Sample Category Title

Dollar Rally Shifts into a Lower Gear

Markets

Developments in the Middle East gradually lost their grip on global markets with central bank talk again taking the lead. Fed Vice-Chair Jefferson delivered a perfect assist for Chair Powell to acknowledge the consequences of recent strong US activity data while inflation remains stubbornly high. Jefferson warned that the Fed will have to keep rates higher for longer if inflation persists. Expressing his belief for inflation to come down given a steady policy rate didn’t prevent further bond selling. Later, Powell couldn’t but fully accept consequences of the Fed’s data dependent approach. In a panel discussion he admitted that recent data didn’t provide the greater confidence the Fed needs to start policy erasing. “Given the strength of the labor market and progress on inflation so far, it is appropriate to allow restrictive policy further time to work and let the data and the evolving outlook guide us”. Market expectations for a first Fed rate cut are pushed back beyond summer (90% for September) and investors only see about 50% chance that a second cut will follow this year. US bond yields added between 4.6 bps (30-y) and 8.2 bps (5-y). The 2-y yield again tested the 5% barrier and longer maturities all touched new YTD highs. German yields added between 2.4 bps (2-y) and 4.6 bps (10-y). ECB speakers including President Lagarde and Villeroy confirmed last week’s guidance that the ECB intends to start cutting rates in June. They admit that the inflation path will be more bumpy later this year. The impact of geopolitical tensions (oil) and the valuation of the euro are on the radar. The amount of additional cuts in H2 is uncertain. (US) equities held relatively stable despite the Fed’s higher for longer message (S&P 500 -0.21%). The dollar rally shifted into a lower gear, but the US currency clearly holds pole position. EUR/USD eased slightly further (close 1.0919). The yen continues outperforming despite multiple verbal warnings from Japanese officials (USD/JPY close 154.72).

Asian equity markets show a mixed picture, suggesting some stabilization after recent declines. The yuan remains in the defensive against a strong dollar with USD/CNY touching a minor YTD top near 7.24. Central bank speakers include ECB’s de Cos and Schnabel, Fed’s Mester and BoE governor Bailey. US yield markets might look for a short-term equilibrium after their repositioning. In Europe, we keep the 10-y swap yield on the radar as it is testing the YTD peak levels from end February. For now, we see no reason to fight the USD-accent, with the EUR/USD 1.06 big figure within reach.UK March inflation printed higher than expected (headline 0.6% M/M and 3.2% Y/Y vs 0.4% and 3.1% expected). Core inflation slowed less than expected to 4.2% Y/Y as did services inflation. The data make an early BoE rate cut unlikely. Sterling rallies to EUR/GBP 0.8533 after the release.

News & Views

New Zealand inflation printed line with expectations. First quarter price growth amounted to 0.6% q/q, a slight acceleration from the 0.5% in 2023Q4. The yearly gauge slowed from 4.7% to 4%, the weakest in three years. Trimmed-mean measures ranged between 0.7% and 0.8% q/q and 4.4-4.6% y/y. Non-tradeable CPI, a proxy for domestic inflation, picked up from 1.1% q/q to 1.6%. The yearly indicator barely slowed to 5.8, which is more than the central bank expected (5.3%). At the meeting last week, the RBNZ indicated unchanged policy rates until 2025, citing sticky core inflation. There’s nothing in today’s CPI numbers to change the RBNZ’s thinking. Markets expect an inaugural cut at the final policy meeting this year (November) but conviction has dropped. The kiwi dollar appreciates this morning after a few rough days against the US dollar. NZD/USD rises from 0.588 to 0.59.

South Korea’s finance ministry issued a statement after its minister discussed the recent weakening of their respective currencies with his Japanese counterpart. Choi (SK) and Suzuki (JN) expressed “serious concerns” and warned of taking appropriate steps to counter any drastic volatility. SK central bank governor Rhee shortly after labelled the recent SK won moves as a little excessive, noting that yuan and yen weakness are affecting the currency as well. It’s testament to many emerging market currencies coming under selling pressure after central banks having either cut rates or hinting to do in the near future against the background of a Fed keeping rates high for longer. USD/KRW pared some of recent gains after the statement, trading at around 1386 compared to almost 1400 yesterday. Both Choi and Suzuki will meet their US counterpart Yellen in the US today.

EUR/USD Daily Outlook

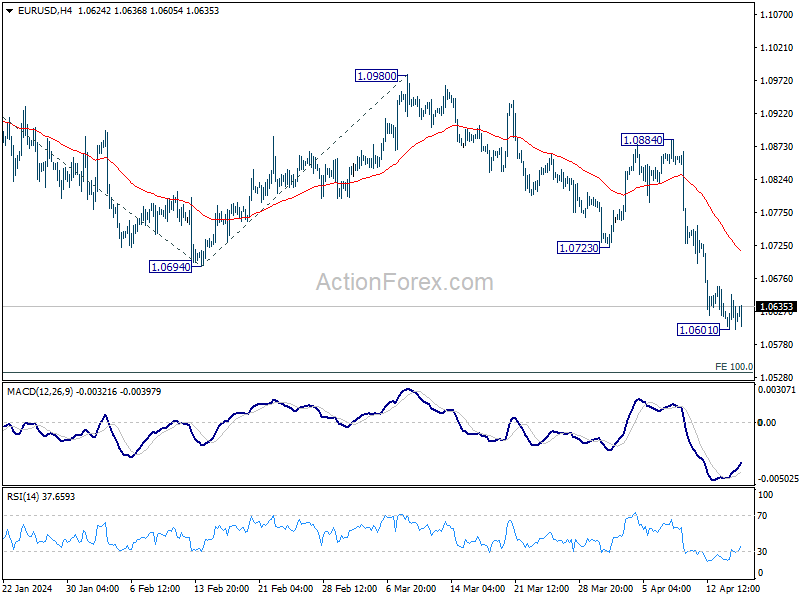

Daily Pivots: (S1) 1.0595; (P) 1.0625; (R1) 1.0648; More...

Intraday bias in EUR/USD remains neutral for consolidations above 1.0601 temporary low. While stronger recovery cannot be ruled out, upside should be limited by 1.0723 support turned resistance. On the downside, break of 1.0601 will resume the decline from 1.1138 to 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below. Strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

USD/JPY Daily Outlook

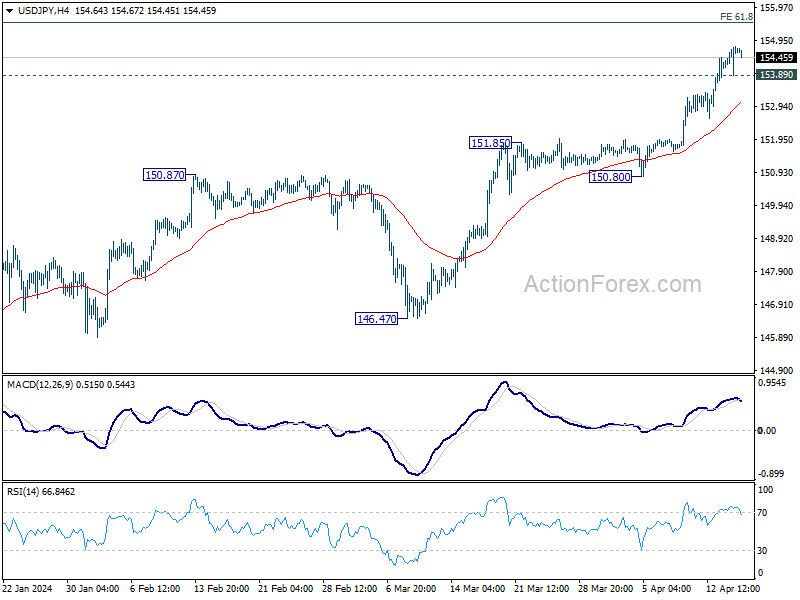

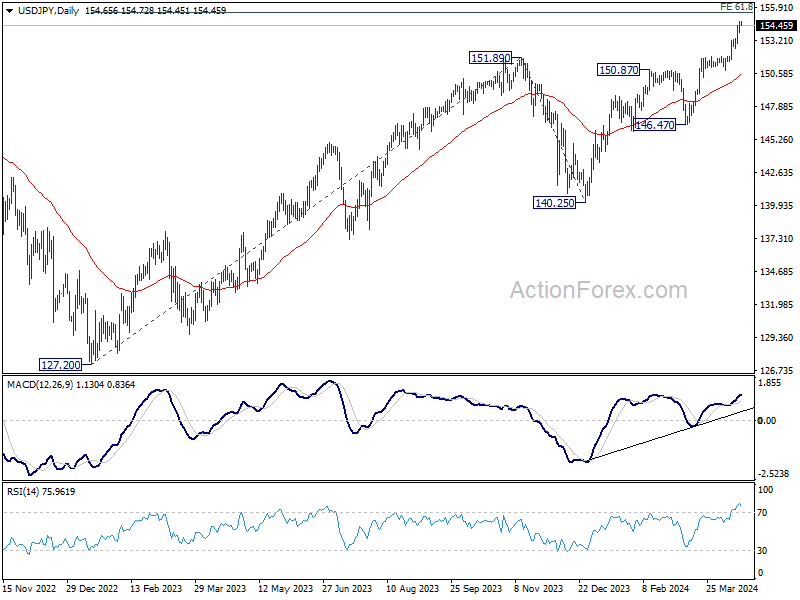

Daily Pivots: (S1) 154.18; (P) 154.48; (R1) 155.04; More...

Intraday bias in USD/JPY stays on the upside at this point. Current up trend should target 155.20 fibonacci projection level next. On the downside, below 153.89 minor support will turn intraday bias neutral and bring consolidations again, before staging another rally.

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. Outlook will now remain bullish as long as 146.47 support holds, even in case of deep pullback.

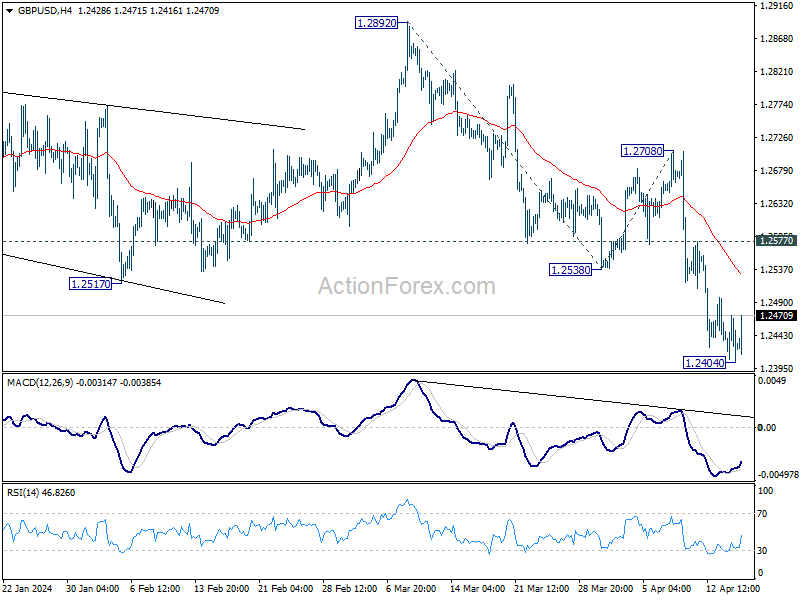

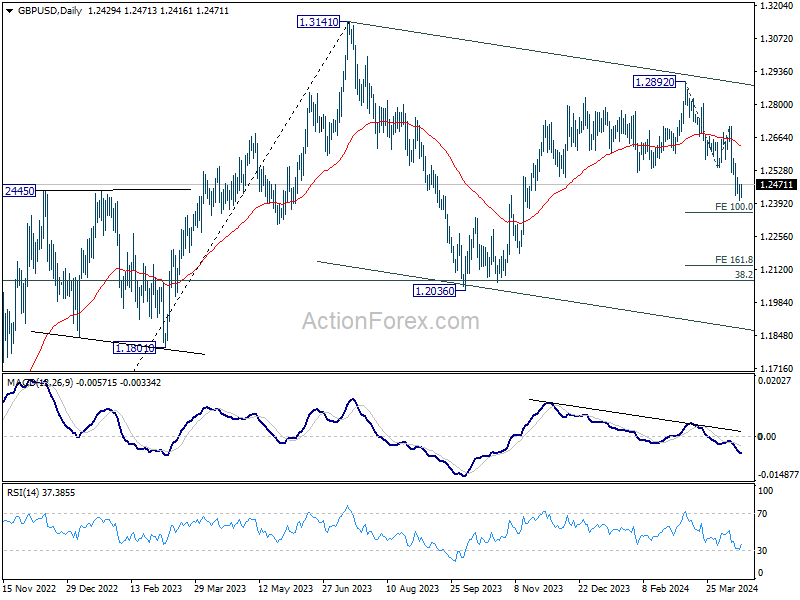

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2397; (P) 1.2435; (R1) 1.2463; More...

Intraday bias in GBP/USD remains neutral for more consolidations. Upside of recovery should be limited by 1.2577 minor resistance to bring another fall. On the downside, firm break of 1.2404 will resume the decline from 1.2892 to 100% projection of 1.2892 to 1.2538 from 1.2708 at 1.2354. Firm break there will target 161.8% projection at 1.2207 next.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Fall from 1.2892 is seen as the third leg. Deeper decline would be seen to 1.2036 support and possibly below. But strong support should emerge from 61.8% retracement of 1.0351 to 1.2452 at 1.1417 to complete the correction.

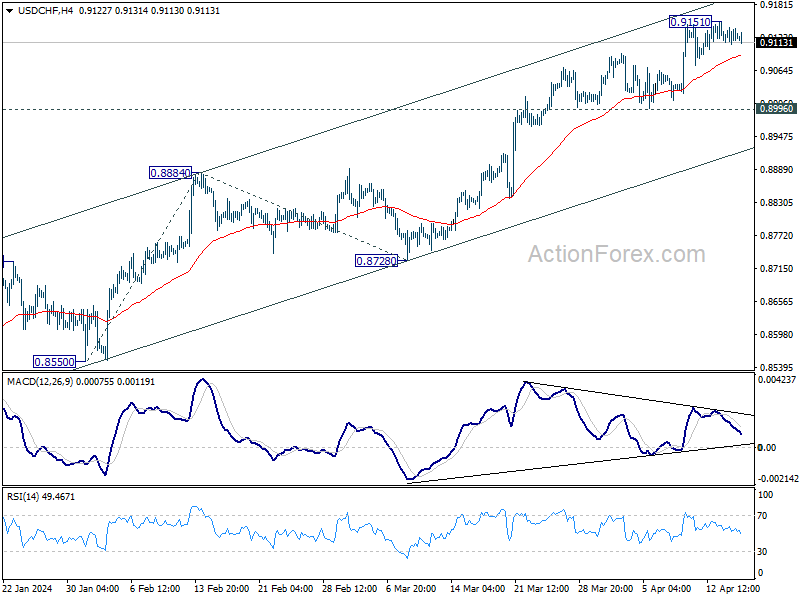

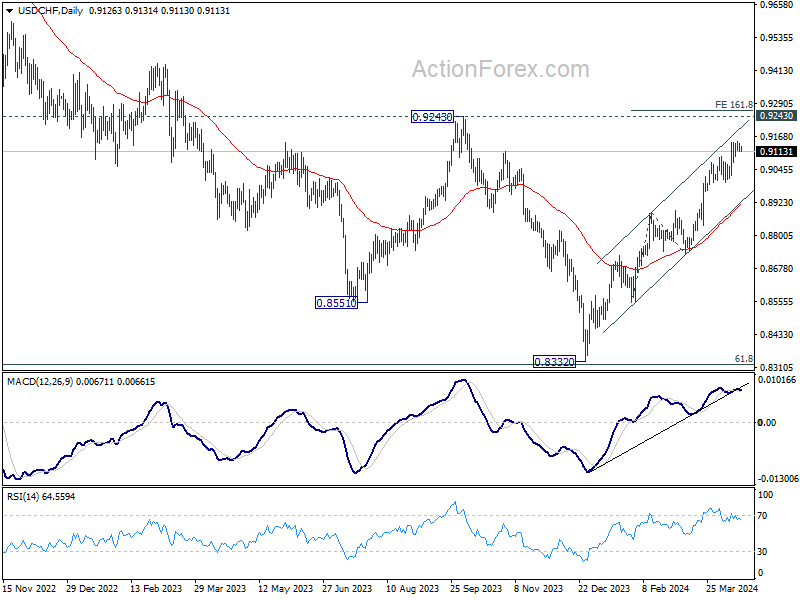

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9111; (P) 0.9132; (R1) 0.9152; More....

USD/CHF is extending consolidation from 0.9151 and intraday bias stays neutral. Further rally is expected as long as 0.8996 support holds. Firm break of 0.9151 will target 161.8% projection of 0.8550 to 0.8884 from 0.8728 at 0.9268.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish.

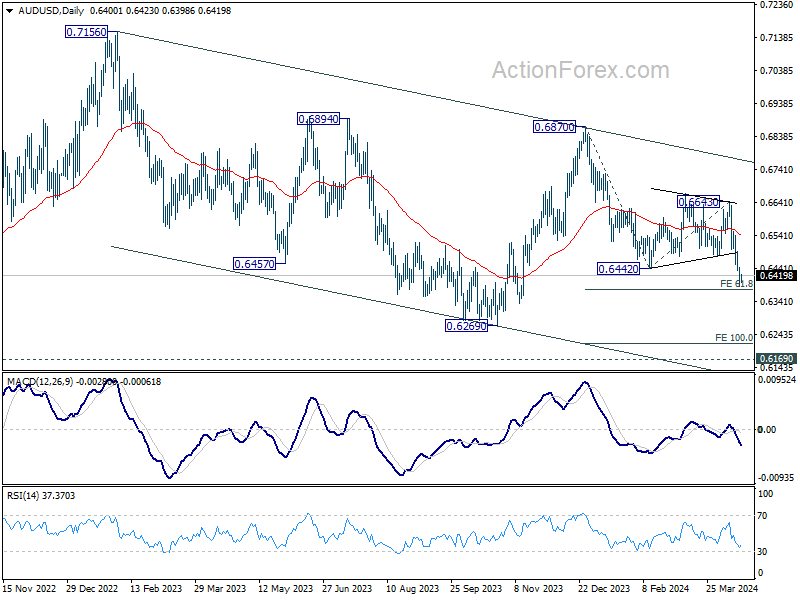

AUD/USD Daily Report

Daily Pivots: (S1) 0.6378; (P) 0.6413; (R1) 0.6437; More...

Intraday bias remains on the downside for the moment. Current fall is part of the larger down trend and should target 61.8% projection of 0.6870 to 0.6442 from 0.6643 at 0.6378. Decisive break there will pave the way to 0.6269 low, and possibly further to 100% projection at 0.6215. On the upside, above 0.6443 minor resistance will turn intraday bias and bring consolidations, before staging another fall.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which is still in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

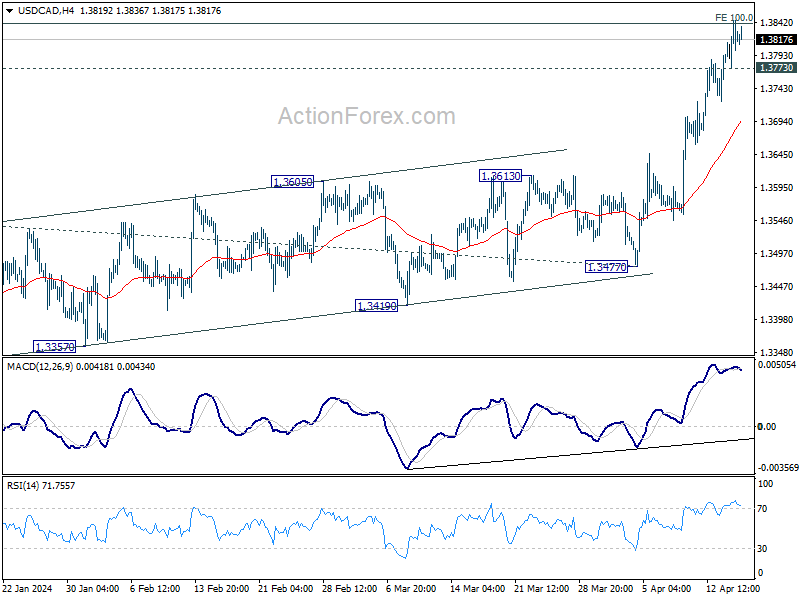

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3787; (P) 1.3816; (R1) 1.3859; More...

Intraday bias in USD/CAD remains on the upside for the moment. Decisive break of 100% projection of 1.3176 to 1.3540 from 1.3477 at 1.3841 will pave the way to 138.2% projection at 1.3980. On the downside, below 1.3773 minor support will turn intraday bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

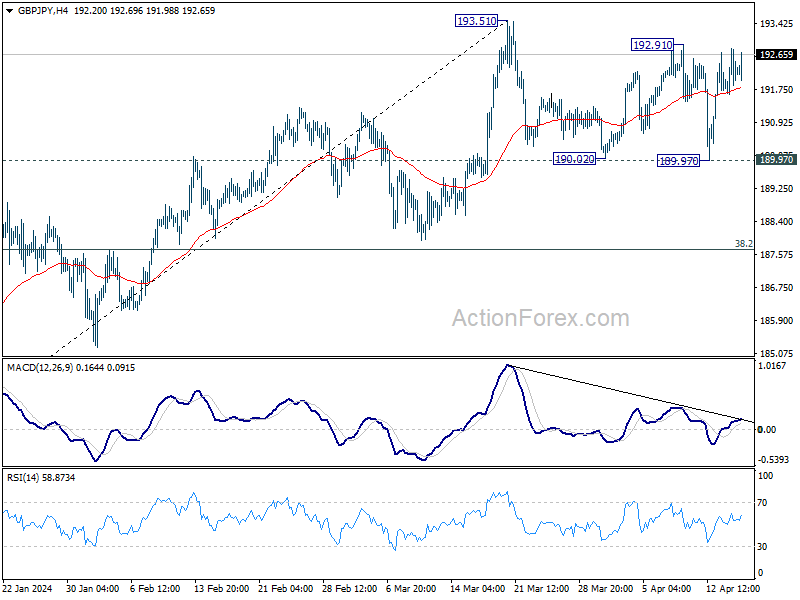

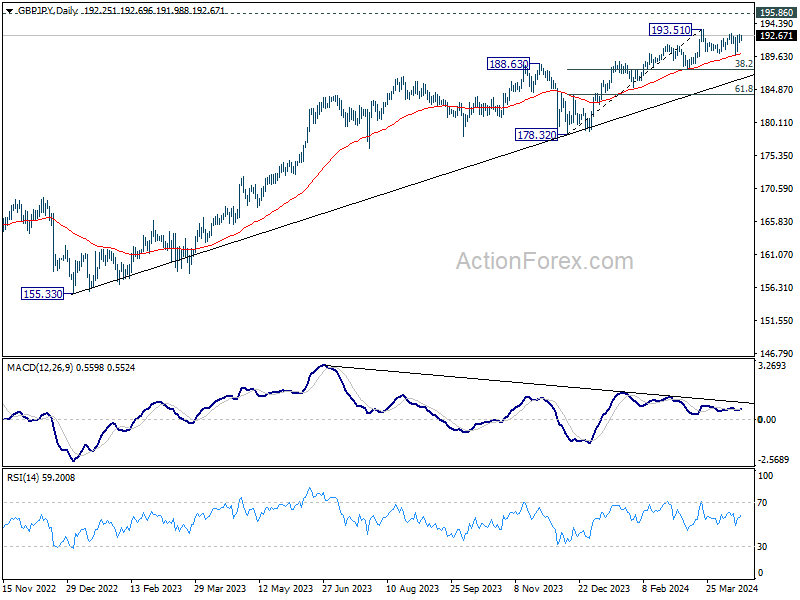

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.68; (P) 192.24; (R1) 192.84; More..

Intraday bias in GBP/JPY remains neutral as range trading continues. On the upside, break of 193.51 will resume larger up trend to 195.86 long term resistance. Nevertheless, decisive break of 189.97 support will indicate that it's at least correcting the rise from 178.32, and target 38.2% retracement of 178.32 to 193.51 at 187.70.

In the bigger picture, current rally is part of the up trend from 123.94 (2020 low), and is in progress for 195.86 long term resistance (2015 high). Break of 187.94 support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish in case of retreat.

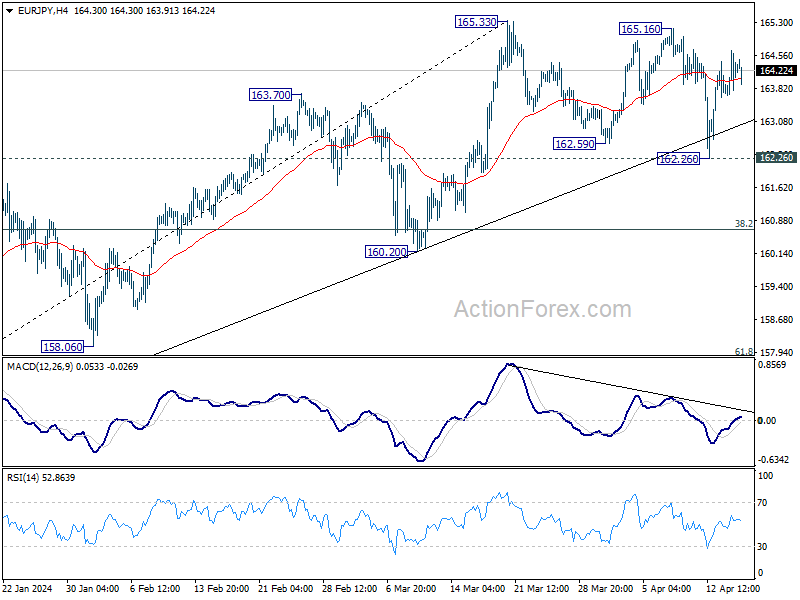

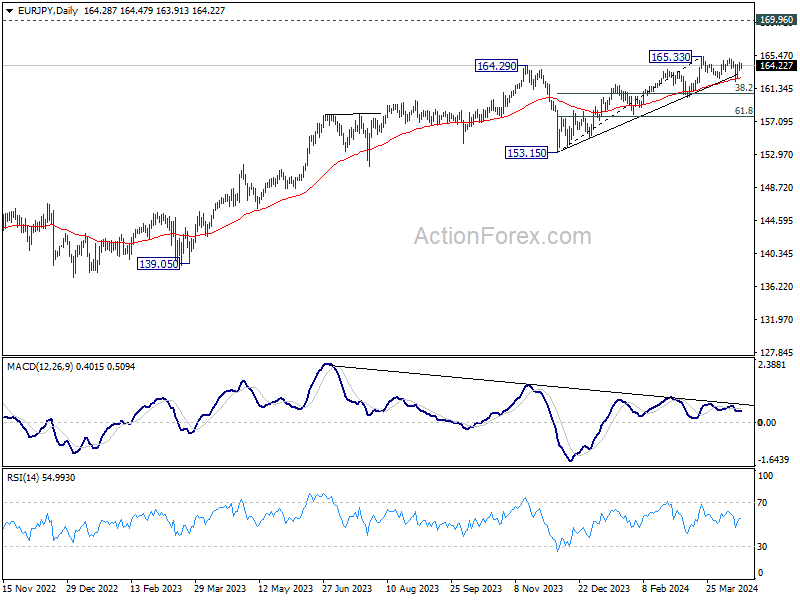

EUR/JPY Daily Outlook

Daily Pivots: (S1) 163.77; (P) 164.22; (R1) 164.77; More...

Intraday bias in EUR/JPY remains neutral as range trading continues. On the upside, firm break of 165.33 will resume larger up trend towards 169.96 key resistance next. However, decisive break of 162.26 support will argue that it's at least correcting the rise from 153.15, and target 38.2% retracement of 153.15 to 165.33 at 160.67.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 169.96 (2008 high). Break of 160.20 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.

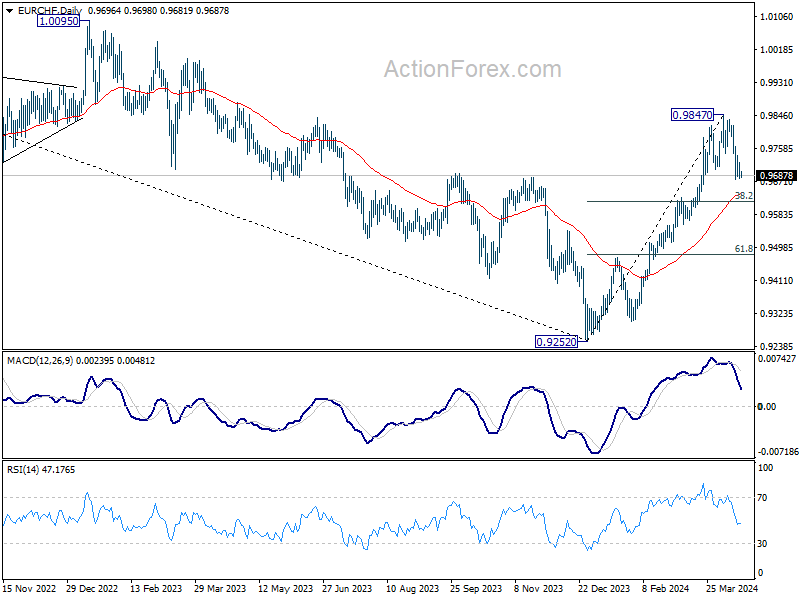

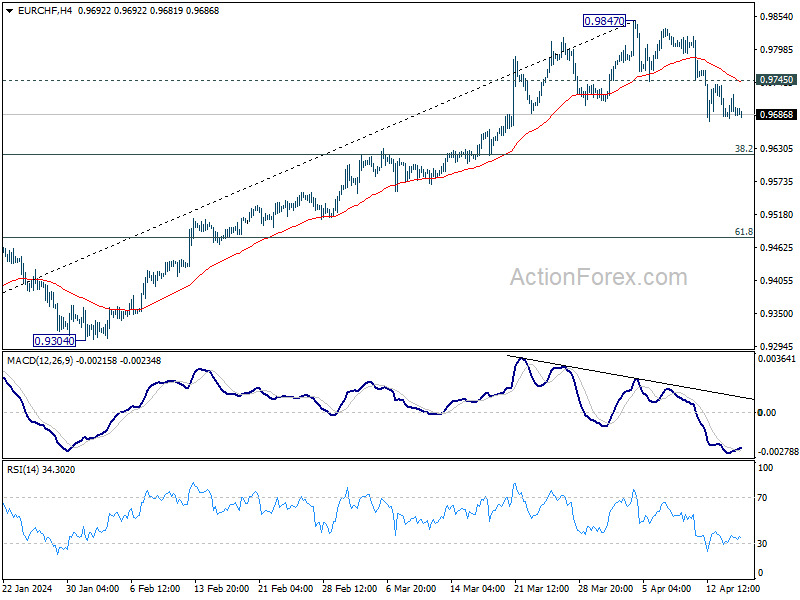

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9666; (P) 0.9704; (R1) 0.9733; More...

Intraday bias in EUR/CHF remains mildly on the downside. Correction from 0.9847 could extend to 38.2% retracement of 0.9252 to 0.9847 at 0.9620. But strong support is expected from there to contain downside to bring rebound, and set the range for the consolidation pattern from 0.9847. On the upside, above 0.9745 minor resistance will turn bias back to the upside for retesting 0.9847 instead.

In the bigger picture, a medium term bottom should be in place at 0.9252 already, on bullish convergence condition in W MACD. Rise from there now target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004. This will remain the favored case as long as 55 D EMA (now at 0.9639) holds.