Sample Category Title

History Made In Singapore As Trump-Kim Summit Kicks Off

The market focus of the world is focused on the events taking place in Singapore, with history being made today as Donald Trump became the first sitting American president to meet face-to face with a North Korean leader.

The market reaction has been mostly positive, and this sentiment is likely to continue with the expectance that President Trump and Kim Jong-un are to discuss the future of Pyongyang’s nuclear programme. While the likelihood of North Korea signing a peace treaty is unlikely at this stage, it does appear that Trump and Kim Jong-un have developed a bond.

Kim Jong-un has said the 'world will see a major change' and this is likely to be a catalyst for further risk appetite in the financial markets. Improved momentum towards global stocks and further risk appetite attracting investors are a possibility following the conclusion of this summit. The talks could be seen as an important step to easing geopolitical tensions in the region, especially when considering how North Korea has pledged to work towards ‘complete denuclearization’. A positive outcome to the summit could open a path for further talks down the pipeline, ultimately supporting global sentiment.

G7 ‘Trumped’ but markets unfazed

Global equity markets are trading mostly higher as investors shrugged off the rough and rocky G7 summit that took place over the weekend.

The talks between world leaders and Trump in Quebec were mostly dominated by disagreements and arguments over trade, fuelling concerns over a potential global trade war. With Trump injecting a dosage of chaos and uncertainty by withdrawing from a joint statement with the G7 allies, trade tensions are likely to remain a recurrent market theme.

Dollar steady ahead of Fed meeting

The Dollar is likely to remain supported against a basket of major currencies ahead of the Federal Reserve decision on Wednesday, which is widely expected to conclude with a US interest rate hike.

It is already considered a foregone conclusion that US interest rates will be increased in June, so attention will mostly be directed towards the economic projections and press conference by Fed Chair, Jerome Powell. Investors will most likely scrutinize the fresh projections and Powell’s conference for clues on rate hike timings beyond June. King Dollar has scope to appreciate further if policymakers adopt a more hawkish stance than anticipated, reinforcing market expectations of at least one more rate hike this year.

From a technical standpoint, the Dollar Index is in the process of a higher technical bounce. An intraday breakout above 93.90 could encourage bulls to target 94.00 and 94.30, respectively.

Euro seeks guidance from ECB

Easing political tensions in Italy have heavily supported the Euro in recent days with the EURUSD rising to a near two-week high at the start of the trading week.

With the European Central Bank meeting scheduled on Thursday, this will be an important trading week for the Euro. Market expectations remain heightened over QE potentially ending this year, and investors will mostly likely seek guidance from the ECB meeting to confirm these speculations. The Euro could extend gains against the Dollar if Mario Draghi adopts a hawkish stance and expresses optimism over the health of the European economy.

Currency spotlight – USDJPY

The Japanese Yen has extended losses against the Dollar this morning, with the USDJPY punching above 110.40 as of writing.

The weakness in the Yen signals an improved risk risk-on sentiment. With the Dollar likely to remain supported by Fed hike expectations, the USDJPY has scope to venture higher. A technical breakout above 110.50 could encourage an incline towards 111.10.

Commodity spotlight – Gold

Gold is likely to remain range bound ahead of the FOMC meeting on Wednesday, which is expected to conclude with a US interest rate increase.

While global trade tensions have somewhat supported the yellow metal, a US rate hike could spell trouble for zero-yielding Gold. Market players could continue closely observing how prices behave around the $1300 psychological level. A decisive breakout above $1300 may trigger an incline higher towards $1324. On the other hand, if the $1300 acts as a firm resistance level, prices could descend back towards $1280.

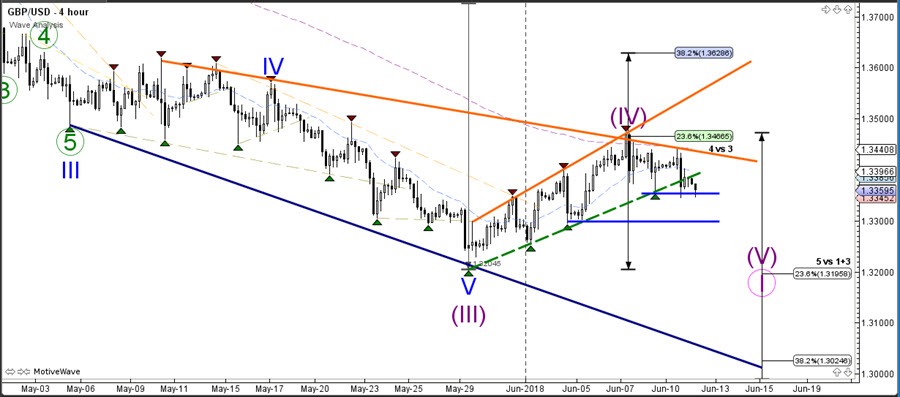

GBP/USD Bear Flag Break Awaits Wave 3 Momentum

The GBP/USD is breaking below the support trend line of the bear flag chart pattern after bouncing at the 23.6% Fibonacci retracement level. The bearish breakout could indicate the restart of the downtrend and aim for a target zone at 1.30.

The GBP/USD still needs to break other support levels (blue) before a full bearish breakout could be expected. A break above the resistance trend line (orange) could indicate a larger correction towards the 38.2% Fibonacci level.

The GBP/USD is building a bearish channel. Price will need to break the bottom of the channel before an impulsive and bearish wave 3 could be expected and confirmed. A break above the channel invalidates the current wave pattern.

USD/JPY Bullish Channel Breaks Above Triangle Pattern

The USD/JPY broke above the key resistance trend line (dotted orange), which could confirm a bullish wave Y (purple) that is aiming for 111.50– 112.50.

The USD/JPY is probably building a WXY (purple) correction within a larger triangle pattern from the daily chart (wave D purple).

The USD/JPY remains rooted in an smaller bullish channel (purple) of a larger uptrend channel. Price could be developing a potential ABC correction within wave Y (purple) so any bearish pullback could see a bounce at the bottom of the channel.

ECB Ready To Map The End Of APP

- ECB orchestrated communication to build expectations

- Draghi to change forward guidance on APP: December 2018 firm end date

- Window of opportunity via higher inflation expectations

- Announcement should set a bottom below yields, euro to take the edge over USD

Expectations going into the previous, April, ECB meeting were low and President Draghi immediately took the sting out of the Q&A session by indicating that they didn’t discuss monetary policy. The Italian political crisis in the second half of May threatened to produce a similar outcome at this week’s ECB meeting if it wasn’t for last week’s orchestrated ECB interventions. A well‐placed and welltimed “sources” article reminded investors that the June policy meeting is a “live” one. That’s central bank lingo suggesting possible changes to communication/policy could be taken. Soft rumours rapidly turned into clearer and somewhat hawkish comments from the likes of ECB Praet, Weidmann, Knot and Hansson.

Chief economist Praet is one of the architects of the current exceptional monetary policy. He always defended the very accommodative policy by arguing that enough slack remains for the EMU economy to grow without creating inflationary pressures. Last week he changed course by pointing to increasing signals that inflation is converging towards the ECB’s 2% aim. He added that the central bank will have to assess on June 14 whether to signal an eventual end to the APP. The significance of what was a rare and specific hint from Praet shouldn’t be underestimated. Dutch central bank governor Knot added that it would be reasonable to announce the end of the net asset purchases soon. Bundesbank president Weidmann, another heavyweight, said that market expectations of an end to QE this year are plausible. Estonia’s central‐bank governor Hansson suggested that official interest rates might even climb sooner than investors expect.

Tapering in Q4 2018

Aggregating last week’s ECB rhetoric suggests at the very least a preannouncement this week about the future of APP even if specific details of the ending of the programme might not fully emerge until in the following council meeting in late July. However, we think that, on balance, recent comments in the media mean risks have shifted to the point where markets will expect a clear communication outlining the ECB’s future intentions in regard to QE on Thursday. The most plausible explanation for the ECB’s encouragement of such expectations is that it wants to eliminate any room for ‘event risk’ to pop up and map out 2018 monetary policy as soon as possible.

More specifically, we think Draghi may announce that the ECB will taper its asset purchases by €10bn/month to conclude the programme by December 2018. The forward guidance currently reads that net asset purchases are intended to continue at a monthly pace of €30bn until the end of September, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. Praet’s comments suggest that this final condition has now been met.

The latest EMU inflation numbers create a window of opportunity for the ECB to finally take the next step in its normalization process. Preliminary estimates for May show that headline inflation jumped from 1.2% Y/Y to 1.9% Y/Y and core inflation picked up from 0.7% Y/Y and 1.1% Y/Y. Seasonal factors and the rise in energy prices are significantly responsible for what appears to be a notable change in trend. The numbers will probably remain elevated, at least for the next two months. While the ECB won’t let itself be unduly swayed by unusual and possibly reversible movements in monthly inflation data , it will be interesting to see if the May figures are seen as indicative of a long expected firming in inflation. If this is the case, it could prompt upward revisions to new inflation forecasts which the ECB will release on Thursday. March projections showed an average 1.4% inflation rate both this year and next and 1.7% in 2020. The ECB assumed an average oil price of $65/barrel and a spot rate of 1.23 for EUR/USD. Updates to both imply higher inflation, at least for this year. Praet’s hint about building underlying inflation pressures could translate into a crucial upgrade of the 2020 forecast which would underpin a decision to end the asset purchase programme

Growth forecasts amounted to 2.4% in 2018, 1.9% in 2019 and 1.7% in 2020. The disappointing Q1 GDP print suggests a downward revision for this year. The KBC forecast for 2018 is 2.1%. We don’t think that the ECB will move too quickly or aggressively to downgrade its 2019 and 2020 forecasts although a slight pull‐back could be the counterpoint to a slightly higher inflation forecast. The ECB is clearly focused on the potential negative impact from the escalating trade war, but may appear as a significant downside risk in the balance of risks rather than as a key element of the central scenario.

The continuous decline in the EMU composite PMI, from a cycle high of 58.8 in January to 54.1 in May is partially because of a natural rolling over and partially because of stress‐related to eg the trade conflict and the Italian crisis

However, the absolute level of the PMI at present remains consistent with a very healthy pace of growth in the Euro area, giving the ECB leeway to pursue a very gradual normalization process.

The forward guidance on interest rates and QE reinvestments are both likely to remain unchanged. The ECB may want to signal that a journey out of unconventional policy is about to begin, but the pace of travel is unlikely to be speedy. The ECB at this stage doesn’t want to trigger early rate hike expectations. We do agree with ECB Hansson though that current expectations about a first rate hike (end 2019) are too dovish. We eye a first deposit rate increase by mid‐2019. The reinvestment policy is expected to remain in place in the foreseeable future

Higher EMU yields and stronger euro?

If the ECB provides clear signals on Thursday of its intent to end QE, it will want to sugar coat this pill. So, Mr Draghi will likely emphasize that monetary policy will remain very accommodative. However, an ECB announcement about an end date of APP would be a significant development and should soon put a firm bottom below European interest rates. The German 10‐yr yield could return above the 0.5% mark and thereafter proceed initially towards a test of this year’s high around 0.8%. In Q4 2018, interest rate expectations will start to build whether the ECB wants it or not. The next significant move of the ECB, changing forward guidance on interest rates, could come at the December meeting. The ECB meeting coincides with the Fed meeting this week with the US central banks expected to hike its policy rate by 25 bps to 1.75%‐2% with a potential hawkish shift in the dots. The US side of the story is more discounted than the European one, suggesting that the balance could shift in favour of the single currency on FX markets. First resistance in EUR/USD stands around 1.1830

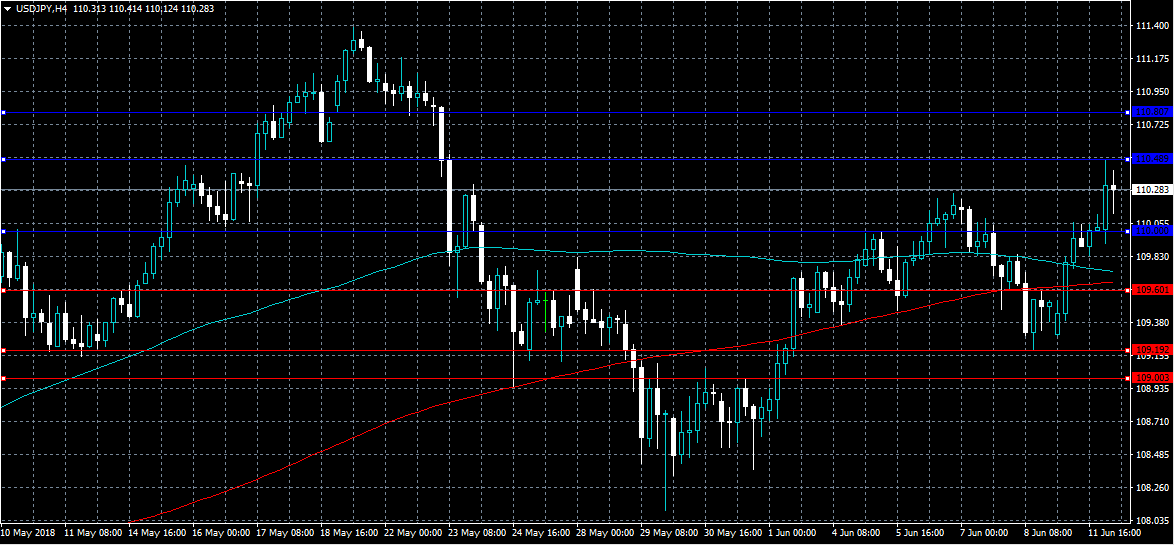

USDJPY Now Bullish Above 110.00 Level

The US dollar now trades back above the 110.00 level against the Japanese yen, with the pair earlier hitting 110.48, as the US dollar index gains back lost ground. The USDJPY currently trades around the 110.20 level, with risk-on trading sentiment supporting further intraday upside in the pair. Traders now look for fresh news from the meeting between President Trump and North Korean leader Kim Jong-un, and the release of key CPI inflation data from the United States economy.

The USDJPY pair is bullish while trading above the 110.00 level, key resistance is found at the 110.48 and 110.80 levels.

If the USDJPY pair moves below the key 110.00 level, key intraday support is now found at the 109.60 and 109.19 levels.

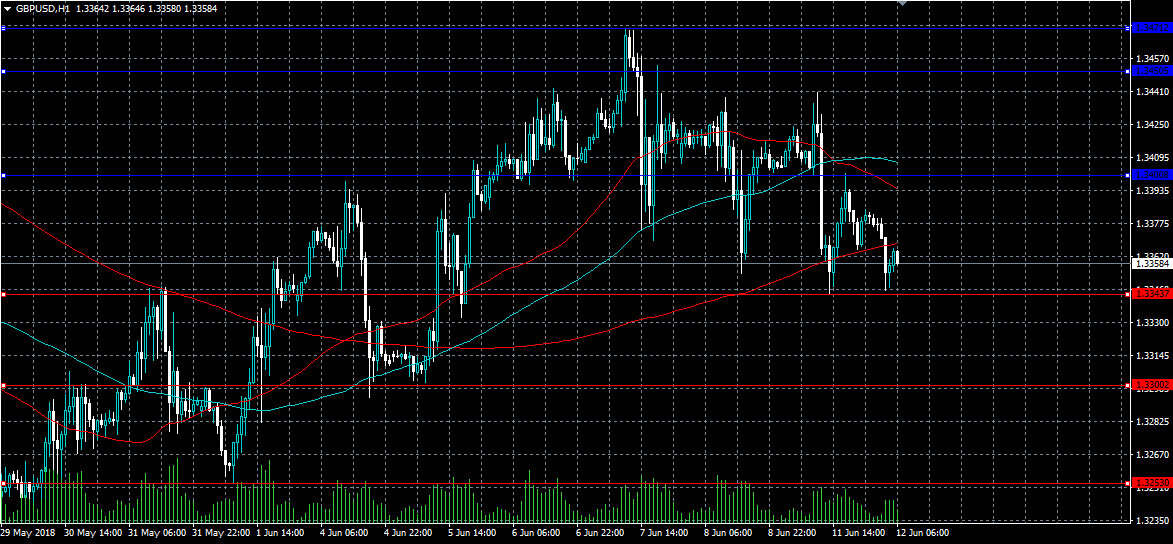

GBPUSD Intraday Bearish Below 1.3352

The British pound remains weak against the greenback in early Tuesday trading, as worse than expected UK economic data and a stronger US dollar weigh on sterling sentiment. The GBPUSD pair currently trades around the 1.3360 level, after finding interim technical support from the 1.3343 level. Traders now look towards the release of key Wage Earnings and Employment data from the United Kingdom economy.

The GBPUSD pair is bearish while trading below the 1.3352level, key technical support is now located at the 1.3343 and 1.3300 levels.

If the GBPUSD pair continues to hold above the 1.3352 level, buyers may test towards the 1.3400 and 1.3450 resistance levels.

Bitcoin Slides To 2-Month Low After Exchange Hack

The price of bitcoin rose in April from a multi-month low of $6430 to a high of $9725. This was a 50% increase in the price as traders expected more demand for the cryptocurrency. Since this time last year, the price of bitcoin has fallen by more than 50%, which is lower than the 1000% gain it made last year.

This weekend, the price declined to $6530, the lowest level since early April. The decline was attributed to the hack of a small South Korean cryptocurrency exchange known as Coinrail. The hack resulted in the loss of about 30% of the exchange’s virtual currencies. 70% of the remaining currencies were stored in a cold wallet, which is not connected to the internet.

After the hack, the market value of cryptocurrencies declined by more than $42 billion. South Korea is one of the largest cryptocurrency trading centres and is home to world-leading exchanges such as Bithump which has exceptionally high transaction volumes.

The hack highlighted the need for tighter regulations globally. In recent months, a number of cryptocurrency-related hacks have been reported and hackers are continually attempting to attack prominent exchanges like Coinbase.

The BTC/USD pair is currently trading at $6757, which is slightly higher than yesterday’s low of $6530. It is trading below the 60 and 100-day moving average, with its RSI near the oversold level. The pair could reverse its downward trend as bulls take over. This could see the pair test the 60-day moving average at $7350.

UK, US Data In The Spotlight On Tuesday

Economic data is in the spotlight on Tuesday, although other factors will also impact the financial markets. A high-stakes summit between US President Donald Trump and North Korea's Kim John-un will also influence investor sentiment as both sides negotiate nuclear disarmament on the Korean peninsula.

The UK Office for National Statistics will kickoff an active release schedule at 08:30 GMT by unveiling the latest employment numbers. UK unemployment levels likely rose by 11,300 for May. Unemployment in the three months through April is forecast to hold steady at 4.2%. Meanwhile, average hourly earnings including bonuses likely rose .26% annually in the February-March period.

Shifting gears to the Eurozone, the ZEW institute will report on German investor sentiment at 09:00 GMT. ZEW will also release a separate euro-wide study reflecting economic sentiment for the month of June.

North America's release schedule will be headlined by the US Labor Department's monthly consumer inflation index. The consumer price index (CPI) is forecast to rise to 2.8% in the 12 months through May, placing more pressure on the Federal Reserve to continue normalizing monetary policy.

Commodity traders will also be keeping an eye out for weekly crude inventory data courtesy of the American Petroleum Institute (API). The API numbers usually provide a decent barometer for the official inventory data due the following morning.

In terms of geopolitics, US President Donald Trump greeted North Korea's Kim Jong-un in Singapore on Tuesday for the start of bilateral talks. Both leaders shook hands at the summit, a landmark moment in what is expected to be a long and uncertain journey.

Tuesday will also see the start of the Federal Reserve's two-day policy meeting in Washington. Fed officials are widely expected to vote in favor of raising the benchmark interest rate on Wednesday.

EUR/USD

Europe's common currency started the week on the back foot as the dollar gained ground on a basket of currencies. The EUR/USD exchange rate has run into fierce resistance near the 1.1820 handle, as demonstrated by the double-top formation around that level. The bulls need to penetrate this handle to keep upside momentum alive

GBP/USD

Cable resumed its downward correction on Monday, as prices continued to backtrack from last week's swing high. GBP/USD fell another 0.2% at the start of Tuesday trading, with prices hovering at 1.3358. The pair faces strong resistance near 1.3470, which corresponds with the 7 June high.

USD/CAD

The USD/CAD exchange rate successfully breached the 1.3000 level on Monday, as trade tensions continued to weigh on the loonie. The pair is currently trading just a few pips shy of the psychological 1.3000 handle with prices poised to rise further should the Fed strike a hawkish tone.

Full text of Kim and Trump comprehensive document

Here are some of the texts:

"President Trump committed to provide security guarantees to the DPRK, and Chairman Kim Jong Un reaffirmed his firm and unwavering commitment to complete denuclearization of the Korean Peninsula."

1. The United States and the DPRK commit to establish new US-DPRK relations in accordance with the desire of the peoples of the two countries for peace and prosperity.

2. The United States and the DPRK will join their efforts to build a lasting and stable peace regime on the Korean Peninsula.

3. Reaffirming the April 27, 2018 Panmunjom Declaration, the DPRK commits to work toward complete denuclearization of the Korean Peninsula.

4. The United States and the DPRK commit to recovering POW/MIA remains, including the immediate repatriation of those already identified.

The United States and the DPRK commit to hold follow-on negotiations, led by the US Secretary of State, Mike Pompeo, and a relevant high-level DPRK official, at the earliest possible date, to implement the outcomes of the US-DPRK summit.

President Donald J Trump of the United States of America & Chairman Kim Jong Un of the State Affairs Commission of the Democratic People's Republic of Korea have committed to cooperate for the development of new US-DPRK relations and for the promotion of peace, prosperity, and security of the Korean Peninsula and of the world.

Full text:

https://twitter.com/chadocl/status/1006427837434216449

The signing:

https://twitter.com/ABC/status/1006421470317293569

Smart, talented Kim scored outstanding diplomatic win

North Korea leader Kim Jong-un signed a "comprehensive letter" today, following the high profile, Singaporean paid, summit. Kim scored an outstanding diplomatic win as he's now turned from a friendless dictator to a "very smart", "talented" man who loves his country very much.

Kim said that the two leaders had a historical meeting and "decided to leave the past behind". Kim promised "the world will see a major change". Trump said he had formed a "very special bond" with Kim. And, Trump expected the denuclearization process to start "very, very quickly". Trump also hailed Kim as a "very smart" and a "very worthy, very hard negotiator"and added, "I learned he's a very talented man. I also learned that he loves his country very much." He also said the summit had gone "better than anybody could have expected".

In the document they signed, it's delcared that North Korea would work toward the "complete denuclearization of the Korean peninsula" and committing to a "lasting and stable peace." In exchange, the US promised to provide unspecified "security guarantees" to Kim. Also, they agreed to establish new relations "in accordance with the desire of the peoples of the two countries for peace and prosperity" and said they would work on recovering "POW/MIA remains."