Sample Category Title

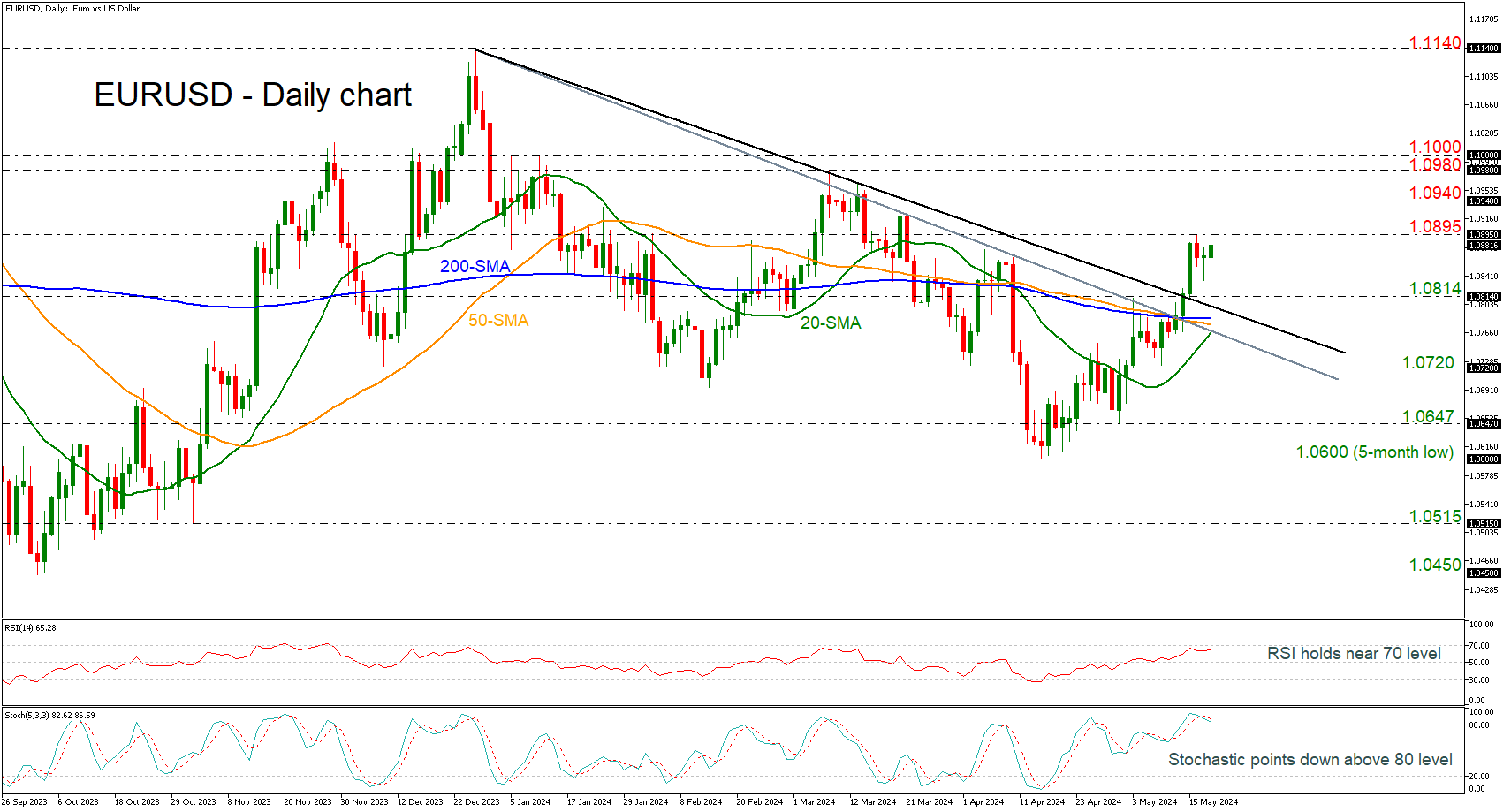

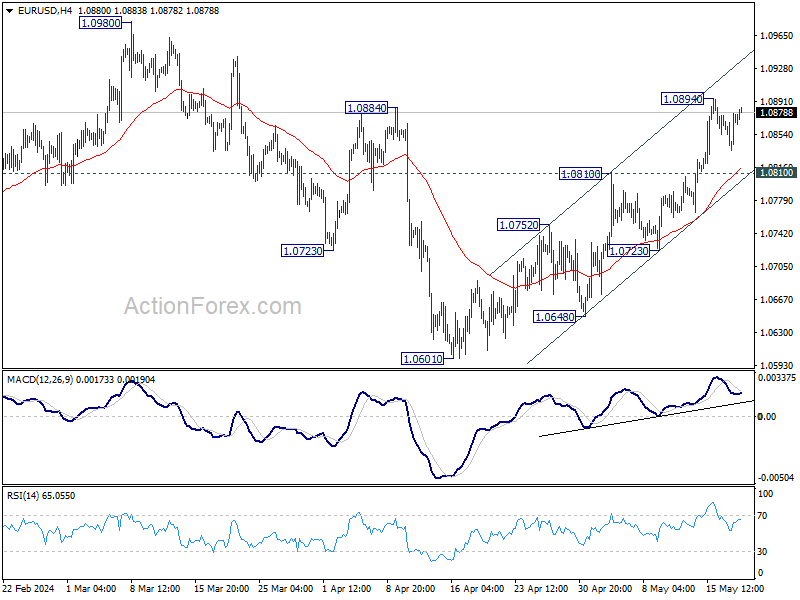

EURUSD Fails to Surpass 1.0900

- EURUSD holds above medium-term downtrend line

- Oscillators indicate bearish structure

EURUSD appears to be maintaining a horizontal trajectory in the very short-term, trapped between the 1.0895 resistance level and the 1.0814 support. A paused state of directional momentum is reflected in the technical oscillators. The stochastic posted a bearish crossover within its %K and %D lines in the overbought territory, while the RSI is failing to jump above the 70 level.

To the upside, emanating pressure over the last couple of months has denied upside moves. If buyers manage to jump above the 1.0895 barrier, a revisit of the 1.0940 mark could unfold. Overcoming these constrictions could see resistance develop at the 1.0980-1.1000, which is acting as a crucial obstacle for traders.

Otherwise, if sellers drive the pair below the 1.0814 support it could interrupt the pair ahead of the penetrated descending trend line and the 200 and the 50-day simple moving averages (SMAs) around 1.0785. In the event selling interest persists, the key support of the 20-day SMA at 1.0765 could halt the decline. Should it fail to do so, the 1.0720 bar could confirm another bearish wave.

Summarizing, the 1.0895 and 1.0900 levels are the immediate obstacles the bulls need to overcome in order for the outlook to change to a bullish one.

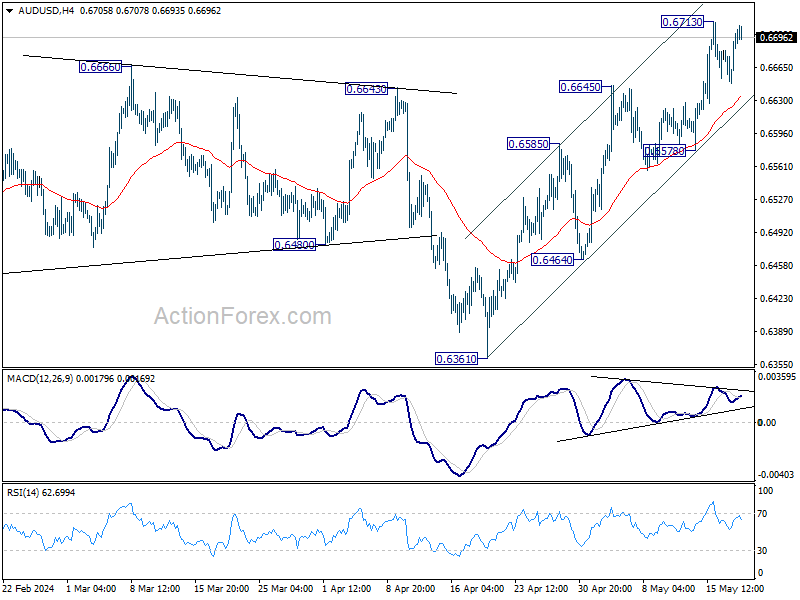

AUD/USD Daily Report

Daily Pivots: (S1) 0.6662; (P) 0.6681; (R1) 0.6714; More...

Intraday bias in AUD/USD remains neutral for consolidation below 0.6713. Further rally is expected as long as 0.6578 support holds. As noted before, fall from 0.6870 has probably completed with three waves down to 0.6361 already. Above 0.6713 will target 0.6870 resistance next.

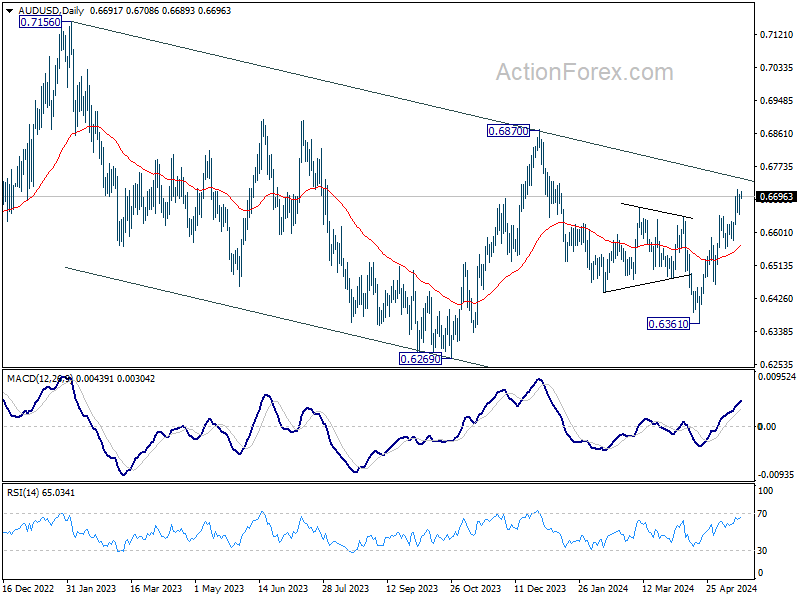

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

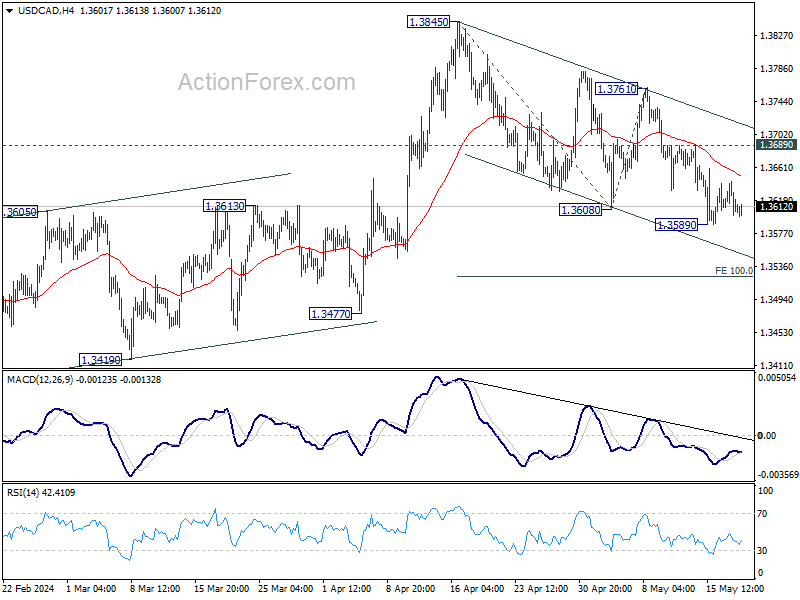

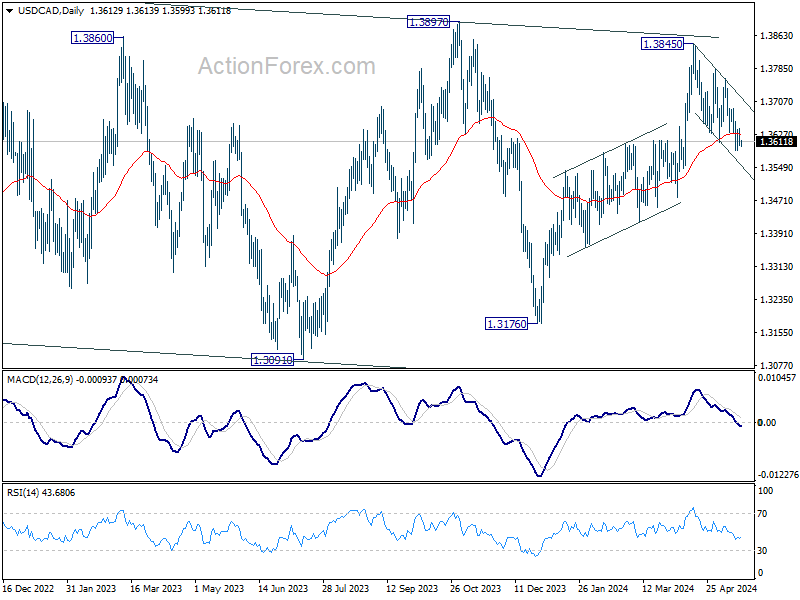

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3594; (P) 1.3619; (R1) 1.3637; More...

Intraday bias in USD/CAD remains neutral for the moment. Break of 1.3589 will resume whole fall from 1.3845 and target 100% projection of 1.3845 to 1.3608 from 1.3761 at 1.3524. Also, sustained trading below 55 D EMA (now at 1.3628) will argue that whole rise from 1.3176 has completed already.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

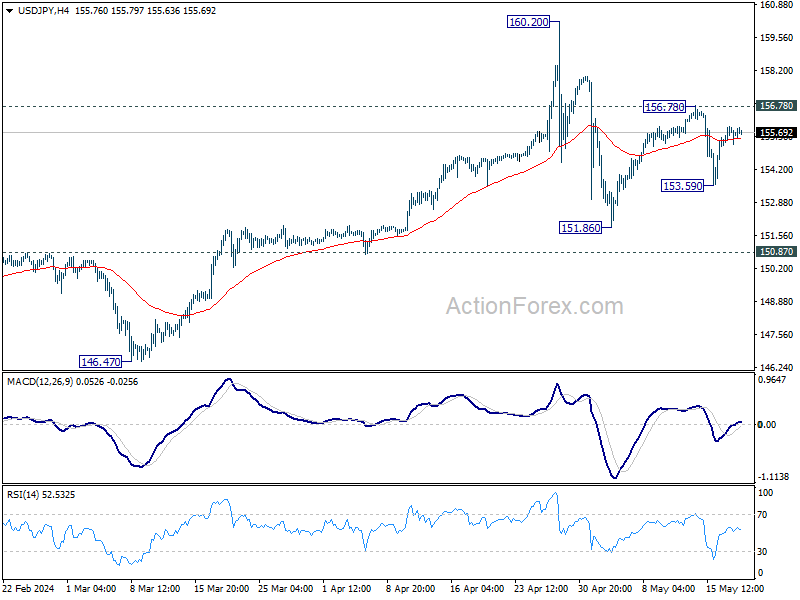

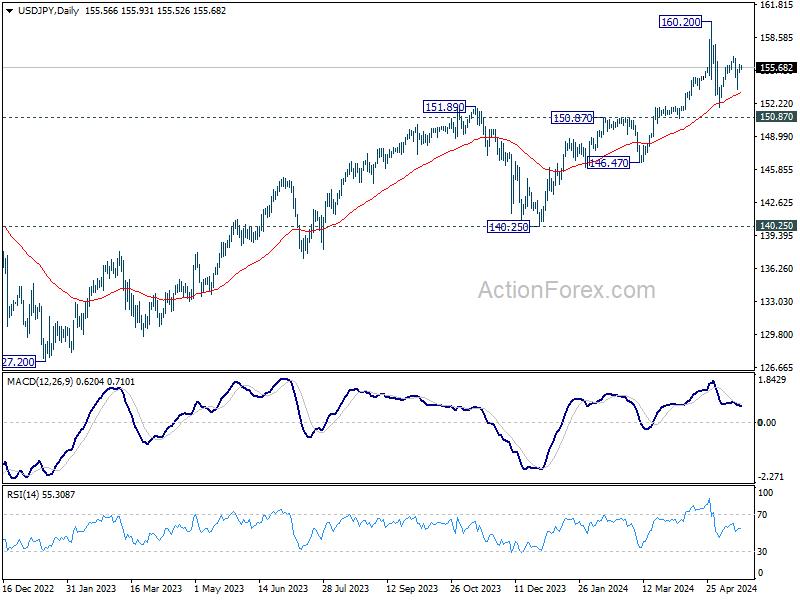

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.29; (P) 155.63; (R1) 156.02; More...

Intraday bias in USD/JPY stays neutral at this point. Price actions from 160.20 are seen as a corrective pattern. On the upside, break of 156.78 will resume the rise from 151.86, as the second leg, to retest 160.20 high. On the downside, below 153.59 will target 151.86 and below as the third leg.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

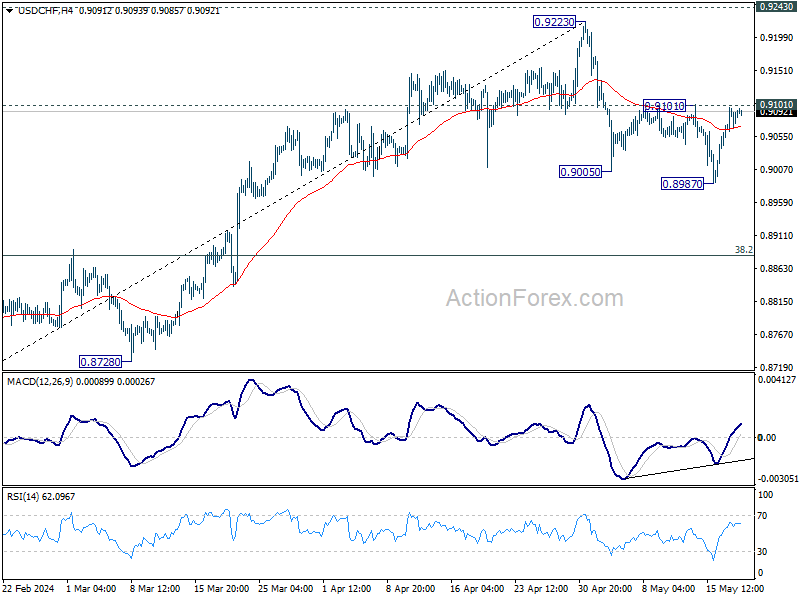

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9062; (P) 0.9080; (R1) 0.9110; More....

Intraday bias in USD/CHF remains neutral at this point. On the upside, firm break of 0.9101 will argue that corrective fall from 0.9223 has completed with three waves down to 0.8987 already. Further rise should then be seen to retest 0.9223. On the downside, though, break of 0.8987 will resume the fall to 38.2% retracement of 0.8332 to 0.9223 at 0.8883.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0844; (P) 1.0861; (R1) 1.0886; More...

Intraday bias in EUR/USD remains neutral for consolidation below 1.0894. Further rally is expected as long as 1.0810 resistance turned support holds. Break of 1.0894 will resume the rise to 1.0980 resistance. Decisive break there will confirm that whole fall from 1.1138 has completed at 1.0601 already.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

How High is Too High?

Equity bulls around the globe celebrated in style the softer-than-expected US CPI data last week. The global equity rally was further juiced by the expectation that a softer inflation in the US would not only allow the Federal Reserve (Fed) to start cutting the rates this year, but also allow the other major central banks, like the European Central Bank (ECB) and the Bank of England (BoE), to carry on with their plans to cut their own rates and – maybe – cut more than people think they could. The S&P500, Nasdaq 100 and Dow Jones renewed record last week, the Big US retailers quarterly results hinted that consumer demand may be coming to a slippery ground, the latter sent Walmart shares to a fresh high last week after the announcement of its Q1 results. Macy’s, Lowe’s and Target earnings are due this week and could come to cement the ‘troubled outlook for spending’ story – that could continue to butter the bread of the Fed doves and further fuel the reflation trade that benefits grandly to the stocks at this side of the Atlantic Ocean as well. The European Stoxx 600 and the British FTSE 100 followed suit with fresh records, the treasuries had their best month this year and the US dollar fell.

But note that the US 2-year yield rebounded past the 4.80% level the greenback kicks off the week under some selling pressure, and the US dollar index held ground above a major Fibonacci support, the 38.2% retracement on the ytd rally that distinguishes the ytd positive trend from a medium term bearish reversal. The soft CPI data could’ve certainly marked the end of this year’s positive trend but people still took into consideration that the producer price data released just a bit earlier than the US CPI last week came in hotter-than-expected and as JP’s Jamie Dimon said ‘costs link to the green economy, remilitarization, infrastructure spending, trade disputes, and large fiscal deficits may mean inflation will stay sticky’. And he is probably right.

But regardless of the warnings, the equity market cleared an important barrier to the present optimism, and is looking to jump over the next big barrier – Nvidia earnings – this week. Nvidia is expected to reveal another blowout quarter where sales may have hit the $24bn mark. Remember that big AI spenders like Meta said earlier in this earning season that they will be spending more on AI. The latter hinted that demand for Nvidia’s AI chips may remain sustained for some more time. Price-wise, Nvidia gained more than 700% since the beginning of last year on AI boom, and is trading at a spitting distance from the $1000 per share level. This week’s results will either send the share above this $1000 level or trigger profit taking near it. But any misstep from Nvidia – which has been the icon of the AI rally – has potential to trigger a broader market selloff, especially across the technology stocks. Note that, the price-to-estimated earnings of the S&P500’s technology sector bounced above the 28 level, which has acted as an important resistance since 2020. Therefore, the current levels could well be appropriate for a correction. And a potential disappointment from Nvidia could pull that trigger.

Also this week

Canada and the UK are due to announce their latest CPI updates on Tuesday and Wednesday respectively, the Reserve Bank of New Zealand (RBNZ) is expected to maintain its policy rate unchanged at 5.50% and the FOMC is scheduled to release the minutes of its latest meeting. Inflation in the UK is expected to have fallen from 3.2% to 2.1% in April. If that’s the case, the BoE rate cut bets could take a lift and limit Cable’s upside potential before the 1.28 mark. Elsewhere, the EURUSD rallied and stepped into the bullish consolidation zone last week on the back of a softer-than-expected US inflation, but sees resistance into the 1.09 mark. Released last Friday, the series of inflation numbers from the Eurozone came with no surprise. Inflation in the Eurozone eased in April, keeping the prospects of a June rate cut well alive. The divergence between the ECB and the Fed outlooks narrowed slightly due to a softer-than-expected US CPI report, but it could not suffice to justify an extension of gains toward the 1.10 psychological mark.

In commodities, US crude rebounded and is testing the $80pb psychological offers this morning. The dovish central bank expectations continue to support the reflation trade, which in return is supportive of energy and commodity prices. Fresh Chinese stimulus measures aiming to address the country’s heavily bleeding property market, and the latest – and better-than-expected – rebound in Chinese industrial production also support the rally in commodity prices. The copper futures begin the week at fresh ATH and the CSI 300 index is pushing higher this Monday, as well.

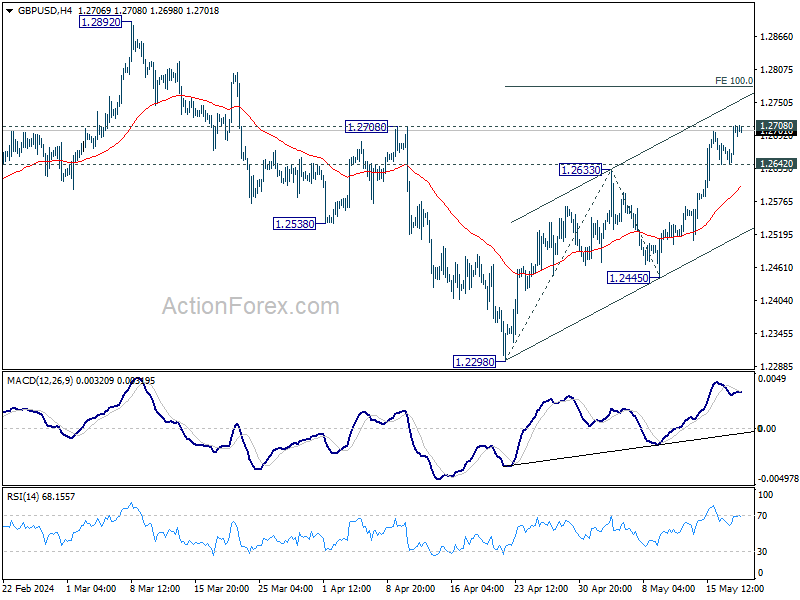

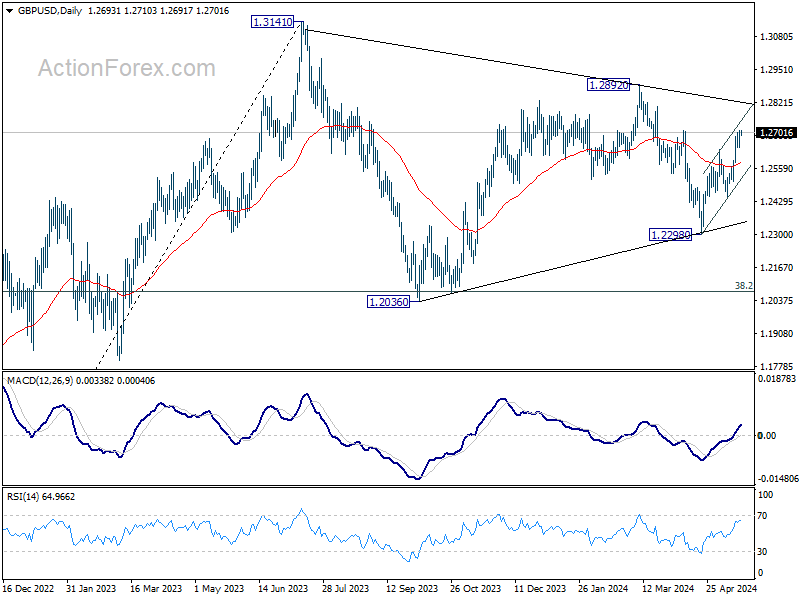

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2660; (P) 1.2686; (R1) 1.2727; More...

Intraday bias in GBP/USD remains on the upside for the moment. Firm break of 1.2708 resistance will extend the rise from 1.2298 to 100% projection of 1.2298 to 1.2633 from 1.2445 at 1.2780. On the downside, below 1.2642 minor support will turn intraday bias neutral again. But further rise will now remain in favor as long as 1.2445 support holds, in case of retreat.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

Week Begins with Market Optimism, Metals See Strong Gains

Asian markets kicked off the week on a positive note, buoyed by the record-breaking rally in US markets last week. Despite escalating geopolitical tensions in the Middle East, which have spurred strong rallies in metals, stock investors appear relatively calm. Trading activity today may be muted due to bank holidays in several European countries and Canada, along with an empty US economic calendar. However, market participants will be paying close attention to comments from BoE MPC member Ben Broadbent and several Fed officials. Later in the week, volatility is expected to rise with RBNZ rate decision, RBA and Fed minutes as well as key CPI and PMI data from several countries.

In the currency markets, Australian Dollar is currently leading the pack, followed by Euro and Canadian Dollar. Conversely, New Zealand Dollar is the weakest performer, likely due to caution ahead of RBNZ rate decision. Dollar and Japanese Yen are also lagging, with Swiss Franc not far behind. This pattern aligns with the prevailing risk-on sentiment in the markets.

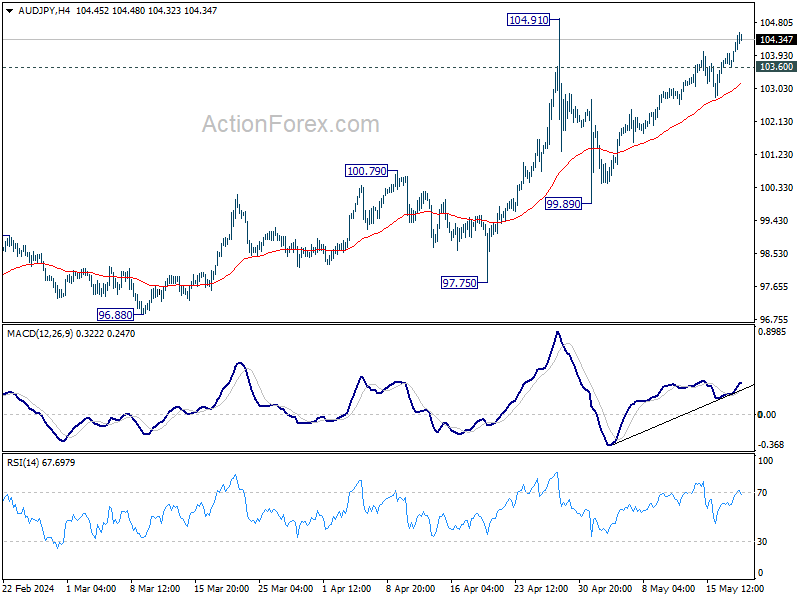

Technically, AUD/JPY's rally from 99.89 continues today and it's in progress for retesting 104.91 high. Resistance could be seen there to limit upside. Break of 103.60 minor support will turn intraday bias neutral first. Sustained break of 55 4H EMA (now at 103.17) will argue that the corrective pattern from 104.91 has started the third leg, and bring deeper fall back towards 99.89. However, decisive break of 104.91 will confirm larger up trend resumption instead.

In Asia, Nikkei rose 0.73%. Hong Kong HSI is up 0.61%. China Shanghai SSE is up 0.54%. Singapore Strait Times is down -0.07%. Japan 10-year JGB yield is up 0.0256 at 0.978.

China holds rates steady amidst property sector support measures

China kept its benchmark lending rates unchanged at today's monthly fixing, aligning with market expectations. One-year Loan Prime Rate remained at 3.45%, while Five-year LPR stayed at 3.95%. This decision follows the People's Bank of China's move last week to maintain a key policy rate at 2.50% while rolling over maturing medium-term lending facilities.

Additionally, China announced on Friday a series of measures to stabilize its crisis-hit property sector, including the central bank facilitating CNY 1T in extra funding and easing mortgage rules. This strong supportive policy rollout has increased the likelihood of further monetary easing in the coming months.

Some economists now expect one or two cuts to LPR later this year, alongside a reduction in the reserve requirement ratio. These anticipated measures aim to bolster the property sector and sustain economic growth amid ongoing challenges.

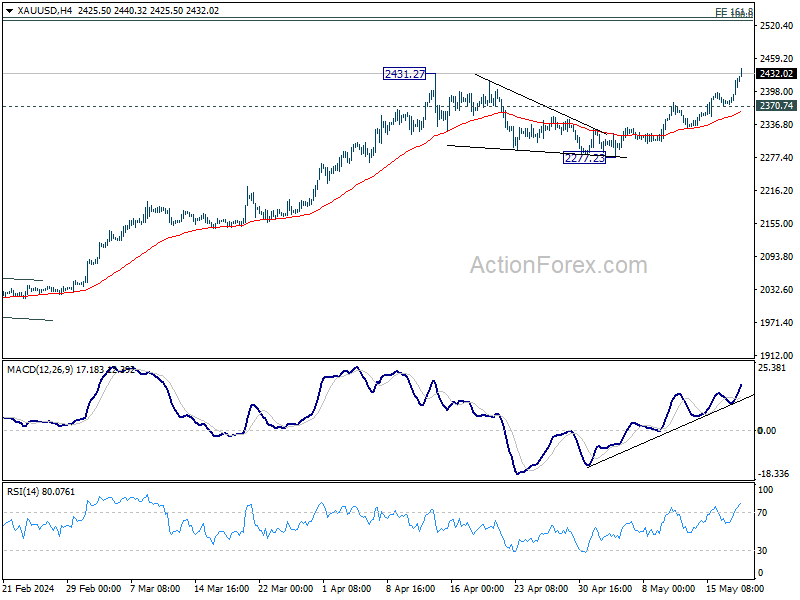

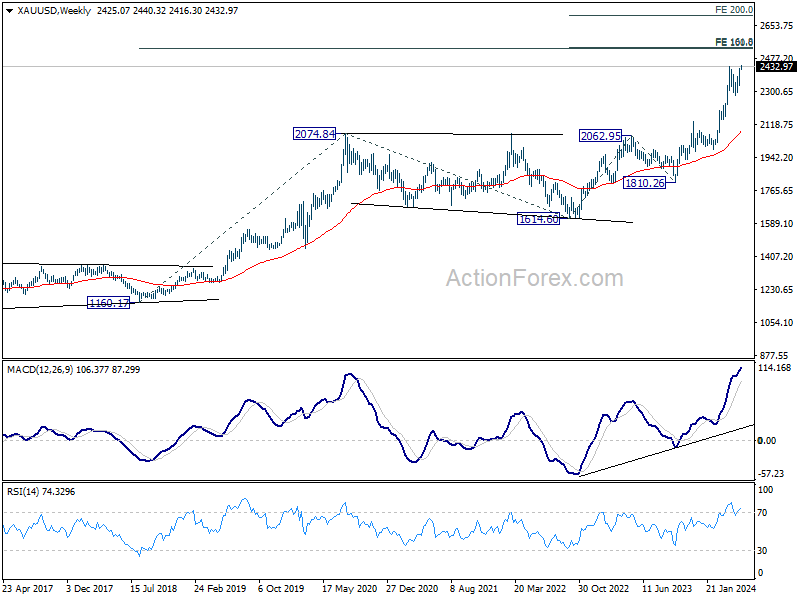

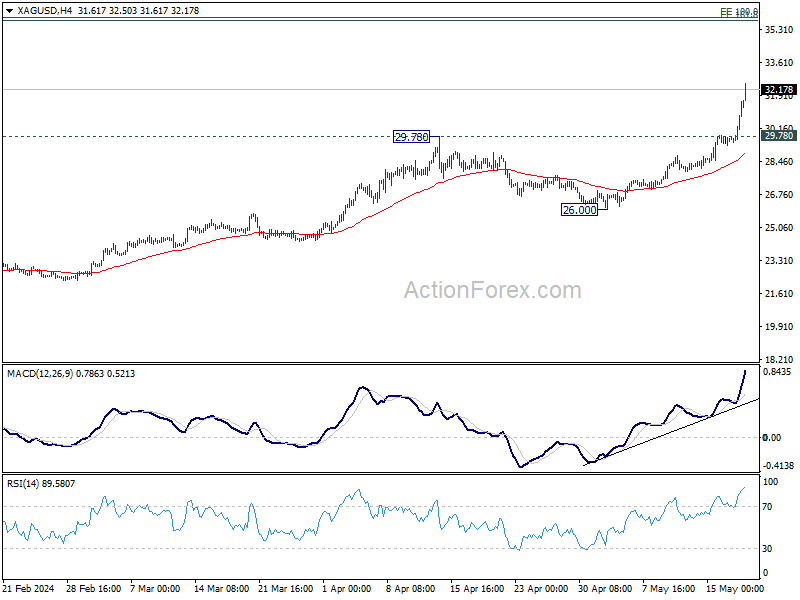

Gold soars to record on geotensions, Silver rallies too

Gold reached a new record high today, fueled by escalating geopolitical tensions in the Middle East and the prospect of easing policies from major central banks this year. Investors are flocking to the safe-haven asset following a series of unsettling events. On Sunday, a helicopter carrying Iranian President Ebrahim Raisi crashed in dense fog, heightening regional instability. Additionally, a China-bound oil tanker was hit by a Houthi missile in the Red Sea on Saturday, further exacerbating tensions. The anticipated shift towards more accommodative monetary policies by global central banks is also reducing the opportunity cost of holding Gold, providing further support for its rally.

Technically, strong resistance could emerge at around 2500 to limit Gold's up trend, at least on first attempt. There lies 161.8% projection of 1614.60 to 2062.95 from 1810.26 at 2535.69, and 100% projection of 1160.17 to 2074.84 at 1614.60 at 2529.27.

However, decisive break of 2500 would set the stage for 200% projection of 1614.60 to 2062.95 from 1810.26 at 2706.96 next. In any case, near term outlook will stay bullish as long as 2370.74 support holds.

Silver is also in strong rally at this point. Near term outlook will stay bullish as long as 29.78 resistance turned support holds. Next target is cluster projection level at 35.80/94, 161.8% projection of 17.54 to 26.12 from 21.92 at 35.80 and 100% projection of 11.67 to 30.07 from 17.54 at 35.94.

RBNZ; RBA and FOMC Minutes; CPIs and PMIs

Several key central bank activities will take center stage this week, along with consumer inflation data and PMIs from several major economies.

RBNZ rate decision is widely expected to keep OCR unchanged at 5.50%. Investors and analysts will be particularly interested in the new Monetary Policy Statement for any changes in its OCR forecasts. Previously, the forecasts suggested 40% probability of a rate hike in Q3, followed by the first rate cut in Q2 2025. The upcoming statement may adjust these probabilities, with prospects of eliminating the chance of another hike, though it may stop short of advancing the timeline for the first rate cut.

Attention will also be directed towards the minutes from RBA and FOMC meetings. RBA has maintained a flexible stance, by not ruling anything in and out. Market observers will scrutinize the minutes for any indications of how inclined (or not) the board towards a rate hike. As for FOMC minutes, market will look for further evidence to rule out the chance of another rate hike. Regarding the first Fed rate cut, it's too early for the minutes to tell whether September is the timing.

Additionally, inflation data from Canada, the UK, and Japan will be closely watched. For BoE and BoC, substantial decline in inflation is necessary before considering a rate cut in June. If inflation remains elevated, BoE might look to August, and the BoC to July, for potential rate adjustments.

Other significant economic indicators to monitor include durable goods orders from the US and retail sales data from Canada, the UK, and New Zealand. PMIs from Australia, Japan, Eurozone, the UK, and the US will also provide valuable insights.

Here are some highlights for the week:

- Monday: Japan tertiary industry index.

- Tuesday: Australia Westpac consumer sentiment, RBA minutes; Eurozone current account, trade balance; Canada CPI.

- Wednesday: Japan machine orders, trade balance; RBNZ rate decision; UK CPI, PPI; US existing home sales.

- Thursday: New Zealand retail sales; Australia PMIs, inflation expectations; Japan PMIs; Eurozone PMIs; UK PMIs; US jobless claims, PMIs, new home sales.

- Friday New Zealand trade balance; Japan CPI; UK consumer confidence, retail sales; Canada retail sales; US durable goods orders.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2660; (P) 1.2686; (R1) 1.2727; More...

Intraday bias in GBP/USD remains on the upside for the moment. Firm break of 1.2708 resistance will extend the rise from 1.2298 to 100% projection of 1.2298 to 1.2633 from 1.2445 at 1.2780. On the downside, below 1.2642 minor support will turn intraday bias neutral again. But further rise will now remain in favor as long as 1.2445 support holds, in case of retreat.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:15 | CNY | PBoC 1-y Loan Prime Rate | 3.45% | 3.45% | 3.45% | |

| 01:15 | CNY | PBoC 5-y Loan Prime Rate | 3.95% | 3.95% | 3.95% | |

| 04:30 | JPY | Tertiary Industry Index M/M Mar | -2.40% | 0.10% | 1.50% |

Westpac New Zealand RBNZ Pulse Client Survey

Ahead of this week’s RBNZ policy meeting, our survey finds that offshore clients are more dovish than those onshore. Both groups are more dovish than the RBNZ.

- Market participants see an earlier start to RBNZ easing than RBNZ and Westpac forecasts.

- Survey participants are less dovish than market pricing.

- Offshore market participants are more dovish than New Zealand-based clients.

- Participants see the path of non-tradable and headline inflation as key risk factors.

- Offshore market participants see potential labour market weakness as being more important compared to New Zealand- based clients.

- There is a significant gulf between the RBNZ’s stance and the hopes of offshore market participants, which raises the stakes of the May Monetary Policy Statement and June quarter CPI.