Sample Category Title

Weekly Economic & Financial Commentary: Outlook for Fed Policy Remains Highly Uncertain

Summary

United States: One Day or Another: FOMC Still in Wait-and-See Mode

- In this week's most closely-watched release, the FOMC elected to maintain its federal funds rate target at 4.25%–4.50%, citing continued economic resilience and still-elevated inflation. With the incoming data broadly continuing to point to a U.S. economy that is slowing but not grinding to a halt, the FOMC remains in a holding pattern as it awaits a fuller picture of how tariffs play out in the data.

- Next week: Home Sales (Mon. & Wed.), Durable Goods (Thu.), Personal Income & Spending (Fri.)

International: More Daylight, More Monetary Policy Decisions

- The days got longer this week, and equally long was the list of foreign central banks meeting to deliver monetary policy decisions. The Bank of Japan, Bank of England and Chilean central bank held rates steady, as expected, while Norway's central bank surprised market participants with a rate cut. The Swiss National Bank and Sweden's central bank both delivered rate cuts, and the Brazilian central bank hiked rates, in our view, for the last time this easing cycle.

- Next week: Eurozone PMIs (Mon.), Canada CPI (Tue.), Banxico Policy Rate (Thu.)

Interest Rate Watch: Outlook for Fed Policy Remains Highly Uncertain

- Although the median dot in the FOMC's "dot plot" continues to look for 50 bps of rate cuts by the end of the year, Chair Powell suggested in his press conference after this week's FOMC meeting that the outlook for monetary policy is highly uncertain.

Credit Market Insights: A Compression in Spreads

- Corporate bond markets have settled into a more stable rhythm in recent weeks, following a period of heightened volatility earlier this year. Credit investors are still focusing on potential risks, but the extreme high-risk sentiment has cooled. For now, spreads are continuing on their previous trend of cautious optimism.

Topic of the Week: What's Behind the Recent Rise in Home Supply?

- Resale inventories are normalizing. The reasons? Weak demand as a result of persistently high mortgage rates, the return to office, easing of the mortgage rate lock-in effect, rising "hidden" homeownership costs and cooling labor market all appear to be behind the climb in supply.

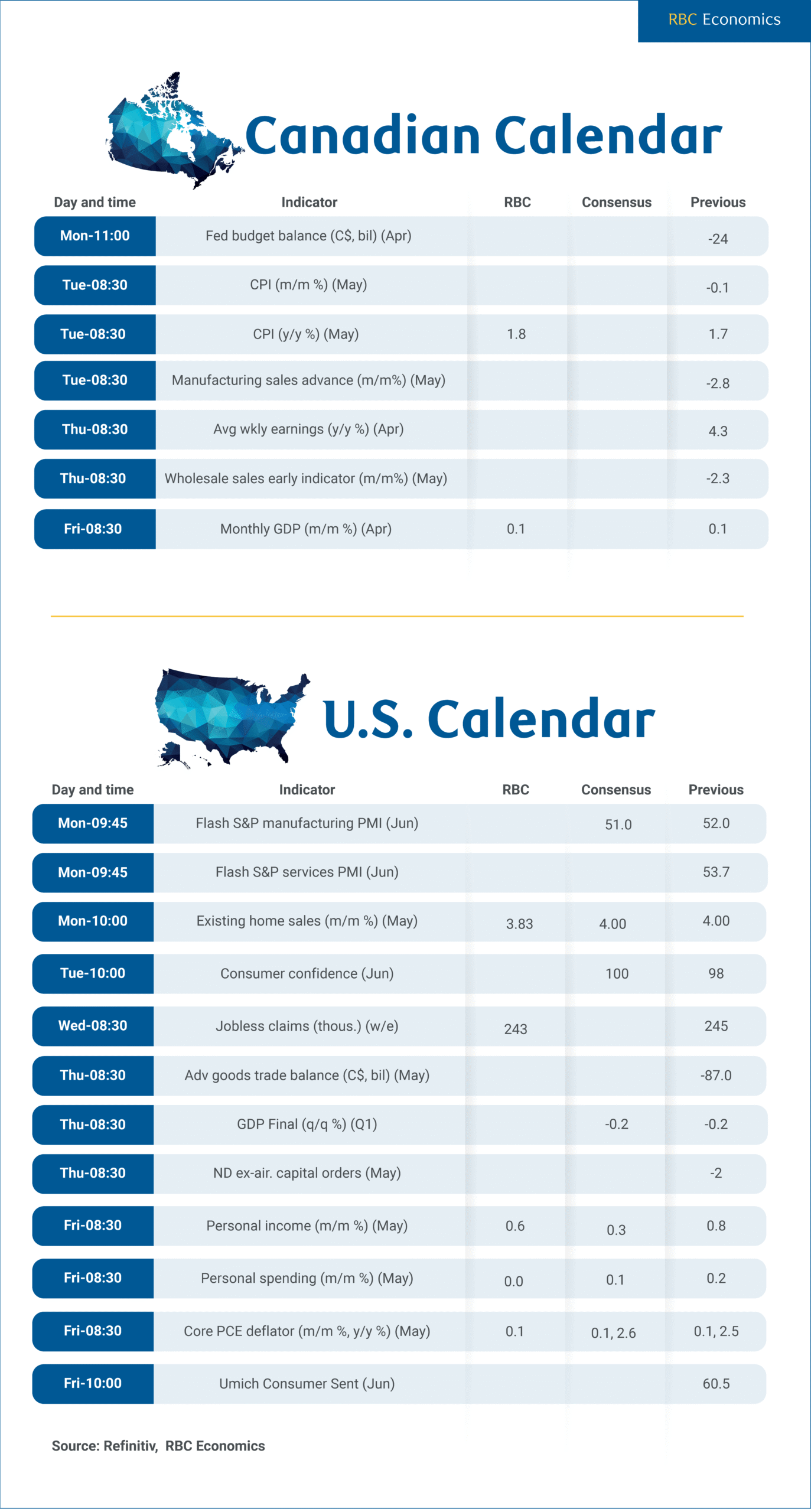

Tariffs Stalled Canada’s Growth in April But Had Limited Impact on May Inflation

We expect next Friday’s Canadian growth domestic product data will show slowing growth following a jump in the first quarter that was largely driven by front-running tariffs.

GDP is expected to have eked out a 0.1% increase in April, matching Statistics Canada's preliminary estimate from a month ago. The trade-exposed manufacturing sector softened with sales falling sharply in subsectors targeted directly by U.S. tariffs including transportation equipment, and metal products. However, retail sales volumes edged up in April, and early data indicates a jump in oil production in Alberta.

The advance estimate for May output will be closely watched as early indicators are mixed. Trade-reliant sectors like manufacturing continued to weaken with contracting hours worked and employment declining. But, other parts of the economy provided offset and overall employment still edged higher in May. Data from Indeed.com showed hiring demand stabilizing into June.

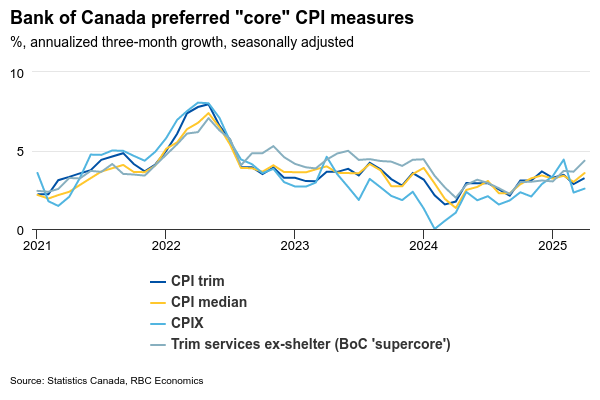

Tariffs have impacted production and employment in certain sectors, but it's likely too soon to see substantial effects in consumer prices. Some import-reliant categories like food and autos have experienced accelerating price growth, but recent upside surprises in consumer prices have predominantly come from domestically produced and consumed services.

For May, we expect Canadian consumer price index growth to edge up 1.8% year-over-year from April's 1.7% with excluding food and energy price growth holding steady at 2.6%. The removal of the consumer carbon tax in April in most provinces will continue to keep energy prices well below levels from a year ago. The Bank of Canada's preferred core measures (which exclude indirect taxes like the carbon tax) likely eased slightly after exceeding 3% in April.

Summary 6/23 – 6/27

Monday, Jun 23, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Jun P | 51 | |

| 23:00 | AUD | Services PMI Jun P | 50.6 | |

| 00:30 | JPY | Manufacturing PMI Jun P | 49.5 | 49.4 |

| 00:30 | JPY | Services PMI Jun P | 51 | |

| 07:15 | EUR | France Manufacturing PMI Jun P | 49.8 | 49.8 |

| 07:15 | EUR | France Services PMI Jun P | 49.2 | 48.9 |

| 07:30 | EUR | Germany Manufacturing PMI Jun P | 48.8 | 48.3 |

| 07:30 | EUR | Germany Services PMI Jun P | 47.8 | 47.1 |

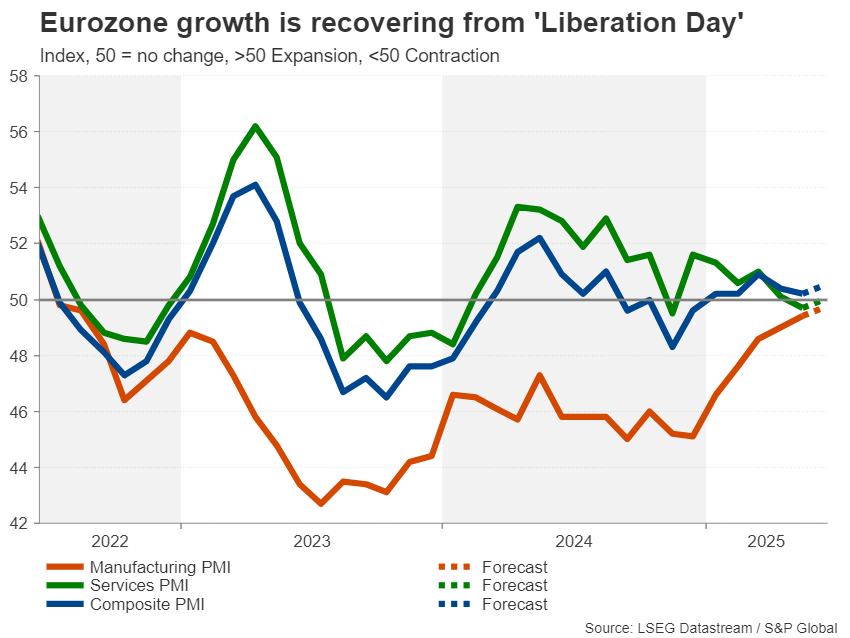

| 08:00 | EUR | Eurozone Manufacturing PMI Jun P | 49.7 | 49.4 |

| 08:00 | EUR | Eurozone Services PMI Jun P | 50.1 | 49.7 |

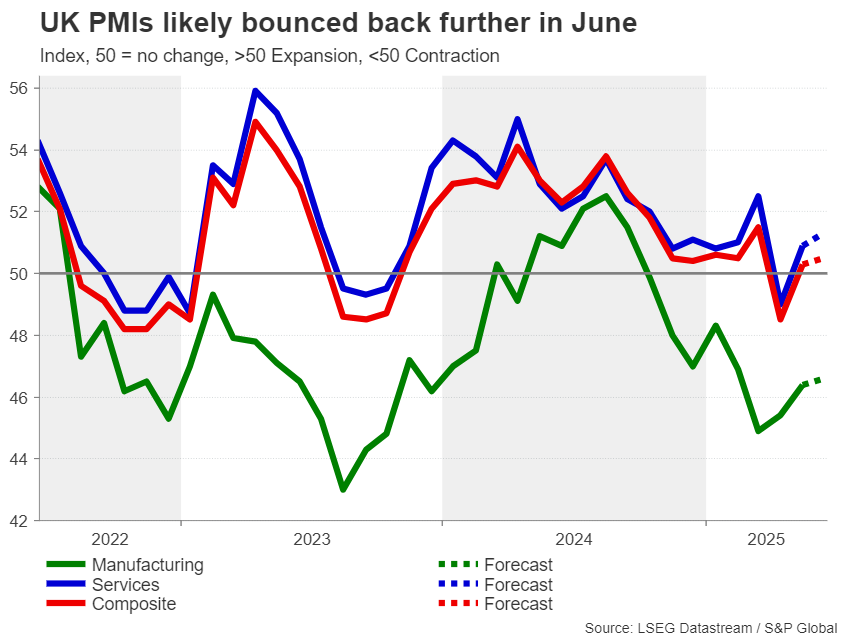

| 08:30 | GBP | Manufacturing PMI Jun P | 46.9 | 46.4 |

| 08:30 | GBP | Services PMI Jun P | 51.2 | 50.9 |

| 13:45 | USD | Manufacturing PMI Jun P | 51.1 | 52 |

| 13:45 | USD | Services PMI Jun P | 52.9 | 53.7 |

| 14:00 | USD | Existing Home Sales May | 3.95M | 4.00M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Jun P | |

| Forecast: | Previous: 51 | ||

| 23:00 | AUD | Services PMI Jun P | |

| Forecast: | Previous: 50.6 | ||

| 00:30 | JPY | Manufacturing PMI Jun P | |

| Forecast: 49.5 | Previous: 49.4 | ||

| 00:30 | JPY | Services PMI Jun P | |

| Forecast: | Previous: 51 | ||

| 07:15 | EUR | France Manufacturing PMI Jun P | |

| Forecast: 49.8 | Previous: 49.8 | ||

| 07:15 | EUR | France Services PMI Jun P | |

| Forecast: 49.2 | Previous: 48.9 | ||

| 07:30 | EUR | Germany Manufacturing PMI Jun P | |

| Forecast: 48.8 | Previous: 48.3 | ||

| 07:30 | EUR | Germany Services PMI Jun P | |

| Forecast: 47.8 | Previous: 47.1 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jun P | |

| Forecast: 49.7 | Previous: 49.4 | ||

| 08:00 | EUR | Eurozone Services PMI Jun P | |

| Forecast: 50.1 | Previous: 49.7 | ||

| 08:30 | GBP | Manufacturing PMI Jun P | |

| Forecast: 46.9 | Previous: 46.4 | ||

| 08:30 | GBP | Services PMI Jun P | |

| Forecast: 51.2 | Previous: 50.9 | ||

| 13:45 | USD | Manufacturing PMI Jun P | |

| Forecast: 51.1 | Previous: 52 | ||

| 13:45 | USD | Services PMI Jun P | |

| Forecast: 52.9 | Previous: 53.7 | ||

| 14:00 | USD | Existing Home Sales May | |

| Forecast: 3.95M | Previous: 4.00M | ||

Tuesday, Jun 24, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 08:00 | EUR | Germany IFO Business Climate Jun | 88.2 | 87.5 |

| 08:00 | EUR | Germany IFO Current Assessment Jun | 86.5 | 86.1 |

| 08:00 | EUR | Germany IFO Expectations Jun | 89.5 | 88.9 |

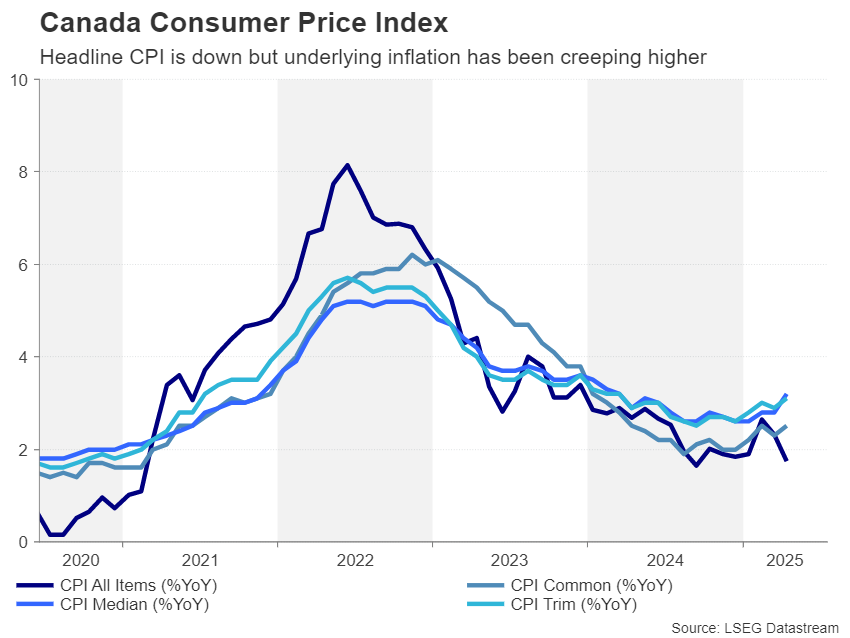

| 12:30 | CAD | CPI M/M May | -0.10% | |

| 12:30 | CAD | CPI Y/Y May | 1.70% | |

| 12:30 | CAD | CPI Median Y/Y May | 3.20% | |

| 12:30 | CAD | CPI Trimmed Y/Y May | 3.10% | |

| 12:30 | CAD | CPI Common Y/Y May | 2.50% | |

| 12:30 | USD | Current Account (USD) Q1 | -444B | -304B |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Apr | 4.20% | 4.10% |

| 13:00 | USD | Housing Price Index M/M Apr | 0.10% | -0.10% |

| 14:00 | USD | Consumer Confidence Jun | 99.1 | 98.0 |

| 22:45 | NZD | Trade Balance (NZD) May | 1060M | 1426M |

| 23:50 | JPY | Corporate Service Price Index Y/Y May | 3.10% | 3.10% |

| 23:50 | JPY | BoJ Summary of Opinions |

| GMT | Ccy | Events | |

|---|---|---|---|

| 08:00 | EUR | Germany IFO Business Climate Jun | |

| Forecast: 88.2 | Previous: 87.5 | ||

| 08:00 | EUR | Germany IFO Current Assessment Jun | |

| Forecast: 86.5 | Previous: 86.1 | ||

| 08:00 | EUR | Germany IFO Expectations Jun | |

| Forecast: 89.5 | Previous: 88.9 | ||

| 12:30 | CAD | CPI M/M May | |

| Forecast: | Previous: -0.10% | ||

| 12:30 | CAD | CPI Y/Y May | |

| Forecast: | Previous: 1.70% | ||

| 12:30 | CAD | CPI Median Y/Y May | |

| Forecast: | Previous: 3.20% | ||

| 12:30 | CAD | CPI Trimmed Y/Y May | |

| Forecast: | Previous: 3.10% | ||

| 12:30 | CAD | CPI Common Y/Y May | |

| Forecast: | Previous: 2.50% | ||

| 12:30 | USD | Current Account (USD) Q1 | |

| Forecast: -444B | Previous: -304B | ||

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Apr | |

| Forecast: 4.20% | Previous: 4.10% | ||

| 13:00 | USD | Housing Price Index M/M Apr | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 14:00 | USD | Consumer Confidence Jun | |

| Forecast: 99.1 | Previous: 98.0 | ||

| 22:45 | NZD | Trade Balance (NZD) May | |

| Forecast: 1060M | Previous: 1426M | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y May | |

| Forecast: 3.10% | Previous: 3.10% | ||

| 23:50 | JPY | BoJ Summary of Opinions | |

| Forecast: | Previous: | ||

Wednesday, Jun 25, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Monthly CPI Y/Y May | 2.40% | 2.40% |

| 08:00 | CHF | UBS Economic Expectations Jun | -22 | |

| 14:00 | USD | New Home Sales May | 692K | 743K |

| 14:30 | USD | Crude Oil Inventories | -11.5M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Monthly CPI Y/Y May | |

| Forecast: 2.40% | Previous: 2.40% | ||

| 08:00 | CHF | UBS Economic Expectations Jun | |

| Forecast: | Previous: -22 | ||

| 14:00 | USD | New Home Sales May | |

| Forecast: 692K | Previous: 743K | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -11.5M | ||

Thursday, Jun 26, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | EUR | Germany GfK Consumer Sentiment Jul | -19 | -19.9 |

| 12:30 | USD | Initial Jobless Claims (Jun 20) | 247K | 245K |

| 12:30 | USD | GDP Annualized Q1 F | -0.20% | -0.20% |

| 12:30 | USD | GDP Price Index Q1 F | 3.70% | 3.70% |

| 12:30 | USD | Goods Trade Balance (USD) May P | -91.9B | -87.0B |

| 12:30 | USD | Wholesale Inventories May P | 0.10% | 0.20% |

| 12:30 | USD | Durable Goods Orders May | 6.80% | -6.30% |

| 12:30 | USD | Durable Goods Orders ex Transport May | 0.10% | 0.20% |

| 14:00 | USD | Pending Home Sales M/M May | 0.00% | -6.30% |

| 14:30 | USD | Natural Gas Storage | 95B | |

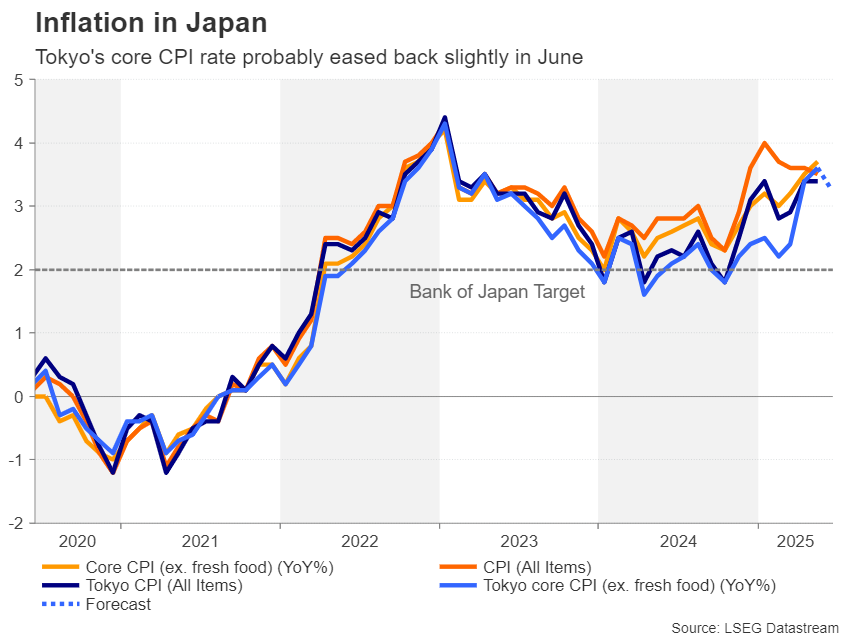

| 23:30 | JPY | Tokyo CPI Y/Y Jun | 3.40% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Jun | 3.40% | 3.60% |

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y Jun | 3.30% | |

| 23:30 | JPY | Unemployment Rate May | 2.50% | 2.50% |

| 23:50 | JPY | Retail Trade Y/Y May | 2.40% | 3.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | EUR | Germany GfK Consumer Sentiment Jul | |

| Forecast: -19 | Previous: -19.9 | ||

| 12:30 | USD | Initial Jobless Claims (Jun 20) | |

| Forecast: 247K | Previous: 245K | ||

| 12:30 | USD | GDP Annualized Q1 F | |

| Forecast: -0.20% | Previous: -0.20% | ||

| 12:30 | USD | GDP Price Index Q1 F | |

| Forecast: 3.70% | Previous: 3.70% | ||

| 12:30 | USD | Goods Trade Balance (USD) May P | |

| Forecast: -91.9B | Previous: -87.0B | ||

| 12:30 | USD | Wholesale Inventories May P | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 12:30 | USD | Durable Goods Orders May | |

| Forecast: 6.80% | Previous: -6.30% | ||

| 12:30 | USD | Durable Goods Orders ex Transport May | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 14:00 | USD | Pending Home Sales M/M May | |

| Forecast: 0.00% | Previous: -6.30% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 95B | ||

| 23:30 | JPY | Tokyo CPI Y/Y Jun | |

| Forecast: | Previous: 3.40% | ||

| 23:30 | JPY | Tokyo CPI Core Y/Y Jun | |

| Forecast: 3.40% | Previous: 3.60% | ||

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y Jun | |

| Forecast: | Previous: 3.30% | ||

| 23:30 | JPY | Unemployment Rate May | |

| Forecast: 2.50% | Previous: 2.50% | ||

| 23:50 | JPY | Retail Trade Y/Y May | |

| Forecast: 2.40% | Previous: 3.30% | ||

Friday, Jun 27, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Jun | 95.5 | 94.8 |

| 09:00 | EUR | Eurozone Services Sentiment Jun | 1.5 | |

| 09:00 | EUR | Eurozone Industrial Confidence Jun | -10.3 | |

| 09:00 | EUR | Eurozone Consumer Confidence Jun F | -15.3 | -15.3 |

| 12:30 | CAD | GDP M/M Apr | 0.00% | 0.10% |

| 12:30 | USD | Personal Income M/M May | 0.20% | 0.80% |

| 12:30 | USD | Personal Spending May | 0.20% | 0.20% |

| 12:30 | USD | PCE Price Index M/M May | 0.10% | |

| 12:30 | USD | PCE Price Index Y/Y May | 2.10% | |

| 12:30 | USD | Core PCE Price Index M/M May | 0.10% | 0.10% |

| 12:30 | USD | Core PCE Price Index Y/Y May | 2.50% | |

| 14:00 | USD | UoM Consumer Sentiment Jun F | 60.5 | 60.5 |

| 14:00 | USD | UoM 1-year Inflation Expectations Jun F | 5.10% | 5.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Jun | |

| Forecast: 95.5 | Previous: 94.8 | ||

| 09:00 | EUR | Eurozone Services Sentiment Jun | |

| Forecast: | Previous: 1.5 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Jun | |

| Forecast: | Previous: -10.3 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Jun F | |

| Forecast: -15.3 | Previous: -15.3 | ||

| 12:30 | CAD | GDP M/M Apr | |

| Forecast: 0.00% | Previous: 0.10% | ||

| 12:30 | USD | Personal Income M/M May | |

| Forecast: 0.20% | Previous: 0.80% | ||

| 12:30 | USD | Personal Spending May | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 12:30 | USD | PCE Price Index M/M May | |

| Forecast: | Previous: 0.10% | ||

| 12:30 | USD | PCE Price Index Y/Y May | |

| Forecast: | Previous: 2.10% | ||

| 12:30 | USD | Core PCE Price Index M/M May | |

| Forecast: 0.10% | Previous: 0.10% | ||

| 12:30 | USD | Core PCE Price Index Y/Y May | |

| Forecast: | Previous: 2.50% | ||

| 14:00 | USD | UoM Consumer Sentiment Jun F | |

| Forecast: 60.5 | Previous: 60.5 | ||

| 14:00 | USD | UoM 1-year Inflation Expectations Jun F | |

| Forecast: 5.10% | Previous: 5.10% | ||

Week Ahead – PCE Inflation and Flash PMIs on Tap Amid Middle East Jitters

- Ongoing Israel-Iran tensions to keep risk sentiment in check.

- US core PCE and consumption data to offer much-needed distraction.

- CPI readings also due in Canada, Australia and Japan.

- Flash PMIs for June in the spotlight too amid tariff chaos.

US data eyed amid doubts about economy and geopolitics

There’s been some good news and bad news for the US economy lately, as investors attempt to gauge the impact of President Trump’s tariff war. The good news is that so far, there’s been very little pressure on consumer prices from the universal 10% tariff rate that applies on most goods entering the United States. The labour market is also proving to be a lot more resilient than anticipated.

The bad news is that American consumers appear to be turning more cautious with their spending, and although the economy is still churning out new jobs, there could be some major cracks forming under the surface.

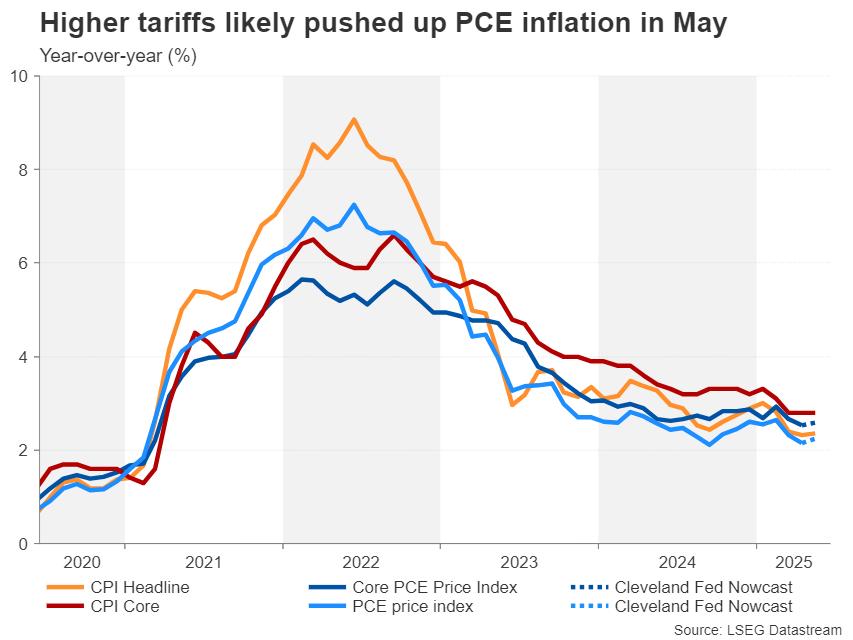

Friday’s data on PCE inflation and personal income and spending will therefore be crucial, as it will shed more light on both price pressures and the strength of consumer demand.

Personal consumption moderated to 0.2% m/m in April but is expected to have quickened slightly in May to 0.3% m/m. However, personal income growth likely halved to 0.4% m/m.

As for the Fed’s favourite inflation metrics, the PCE price indices are not anticipated to alarm investors but may point to a small pickup on the back of the higher tariffs coming into effect in April.

The headline rate of the PCE price index is projected to rise from 2.1% to 2.25% y/y according to the Cleveland Fed’s Nowcast model, while the core PCE price index is estimated to edge up slightly from 2.5% to 2.58% y/y.

Which way will Fed rate cut expectations sway?

Ahead of all that, the focal point at the start of the week will be the flash S&P Global PMIs for June, which will be watched for any signs that the still raging trade war is hurting business activity. Also due on Monday are pending home sales for May.

The Conference Board’s latest consumer confidence index is out on Tuesday, followed by new home sales on Wednesday. There will be more housing data on Thursday with pending home sales, as well as durable goods orders and the final estimate of Q1 GDP growth.

The reaction in Fed fund futures, which will set the tone for the US dollar and on Wall Street, will be determined by the extent to which any downside surprises are offset by upside ones, with extra weighting given to the core PCE print.

However, investors will also be paying attention to Fed Chair Powell’s two-day semi-annual testimony before Congress on Tuesday and Wednesday for any fresh clues on the policy outlook.

Market expectations for Fed rate cuts continue to pivot around 50 basis points of reductions by year-end. Any hawkish remarks by Powell or indications that the higher levies are starting to feed into consumer prices could push those odds much lower, likely lifting the dollar but sparking a selloff in US equities.

Risk of US being dragged into Israel-Iran conflict

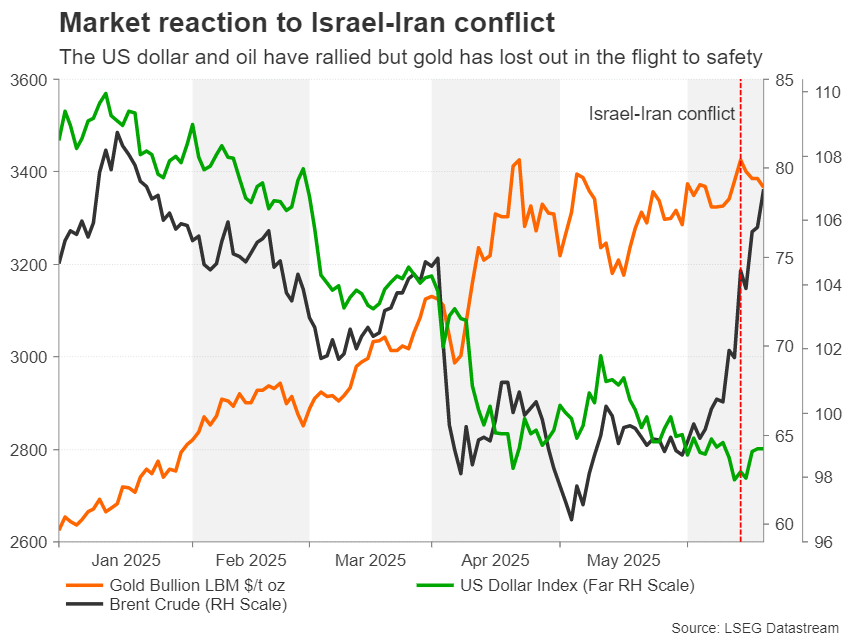

Complicating matters, however, is the recent escalation in the Middle East, with neither Israel nor Iran appearing ready to back down in the week-long exchange of missiles. Although outside of energy markets, investors’ response has been somewhat muted, the biggest worry now is that the United States might enter the conflict. There is intense speculation that Washington and Tel Aviv want to wipe out Iran’s nuclear capabilities, risking triggering a wider regional war.

Any further escalation could extend oil’s and the dollar’s latest rebounds, and the safe-haven gold might even join the rally too. But risk assets, particularly stocks, could come under pressure. The only relief for Wall Street in such a scenario would be the announcement of a new trade deal between the US and one of its main trading partners such as India or Japan.

Euro’s setback likely to be temporary

The euro has been a surprise beneficiary of the trade war, as Trump’s dangerous rhetoric has been seen as damaging to America’s standing in the world, with investors questioning whether the country remains a safe and attractive place to do business in. However, the flare up in the Middle East has exposed Europe’s vulnerability to fluctuations in energy prices. And it’s not just about oil, as gas prices have also been rising since the conflict started – Iran is the world’s third largest producer of natural gas.

But barring a much more severe crisis, the euro’s prospects are looking up in the bigger picture as the European Central Bank’s easing cycle is coming to an end while the Fed’s has paused less than halfway through. Moreover, Eurozone growth has been unexpectedly robust in the first few months of 2025, and so should Monday’s flash PMI numbers continue to suggest that the economy took only a minor hit from the trade war, the euro might recoup some of its recent pullback.

Investors will also be keeping an eye on the Ifo business climate index due out of Germany on Tuesday.

Pound underperforms amid geopolitical risks

Across the channel, the flash PMIs will also be the only highlight in the UK. Like the euro area, the British economy had a strong first quarter. Additionally, the UK has signed a trade deal with India, agreed on an improved post-Brexit deal with the EU, and is the first country to reach a trade pact with President Trump.

All this underpins sterling’s uptrend that started in mid-January but is now being tested by the heightened geopolitical and trade uncertainty. The UK’s twin deficit problem leaves the pound much more exposed to market volatility than some of its peers like the euro, regardless of the UK’s otherwise sound economic fundamentals.

Hence, even if Monday’s PMI readings show a further recovery in June from the April dip, gains are likely to be limited as long as safety flows are headed in the dollar’s direction away from riskier bets.

Will Canadian CPI add to BoC’s worries?

Despite some reports that the US and Canada are close to agreeing on a deal that would permanently keep tariffs between the two countries low, there has yet to be any announcement. A deal would clear a lot of the fog over the outlook for the Bank of Canada, as it tries to navigate the downside risks to growth and a buildup of price pressures.

Underlying inflation has been steadily rising in Canada this year, with some measures exceeding 3.0%. The latest CPI figures are due on Tuesday and will be watched closely for signs that core inflation has started to ease.

If there’s no improvement in the May data, investors will likely further scale back their expectations of a 25-bps rate cut at the July meeting, which currently stand at just over 20%. This could help the Canadian dollar to get back on the front foot against the US dollar, which saw its safe-haven status being restored from the tensions in the Middle East.

Other Canadian data will include the monthly GDP print on Friday.

CPI on investors’ radar in Australia and Japan too

Finally, CPI reports will also be doing the rounds in Australia and Japan. Australia’s monthly CPI release will come under scrutiny on Wednesday ahead of the Reserve Bank of Australia’s next policy decision on July 8 where a 25-bps rate cut is about 65% priced in.

The Australian dollar, which has not shown much reaction to the Israel-Iran conflict, could advance against the US dollar if CPI edges higher, as investors would become less confident about future RBA rate cuts even if a reduction in July remains on the table.

The Bank of Japan is facing even greater uncertainty regarding the direction of monetary policy as the trade war poses a danger to Japan’s fragile economic recovery.

The yen has lost out to the dollar during the latest geopolitical episode, but there could be some gains for the Japanese currency next week as there’s a flurry of releases on the way. The flash PMIs are up first on Monday, followed by the Tokyo CPI numbers on Friday, alongside the unemployment rate and retail sales for May.

Core CPI in Tokyo reached a more than two-year high of 3.6% y/y in May. A further uptick in June would bolster bets of the Bank of Japan hiking interest rates again later this year, potentially lifting the yen.

The Wrong Kinds of Targets

‘What gets measured gets managed’ highlights the risk of targeting the wrong metrics or an arbitrary level of the right one. This could be an issue for defence spending targets, with implications for public finances and yields more generally.

- ‘What gets measured gets managed’ is a warning against picking the wrong metrics. In some areas, like central bank inflation targets, both the metric and the target level have an evidenced-based rationale. Other targets can be misconceived though, or the metric might be reasonable but the target level completely arbitrary.

- The risk of an inappropriate metric or target level is relevant to current debates about the appropriate level of defence spending. Just spending more money on something does not always yield better outcomes. And some of the most impactful policies to protect a nation’s security might not even look like defence spending.

- Increased defence spending probably won’t translate one-for-one into bigger public deficits. How this debate plays out in different countries could materially affect budget outcomes, debt issuance and so long bond yields over time.

The saying ‘what gets measured gets managed’, sometimes mistakenly attributed to Peter Drucker, highlights the perils and pitfalls of poorly designed quantitative targets. The management literature is full of examples of metrics and targets gone wrong. Sometimes the metric does not align to the intended result. The call centres that incentivised the number of calls handled – not the number of issues resolved – are a canonical example of this problem. More broadly, incentives to do things quickly rather than properly often run into strife down the track.

Sometimes the misalignment arises because the metric keyed off a presumed intermediate objective, like number of sales calls, rather than the measurable ultimate goal (actual sales or profits). But as central banks found out with targets for money supply growth in the 1980s, these metrics presume a simple and stable relationship between the metric and the true target that might not hold in practice. (See also: Goodhart’s Law.)

Other times, the metric seems reasonable, but the target level is arbitrary or lacking good foundations. Certainly the debt and deficit limits in the EU’s Maastricht Treaty have been criticised on these grounds. Another example closer to home is that spending a large fraction of your income on housing does seem like a signal that housing is not affordable. Who is to say, though, that 30% of gross income is the threshold between affordable and unaffordable? It

turns out that this rule of thumb originated many decades ago in US government housing assistance programs for low-income households. That is unlikely to be a relevant benchmark for Australian home-buyers nowadays. Thus, it is helpful that mortgage lending decisions are based on more sophisticated and relevant metrics.

At least in economic policy, we have moved on from the 1980s era of money supply targets (though I am less sure we have completely moved away from ‘checklists’). The inflation targets introduced in the 1990s were backed up by analysis showing that keeping inflation low improved economic performance and the welfare of the population. The exact level of the target is less relevant. Measurement issues mean it needs to be above zero, but provided it is low enough that inflation is not distorting decisions, it matters little exactly what the target is. A target of 2% or 2½% will do just as well as the other, with no benefit to switching between them.

The tendency to frame a desirable objective with a potentially ill-conceived metric or target level is not confined to economic policy. We are seeing something similar in current debates on defence spending. Who is to say that a particular share of GDP is the ‘right’ amount to spend on defence?

After all, it would be all too easy to meet a spending target by wasting a large amount of money: think military bases in the wrong place, and overpriced equipment that doesn’t work or isn’t appropriate to modern warfare. And it is hard to withstand arguments along the lines of, ‘how can you justify not spending every available dollar and bearing any conceivable cost to save lives or avoid this existential risk?’

The counter to these sorts of arguments is one of the most basic concepts in economics: opportunity cost. Choosing to spend money (or time) on one thing means not spending that money or time on anything else. Giving up that ‘anything else’ is the opportunity cost. So the right question is to ask ourselves is: ‘how can we save lives or preserve our way of life in the most effective way possible, so that we don’t have to impose costs on people that end up undermining society’s resolve to achieve that goal?’

There is also the issue of what counts as defence spending. To be honest, if I were appointed national security advisor for a day, among my first priorities would be to massively fund university research into alternative battery and magnet technologies that do not rely on rare-earth metals for which single countries dominate supply, as well as research into cleaner processing of those minerals. That would not even count as defence spending. My other initial priority – fostering a domestic drone industry, including design, manufacturing and operation – would probably also not count as defence spending, given that civilian uses would do just as well to build up that capability.

On top of the defence-specific and national security issues here, how the debate about the appropriate level of defence spending plays out has broader economic implications. Increased defence spending need not translate one-for-one into higher government spending, let alone larger government deficits. Governments will try to find savings and trade-offs elsewhere to make things fit; that is opportunity cost in operation. But to the extent that it does boost government borrowing, this has implications for bond markets, for the global level of yields, and for the size and shape of private investment. With increased resolve in Europe and Germany changing its constitution to enable re-armament, some upward pressure on yields seems inevitable. This will depend, though, on what other choices governments make.

Weekly Focus – War and Risk of Escalation Weigh on Market Sentiment

The war between Israel and Iran and the risk of further escalation weighed on markets this week. Equity markets largely traded in red and US treasury yields slid lower. That said, markets were by no means in full risk-off sentiment, with gold prices sliding gradually lower during the week and no noticeable outperformance of traditional FX safe havens. With oil prices up close to USD10 per barrel compared to levels before Israel's attack on Iran, US recession risk lower and US equity outperformance, the USD has seen several tailwinds. Even so, it struggles to find persistent support and we see growing evidence that the de-dollarization narrative is gaining traction.

On the data front, the past week showed us that private spending on neither side of the trade war seems much affected through May. US retail sales did not show much sign of weakness, at least not in core spending, particularly not when you measure them against the dire consumer confidence. Chinese retail sales even surprised to the upside, lifted by stimulus. However, one key root cause for consumer concern, the weak housing market, softened further with continued low activity and declining prices. In Germany, the expectations component of the ZEW survey has now almost fully recovered from the 'Liberation Day' decline in April. Current conditions have also improved but remains low in a historical perspective.

We have seen a regular central bank flurry this week with several rate cuts including a major surprise from Norges Bank, see more in the scandi section. The Swiss National Bank (SNB) has now cut rates all the way to zero, as inflation remains muted not least on the back of a strong Swiss Franc. The SNB highlight that they will not take the decision to go negative lightly, though. Both the Bank of Japan and the Bank of England kept rates unchanged and saw fresh inflation data ticking in way too high this week. In Japan, inflation is mostly driven by food, and trade war uncertainties are pausing the hiking cycle. In the UK, inflation pressures are broader, but we expect they will find room to cut rates come August. The Fed kept monetary policy unchanged and did not provide markets with new guidance. The market reaction was very muted. We continue to see cuts in September and December, followed by three more in 2026.

Next week on the data front, we kick off with PMIs. We expect the euro area manufacturing PMI to stall just below 50 as tailwinds from front-loaded exports to the US fades. Weak consumer confidence should continue to weigh on the service sector which has lost steam in recent months. We will also keep a close eye on inflation data on Friday. At the NATO summit, the countries are likely to adopt the new 5% target for defence expenditure as a share of GDP (3.5% as actual defence spending and 1.5% as additional investments in resilience). In between, we will continuously monitor the situation in the Middle East and the risk that the US is pulled further into the conflict.

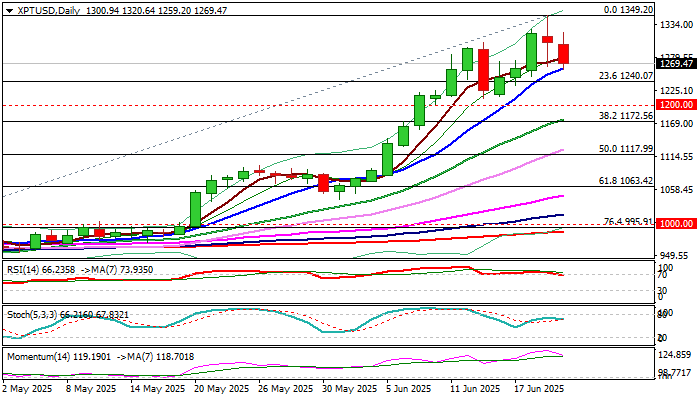

Platinum Eases from New Multi-Month High as Traders Take Profit from Nearly 30% Rally in June

Platinum extends pullback into second consecutive day and fresh bears accelerated on Friday on stronger profit taking from new multi-year peak ($1349 – the highest since Sep 2014).

The metal was in steep rally in past two months, which gained pace in June, when the price advanced almost 30% in first three weeks of the month.

Strong acceleration was sparked by breach of psychological $1000 level in early May and boosted by growing demand and unchanged supply that created a disbalance and lifted the price sharply.

Profit-taking after such strong rally could be also significant, as pullback was signaled by bearish divergence on RSI and Stochastic indicators before the price started to ease, as well as strong reaction to steep advance in past two months.

Easing geopolitical situation is also likely to contribute to near-term action.

Reversal pattern is about to be completed on daily chart that would contribute to bearish outlook.

Bears cracked initial support at $1260 (rising 10DMA), guarding Fibo support at $1240 (23.6% retracement of $886/#1349 uptrend), violation of which to expose psychological $1200 level and Fibo 38.2% at $1172.

Res: 1300; 1320; 1327; 1349.

Sup: 1260; 1240; 1200; 1172.

Sunset Market Commentary

Markets

US President Trump’s decision to give diplomacy a chance in the Middle East conflict brought some relief to risky assets. European leaders to that end hold nuclear talks with Iran in Geneva today. Trump said he’ll decide “within the next two weeks” whether or not the US will get militarily involved. There were concerns of an immediate direct attack after the country had sent military aircrafts and warships to the region these last couple of days. “Within the next two weeks” is quite vague and it wouldn’t be the first time Trump joined a disinformation campaign (he said he didn’t knew about the Israeli opening strike on Thursday yet evacuated amongst others the Iraqi embassy hours prior to it). The wording (“within”) also keeps all options on the table (including a weekend strike?!) but it eases some of the tension in markets nonetheless. The technical picture of the likes of the EuroStoxx50 began to look pretty dire after a slide that began late last week but the index is rallying around 1.2% now. Wall Street opens with minor gains but dodged the risk-off downleg on Thursday due to Juneteenth. Core bonds lose ground with Treasuries underperforming Bunds. US yields march 1.7-4.3 bps higher in a bear steepener. But then Fed Waller upended the rise to a certain extent with some remarkably dovish comments. He played down the inflation impact coming from tariffs. Unless in case of a big shock, the Fed should look through it. Waller thinks the Fed should not wait much longer for rate cuts (July could be a candidate, he said), favouring to move pre-emptively and not wait until the labour market tanks. German rates add around 1 bp across the curve. FX markets trade muted. The US dollar is performing mixed against G10 peers and loses out amongst others against the euro. EUR/USD ekes out a slight gain to change hands around 1.152. The trade-weighted dollar index eases to 98.7. DXY clearly struggles to escape from the recent multiyear lows. Sterling quickly overcame early morning weakness triggered by awful retail sales. Headline volumes dropped by 2.7% m/m, wiping out all of gains made YtD through April. The gauge excluding auto fuel was equally bad (-2.8% m/m) and suggests the consumer, representing around two-thirds of the British economy, is letting down. We’ll need to see some follow-up readings first before drawing any conclusions though. That appeared sterling’s take as well with EUR/GBP now actually down for the day (0.852). The Japanese yen trades stoic even after this morning’s inflation numbers came well above the 2% central bank target and suggest continued growing price pressures, including in the services economy. USD/JPY fills bids around 145.6.

As this week is coming to an end, let’s take a look at the next one. The eco calendar is well filled. May PMI business confidence are on tap on Monday. The US Conference Board consumer confidence and the Hungarian central bank meeting are due on Tuesday while the Czechs meet the day after. Fed chair Powell also on Tuesday delivers its semi-annual testimony before Congress. His British colleague Bailey is doing a similar thing the same day (before the House of Lords). June 26-27 features an EU leader summit which centers, amongst others, around the international role of the euro. US PCE inflation and the first EMU member states CPI prints are scheduled for release on Friday. We’re also on the look out for the trade and fiscal topic to return as Trump’s July 9 tariff pause deadline and the July 4 target date for the Big Beautiful Bill is drawing near.

News & Views

The National Bank of Belgium’s monthly survey showed that consumer confidence in the country improved further to -7 to -4. In this respect the index returned back to the level last seen in February of this year. More positive expectations concerning the economic situation in Belgium and waning fears of unemployment are boosting confidence. The subindex assessing confidence on the economic situation in Belgium improved to -24 from -30 in May, to be compared to a cycle low of -44 in April. Concerns about unemployment eased to 6 from 13. On a personal level, households’ expectations regarding their savings (19) and their own financial situation (-3) remained unchanged compared to last month.

Canada: Retail Sales Rise in April But Q2 Outlook Remains Murky

Retail sales edged up 0.3% in April month-on-month (m/m), slightly below the Statistics Canada's advanced estimate.

After adjusting for inflation, the volume of retail sales increased 0.5% m/m.

For the second straight month, strength in motor vehicles and parts sales (+1.9% m/m) was the primary driver of headline growth. Ex-autos, sales were down 0.3% m/m.

Receipts at gas stations and fuel vendors plunged by -2.7% as gas prices tumbled 18.1% as the consumer carbon tax ended.

Excluding auto sales and receipts at gas stations, core retail sales edged up by 0.1% m/m. The marginal increase was supported by strong growth at miscellaneous store retailers (+2.0% m/m). Most other categories either made minimal contributions or weighed on overall sales.

E-commerce sales rose by 3.6% m/m in April.

Statistics Canada's advanced estimate points to a 1.1% m/m contraction in May.

Key Implications

As expected, consumers continued front-load vehicle purchases in anticipation of price increases that are likely to come due to tariffs. However, core sales may be an early signal of broader consumer hesitancy in the face of trade policy headwinds. According to a supplementary by Statistics Canada survey, 36% of retail businesses reported being affected by trade tensions in April. The most commonly cited impact included price increases, change in demand, and supply chain disruptions.

The advance estimate sets a somber tone for the second quarter. In addition, our internal credit and debit card spending data shows a meaningful softening in spending through May, suggesting that consumers tightened their purse strings. As a result, we expect real personal consumption expenditures to be flat this quarter, with consumer spending likely to contract in Q3 if U.S. tariffs continues to weigh on sentiment and job prospects.

Crypto Traders Hedging Risks of Correction

While Bitcoin is consolidating in the spot market, the futures market is signalling growing risks of a Bitcoin correction. Traders are hedging against the risk of a pullback to $100,000 and below against the backdrop of escalating geopolitical conflict. This significantly worsens global risk appetite and increases uncertainty in the Fed’s monetary policy. Jerome Powell expects a significant acceleration in inflation in the US. This is not good news for US stocks and income assets in general.

The ratio between put and call options on Bitcoin on the Deribit cryptocurrency derivatives exchange jumped to 2.17 in one day, signalling high investor demand for protection.

The news of Congress passing legislation on stablecoins failed to help Bitcoin. The United States, led by the president, is confirming its loyalty to the crypto industry. Since Donald Trump’s victory in the presidential election, Bitcoin has risen by 50%.

Its future largely depends on developments in the Middle East. Escalation in the form of other countries getting involved and Iran blocking the Strait of Hormuz could lead to a further deterioration in global risk appetite and a rollback of the upward trend in the coin.