Sample Category Title

Sunset Market Commentary

Markets

(European) yields are extending a corrective decline that (re)accelerated at the start of the year. EMU short-term rates touched the highest levels since March early December, after comments from ECB’s Schnabel made markets fully embracing the idea that the case for further easing had become extremely thin. The debate even tentatively turned toward the timing of a potential first rate hike. For long-term yields, this upward momentum stretched further into December as markets understood that fiscal policy/deficit spending would have to do the heavy lifting as Germany/Europe has to address structural reforms and modernize its military capacities. However, the move ran into resistance in the final days of last year. Technical considerations and mild EMU data now even provide the perfect excuse to reduce bond short positions. Today’s EMU January inflation data perfectly fitted this pattern. EMU headline inflation at 2% J/J (0.2% M/M) returned to the ECB target. Core inflation softened slightly more than expected to 2.3% Y/Y (from 2.4%). Favorable energy base effects also are boding well for more sub-target EMU inflation data in the early months of 2026. Ongoing sticky services inflation (0.7% M/M and 3.4% Y/Y) in this mindset was easily put aside. We don’t see any reason for the ECB to change its firm wait-and-see stance due to this ‘technically-inspired’ inflation pattern. Even so, EMU swap yields are declining between 1.7 bps (2-y) and 4 bps (30-y). It’s too early to elaborate on the timing of a potential first rate hike. Joining this momentum trade, UK bonds even outperformed core EMU bonds with yields easing between 1.5 bps (2-y) and 7 bps (30-y). US yields initially followed this trend from some distance as investors awaited a set of US data that had/still has potential to amend expectations on the timing of further Fed easing. ADP reported December private job growth at a slightly softer than expected 41k. JOLTS (job openings) data and the US Services ISM still will be published after finishing this report. US yields currently are converging toward the EU pattern, declining between 1.5 bps (2-y) and 5 bps (30-y). The overall more benign mood on inflation probably is also supported by weak oil prices with Brent oil holding near $ 60 p/b. Equities are taking a breather after a solid start of the year (Eurostoxx 50 -0.1%, S&P 500 +0.1% still testing the all-time record).

On FX, moves in the major USD-cross rates are limited. The dollar basically holds its recent ‘gains’. DXY is changing hands near to 98.55. EUR/USD us going nowhere at 1.169. The yen for now hardly suffers from the rising tensions between Japan and China (USD/JPY 156.45). Sterling enters calmer waters after a strong start to the new year (EUR/GBP 0.8665).

News & Views

Czech inflation dropped a more than expected 0.3% m/m in December, keeping the annual figure at 2.1% instead of the anticipated uptick to 2.3%. Sharply declining food prices (-1.2% m/m) together with easing energy prices (-0.6% m/m, -4.2% y/y) explain most of the surprise CPI drop. They offset amongst others accelerating services inflation (0.2% m/m, 4.8% y/y). The December CPI outcome fell short of the central bank’s 2.3% expectation and as such remains close to the 2% midpoint target (+/- 1 ppt tolerance range). In the coming months inflation is likely to drop below 2% due to base effects and lower electricity prices (waiver of renewable energy surcharge). That could fuel speculation for a resumption of the rate cutting cycle, in particular because the CNB adopted a less hawkish tone at the latest policy meeting. The jury remains out on the matter because core inflation (services in particular) gauges appear more stubborn. In any case, after today’s inflation numbers and since the CNB December meeting, bets for a 2026 rate hike earlier last year now seem totally premature and made way for speculation on a tentative cut. The Czech crown lost ground, pushing EUR/CZK from 24.17 to 24.30.

Hungary’s debt management agency (AKK) kickstarted its 2026 financing plan today with a dual tranche EUR benchmark deal. The syndicated launch consists of a 7-yr regular bond and a 12-yr green bond, yet to be priced and determined in size. AKK’s in its 2026 funding plan has penciled in a total HUF 5445 bn net issuance, dropping from HUF 6258 bn in 2025. FX denominated net issuance is planned at HUF 2541 bn, with the bulk carried by FX bonds (HUF 1482 bn) and loans from the EU’s SAFE facility (HUF 781 bn). Its share relative to total debt should stay around the optimally deemed 30% by end-2026. A newly introduced +/- 3%pt tolerance band allows for some flexibility.

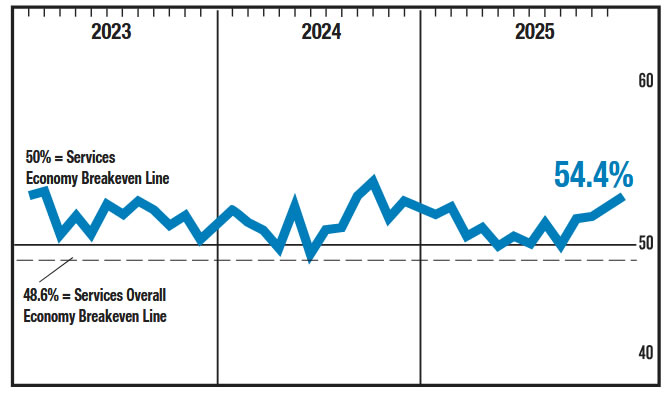

US ISM services jumps to 54.4, employment returns to expansion

US services activity rebounded sharply in December, with the ISM Services PMI jumping from 52.6 to 54.4, well above expectations of 52.3, marking the highest level in more than a year. The reading sits comfortably above its 12-month average and points to a clear reacceleration in momentum toward year-end.

The strength was broad-based. Business activity rose from 54.5 to 56.0, while new orders surged from 52.9 to 57.9, signaling renewed demand. Most notably, employment index climbed from 48.9 to 52.0, returning to expansion territory for the first time since May 2025 and easing concerns about labor market softening in the services sector. Price pressures moderated slightly, with the prices index easing from 65.4 to 64.3, but remaining elevated.

Eleven industries reported growth in December, and the ISM noted that the headline reading historically aligns with roughly 1.9 percentage points of annualized GDP growth.

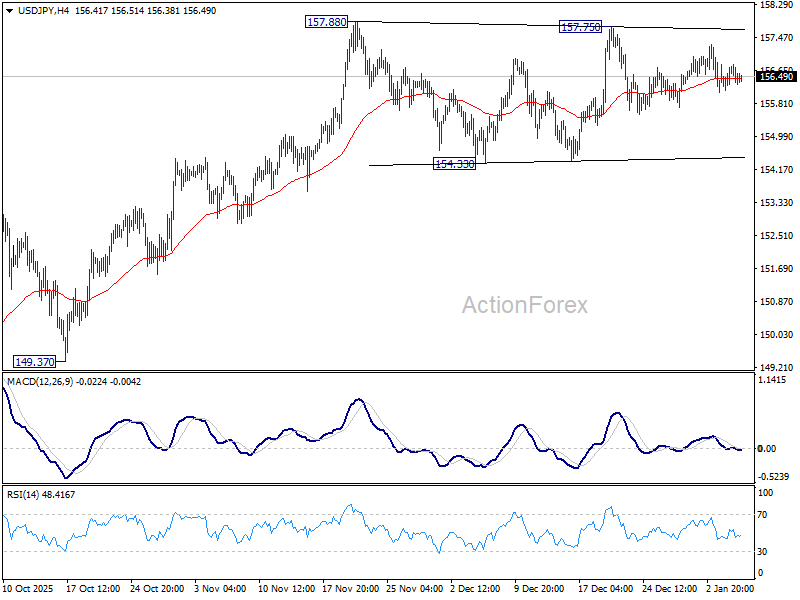

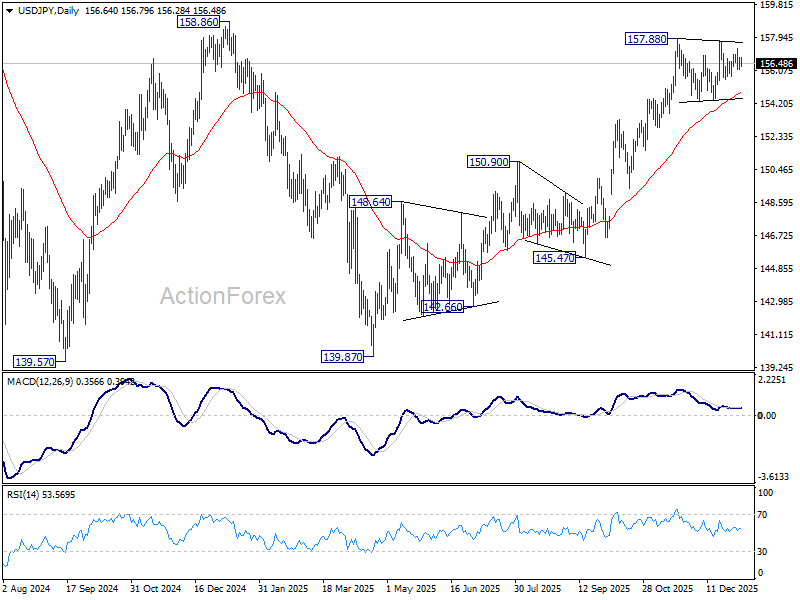

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.29; (P) 156.54; (R1) 156.93; More...

No change in USD/JPY's outlook as consolidations continues below 157.88. Intraday bias remains neutral at this point. Further rally is expected with 154.33 support intact. On the upside, firm break of 158.85 key structural resistance will be an important medium term bullish sign. Next target will be 161.94 high. However, decisive break of 154.33 will turn bias to the downside for deeper correction.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

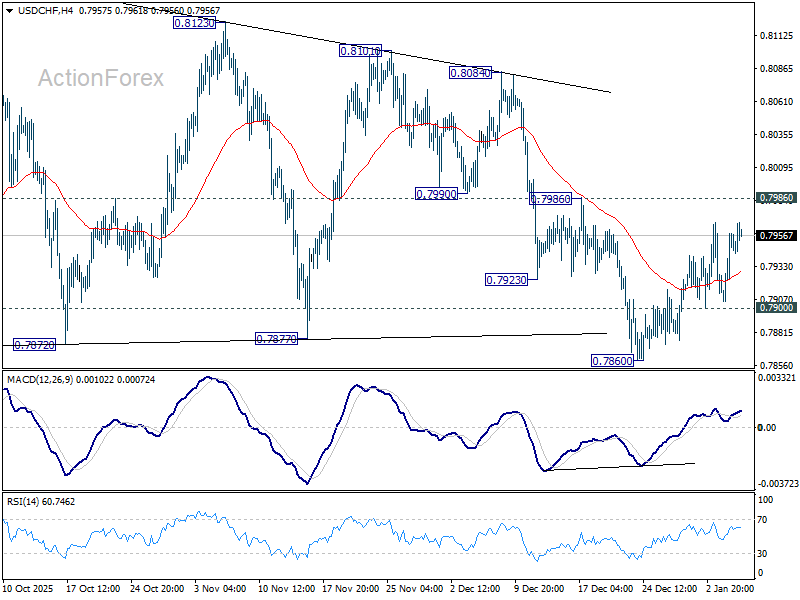

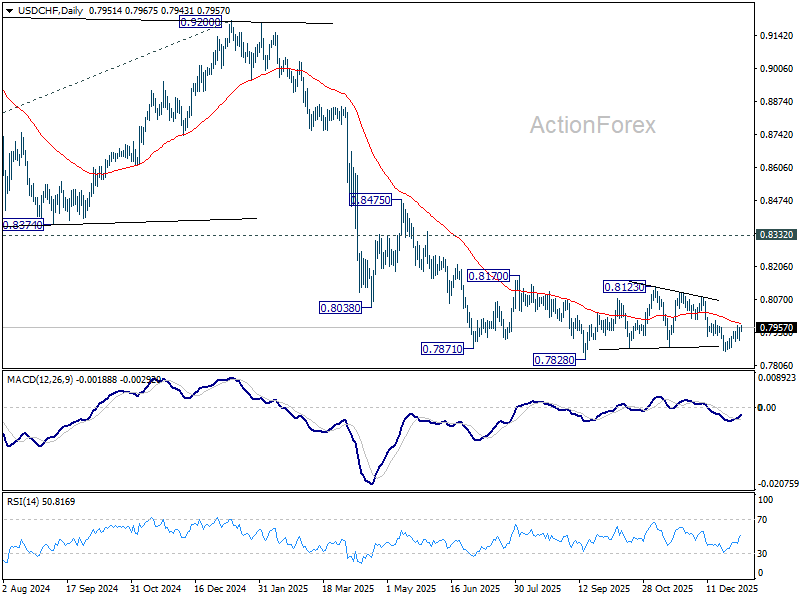

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7923; (P) 0.7942; (R1) 0.7977; More….

No change in USD/CHF's outlook and intraday bias remains neutral at this point. Further decline is mildly in favor with 0.7986 resistance intact. On the downside, below 0.7900 minor support will turn bias to the downside. Break of 0.7860 will target a retest on 0.7828 low. However, break of 0.7986 will argue that corrective pattern from 0.7828 is still extending with another rising leg already in progress.

In the bigger picture, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low). Long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

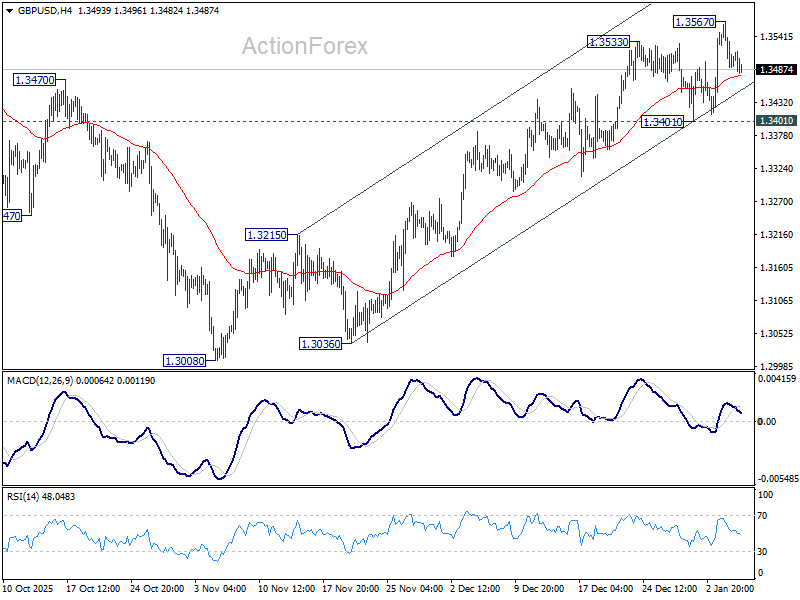

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3473; (P) 1.3521; (R1) 1.3549; More...

Intraday bias in GBP/USD remains neutral and more consolidations would be seen below 1.3567. But further rally is expected as long as 1.3401 support holds. On the upside, break of 1.3567 will resume the rise from 1.3008 to retest 1.3787 high.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

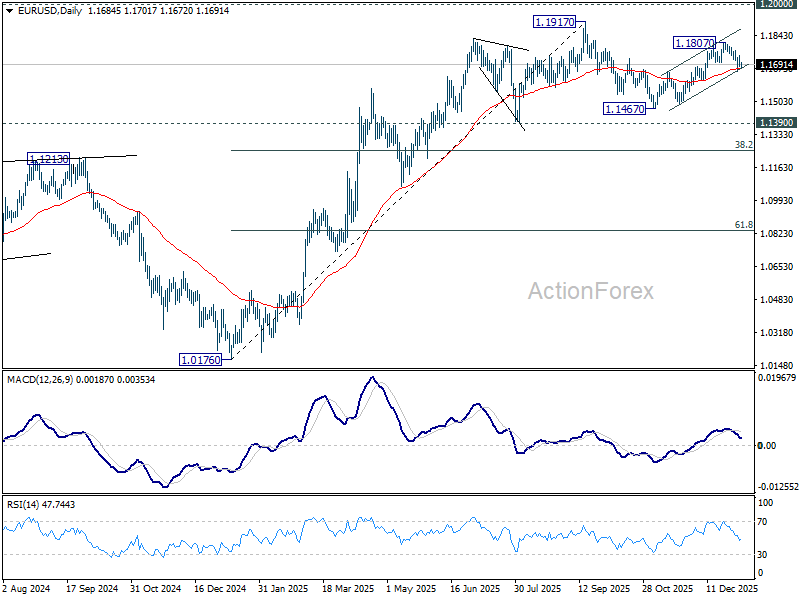

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1667; (P) 1.1705; (R1) 1.1726; More….

EUR/USD is still bounded in tight range above 1.1658 and intraday bias stays neutral. Rise from 1.1467 could still be in progress. Firm break of 1.1807 resistance will resume the rally to retest 1.1917 high. However, break of 1.1658 support will target 1.1467, as corrective pattern from 1.1917 has started the third leg.

In the bigger picture, as long as 55 W EMA (now at 1.1408) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

ADP Reinforces ‘Cooling Not Cracking’ Jobs Narrative, Markets Back in Standby Mode

Global markets are trading in mixed fashion, with risk appetite showing early signs of fatigue after a strong start to the year. US equity futures are sluggish, pointing to a flat open after both the DOW and S&P 500 closed at record highs yesterday. December ADP private payrolls from the US came in slightly weaker than expected, but the data generated little market reaction. That muted response reflects the broader interpretation that the labor market is cooling gradually rather than deteriorating sharply.

The combination of modest job growth and still-firm wage pressures fits neatly into the prevailing narrative. Hiring momentum has slowed, but companies are not shedding workers aggressively2. This “no hiring, no firing” pattern continues to dominate, with firms — particularly medium-sized businesses — still competing for talent. That dynamic helps explain why wage growth remains elevated despite softer headline job gains.

For policymakers, such conditions argue against any aggressive easing cycle. While the Fed may still deliver additional rate cuts later this year, the labor backdrop does little to justify a rapid or front-loaded move.

Still, Friday’s non-farm payrolls report remains the key event risk. Unlike ADP, NFP will provide a more comprehensive read on employment, wages, and participation, shaping expectations for the Fed’s next steps.

Elsewhere, precious metals are pulling back, with Gold and Silver retreating after touching record highs earlier in the week. The move appears to reflect profit-taking rather than a shift in fundamentals. The pullback extends the sideways consolidation that has been in place since late December. While geopolitics helped propel metals higher earlier in the week, momentum has faded for now.

In FX terms, Aussie remains the strongest performer for the week so far, followed by Kiwi, and then Yen. Loonie sits at the bottom, trailed by Swiss Franc and Euro. Dollar and Sterling are trading in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.61%. DAX is up 0.64%. CAC is up 0.01%. UK 10-year yield is down -0.077 at 4.410. Germany 10-year yield is down -0.046 at 2.799. Earlier in Asia, Nikkei fell -1.06%. Hong Kong HSI fell -0.94%. China Shanghai SSE rose 0.05%. Singapore Strait Times rose 0.16%. Japan 10-year JGB yield fell -0.009 to 2.121.

US ADP jobs rose 41k, wage pressures hold firm

US private-sector job recovered at the end of 2025, with ADP reporting a 41k rise in employment in December, but missed expectations of 50k. Hiring remained uneven, with goods-producing jobs slipping -3k, while service-providing roles rose 44k.

By company size, small businesses 9k jobs after November losses, while medium-sized firms added 34k. Large employers contributed just 2k. As ADP Chief Economist Nela Richardson noted, small establishments recovered into year-end even as large firms pulled back.

Wage dynamics remained firm. Pay growth for job-stayers was unchanged at 4.4% year-on-year, while job-changers saw an acceleration to 6.6% from 6.3%.

Eurozone inflation cools to 2.0% in December, services still main driver

Eurozone inflation edged lower in December, with flash data showing headline CPI slowing from 2.1% to 2.0% yoy, undershooting expectations of 2.1%. Core inflation also eased, with CPI excluding energy, food, alcohol and tobacco falling from 2.4% to 2.3%, below the 2.4% consensus forecast.

Services remained the dominant source of price pressure, posting an annual rate of 3.4%, down slightly from 3.5% in November. Food, alcohol and tobacco inflation ticked higher to 2.6%.

Non-energy industrial goods inflation eased further to 0.4%. Energy prices remained a strong disinflationary force, with prices falling -1.9% yoy after a smaller decline in November.

Japan PMI composite finalized at 51.1, but confidence and hiring hold up

Japan’s service sector lost some momentum at the end of 2025, with Services PMI finalized at 51.6 in December, down from 53.2 in November. Composite PMI eased to 51.1 from 52.0, marking a seven-month low.

According to S&P Global Market Intelligence Economics Associate Director Annabel Fiddes, services firms reported slower growth in activity and new orders, while manufacturing showed relative improvement. Despite softer demand signals, business confidence across Japan’s private sector remained firm, supporting a "solid and accelerated rise in employment".

Cost pressures, however, remain a key challenge. Input prices rose at the fastest pace since April, driven by higher costs, prompting firms to lift selling prices at a solid rate. With demand conditions softening slightly, companies face a "difficult balance" between passing on higher costs to protect margins and maintaining competitiveness.

Australia CPI cools more than expected to 3.4%, easing near-term pressure on RBA

Australia’s inflation cooled more than expected in November, offering some relief after months of intensifying price pressure. Headline CPI slowed from 3.8% yoy to 3.4%, undershooting expectations of 3.6%. Trimmed mean inflation eased modestly from 3.3% yoy to 3.2%, pointing to a gradual moderation in underlying pressures.

The slowdown was broad-based. Annual goods inflation fell to 3.3% yoy from 3.8%, driven largely by a sharp deceleration in electricity prices, which rose 19.7% over the year compared with 37.1% previously. Services inflation also eased, slowing to 3.6% yoy from 3.9%, helped by a pullback in domestic holiday travel costs after October’s school-holiday and major sporting-event surge.

Despite the moderation, price pressures remain elevated in key areas. Housing inflation stayed firm at 5.2% yoy, while rents and medical services continued to rise at a solid pace. The data ease immediate pressure on the RBA for rate hike. But with inflation still well above target range, policymakers are likely to remain cautious about declaring victory too early.

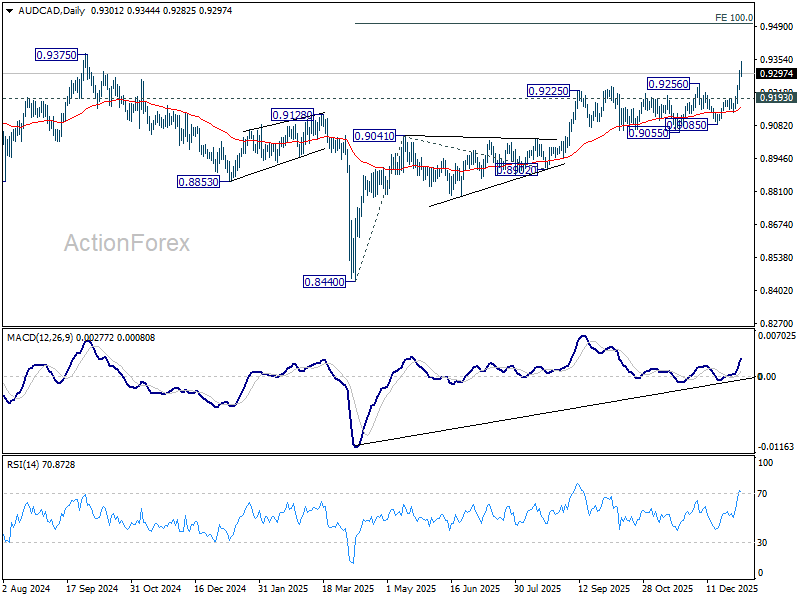

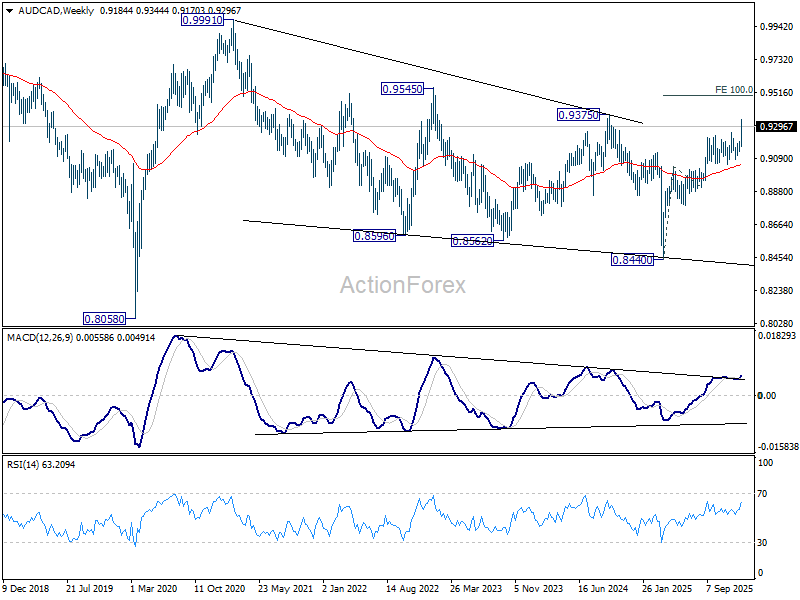

AUD/CAD Medium-Term Parity Case Builds on Metal Boom and RBA Outlook

Australian Dollar has taken a clear leadership role among commodity currencies as the new year starts, outperforming peers as powerful tailwinds from metals markets combine with resilient domestic rate expectations.

Iron ore prices surged to their highest level since February, driven by optimism over Chinese macro support and seasonal restocking ahead of the Lunar New Year. That confidence was underlined by fresh guidance from the PBoC which said it will deploy interest-rate cuts, reserve-requirement reductions and other tools in a flexible and efficient manner to maintain ample liquidity and support credit growth.

Policymakers also pledged to step up counter-cyclical and cross-cyclical adjustments, boost domestic demand and manage financial risks, signaling a determination to stabilize growth early in the new five-year planning cycle. For commodity exporters, the message has been unambiguously supportive.

Also, Copper has delivered an additional boost, pushing to a fresh series of record highs. The rally has been driven by supply-side disruptions and deepening concerns over medium-term availability rather than short-term speculative flows.

Production setbacks at several major mines, including Freeport‑McMoRan’s Grasberg operation, have tightened global supply. At the same time, demand expectations continue to rise due to Copper’s critical role in construction, energy transition, artificial intelligence data centers and defense industries.

Back home, November CPI data in Australia surprised to the downside, reducing pressure for an immediate February rate hike by the RBA. Even so, the broader policy outlook remains tilted toward tightening rather than easing.

Underlying inflation pressures are easing only slowly, particularly in services, keeping policymakers cautious. Markets still expect rates to remain on hold in February but see a high likelihood of a hike by June and another before the end of the year.

That policy-commodity mix has translated directly into Aussie strength. Technically, AUD/CAD has broken decisively above 0.9256 resistance, confirming resumption of the uptrend from 0.8440 (2025 low). Next upside target stands at 100% projection of 0.8440 to 0.9041 from 0.8902 at 0.9503.

More importantly, the upside breakout strengthens the case that the entire corrective decline from the 0.9991 (2021 high) ended at 0.8440. Medium-term focus now shifts to 0.9545, where decisive break would argue that the longer-term rise from the 2020 low at 0.8058 is ready to resume toward parity.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1667; (P) 1.1705; (R1) 1.1726; More….

EUR/USD is still bounded in tight range above 1.1658 and intraday bias stays neutral. Rise from 1.1467 could still be in progress. Firm break of 1.1807 resistance will resume the rally to retest 1.1917 high. However, break of 1.1658 support will target 1.1467, as corrective pattern from 1.1917 has started the third leg.

In the bigger picture, as long as 55 W EMA (now at 1.1408) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

US ADP jobs rose 41k, wage pressures hold firm

US private-sector job recovered at the end of 2025, with ADP reporting a 41k rise in employment in December, but missed expectations of 50k. Hiring remained uneven, with goods-producing jobs slipping -3k, while service-providing roles rose 44k.

By company size, small businesses 9k jobs after November losses, while medium-sized firms added 34k. Large employers contributed just 2k. As ADP Chief Economist Nela Richardson noted, small establishments recovered into year-end even as large firms pulled back.

Wage dynamics remained firm. Pay growth for job-stayers was unchanged at 4.4% year-on-year, while job-changers saw an acceleration to 6.6% from 6.3%.

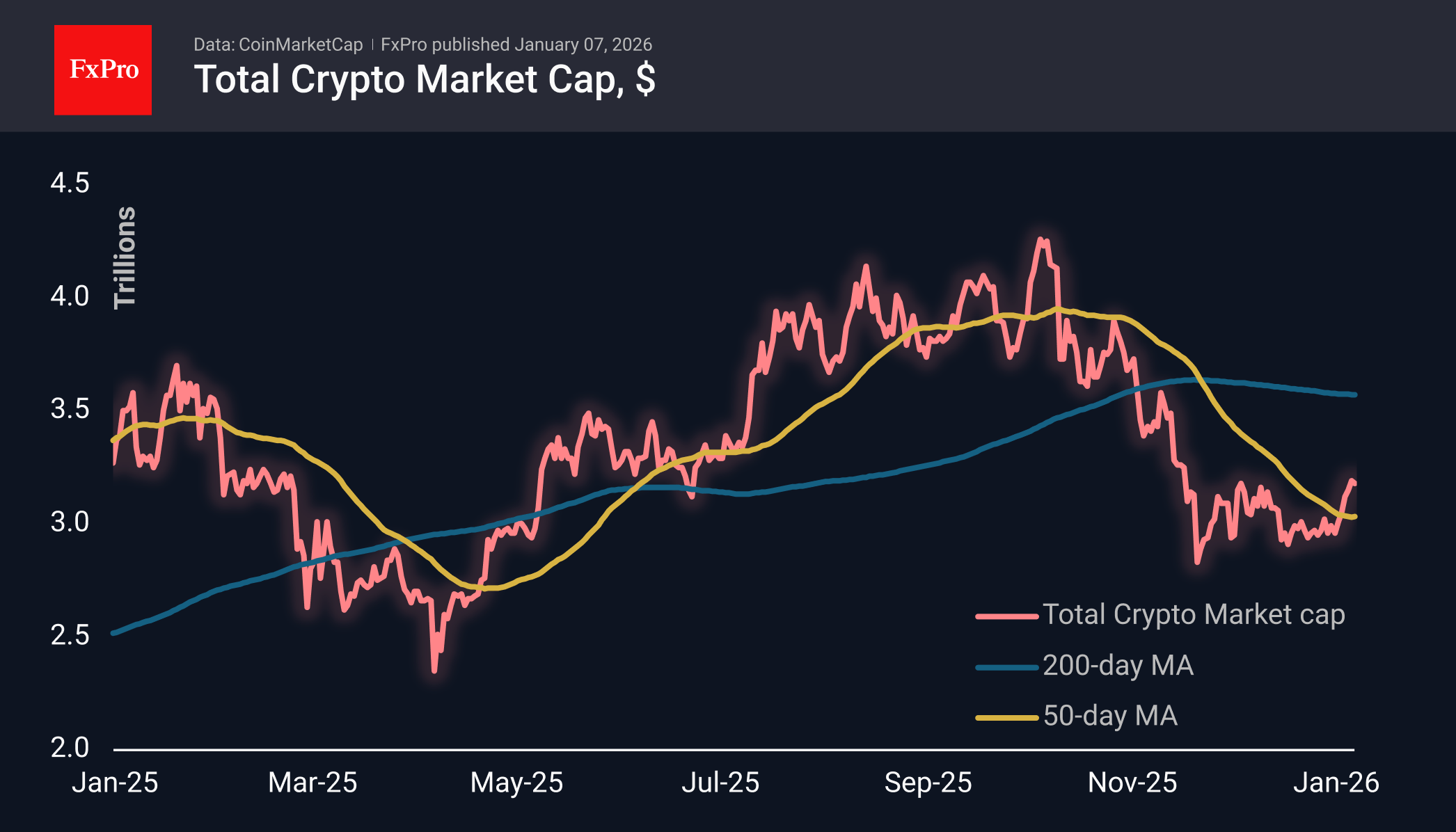

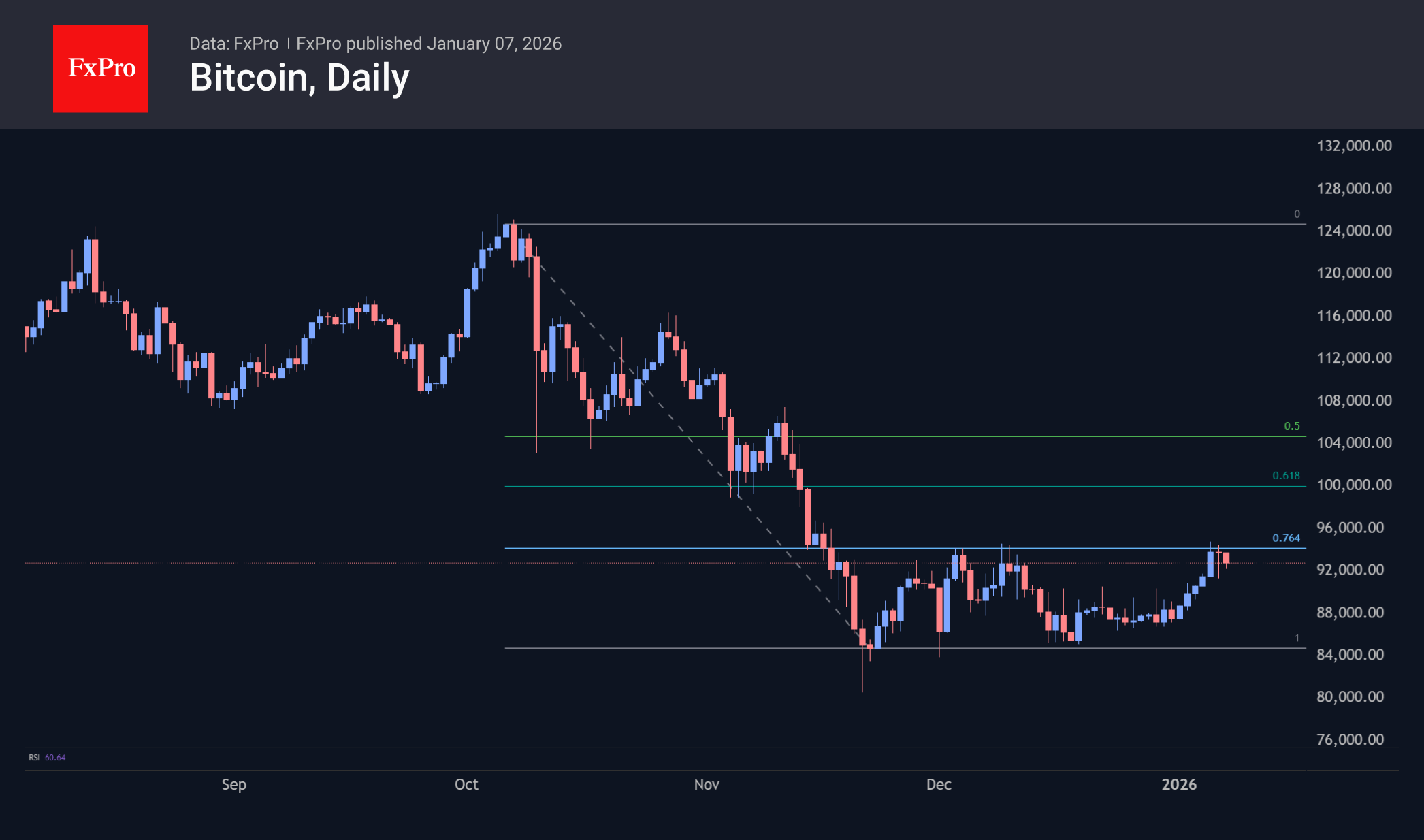

Crypto Market Has Hit Upper Limit of Rebound

Market Overview

This week’s strengthening of the crypto market has hit local resistance near the $3.2 trillion total capitalisation level. The market recovery in early December also stalled at around these levels, which is why the current level is attracting some cautious sellers. For now, the recovery is being stifled by intense selling pressure, which allows us to remain cautious about the near-term outlook.

The sentiment index has risen sharply over the last two days, buoyed by rising prices, and has returned to neutral territory from the fear zone. Notably, this shift in sentiment has been reflected in altcoins, which have experienced significant price increases since the start of the year.

On Monday and Tuesday, Bitcoin rose to the upper limit of its trading range since mid-November, at $95K, followed by a drop to $91K and a further recovery to $92.6K, where the quotes stand at the time of writing. Clearly, the easy part of the BTC rebound is behind us, and further growth can be seen as a signal of a prolonged recovery, which bears are still strongly resisting.

News Background

The risks of a deep fall in Bitcoin in the current market cycle remain limited, as do the chances of a significant rally. Bitcoin’s four-year cycle remains in place, and 2026 is likely to be a period of consolidation and sideways movement, according to VanEck.

Over the past week, the Binance exchange has recorded the most significant inflow of Bitcoin and Ethereum in a month, amounting to nearly $2.4 billion. The inflow of cryptocurrency may be linked to holders’ desire to sell their assets, according to CryptoOnchain.

The myth that crypto whales are aggressively buying up Bitcoin is not true. Their activity is overestimated due to distortions associated with the work of crypto exchanges, according to CryptoQuant. Exchanges consolidate funds from many small wallets into a few large ones for regulatory reasons, which leads to the misclassification of such activity.

A rare buy signal has appeared on the weekly Bitcoin chart according to the McMillan Volatility Band indicator, said analyst Lawrence McMillan. In the entire history of BTC, such a signal has appeared only three times, and each time it coincided with successful buying points.

According to Token Terminal, the Ethereum network has set a new record for the volume of stablecoin transfers. The figure in the fourth quarter of last year exceeded $8 trillion — in six months, the volume has almost doubled.

Starting this year, crypto services in 48 countries are required to begin collecting information on cryptocurrency transactions. Member states of the Organisation for Economic Co-operation and Development (OECD) intend to exchange this data to increase tax revenues.

AUD/CAD medium-term parity case builds, on metal boom and RBA outlook

Australian Dollar has taken a clear leadership role among commodity currencies as the new year starts, outperforming peers as powerful tailwinds from metals markets combine with resilient domestic rate expectations.

Iron ore prices surged to their highest level since February, driven by optimism over Chinese macro support and seasonal restocking ahead of the Lunar New Year. That confidence was underlined by fresh guidance from the PBoC which said it will deploy interest-rate cuts, reserve-requirement reductions and other tools in a flexible and efficient manner to maintain ample liquidity and support credit growth.

Policymakers also pledged to step up counter-cyclical and cross-cyclical adjustments, boost domestic demand and manage financial risks, signaling a determination to stabilize growth early in the new five-year planning cycle. For commodity exporters, the message has been unambiguously supportive.

Also, Copper has delivered an additional boost, pushing to a fresh series of record highs. The rally has been driven by supply-side disruptions and deepening concerns over medium-term availability rather than short-term speculative flows.

Production setbacks at several major mines, including FreeportMcMoRan’s Grasberg operation, have tightened global supply. At the same time, demand expectations continue to rise due to Copper’s critical role in construction, energy transition, artificial intelligence data centers and defense industries.

Back home, November CPI data in Australia surprised to the downside, reducing pressure for an immediate February rate hike by the RBA. Even so, the broader policy outlook remains tilted toward tightening rather than easing.

Underlying inflation pressures are easing only slowly, particularly in services, keeping policymakers cautious. Markets still expect rates to remain on hold in February but see a high likelihood of a hike by June and another before the end of the year.

That policy-commodity mix has translated directly into Aussie strength. Technically, AUD/CAD has broken decisively above 0.9256 resistance, confirming resumption of the uptrend from 0.8440 (2025 low). Next upside target stands at 100% projection of 0.8440 to 0.9041 from 0.8902 at 0.9503.

More importantly, the upside breakout strengthens the case that the entire corrective decline from the 0.9991 (2021 high) ended at 0.8440. Medium-term focus now shifts to 0.9545, where decisive break would argue that the longer-term rise from the 2020 low at 0.8058 is ready to resume toward parity.