Sample Category Title

ECB March meeting accounts: Consensus against immediate rate cut, eyes on June for Data

ECB's March meeting accounts unveiled a unified stance among Governing Council members against discussing rate cuts at that time, citing it as "premature." However, the narrative within the ECB is evolving, with increasing acknowledgment that "the case for considering rate cuts was strengthening," pointing towards a strategic shift contingent on forthcoming economic data.

The meeting underscored a collective patience to assess more comprehensive data before making decisive moves on interest rates. Specifically, the council highlighted the importance of the June meeting, which will benefit from new staff projections and a broader array of data, particularly concerning "wage dynamics." This contrasts with the April meeting, where available data would be "much more limited," thus making it harder to be sufficiently confidenct in the ongoing disinflation process's durability.

ECB's deliberations reflect caution over the sustainability of disinflation, especially concerning "services and domestic inflation." The uncertain prospects for wage growth, productivity, and profit margins are central to these concerns. For ECB to consider rate reductions with greater confidence, incoming data must align with March's ECB staff projections, affirming that disinflation will consistently head towards the ECB's target.

(ECB) Monetary policy accounts

Account of the monetary policy meeting of the Governing Council of the European Central Bank held in Frankfurt am Main on Wednesday and Thursday, 6-7 March 2024

4 April 2024

1. Review of financial, economic and monetary developments and policy options

Financial market developments

Ms Schnabel noted that, since the Governing Council's previous monetary policy meeting on 24-25 January 2024, monetary policy expectations had retracted further from the early and large interest rate cuts initially foreseen at the turn of the year.

More favourable news on the global economy and less favourable news on inflation had both been key factors in shaping financial market developments. In the case of the first factor, macroeconomic data surprises had moved into positive territory in the euro area, the United States and China for the first time since May 2023. As a result, investors attached a discernibly lower probability to the scenario of a hard landing for the global economy.

The second factor related to a reassessment of the medium-term inflation outlook. Higher than expected inflation releases in the euro area and the United States, especially for core inflation, had dented investors' hopes of rapid and smooth disinflation. Looking at the path of headline and core inflation in the euro area (as measured, respectively, by the Harmonised Index of Consumer Prices – HICP – and the overall index excluding energy and food) over 2024, inflation-linked bond markets were pricing in somewhat higher headline inflation rates throughout the year, compared with expectations at the time of the Governing Council's monetary policy meeting in January.

In response to investors' expectations of lower downside tail risks to economic activity and a slightly bumpier path of disinflation, rate markets had priced in a substantially shallower easing cycle in the euro area, with expected cumulative interest rate cuts by the end of 2024 having declined notably from around 160 basis points in late December to around 90 basis points at present. After the latest repricing, the gap between expectations in interest rate markets and those reported by market analysts had largely disappeared.

In the United States, strong labour market data, higher than expected inflation figures and more cautious communication by the Federal Reserve System had triggered an even greater repricing of policy rate expectations. As a result, overnight index swap (OIS) forward curves were also pricing in a substantially shallower easing cycle in the United States.

A key explanatory factor for expectations of a synchronised monetary policy easing cycle across advanced economies was the common component in global inflation. Markets anticipated that the disinflationary momentum would continue unfolding synchronously over the coming year. Spillovers from the United States were another factor explaining the close co-movement of monetary policy expectations across jurisdictions. US data releases continued to exert a significant influence on yields in other advanced economies.

A decomposition of euro area and US OIS rates across different maturities into inflation compensation and real rates showed that, in the euro area, inflation compensation had increased notably across the curve. At the same time, real rates had declined, in particular at the longer end, implying a mild loosening of financing conditions through risk-free rates. In the United States, the rise in inflation compensation was slightly less pronounced, with real rates remaining firm across the curve.

The widening yield differential had been mirrored by a slight depreciation in the euro's exchange rate against the US dollar. In nominal effective terms, the euro had remained broadly unchanged, while the US dollar had appreciated.

Despite the repricing of the near-term inflation outlook, risks to the longer-term inflation outlook had not materially changed since January 2024, as the five-year forward inflation-linked swap (ILS) rate five years ahead had remained broadly unchanged. Compared with the close-to-peak levels at the September 2023 Governing Council meeting, ILS forward rates had come down materially, driven mostly by a decline in inflation risk premia. The sharp past tightening seemed to have been effective in containing and eventually lowering risks to the longer-term inflation outlook. Nevertheless, the five-year forward ILS rate five years ahead still stood markedly above its historical mean. Consistent with ILS rates, euro area option prices also indicated that risks of high inflation had come down but remained somewhat elevated compared with historical averages.

Risk asset markets appeared to have looked through the tightening impulse stemming from expectations of a later and shallower easing cycle, supported by improved risk sentiment. The benchmark stock market indices across all major advanced and emerging economies, including China, had followed a bullish trend since the Governing Council's January meeting.

The buoyant risk sentiment had also been visible in corporate bond markets. The same was true for sovereign bond markets, where spreads over German Bunds had continued to narrow, with the differential between Italian and German ten-year government bond yields at its smallest since March 2022. Investors appeared to remain keen on locking in attractive returns amid expectations that the peak of the tightening cycle had been reached. Bid-to-cover ratios continued their gradual upward trend, pointing to strong demand for bonds despite record high sovereign issuance for the year to date.

Despite the benign price developments across risk asset markets, some pockets of risk were emerging, for example related to the commercial real estate market, but these had not had broader repercussions for financial intermediaries and markets. Moreover, the continued rally in riskier market segments – despite the repricing of monetary policy expectations – and stretched valuations of some assets could point to complacency in financial markets.

The global environment and economic and monetary developments in the euro area

Starting with the global outlook, Mr Lane noted that global economic activity was still subdued but there were some signs of improvement. Trade momentum in goods and services was expected to strengthen in the first quarter of the year. The March ECB staff macroeconomic projections for the euro area foresaw a significant pick-up in euro area foreign demand, in line with previous exercises. Euro area foreign demand was projected to grow by 2.4% in 2024, 3.1% in 2025 and 3.2% in 2026, reflecting expectations of a normalisation in demand for goods, which would benefit European producers. As for commodities, since the last meeting oil prices had increased, while gas prices had declined further. International metal prices had also declined, although food prices had edged up.

Turning to the euro area, Mr Lane recalled that, according to the recent Eurostat flash release, euro area headline inflation had declined to 2.6% in February from 2.8% in January. While energy inflation had become less negative, partly owing to the withdrawal of some fiscal support, food inflation had fallen strongly to 4.0% in February from 5.6% in January. This reflected an easing in both processed and unprocessed food inflation. Core inflation had decreased to 3.1% in February from 3.3% in January. Over the same period, the rate of non-energy industrial goods inflation had decelerated to 1.6% from 2.0%. Services inflation had edged down by 0.1 percentage points to 3.9%. Inflation in wage-sensitive services remained higher than in non-wage-sensitive services, supporting the view that high wage growth was playing an important role in elevated services inflation.

Most measures of underlying inflation had declined further in January, as the impact of past adverse supply shocks continued to fade, lower energy prices reduced cost pressures and tighter monetary policy weighed on demand. At the lower end of the range, the indicator of the Persistent and Common Component of Inflation had been close to 2% since November. However, the annual growth rate of the indicator of domestic inflation was unchanged at 4.5%. Domestic price pressures as measured by growth in the GDP deflator were still high, although the deflator was projected to continue to decrease gradually. Profit growth offered a first buffer against high labour cost pressures and would recover thereafter.

According to the March ECB staff projections, growth in compensation per employee was estimated to have slowed to 4.8% in the fourth quarter of 2023, from 5.3% in the third quarter. Based on already available country data, the forthcoming release of euro area data on 8 March for the growth in compensation per employee in the fourth quarter of 2023 was expected to turn out slightly lower than projected. Negotiated wage growth including one-off payments had declined in the fourth quarter by 0.2 percentage points to 4.5%. The latest signals from the ECB forward-looking wage trackers also indicated a gradual slowing of negotiated wage growth in the euro area. Additionally, the contribution from wage drift – the most cyclically sensitive element of compensation – had declined visibly, having been around 2 percentage points at the start of 2022. Both the Indeed tracker and feedback from firms participating in the ECB's Corporate Telephone Survey pointed to lower wage growth this year compared with 2023. Moreover, profits seemed to be absorbing part of the rising labour costs, which would reduce their inflationary effects.

Inflation was expected to continue its downward path in the coming months. In the near term, there would likely be some volatility in headline inflation owing to base effects in the energy component and to the timing of Easter. Thereafter, headline inflation was expected to decline to the ECB's target as labour cost dynamics moderated and past energy shocks, supply bottlenecks and pandemic reopening effects dissipated. Headline inflation was projected to average 2.3% in 2024, 2.0% in 2025 and 1.9% in 2026. Relative to the December projections, headline inflation had been revised down by 0.4 percentage points for 2024 and 0.1 percentage points for 2025, while remaining unchanged for 2026. Core inflation projections had been revised down across the projection horizon to 2.6% for this year, 2.1% for 2025 and 2.0% for 2026. This implied downward revisions to core inflation of 0.1 percentage points for this year, 0.2 percentage points for next year and 0.1 percentage points for 2026.

Upside risks to inflation included the heightened geopolitical tensions, especially in the Middle East, which could push energy prices and freight costs higher in the near term and disrupt global trade. Inflation could also turn out higher than anticipated if wages increased by more than expected or profit margins proved more resilient. By contrast, inflation could surprise on the downside if monetary policy dampened demand more than expected, or if the economic environment in the rest of the world worsened unexpectedly.

Economic activity in the euro area had remained weak in the first two months of 2024. Consumers continued to hold back on spending, housing investment had remained subdued and companies had exported less, reflecting a slowdown in external demand and some losses in competitiveness. Business investment had also remained weak, reflecting the impact of restrictive monetary policy, the depletion of order backlogs and subdued demand.

Forward-looking indicators such as Purchasing Managers' Indices (PMIs) were improving but remained at low levels overall. While surveys pointed to a gradual recovery in economic activity over the course of the year, the recovery was expected to proceed at a slower pace than previously anticipated. This reflected the carry-over from the recent weaker data outturns for 2023 and the still-subdued level of survey indicators. As inflation fell and wages kept growing, real incomes would rebound, supporting growth. Further ahead, both housing and business investment should be supported by an easing of financing conditions. Business investment was also expected to pick up as demand strengthened. In addition, demand for euro area exports should improve as global demand rebounded and price competitiveness pressures eased.

With respect to domestic demand components, the projections saw a significant pick-up in consumption in 2024. Investment was expected to contract as a result of the ongoing transmission of monetary policy tightening and was hence not expected to contribute to the recovery this year. The recovery would instead be led by consumption and exports, with goods consumption playing a key role. This was, in turn, interconnected with the projection for labour costs. Unit labour costs were seen as decelerating more quickly than compensation per employee over the projection horizon, owing to the expected pick-up in productivity. Manufacturing output, especially, had been depressed, but labour had not yet been shed, which resulted in a higher ratio of employment to output and hence lower labour productivity. The projections suggested that a recovery in output – and especially manufacturing output – would be achieved through a recovery in productivity. Taken together, these factors explained the glide path back to the inflation target.

Employment had grown by 0.3% in the final quarter of 2023, again outpacing economic activity. The unemployment rate had edged down to a historical low of 6.4% in January from 6.5% in December, which itself had been revised up. Meanwhile, employers were announcing fewer job vacancies and fewer firms were reporting that their production was being limited by labour shortages.

As for the labour market, the construction and manufacturing sectors remained basically in stagnation or even contraction, with the latest employment PMIs remaining well below 50. Looking at services, in the high-tech sector employment PMIs remained at levels slightly above 50, while in the low-tech sector they had recovered strongly and stood above 55. There was also a noticeable decline in the number of firms reporting that labour was limiting their production possibilities – especially in services.

The new ECB staff projections indicated subdued growth in the near term, followed by a recovery thanks to rising real incomes, the fading impact of past monetary policy tightening on financing conditions and improving foreign demand. Output growth was expected to average 0.6% in 2024, 1.5% in 2025 and 1.6% in 2026. Relative to the December projections, growth had been revised down by 0.2 percentage points for 2024, while it was unchanged for 2025 and had been revised up by 0.1 percentage points for 2026. The fiscal outlook in the March 2024 projections was little changed from the December 2023 projections.

The risks to economic activity remained tilted to the downside. Growth could be lower if the effects of monetary policy turned out stronger than expected. A weaker world economy or a further slowdown in global trade would also weigh on euro area growth. Russia's unjustified war against Ukraine and the tragic conflict in the Middle East were major sources of geopolitical risk. This could result in firms and households becoming less confident about the future and global trade being disrupted. Growth could be higher if inflation came down more quickly than expected, if rising real incomes meant that spending increased by more than anticipated, or if the world economy grew more strongly than expected.

Turning to the monetary and financial analysis, market interest rates had increased since the last monetary policy meeting. The transmission of past policy rate hikes to broader financing conditions remained strong. Lending rates on business loans had broadly stabilised, while mortgage rates had declined in December and January. Nevertheless, lending rates remained elevated at 5.2% for business loans and 3.9% for mortgages.

High bank lending rates, tight credit standards and lower business investment continued to dampen demand for loans with longer maturities. The annual growth rate of bank lending to firms, which had turned positive and stood at 0.5% in December, had edged lower again in January, reaching 0.2% owing to a negative flow in the month. The year-on-year growth in loans to households had continued to weaken, slowing to 0.3% in January.

The annual growth rates of M3 – the broad monetary aggregate – and M1 – the narrow monetary aggregate of currency in circulation and overnight deposits – had remained weak in January, standing at 0.1% and -8.6% respectively. After standing in negative territory until November, the annual growth rate of M3 had been marginally positive in December and January. The increase in M3 was mostly explained by the strengthening of net inflows from the rest of the world, driven mainly by the strong trade surplus amid weak imports. Weak deposit creation continued to underpin a shift in bank funding composition towards more expensive funding sources.

Monetary policy considerations and policy options

Based on the assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission, at the meeting Mr Lane proposed keeping the three key ECB interest rates unchanged.

The three elements of the Governing Council's reaction function supported an unchanged policy at the meeting. Headline inflation was now projected to be markedly lower in 2024 compared with previous expectations, returning to target by mid-2025 and slightly undershooting 2% in subsequent quarters. Growth was expected to recover only gradually through most of 2024. The overall trend in underlying inflation continued to soften. At the same time, some key measures including domestic inflation remained elevated, while further confirmation was still needed concerning the projected outlook for wage inflation and unit margins. The third criterion, namely the ongoing strong transmission of monetary policy, was confirmed, albeit with some signs of stabilisation owing to the anticipation of future rate cuts.

Based on those three criteria, the key ECB interest rates were at levels that, maintained for a sufficiently long duration, would make a substantial contribution to the ECB's goal of returning inflation to its medium-term target in a timely manner. This warranted continuing to follow a data-dependent approach to determining the appropriate level and duration of restriction, while ensuring that policy rates would be set at sufficiently restrictive levels for as long as necessary. An overall evaluation of the policy trajectory could be obtained from the joint evolution of the inflation outlook (including the new staff projections), underlying inflation and the strength of monetary transmission in recent months. The developments here should increase confidence that the monetary policy decisions already taken would deliver the ECB's medium-term inflation target, especially in view of the projected narrowing of the distance to the target already in 2024. At the same time, only further along in the disinflation process could the ECB be sufficiently confident that inflation would hit the target in a timely manner and settle at target sustainably.

Mr Lane also proposed preserving the option to apply flexibility in reinvesting redemptions coming due in the pandemic emergency purchase programme (PEPP) portfolio, with a view to countering risks to the monetary policy transmission mechanism related to the pandemic.

2. Governing Council's discussion and monetary policy decisions

Economic, monetary and financial analyses

As regards the external environment, while global GDP growth remained subdued, there were early signs of improvement. A broad set of early indicators suggested that global growth had declined throughout 2023, reflecting tight monetary policy working its way through the global economy and fading tailwinds for consumption, such as from pandemic-related excess savings. Indicators had improved at the turn of the year, so global growth was expected to pick up in the first quarter of 2024 following a moderation in the last quarter of 2023. Global trade had also showed early signs of improvement at the start of 2024. The post-pandemic factors that had caused a period of weak trade in 2023, for example owing to the rotation of demand from goods to services, should ease in the period ahead. As regards key global economies, growth in the United States had been above expectations in the last quarter of 2023 and the labour market had been robust. At the same time, the Chinese economy continued to struggle with a weakening housing sector. Overall, it was underlined that the global economic outlook was still uncertain.

Turning to energy commodities, oil prices were expected to decline because of the supply surplus in the global market, which was expected to persist in 2024 despite OPEC+ producers having announced production cuts. European gas prices had fallen further since the Governing Council's last monetary policy meeting, as demand remained subdued and gas storage levels were relatively high. Nevertheless, it was highlighted that gas prices were volatile. With respect to the international determinants of consumer price inflation, price pressures were limited – despite the tensions in the Red Sea area – as demand for goods was still weak and inventory levels remained high.

With regard to economic activity in the euro area, members concurred with Mr Lane that the economy remained weak. Consumers continued to hold back on their spending, investment had moderated and companies were exporting less, reflecting a slowdown in external demand and some losses in competitiveness. However, surveys pointed to a gradual recovery over the course of the year. As inflation was falling and wages continued to grow, real incomes would rebound, supporting growth. In addition, the dampening impact of past interest rate increases would gradually fade and demand for euro area exports should pick up. The unemployment rate was at its lowest since the start of the euro. Employment had grown by 0.3% in the final quarter of 2023, again outpacing economic activity. As a result, output per person had declined further. Meanwhile, employers were posting fewer job vacancies and fewer firms were reporting that their production was being limited by labour shortages.

Members widely acknowledged the weaker than expected growth in the short term. Economic activity had stagnated for five quarters in a row and was expected to remain weak for two more quarters. Moreover, risks were seen to be on the downside, as mechanical nowcasting tools still showed lower numbers than those in the March projections for the first and second quarters of 2024. Consequently, the euro area economy was so far not showing convincing signs of improvement, which would likely imply six quarters of economic stagnation. Across sectors, there was also no indication of a recovery in manufacturing or construction, while private consumption, investment and external demand had remained weak overall throughout 2023.

At the same time, it was pointed out that data available since the last Governing Council meeting had confirmed the bottoming-out of the euro area economy, which was being supported by foreign demand recovering and the continued solid growth in the United States, as well as recently some more positive news about China. The most recent PMIs for the euro area had been stronger than expected, with services moving back into expansionary territory, while manufacturing remained weak but stood significantly above the trough of last summer. New orders had also been steadily increasing in the manufacturing and services sectors since November.

Members expressed broad agreement with the latest macroeconomic staff projections. It was emphasised that the March projections had seen the fifth consecutive downward revision to growth and the second downward revision to inflation for 2024, with also a downward revision to inflation for 2025. The macroeconomic projections had now broadly converged with the Consensus Economics forecasts, both for 2024 and for 2025.

At the same time, it was noted that the projections for growth and inflation, as well as credit developments, were pointing to a benign outlook, in which both a hard landing and a credit crunch would be avoided. The macroeconomic projections overall showed an encouraging picture, with an outlook that was well on track to bring inflation back to target. Revisions were becoming smaller, so there was reason to have more confidence in the baseline projections, although the risks to the growth outlook were still tilted to the downside, at least in the short term. Moreover, the contributions of cyclical and structural factors to growth and longer-term potential were hard to disentangle in real time.

The main drivers of the expected recovery were increasing real incomes, higher government consumption, improving terms of trade and monetary policy becoming less restrictive. Private consumption was expected to pick up once real household income started to gradually improve, supporting a concomitant recovery in business investment. In this context, it would be important for investment to resume in line with what was necessary for the digital and green transformations, which would ultimately also reduce medium-term price stability risks and benefit monetary policy by increasing the robustness of the supply side of the economy.

In addition, fiscal policy was seen as a key driver of economic growth over the projection horizon, in terms of both government consumption and public investment, in particular through the Next Generation EU (NGEU) programme. The release of the final 2023 deficit figures in the coming weeks should enable a clearer assessment of the fiscal policy stance. Several countries were running excessively high deficits, which might pose challenges further down the road. However, it was mentioned that in some countries the fiscal imbalances stemmed to a large extent from shortfalls in tax receipts, reflecting the weak economy, rather than from spending overruns.

It was reiterated that governments should continue to roll back energy-related support measures to allow the disinflation process to proceed sustainably. Fiscal and structural policies should be strengthened to make the euro area economy more productive and competitive, expand supply capacity and gradually bring down high public debt ratios. A speedier implementation of the NGEU programme and more determined efforts to remove national barriers to deeper and more integrated banking and capital markets could help increase investment in the green and digital transitions and reduce price pressures in the medium term. The EU's revised economic governance framework should be implemented without delay.

Turning to the labour market, it was widely stressed that a thorough understanding of the market remained crucial for assessing the outlook for wages and inflation. This applied not just to wage dynamics but also to labour productivity. It was pointed out that the share of firms citing labour shortages as a constraint on output remained high but had been falling, pointing to less labour market tightness. However, firms continued to hoard labour, which could be interpreted as a sign that they were trying to avoid shortages in the future. Labour hoarding would allow them to meet a future resurgence in demand with the workforce already in place, which had positive implications for labour productivity.

Additionally, it was remarked that monetary policy transmission remained strong, with a significant portion of recent downward revisions to the growth outlook seeming to stem from monetary policy having a more forceful effect on growth than expected. Looking ahead, the projected improvement in economic activity was also based on rate cuts as embedded in the market rate assumptions underpinning the projections.

Against this background, members assessed that the risks to economic growth remained tilted to the downside. Growth could be lower if the effects of monetary policy turned out stronger than expected. A weaker world economy or a further slowdown in global trade would also weigh on euro area growth. Russia's unjustified war against Ukraine and the tragic conflict in the Middle East were major sources of geopolitical risk. This could result in firms and households becoming less confident about the future and global trade being disrupted. Growth could be higher if inflation came down more quickly than expected and rising real incomes meant that spending increased by more than anticipated, or if the world economy grew more strongly than expected.

The point was made that two scenarios could unfold if downside risks to economic activity materialised. In one possible scenario, weak demand would lead to a slowdown in profit and wage growth and inflation would be dampened. In an alternative downside scenario, however, the projected recovery in productivity would not materialise. Given the ongoing strength of wage developments, weaker economic growth could translate into higher unit labour costs, contributing to upside domestic price pressures and slowing down the disinflation process.

With regard to price developments, members concurred with the assessment presented by Mr Lane in his introduction and welcomed the recent decline in inflation, reflecting a faster than anticipated disinflationary process. This was partly due to the unwinding of past supply shocks but was also a sign that monetary policy was working. Over the past year both headline and core inflation had fallen by several percentage points, and even services inflation had declined over the past six months. The latest staff projections suggested that inflation would, at least temporarily, already reach a trough close to target in the second half of 2024, which was much earlier than previously expected. On this basis, the view was expressed that the disinflation process was making good progress.

At the same time, it was mentioned that the disinflationary process remained bumpy and fragile, and that a timely and sustainable return to target as foreseen in the projections still relied on a sufficiently restrictive monetary policy stance. Inflation momentum, as measured by the annualised three-month-on-three-month rate, had jumped for all HICP components except food. This was consistent with the latest PMIs showing that the share of services firms indicating rising selling prices had steadily increased since November, which posed upside risks to the inflation outlook, especially for core inflation. One important upside risk was associated with energy prices, which had recently eased significantly. For gas prices, in particular, risks were strongly tilted to the upside, as shown by option-implied distributions. It was important to keep in mind that wrong assumptions on energy prices would eventually feed through to all inflation components, either through input prices or indirectly, via wages. That implied that the benign inflation outlook in the latest projections depended critically on the favourable energy price assumptions. Moreover, the combination of El Niño and La Niña, in conjunction with the impact of global warming and climate change, was creating upside risks for food prices. It was added that month-on-month figures showed that core inflation had again been on the rise for the last couple of months, which called for continued caution on the inflation outlook.

Services inflation, with the latest figure at 3.9%, had barely moved from the 4% recorded for November, which lent further support to the picture of "last mile" persistence in that component of inflation. In January, around 90% of the services consumption basket had still been growing at an annual rate above 2%. The turnaround in services inflation had started late, only from July 2023, and services inflation had lost a mere 1.7 percentage points of the 4 percentage point increase observed since the start of the pandemic. Given the large and rising weight of services in euro area value added, this stickiness had significantly restrained the overall disinflation process. At the same time, monetary policy transmission to services inflation might be weaker and slower than in manufacturing, as services tended to be less capital-intensive and hence less exposed to changes in external financing conditions. In the October 2023 Corporate Telephone Survey, services firms had reported hardly any impact of financing conditions on their past or future activity, in part reflecting their large cash buffers. Moreover, less exposure to global competition meant there was less pressure on services firms to absorb rising costs by curtailing their margins. Overall, this evidence was consistent with the notion that monetary policy transmission to services inflation worked mainly indirectly, through the effect of monetary policy on inflation expectations and wages, as well as through a general dampening of aggregate demand. Furthermore, the rotation of consumption from goods back to services and the resilience of the labour market might have weakened even this indirect transmission channel. All this argued for perseverance in keeping monetary policy sufficiently restrictive. While the progress on inflation had indeed been encouraging, the February inflation figure was a warning sign that the last mile was likely to be more uncertain, slower and bumpier.

At the same time, it was recalled that services inflation had always been more persistent. Although it had indeed remained stubbornly high for the last four months, that was to be expected and had already been incorporated in the projections. Moreover, owing to weaker productivity growth in the services sector, services inflation had traditionally been higher on average than the overall inflation rate. While the annual growth rate of services inflation in February had still been too high, its momentum had been on a falling trend since April 2023 and had been close to 2% in January 2024, although it had picked up again in February to 3.1%. In this context, it was also mentioned that between November and January services inflation had been pushed up by developments in transport, insurance services and package holidays. These components were not classified as wage-sensitive. More generally, it was argued that wage-sensitive components had not exerted particular upward pressure on services inflation since last June. Services inflation had mainly been higher than goods inflation because of the rotation of demand from goods to services after the pandemic, with the result that it had started to increase later, had peaked later and had started to decrease later. The point was made that services inflation had also been higher than in a normal disinflation episode because wages had responded at a slower pace to the supply shock from energy prices. Given the price level gap between goods and services, it was at present not clear whether services prices would converge to goods prices or the other way round.

Turning to wage and profit developments, members recalled that information on the nexus of wages, profits and productivity remained a key element in building confidence around the inflation outlook. There were still several question marks over all three elements of this nexus, so more evidence was needed before it could be concluded that inflation had durably turned the corner. The March 2024 staff projections foresaw a significant decline in the growth of unit labour costs, which had been revised down for 2025 and 2026 compared with the December 2023 projections. But convincing evidence was yet to emerge that nominal wage growth was coming down as expected and, in particular, that firms were absorbing the higher unit labour costs through their profits. Revisions compared with the December staff projections implied significantly stronger contributions from unit profits to domestic inflation than had been expected, and the GDP deflator had so far remained stubbornly above 5%. While the most recent data on profits in 2023 were encouraging, a much stronger absorption of higher labour costs by lower profit margins needed to materialise over 2024.

Furthermore, the projections envisaged a steady recovery of productivity growth over the projection horizon. This might not materialise if the observed slowdown in productivity growth was due not only to cyclical factors such as labour hoarding, but also to factors such as a change in the composition of the labour force, structurally higher sick leave or a shift in employment towards the services sector, which could make the productivity slowdown more persistent. More generally, a significant part of the current weakness in manufacturing was likely to be of a structural nature, which would have different implications for the evolution of inflation, particularly as previous downward revisions to potential output growth might prove insufficient. At the same time, it was mentioned that labour productivity was procyclical in the euro area, so that when economic activity was subdued, weak productivity developments could also be interpreted as a sign of excessive monetary policy tightening.

Incoming information on wages in many countries suggested that wage developments continued to deserve special attention. While the data for the whole euro area on compensation per employee for the fourth quarter of 2023 were not yet available, information had already been received for 15 euro area countries. That information suggested wage growth had slowed significantly in the fourth quarter of last year. As regards the GDP deflator, the headline figure for the fourth quarter had already been released for some countries and incorporated in the March ECB staff projections. The incoming wage growth figures for the first quarter of 2024 from the Indeed tracker based on job adverts could be seen as a leading indicator for negotiated wages. These figures suggested that negotiated wage increases could slow further. Especially when comparing with the inflation outlook contained in the September 2023 staff projections, the subsequent downside inflation surprises had diminished the need for nominal wages to catch up with past inflation.

The question was also raised whether, in the near future, profit margins would be able to keep absorbing the rise in unit labour costs. Otherwise, businesses might increasingly pass on higher unit labour costs by raising prices. In 2022 the level of profits had been atypically high, which suggested that there was sufficient room for margins to compress and that profits would likely be affected by weak demand.

As regards longer-term inflation expectations, members took note of the assessments by Ms Schnabel and Mr Lane of the latest developments in market-based measures of inflation compensation and survey-based indicators. Market-based measures of inflation compensation had come down notably and remained broadly anchored at 2%.

Upside risks to inflation included the heightened geopolitical tensions, especially in the Middle East, which could push energy prices and freight costs higher in the near term and disrupt global trade. Inflation could also turn out higher than anticipated if wages increased by more than expected or profit margins proved more resilient. By contrast, inflation could surprise on the downside if monetary policy dampened demand more than expected, or if the economic environment in the rest of the world worsened unexpectedly.

Turning to the monetary and financial analysis, members largely concurred with the assessments provided by Mr Lane and Ms Schnabel in their introductions. Market interest rates had risen since the Governing Council's previous meeting. These had converged towards the views of analysts and now priced in three fewer interest rate cuts in 2024, with an 85% probability of a first rate cut in June. It was argued that this repricing reflected a recognition that disinflation was going to be slower and less certain than previously expected. In addition, spillovers from higher market interest rates in the United States were also mentioned. Market expectations for future interest rates were seen as broadly in line with macroeconomic fundamentals, including the inflation outlook and interest rate assumptions as embedded in the latest staff projections.

Financial markets had continued to function well but might be underpricing risk in some asset categories. Spreads on high-yield corporate bonds in the euro area had narrowed to levels not seen for the past 15 years but could widen if defaults picked up. Sovereign bond spreads had also continued to narrow but could increase as a result of fiscal risks. Equity markets appeared buoyant, especially in the United States. Meanwhile, the euro exchange rate had changed little, both against the US dollar and in nominal effective terms.

Members agreed that the ECB's restrictive monetary policy had been transmitted strongly to broader financing conditions for firms and households and that these conditions remained tight. It was remarked that a reduced supply of liquidity was also contributing to monetary tightening, owing to ongoing and prospective reductions in the asset purchase programme (APP) and PEPP portfolios, as well as maturing targeted longer-term refinancing operations. Interest rates on business loans had broadly stabilised and mortgage rates had declined in December and January. This had contributed to a slight easing in financing conditions, but lending rates remained elevated in historical terms. Furthermore, continued repricing of the outstanding stock of loans was also contributing to a strong transmission of the past rate hikes. Bank funding costs were high, and banks were tightening lending standards and increasingly favouring safer assets as the riskiness of borrowers increased. This had negative implications for credit supply. It was also contended that because new loans were less risky their risk-adjusted cost was actually still rising.

There were signs that annual growth in bank loans to firms was stabilising at low levels, notwithstanding some volatility in monthly flows around the turn of the year. Meanwhile the growth in loans to households continued to weaken in annual terms. Broad money, as measured by M3, was growing at a subdued annual rate, with the three-month annualised growth rate momentum rebounding somewhat since mid-2023. It was also argued that the impact of credit tightening had been stronger than expected, especially on mortgage lending. Additionally, the outlook for credit remained moderate, owing to the substantial impact of high interest rates and tight credit standards over the projection horizon. Caution was expressed about assuming that a turning point in lending growth had been reached. Attention was drawn to analysis suggesting that the ratio of corporate bank loans to GDP was projected to fall to historical lows of below 35% in the coming quarters. At the same time, it was argued that the staff projections did not entail a credit crunch. Also, credit dynamics still appeared to suggest a soft landing, given increasing evidence that loan growth had reached a trough. Moreover, declining bank funding costs should also support slightly lower lending rates on new loans. In that context, it was argued that the peak of monetary policy transmission to bank lending volumes might have been reached.

Some concerns were expressed that financial stability risks were emerging, given signs of financial distress among low income households. The proportion of mortgage holders struggling to meet payments was rising rapidly to historical highs, which would probably persist for an extended period. The risks facing some non-financial firms and the risks from the commercial real estate sector were also highlighted. Against this background, banks' non-performing and underperforming loans were increasing, which could make it tougher for non-financial corporates to access bank credit. Narrow spreads on high-yield bonds were currently a mitigating factor, but if spreads were to increase owing to higher default rates, non-financial corporates' access to debt financing could suffer. At the same time, bank equity prices remained elevated overall, suggesting that asset quality risks remained contained.

Monetary policy stance and policy considerations

Turning to the monetary policy stance, members assessed the data available since the last monetary policy meeting in accordance with the three main elements that the Governing Council had communicated in 2023 as shaping its reaction function. These comprised (i) the implications of the incoming economic and financial data for the inflation outlook, (ii) the dynamics of underlying inflation, and (iii) the strength of monetary policy transmission. Overall, there had been further progress on all three elements, which warranted increased confidence that inflation was on track to reach the ECB's target in a timely and sustainable manner. However, more data and evidence were needed for the Governing Council to be sufficiently confident of this.

Starting with the inflation outlook, members broadly concurred with the assessment that had been presented by Mr Lane in his introduction. Inflation was continuing to decline towards the 2% target broadly as expected, and this good progress was seen as encouraging. The fact that inflation had been slightly higher than anticipated in February was not seen as changing this general picture. Nevertheless, it was argued that the associated increase in momentum for all HICP components except food, as measured by the annualised three-month-on-three-month rate of inflation, was a warning. A more uncertain, slower and bumpier disinflation process could lie ahead. Still, inflation was expected to continue its downward trend in the coming months – near-term projections having been revised down compared with the December staff projections – and to show continued moderation in 2024. A bumpy profile and a trough were expected after the summer, driven by base effects. Further ahead, inflation was on track to decline to the 2% target as a result of moderating labour costs and the fading effects of past energy shocks, supply bottlenecks and the post-pandemic reopening of the economy. According to the latest staff projections, inflation was expected to be back at target – or even slightly below target – in the medium term, and earlier than had been previously anticipated, especially compared with the September 2023 staff projections.

Members agreed that most measures of underlying inflation had declined further since the last monetary policy meeting, owing to the indirect effects of lower energy prices receding, the impact of past supply shocks fading and tight monetary policy weighing on demand. The staff projections for core inflation had also been revised down. It was now expected to fall to 2% in 2026. However, domestic price pressures were still elevated, owing to a combination of robust wage growth, falling labour productivity and sticky services inflation. It remained to be seen whether unit labour costs would decline in line with the projections, which relied on a recovery in productivity growth together with moderating wage growth. Further uncertainty surrounded both the projected continued decline in the contribution of unit profits to the GDP deflator as well as the extent to which firms would absorb higher labour costs, rather than passing them on to consumers. It was also noted that, over the entire horizon, the March ECB staff projections for core inflation were at the lower end of a range of other forecasts. Continuing uncertainty about the effects of the wage-profits-productivity nexus on domestic inflation highlighted the need for caution and for more evidence that core inflation would continue to decline. At the same time, there were signs that wage growth was starting to moderate. In addition, profits were absorbing part of the rising labour costs, reducing their inflationary effects. Moreover, services inflation could be expected to be more persistent and lag behind other components of inflation.

Finally, members generally agreed that monetary policy transmission was working well, with less uncertainty about the strength of transmission than when interest rates were still rising. Monetary policy was being transmitted robustly to financial markets, financing conditions, credit conditions and aggregate demand. This had helped to lower inflation but had also weighed on growth – potentially more than had been expected and with measurable effects on small and young enterprises. It was recalled that a significant part of policy transmission remained in the pipeline, as the coming quarters would see the impact of past policy tightening continuing to be transmitted to bank funding conditions, broader financing conditions, credit volumes and the real economy. It was also argued that there would be some tightening in financing conditions in 2024 stemming from the contraction of the Eurosystem balance sheet. At the same time, it was contended that the tightening impulse from monetary policy was gradually fading. The point was made that financial and financing conditions – and thereby the effective monetary policy stance – had already eased and might continue to ease as markets repriced their rate expectations. Moreover, transmission was seen as weaker and slower for services inflation, which tended to be less capital-intensive and therefore less reliant on external financing.

Overall, members expressed increased confidence that inflation was on track to decline sustainably to the 2% inflation target in a timely manner. However, patience and caution were still needed, and more evidence and data were required for the Governing Council to be sufficiently confident that the task had been accomplished. It was therefore important not to be complacent, as the disinflationary process remained fragile and conditional on a number of benign assumptions about wages, profits and productivity. Furthermore, a smooth and sustainable return of inflation to target, as implied by the projections, was also contingent on the monetary policy stance remaining restrictive enough for long enough. At the same time, it was widely felt that, while there were clearly risks to the outlook, monetary policy was working and the disinflation process remained solid and robust. The view was taken that the risks of overshooting versus undershooting the ECB's symmetric inflation target in the medium term were broadly balanced or becoming more balanced.

Monetary policy decisions and communication

All members agreed with the proposal by Mr Lane to maintain the three key ECB interest rates at their current levels. There was consensus that it would be premature to discuss rate cuts at the present meeting. Instead, it was affirmed that it was important to be further along in the disinflation process and accumulate additional evidence for the Governing Council to be sufficiently confident that inflation was set to return to target in a timely and sustainable manner. It was reiterated that, based on its current assessment, the Governing Council considered the key ECB interest rates to be at levels that, maintained for a sufficiently long duration, would make a substantial contribution to returning inflation to its 2% medium-term target in a timely manner. Future decisions would ensure that policy rates would be set at sufficiently restrictive levels for as long as necessary.

Members underlined the need for policy to remain data-dependent and to continue to be based on the elements of the reaction function already communicated. While it was wise to await incoming data and evidence, the case for considering rate cuts was strengthening. This was based on the latest ECB staff projections, the further progress on the three criteria specified by the Governing Council in 2023, more contained projection errors and a more balanced risk assessment, with the date of a first rate cut coming more clearly into view. It was also recalled that the ECB's focus and mandate were price stability in the euro area, although spillovers from other major policy areas would naturally be taken into account.

It was highlighted that, in addition to new staff projections, the Governing Council would have significantly more data and information by the June meeting, especially on wage dynamics. By contrast, the new information available in time for the April meeting would be much more limited, making it harder to be sufficiently confident about the sustainability of the disinflation process by then. Questions remained about the sustainability of the disinflationary process, particularly in services and domestic inflation, on account of the uncertain outlook for wage growth, productivity growth and profit margins. In order to increase confidence that inflation would sustainably return to the ECB's target, incoming data needed to confirm that important assumptions and predictions about these indicators in the March ECB staff projections would indeed hold true.

Members also agreed with Mr Lane's proposal to continue applying flexibility in reinvesting redemptions falling due in the PEPP portfolio, in line with the Executive Board proposal presented by Ms Schnabel in her introduction.

Taking into account the foregoing discussion among the members, upon a proposal by the President, the Governing Council took the monetary policy decisions as set out in the monetary policy press release. The members of the Governing Council subsequently finalised the monetary policy statement, which the President and the Vice-President would, as usual, deliver at the press conference following the Governing Council meeting.

Monetary policy statement

Monetary policy statement for the press conference of 7 March 2024

Press release

Meeting of the ECB's Governing Council, 6-7 March 2024

Members

- Ms Lagarde, President

- Mr de Guindos, Vice-President

- Mr Centeno

- Mr Cipollone

- Mr Elderson

- Mr Hernández de Cos*

- Mr Herodotou

- Mr Holzmann

- Mr Kazāks

- Mr Kažimír*

- Mr Knot

- Mr Lane

- Mr Makhlouf

- Mr Müller

- Mr Nagel

- Mr Panetta

- Mr Reinesch

- Mr Rehn*

- Ms Schnabel

- Mr Scicluna

- Mr Šimkus

- Mr Stournaras

- Mr Vasle*

- Mr Villeroy de Galhau

- Mr Vujčić

- Mr Wunsch*

* Members not holding a voting right in March 2024 under Article 10.2 of the ESCB Statute.

Other attendees

- Ms Senkovic, Secretary, Director General Secretariat

- Mr Rostagno, Secretary for monetary policy, Director General Monetary Policy

- Mr Winkler, Deputy Secretary for monetary policy, Senior Adviser, DG Economics

Accompanying persons

- Ms Bénassy-Quéré

- Mr Dabušinskas

- Mr Demarco

- Mr Gavilán

- Mr Haber

- Mr Horváth

- Mr Kaasik

- Mr Koukoularides

- Mr Lünnemann

- Mr Madouros

- Ms Mauderer

- Mr Nicoletti Altimari

- Mr Novo

- Mr Sleijpen

- Mr Šošić

- Mr Tavlas

- Mr Välimäki

- Mr Vanackere

- Ms Žumer Šujica

Other ECB staff

- Mr Proissl, Director General Communications

- Mr Straub, Counsellor to the President

- Ms Rahmouni-Rousseau, Director General Market Operations

- Mr Arce, Director General Economics

- Mr Sousa, Deputy Director General Economics

Release of the next monetary policy account foreseen on 10 May 2024.

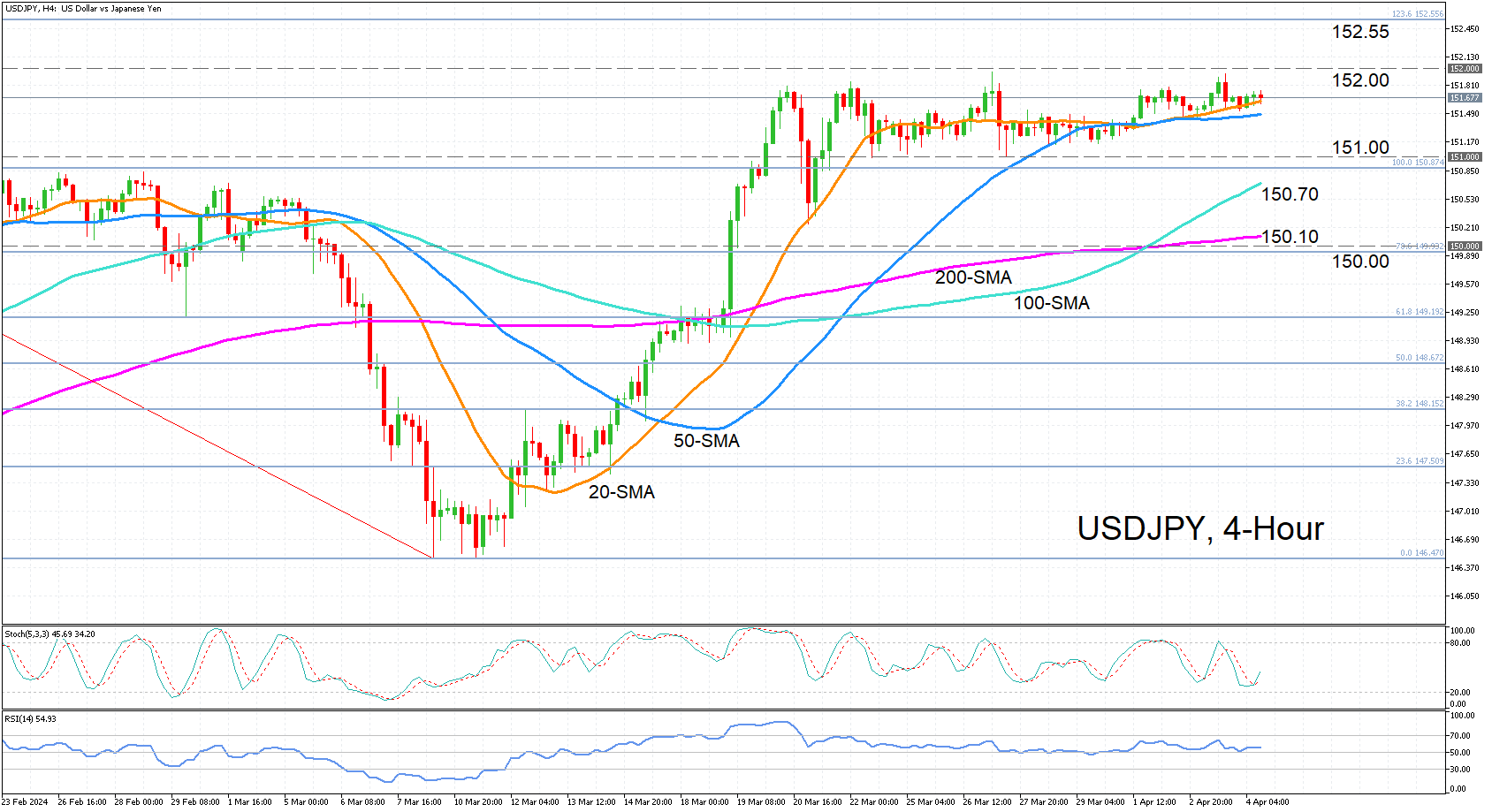

USDJPY Hovers Beneath 152 Ceiling as Bulls Refuse to Give Up

- USDJPY remains stuck within 151-152 range

- Neutral trend looks safe for now

- But strong support keeps bullish forces alive

USDJPY has been gradually inching higher after dropping near the floor of the sideway range at the end of March to briefly touch 151.01. Prices made it all the way to 151.94 on Wednesday before easing again.

However, with both the 20- and 50-day simple moving averages (SMA) lurking below the price action, there is still a possibility of a fresh attempt to break above the 152.00 ceiling in the near term. Looking at the momentum indicators, the stochastic oscillator is sending positive signals in the four-hour chart, as the %K line has crossed above the %D line. The RSI is somewhat more neutral as it remains flat, but it managed to hold above the 50 level after the latest dip.

Should the positive momentum gather more traction, the bulls will likely again target the 152.00 handle. A successful break above it would bring the 123.6% Fibonacci extension of the early February-March downleg at 152.55 into view. Further gains would turn attention to the 161.8% Fibonacci of 153.60.

However, if the bears manage to defend the 152.00 level in the coming days, a sharp pullback would become inevitable. The 151.00 floor would become the first major test in the negative scenario, with the 100-day SMA offering further support at 150.70, after which the 200-day SMA would come into scope at 150.10. A drop below the psychologically important level of 150.00 would shift the short-term risk to the downside.

In brief, USDJPY still stands a chance of hitting fresh 34-year highs. But the longer it lingers within its current sideways range without breaching the upper bound, the more likely that it will reverse lower at some point.

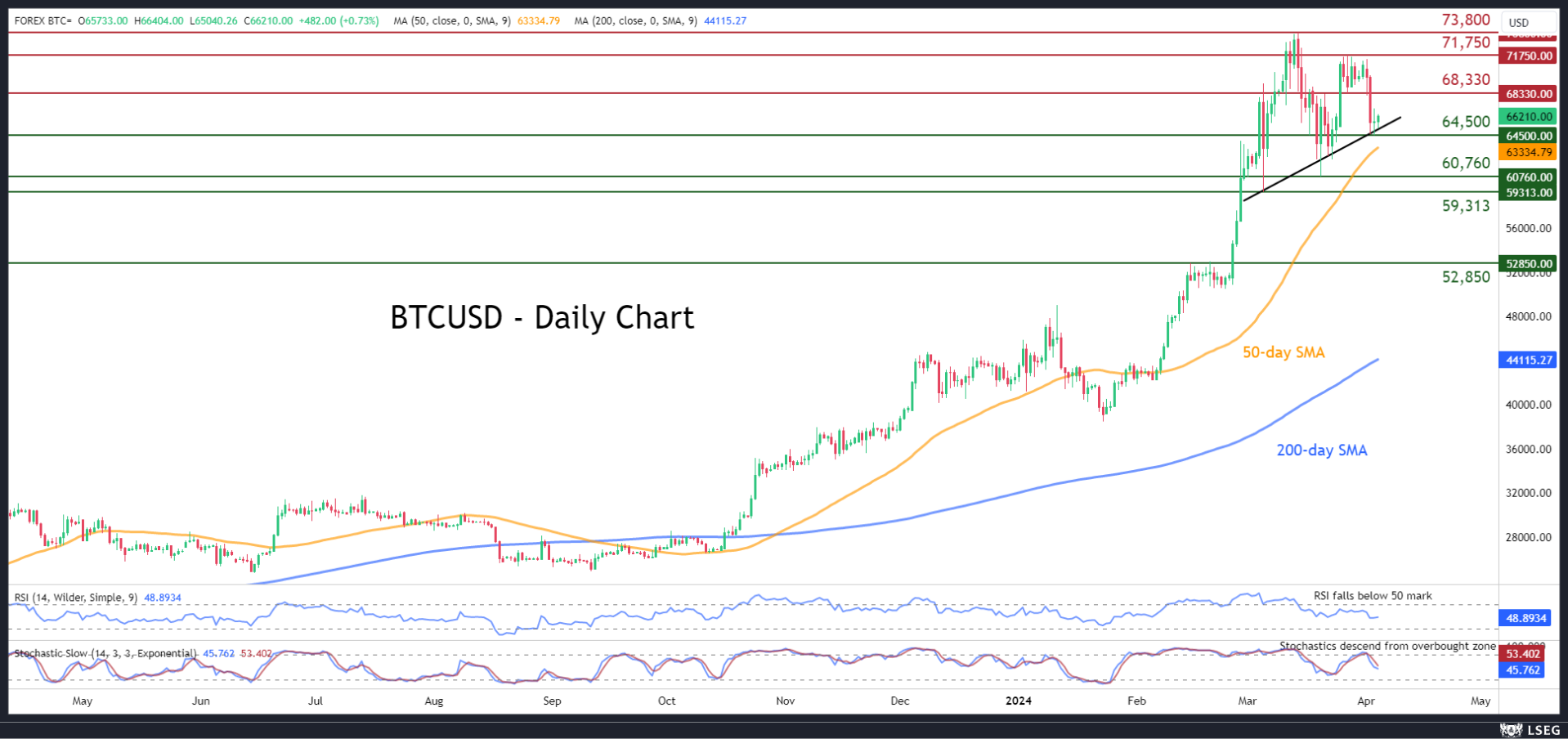

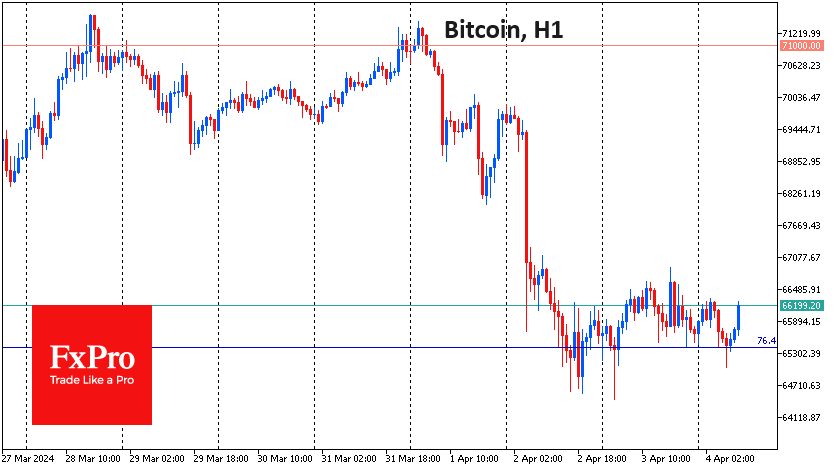

BTCUSD Pauses Pullback But Still Under Pressure

- BTCUSD halts its retreat and recoups some losses

- But momentum indicators remain tilted to the downside

BTCUSD (Bitcoin) experienced a strong pullback following its repeated inability to conquer the 71,750 hurdle. Although the price seems to be finding its footing in the last couple of sessions supported by a short-term ascending trendline, near-term risks remain tilted to the downside.

If bearish pressures persist, Bitcoin could revisit its recent support of 64,500. Further declines could then cease at the March deflection point of 60,760. Even lower, the March bottom of 59,313 may act as the next line of defence.

Alternatively, should the price move higher after its recent bounce, the March support of 68,300 could serve as initial resistance. A break above that region could pave the way for the March resistance region of 71,750. Failing to halt there, the price may ascend to retest its all-time high of 73,800.

In brief, BTCUSD appears to have put an end to its latest slide, but it is clearly not out of the woods just yet. That being said, a downside violation of the short-term ascending trendline might accelerate the recent pullback.

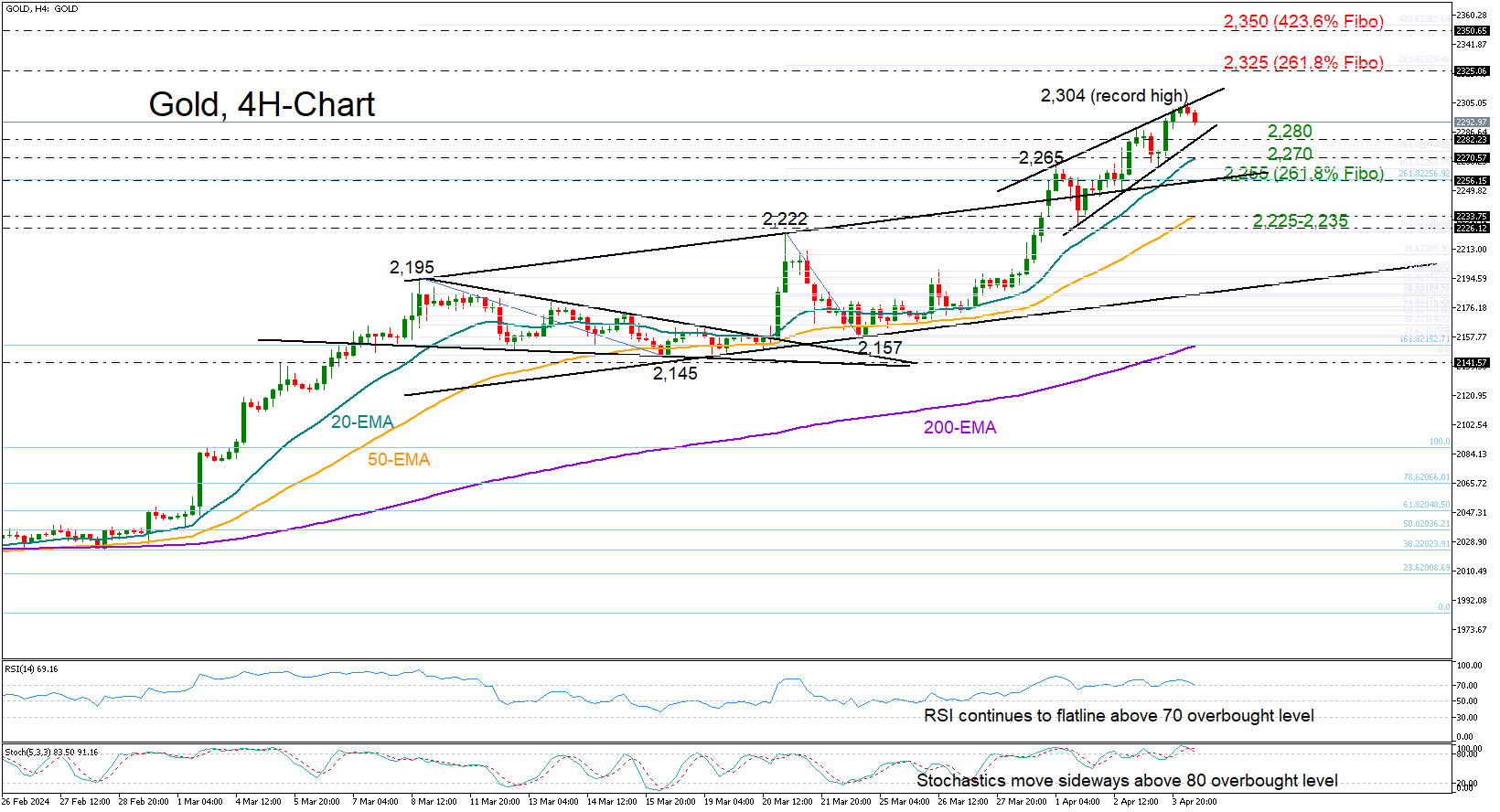

Gold Rally Turns Golden After Another Record

- Gold unlocks fresh all-time high

- Bullish wave could stabilize, but perhaps temporarily

Gold has been in an uninterrupted record rally over the past week, ticking to a new high of 2,304 before losing some steam early on Thursday.

While investors continue to debate the longevity of the bullish wave as the rate cut scenario remains a hot topic in the US, it is possible that some profit taking could occur. The pause near the short-term resistance line and the overbought signals coming from the RSI and stochastic oscillator endorse that case.

If the current weakness lingers, the price could retrace to the support trendline at 2,280. The 20-period exponential moving average (EMA) at 2,270 and the support-turned-into-resistance trendline at 2,255 will be closely monitored before the spotlight turns to the 50-period SMA and the 2,225 constraining zone. An extension lower would neutralize the short-term positive outlook.

Should the bull run resume above 2,300, the 261.8% Fibonacci extension of the 2,222-2,157 pullback at 2,325 could be the next obstacle. The 423.6% Fibonacci extension of the 2,195-2,145 downfall at 2,350 might attempt to stop the rally ahead of the 2,400 psychological level.

To sum up, the technical picture indicates an overstretched rally, but the market’s upward structure remains strong, suggesting that any potential pullback would be a normal part of the positive trend.

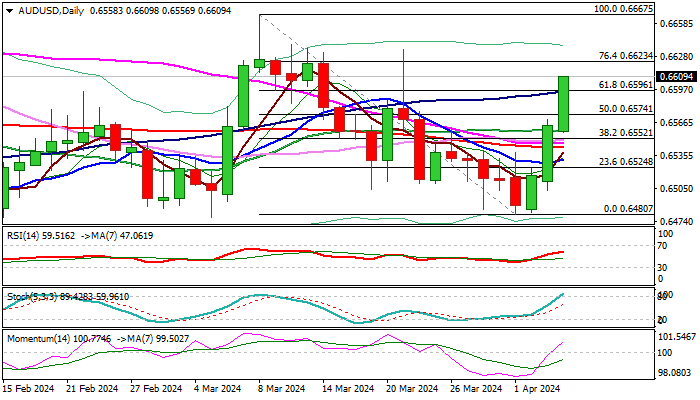

AUD/USD: Strong Recovery Cracks Pivotal Barriers at 0.6600 Zone

AUDUSD rallies for the third straight day, lifted by weaker US dollar and downbeat US services PMI data (released on Wednesday).

Bulls cracked pivotal 0.6600 resistance zone (double-Fibo/100DMA/round-figure), trading at these levels for the first time since Mar 21.

Improved picture on daily chart (momentum broke into positive territory and MA’s turned to bullish setup) contributes to positive outlook, with break and close above 0.6600 zone to open way for possible full retracement of 0.6667/0.6480 bear-leg.

However, overbought conditions warn that current rally may slow for consolidation, with bullish near-term bias to remain in play while the price action stays above broken daily Kijun-sen/50% retracement (0.6570).

Res: 0.6623; 0.6634; 0.6656; 0.6667.

Sup: 0.6596; 0.6570; 0.6552; 0.6537.

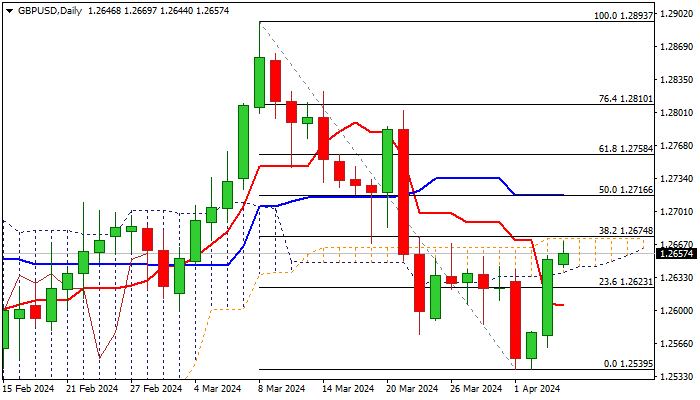

GBP/USD: Slight Bullish Bias Above 200-DMA But Thin Daily Cloud Still Significant Obstacle

Cable extends recovery from 1.2540 double bottom (Apr 1 / 2 lows) and pressuring significant barrier at 1.2674 (daily cloud top / Fibo 38.2% of 1.2893/1.2539), as bulls regained traction after a false break below pivotal 200DMA support (1.2586).

Near-term action is expected to keep slight bullish bias while holding above 200DMA, though sustained break above 1.2674 pivot is needed to confirm fresh bullish signal, after thin daily cloud capped a number of attempts higher.

Daily studies lack clear direction signal as MA’s are in mixed setup, RSI in sideways mode and holding in a neutral zone, while 14-d momentum is heading north but still in the negative territory.

Weaker dollar continues to underpin pound, but possibility of recovery stall on repeated failure to break through daily cloud, which would keep the downside at risk, should not be ignored.

Res: 1.2674; 1.2716; 1.2758; 1.2803.

Sup: 1.2638; 1.2586; 1.2539; 1.2518.

EUR/USD Extends Gains as Euro Services PMIs Improve

The euro is on a bit of a roll and has pushed slightly higher on Thursday. In the European session, EUR/USD is trading at 1.0857, up 0.19%. The euro is up for a third straight day and has climbed 0.8% since Monday.

Eurozone and German services PMIs accelerate

Business activity improved across the eurozone in March. The eurozone services PMI rose to 51.5, up from 50.2 in February. The German reading improved to a revised 50.1, up from 48.3 in February. This marks the first expansion in Germany’s services sector in six months. Spain, France and Italy all showed stronger expansion in March. The 50.0 line separates contraction from expansion.

The services sector has carried the eurozone economy as manufacturing continues to decline. The eurozone has managed to avoid a recession, but the economy remains fragile. At the same time, inflation has been falling faster than expected, and European Central Bank policy makers have the tough task of determining the appropriate time to start cutting the deposit rate, which is currently at a record high 4%.

The markets are anticipating a rate cut in June and some ECB members have publicly stated that they support such a move. ECB member Robert Holzmann, considered a hawk on rate policy, said on Wednesday that he isn’t against a June cut but would want to see more data before making a decision. Holzmann added that if the ECB lowers rates in June and the Federal Reserve stays on the sidelines, this would reduce the effectiveness of the ECB lowering its deposit rate.

In the US, employment numbers are in focus, with nonfarm payrolls on Friday. The markets are expecting a drop to 200,000 in March, compared to 275,000 a month earlier. Unemployment claims will be released later today and are not expected to show much change. The market estimate stands at 214,000, compared to the previous reading of 210,000.

EUR/USD Technical

- EUR/USD is testing resistance at 1.0849. Above, there is resistance at 1.0904

- 1.0808 and 1.0753 are providing support

Relatively Calm Bitcoin

Market picture

The crypto market rolled back another 0.9% in 24 hours to a capitalisation of $2.48 trillion – the lowest in a week and a half. Bitcoin reversed by the same amplitude, while there was no uniformity in dynamics among the top coins. Ethereum was unchanged for the day, remaining at $3300, Solana lost 3.1%, Dogecoin fell another 4%, BNB rose 4.2%, and Toncoin strengthened 0.3%. The Cryptocurrency Fear and Greed Index rolled back to 70, its lowest since 14 February.

Bitcoin ended Wednesday where it started the day, trading at $65.5K. Enthusiasts continue to buy back the first cryptocurrency on dips closer to $65K. On the other hand, Bitcoin’s inability to rise is alarming, although the day before, we saw a weaker dollar and stronger stock indices, which is fuelling risk appetite.

The cryptocurrency market’s lagging performance can easily be attributed to accumulated overbought conditions and wariness ahead of the monthly labour market report. At the same time, we regard the current weakness as consolidation within the bull market, almost excluding the risks of a long-term reversal.

News background

Spot trading volume on cryptocurrency exchanges reached $2.5 trillion in March, The Block calculated. That’s the highest since November 2021. The record of $4.1 trillion was set in May 2021. The total trading volume of BTC futures contracts in March rose 86% to $2.5 trillion.

According to data compiled by Bloomberg, March was a record-breaking month in terms of spot bitcoin-ETF trading volume. The figure nearly tripled from the previous month, from $42bn to $111bn. According to SoSoValue, three exchange-traded funds from Grayscale (GBTC), BlackRock (IBIT) and Fidelity (FBTC) continue to dominate trading volume. Meanwhile, total outflows from GBTC have reached $15bn since launch.

The crypto market can expect an outflow of liquidity due to the renewed appeal of gold with speculative investors, suggested Eric Balchunas, an ETF expert at Bloomberg.

A US government-controlled wallet with 30,174 BTC initiated a transfer of about 2000 BTC to the Coinbase Prime platform address. Experts have allowed the sale of assets. Presumably, this is part of the assets seized from the Silk Road darknet marketplace.

MN Trading founder Michael van de Poppe said that “at the peak of bullish momentum”, bearish narratives like the sale of bitcoins by US authorities have a “huge impact” on investor sentiment.

Regulatory questions directed to the SEC often need to be answered, suggesting a decline in the Commission’s genuine engagement with the public, said Hester Pearce, the agency’s commissioner.

Brent Oil Price Reaches Its Highest Since October 2023

The Brent oil chart today shows that the price has exceeded USD 89 per barrel — this is the highest level since the end of October 2023.

Reasons for strong demand for oil:

→ The OPEC+ meeting ended this week. Exporting countries maintained their policy of limiting oil production unchanged.

→ Ukrainian drone attacks on oil refineries in Russia.

→ Latest data on the strength of the US economy.

Technical analysis of the Brent market shows that:

→ The price moves within the ascending channel (shown in blue), which originates back in 2023.

→ Increased demand in the spring of 2024 led to the fact that the Brent price rose into the upper half of the blue channel and formed a steeper growth trajectory (shown by black lines).

→ The median line of the blue channel acted as support (shown by arrows).

The upper limit of the blue channel is around USD 92 per barrel of Brent and it is possible that the price may reach these values in the next 1-2 months.

However, the prerequisites for a correction are not currently in place after an increase of more than 5% over the last 5 trading sessions:

→ the RSI indicator indicates overbought;

→ the price is at the upper black line.

If a correction scenario is realized in the market, the Brent price may drop to the $87 level, which previously acted as resistance.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.