Sample Category Title

Strong Profit-Taking in Gold or Beginning of Reversal?

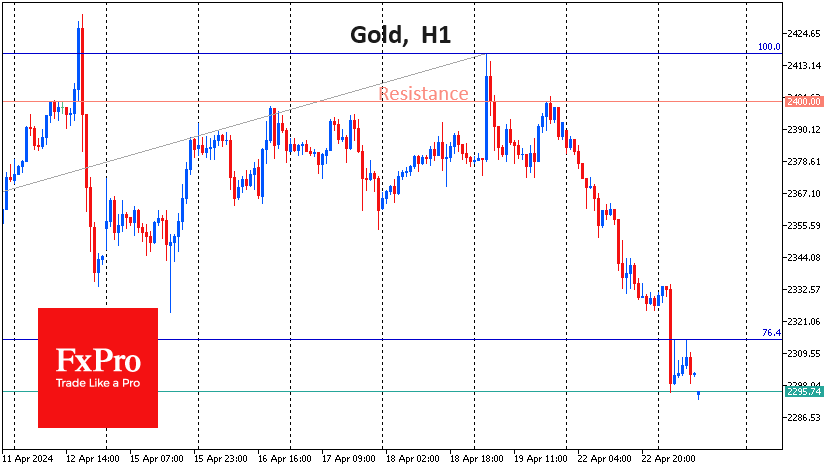

Gold is under pressure this week, having pulled back to the $2300 per troy ounce level. The decline since Friday’s close is over 3.7%. The formal trigger is a more moderate escalation in the Palestinian-Israeli conflict than expected at the beginning of the month. However, we view the current pullback as a welcome technical correction that could develop into a bear market.

Last Friday, the price of a troy ounce of gold on the spot market broke the $2400 mark for the second time in history. And once again, there was strong resistance at this round level. Since the beginning of the week, we have seen systematic intraday selling of gold and silver, not related to the stock market or currencies. That is, traders focus on this idea, ignoring global fluctuations in risk demand.

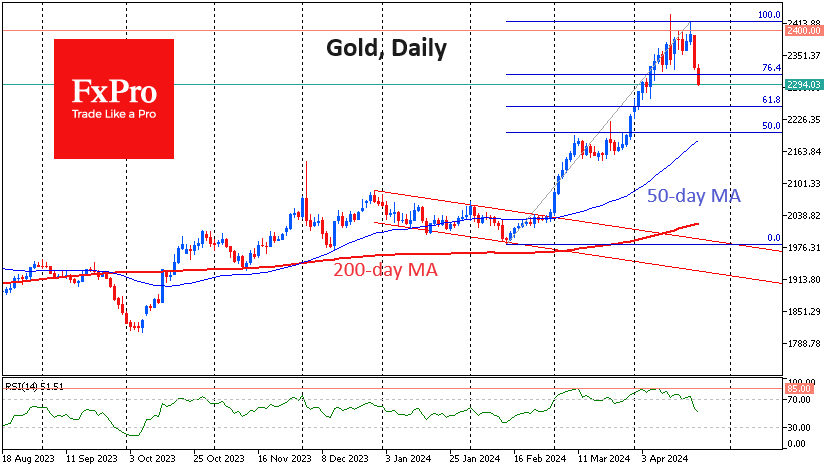

In a correction, the price has already now pulled back below the 76.4% intermediate retracement level of the rally from the February lows to the April peak. This is an important signal of a more global shakeout, as we recently saw such a shallow correction in March in a more obvious bull market.

The downside amplitude over these two days, which is the largest in the last two years, cannot be ignored.

On the daily timeframes, the RSI has pulled back sharply from the overbought area, also indicating an active downward move. Earlier, we noted a divergence between this indicator and the price, where two RSI touches of the 85 level were at $2100 and $2350. This was an important precursor to the decline, the development of which we are now seeing.

Nevertheless, the positive scenario remains valid as long as the price is above $2360, where the 61.8% Fibonacci retracement level lies. We assume that gold is capable of returning to the upside after a technical shakeout.

A sell-off in gold over the next couple of days could quickly take the price to $2360. A dip below would be an important first signal of a true reversal. The ability to go below $2185-2200 within a couple of weeks would raise the question of a long-term trend reversal with a potential downside target before the end of the year at $1900.

BoE’s Haskel: Inflation outlook hinges on quick reduction of job vacancies to unemployment ratio

During a seminar today, BoE MPC member Jonathan Haskel emphasized the critical role of the labor market in shaping the UK's inflation outlook.

Haskel pointed out that the labor market tightness, specifically the ratio of job vacancies to unemployment, is a key factor in assessing inflationary pressures. Although this ratio is gradually decreasing, Haskel expressed concern over the pace, stating it is "rather slowly" and it remains uncertain if it is sufficient to align inflation with the target levels.

"The persistence of inflation depends a lot on how quickly that ratio comes down," Haskel remarked, underscoring the direct impact of labor market conditions on inflation trends.

ECB’s de Guindos: June cut a failt accompli, uncertain afterwards

In an interview with Le Monde, ECB Vice President Luis de Guindos indicated barring any surprises, a June rate cut is a "fait accompli."

"If things move in the same direction as they have in recent weeks, we will loosen our restrictive monetary policy stance in June," he said.

However, looking beyond June, the Vice President expressed considerable caution due to heightened levels of uncertainty. "I'm inclined to be very cautious," said de Guindos.

UK 100 Index Hits New All-Time Highs But Rally May Be Cooling

- UK 100 index reaches 8,000 milestone

- But further gains may have to wait as uptrend starts to lose steam

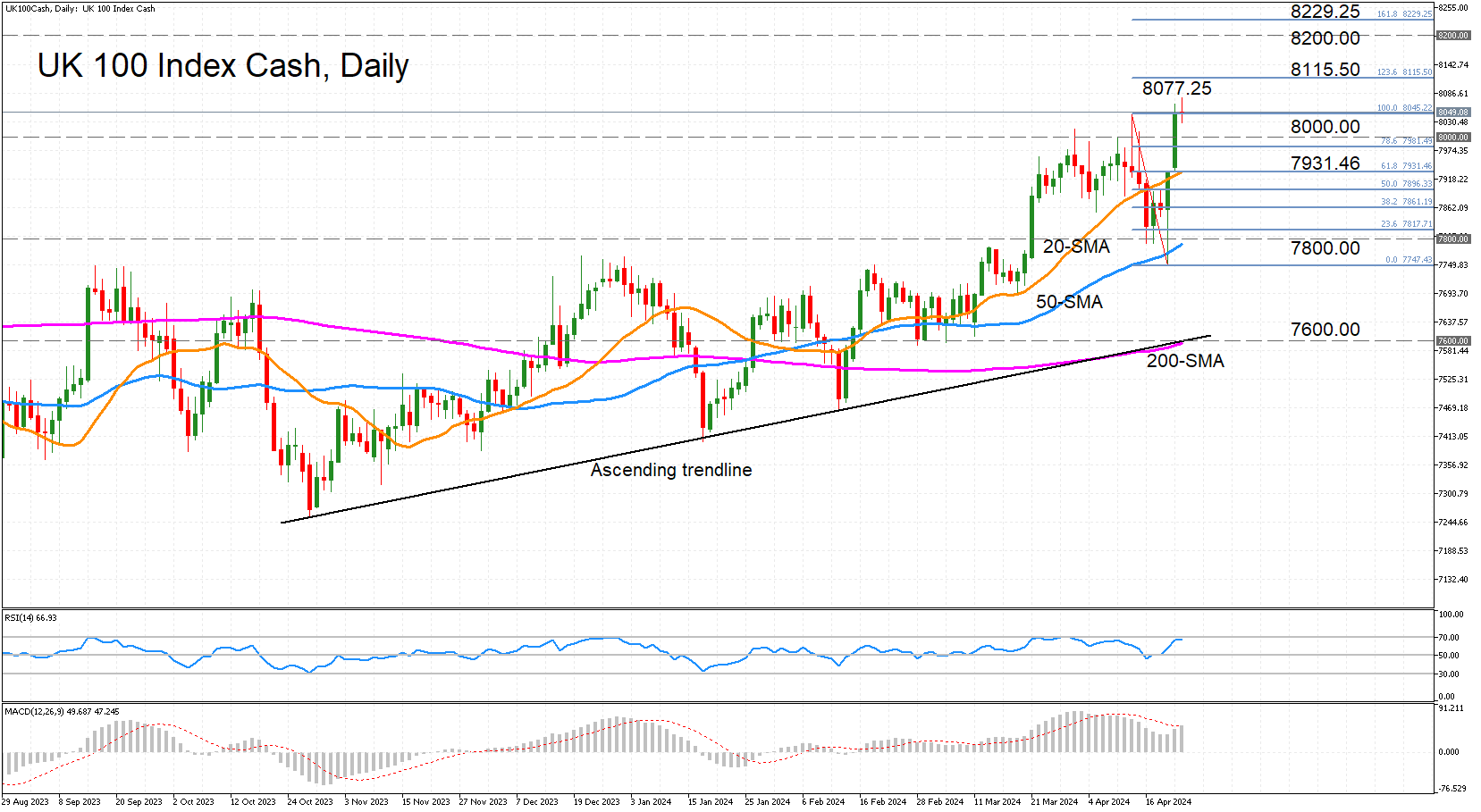

The UK 100 stock index (cash) closed at a new all-time high of 8,046.44 on Monday and climbed to an intra-day record of 8,077.25 earlier today. But whilst another record close is possible in the near term, positive momentum appears to be waning.

The RSI is currently edging sideways slightly below the 70 overbought mark, while the MACD seems to be struggling to cross above its red signal line. Yet, the bullish bias remains fairly strong so how today’s session ends could prove critical to the short-term direction.

If the index manages to regain some upside momentum, the next stop could be 8,115.50, which is the 123.6% Fibonacci extension of the April downleg. Higher up, the 8,200.00 level could attract attention before the 161.8% Fibonacci of 8,229.25 is targeted by the bulls.

To the downside, there could be immediate support at 8,000.00, but the 20-day simple moving average (SMA) is another important support to watch as it is intersecting the 61.8% Fibonacci retracement of 7,931.46. A drop below this point would shift the focus to the busy 7,800.00 region, which is being approached by the 50-day SMA. Breaching this would add to the bearish risks and open the door to the 200-day SMA that has converged with the medium-term ascending trendline in the 7,600.00 area.

In brief, a further rise into uncharted territory is possible in the next few sessions, but there is also a risk that the rally pauses for breath before resuming the uptrend.

FTSE100 Hits New Record High

FTSE 100 index hit new marginally higher record high on Tuesday, as strong bullish acceleration extends into third straight day.

Strong gains in UK defense stocks, food producers and retailers, along with weaker pound and rising commodity prices contributed to strong advance of blue-chip stock index.

Bullish daily studies support the action, but overbought conditions warn of a partial profit-taking, after the index advanced 2.8% in past three days.

Dips should find solid ground at 7950/30 zone (Fibo 38.2% of 7746/8076 upleg / converged 10/20DMA’s) to position for fresh push higher and attack at Fibo projections at 8117 and 8161 (123.6% and 138.2% respectively).

Caution on break here and loss of 7900 zone, which would shift near-term focus lower.

Res: 8076; 8117; 8161;8200

Sup: 8000; 7950; 7930; 7900

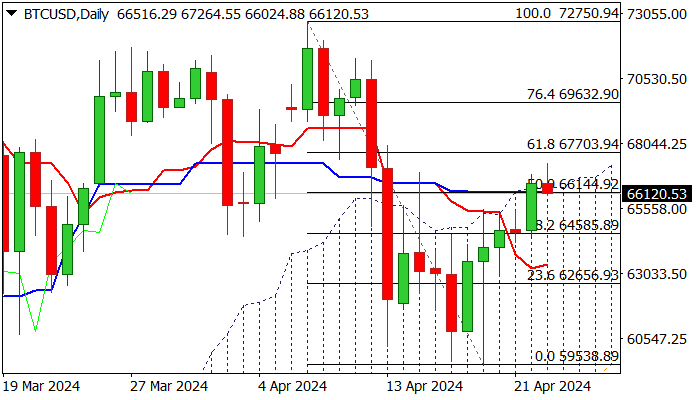

BTC/USD – Slight Bullish Bias Above Daily Cloud, But Stronger Direction Signals Still Needed

Bitcoin is consolidating in early Tuesday, after advancing 2.8% on Monday and remains constructive as the latest jump has generated positive signal on a marginal close above important barriers at $66144 (50% retracement of $72750/$59538) and $66330 (top of ascending daily Ichimoku cloud).

Geopolitics and broader financial market sentiment remain bitcoin’s main driver, with conflicting studies on daily chart (14-d momentum remains in negative territory / MA’s are in mixed setup, but daily cloud underpins, and near-term bias is expected to remain with bulls while the price stays above the cloud.

However, stronger signals can be expected on sustained break above Fibo 61.8% barrier at $67700 (bullish) or fall below 10DMA at $64039 (bearish).

Res: 67700; 68000; 68325; 69632

Sup: 66144; 64585; 64039; 62656

Bitcoin Awaits Signal from Equity Indices

Market picture

The capitalisation of the crypto market over the past 24 hours has added only 0.15% to $2.44 trillion. Crypto sentiment indices remain in the ‘greed’ territory, scoring 71 points, compared to 73 points the day before.

Bitcoin added about a quarter of a percent during the day, reaching $66.5K. Early on Tuesday morning, the price briefly exceeded $67.1K, touching the 50-day MA, but then retreated. It seems that this time, the crypto market is waiting for a signal from stock indices rather than giving such a signal about risk appetite. The calm may be illusory and quickly come to an end. We reiterate that consolidation above $67.1K could open the way to the $72-74K area. A reversal to the downside could end with a quick rollback to the $60K area.

According to CoinShares, investments in crypto funds over the past week have decreased by $206 million after an outflow of $126 million the previous week. Investments in Bitcoin decreased by $192 million, in Ethereum – by $34 million, in Solana – by $0.3 million.

News background

There was a further outflow of capital from the Grayscale fund totalling $450 million, which could not be compensated by the inflow into the two largest ETFs totalling $259 million. Investors’ appetite for ETFs is declining, probably due to overall pressure on stock markets due to changing expectations for Fed policy and a strengthening dollar.

The average transaction fee in the Bitcoin network has dropped to $34.86 after reaching a record $128.45 on the day of the halving on April 20. The growth of transaction fees began on the eve of the halving. Experts linked the trend with user activity in anticipation of the launch of the Runes protocol, which was timed to coincide with the event.

The Bitcoin Initiative group of Bitcoin supporters has initiated a referendum to amend the Swiss constitution. The group intends to oblige the Swiss National Bank (SNB) to include BTC along with gold in its reserves.

FTX management will get rid of a new batch of the bankrupt exchange Solana (SOL) in the form of an auction after criticism from creditors, said Figure Markets CEO Mike Cagney.

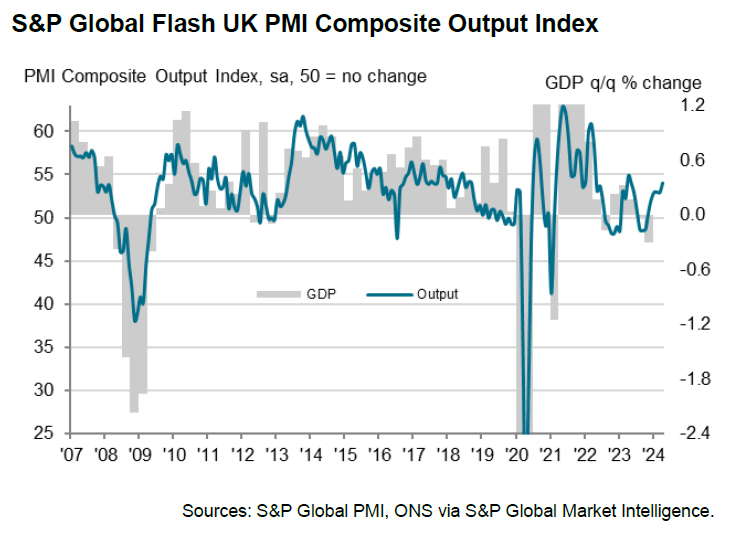

UK PMI composite rises to 54, sustainable path to target inflation not achieved yet

UK PMI Manufacturing fell from 50.3 to 48.7 in April, below expectation of 50.2. PMI Services rose from 53.1 to 54.9, above expectation of 50.2, and an 11-month high. PMI Composite rose from 52.8 to 54.0, also an 11-month high.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, stated that UK economy's rebound from last year's recession "continued to gain momentum". He noted that GDP is now growing at an increased quarterly rate of 0.4%, up from 0.3% in the first quarter.

This economic upturn has led to increased hiring, driven further by the rise in the National Living Wage in April. However, these factors have also escalated cost pressures significantly. Although the inflation of selling prices has moderated slightly, the combination of rising costs and solid demand could lead businesses to hike prices in the near future.

"While the improving economic recovery picture is welcome news, the upward pressure on inflation will add to concerns that a sustainable path to below target inflation has not yet been achieved," he added.

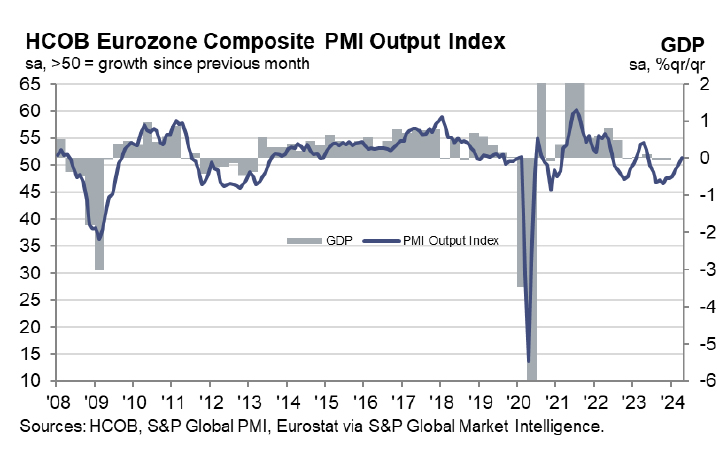

Eurozone PMI composite rises to 51.4, recovery to sustain

Eurozone's PMI Manufacturing fell from 46.1 to 45.6 in April, below expectation of 46.5. PMI Services rose from 51.5 to 52.9, above expectation of 51.8, an 11-month high. PMI Composite rose from 50.3 to 51.4, also an 11-month high.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that Eurozone had a "good start" to Q2, with GDP projected to expand by 0.3%, mirroring the growth rate of the first quarter.

De la Rubia outlined three factors contributing to the sustainability of the recovery. Positive momentum in new business over the past two months has spurred more aggressive hiring policies. Service providers have shown confidence in their pricing power. The recovery in Germany and France, Eurozone's largest economies, have particularly underscored the broader regional trend.

However, the latest figures pose a critical test for ECB on its readiness to cut interest rates in June. The "accelerated increases in input costs", driven by higher oil prices and wages, necessitates close scrutiny. Moreover, the quicker pace at which service sector companies are raising prices suggests that "services inflation will persist".

Despite these inflationary pressures, HCOB still expects an ECB rate cut in June, although de la Rubia expects ECB to proceed with more caution rather than adopting the "pragmatic speed" earlier suggested by Governing Council member François Villeroy de Galhau.

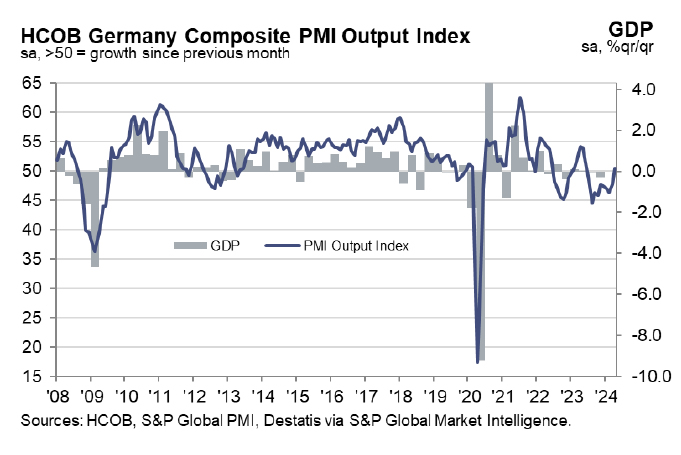

Germany PMI composite soars to 53.3, indicative of 0.2% GDP expansion in Q2

Germany's PMI Manufacturing ticked up from 41.9 to 42.2 in April, below expectation of 42.9. PMI Services jumped from 50.1 to 53.3, well above expectation of 50.5, a 10-month high. PMI Composite rose from 47.7 to 50.5, also a 10-month high.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, said: Factoring in the PMI numbers into our GDP Nowcast, we estimate that GDP may expand by 0.2% in the second quarter, following an estimated 0.1% growth in the first quarter.