Sample Category Title

CHF Renewed Its Decline on Weak Inflation

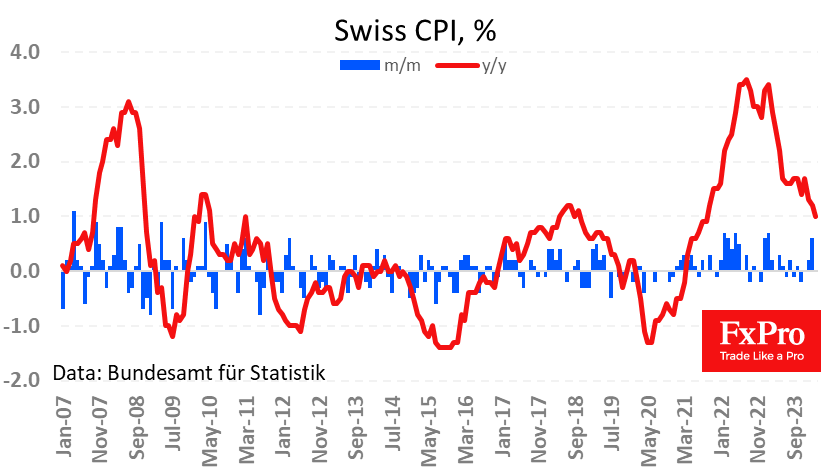

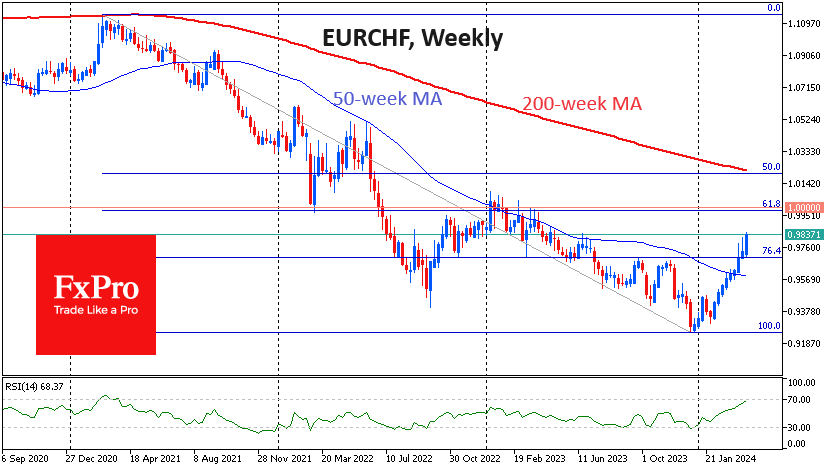

Weak Swiss inflation renewed the downward momentum of the franc, which is losing over 0.5% against the euro, sending EURCHF to highs last seen in May 2023.

The Swiss Consumer Price Index was virtually unchanged for March, with annual inflation slowing to just 1.0% – the lowest since September 2021. The Swiss National Bank has already unofficially celebrated a victory over inflation by unexpectedly cutting rates last month.

Fresh inflation data reinforces expectations of further policy easing. The franc has fallen for the past nine consecutive weeks, losing over 6% against the euro from extremes late last year. This is a significant move for a low-volatility pair like EURCHF, which has already returned to levels at the start of 2023. A further fall in the franc against the euro would work to inflate inflation, which is unlikely to please the SNB.

On balance, this means that the inertial upward movement in EURCHF could continue in the coming days or weeks, bringing the pair closer to parity. However, a subsequent depreciation of the franc against the euro or dollar has the potential to force the SNB to reconsider the soft approach. This is well within their power, as this CB is very active in forex and has room for policy tightening.

EUR/USD Surges Following Powell’s Remarks on Interest Rates

The EUR/USD pair moved upward to 1.0844 on Thursday, marking an unexpected shift following a period of strong US dollar performance. This change in dynamics can be attributed to investors' positive response to comments made by US Federal Reserve Chair Jerome Powell regarding the future of interest rates. Powell's remarks led to a surge in risk appetite, resulting in the dollar's decline.

Powell indicated that economic indicators would heavily influence the Federal Reserve's decisions on interest rate adjustments. Traders interpreted his comments as suggesting that, given the recent modest nature of US economic data, the anticipated forecast of three rate cuts in 2024, starting in June, remains on the table. The expectation is for the Federal Reserve to reduce interest rates by 75 basis points by the year's end, which aligns with earlier statements from the Fed. These hinted at a majority consensus among monetary policy committee members to commence rate cuts within the year, contingent on economic data.

Powell's reaffirming the Fed's trajectory towards lower interest rates, with specific timing depending on upcoming data, sets the stage for March's closely watched US employment market reports. The focus will be on whether the unemployment rate has remained steady and whether there has been any deceleration in the growth of average wages.

Technical analysis of EUR/USD

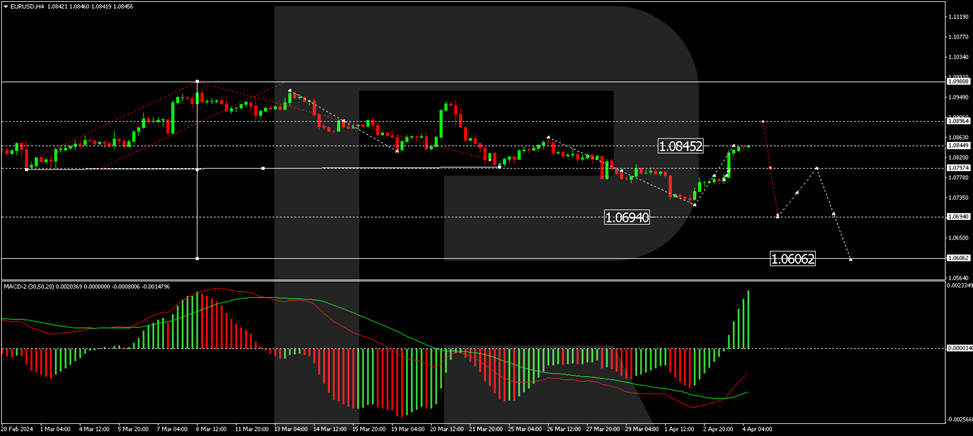

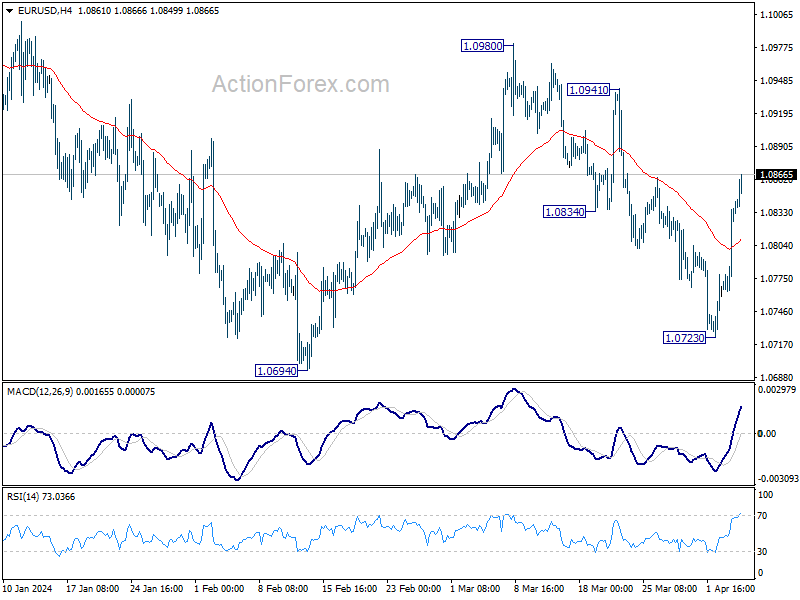

On the H4 chart, the EUR/USD pair has completed a correction to 1.0783, with a narrow consolidation range now established around this level. An upward breakout from this range could lead to a continuation of the correction to 1.0847, potentially followed by a new downward wave to 1.0694. This scenario is supported by the MACD indicator, where the signal line is below zero and the histogram peaks, suggesting a potential sharp decline.

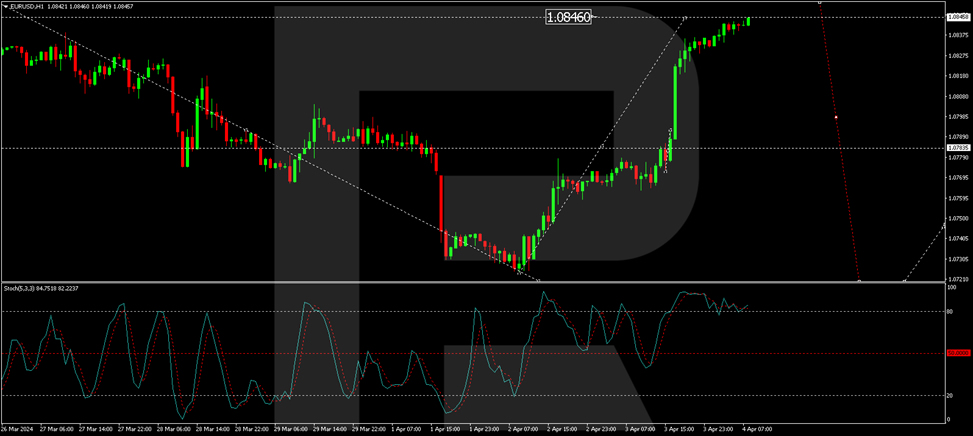

The H1 chart reveals a corrective pattern towards 1.0847, with an expected shift towards 1.0783 to commence a decline phase. A new consolidation range at these levels could lead to further correction to 1.0888 or a downward wave to 1.0694 upon a breakout. The Stochastic oscillator, positioned above 80, anticipates a significant drop to the 50 mark, potentially leading to further declines.

Swiss Franc Dips as Swiss Inflation Falls

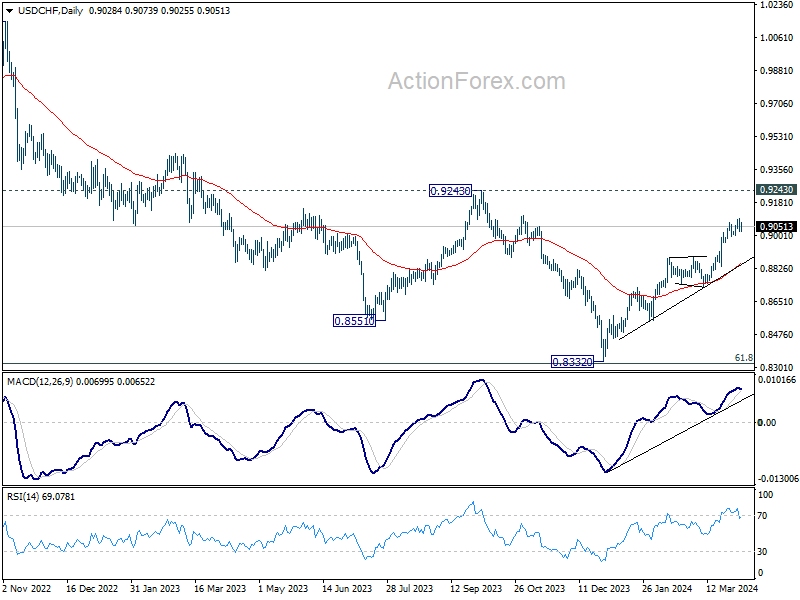

The Swiss franc is lower on Thursday. Early in the North American session, USD/CHF is trading at 0.9050, up 0.24%. It has been a bumpy year for the Swiss franc, which is down 7.7% against the US dollar and is trading at its lowest level since November.

Switzerland’s inflation rate eases to 1%

Switzerland is the envy of most major economies, with a very low inflation rate. Inflation rose by just 1% y/y in March, down from 1.2% and below the market estimate of 1.3%. This was the lowest level since September 2021.

Inflation has stayed within the Swiss National Bank’s target of 0-2% for ten straight months and policy makers at the central bank can give themselves a pat on the back for a job well done. The SNB had embarked on a rate hike-cycle in order to prevent inflation from breaching the upper band of the target, but with inflation now falling, there is the concern that inflation could fall too low, which could lead to deflation.

The SNB trimmed rates in March by quarter-point, the first major central bank to lower rates. This brought the SNB’s key rate to 1.5%. The SNB meets every quarter, and today’s inflation report has raised expectations that another cut is coming at the June meeting.

In the US, unemployment claims were higher than expected, at 221,000 last week. This was higher than the previous reading, which was revised to 212,000 and beat the market estimate of 214,000. The nonfarm payrolls report, a critical indicator, will be published on Friday. The market estimate stands at 200,000 for March, compared to 275,000 a month earlier.

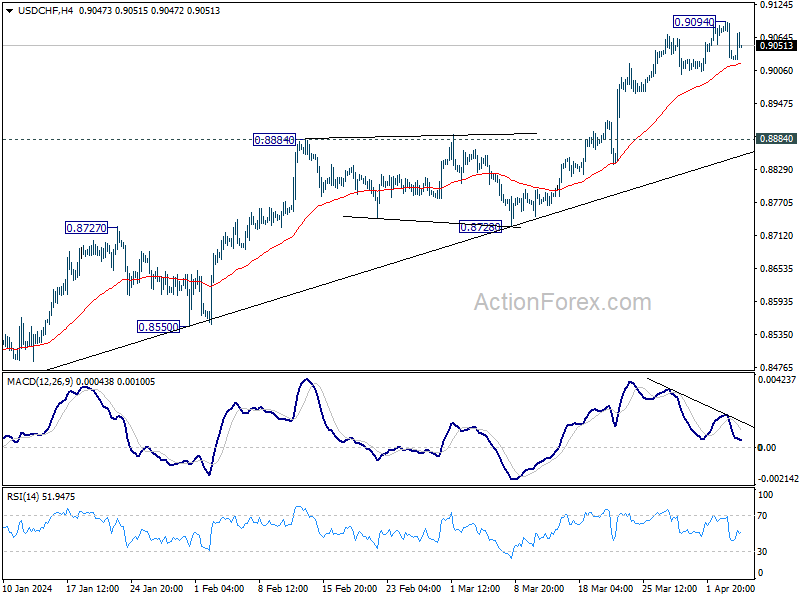

USD/CHF Technical

- USD/CHF tested resistance at 0.9074 earlier. Above, there is resistance at 0.9119

- 0.9050 and 0.9005 are providing support

Sunset Market Commentary

Markets

What a difference a revision makes… So often overlooked final figures of monthly (EMU) PMI broke headlines today. The euro area economy returned to growth for the first time since May 2023 after an upwardly adjusted composite PMI (50.3 from 49.9). Further growth expectations are the most optimistic since the start of the Russian invasion in Ukraine back in February 2022. Renewed growth in business activity was aided by a stabilization of demand and continued efforts to clear backlogs of work. Inflationary pressures are easing though both input and output costs remain above pre-pandemic averages. The rate of job creation weakened slightly from February’s 7-month high. On a country level, Spain and Italy provided the greatest boosts with their growth rates accelerating to the strongest for nearly a year (composite PMI’s of respectively 55.3 and 53.5). Contractions in Germany and France were smaller than initially feared. In spite of the positive surprise coming from these PMI’s, markets didn’t even blink. Minutes of the March ECB policy meeting confirmed that the central bank is on track to lower its policy rate in June: “While it was wise to await incoming data and evidence, the case for considering rate cuts was strengthening.” With the timing of a first move “coming more clearly into view”. The EMU economy is expected to be weak for two more quarters with the ECB becoming increasingly confident on inflation. The jury remains out for H2 2024 policy decisions though with the central bank also admitting that the inflation profile is expected to be bumpy after the summer (low comparative base). On top, they expected oil prices to decline when presenting new GDP and CPI forecasts in March (avg Brent oil price $79.6/b compared to $90/b currently). We stick with to the view that EMU money markets are too aggressively banking on follow-up rate cuts after June (leaning to 3 additional ones by December). As for PMI’s, the market impact of ECB Minutes was non-existing. Weekly jobless claims were today’s only US eco release. They continue to hover near extremely low levels (221k from 212k), leaving it up to tomorrow’s payrolls report to decide on the fate of technical tests of resistance levels across the US yield curve. Trading was one stretched yawn during most of European dealings with one erratic move (core bonds higher; Bunds outperforming US Treasuries) at the onset of US trading. It’s somewhat of a continuation of yesterday’s rebound. The dollar continues drifting south with EUR/USD currently changing hands around 1.0870.

News & Views

Swiss CPI showed unchanged prices in March from February. Y/Y-inflation slowed from 1.2% to 1%. The stability of the index compared with the previous month was the result of opposing trends that offset one another overall. Prices for international package holidays and air transport increased, as well as those for clothing and footwear. Prices for supplementary accommodation and cars decreased, as did those for hire of private means of transport. Core inflation rose 0.1% M/M and 1% Y/Y (from 1.1%). Domestic prices declined 0.2% M/M, but were still 1.8% higher compared to last year. The disinflationary impact of prices of imported products eases as prices rose 0.7% M/M (-1.3% Y/Y). Inflation settled over the previous months well within the SNB’s target range (0%-2%) and justifies the 25 bps March SNB rate cut. With inflation at target, the SNB also wants to avoid a further rise in the real effective exchange rate to the franc. This aim is materializing. EUR/CHF today rose to 0.984, from below 0.92 at the turn of the year.

Minutes of the Riksbank’s March policy meeting confirmed that Swedish inflation has fallen slightly more than expected with forward looking indicators pointing to a continued fall in price pressures. Inflation (both CPIF including and excluding energy) is expected to return to 2% next year. Improving inflation prospects and the lower risk of inflation becoming entrenched at too high levels suggest that the RB approaches the situation where the need to conduct a contractionary monetary policy is declining. In this context, governor Thedeen sees “some probability of a policy rate cut in May, on condition that inflation prospects, including the development of the krona, do not deteriorate significantly”. Thedeen sees a fast start of the cutting cycle as providing greater flexibility to proceed cautiously with further adjustments to the interest rate. Despite the prospect of a ‘frontloaded’ May rate cut, the Swedish krona strengthened slightly today (EUR/SEK 10.51 currently). This might have been partially due to a strong rebound in the county’s PMI confidence indicators (composite PMI 52.8 from 50.6; Services PMI 53.9 from 51.2).

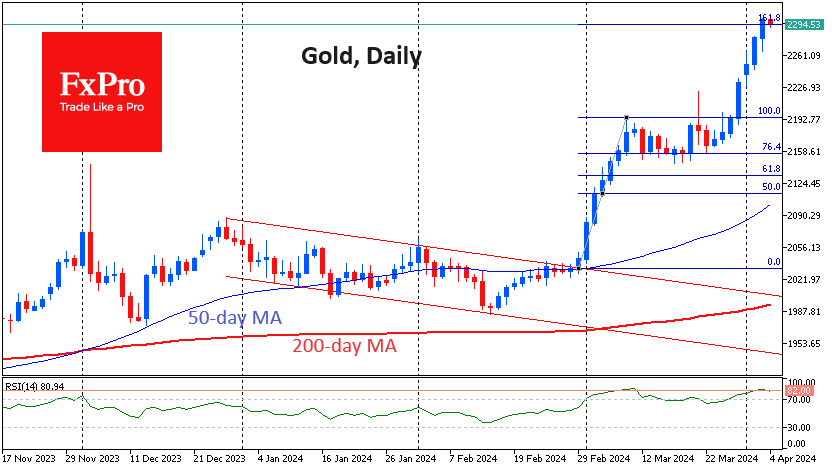

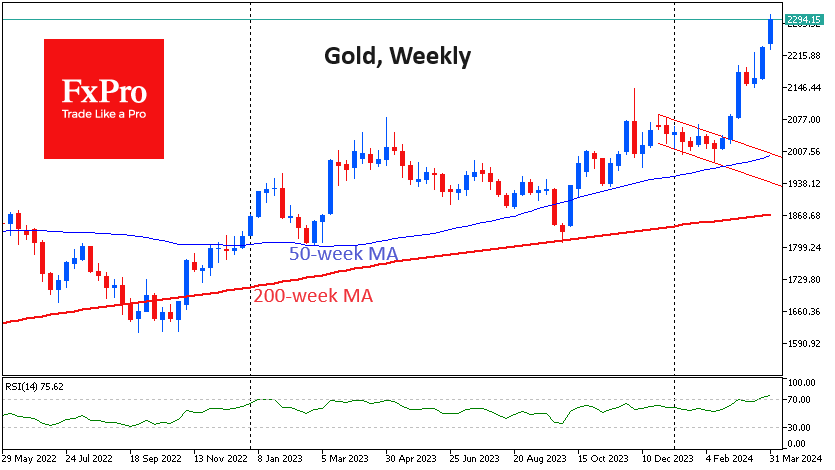

Gold Too Hot

Overnight, the gold price briefly exceeded $2300, recording another round level, not counting an update of the all-time high. This is an occasion to assess gold’s prospects, which are becoming a little less unambiguous.

Touching the level of $2300 marked the achievement of the 161.8% Fibonacci retracement of the growth impulse from 29 February to 8 March. Then gold proved bullish as it continued to gain strength above the 50-day moving average. The subsequent long consolidation with a shallow correction confirmed the strong bullish sentiment of the metal. Gold has added every trading session since 25 March but has so far been subdued since the start of the day on Thursday morning. The next step in this pattern is profit-taking, allowing the price to cool somewhat.

On the daily timeframes, the RSI on Wednesday was close to the early March peaks, after which the past consolidation began. The bears took control in March 2022 at similar overbought levels. However, in July 2020, the price continued to grow after reaching similar RSI parameters. In similar conditions in 2019 and 2020, there was a growth stop but not a reversal. The balance of power is in favour of the bears.

Friday’s NFPs have repeatedly served as a turning point for gold, and they could be again this time. The March release halted gold’s rally: the November, December and February releases triggered a sell-off, and the October release was the final point of a five-month downtrend.

Now is the time for bulls to be wary of the importance of labour market data for gold. They have a lot to lose as the price flew into space, partly ignoring the latest economic data coming out on the dollar’s side, from strong manufacturing PMIs to the acceleration in wage growth that ADP talked about on Wednesday.

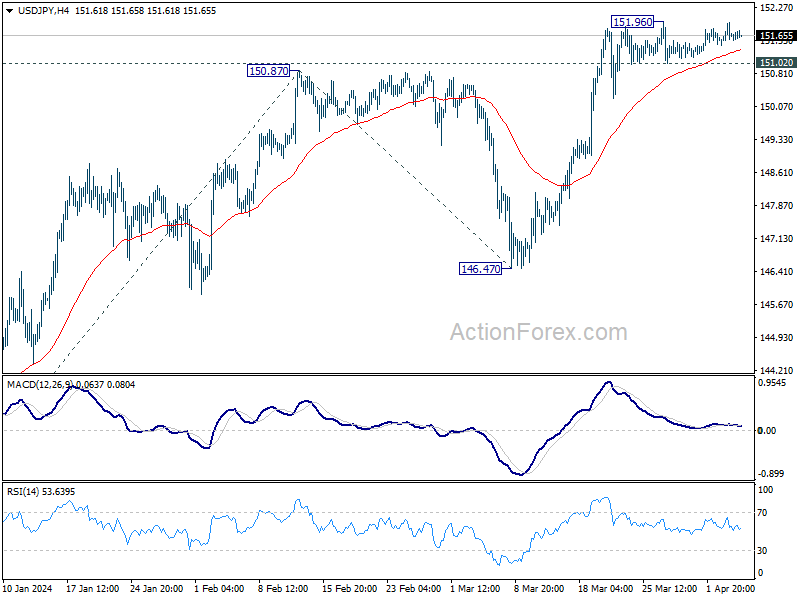

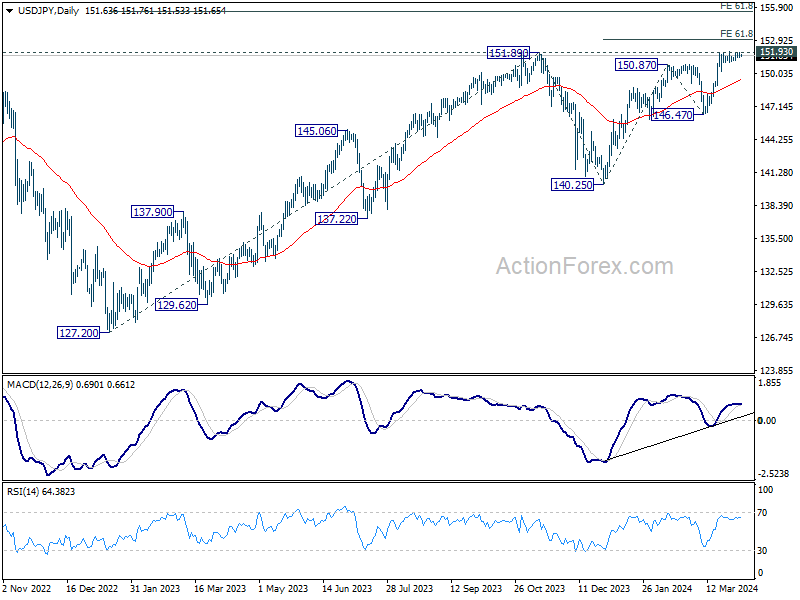

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.44; (P) 151.70; (R1) 151.96; More...

No change in USD/JPY's outlook as range trading continues. Intraday bias remains neutral. On the downside, break of 151.02 support should confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 149.51). Nevertheless, sustained break of 151.93 key resistance will confirm long term up trend resumption. Next near term target will be 61.8% projection of 140.25 to 150.87 from 146.47 at 153.03.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9005; (P) 0.9050; (R1) 0.9074; More....

Intraday bias in USD/CHF remains neutral for consolidation below 0.9094. On the downside, break of 55 4H EMA (now at 0.9018) will bring deeper pullback. But downside should be contained by 0.8884 resistance turned support to bring rebound. On the upside, break of 0.9094 will resume larger rise from 0.8332 to 0.9243 key resistance.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

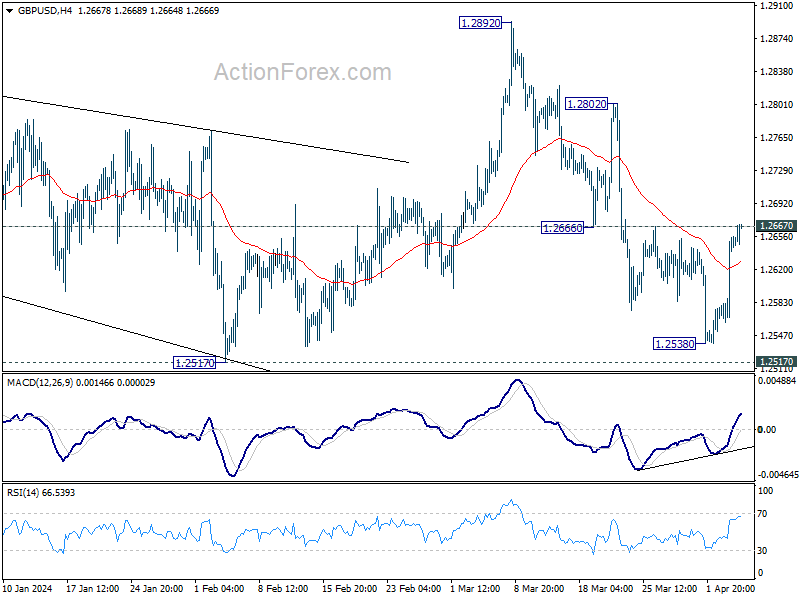

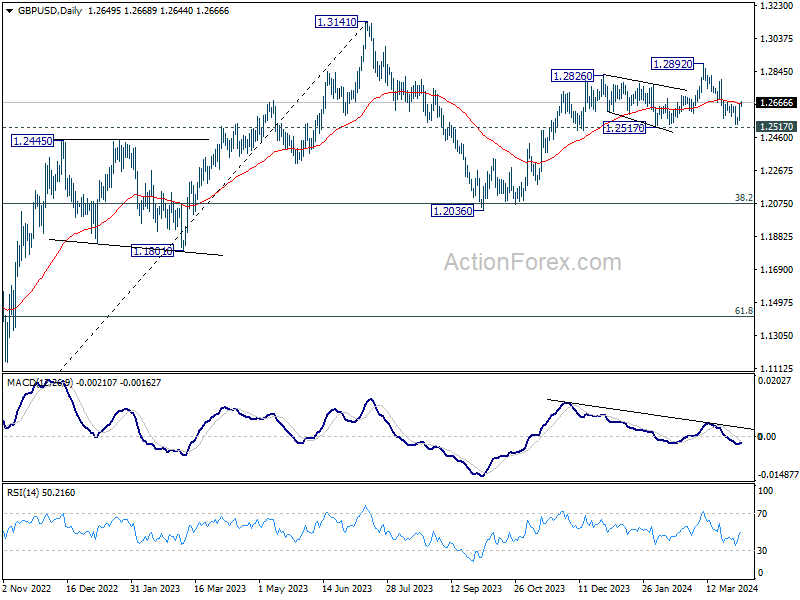

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2592; (P) 1.2624; (R1) 1.2685; More...

Immediate focus is now on 1.2667 resistance. Firm break there will suggest that fall from 1.2892 has completed at 1.2538. Intraday bias will be turned back to the upside for 1.2802 resistance next. On the downside, below 55 4H EMA (now at 1.2628) will bring retest of 1.2538 instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which might still be in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0788; (P) 1.0812; (R1) 1.0861; More...

Intraday bias in EUR/USD remains on the upside at this point. Rise from 1.0723 is seen as the third leg of the corrective pattern from 1.0694. Further rally would be seen to 1.0941/0980 resistance zone. On the downside, though, below 55 4H EMA (now at 1.0807) will bring retest of 1.0694/0723 support zone instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

Swiss Franc Plummets on CPI Data Which Fuels Expectations of Further SNB Easing

Swiss Franc faced broad selling pressure in European session, driven by CPI lower than CPI data. Inflation in Switzerland slowed to its lowest since September 2021 at 1.0%, and remained within the SNB's target range for the tenth consecutive month. This development sparked speculation among market participants about the possibility of further monetary easing by SNB, with some expecting a rate cut in each of June and September. SNB had already taken a lead among major central banks by cutting its key rate to 1.5% in March, and more could be in the queue.

On the other hand, Australian Dollar gained momentum from the continued rally in precious and industrial metals, with New Zealand and Canadian Dollars trailing behind. Japanese Yen is currently as the second weakest currency for the day, following Swiss Franc, while Dollar and Sterling showed relative weakness. Euro, however, saw a slight uplift due to upward revision in PMI Services data, coupled with the ECB's meeting minutes, which reinforced expectations for a potential rate cut in. At the same time, ECB's meeting accounts came in as expected, indicating that suitability for June for rate cut rather than April.

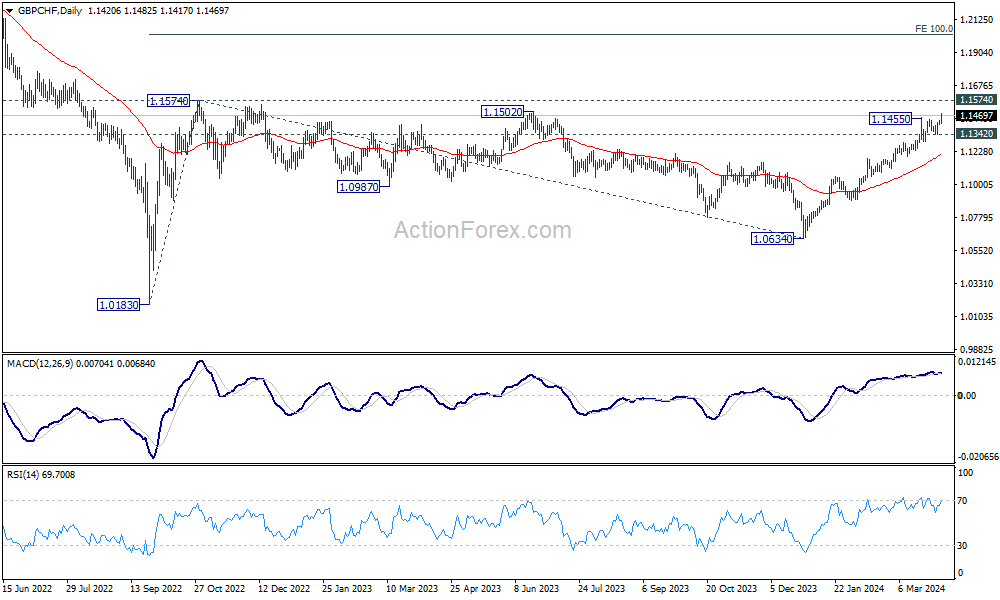

Technically, GBP/CHF's rally from 1.0634 resumed by breaking through 1.1455 resistance today. Near term outlook will stay bullish as long as 1.1342 support holds. Decisive break of 1.1574 resistance will confirm resumption of whole medium term rise from 1.0183 (2022 low), and set the stage for 100% projection of 1.0183 to 1.1574 from 1.0634 at 1.2025.

In Europe, at the time of writing, FTSE is up 0.41%. DAX is up 0.06%. CAC is down -0.15%. UK 10-year yield is down -0.0508 at 4.010. Germany 10-year yield is down -0.029 at 2.372. Earlier in Asia, Nikkei rose 0.81%. Japan 10-year JGB yield rose 0.0114 to 0.778. Singapore Strait Times rose 0.38%. Hong Kong and China were on holiday.

ECB March meeting accounts: Consensus against immediate rate cut, eyes on June for Data

ECB's March meeting accounts unveiled a unified stance among Governing Council members against discussing rate cuts at that time, citing it as "premature." However, the narrative within the ECB is evolving, with increasing acknowledgment that "the case for considering rate cuts was strengthening," pointing towards a strategic shift contingent on forthcoming economic data.

The meeting underscored a collective patience to assess more comprehensive data before making decisive moves on interest rates. Specifically, the council highlighted the importance of the June meeting, which will benefit from new staff projections and a broader array of data, particularly concerning "wage dynamics." This contrasts with the April meeting, where available data would be "much more limited," thus making it harder to be sufficiently confident in the ongoing disinflation process's durability.

ECB's deliberations reflect caution over the sustainability of disinflation, especially concerning "services and domestic inflation." The uncertain prospects for wage growth, productivity, and profit margins are central to these concerns. For ECB to consider rate reductions with greater confidence, incoming data must align with March's ECB staff projections, affirming that disinflation will consistently head towards the ECB's target.

Eurozone PMI services finalized at 51.5, gradually finding its footing

Eurozone PMI Services was finalized at 51.5 in March, up from February's 50.2, a 9-month high. PMI Composite was finalized at 50.3, up from prior month's 49.2, a 10-month high.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, said the service sector is "gradually finding its footing." He further highlighted the importance of wage growth outpacing inflation, enhancing households' purchasing power and supporting the service sector's revival. However, he tempered expectations by noting, "a full-fledged boom is not on the horizon."

Despite economic challenges, service providers have continued to expand their workforce. Moreover, business expectations within the service industry have soared to their highest in over two years, surpassing the long-term average.

Meanwhile, March witnessed a slight deceleration in inflation regarding both costs and sales prices, a development likely to be viewed favorably by ECB. Despite this positive sign, de la Rubia cautioned against premature conclusions about a turning trend in inflation, maintaining the forecast that interest rate cuts are more likely in June than in April.

UK PMI Services finalized at 53.1, inflation pressures persist

UK PMI Services was finalized at 53.1 in March, down from February's 53.8. PMI Composite was finalized at 52.8, down from prior month's 53.0.

Tim Moore, Economics Director at S&P Global Market Intelligence, said, "The solid growth rate achieved in March reinforces the view that a rebound in service sector performance is helping the UK economy to pull out of last year's shallow recession."

Meanwhile, Input prices have continued to rise sharply, with inflation rates only slightly below their six-month average. The primary factors contributing to the uptick in input costs include higher salary payments and increased transportation bills.

The rate at which prices charged by service providers have increased slowed to its lowest point since September 2023. Despite this deceleration, the index remains well above its long-term trend, signaling enduring inflationary pressures within the UK's domestic economy.

Swiss CPI falls to 1% yoy in Mar, misses expectations

Swiss CPI was flat month-over-month in March, below expectation of 0.3% mom. Core CPI (excluding fresh and seasonal products, energy and fuel) rose 0.1% mom. Domestic products prices fell -0.2% mom. Imported products pries rose 0.7% mom.

Over the 12-month period, CPI slowed from 1.2% yoy to 1.0% yoy, below expectation of 1.4% yoy. Core CPI slowed from 1.1% yoy to 1.0% yoy. Domestic products prices slowed from 1.9% yoy to 1.8% yoy. Imported products prices fell from -1.0% yoy to -1.3% yoy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0788; (P) 1.0812; (R1) 1.0861; More...

Intraday bias in EUR/USD remains on the upside at this point. Rise from 1.0723 is seen as the third leg of the corrective pattern from 1.0694. Further rally would be seen to 1.0941/0980 resistance zone. On the downside, though, below 55 4H EMA (now at 1.0807) will bring retest of 1.0694/0723 support zone instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Feb | 14.90% | -8.80% | -8.60% | |

| 00:30 | AUD | Building Permits M/M Feb | -1.90% | 3.20% | -1.00% | -2.50% |

| 06:30 | CHF | CPI M/M Mar | 0.00% | 0.30% | 0.60% | |

| 06:30 | CHF | CPI Y/Y Mar | 1.00% | 1.40% | 1.20% | |

| 07:45 | EUR | Italy Services PMI Mar | 54.6 | 53.2 | 52.2 | |

| 07:50 | EUR | France Services PMI Mar F | 48.3 | 47.8 | 47.8 | |

| 07:55 | EUR | Germany Services PMI Mar F | 50.1 | 49.8 | 49.8 | |

| 08:00 | EUR | Eurozone Services PMI Mar F | 51.5 | 51.1 | 51.1 | |

| 08:30 | GBP | Services PMI Mar | 53.1 | 53.4 | 53.4 | |

| 09:00 | EUR | Eurozone PPI M/M Feb | -1.00% | -0.70% | -0.90% | |

| 09:00 | EUR | Eurozone PPI Y/Y Feb | -8.30% | -8.60% | -8.60% | -8.00% |

| 11:30 | USD | Challenger Job Cuts Y/Y Mar | 0.70% | 8.80% | ||

| 11:30 | EUR | ECB Meeting Accounts | ||||

| 12:30 | CAD | Trade Balance (CAD) Feb | 1.4B | 0.5B | 0.5B | 0.6B |

| 12:30 | USD | Trade Balance (USD) Feb | -68.9B | -66.0B | -67.4B | -67.6B |

| 12:30 | USD | Initial Jobless Claims (Mar 29) | 221K | 212K | 210K | 212K |

| 14:30 | USD | Natural Gas Storage | -42B | -36B |