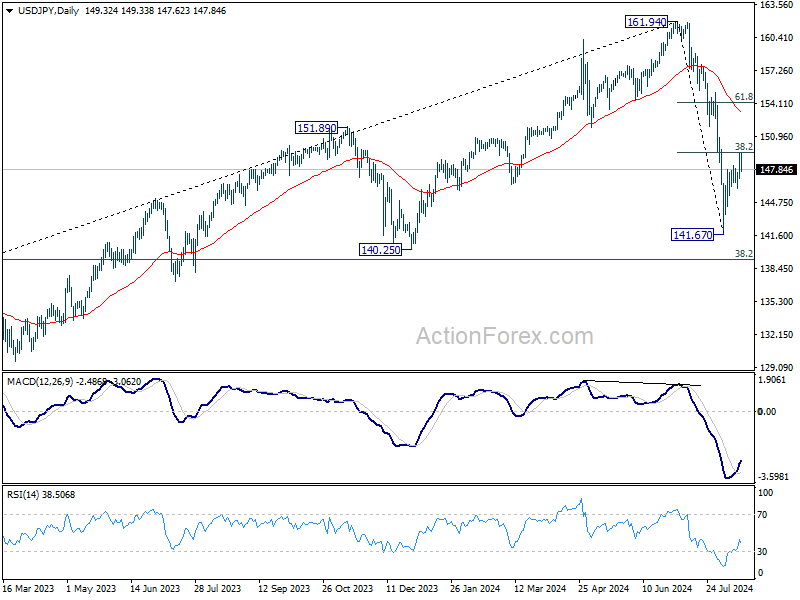

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.76; (P) 148.58; (R1) 150.09; More...

Intraday bias in USD/JPY is turned neutral as it retreated after failing to break through 38.2% retracement of 161.94 to 141.67 at 149.41. On the downside, break of 146.06 minor support will suggest rejection by 149.91, and turn intraday bias back to the downside for retesting 141.67 low instead. On the upside, sustained break of 149.41 will extend the rebound to 61.8% retracement at 154.19, as the second leg of the corrective pattern from 161.94.

In the bigger picture, fall from 161.94 medium term is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.77) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

Yen and Swiss Franc Recover as Benchmark Yields Ease

As the US session gets underway, both Yen and Swiss Franc are beginning to recover, aided by the slight pullback in benchmark Treasury yields in the US and Europe. This recovery comes after a tough week for the two safe-haven currencies, which have been the worst performers amid broad risk-on sentiment. Despite today's gains, Yen and Swiss Franc still face an uphill battle to reverse their losses and end the week on a positive note.

British Pound, on the other hand, continues to show strength, particularly against Dollar and Euro. Sterling was supported by data showing rebound in retail sales, even that slightly missed expectations. Overall, this week's slew of data didn't add too much evidence to convince BoE to continue with another rate cut at next meeting. Meanwhile, commodity currencies like the Australian and Canadian Dollars have had a more subdued performance.

The final positions for these currencies as the week closes may be influenced by the upcoming University of Michigan consumer sentiment and inflation expectation data, and their impact of risk sentiment.

In Europe, at the time of writing, FTSE is down -0.62%. DAX is up 0.33%. CAC is flat. UK 10-year yield is down -0.0119 at 3.914. Germany 10-year yield is down -0.036 at 2.229. Earlier in Asia, Nikkei surged 3.64%. Hong Kong HSI rose 1.88%. China Shanghai SSE rose 0.07%. Singapore Strait Times rose 1.12%. Japan 10-year JGB yield rose 0.0372 to 0.875.

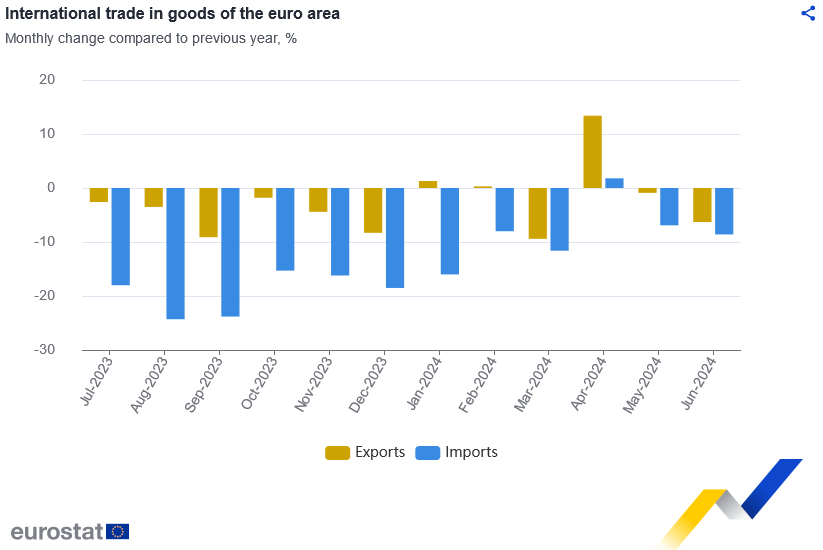

Eurozone goods exports fall -6.3% yoy in Jun, goods imports down -8.6% yoy

Eurozone goods exports fell -6.3% yoy to EUR 236.7B in June. Goods imports fall -8.6% yoy to EUR 214.3B. Trade balance showed a EUR 22.3B surplus. Intra-Eurozone trade fell -8.5% yoy to EUR 214.5B.

In seasonally adjusted term, goods exports fell -0.2% mom to EUR 236.2B. Goods imports fell -2.4% mom to EUR 218.7B. Trade surplus widened from EUR 12.4B in the prior month to EUR 17.5B, larger than expectation of EUR 14.5B. Intra-Eurozone trade rose 0.4% mom to EUR 210.7B.

UK retail sales rises 0.5% mom in Jul, vs exp 0.6% mom

UK retail sales volumes rose by 0.5% mom in July, slightly below market expectations of 0.6% increase. On a broader scale, sales volumes in the three months leading up to July saw a 1.1% rise compared to the previous three months ending in April.

Breaking down the data, non-food stores—which include department, clothing, household, and other non-food stores—saw a notable 1.4% increase in sales volumes. Non-store retail sales, which encompass online and other forms of retail not conducted in physical stores, rose by 0.7%, driven primarily by a rebound in retailers other than mail order services. However, the overall growth was tempered by a -1.9% decline in automotive fuel sales volumes.

RBA's Bullock dismisses near-term rate cut expectations

In her remarks to the House of Representatives' economics committee, RBA Governor Michele Bullock emphasized the careful balancing act in managing inflation while minimizing harm to the labor market. Bullock reiterated that the Board believes current monetary policy is "sufficiently restrictive" to bring inflation down over a reasonable timeframe without causing undue damage to employment.

Despite financial markets anticipating a rate cut by the end of the year, Bullock was clear in her message that it is "premature to be thinking about rate cuts" at this stage. She pointed out that inflation remains too high and, in underlying terms, is not expected to fall back within the target range until the end of next year.

While acknowledging that economic circumstances could change, Bullock firmly stated that, based on the current outlook, the Board "does not expect that it will be in a position to cut rates in the near term."

RBNZ confident in inflation outlook, emphasizes measured approach to further rate cuts

In a speech today, RBNZ Governor Adrian Orr expressed a "very strong level of confidence" that forward indicators are pointing to a return to low and stable inflation, within the target range of 1% to 3%. Orr emphasized the importance of keeping inflation expectations and pricing intentions "anchored" as the central bank continues to monitor economic conditions.

Assistant Governor Karen Silk, speaking in a separate interview, noted that RBNZ is observing a continued decline in price and wage-setting behaviors. Silk mentioned that if this adjustment occurs more rapidly than anticipated, it could open the door for the central bank to consider a different, potentially faster path for rate cuts.

Earlier this week, RBNZ lowered the OCR by 25 bps to 5.25% and projected that it would fall below 4% by the end of 2025. Silk reiterated that RBNZ is taking a "measured approach" to policy loosening and remains committed to a data-dependent strategy.

New Zealand BNZ manufacturing rises to 44, 17th month of contraction

New Zealand's manufacturing sector showed a slight improvement in July, with the BusinessNZ Performance of Manufacturing Index rising from 41.2 to 44.0. Despite this rebound, the sector remains deeply entrenched in contraction, marking its 17th consecutive month below the expansion threshold. The current level is still significantly below the long-term average of 52.6.

Breaking down the data, production saw an uptick, increasing from 35.7 to 43.4, while new orders also rose, moving from 39.0 to 42.5. However, employment in the sector continued to decline, slipping from 44.0 to 43.1. Finished stocks decreased from 47.7 to 46.5, and deliveries fell slightly from 44.8 to 44.3.

Despite the relative improvement in activity, the proportion of negative comments from respondents remained high, though it eased slightly to 71.1% in July from 76.3% in June. Businesses cited ongoing issues such as a lack of orders, customers, and sales, which have been persistent concerns in recent months.

BNZ's Senior Economist Doug Steel commented that "manufacturing activity will turn when the broader economy turns." He added that easing monetary conditions, including a lower OCR, could help stimulate a general pick-up in sales, but emphasized that this recovery would take time.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.76; (P) 148.58; (R1) 150.09; More...

Intraday bias in USD/JPY is turned neutral as it retreated after failing to break through 38.2% retracement of 161.94 to 141.67 at 149.41. On the downside, break of 146.06 minor support will suggest rejection by 149.91, and turn intraday bias back to the downside for retesting 141.67 low instead. On the upside, sustained break of 149.41 will extend the rebound to 61.8% retracement at 154.19, as the second leg of the corrective pattern from 161.94.

In the bigger picture, fall from 161.94 medium term is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.77) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Jul | 44 | 41.1 | 41.2 | |

| 22:45 | NZD | PPI Input Q/Q Q2 | 1.40% | 0.50% | 0.70% | |

| 22:45 | NZD | PPI Output Q/Q Q2 | 1.10% | 0.60% | 0.90% | 0.80% |

| 04:30 | JPY | Tertiary Industry Index M/M Jun | -1.30% | 0.30% | -0.40% | 0.60% |

| 06:00 | GBP | Retail Sales M/M Jul | 0.50% | 0.60% | -1.20% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jun | 17.5B | 14.5B | 12.3B | 12.4B |

| 12:15 | CAD | Housing Starts Jul | 280K | 245K | 242K | |

| 12:30 | CAD | Manufacturing Sales M/M Jun | -2.10% | -2.50% | 0.40% | |

| 12:30 | USD | Building Permits Jul | 1.40M | 1.44M | 1.45M | |

| 12:30 | USD | Housing Starts Jul | 1.24M | 1.34M | 1.35M | |

| 14:00 | USD | Michigan Consumer Sentiment Index Aug P | 67.3 | 66.4 |

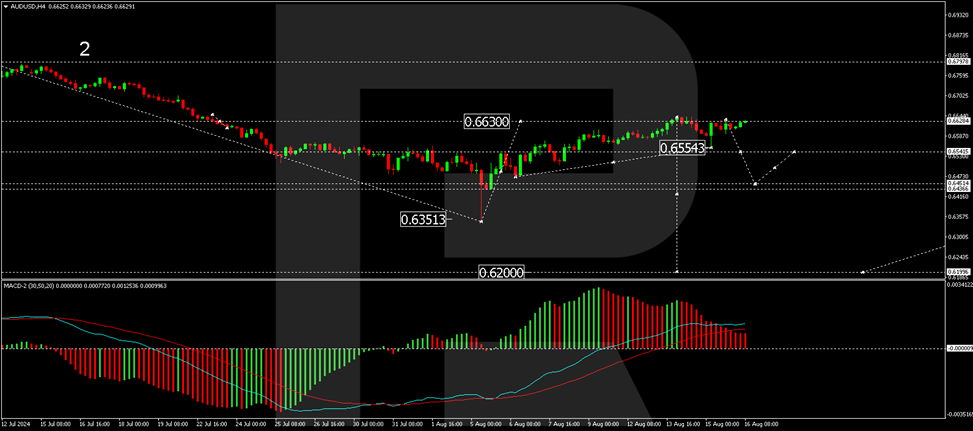

AUD/USD Climbs as RBA Maintains Firm Stance on Interest Rates

The Australian dollar (AUD) is witnessing a rise against the US dollar (USD) for the second consecutive day, reaching 0.6629. This upward movement is bolstered by the Reserve Bank of Australia's (RBA) current policy stance. RBA Governor Michelle Bullock emphasized today that discussions on interest rate cuts are premature despite some easing in inflationary pressures.

Inflation, according to Governor Bullock, remains uncomfortably high, with expectations for it to settle within the target range of 2-3% only towards the end of next year. This viewpoint underpinned the RBA's decision last week to maintain the official cash rate at 4.35%, marking the sixth consecutive hold. The RBA cites ongoing economic stability and persistent inflation risks as key reasons for their cautious approach.

This stance starkly contrasts with other major central banks, including the Reserve Bank of New Zealand (RBNZ), which have been more open to adjusting rates. However, the RBA's consistent and factual communication strategy has minimized speculative market reactions, contributing to a more stable forex forecast for the AUD.

Technical analysis of AUD/USD

The AUD/USD pair has reached a peak at 0.6640 and is now showing signs of consolidating below this level. Should the pair break downwards from this consolidation, a decline to 0.6450 could be anticipated. Following this potential drop, a rebound to 0.6545 for a retest from below might occur before a further descent towards 0.6200. This bearish outlook is supported by the MACD indicator, which shows the signal line retreating from highs and gearing towards a downturn.

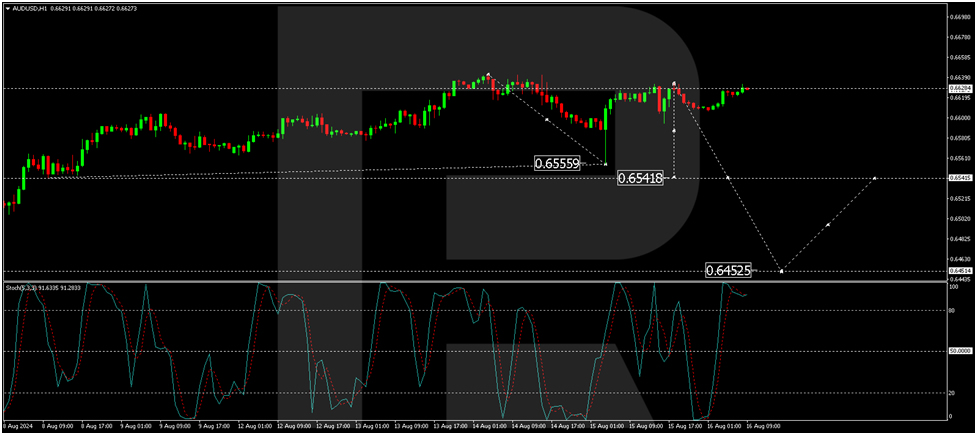

On the hourly chart, after a decline to 0.6555, the AUD/USD pair corrected upwards to 0.6628. A consolidation below this level is expected, which could lead to a new downward wave aiming for 0.6540. This bearish prediction aligns with the Stochastic oscillator readings, where the signal line is poised to move from above 80 downwards to 20, indicating potential selling pressure ahead.

Euro Edges Higher, US Dollar Under Pressure

The euro has edged higher on Friday. In the European session, EUR/USD is trading at 1.0994, up 0.21% on the day at the time of writing.

The US dollar is under pressure and the euro rose as much as 1.2% this week before paring about half of those gains. On Wednesday, the euro hit 1.1047, its highest level against the US dollar this year.

Investors are showing greater pessimism about economic conditions. Eurozone investor sentiment fell to 17.9 in August, down sharply from 43.7 a month earlier. This was the lowest reading since November 2023. Germany, the largest economy in the eurozone, showed a similar trend. There are significant uncertainties about the eurozone and German economies and these worries increased due to the recent turmoil in the global stock markets.

Solid US data eases market nerves

Exactly two weeks ago, the US jobs report was weaker than expected, triggering a meltdown across global stock markets. Investors panicked that the US economy was hurtling towards a recession but the markets have recovered courtesy of solid US numbers this week.

US inflation dipped to 2.9% y/y in July, down a notch from 3% a month earlier which was also the market estimate. Retail sales jumped 1% m/m, bouncing back from -0.2% in June and breezing past the market estimate of 0.4%. As well, unemployment claims were lower than the market estimate for a second straight week.

The rout in the financial markets raised expectations for a half-point cut from the Federal Reserve to as high as 60%, but this has fallen to 30% since the retail sales report (a quarter-point has been priced in at 70%). The Fed meets next on September 18 and a rate cut is virtually guaranteed but the size of the cut remains an open question.

EUR/USD Technical

- EUR/USD is testing resistance at 1.0980. Above, there is resistance at 1.1010

- 1.0942 and 1.0912 are the next support levels

New Zealand Dollar Stems Slide

The New Zealand dollar has rebounded on Friday after a 1.4% slide over the past two days. NZD/USD is trading at 0.6017, up 0.70% in the European session at the time of writing.

Solid US numbers raises risk appetite

Exactly two weeks ago, a soft employment report out of the US panicked investors and caused a meltdown across global stock markets. The turmoil was brief as the stock markets have rallied. The fears that the US economy was hurtling towards a recession have eased this week, as US CPI was within expectations and US retail sales was much higher than the forecast.

US inflation dipped to 2.9% y/y in July, down a notch from 3% a month earlier which was also the market estimate. Retail sales jumped 1% m/m, bouncing back from -0.2% in June and breezing past the market estimate of 0.4%. As well, unemployment claims were lower than the market estimate for a second straight week.

The rout in the financial markets raised expectations for a half-point cut from the Fed to as high as 60%, but this has fallen to 30% since the retail sales report (a quarter-point has been priced in at 70%).

The volatility in the stock markets has been driven by the strength of the US numbers. This week’s positive data has not allayed investor fears completely and if upcoming key data is weaker than expected, we could see the financial markets react negatively.

The US dollar is showing weakness as the market turmoil has eased. Risk appetite has returned, which has given the New Zealand dollar a strong boost today.

NZD/USD Technical

- There is resistance at 0.6073 and 0.6146

- 0.5961 and 0.5888 are providing support

Eurozone goods exports fall -6.3% yoy in Jun, goods imports down -8.6% yoy

Eurozone goods exports fell -6.3% yoy to EUR 236.7B in June. Goods imports fall -8.6% yoy to EUR 214.3B. Trade balance showed a EUR 22.3B surplus. Intra-Eurozone trade fell -8.5% yoy to EUR 214.5B.

In seasonally adjusted term, goods exports fell -0.2% mom to EUR 236.2B. Goods imports fell -2.4% mom to EUR 218.7B. Trade surplus widened from EUR 12.4B in the prior month to EUR 17.5B, larger than expectation of EUR 14.5B. Intra-Eurozone trade rose 0.4% mom to EUR 210.7B.

GBP/USD Extends Gains as Retail Sales Bounce Back

The British pound has extended its gains on Friday. GBP/USD is trading at 1.2887 in the European session, up 0.31% on the day at the time of writing. It has been a winning week for the pound, which has climbed 1%.

UK retail sales jump in July

There was more good news from the UK economy as retail sales rebounded in July by 0.5% m/m, after a revised decline of 0.9% in June and in line with the market estimate. Annually, GDP surged 1.4%, compared to -0.8% in June and matching the market estimate. The pound has moved higher in response to the positive retail sales data.

The bounce in retail sales reflects summer discounts and purchases related to the Euro 2024 and the Paris Olympics, such as apparel. As well, with inflation finally under control and running close to 2%, consumers are responding by opening up their wallets and purses. The positive retail sales report follows yesterday’s solid GDP release. The UK economy recorded rose 0.6% in Q2, a second straight quarter of growth.

The economy is showing some strength in the second quarter but that may not have much effect on the Bank of England’s rate path. The increase in growth may not be sustainable and BoE policy makers have said that they are more focused on inflation, particularly service inflation, which remains much higher than the BoE’s 2% target. The markets are expecting further cutting before the end of the year and have priced in a rate reduction at the November meeting.

GBP/USD Technical

- GBP/USD is testing resistance at 1.2884. Above, there is resistance at 1.2914

- 1.2841 and 1.2811 are the next support levels