Sample Category Title

Summary 4/22 – 4/26

Monday, Apr 22, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Apr P | 47.3 | |

| 23:00 | AUD | Services PMI Apr P | 54.4 | |

| 23:01 | GBP | Rightmove House Price Index M/M Apr | 1.50% | |

| 01:15 | CNY | PBoC 1-y Loan Prime Rate | 3.45% | 3.45% |

| 01:15 | CNY | PBoC 4-y Loan Prime Rate | 3.95% | 3.95% |

| 12:30 | CAD | Industrial Product Price M/M Mar | 0.80% | 0.70% |

| 12:30 | CAD | Raw Material Price Index Mar | 2.90% | 2.10% |

| 12:30 | CAD | New Housing Price Index M/M Mar | 0.10% | 0.10% |

| 14:00 | EUR | Eurozone Consumer Confidence Apr P | -14 | -15 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Apr P | |

| Forecast: | Previous: 47.3 | ||

| 23:00 | AUD | Services PMI Apr P | |

| Forecast: | Previous: 54.4 | ||

| 23:01 | GBP | Rightmove House Price Index M/M Apr | |

| Forecast: | Previous: 1.50% | ||

| 01:15 | CNY | PBoC 1-y Loan Prime Rate | |

| Forecast: 3.45% | Previous: 3.45% | ||

| 01:15 | CNY | PBoC 4-y Loan Prime Rate | |

| Forecast: 3.95% | Previous: 3.95% | ||

| 12:30 | CAD | Industrial Product Price M/M Mar | |

| Forecast: 0.80% | Previous: 0.70% | ||

| 12:30 | CAD | Raw Material Price Index Mar | |

| Forecast: 2.90% | Previous: 2.10% | ||

| 12:30 | CAD | New Housing Price Index M/M Mar | |

| Forecast: 0.10% | Previous: 0.10% | ||

| 14:00 | EUR | Eurozone Consumer Confidence Apr P | |

| Forecast: -14 | Previous: -15 | ||

Tuesday, Apr 23, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Apr P | 48 | 48.2 |

| 00:30 | JPY | Services PMI Apr P | 54.1 | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Mar | 8.9B | 7.5B |

| 07:15 | EUR | France Manufacturing PMI Apr P | 46.9 | 46.2 |

| 07:15 | EUR | France Services PMI Apr P | 49 | 48.3 |

| 07:30 | EUR | Germany Manufacturing PMI Apr P | 42.9 | 41.9 |

| 07:30 | EUR | Germany Services PMI Apr P | 50.5 | 50.1 |

| 08:00 | EUR | Eurozone Manufacturing PMI Apr P | 46.5 | 46.1 |

| 08:00 | EUR | Eurozone Services PMI Apr P | 51.8 | 51.5 |

| 08:30 | GBP | Manufacturing PMI Apr P | 50.2 | 50.3 |

| 08:30 | GBP | Services PMI Apr P | 53 | 53.1 |

| 13:45 | USD | Manufacturing PMI Apr P | 52 | 51.9 |

| 13:45 | USD | Services PMI Apr P | 52 | 51.7 |

| 14:00 | USD | New Home Sales Mar | 668K | 662K |

| 22:45 | NZD | Trade Balance (NZD) Mar | -505M | -218M |

| 23:50 | JPY | Corporate Service Price Index Y/Y Mar | 2.10% | 2.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Apr P | |

| Forecast: 48 | Previous: 48.2 | ||

| 00:30 | JPY | Services PMI Apr P | |

| Forecast: | Previous: 54.1 | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Mar | |

| Forecast: 8.9B | Previous: 7.5B | ||

| 07:15 | EUR | France Manufacturing PMI Apr P | |

| Forecast: 46.9 | Previous: 46.2 | ||

| 07:15 | EUR | France Services PMI Apr P | |

| Forecast: 49 | Previous: 48.3 | ||

| 07:30 | EUR | Germany Manufacturing PMI Apr P | |

| Forecast: 42.9 | Previous: 41.9 | ||

| 07:30 | EUR | Germany Services PMI Apr P | |

| Forecast: 50.5 | Previous: 50.1 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Apr P | |

| Forecast: 46.5 | Previous: 46.1 | ||

| 08:00 | EUR | Eurozone Services PMI Apr P | |

| Forecast: 51.8 | Previous: 51.5 | ||

| 08:30 | GBP | Manufacturing PMI Apr P | |

| Forecast: 50.2 | Previous: 50.3 | ||

| 08:30 | GBP | Services PMI Apr P | |

| Forecast: 53 | Previous: 53.1 | ||

| 13:45 | USD | Manufacturing PMI Apr P | |

| Forecast: 52 | Previous: 51.9 | ||

| 13:45 | USD | Services PMI Apr P | |

| Forecast: 52 | Previous: 51.7 | ||

| 14:00 | USD | New Home Sales Mar | |

| Forecast: 668K | Previous: 662K | ||

| 22:45 | NZD | Trade Balance (NZD) Mar | |

| Forecast: -505M | Previous: -218M | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Mar | |

| Forecast: 2.10% | Previous: 2.10% | ||

Wednesday, Apr 24, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Monthly CPI Y/Y Mar | 3.40% | 3.40% |

| 01:30 | AUD | CPI Q/Q Q1 | 0.80% | 0.60% |

| 01:30 | AUD | CPI Y/Y Q1 | 3.40% | 4.10% |

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q1 | 0.90% | 0.80% |

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q1 | 4.20% | |

| 08:00 | CHF | Credit Suisse Economic Expectations Apr | 11.5 | |

| 08:00 | EUR | Germany IFO Business Climate Apr | 88.5 | 87.8 |

| 08:00 | EUR | Germany IFO Expectations Apr | 87.5 | |

| 08:00 | EUR | Germany IFO Current Assessment Apr | 88.1 | |

| 12:30 | USD | Durable Goods Orders Mar | 2.50% | 1.30% |

| 12:30 | USD | Durable Goods Orders ex Transportation Mar | 0.30% | 0.50% |

| 12:30 | USD | Durable Goods Orders ex Defense Mar | 2.00% | 2.20% |

| 12:30 | CAD | Retail Sales M/M Feb | 0.10% | -0.30% |

| 12:30 | CAD | Retail Sales ex Autos M/M Feb | 0.00% | 0.50% |

| 14:30 | USD | Crude Oil Inventories | 1.7M | 2.7M |

| 17:30 | CAD | BoC Summary of Deliberations |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Monthly CPI Y/Y Mar | |

| Forecast: 3.40% | Previous: 3.40% | ||

| 01:30 | AUD | CPI Q/Q Q1 | |

| Forecast: 0.80% | Previous: 0.60% | ||

| 01:30 | AUD | CPI Y/Y Q1 | |

| Forecast: 3.40% | Previous: 4.10% | ||

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q1 | |

| Forecast: 0.90% | Previous: 0.80% | ||

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q1 | |

| Forecast: | Previous: 4.20% | ||

| 08:00 | CHF | Credit Suisse Economic Expectations Apr | |

| Forecast: | Previous: 11.5 | ||

| 08:00 | EUR | Germany IFO Business Climate Apr | |

| Forecast: 88.5 | Previous: 87.8 | ||

| 08:00 | EUR | Germany IFO Expectations Apr | |

| Forecast: | Previous: 87.5 | ||

| 08:00 | EUR | Germany IFO Current Assessment Apr | |

| Forecast: | Previous: 88.1 | ||

| 12:30 | USD | Durable Goods Orders Mar | |

| Forecast: 2.50% | Previous: 1.30% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Mar | |

| Forecast: 0.30% | Previous: 0.50% | ||

| 12:30 | USD | Durable Goods Orders ex Defense Mar | |

| Forecast: 2.00% | Previous: 2.20% | ||

| 12:30 | CAD | Retail Sales M/M Feb | |

| Forecast: 0.10% | Previous: -0.30% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Feb | |

| Forecast: 0.00% | Previous: 0.50% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: 1.7M | Previous: 2.7M | ||

| 17:30 | CAD | BoC Summary of Deliberations | |

| Forecast: | Previous: | ||

Thursday, Apr 25, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | EUR | Germany GfK Consumer Confidence May | -25.5 | -27.4 |

| 08:00 | EUR | ECB Economic Bulletin | ||

| 12:30 | USD | Initial Jobless Claims (Apr 19) | 210K | 212K |

| 12:30 | USD | GDP Annualized Q1 P | 2.10% | 3.40% |

| 12:30 | USD | GDP Price Index Q1 P | 3.00% | 1.60% |

| 12:30 | USD | Goods Trade Balance (USD) Mar P | -91.2B | -90.3B |

| 12:30 | USD | Wholesale Inventories Mar P | 0.20% | 0.50% |

| 14:00 | USD | Pending Home Sales M/M Mar | 0.90% | 1.60% |

| 14:30 | USD | Natural Gas Storage | 50B | |

| 23:01 | GBP | GfK Consumer Confidence Apr | -20 | -21 |

| 23:30 | JPY | Tokyo CPI Y/Y Apr | 2.60% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Apr | 2.20% | 2.40% |

| 23:30 | JPY | Tokyo CPI ex Food & Energy Y/Y Apr | 2.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | EUR | Germany GfK Consumer Confidence May | |

| Forecast: -25.5 | Previous: -27.4 | ||

| 08:00 | EUR | ECB Economic Bulletin | |

| Forecast: | Previous: | ||

| 12:30 | USD | Initial Jobless Claims (Apr 19) | |

| Forecast: 210K | Previous: 212K | ||

| 12:30 | USD | GDP Annualized Q1 P | |

| Forecast: 2.10% | Previous: 3.40% | ||

| 12:30 | USD | GDP Price Index Q1 P | |

| Forecast: 3.00% | Previous: 1.60% | ||

| 12:30 | USD | Goods Trade Balance (USD) Mar P | |

| Forecast: -91.2B | Previous: -90.3B | ||

| 12:30 | USD | Wholesale Inventories Mar P | |

| Forecast: 0.20% | Previous: 0.50% | ||

| 14:00 | USD | Pending Home Sales M/M Mar | |

| Forecast: 0.90% | Previous: 1.60% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 50B | ||

| 23:01 | GBP | GfK Consumer Confidence Apr | |

| Forecast: -20 | Previous: -21 | ||

| 23:30 | JPY | Tokyo CPI Y/Y Apr | |

| Forecast: | Previous: 2.60% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Apr | |

| Forecast: 2.20% | Previous: 2.40% | ||

| 23:30 | JPY | Tokyo CPI ex Food & Energy Y/Y Apr | |

| Forecast: | Previous: 2.90% | ||

Friday, Apr 26, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| JPY | BoJ Interest Rate Decision | 0.10% | 0.10% | |

| 01:30 | AUD | Import Price Index Q/Q Q1 | 1.10% | |

| 01:30 | AUD | PPI Q/Q Q1 | 0.90% | |

| 01:30 | AUD | PPI Y/Y Q1 | 4.10% | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Mar | 0.50% | 0.40% |

| 12:30 | USD | Personal Income M/M Mar | 0.50% | 0.30% |

| 12:30 | USD | Personal Spending Mar | 0.30% | 0.80% |

| 12:30 | USD | PCE Price Index M/M Mar | 0.30% | 0.30% |

| 12:30 | USD | PCE Price Index Y/Y Mar | 2.50% | |

| 12:30 | USD | Core PCE Price Index M/M Mar | 0.30% | 0.30% |

| 12:30 | USD | Core PCE Price Index Y/Y Mar | 2.80% | |

| 14:00 | USD | Michigan Consumer Sentiment Index Apr F | 77.9 | 77.9 |

| GMT | Ccy | Events | |

|---|---|---|---|

| JPY | BoJ Interest Rate Decision | ||

| Forecast: 0.10% | Previous: 0.10% | ||

| 01:30 | AUD | Import Price Index Q/Q Q1 | |

| Forecast: | Previous: 1.10% | ||

| 01:30 | AUD | PPI Q/Q Q1 | |

| Forecast: | Previous: 0.90% | ||

| 01:30 | AUD | PPI Y/Y Q1 | |

| Forecast: | Previous: 4.10% | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Mar | |

| Forecast: 0.50% | Previous: 0.40% | ||

| 12:30 | USD | Personal Income M/M Mar | |

| Forecast: 0.50% | Previous: 0.30% | ||

| 12:30 | USD | Personal Spending Mar | |

| Forecast: 0.30% | Previous: 0.80% | ||

| 12:30 | USD | PCE Price Index M/M Mar | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 12:30 | USD | PCE Price Index Y/Y Mar | |

| Forecast: | Previous: 2.50% | ||

| 12:30 | USD | Core PCE Price Index M/M Mar | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Mar | |

| Forecast: | Previous: 2.80% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Apr F | |

| Forecast: 77.9 | Previous: 77.9 | ||

The Weekly Bottom Line: Dialing Back Expectations

U.S. Highlights

- U.S. headline retail sales beat expectations in March, advancing for a second consecutive month. The strong showing bolstered the case for a delayed start to the Fed’s interest rate cutting cycle.

- Comments from senior Federal Reserve officials has the timing of possible interest rate cuts in question amid signs of persistent strength in the U.S. economy and higher-than-anticipated inflation.

- In contrast, the housing market continues to feel the weight of higher interest rates as housing starts and home sales dipped in March.

Canadian Highlights

- The federal government took the stage this week as it presented a beefed-up budget, with a focus on addressing housing affordability.

- Canadian CPI inflation also made headlines with an encouraging print, which saw core inflation rates move further towards the Bank of Canada’s (BoC) target.

- Market expectations for the first BoC interest rate cut continued to solidify around June or July, increasing the probability that it will move ahead of the Fed.

U.S. – Dialing Back Expectations

This week featured releases on retail sales and the housing market in March. Also high on the market’s radar were comments made by the Federal Reserve Chair, which suggested the central bank may be changing its tune on the path and timing of interest rate cuts. Overall, markets responded strongly to the new information with stocks heading lower and treasury yields rising (10 year yields were up 9 basis points at time of writing) as investors recalibrated their expectations for rate cuts this year.

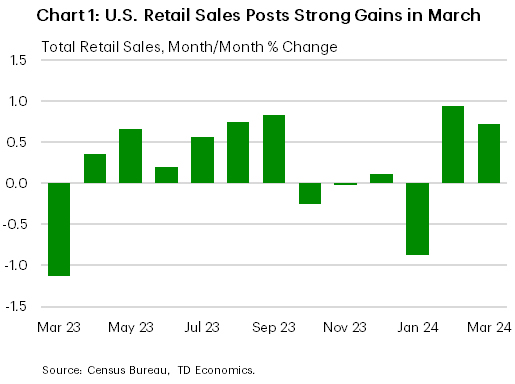

A stronger-than-expected gain in retail sales in March reinforced that the U.S. economy is still strong, and is expected to lead growth among developed countries this year, according to recent IMF projections. Headline retail sales rose for a second consecutive month in March, after a string of monthly declines, with sales in the key control group acting as a driver (Chart 1). Given the soft start to the year, March’s increase just managed to lift the quarter into positive territory (up 0.2% q/q annualized). The notable uptick also represents an upside risk to our own forecast for 2024 Q1 consumer spending, and doesn’t help the Fed in its goal of taming price growth.

On Tuesday, the Federal Reserve Chairman and the Vice Chair at two separate events both signaled that the central bank may be changing its tune. While policymakers started the year anticipating that they would commence the rate cutting cycle soon, hotter-than-expected inflation has shifted that calculus. In a prepared remark, Vice Chair Jefferson noted that interest rates could remain at their current restrictive level for longer if inflation persisted. Later, Fed Chair Powell echoed that sentiment. He noted that excluding a sudden economic slowdown, interest rates would need to stay restrictive for longer. The Fed Chair’s new tone is essentially one of dialing back expectations as markets had aggressively priced in numerous cuts this year. Investors on average are now expecting one and two cuts.

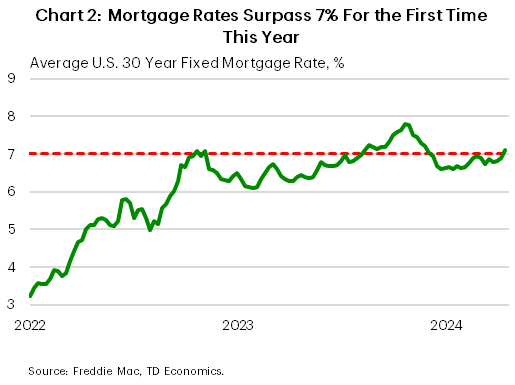

Higher rates are having a measurable effect on the housing market as data on existing home sales and housing starts and permits all declined in March. Both housing starts and building permits retrenched in March. In another release, existing home sales fell 4.3% m/m in March – the largest decline in over a year. While the measure managed to post a gain for the first quarter as a whole, relative to the subdued levels in 2023 Q4, the prospect of higher for longer interest rates are likely to see these gains pared back in the future. In fact, this week, the average rate on a 30-year fixed rate mortgage climbed above 7% for the first time this year and is likely to weigh on housing activity going forward (Chart 2).

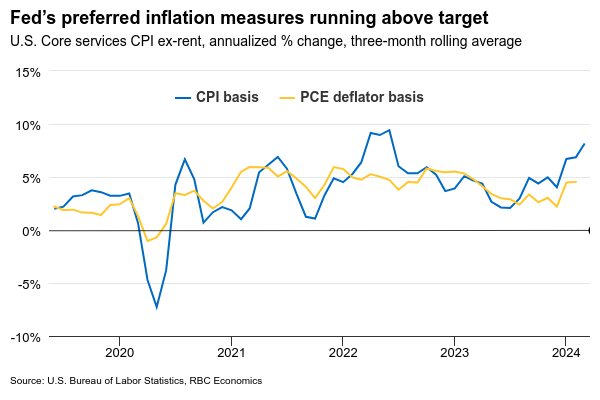

Given recent readings on inflation and retail spending, and FOMC members comments acknowledging that rates will likely need to remain restrictive for longer, next week’s consumer spending and income data for March are highly anticipated. In particular, the Fed’s preferred inflation metric – the core PCE deflator – will be very closely watched to see how much of the recent hot CPI inflation carries over to PCE.

Canada – Another Big Budget for the Liberals

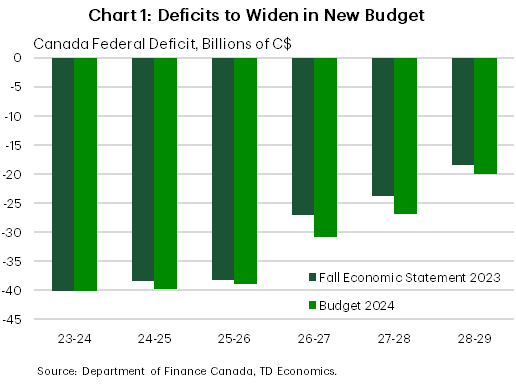

The federal government took the stage this week as it presented a beefed-up budget full of new spending promises. The government was applauded for making strides to address the country’s housing shortage but is also taking heat for hiking taxes via a new capital gains inclusion rate. Canadian CPI inflation made headlines too, with an encouraging print that reinforced bets the Bank of Canada (BoC) would initiate its first cut in June or July.

The Liberal government spent the better part of the last few weeks touring the country marketing its housing plan, which was fully unveiled in Budget 2024. This is one of the biggest pieces of housing policy Canada has ever seen, which aims to build nearly 4 million new homes by 2031. Encouragingly, there are also a host of policies to ramp-up rental supply, which has been stretched thin due to the government’s failure to control the rapid growth of Canada’s population. While the government is moving in the right direction, achieving its ambitious goals will be a challenge. Canada is currently on track to build just under 2 million homes over the next eight years, so doubling that will be a tall order for a construction sector that is already bumping up against capacity constraints.

The budget wasn’t just about building new homes. The government announced $53 billion in new spending, with just 16% of that dedicated to housing. Indeed, there were over two hundred new policy items in the budget. There was spending on defence, pharmacare, a disability benefit, money for AI investment, an EV supply chain investment credit, and money aimed towards indigenous reconciliation. This continues a trend where the Liberal government attempts to fill as many gaps as it can through increased spending. Recall that the BoC has previously called out the government’s spending ways for contributing to Canadian inflation.

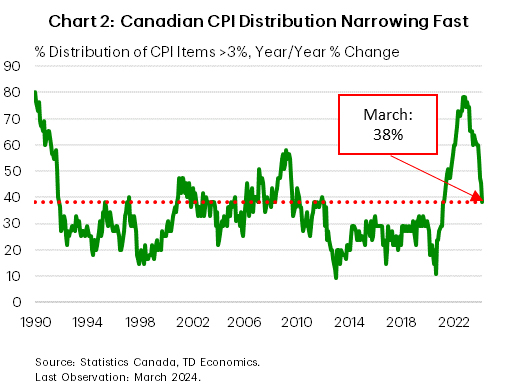

Speaking of inflation, it is not often that a Canadian CPI inflation report takes a backseat, but that’s what happened this week. Importantly, the average of the BoC’s core inflation measures came in at 3.0% year-on-year (down a tenth). On a three-month basis these are averaging just above one percent – a signal that the annual numbers will continue to decelerate in the coming months. This goes to the argument that we have been making for quite some time. That the slowdown in the Canadian economy has set the foundation for lower inflation. We are seeing this play out.

Has the BoC seen enough to cut rates? While we think the inflation evidence is clear, the central bank is taking a patient approach. While economic growth has been weak, the bottom hasn’t fallen out of the economy. This has afforded the Bank extra time to wait-out inflation, ensuring that the recent move is more durable. Notably, markets believe the moment is quickly approaching, with bets narrowing in on the June/July announcement dates. Interestingly, this also means that the BoC is expected to make its move well ahead of the Fed. The loonie has consequently reached it’s lowest level since late 2023 against the greenback.

Weekly Economic & Financial Commentary: Another Week, Another Strong Showing from the U.S. Consumer

Summary

United States: Another Week, Another Strong Showing from the U.S. Consumer

- Robust retail sales data were the main story on the U.S. economic data front this week. Elsewhere, data for industrial production and jobless claims offered additional evidence that the U.S. economy remains on solid footing.

- Next week: New Home Sales (Tue.), GDP (Thu.), Personal Income & Spending (Fri.)

International: Israel-Iran Tensions Come to the Surface

- Recent tension between Israel and Iran shows that finding a steady state in the Israel-Hamas war remains elusive. We continue to believe military conflict will remain contained and not expand into Tehran or the broader Middle East. In England, inflation continues to ease, but perhaps not as quickly as policymakers may have hoped for.

- Next week: Middle East Geopolitical Tensions, India Prime Minister Election (Apr.-Jun.), Central Bank of Turkey (Thu.)

Interest Rate Watch: Will Home Buyers Ever Get Some Relief from Elevated Mortgage Rates?

- The 30-year fixed rate mortgage has risen recently, but it still remains below last autumn's high-water mark of 8%.

Topic of the Week: Steel Your Nerves, Biden Proposes Higher Tariffs on Chinese Imports

- This week, President Biden announced a plan to more than triple tariffs on Chinese aluminum and steel products. As stated in our recent special report, tariffs are often imposed to promote demand for local products and spur domestic production, but the effects of tariffs on Chinese-imported goods have been marginal for U.S. industrial production over the past six years. Will the same hold true with Biden's proposed policy?

U.S. Economy’s Outperformance Carried on into the Start of the Year

The first estimate of U.S. Q1 gross domestic product next Thursday is expected to show another robust increase—extending a long stretch of outperformance in the U.S. economy versus advanced economy peers.

We expect U.S. output to have grown by an annualized 2.3% from Q4 last year, powered by stronger consumer spending and a tick-up in residential investment. But not all sectors of the economy have been faring equally well. Manufacturing production declined for a third straight quarter in Q1. And a pullback in non-residential construction will likely put an end to a string of five consecutive large quarterly increases in structures investment. But U.S. consumers continue to power through headwinds from higher interest rates as they hold onto ultra-long-term mortgages and spend out of savings accumulated during the pandemic. Core retail sales (excluding auto and gasoline stations) contracted mildly in January but rebounded in February and rose by almost 1 percent in March.

The strong U.S. economy is not as much of a concern for the Fed as is the re-emergence of inflation pressures. The tick higher in price growth—after having moderated sharply in 2023—alongside resilient consumer spending has revived likelihood that the economy will need to slow more significantly to get inflation pressures back fully in check. At a forum in Washington D.C. on Tuesday, Fed chair Jerome Powell highlighted a “lack of further progress” with inflation this year and how “it’s appropriate to allow restrictive policy further time to work.” Already, we’ve dialed back our expectation for rate cuts from the Fed this year, and now expect one 25 basis point rate cut in December. That’s also less than the 75 bps of cuts expected this year by the median FOMC policymaker in March. Moving forward, we continue to anticipate that the U.S. economy will start to lose its current momentum over the second half of 2024. But each additional upside surprise on economic growth and labour markets makes it less likely that inflation will resume a downward trend, and raises the risk that interest rates will need to remain higher for longer.

Week ahead data watch

Statistics Canada’s advance indicator showed retail sales edged up 0.1% in February mostly thanks to higher gasoline prices. A rise in unit auto sales (7% seasonally adjusted) points to some upside risk to the early February estimate but would still leave core retail sales (excluding gasoline stations and vehicles) down in February. Early indications for March are soft—auto sales retraced most of their February increase. Our tracking of card transactions also points to a broader pullback in spending in March.

We expect U.S. personal consumption to increase by 0.7% in March, given a robust retail sales increase. Personal income likely grew by 0.6%, echoing an uptick in March’s hourly wages (0.3%) and a 303,000 surge in employment.

February SEPH data will be watched closely for more signs of cooling in the Canadian labour market. Wage growth data will be closed watched, as it has been underperforming the timelier labour force survey data but is more in line with falling job openings, as hiring demand slows.

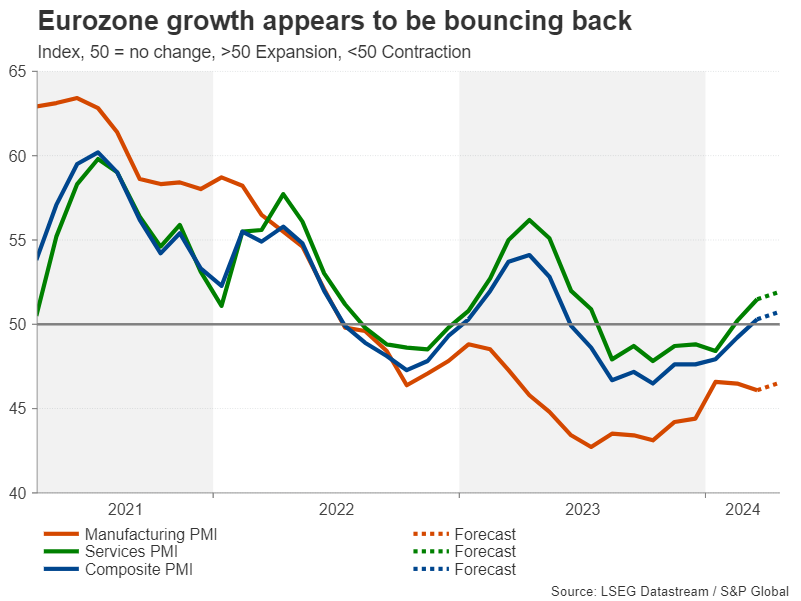

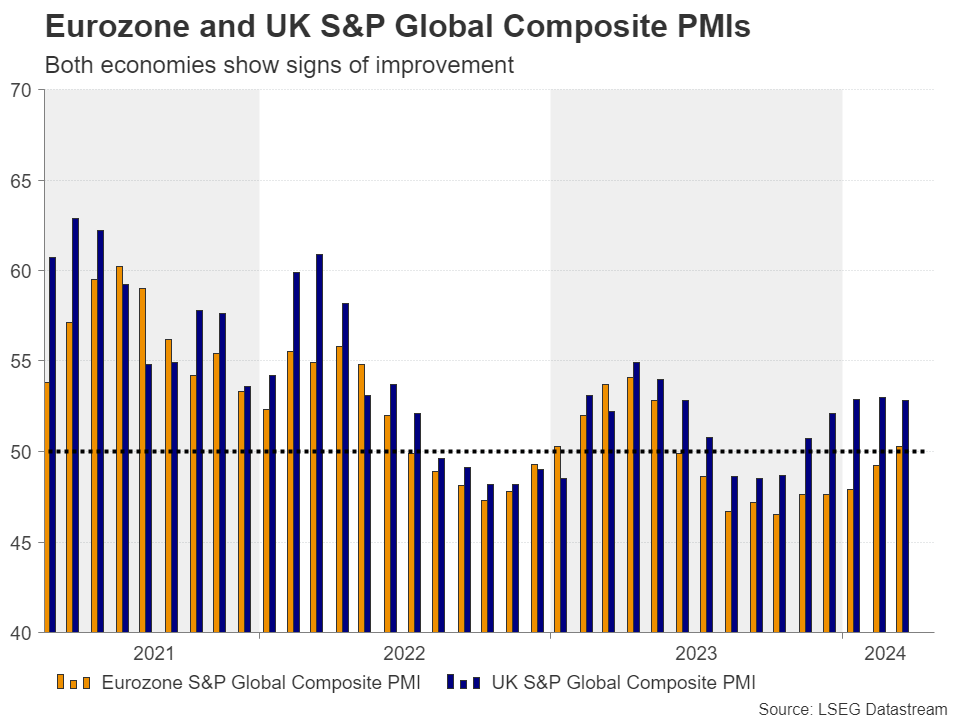

Eurozone PMIs Eyed as Euro’s Focus Turns to Rate Cuts Beyond June

- Eurozone appears to be on the mend but ECB still on track to cut in June

- For the euro, rate outlook beyond June increasingly more important

- Flash PMI readings for April are due on Tuesday, 08:00 GMT

Will PMIs confirm tepid recovery signs?

The euro area economy stagnated in the middle of 2023 but narrowly managed to dodge a technical recession, defined as two consecutive quarters of negative growth. The most recent data have been somewhat more upbeat, and the Eurozone may be turning a corner.

Services activity expanded in the previous two months according to the S&P Global surveys, and while the manufacturing sector remains in deep water, this was enough to lift the overall composite PMI to above 50.0 for the first time since May 2023.

With China’s economic recovery also gaining some traction and the energy crisis fading, there is hope that the pain for Europe’s manufacturers will ease more substantially in the coming months.

Forecasts point to a further pickup in the services PMI to 51.9 and for the manufacturing PMI to have improved to 46.5 in April.

Waiting for the final piece of the jigsaw

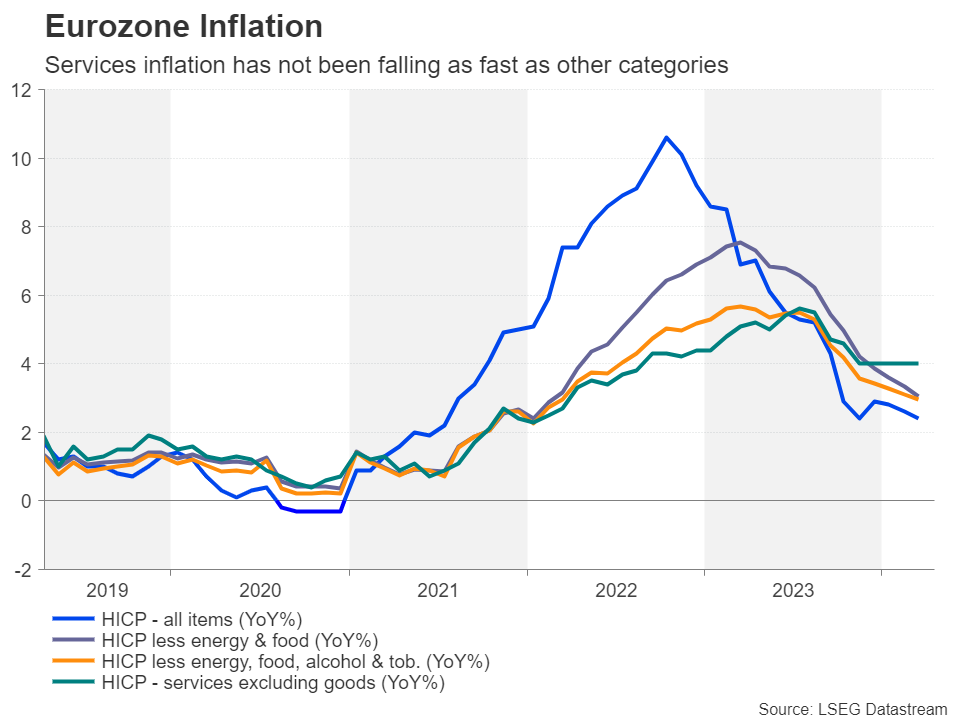

For policymakers at the European Central Bank, the number one concern is of course inflation, and on that front, things are also looking up. Headline inflation fell to 2.4% in March and underlying measures have been trending lower all year, unlike in the US where progress has been mixed.

Some ECB officials were ready to cut in April, but most Governing Council members including President Lagarde are not yet totally convinced. In particular, services inflation remains problematic, and for policymakers to become more confident that services CPI, currently stuck at 4.0%, won’t become sticky, they would have to see wage pressures cool off.

Services prices tend to be more strongly correlated with wage growth than manufacturing prices so the ECB is awaiting Q1 figures on negotiated wages due at the end of May to get the all clear to cut in June.

Rate cut hopes dealt a setback

In this respect, the PMI numbers won’t pose a hurdle to June rate cut prospects. However, they may shape expectations for the rate path beyond June. Rate cut bets for central banks globally have been scaled back sharply over the past month following the string of strong data out of the US that dented hopes of aggressive Fed easing.

Rate cut expectations for the ECB have been dialled back too, with investors pricing in just under 75 basis points of reductions. Better-than-expected PMI readings would keep a June cut firmly in play but may add to doubts about additional easing later in the year.

Can the euro recoup recent losses?

The euro has been under pressure lately, as the ECB looks set to start taking its foot off the brake before the Fed does. After hitting a five-month low of $1.0599 earlier in the week, the single currency has rebounded to around $1.6050. If the PMI surveys impress, they could help the euro recover further towards the April high of $1.0885.

On the other hand, if there’s a surprise deterioration in the PMIs, the euro is likely to come under renewed pressure, as investors would move to ratchet up their rate cut bets for June, which is not fully priced in, and for the rest of the year. The euro could breach the 78.6% Fibonacci retracement of the October-December upleg at $1.0595 in such a scenario before targeting the October 2023 low of $1.0447.

Hawkish Fed could frustrate ECB doves

In the absence of a bounce back in growth, diverging monetary policy paths between the Fed and ECB could weigh more heavily on the euro in the coming months. But this could pose an upside risk too. If persistent inflation keeps the Fed from cutting rates at all this year, it will be difficult for the ECB to diverge significantly from its US counterpart as that could send the euro plunging.

Meanwhile, markets may also be overlooking the possibility of an economic rebound potentially jeopardizing the ECB’s rate cutting ambitions. In addition, the ongoing threat of a further escalation of tensions in the Middle East is something ECB policymakers are keeping an eye on due to the risk of higher oil prices.

Supercharged US Dollar Turns to GDP Growth Data

- Dollar goes on a rampage as traders unwind Fed rate cut bets

- Risk aversion in stock markets amid Iran tensions helps too

- Upcoming US releases will decide whether rally can go further

Dollar shines bright

It’s been a phenomenal year for the US dollar so far. The greenback has gained more than 4% against a basket of currencies, turbocharged by a series of solid economic readings that have forced investors to dial back bets of imminent Fed rate cuts.

Heavy government spending and a surge in population growth driven by an influx of immigration have helped shield the US economy, bolstering the labor market and consumer demand.

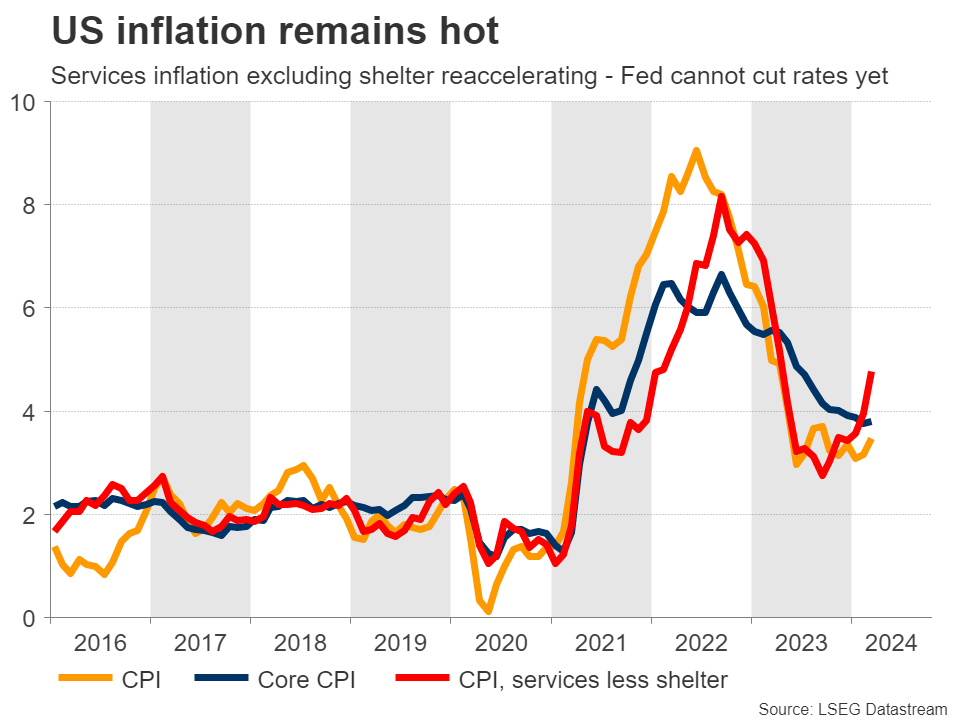

Reflecting this resilience, inflationary pressures have been persistently hot. In fact, some measures of underlying inflation have re-accelerated in recent months, making it extremely difficult for the Fed to cut interest rates.

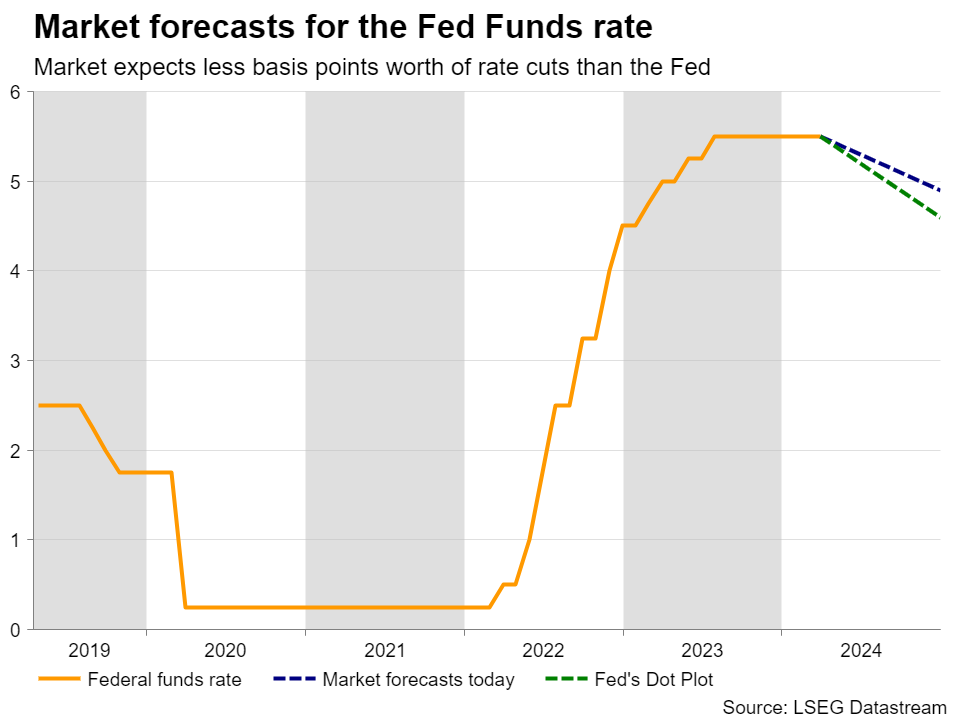

Market pricing now points to less than two rate cuts this year, down from six just a few months ago. Hence, the market is pricing a higher-for-longer scenario for interest rates, which has helped bolster the US dollar.

Beyond that, the latest correction in stock markets and the tensions in the Middle East have further boosted the safe-haven US dollar through the risk sentiment channel.

Barrage of data coming up

Next week’s US data releases could go a long way in deciding whether this rally still has miles left in the tank. The ball will get rolling on Tuesday with the S&P Global business surveys for April, ahead of the latest batch of durable goods orders on Wednesday.

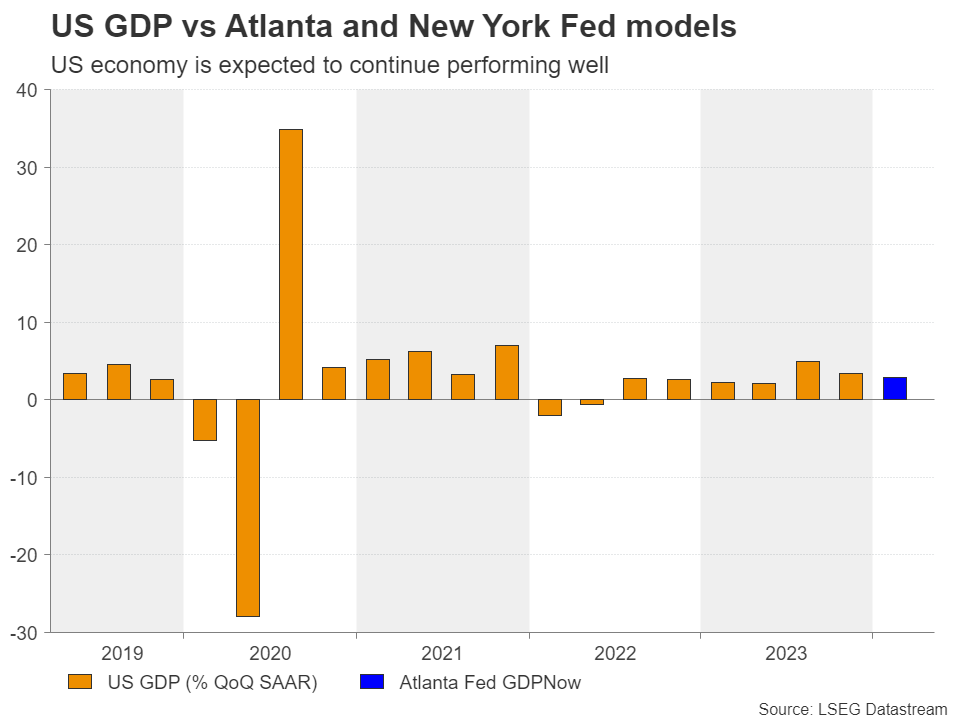

But the main event will probably come on Thursday with the advance estimate of GDP for the first quarter. Economist forecasts suggest the US economy grew by an annualized pace of 2.1% last quarter.

As for any surprises, there is some scope for a stronger-than-expected GDP print, considering that the Atlanta Fed GDPNow model estimates growth at 2.9% instead. This model has a fairly strong track record in predicting GDP surprises, and if this is the case, that could provide more fuel for the dollar.

Taking a look at the euro/dollar chart, the pair has been trading in a narrow range between 1.0690 and 1.0600 for about a week now. A break in either direction will reveal what’s next. More broadly, the price has been in a downtrend since the beginning of the year.

Finally on Friday, the core PCE price index for March will hit the markets, alongside personal consumption and income figures. Forecasts suggest core PCE inflation held steady at 2.8% in annual terms.

That said, this dataset might attract less attention this time, as it will be released after the GDP numbers, which will give investors a sense of how the economy and inflation evolved in March.

Week Ahead – US GDP and BoJ Decision on Top of Next Week’s Agenda

- US GDP, core PCE and PMIs the next tests for the dollar

- Investors await BoJ for guidance about next rate hike

- EU and UK PMIs, as well as Australian CPIs also on tap

- Earnings season heats up as tech giants report

Will US data throw more Fed rate cuts off the table?

The dollar staged a strong recovery the last couple of weeks, with the bulls being encouraged to initiate long positions as soon as the US CPI data revealed that inflation in the world’s largest economy reaccelerated in March.

With several Fed policymakers, including Chair Powell, signaling in the aftermath of the release that there is no urgency to ease monetary policy soon, and with retail sales coming in much stronger than expected on Monday, investors further reduced the amount of rate cuts they expect for this year. They are now expecting interest rates to be lowered by only 42bps, far fewer than the Fed’s own projections of 75.

Attention next week is likely to fall on the first estimate of GDP for Q1 on Thursday, as well as on the core PCE index for March on Friday. The world’s largest economy grew 3.4% q/q SAAR in the last three months of 2023 and according to the Atlanta Fed GDPNow model, it continued to fare strongly, growing by 2.9% in Q1. As for the core PCE index, the Fed’s favorite inflation metric, the stickiness in consumer prices for the month likely tilts the risks to the upside. The preliminary S&P Global PMIs for April are also coming out on Tuesday and market participants will get a glimpse of how the US economy has entered Q2.

Another week packed with strong US data may weigh more on Fed rate cut expectations, and the question could well change from how many basis points could the Fed cut to whether it will cut at all this year. Such a development is is likely to allow the US dollar to continue marching north.

BoJ meets amid intervention alerts

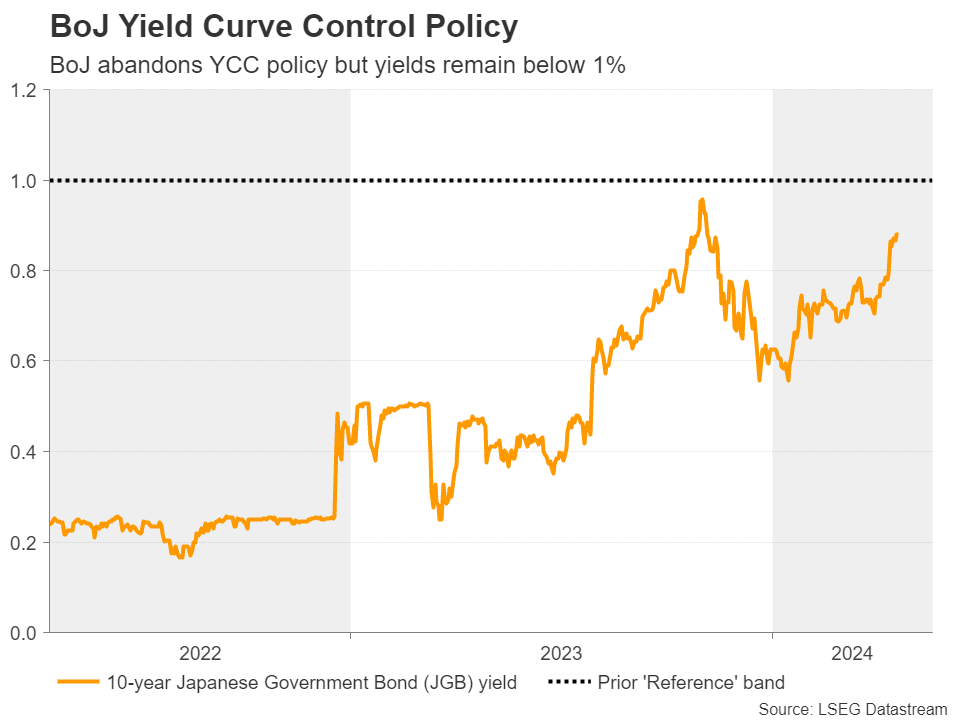

Another major event on next week’s agenda is Friday’s Bank of Japan (BoJ) decision. When they last met, Japanese officials decided to end years of negative interest rates, raising them by 10bps, and abolished its yield curve control policy.

That said, with the Bank saying that they will continue buying bonds with broadly the same amounts as before, and with Governor Ueda noting that they will maintain accommodative policy conditions, investors continued to believe that any subsequent hikes will be very gradual and slow.

Since then, despite the market bringing forward the timing of a second hike and assigning an 86% chance to July, the yen continued to tumble, triggering intense intervention warnings by Japanese officials. That didn’t stop the yen’s slide either, with dollar/yen getting very close to the 155.00 level this week.

Commenting on the yen’s fall, Governor Ueda recently said that the central bank would not directly respond to currency moves, brushing aside speculation that the yen’s tumble could force them to hike sooner, although he added that if inflation continues to accelerate, another hike is likely later this year.

With all that in mind, and with inflation picking up notably since the BoJ’s last gathering, investors may be on the lookout for hints on whether a hike during summer months is indeed more likely now. This means that another dovish appearance could result in further yen selling, increasing dramatically the chances for intervention if Japanese authorities do not step in even before of course.

Traders may get an idea of where inflation is headed in April a few hours ahead of the meeting, when the Tokyo CPIs are scheduled to be released.

Euro and pound traders await PMIs

Apart from the flash S&P Global PMIs for the US, the Eurozone and UK prints will also be released on Tuesday.

At its latest gathering last week, the European Central Bank (ECB) kept interest rates untouched but sent clearer signals that it may start lowering interest rates soon, with reports after the decision saying that policymakers still expect the first quarter-point reduction in June.

As for the Bank of England (BoE), following this week’s better than expected jobs data and the higher-than-forecast inflation prints, a 25bps rate cut is fully priced in for September.

Both the Eurozone and UK economies have been showing some signs of improvement lately, at least according to their recent PMI numbers, but inflation in both areas seems to be headed towards the ECB’s and BoE’s objectives. Thus, even if these releases surprise to the upside, market expectations with regards to the ECB’s and BoE’s actions are unlikely to be dramatically altered and thereby, the euro and the pound are unlikely to stage a strong comeback against the almighty greenback.

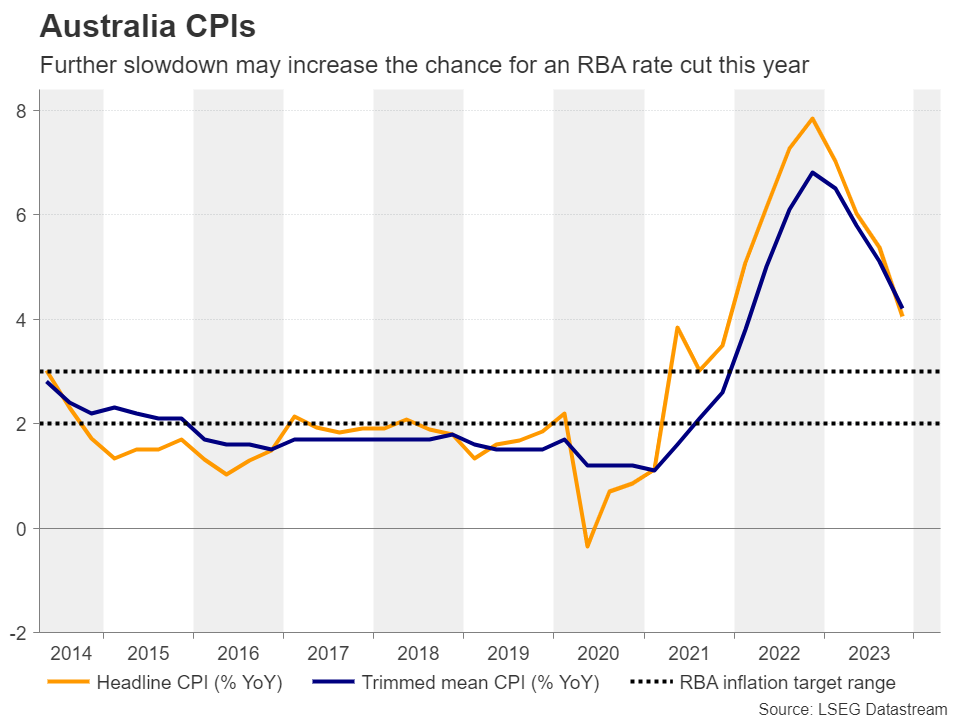

Does Australia’s inflation continue to slow?

In Australia, although there is a nearly 10% chance for a rate cut by the RBA at its upcoming gathering in May, a quarter-point reduction is not fully priced in for this year. With the Bank not giving clear indications of where it may be headed next, aussie traders will pay close attention to Wednesday’s CPI data for signs of whether inflation continues to slow.

The monthly seasonally adjusted y/y rate rebounded somewhat in March, but this was after it declined notably in February from January, which means that, overall, inflation may have continued cooling in Q1. This could increase the likelihood for a 25bps RBA rate cut by December.

Tech earnings enter the spotlight as well

On Wall Street, all three of its major indices have been in a corrective phase lately due to increasing tensions in the Middle East and due to the diminishing Fed rate cut expectations.

That said, besides those two major themes, equity investors are likely to also keep their attention locked on the earnings season as several high-growth tech giants announce their results next week. On Tuesday, the spotlight will fall on Alphabet and Tesla, while on Wednesday, it will be Meta’s turn. On Thursday, the torch will be passed to Microsoft and Amazon.

Weekly Focus – Middle East Situation Remains Tense

Market sentiment has remained volatile throughout the week. Iran's strikes to Israel last weekend sparked uncertainty, which eased gradually through the week, only to be re-ignited by Israel's retaliation last night. The jury is still out on whether this leads to a wider regional escalation, but at the time of writing, Iranian sources have said there is no plan for immediate retaliation. Oil prices are still below levels seen a week ago, equity markets are down, and government bond yields are relatively little changed despite the volatility.

On Saturday, US congress will vote on new support measures for Israel, Ukraine and Taiwan. House speaker Mike Johnson has blocked the bills from a vote on the House floor for months, but the Iran's attack seemed to spark a bipartisan sense of urgency. As some of the hardline House republicans still oppose the measures, Johnson turned to democrats for support by including humanitarian aid to Gaza as part of the package. As such, the bills advanced through the House Rules Committee on Thursday with all democrat members voting in favour. The move is politically risky for Johnson himself, but good news for Ukraine. We do not yet know if Israel's latest strikes will affect the discussions in any way, but as a base case, we expect the bills to pass the final vote over the weekend.

While the past week was light in terms of macro data, the releases were generally on the strong side. US retail sales grew more than expected in March, as control group sales edged up by 1.1% m/m SA (Feb +0.3%). That said, more favourable seasonal adjustment factor and declines seen in sales of some of the 'big ticket' categories spark questions about the strength of the underlying trend. While US macro data shows few signs of cooling, we still remain optimistic that disinflation can continue towards the latter half of the year, with the Fed cutting rates three times this year, see Reading the Markets USD - Supply-driven growth can still rhyme with disinflation, 16 April.

Chinese Q1 GDP growth also exceeded expectations at 5.3% y/y (Q4 5.2%), although the latest March data for retail sales was disappointing. In our view, the data remains consistent with the Chinese economy 'muddling through' its latest challenges. There are some rays of light in the horizon for example on the housing sector, but growth in consumption and credit remains moderate at best despite the stimulus.

Next week, the main data focus will be on preliminary PMI data for April, as markets gauge strength of the economies at the beginning of Q2. While winter brought welcome news of recovery in the global manufacturing cycle, the latest leading signals point towards tentative signs of a peak in H2. In addition, the latest upticks in oil and industrial metal prices are set to dampen demand going forward. We discussed the outlook this week in Research Global - Manufacturing recovery to continue into the summer, 15 April.

We expect the Bank of Japan (BoJ) to stay put on the policy meeting ending early Friday after they made the decisive move to hike the policy rate out of negative territory in March. BoJ will present its new economic projections up to 2026, and focus will naturally be on the expected persistence of inflation after the recent range of solid wage growth indications. We expect BoJ to hike rates one more time this year, most likely in the July meetings.

Sunset Market Commentary

Markets

The impact of this morning’s “limited” Israeli retaliatory attacks against Iran gradually waned throughout today’s trading session. Initial flows all changed course. Some examples: US yields are currently up to 3 bps lower compared to over 10 bps during (illiquid) Asian trading hours. Brent crude surged from $87/b to almost $91/b before returning to the starting position. EUR/CHF yo-yoed from 0.97 to 0.9565 and back. Today’s empty eco calendar in the EMU and the US obviously couldn’t entice. Luckily, some ECB governors hit the wires to entertain us. The way they close ranks on a 25 bps rate cut in June contrasts with the diverging views for H2 2024. ECB Kazaks says that it’s too soon to declare inflation victory. He acknowledges that the ECB does take the Fed into account, even though the central bank has its own mandate. ECB Vasle earlier this week suggested that ECB and Fed policy can diverge (short term) but that they can’t continue running async. ECB Holzmann put it into numbers yesterday. If the Fed ends up keeping policy rates stable this year, the ECB can’t go along cutting rates 3 or 4 times. ECB Vucjic joined the choir, saying that the ECB can move first but that Fed divergence would be felt. He also warned for the bumpy inflation path ahead. Base effects will cause the disinflation process to a virtual stand-still while higher energy (or commodity prices in general) have the potential to move the monthly inflation pace. On the other sides of the aisle are the likes of Maltese ECB governor Scicluna who grabbed dovish headlines by suggesting to cut at a 50 bps (!) pace should inflation move back below 2%. Good luck with that. ECB President Lagarde reiterated on the sidelines of the IMF-gathering in Washington that Frankfurt won’t pre-commit to a specific rate path. Risks to the inflation outlook are two-sided, she added. In its March projections, the ECB put forward 2.3% average inflation for this year, 2% in 2025 and 1.9% in 2026. Upside risks around this trajectory include geopolitics (and their impact on oil prices; ECB took into account average price for Brent crude <$80/b), wages (sticky 4.46% Y/Y in Q4 with Q1 2023-figure to be released mid-May) and more resilient profit margins at companies as consumption holds up given high employment levels. Downside risks include a smoother transmission mechanism and an unexpected deterioration in the economy. European rate markets gradually come to terms with the fact that follow-up rate cuts after June are not a given. You see a repricing away from 3 or 4 cuts this year to 2 or 3 tops. The front end of the curve underperforms with German yields adding up to 4 bps (2-yr) and setting a new YTD high at that tenor. The 10-yr yield rises by 1.3 bps to test resistance at 2.52%. The euro gets some reprieve from today’s rate dynamics, with the pair rebounding from 1.0610 to 1.0670.

News & Views

Belgium’s budget deficit widened significantly in 2023, the National Bank of Belgium reported in a press release today. The increase from 3.6% in 2022 to 4.4% last year pushed up the debt ratio to 105.2% of GDP (+0.9%pt vs 2022) and came despite the phasing out of temporary factors linked to the pandemic and the energy and Ukraine crises. The NBB tied the deepening deficit to a marked rise in public spending (a.o. after lifting the minimum benefit levels) as well as the structural increase in costs associated with population ageing, rising interest rates and the automatic indexation of social benefits and public sector salaries. Primary expenditure (ex. interest payments) picked up again as a result to 52.6% of GDP after two years of declines. The interest burden rose from 1.6% to 2% of GDP. The rise in the budget deficit reflected a widening of the deficit at both the federal level, by €6.8 billion to €20.6 billion, and the level of the communities and regions, by €2.0 billion to €7.1 billion. Breaking down the latter, the Flemish Community printed a €2.8 billion deficit, the Walloon region €2.2 billion and the Brussels-Capital region €1.5 billion. Each saw their debt-to-revenue ratio rise to 52%, 204% and 205% respectively.

Slovakia tapped bond markets outside the euro area for the first time in a decade. It sold a total of CHF635 million in 4-year and 10-year notes yesterday. Speaking to Bloomberg afterwards, the country’s debt chief Bytcanek said there are plans for further issuance in Swiss francs and possibly the dollar (next year) for the sake of diversification. Growing financing needs combined with rising yields on its euro-denominated bonds and the ECB offloading its bloated bond portfolio have at least as much pushed the country to explore ex-EMU markets. Slovakia is on track to record the highest budget shortfall in the EU with government estimates amounting to 6% of GDP. In absolute terms, debt repayments and projected deficits for the current and forthcoming years are estimated at some €10bn annually.

Euro Edges Higher, ECB Eyes June Cut

Euro recovers after dip

The euro fell as much as 0.30% earlier but has recovered and edged higher. In the North American session, EUR/USD is trading at 1.0666, up 0.21%. The euro remains under pressure from the strong US dollar. Last week, EUR/USD fell 1.8% and dropped as low as 1.0601 this week, its lowest level since early November.

The data cupboard is bare today, with no US releases and only one event in the eurozone. German PPI dropped 2.9% y/y in March, marking a ninth straight month of producer deflation.

ECB poised to lower rates in June

With consumer inflation falling in the eurozone, European Central Bank policy makers have been signaling that a rate cut could be coming in June. The ECB doubled down on that message on Thursday. ECB Vice President Luis de Guindos and Governing Council member Francois Villeroy stated clearly that the central bank was poised to cut rates at the June meeting.

What is less certain is whether the ECB will lower rates in July as well. The markets have priced in cuts in June, September and December. The ECB has kept the deposit rate unchanged at 4.5% for five consecutive times, including at last week’s meeting. The rate statement said that a rate cut would be “appropriate” provided that the ECB remained confident that inflation was falling back to the 2% target.

The ECB has been cautious about committing to a rate cut, concerned that lowering rates too soon might allow inflation to rebound and force the central bank to zig-zag and raise rates. Inflation has been moving lower, although there are new worries that the fighting between Israel and Iran could cause a jump in oil prices which would lead to higher inflation.

EUR/USD Technical

Taking a look at the weekly support and resistance lines, EUR/USD remained rangebound this week:

- There is resistance at 1.0716 and 1.0810

- 1.0548 and 1.0454 are providing support