Sample Category Title

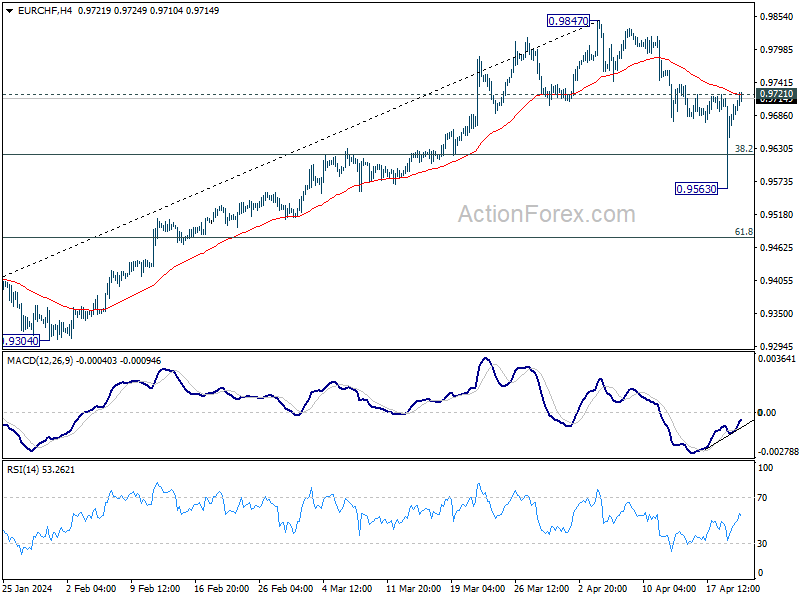

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9606; (P) 0.9662; (R1) 0.9758; More...

Intraday bias in EUR/CHF remains neutral at this point. On the upside, firm break of 0.9721 resistance will argue that correction from 0.9847 has completed already, and turn intraday bias back to the upside for retesting 0.9847. However, break of 0.9563 will bring deeper fall to 61.8% retracement of 0.9252 to 0.9847 at 0.9479.

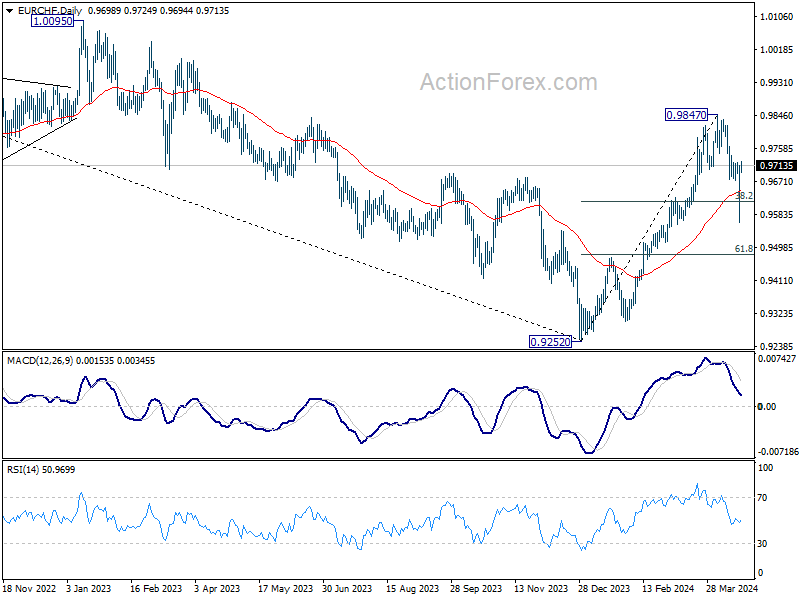

In the bigger picture, while 55 D EMA (now at 0.9644) was breached, EUR/CHF rebounded strongly since then. Rise from 0.9252 medium term bottom should still be in progress. Break of 0.9847 will target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004. however, sustained trading below 55 D EMA will argue that the rebound has completed.

Germany’s BDI expects production decline and stagnant exports this year

Germany's industrial sector continues to faces another challenging year ahead, with Federation of German Industries (BDI) issuing a warning about the downturn in industrial production and the stagnation of exports for 2024. According to BDI's latest forecasts, industrial production is anticipated to drop by -1.5% this year. Additionally, exports are expected to remain flat.

BDI President Siegfried Russwurm highlighted the persistent struggles of the German industry, which has not fully recovered from "cost and demand shocks," driven by spikes in energy prices and inflation pressures.

Russwurm expressed concern over the long-term trend, noting that, despite some signs of a moderate recovery, the "overall production figures" have been following a "worrying downward trend" for several years.

Sterling Finally Snapped. Speech by BoE Ramsden the Straw that Broke the Camel’s Back.

Markets

Sterling finally snapped. A speech by Bank of England Ramsden was the straw that broke the camel’s back. He referred amongst others to the April CPI figure which will likely show the UK converging with the EU. Earlier last week, Bank of England governor Bailey also referred to that number which might even (temporarily) dip to/below the BoE’s 2% inflation target. Bailey’s comments suggested that the BoE would rather team up with the ECB in turning policy less restrictive in the near term than with the Fed which is clearly hinting at higher for longer. Ramsden on Friday added that he has more confidence that inflation persistence is easing with the current restrictive policy stance cutting service inflation. Employment and activity data showed weakness as well last week while the BoE covered the upside (March) CPI surprise with its dovish statements. UK money markets over the past weeks followed the US rather than the EMU example, making them vulnerable to a correction on the BoE’s guidance. UK gilts on Friday outperformed with yields falling 2.1 bps (30-yr) to 10.2 bps (2-yr). Money markets currently discount an inaugural 25 bps rate cut in August, with a second one to be delivered at the end of the year. Loss of interest rate support hurt sterling. EUR/GBP managed a first close outside of the 0.85-0.86 trading range since mid-January. The pair jumped from 0.8558 to 0.8614, taking out 38% retracement on the EUR/GBP-decline from Nov 23 (0.8768) to Feb 24 (0.8493) at 0.8601 in the process. EUR/GBP 0.8665 (62% retracement) is minor next resistance ahead of that 0.8768. Cable (GBP/USD) already fell out of the 2024 sideways trading range on USD-strength (< GBP/USD 1.2519) with the pair closing at a new YTD low of 1.2367. Similar 62% retracement as in EUR/GBP stands at 1.2364, the final support ahead of 1.2037.

Today’s eco calendar won’t move markets with EMU April consumer confidence the sole important release. ECB President Lagarde gives a lecture at Yale university, but she’ll stick to previous comments. On Friday for example she stressed two-sided inflation risk and that the ECB won’t commit to a preset rate path in H2 2024. We saw some underperformance at the front end of the EMU curve on Friday as more governors put (hawkish) risks against a (dovish) rate path for H2. This also gave some temporary support for EUR/USD (1.660). Stock markets remain in correction/sell-on-upticksmode with Nasdaq losing another 2%. On a weekly basis, the tech index fell over 6%.

News & Views

S&P raised the outlook on the Greek BBB- rating from stable to positive, reflecting an expectation that the tight fiscal regime will continue to spur a reduction in the government debt ratio. S&P also expects growth to continue to outperform EMU peers. The New Democracy government after last year’s election outlined and begun implementing a robust reform agenda aimed at unblocking structural bottlenecks. 2023 growth was slightly softer than expected, but at 2% remained relatively healthy. Even so, S&P indicates that fiscal receipts have not softened, increasing by 6.2% last year, due to still high inflation and dividends from fiscal reforms. In the medium term, S&P projects real GDP growth to average 2.4% in 2024-2027, due to a pick-up in investment driven by NextGenEU projects, improved balance sheets of households and the banking system and the fact that the Greek economy is still 22% below its pre-debt crisis peak. Greece could reach the government’s primary budget balance target of 2.1% this year. Public debt which reached a peak level of 207% of GDP in 2020 is expected to fall to about 131% by 2027.

German Finance Minister Lindner on the sidelines of the IMF meeting in Washington said its country is opposed to a new round of joint debt issuance by the EU as members states should maintain responsibility for their own finances. The comments came as other EU members aim for now joint borrowing to finance the energy transition, the shift to the digital economy and a revamp of their militaries to address Russia’s threat. In this respect, Lindner indicated that this opposition is not only a question of getting around objections of the constitutional court on a stricter interpretation of legal limits on government borrowing. Lindner also argued that the results of the EU’s €800bn pandemic recovery fund were mixed and that a repletion of doesn’t seem advisable.

Graphs

GE 10y yield

ECB President Lagarde clearly hinted at a summer (June?) rate cut and seems to have broad backing. EMU disinflation will continue the next two months and bring headline CPI (temporary) at/below the 2% target. Together with weak growth momentum, this gives backing to deliver a first 25 bps rate cut. A more bumpy inflation path in H2 2024 and the Fed’s higher for longer strategy make follow-up move difficult.

US 10y yield

The March dot plot contained several hawkish elements including a symbolically higher neutral rate. In our view they set the stage for a later (September at the earliest) start of a possibly shallower cutting cycle. Upcoming CPI readings (through base effects) and resilient eco data should confirm this. US yields continue to enjoy a solid bottom across the maturity spectrum, setting fresh YTD highs.

EUR/USD

Economic divergence (US > EMU) and a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead pulled EUR/USD towards the YTD low at 1.0695. Stronger-than-expected US March inflation figures forced a technical break, opening the path to last year’s low at 1.0494.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Most BoE members align with the ECB rather than with Fed view, suggesting that the disinflation process provides a window of opportunity to make policy less restrictive (in the near term). Sterling’s downside turned more vulnerable with the topside of the sideways EUR/GBP 0.8493 - 0.8768 trading range serving as the first real technical reference.

Relief Before Earnings

The week starts with a relief rally in equities following a calm weekend on the geopolitical scene. The US 2-year yield pushes above 5% ahead of US GDP and PCE updates. Four of Magnificent 7 are due to report earnings this week.

Oil under pressure following calm weekend

US crude kicks off the week under selling pressure, near the $81.50pb level. But the $80pb psychological level, which also coincides with the major 38.2% Fibonacci retracement on December to April rebound, will likely act as a strong support to the actual retreat as the Middle East tensions could resurface anytime.

But, one thing that could send the price of a barrel below that level is a further fall in rate cut expectations from the Federal Reserve (Fed), and eventually the other central banks. Even though the European Central Bank’s (ECB) Villeroy said that the ECB shouldn’t wait much even though the Mid East tensions drive oil prices higher, there is little chance that the ECB will ignore a potential U-turn in euro area inflation dynamics on the back of surging energy prices and US dollar appreciation.

US two-year yield above 5%.

The strong economic data from the US and hawkish comments from the Fed members closed the door on the expectation of a summer rate cut from the Fed. The US 2-year yield has been testing the 5% level since 10th of April and looks ready to go above this week. The US will reveal the first estimate of Q1 GDP on Thursday and the core PCE price index on Friday. The US economy is expected to have grown 2.5% in Q1 and the core PCE is seen flat on a monthly basis and lower on a yearly basis. Atlanta Fed’s GDPNow forecast points at a first quarter growth of nearly 3% and the last three CPI prints in the US surprised to the upside. Risks to the US economic data remain tilted to the upside.

Is it a bad thing? Robust growth is good news for everyone if inflation continues to slow. Otherwise it’s bad news, because it means that the Fed should try harder to fight inflation by keeping its monetary policy at a sufficiently restrictive level to slow down the economy and eventually push it into recession. Therefore, the combination of growth and inflation will give investors the next indication regarding how far the Fed stands from its first rate hike. Activity on Fed funds futures gives more than 50% for a September rate cut. And because September is too close to November elections, that could delay the first cut to the end of the year. Voila.

All eyes on magnificent seven

The S&P500 and Nasdaq have significantly decoupled from the yields and the Fed expectations since last year as the AI rally fueled optimism in technology stocks and sent these indices to record levels. But the first set of earnings from the most popular chip stocks disappointed last week. Both ASML and TSM reported their Q1 results last week, and both companies failed to satisfy investors despite highlighting that the AI should continue to boost their revenue and profits this year.

This week, 4 of the Magnificent 7 companies will be revealing their Q1 results: Microsoft, Google, Meta and Tesla..

And if the tech stocks can’t boost appetite, the rest of the S&P500 will hard it hard to do so. The S&P500 index is expected to print a 4% earnings decline in Q1 – a decent contrast with the +38% expected for the Magnificent 7. And among the Magnificent 7, Tesla and Apple don’t look promising. So all hopes rely on 5 stocks. 5 stocks will determine where the S&P500 should be headed next.

US House Passes Military Aid Bill to Ukraine, Israel and Taiwan

In focus today

In a relatively quiet start to the week economic data-wise, markets will continue to closely monitor developments in the Middle East. Reports still suggest that Israel's retaliatory attack on Iran on Friday was relatively limited in size and force which alongside Iran's lack of response over the weekend could indicate a de-escalation of the conflict. This has also set the tone in the market opening this morning with price action generally reflecting relief.

In the euro area, focus is on consumer confidence for April today. Consumer confidence has remained stuck at low levels for the past months despite solid fundamentals for household finances. Private consumption has likely remained weak for this reason so an increase in consumer confidence could be a trigger for stronger consumption and thus growth.

Tuesday and Wednesday we look out for business sentiment surveys PMIs from the euro area and Ifo from Germany. Thursday, we receive first estimate of the Q1 GDP from the US. On Friday the Fed's preferred inflation measure PCE is released. Also Friday we get the Tokyo CPI excl. fresh foods for April. We expect the Bank of Japan to keep rates at the current level when they announce their rate decision the night before Friday. We expect the Hungarian Central Bank to announce a 50 bp cut to interest rates on Tuesday.

Economic and market news

What happened over night

In China, the loan prime rates were left unchanged as expected by markets. Chinese rates are on hold for now due to the pressure on the currency and the hawkish signals from the Fed.

What happened over the weekend

In the US, the house of representatives passed a 95 billion USD legislative package providing security assistance to Ukraine, Israel and Taiwan on Saturday. The Senate, controlled by the Democrats, is expected to vote on the bill Tuesday. They are expected to pass it, since they passed a similar measure over two months ago, which the house speaker Mike Johnson denied letting come to a vote in the House, which he finally did on Saturday.

Fed's Golsbee generally considered a dove said progress on inflation has stalled. It merits a pause to allow incoming data to provide more insight into how the economy evolves, he said.

The Oil market quickly calmed down again last Friday. The market was briefly alarmed by the news of Israel's retaliatory bombings in Iran, sending oil prices above USD90/bbl, but it ended the day around USD88/bbl.

Over the weekend, the US Congress passed new sanctions against the Iranian oil industry. Iran's oil production has increased by 600-700kbl per day over the year. If that oil disappears from the market, others will have to replace it, for example, Saudi Arabia, the US will have to sell from its strategic reserves, or the oil price will rise. Initially, we anticipate that the market will take a wait-and-see approach regarding the effect of the new sanctions. The US will likely tread carefully, given that a sharp rise in oil prices would probably be unpopular among voters ahead of the presidential election in November.

In Europe, ECB's Nagel said that the monetary policy needs to remain restrictive even after the first rate cut, and that it is too early to begin to discuss a rate path beyond the June meeting. We see a first rate cut coming in June as close to a done deal.

Equities: Global equities sold off on Friday as investors fled from tech stocks. Global tech lost more than 3% on Friday, while 5 out of 10 sectors managed to book gains, including financials. It is rare to see such a sharp sector rotation where financials, defensive, and small caps are outperforming simultaneously. The S&P 500 dropped 0.9% on Friday, while banks and insurance were the two best-performing industries despite yields ending marginally lower. The S&P 500 equal-weight outperformed MAG 7 by more than 1%, and defensives outperformed cyclicals by 2%. This just illustrates it was not a geopolitical or macro related, but a micro story where investors are questioning tech and AI-related earnings outlook after being disappointed by ASML and Taiwan Semiconductor. In the US on Friday, the Dow was up 0.6%, the S&P 500 was down 0.9%, the Nasdaq was down 2.1%, and the Russell 2000 was up 0.2%.

FI: There are not that many tier-1 economic data or events this week and the focus will still be on the Middle East. 10Y US Treasury yields have stabilised around the 4.6% together with 2Y UST trading around 5%. The key question is whether the market will continue to reprice the Federal Reserve. Previously, there has been good value in buying 2Y Treasuries around 5% given that we do not expect the Federal Reserve to hike rates. We still believe that the 5% level in 2Y and 4.75% in 10Y offer decent value for investors. The Bund ASW-spread has been testing the 35bp-level given the geopolitical uncertainty but has stabilised around 34-35bp level for now. We still expect it to move back to 30bp when the geopolitical uncertainty dampens.

FX: Friday's session was initially characterized by a strong USD and weaker Scandies, however this reversed towards the close and both SEK and NOK ended the day as outperformers within G10, defying the global equity sell-off. At the other end of the spectra, we found GBP following dovish remarks from previous BoE's Ramsden. USD/JPY looks set to start the week trading above 154.

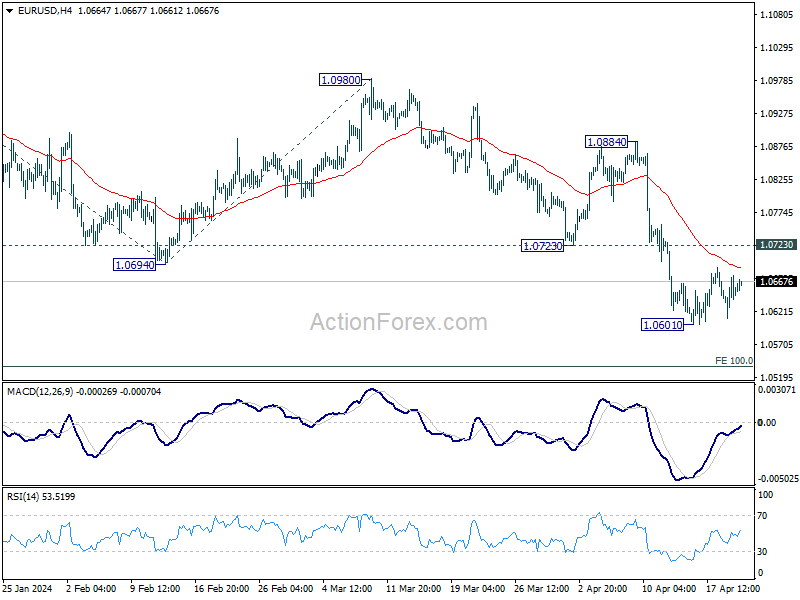

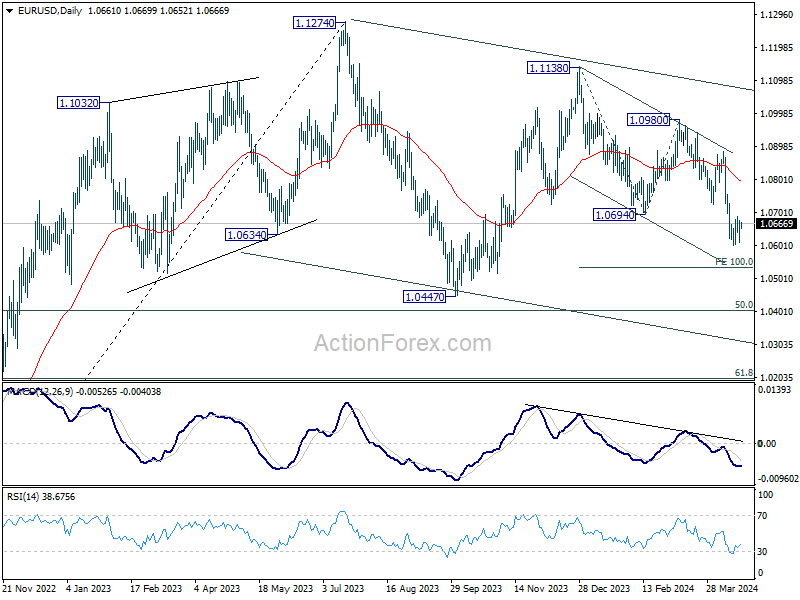

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0618; (P) 1.0648; (R1) 1.0686; More...

Intraday bias in EUR/USD remains neutral and more consolidations could be seen above 1.0601. Upside of recovery should be limited by 1.0723 support turned resistance. Break of 1.0601 will resume the fall from 1.1138 to 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below, Strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

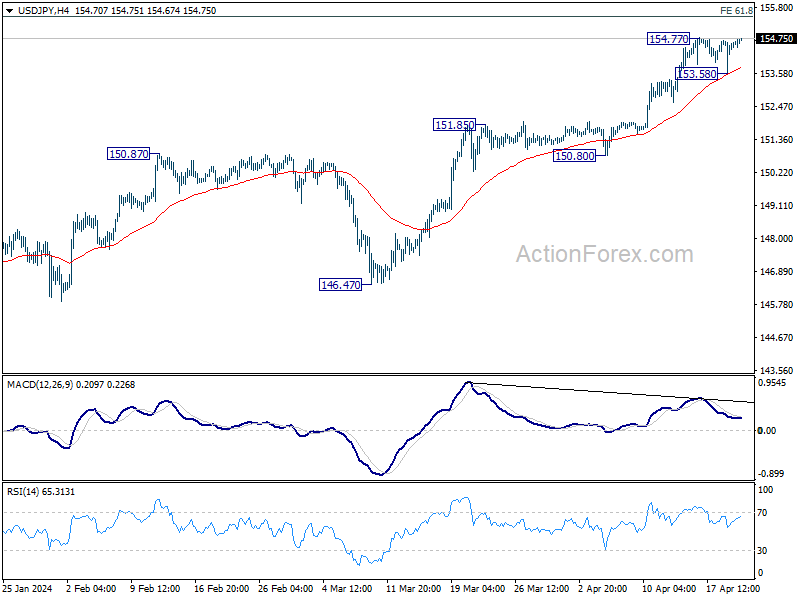

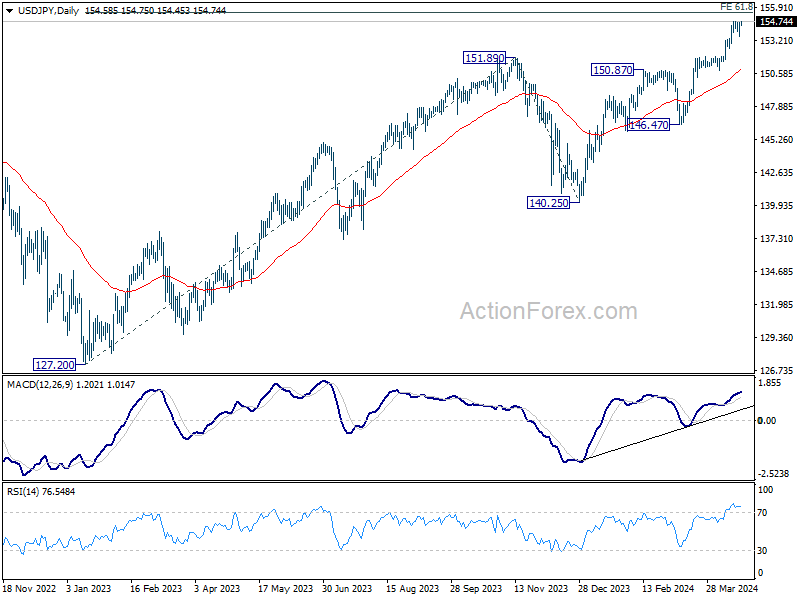

USD/JPY Daily Outlook

Daily Pivots: (S1) 153.93; (P) 154.30; (R1) 155.02; More...

Intraday bias in USD/JPY remains neutral for the moment. On the upside, break of 154.77 will resume larger up trend. But considering bearish divergence condition in 4H MACD, strong resistance should be seen from 155.20 fibonacci level to bring correction on first attempt. On the downside, break of 153.58 will turn bias to the downside, for deeper pull back to 55 D EMA (now at 150.97).

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. Outlook will remain bullish as long as 146.47 support holds, even in case of deep pullback.

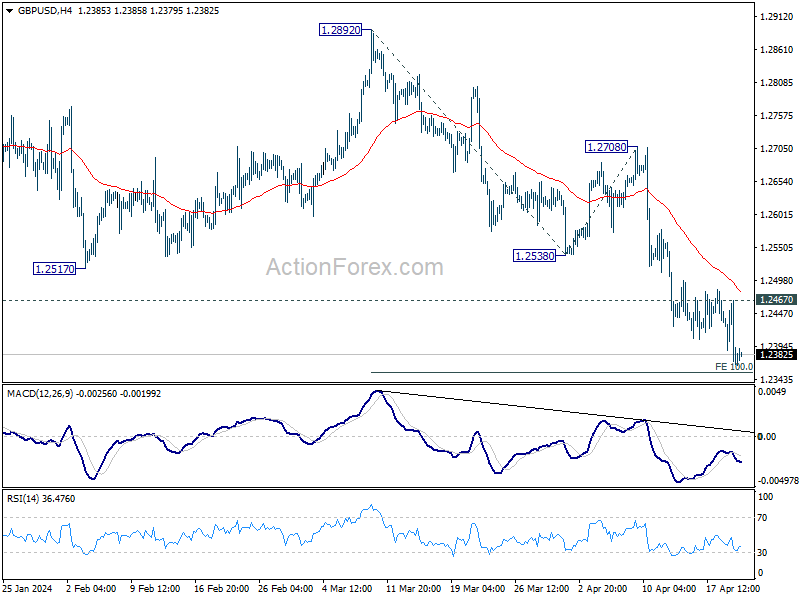

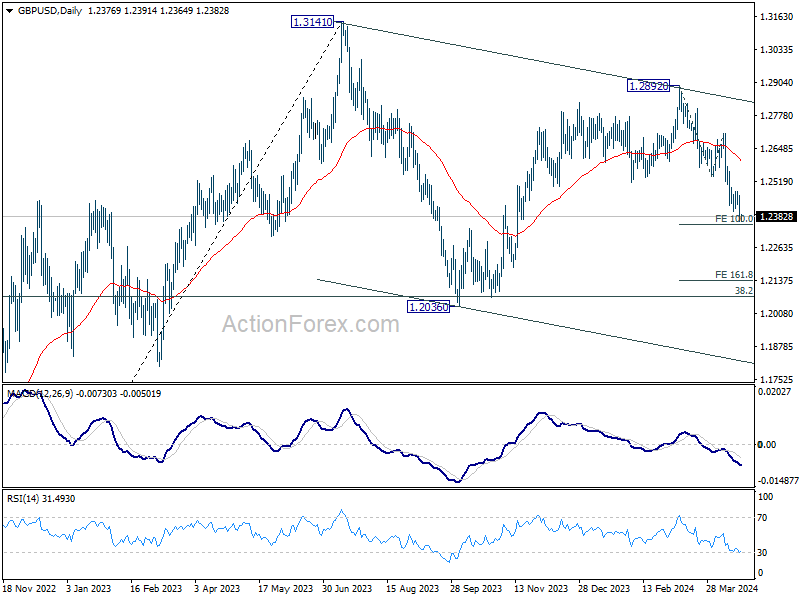

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2336; (P) 1.2402; (R1) 1.2437; More...

Intraday bias in GBP/USD remains on the downside at this point. Decisive break of 100% projection of 1.2892 to 1.2538 from 1.2708 at 1.2354 will extend the fall from 1.2892 to 161.8% projection at 1.2207 next. On the upside, above 1.2467 minor resistance will turn bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Fall from 1.2892 is seen as the third leg. Deeper decline would be seen to 1.2036 support and possibly below. But strong support should emerge from 61.8% retracement of 1.0351 to 1.2452 at 1.1417 to complete the correction.

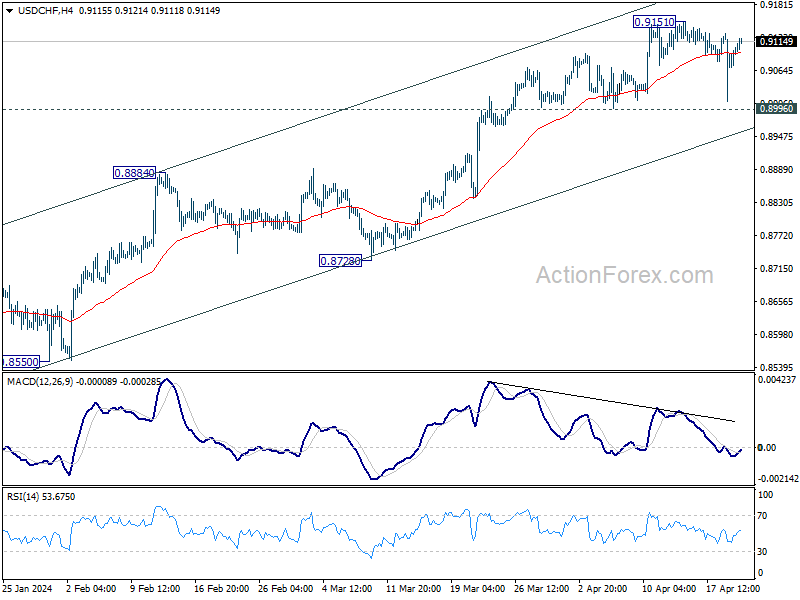

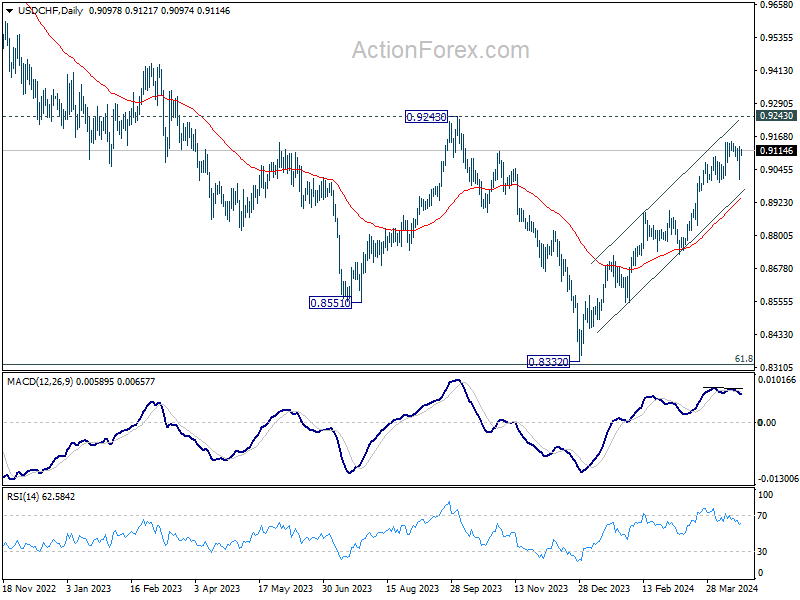

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9032; (P) 0.9084; (R1) 0.9156; More....

Intraday bias in USD/CHF remains neutral as consolidation from 0.9151 is extending. Further rally is expected as long as 0.8996 support holds. Break of 0.9151 will resume the larger rise from 0.8332 to 0.9243 resistance. However, firm break of 0.8996 will turn bias to the downside for 55 D EMA (now at 0.8939).

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish.

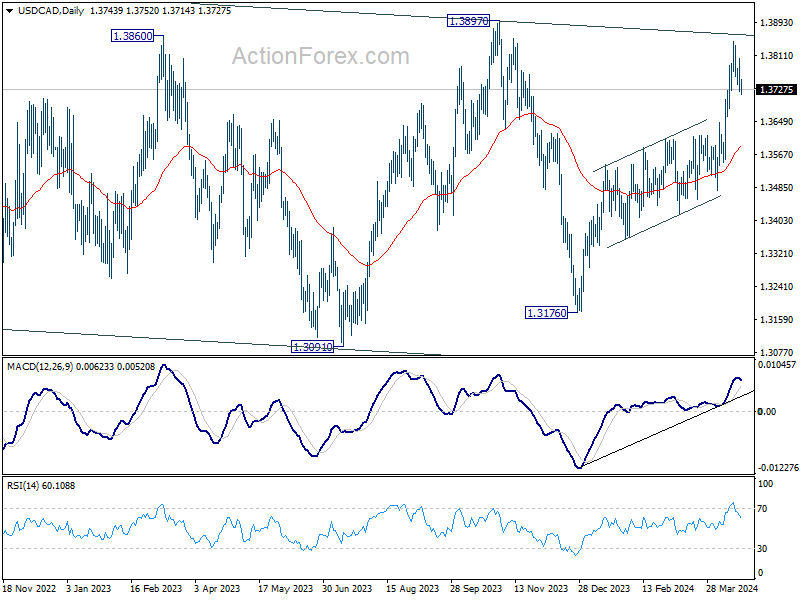

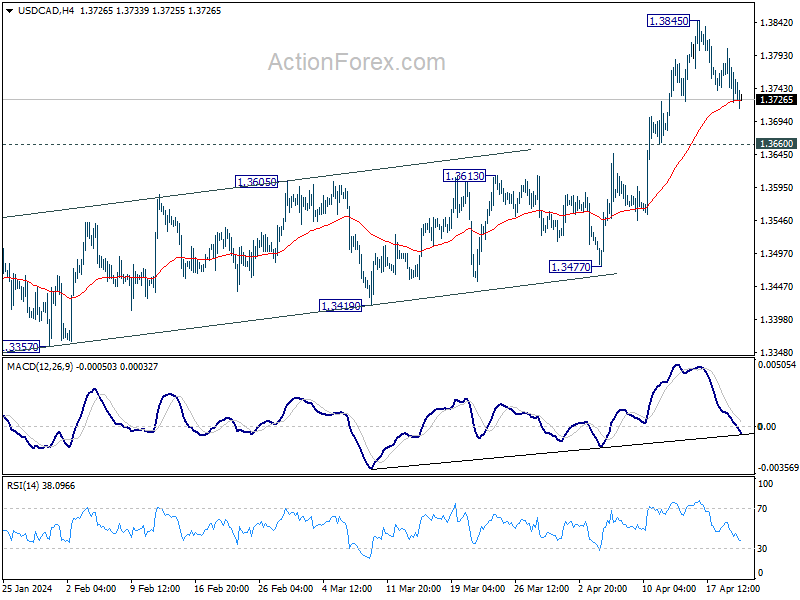

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3714; (P) 1.3760; (R1) 1.3795; More...

Intraday bias in USD/CAD stays neutral at this point. Pull back from 1.3845 could extend lower, but downside should be contained by 1.3660 support to bring another rally. On the upside, firm break of 1.3845 will resume the whole rally from 1.3716 to 1.3976 key resistance.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.