Sample Category Title

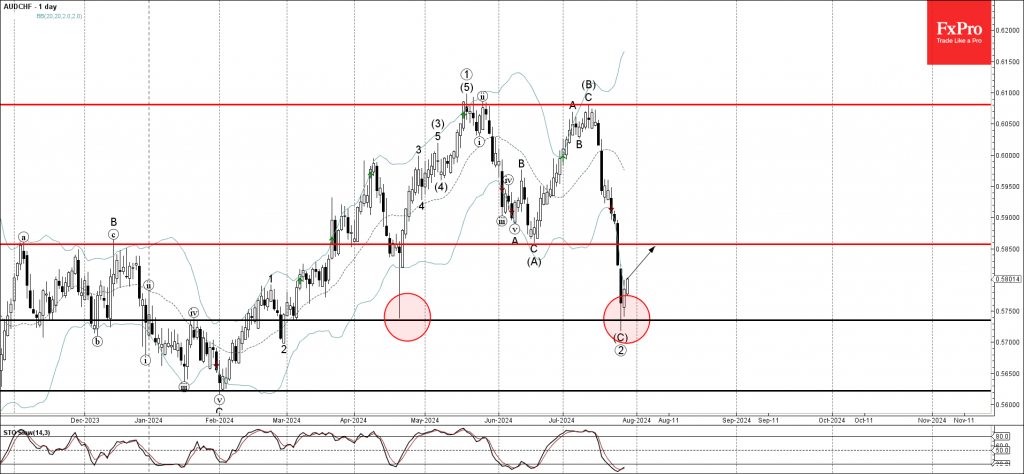

AUDCHF Wave Analysis

- AUDCHF reversed from key support level 0.5735

- Likely to rise to resistance level 0.5850

AUDCHF currency pair recently reversed up with the daily Japanese candlestick Piercing Line from the key support level 0.5735 (the previous monthly low from April, as can be seen below).

The support level 0.5735 was strengthened by the nearby lower daily Bollinger Band.

Given the strength of the support level 0.5735 and the still oversold reading on the daily Stochastic indicator, AUDCHF currency pair can be expected to rise further to the next resistance level 0.5850.

Central Bank Meetings This Week Are Reason for Volatility

The week ahead will be packed with significant economic events, so the market behaviour could turn into quite a bumpy ride this week.

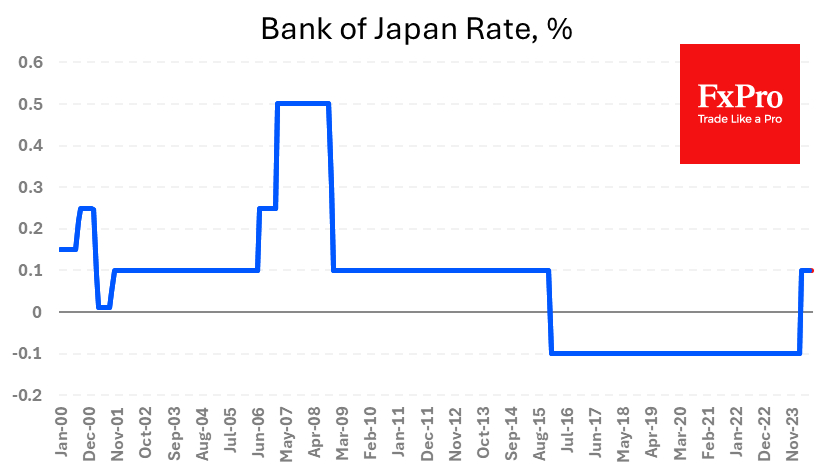

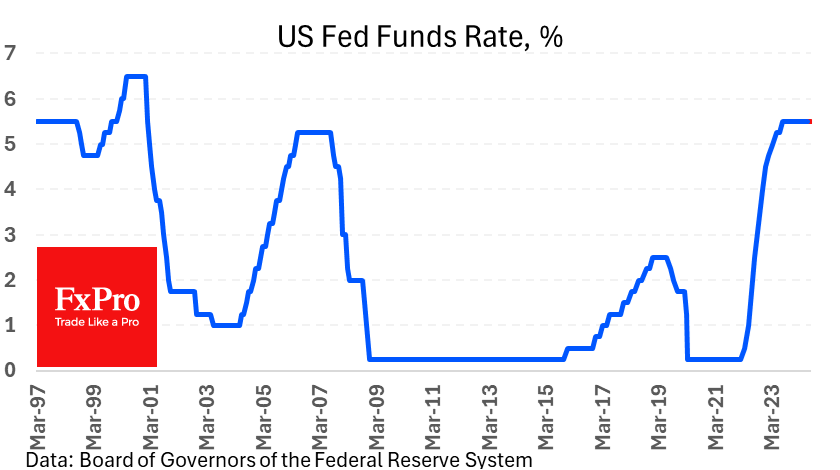

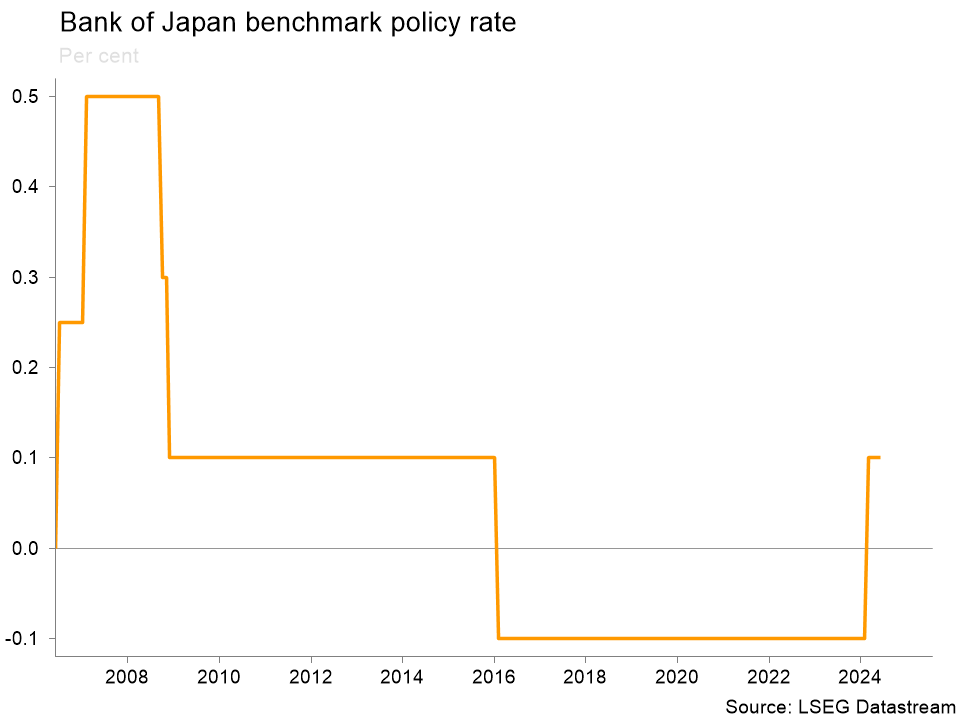

On Wednesday morning, the Bank of Japan will announce its rate decision and the parameters of its balance sheet asset purchase programme. On average, the purchases are expected to be halved, but the key rate is not expected to change. At the same time, the central bank may go for a second rate hike to 0.25% after the March hike from -0.1% to +0.1%. Sharper cuts in balance sheet buying are not ruled out. This is a potentially positive turn of events for the yen. In previous months, the Bank of Japan has been criticised for its loose policy weakening the yen, leading to currency intervention. Tightening monetary policy is a less costly way to support the currency without selling off international reserves.

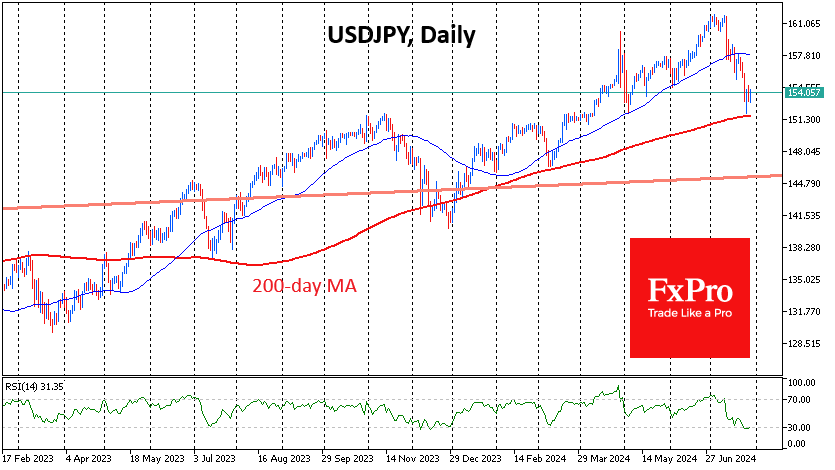

USDJPY retreated below 152 last week, approaching the 200-day average and the area of the highs of October 2022 and November 2023. The Bank of Japan’s actions will determine whether the former resistance has become support or if the Yen bears will finally have their backbone broken.

No actual policy changes are expected from Wednesday night’s Fed rate decision. Still, observers will dive into studying the accompanying commentary changes to gauge the chances of a rate cut in September and the number of those cuts before the end of the year. Rate futures give a 10% chance that the rate will be 50 basis points lower in September than it is now, which is excessive.

Slightly less excessive is the market’s estimate of a 63.5% chance of 3 or more rate cuts before the end of the year. Approaching that probability to 100% or moving to expectations of two cuts promises to be a major field for Fed “expectations management”. A shift to soft sentiment is a market risk: bearish for the dollar and bullish for equities. A surprise tighter rate approach has the potential to set off a spiral of dollar gains and a sell-off in risk assets.

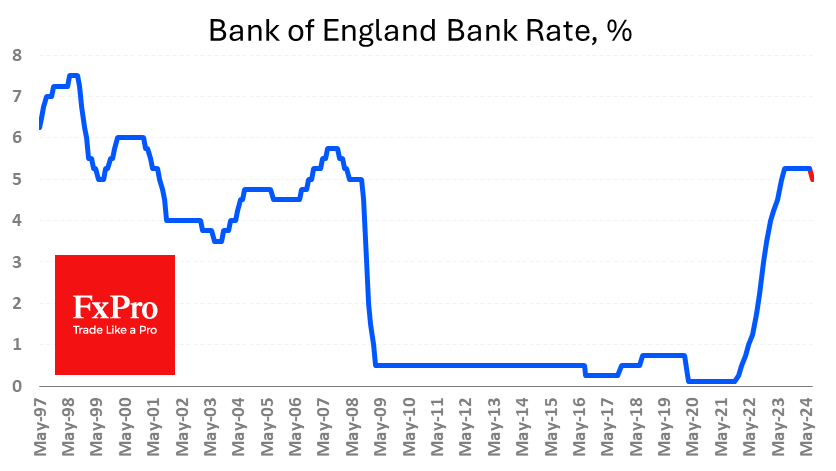

On Thursday, all eyes are on the Bank of England rate decision. The chances of a cut are barely over 50%. If it stays this way until Thursday, any outcome will cause a surge of volatility in the markets of England and pairs with the pound. GBPUSD has added over 3% since the start of the month to 17 July but has squandered half of that gain since then. This could well be a tactical retreat before a fresh attempt to break 1.30, which failed in mid-July. Bank of England’s softness has the potential to erase last month’s gains in GBPUSD rather quickly, pushing the pair back to 1.26.

Will BoJ Raise Rates at this Policy Meeting?

- BoJ may shake the market with a rate hike

- The bank plans to unveil a strategy to roughly halve bond

- Yen recoups some losses with notable bullish correction

- Decision is due on Wednesday at 03:00 GMT

Will BoJ hike rates on Wednesday?

At its next meeting, the Bank of Japan (BoJ), one of the most important central banks in the world, will make an extremely significant decision about interest rates. The world economy is already having a difficult time due to inflation and other economic issues. The Bank of Japan's decision will have a significant impact on the world's financial markets and the Japanese economy.

Along with the rate hike, the BoJ is also going to announce a plan to reduce its usual bond purchases by half over the next few years. Even with these changes, the Bank of Japan has promised to keep buying long-term government bonds as needed and to keep conditions accommodative for now. This shows that the BoJ is cautiously positive about the economy and is still determined to support growth and stability. Bets on a July move have gone up, and a 10-basis-point-hike is now priced in at a 63% chance. So, if the bank leaves rates unchanged, there's a lot of room for disappointment.

Ueda comments, inflation, and yen

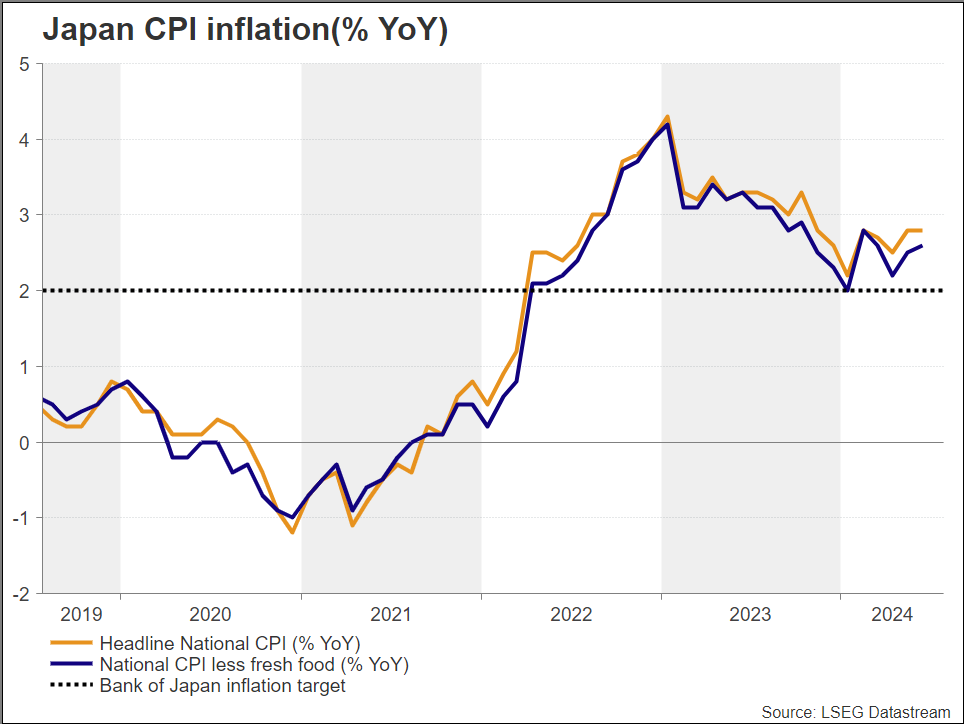

But Kazuo Ueda, the governor of the Bank of Japan, said that inflation expectations are still some way off from hitting 2%. He also said that the BoJ will keep its stance loose until the underlying price trend hits that level. He added that the BoJ may raise rates further if prices rise beyond expectations. This demonstrates that the Bank of Japan is committed to its inflation goal and is willing to make changes to monetary policy as needed to achieve it.

This week’s interest rate decisions are not only significant for the BoJ but also for other major central banks like the Bank of England (BOE) and the Federal Reserve (Fed). Around the world, investors and lawmakers will be paying close attention to these events and what they might mean for global economic trends.

In terms of the Japanese economy, the yearly inflation rate stayed at 2.8% in June, the same as the previous month. It was the highest level since February. Japan's economy was having a hard time at the beginning of 2024, but a small improvement may be on the way thanks to higher wages and more spending by consumers. The real GDP dropped 0.5% from the previous quarter to the first quarter of 2024. It also fell 1.3% from its peak in the second quarter of 2023. In three of the last four quarters, household spending in the US decreased. The economy seems to be at a turning point, which is positive news. Stronger wage growth and more moderate inflation are expected to boost consumer spending. In addition, a weak currency is likely to help exports grow. Even though all these conditions should make the economy better, growth is only expected to be moderate.

Finally, the upcoming interest rate decision by the Bank of Japan and the current state of the Japanese economy present a complex mix of opportunities and challenges. The Bank of Japan's change in monetary policy shows that they have faith in the economy, but ongoing inflation and other economic headwinds show how important it is to handle policy carefully. The BoJ and other central banks will have to deal with these challenges, and the choices they make will have a big impact on the world economy in the coming months.

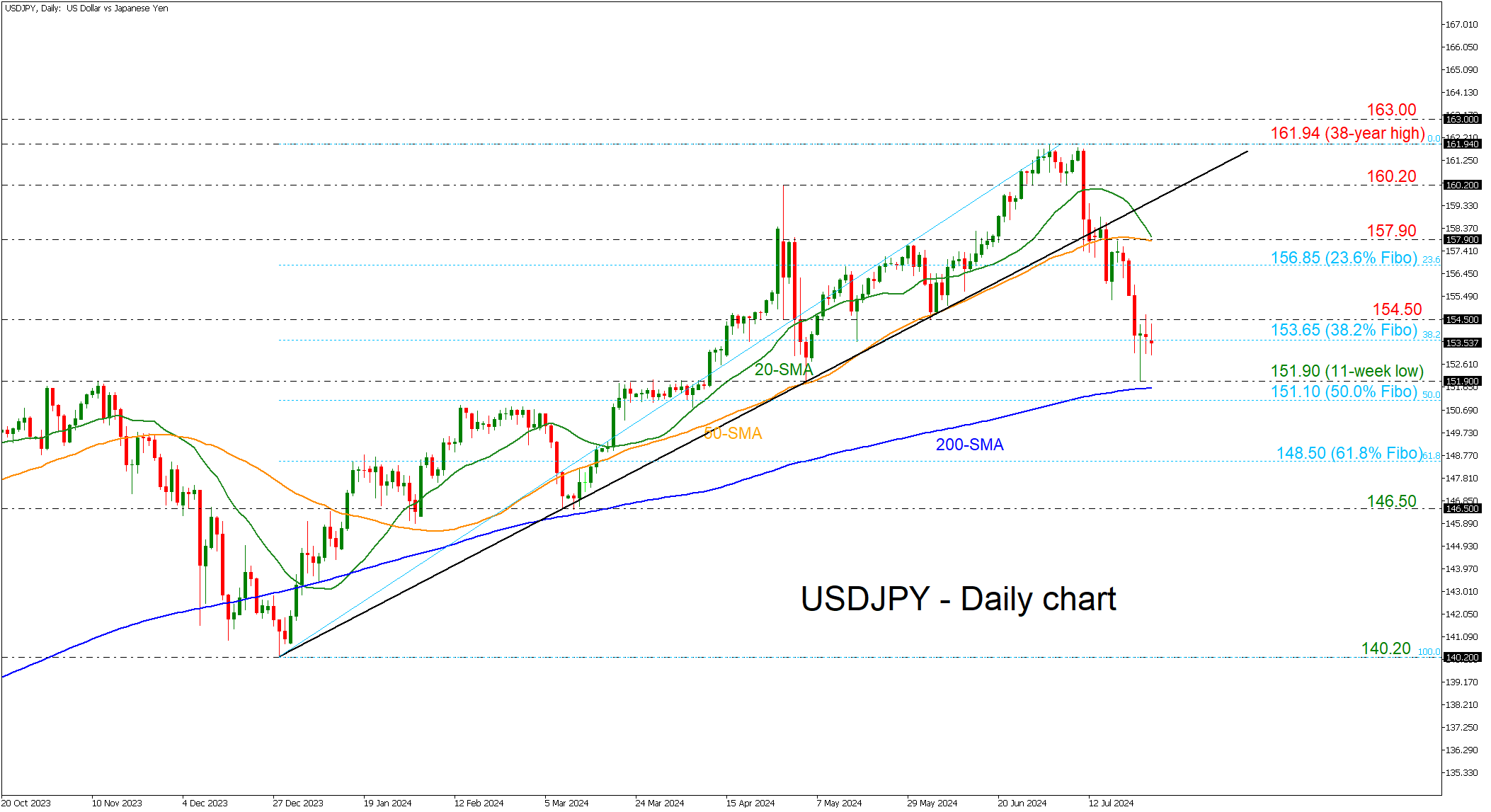

USDJPY moves with weak momentum

From a technical perspective, USDJPY found strong support near the eleven-week low, slightly beneath the 152.00 round number, and near the 200-day simple moving average (SMA). The pair has lost more than 6% since it topped at 161.94 and is still trading well below the long-term descending trend line. The next level to consider as support may be the 200-day SMA near 151.60, ahead of the 50.0% Fibonacci retracement level of the up leg from 140.20 to 161.94 at 151.10.

On the upside, a decisive break above the 154.50 barrier could drive the bulls to the 23.6% Fibonacci level of 156.85. A climb towards the upcoming bearish crossover within the 20- and 50-day SMAs near the 157.90 resistance level could not be enough for a full-scale reversal, as the pair would need to jump above the uptrend line and the previous high of 161.94.

Key Euro Area Data Overshadowed by Developments Elsewhere

- Fed meeting and Middle East developments in the foreground

- Tuesday's eurozone GDP figures could produce a surprise

- Wednesday’s inflation report unlikely to unsettle ECB expectations

- Euro remains under pressure against the pound

Fed meeting overshadows key Euro area data

With the market digesting the latest developments in the US presidential race and preparing for Wednesday’s Fed meeting, a rather busy calendar is in store for euro traders this week. The preliminary GDP print for the second quarter of 2024, the eurozone unemployment rate and, more importantly, the preliminary July inflation report could prove market-moving ahead of the expected summer lull.

The latest ECB gathering proved the least exciting one in 2024, but there were some clear messages from President Lagarde. She was adamant about the new “no pre-commitment” dogma and highlighted that the ECB is data dependent and not data-point dependent. This rhetoric was part of her effort to appease the ECB hawks following the rather eventful June meeting, which ended with a rate cut, but created a strong rift within the ECB ranks and substantially raised the bar for the next rate cut.

ECB members have taken a back seat lately as the political situation in the US unfolds and the Summer Olympic Games in Paris are underway. Maybe this is the best time to collect their thoughts and plan the strategy for the rest of 2024 away from the spotlight but paying close attention to the incoming data releases. These figures have been painting a rather bleak picture of the euro area, potentially justifying the ECB doves’ insistence for the June rate cut.

Eurozone Q2 GDP will be released on Tuesday

On Tuesday, the preliminary GDP print for the second quarter of 2024 will be published. Q1 was stronger than expected, dissipating concerns about a protracted recession. Considering the ECB rate cut in June, the fluid political environment in the euro area and the overall negative market sentiment, one would have expected a rather weak set of forecasts on Tuesday.

However, the market is forecasting a small acceleration to the annual eurozone aggressive figure to 0.6% from 0.4% with the quarterly print seen decelerating a tad. Spain and Italy will most likely continue to grow strongly, covering the momentum loss potentially seen in both Germany and France.

Interestingly, with last week’s US GDP figure surprising on the upside and the eurozone PMI services surveys enjoying a strong uptrade during the second quarter of 2024, there is a small possibility for an upside surprise on Tuesday, which would be rather welcomed by the ECB hawks. On the flip side, the European election in early June and the subsequent double parliamentary elections in France might have significantly impacted consumer appetite and business activity in the region.

Preliminary German CPI on Tuesday, eurozone aggregate print on Wednesday

Later on Tuesday, the preliminary CPI prints from the German states will start to trickle in with the German national figure expected around 12.00 GMT. CPI is seen stable at 2.2% year-on-year growth and thus opening the door for a downside surprise at Wednesday’s euro area aggregate release.

At 09.00 GMT on Wednesday morning, the eurozone headline CPI is forecast to show a 2.4% y-o-y increase, down from the June 2.5% print, with the core indicator also edging slightly lower to 2.8%. The next CPI report will be published in late August, with the hopes of a continuation of the recent downward trend cementing market expectations for a September rate cut, regardless of what the Fed opts for.

Euro/pound downtrend persists

Despite last week’s recovery, the euro remains under pressure against the pound. The worsening economic outlook for the euro area and the new-found political stability in the UK have been supporting the ongoing pound appreciation.

The BoE could surprise with a rate cut on Thursday, but unless the eurozone data produces consistent upside surprises this week, the bearish trend in euro/pound is unlikely to be reversed soon. Having said that, a confident break above the November 20, 2023 trendline could open the door for a test of the early June peak at 0.8498.

Sunset Market Commentary

Markets

Today has mostly been a waiting game in the run-up to an economic calendar that shifts into higher gear starting from tomorrow. The were few to no signs of worry about a potential escalation in the Gaza war after Israel retaliated over the weekend on what it said was a Hezbollah attack in the Golan Heights. Oil prices gapped higher at the open this morning but quickly pared gains to trade slightly lower on the day (< $81 per barrel). The constructive Asian equity sentiment didn’t spill over into European dealings though with the likes of the EuroStoxx50 shedding 0.3% in choppy trading. Stock markets in the US do open higher (in tech-heavy indices). Core bond yields extend their losing streak, confirming that south for the time being remains the path of least resistance. US Treasury yields drop between 0.4 (2-yr) and 3.4 (30-yr) bps with both the 2-yr and 10-yr tenor nearing first technical support areas (4.34%/July low and 4.14% respectively). German yields lose between 2.1 and 6.2 bps in a similar shift of the curve. Here too short and longer term maturities are either nearing or testing important support zones (eg. 2.34% June low for the 10-yr tenor). Markets are bracing for an imminent (Fed) or continuation (ECB) of the monetary easing cycle but are also adjusting their views on the economy after a string of disappointing or outright poor economic data. In the US, the 10-yr real yield has dipped sub 2% since mid-July.

The dollar gained the upper hand on currency markets, especially against an overall weak euro. EUR/USD for no apparent reason slid throughout the day from as high as 1.087 to 1.081 currently. The trade-weighted dollar index rose to its highest level since the June CPI undershoot, July 11. The greenback didn’t gain (much) against the Japanese yen though. USD/JPY stabilized around 153.9 for most of the day. Sterling showed some sharp intraday swings. EUR/GBP shortly after the European open jumped towards a high of 0.846 before paring gains almost as quickly. The pair is currently changing hands around 0.842, down from 0.8437 on Friday. We’ve seen no particular trigger for the moves but the upcoming Bank of England meeting is probably triggering some market nerves. Market implied probability for a cut dropped from over 70% end last week to less than 60% today.

News & Views

Sweden’s economy unexpectedly contracted in the second quarter of the year. A preliminary reading based on the monthly GDP indicator (using an incomplete dataset) showed GDP dropping 0.8% q/q vs an expected stagnation. It followed sharper-than-expected growth in Q1 of 0.7%. These Q1 figures illustrate the possible gap between the first and the final reading with its initial estimate being a 0.1% contraction. Since the numbers lie outside official statistics, Swedish Statistics does not offer details on growth composition. “The Swedish economy grew in June [0.9% m/m] but figures for the second quarter as a whole were weighed down by weak figures in April,” economist at Statistics Sweden Mattias Kain Wyatt added. Given the volatile nature of the monthly dataset and huge revision potential, Sweden’s currency chose not to react panicky. EUR/SEK is hovering sideways around 11.70+ with SEK trying to find a bottom after a heft slide since mid-June.

Belgian GDP grew 0.2% q/q in Q2 of this year, the National Bank of Belgium released today. The economy is now 1.1% bigger compared to the same period in 2023. Quarterly growth was the slowest since 2022Q4 while the yearly measure was the lowest since the huge upswing in the wake of the lockdowns being lifted. The preliminary estimate only contains a sectoral divide showing that rising value added in the services economy (+0.2% q/q) and especially construction (+1.1%) compensated for a -0.3% drop in the industry.

Graphs

EUR/SEK: Swedish currency unbothered by preliminary GDP release showing economy contracted 0.8% q/q

Brent oil’s “gap” higher in wake of Israeli-Gaza war developments evaporated almost immediately

Nasdaq is looking for a bottom after a tech-driven sell-off last week pushed it to the brink of a 10% correction

German 10-yr yield is testing important support area ahead of key data releases this week including GDP and CPI

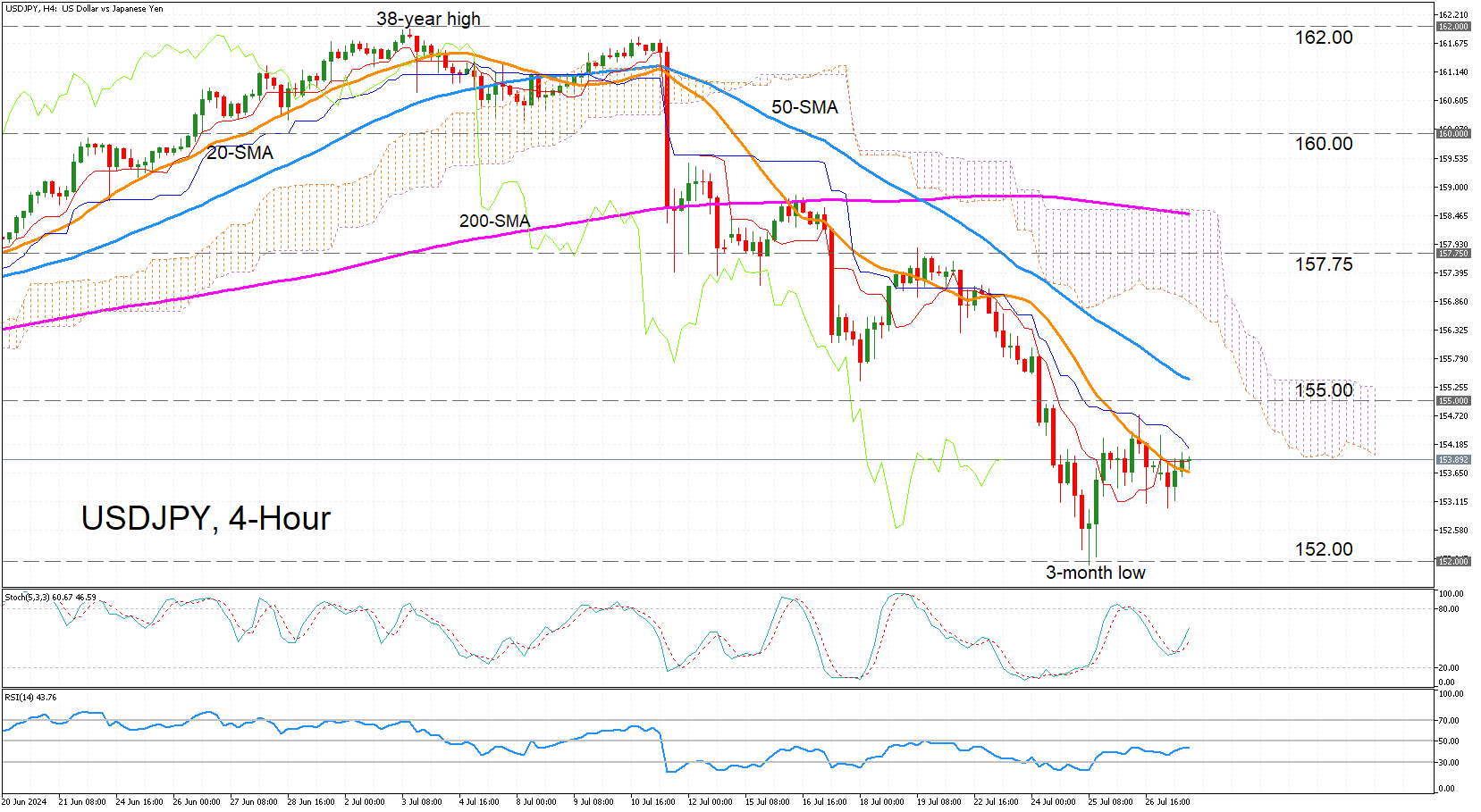

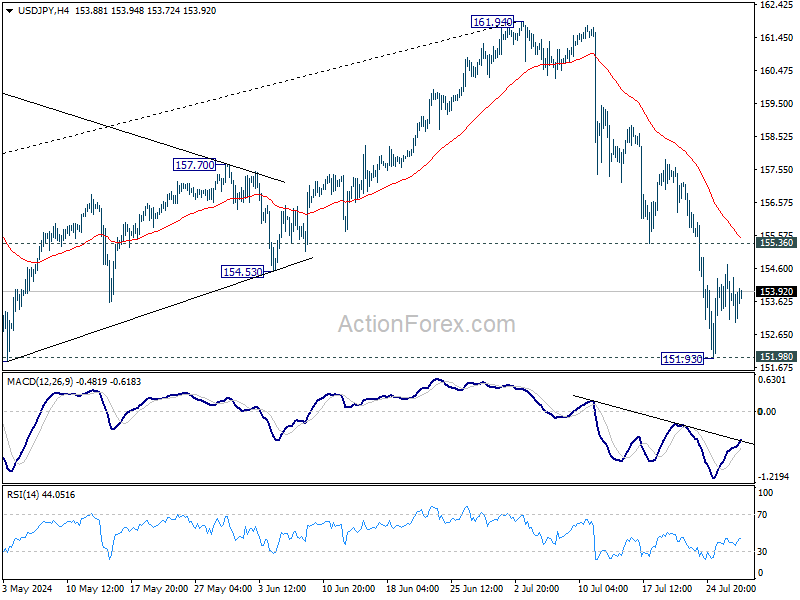

USDJPY Struggles to Reclaim 20-Period SMA

- USDJPY caught in a battle to overcome 20-period SMA

- Near-term momentum is positive but weak

- Bulls face an uphill struggle to regain control

USDJPY has started the week on a somewhat positive note but it’s proving difficult for the bulls to secure the upper hand as a tough battle rages around the 20-period simple moving average (SMA) in the 4-hour chart.

Both the stochastics and RSI have reversed higher, but the positive momentum does not appear to be strong enough to last through the day let alone the next few days.

The price has only just managed to climb above the 20-period SMA but is being capped by the Tenkan-sen line of the Ichimoku cloud. The Kijun-sen line is also closing in on the price slightly above the 154.00 level. If the rebound from last week’s near three-month lows is to have any legs, the price needs to clear these hurdles, as well as the 155.00 region, and aim for the 50-period SMA at 155.40 before trying to re-enter the Ichimoku cloud.

However, if the upside momentum loses steam and the price dips back below the 20-period SMA, the pair could revisit the July 25 low of 151.93. A breach of this low would reinforce the bearish short-term picture. But for the medium-term outlook to also turn bearish, USDJPY would need to slip below its 200-day SMA too not far lower at 151.62.

In brief, there is still hope for the latest rebound to get onto a more solid footing but there are numerous obstacles ahead that could stop the bulls in their tracks.

USD Analysis: Key Data Releases and Technical Outlook for the Week and intraday. EURUSD

Fundamental Analysis

In the absence of high-impact data on Monday, July 29, 2024, market sentiment is focused on the key data releases for the week. First, the Federal Reserve's interest rate decision is set for Wednesday. While no rate change is expected, any adjustment in the statement's language could signal a more dovish or hawkish stance, impacting the dollar. Additionally, the July non-farm payrolls report, due on Friday, is crucial. A gain of 185,000 jobs is expected, with the unemployment rate holding steady at 4.1%. Strong data could reduce expectations for rate cuts, while disappointing figures might increase speculation about a more flexible policy.

Other economic indicators to watch include the Consumer Confidence Index and JOLTS job openings on Tuesday, the ADP employment report and Chicago PMI on Wednesday, and the ISM manufacturing PMI on Thursday. These data points will provide a broader view of the state of the US economy and could influence future monetary policy expectations, thereby affecting the strength of the USD in the markets.

Technical Analysis, H4. Intraday and Swing Overview

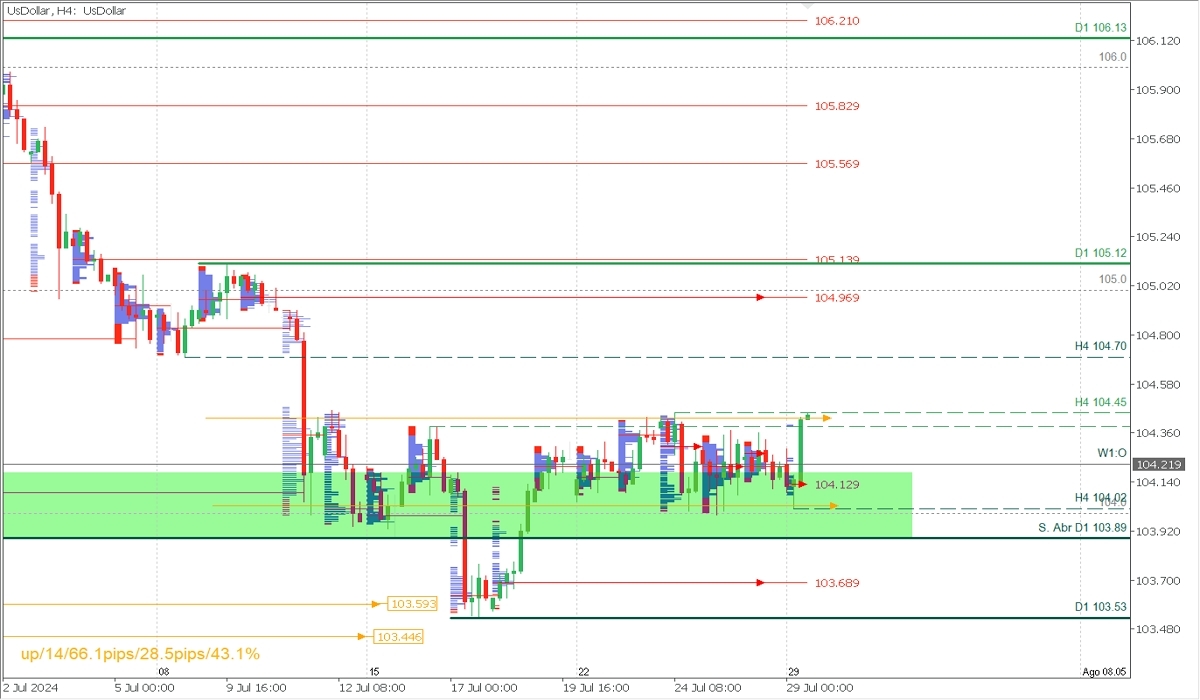

US Dollar Index

Supply Zones (Sell): 104.969 and 105.139

Demand Zones (Buy): 104.129 and 103.689

Following last week's consolidation and the modest breakout of the H4 resistance at 104.39, a new upward move is anticipated to surpass the 104.45 resistance to confirm a bullish reversal, particularly given the price's rise during the European session. To maintain a bullish bias, intraday sales might be limited by the broken resistance of the Asian session at 104.29 or, more broadly, the POC from the initial sessions at 104.129. Purchases could then be renewed above 104.45, targeting a reach and potential surpassing of the 104.70 level, towards the next sell zone at 104.969/105.00. On the other hand, an increase in bearish pressures would be confirmed by a break below the demand zone around 104.129 and a further drop below 104.00, in which case the week's sell targets would be the April support at 103.89 and the demand zone around 103.68.

EURUSD. H1. Intraday

Supply Zones (Sell): 1.08583

Demand Zones (Buy): 1.08297

After reaching the support and daily bearish range average at 1.08297, the first bounce zone is 1.0838/40. If surpassed, consider corrective buys towards 1.0851, the last broken support of the previous bullish correction. Given that the bearish range has already been reached during the European session, it is unlikely that the descent will continue in today's American session. In this context, the price action reflects a continuation of the pair's bearish trend, with the next swing targets (starting tomorrow) being the levels at 1.0826, the uncovered POC at 1.0822, and the daily support at 1.0802. However, if the rebound surpasses the supply zone that triggered the price drop at 1.08583 and 1.0869, the correction could extend towards 1.0890.

Note: POC stands for Point of Control, which is the level or area where the highest volume concentration occurred. If a downward movement originated from this point, it is considered a sell zone and forms a resistance area. Conversely, if there was a prior upward movement, it is considered a buy zone, usually located at the lows, forming support areas.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.96; (P) 153.85; (R1) 154.59; More...

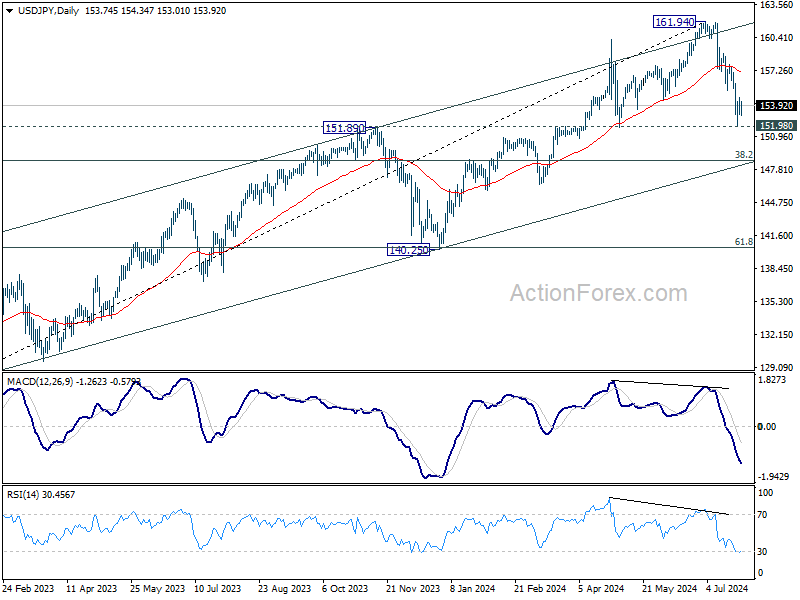

No change in USD/JPY's outlook and intraday bias remains neutral for consolidation above 151.93. Further decline is expected as long as 155.36 support turned resistance holds. On the downside, decisive break of 151.89 resistance turned support will argue that large scale correction is underway to 148.66 fibonacci level. Nevertheless, break of 155.36 will turn bias back to the upside for stronger rebound.

In the bigger picture, considering the depth and momentum of the current decline, 161.94 should be a medium term top already. Fall from there is seen as correcting the whole rise from 127.20 (2023 low) at least. Break of 151.89 will pave the way to 38.2% retracement of 127.20 to 161.94 at 148.66. Risk will now stay on the downside as long as 55 D EMA (now at 157.04) holds, in case of rebound.

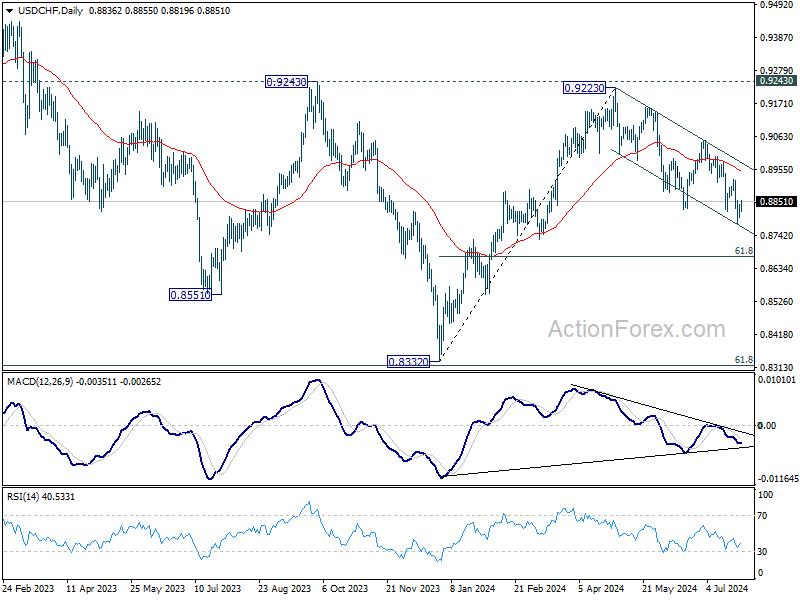

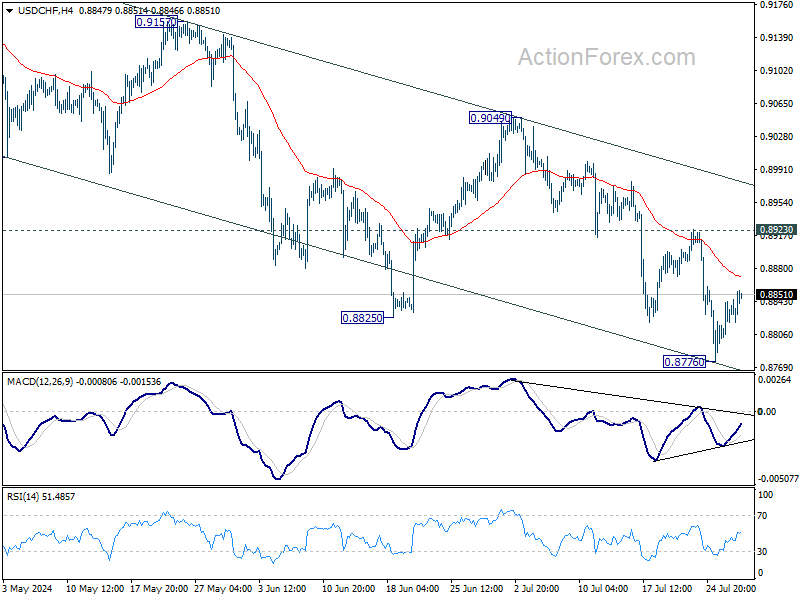

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8812; (P) 0.8828; (R1) 0.8853; More…

No change in USD/CHF's outlook and intraday bias stays neutral for consolidations above 0.8776 temporary low. Further decline is expected as long as 0.8923 resistance holds. On the downside, break of 0.8776 will resume the fall from 0.9223 to 61.8% retracement of 0.8332 to 0.9223 at 0.8672 next. However, break of 0.8923 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, with 0.9243 resistance intact, medium term outlook in USD/CHF is neutral at best. For now, more sideway trading is likely between 0.8332/9243. However, firm break of 0.9243 will indicate larger bullish trend reversal.