Sample Category Title

Japan’s Suzuki points to US-South Korea trilateral meeting as groundwork for Yen intervention

Japan's Finance Minister Shunichi Suzuki signaled the readiness to address the weakening yen, a pressing issue that has raised substantial concern due to its impact on import costs.

Speaking to the parliament, Suzuki conveyed the unease discussed during last week's trilateral meeting with the US and South Korea. He emphasized the economic strain caused by the depreciating currency, stating there was "strong concern" about how a weak yen inflates the cost of imports, stressing the economy and affecting price levels domestically.

Suzuki's remarks indicated that preparations are underway to counteract Yen's decline. "I won't deny that these developments have laid the groundwork for Japan to take appropriate action," he noted, "though I won't say what that action could be".

BoJ’s Ueda: No preset idea on rate hikes

Addressing the parliament today, BoJ Governor Kazuo Ueda said while changes in inflation projections could necessitate a shift in monetary policy, the BoJ currently has no "preset idea on the specific timing and pace" of rate hikes.

Governor Ueda also reiterated the necessity of maintaining ultra-loose monetary policy for now. He pointed out that trend inflation — price rises driven by domestic demand and assessed through various indicators — is still "somewhat below 2%."

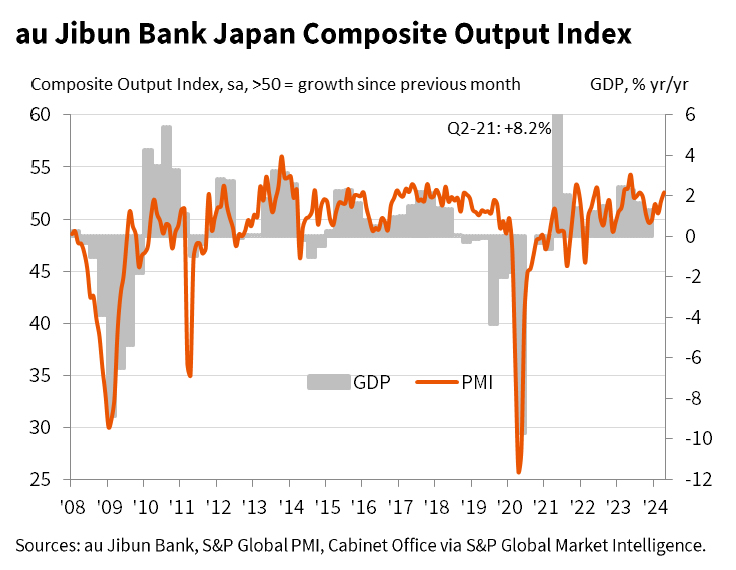

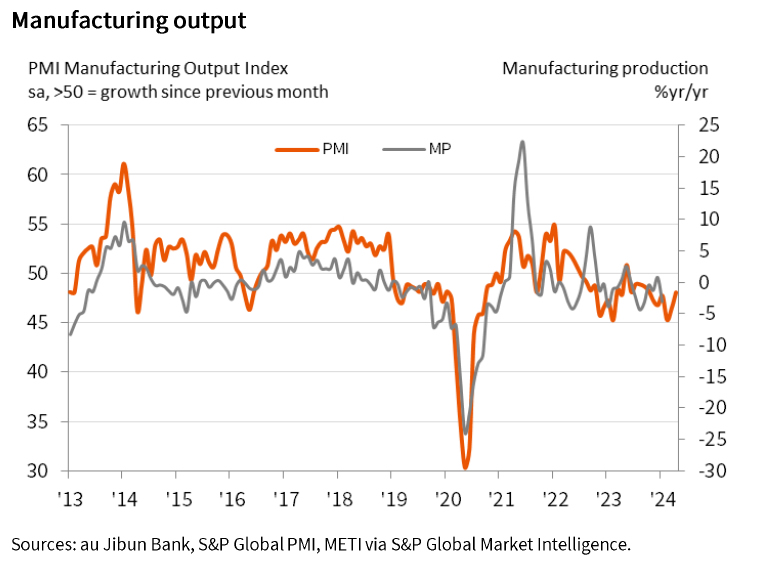

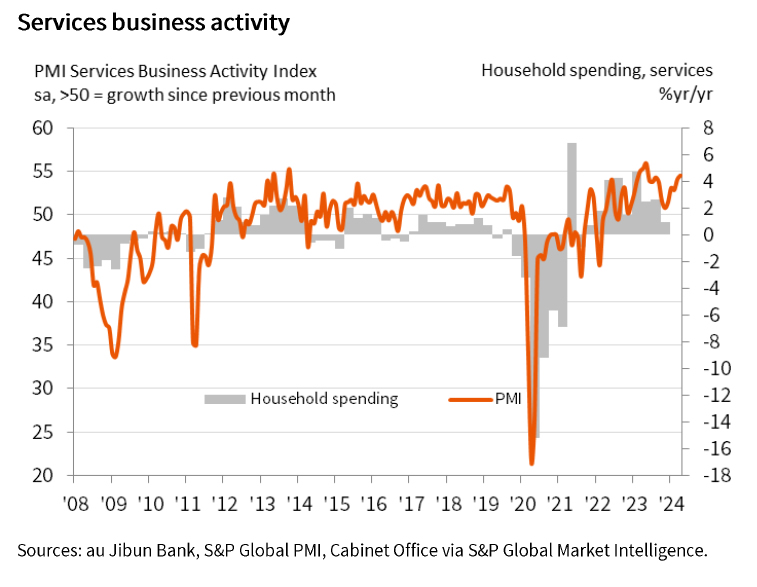

Japan’s PMI Composite climbs to 52.6, weak Yen contributes to intensifying price pressures

Japan's PMI Manufacturing rises from 48.2 to 49.9 in April, above expectation of 48.0, signalling a near-stabilization of manufacturing business conditions. PMI Services rises from 54.1 to 54.6, highest since May 2023. PMI Composite also rose from 51.7 to 52.6, matching the joint-fastest pace set in nearly a year.

Jingyi Pan, Economist Associate Director at S&P Global Market Intelligence, noted that while the service sector continues to be the main driver of growth, there are positive developments in manufacturing as well, where the decline in output has lessened.

April's data, however, also unveiled "additional signs of intensifying price pressures" which were largely attributed to higher input costs inflation affecting both the goods and services sectors.

Notable factors contributing to these rising costs include increased expenses for materials, energy, and wages, with the "weaker Yen having played a significant part as well". Consequently, businesses have been compelled to pass these increased costs onto their clients, resulting in the "fastest increase in average charges in a year."

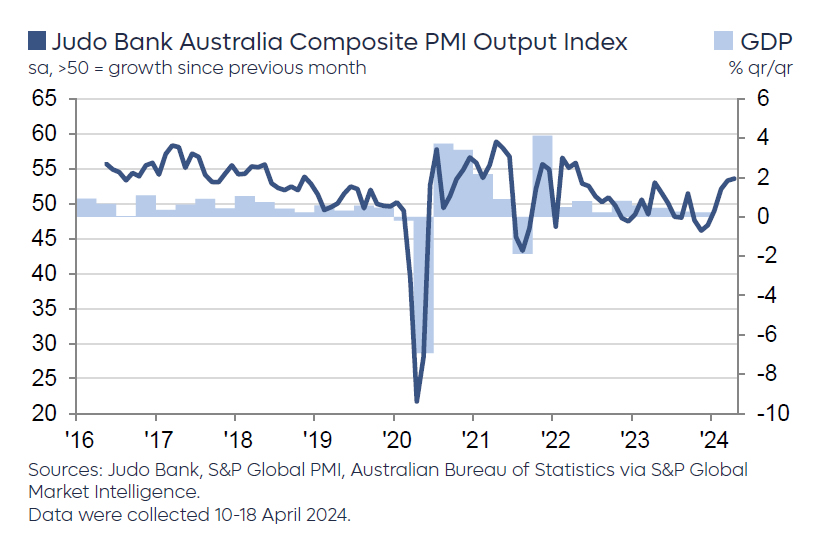

Australia’s PMI Composite rises to 53.6, RBA might hike again in H2

Australia's PMI Manufacturing has nearly reached the neutral mark in April, jumping from 47.3 to 49.9. PMI Services edged higher from 54.2 to 54.4, contributing to PMI's Composite rise from 53.3 to 53.6, marking a 24-month high and indicating the third consecutive month of expansion.

Warren Hogan, Chief Economic Advisor at Judo Bank, said that Composite PMI has averaged 51.5 over Q1, a substantial improvement from 46.9 average in Q4 2023 and correlates with GDP growth of around 0.6% for the March quarter. Hogan suggested that if this trend persists, GDP growth could accelerate to approximately 0.8% in the following quarter.

The results also suggest a cyclical recovery, rebounding from the consumer-led slowdown experienced in 2023. This recovery appears to be more robust than anticipated by RBA, suggesting that the economy is beginning to "wander off their 'narrow path'". This "narrow path" scenario envisages economic activity remaining subdued to ensure inflation eases back to target by late 2025

"The RBA will likely be concerned that a pick-up in activity, before inflation returns to target, could threaten medium to long-term price stability," Hogan added. "These results are inconsistent with interest rate reductions at any stage in the foreseeable future and raise the risk that the RBA may have to start hiking again at some stage over the back half of 2024."

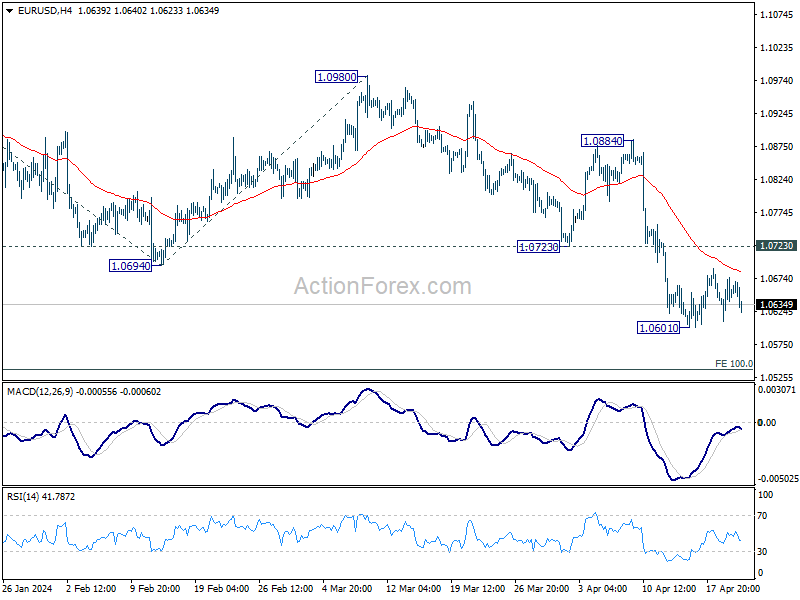

EUR/USD Aims Recovery But Faces Many Hurdles

Key Highlights

- EUR/USD is consolidating losses above the 1.0600 support.

- A key bearish trend line is forming with resistance at 1.0670 on the 4-hour chart.

- GBP/USD extended losses and traded below 1.2420.

- Crude oil prices declined below the $82.50 support zone.

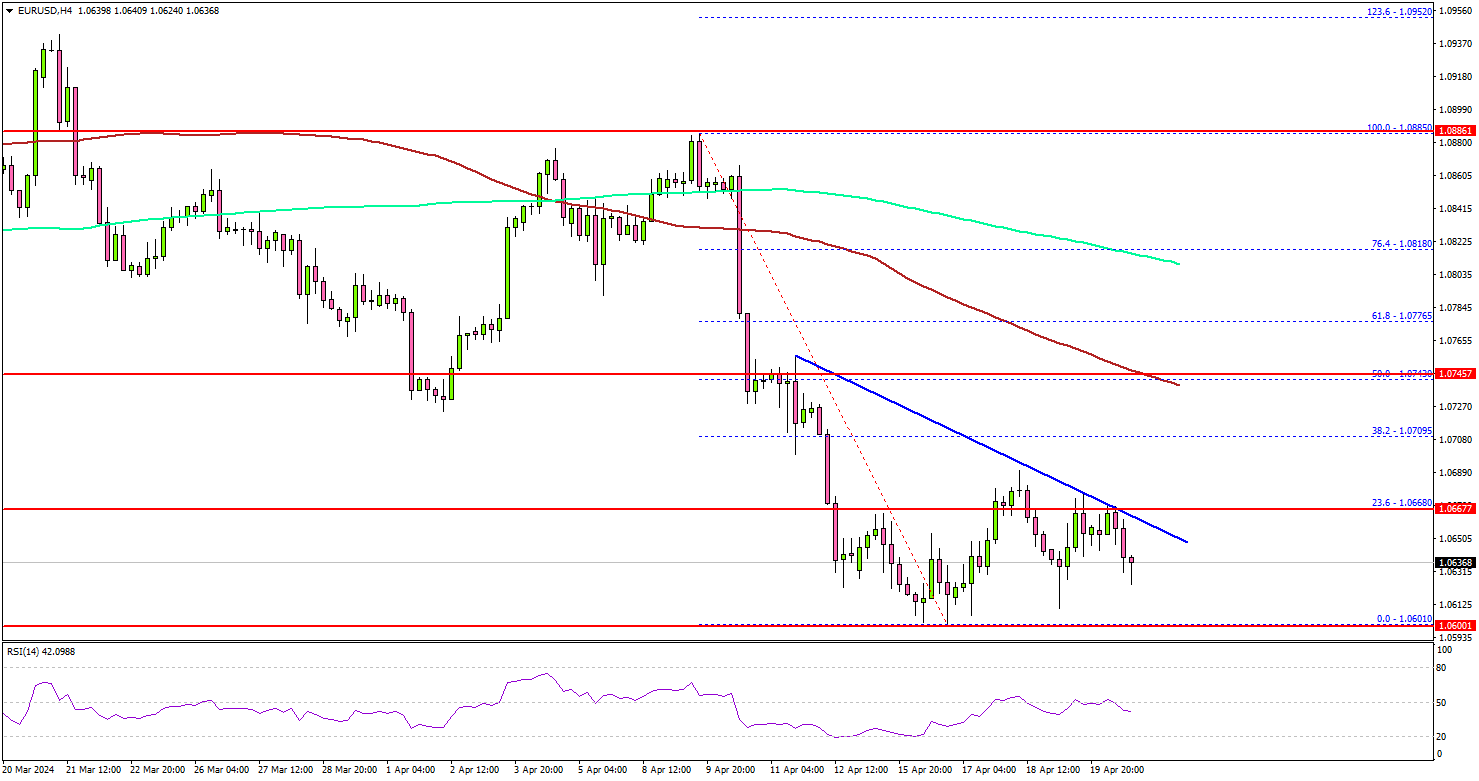

EUR/USD Technical Analysis

The Euro extended losses and traded below the 1.0650 support against the US Dollar. EUR/USD tested the 1.0600 zone and recently started a consolidation phase.

Looking at the 4-hour chart, the pair traded as low as 1.0601 and settled well below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

It is now consolidating and attempting a recovery wave above 1.0640. EUR/USD is testing the 23.6% Fib retracement level of the downward move from the 1.0885 swing high to the 1.0601 low and facing resistance at 1.0665.

There is also a key bearish trend line forming with resistance at 1.0670 on the same chart. The first key resistance is near the 1.0750 zone. It is close to the 50% Fib retracement level of the downward move from the 1.0885 swing high to the 1.0601 low and the 100 simple moving average (red, 4-hour).

A clear move above the 1.0750 resistance could send the pair further higher. In the stated case, EUR/USD bulls could even aim for a move toward 1.0840.

Immediate support is near the 1.0620 level. The next major support is at 1.0600. If there is a downside break below the 1.0600 support, the pair might test 1.0550. The main support is now forming at 1.0520. Any more losses might send the pair toward 1.0485.

Looking at Oil, the bears remained in control amid the Israel-Iran war situation. There was a drop below $82.50, and the bears could aim for more downsides.

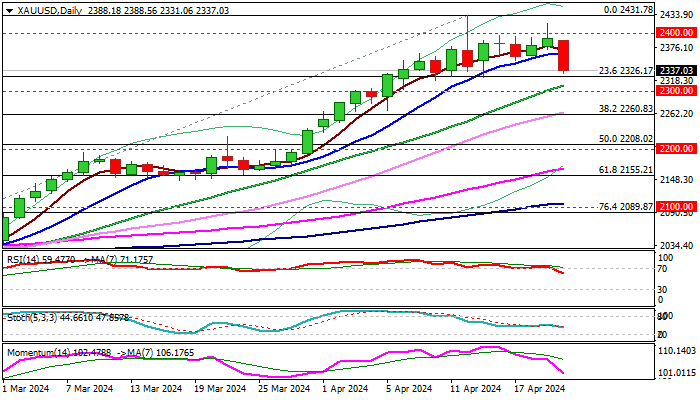

XAU/USD: Gold Falls 2% on Fading Safe Haven Demand

Gold price fell around 2% on Monday as safe haven demand faded on calmer tones from the Middle East, which ease fears for conflict escalation.

Traders partially collected profits after gold repeatedly failed to sustain gains above psychological $2400 level and bull-trap pattern is forming on daily chart.

Fresh bears pressure the first pivots at $2320 zone (recent range floor / Fibo 23.6% of $1984/$2431), loss of which would add to initial negative signals (the price broke below 10DMA and is sharply losing bullish momentum) and allow for deeper pullback.

Psychological $2300 level and Fibo 38.2% ($2260) mark next significant supports, with the latter marking a pivotal support, which should contain extended dips to mark a healthy correction and not harm larger bulls.

Conversely, clear break of $2260 pivot to sideline bulls and shift near-term focus to the downside.

Res: 2363; 2400; 2417; 2431.

Sup: 2320; 2300; 2260; 2222.

Sunset Market Commentary

Markets

Eurostat today published deficit and debt data for the years 2020-2023 in E(M)U). The euro area government deficit declined marginally from 3.7% of GDP in 2022 to 3.6% in 2023. The government debt to GDP ratio decreased over the same period from 90.8% to 88.6%. Zooming in on Belgium, Eurostat reported an increase of the deficit from 3.6% of GDP to 4.4% of GDP with the debt ratio rising from 104.3% to 105.2%. Other notable underperformers in the euro zone include France (-5.5% deficit & 110.6% debt), Italy (-7.4% & 137.3%) and Slovakia (-4.9% & 56%). Bloated public finances are one of the key drivers of our fundamental bearish view on (long term) interest rates. Especially since the ECB left the scene as unlimited, price-insensitive buyer of government bonds under its asset purchase programmes. Credit risk premia make their comeback while the snowball effect and some global trends (energy transition, ageing, defense,…) raise structural spending needs. In June, Europe will again launch excessive debt procedures against some countries (including Belgium) after easing measures in the wake of the Covid-pandemic. The (very) long end of European yield curve continued underperforming today while there was no one-on-one correlation with the timing of today’s figures. German yields currently add up to 3.6 bps (30-yr) with (minor) new YTD highs for tenors ranging from 5-yr until 30-yr. The German 2-yr yield tested the psychological 3% mark for a second session running. Risks related to tomorrow’s April EMU PMI’s seem asymmetric with anything apart from a huge negative surprise possibly sufficient to push yields beyond these recent levels. Changes on the US yield curve were more or less similar varying between -1 bp (2-yr) and +3.3 bps (30-yr). UK Gilts continue their outperformance following Friday’s reset. Bank of England comments cumulated into a shift in market thinking, putting the Bank of England more on par with the ECB than with the Fed. Short term UK yields lose up to 4 bps and contribute to follow-up losses in sterling. EUR/GBP rises from 0.8602 to 0.8638, the highest level since the first trading day of the year. The November top at 0.8768 is the next real reference. GBP/USD underperforms given today’s USD strength, losing a big figure to GBP/USD 1.23. Losses for EUR/USD are technically insignificant with the pair changing hands at 1.0630.

News & Views

The Swiss National Bank announced that it will raise the minimum reserve requirements for domestic banks. The change will start from July 01 2024 on. The new regulation includes the SNB increasing the minimum reserve ratio from 2.5% to 4%. The central bank also broadened the basis for calculating the minimum reserve. Liabilities arising from cancellable customer deposits (excluding those tied to pension provision) will now be included. The SNB said that the adjustments will ensure that the implementation of the SNB’s monetary policy remains effective and efficient. The new setup will reduce the SNB’s interest rate cost after the bank recorded a loss in 2023. The SNB states that the amendments will not affect the current monetary policy stance. After a protracted decline of the Swiss franc between New Year (EUR/USD <0.93) and early April (EUR/CHF 0.984), CHF recently found a new short-term equilibrium near EUR/CHF 0.97.

Belgian consumer confidence dipped slightly in April from -5 to -6. The decline masked a clear deterioration in employment expectations (unemployment indicator rose from 17 to 24). According to the assessment of the NBB, the announcement of the bankruptcy and closure of several companies and retailers did not go unnoticed by consumers, who indicated that they are much more concerned about how the job market will develop in the next three months. For the second month in a row, the deterioration in this component was clear to see (17 from 10 in March). On the other hand, consumer expectations regarding the general economic situation in Belgium improved (-18 from -20). On a personal level, households revised slightly upwards their expectations of their own financial situation (-1 from -2) along with their saving intentions (18 from 17).

Graphs

EMU 10-yr swap yield tests the YTD top. Can PMI’s trigger a break tomorrow?

EUR/CHF: higher reserve requirement by SNB doesn’t impact CHF

Geopolitical tensions move to the background and so do Brent crude prices

GBP/USD: sterling extends losses after BoE signals willingness to go the ECB’s way.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0618; (P) 1.0648; (R1) 1.0686; More...

EUR/USD is staying in consolidation from 1.0601 and intraday bias stays neutral. Upside of recovery should be limited by 1.0723 support turned resistance. Break of 1.0601 will resume the fall from 1.1138 to 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536 next.

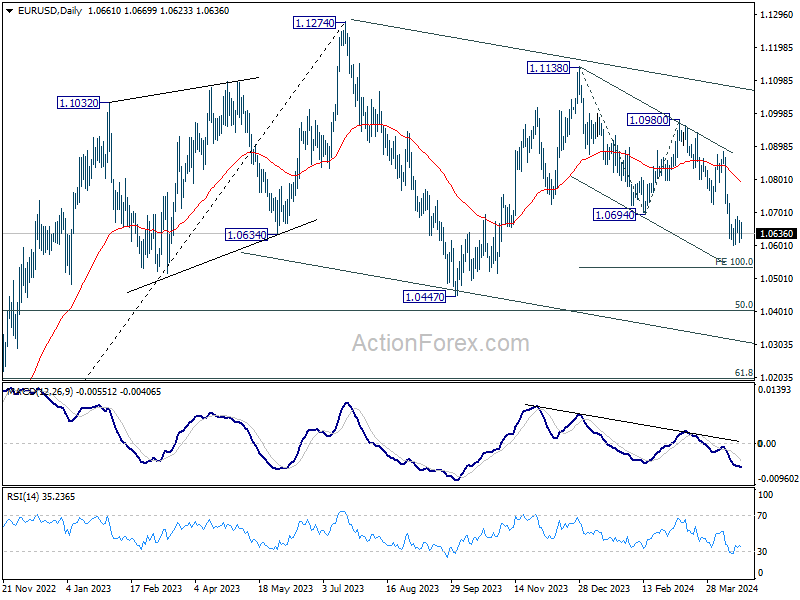

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below, Strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

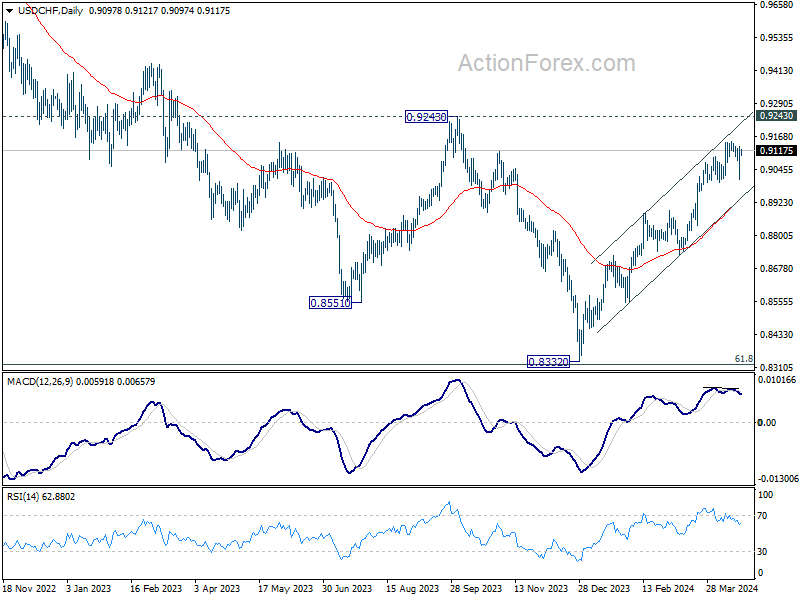

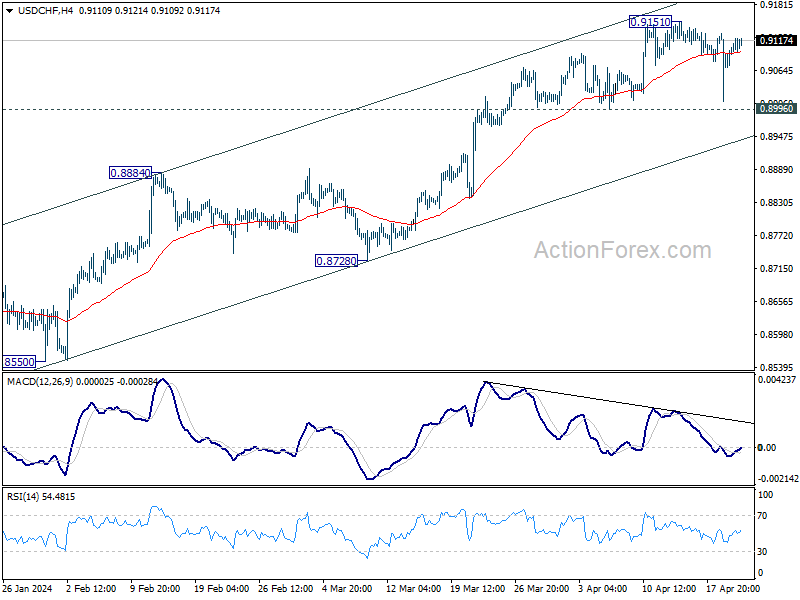

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9032; (P) 0.9084; (R1) 0.9156; More....

USD/CHF is extending the consolidation pattern from 0.9151 and intraday bias stays neutral. Further rally is expected as long as 0.8996 support holds. Break of 0.9151 will resume the larger rise from 0.8332 to 0.9243 resistance. However, firm break of 0.8996 will turn bias to the downside for 55 D EMA (now at 0.8939).

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish.