Sample Category Title

2Y Italian Government Bonds Rallied Some 60bp

Market movers today

While markets are digesting the Trump-Kim summit , we also have a lot of other stuff on the agenda today. In Norway, we will get the Regional Network Survey

In the US, we expect CPI core to rise 0.2% m/m (in line with consensus), implying an increase in the inflation rate to 2.2% y/y from 2.1% in April. The NFIB small business optimism index in May is also due out today.

In the UK, focus is on the House of Lords' amendments to the EU withdrawal bill, which returns to the House of Commons today (two-day debate). Focus will be on whether Conservative rebels will go against PM Theresa May and vote for a softer Brexit. The jobs report for April is also due out at 10:30 CEST. It might be a volatile day for EUR/GBP.

In Germany, ZEW expectations for June are due out today.

Selected market news

There was no market moving news yesterday. Markets took a cautious stance ahead of the Donald Trump-Kim Jong-un meeting as well as the major central bank meetings this week.

Expectations ahead of the summit were relatively diffuse though, as only shortly ahead of the meeting it was announced that a one-to-one talk and working lunch was planned at the historic meeting today. Very little information has been shared at this stage, besides footage of Donald Trump and Kim Jong-un shaking hands. Trump said, ‘I think we're going to have a great discussion' while Kim Jong-un said, ‘many obstacles had been overcome to get this far.' Trump is said to be holding a press conference today at noon CEST.

In the Scandies, yesterday's inflation print in Norway marked yet another CPI disappointment with the core measure falling short (1.2% y/y) of both Norges Bank's (1.6%) and markets' expectations (1.4%). Meanwhile, the details were far more encouraging in terms of both rounding (1.24%) and t he fact that our ‘core-core' measure continued to rise steadily. As a result, westick to the view that today's Regional Network Survey will have to disappoint heavily before Norges Bank will postpone its timing for the first rate hike. In other words, Norges Bank is likely to reiterate the message next week of a September rate hike.

Italian government bonds bounced back on Monday on the back of the comments from the new finance minister. 2Y Italian government bonds rallied some 60bp yesterday and are now back trading at 1%. However, there is still much more to go if the new Italian government can convince the market about being fiscally responsible. Furthermore, the comments reduce the imminent risk of a downgrade from, e.g. Moody's as we now have to wait and see on the actual fiscal policy.

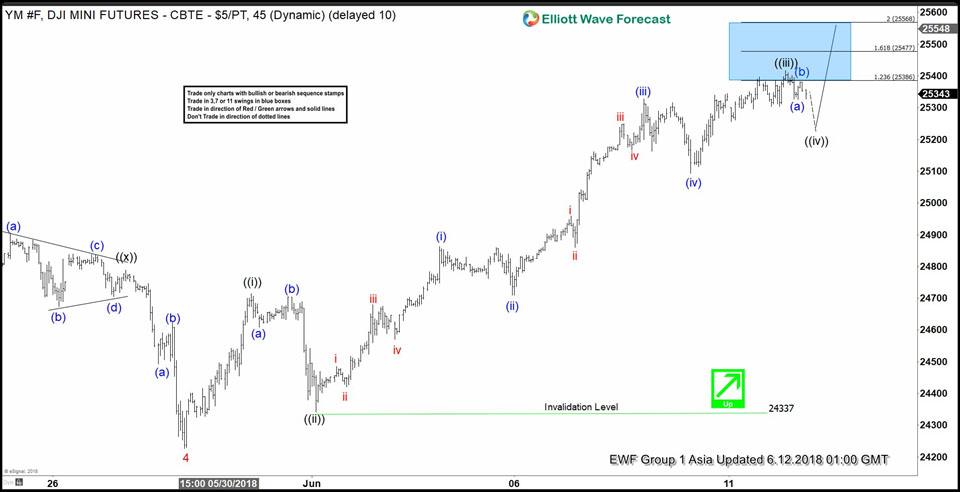

Dow Jones Nearing Completion Of 5 Waves Impulse

Dow Jones futures ticker symbol: $YM_F short-term Elliott wave view suggests that the pullback to 24227 low on 5/29/2018 ended Minor wave 4 pullback. Above from there, the rally is unfolding as impulse Elliott wave structure with extension in 3rd wave higher. As impulse, the internal of Minute degree wave ((i)), ((iii)) and ((v)) should also unfold as an impulse with 5 waves structure.

Up from 24227 low, Minute degree wave ((i)) ended in 5 waves structure at 24715. Down from there, the pullback to 24342 low ended Minute degree wave ((ii)). The rally from there shows a strong reaction to the upside which could end Minute wave ((iii)) at 25418 high. The subdivision of Minute wave ((iii)) show lesser degree impulse structure where Minutte wave (i) ended at 24863, Minutte wave (ii) ended at 24709, Minutte wave (iii) ended at 25327. Minutte wave (iv) ended at 25093 and Minutte wave (v) of ((iii)) ended at 25418 high. Near-term, Minute degree wave ((iv)) pullback is in progress in 3, 7 or 11 swings. As far as a pivot from 24337 low stays intact, expect the Index to see another push higher in Minute wave ((v)) to end 5 waves impulse structure from 5/29/2018 low. The move higher should also complete Minor degree wave 5. We don’t like selling the proposed pullback.

Dow Jones 1 Hour Elliott Wave Chart

China Expected To Follow Fed Move With Its Own Move In OMO/MLF Rates

General Trend:

- USD remains stronger leading into North Korea summit, later pared back most gains; USD/JPY an outperformer touching a 3-week high

- Trump/Kim one on one meeting lasted 41 minutes before they were joined by top aides; both leaders were positive on the meeting, Kim indicated he would work with Trump towards peace

- Trump and Kim sign agreement to acknowledge progress of the talks and pledge to keep momentum going – press

- According to Sec of State Pompeo US will offer an unpresented deal to North Korea, better than 2005 agreement

- Initial analysis agrees the meeting went well, but expectations are tapered. Now will be looking as to what each leader says to their home countries and if US will back off tariffs in order to secure China’s help on next steps with N. Korea.

- USD paired back earlier gains after the one on one summit concluded

- Chinese press speculates that PBOC will likely follow Fed move and raise OMO rates

- Aussie home loans in April continue to fall though less than expected

- Shanghai Cooperation Organization members agree to strengthen cooperation to fight terrorism and efforts to reconstruct war-torn Afghanistan (led by China and Russia, Iran and India also attended)

- White House economic advisor Kudlow suffers a minor heart attack, expected to make full recovery

Headlines/Economic Data

Japan

- Nikkei 225 opened +0.8%

- (JP) JAPAN MAY PPI (CGPI) M/M: 0.6% V 0.2%E; Y/Y: 2.7% V 2.1%E

- (JP) Japan Govt is urging power companies to reduce their plutonium stockpiles in response to American requests – Nikkei

- (JP) Japan Q2 BSI Large All Industry q/q: -2.0 v 3.3 prior; Large Manufacturing q/q: -3.2 v 2.9 prior

- (JP) Japan Fin Min Aso: Still considering personnel appointments at Ministry of Finance (MOF)

- Mitsui E&S, 7003.JP Denies press report it would stop making commercial ships at Chiba shipyard

Korea

- Kospi opened +0.2%

- (KR) Bank of Korea (BOK) Gov Lee: Need to increase policy room for economic changes; reiterates need to sustain its accommodative policy stance

- (KR) US President Trump: Summit went better than expected lot of progress made; going now for a signing - comments post North Korea summit; Follow up: When asked what was being signed, he responded you’ll find out very soon

- (KR) Sec of State Pompeo: US will offer unprecedented security deal to North Korea with assurances that will go further than 2005 agreement - press

- (KR) South Korea police launch investigation into Korea’s seventh largest crypto exchange, Coinrail, who lost KRW40B in altcoins in hack attack over the weekend - Korean press

- (KR) South Korean Deputy Fin Hyung-kwon: CPI expected to remain stable in the 1% range as a rise in oil prices is offset in part by a decline in prices of agricultural goods

China/Hong Kong

- Hang Seng opened -0.1%, Shanghai Composite 0.0%

- (CN) China mid-year liquidity is better than expected; PBOC not likely to tighten liquidity and will keep it stable - China Securities Journal

- (CN) China PBOC is very likely to follow Fed and raise is OMO rates after next Fed move - China Daily

- (CN) China Securities Regulatory Commission (CSRC): China will adhere to international, legal, and market-based principles to actively and steadily advance the testing of issuance and trading of China Depositary Receipts (CDRs) - Xinhua

- (CN) China PBoC Open Market Operation (OMO): Injects combined CNY100B in 7-day, 14-day and 28-day reverse repos v skips prior: Net injects CNY30B v drains CNY20B prior

- (CN) China PBoC sets yuan reference rate at 6.4121 v 6.4064 prior

- (CN) Sina Finance survey finds 44.8% of respondents would be interesting in investing in mutual funds linked to Chinese Depository Receipts (CDR) but may have a hard time selling to retail investors due to 3-year lock-up period – SCMP

- Foxconn Industrial Internet, 601138.CN Shares trade to daily limit for 3rd consecutive day (recent IPO)

- China Resource Cement, [-12%], 1313.HK Profit Alert: Guides H1 significantly higher y/y; to sell 450M shares to CRH

- Looking ahead: China retail sales, industrial production and fixed asset urban due tomorrow

Australia/New Zealand

- ASX 200 opened +0.1%

- VAH.AU CEO John Borghetti will not renew contract past 2020, board to start search for successor

- (NZ) New Zealand May Card Spending Retail m/m: 0.4% v 1.2%e; Total m/m: +0.5% v -0.7% prior

- (AU) Australia sells A$150M in 2% Aug 2035 indexed bonds; avg yield 0.9803%; bid to cover ratio 3.54x

- (AU) Australia May NAB Business Conditions: 15 v 21 prior; Confidence: 6 v 11 prior

- (AU) AUSTRALIA APR HOME LOANS M/M: -1.4% V -1.8%E; INVESTMENT LENDING: -0.9% V -8.8% PRIOR

- (AU) Australia Apr Owner Occupier Loan Value m/m: +0.2% v -2.0% prior

- Stanmore Coal, [+13%], SMR.AU Signs agreement with Peabody Australia to acquire MDL1371 and EPC7282 from Millennium Coal for A$30M

- Silex Systems, [-20.5%], SLX.AU Will not go ahead with plans to acquire majority stake in GE-Hitachi Global Laser Enrichment llc

- Looking ahead: Australia employment data due tomorrow

North America

- MCD Financial press citing internal memo shows restructuring plans, to record Pretax charges of $90-80M in Q2; includes layoffs to be announced by June 28th

- Fedex, FDX Raises Quarterly dividend 30% to $0.65 from $0.50 (indicated yield 0.99%); after the close

Europe

- (RU) Russia first deputy head of upper house international committee Dzhabarov: Russia and its economy have been prepared for possible new restrictions from the G7 countries, and will hardly suffer any losses - press

- (UK) Leading Tory Grieve: Have tabled compromise amendment on Brexit deal, likely to rebel if amendment is rejected

- (IT) ECB's Nowotny (Austria): Do not see a real crisis in Italy - German press

- Levels as of 01:30ET

- Hang Seng +0.4%; Shanghai Composite +0.6%; Kospi +0.0%; Nikkei225 +0.4%; ASX 200 +0.1%

- Equity Futures: S&P500 +0.0%; Nasdaq100 -0.0%, Dax +0.1%; FTSE100 -0.1%

- EUR 1.1741-1.1784; JPY 109.97-110.49; AUD 0.7585-0.7621;NZD 0.6998-0.7045

- Aug Gold -0.1% at $1,301/oz; Jul Crude Oil +0.2% at $66.25/brl; Jul Copper -0.0% at $3.25/lb

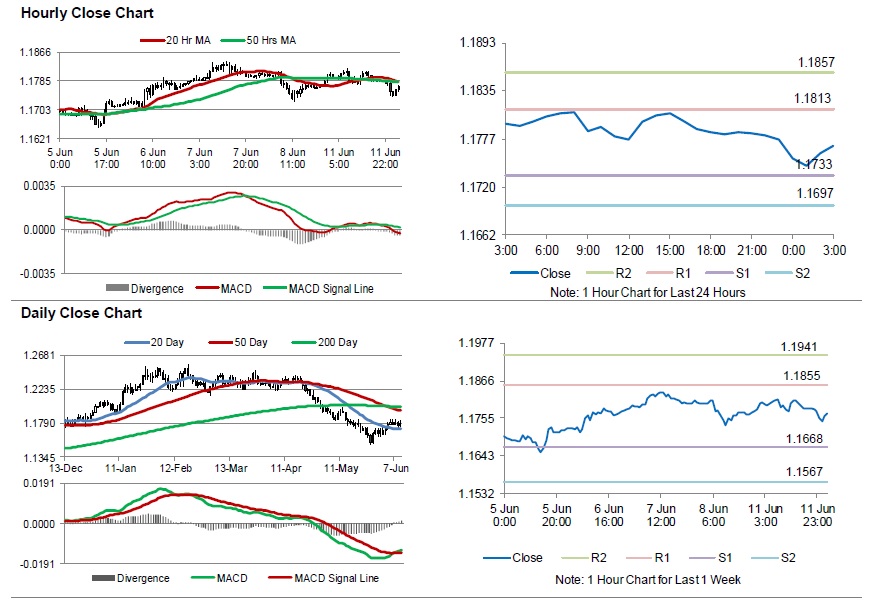

Euro Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the EUR declined 0.22% against the USD and closed at 1.1776.

Meanwhile, in Italy, Europe’s third largest economy, the working day adjusted industrial production eased 1.9% on an annual basis in April, signalling a slowdown in economic growth and compared to a revised gain of 3.5% in the prior month. Market anticipation was for industrial production to climb 3.6%.

In the Asian session, at GMT0300, the pair is trading at 1.1769, with the EUR trading 0.06% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.1733, and a fall through could take it to the next support level of 1.1697. The pair is expected to find its first resistance at 1.1813, and a rise through could take it to the next resistance level of 1.1857.

Moving ahead investors would look forward to the Eurozone’s ZEW economic sentiment index for June, slated to release in a few hours. Additionally, the US consumer price index, the NFIB small business optimism index and monthly budget statement, all for May, scheduled to release later in the day, would garner significant amount of investor attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

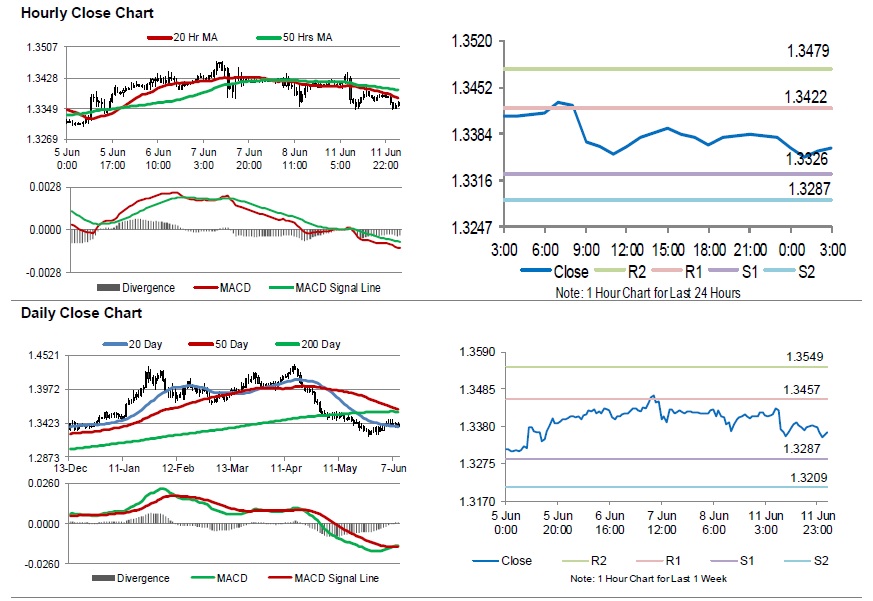

Britain’s Factory Output Unexpectedly Fell In April

For the 24 hours to 23:00 GMT, the GBP declined 0.31% against the USD and closed at 1.3379, amid a slew of disappointing economic releases in the UK.

In the economic news, UK's manufacturing production unexpectedly declined by 1.4% on a monthly basis in April, recording its largest fall since October 2012. Markets had expected manufacturing production to rise 0.3%, after recording a drop of 0.1% in the preceding month. Additionally, the nation's industrial production retreated by 0.8% on a monthly basis in April, defying market expectations for a rise of 0.1%. Industrial production had climbed 0.1% in the previous month. Moreover, trade deficit widened to £5.2 billion in April, compared to a revised deficit of £3.2 billion in the prior month. Markets had envisaged the trade deficit to narrow to £2.5 billion.

In the Asian session, at GMT0300, the pair is trading at 1.3364, with the GBP trading 0.11% lower against the USD from yesterday's close.

The pair is expected to find support at 1.3326, and a fall through could take it to the next support level of 1.3287. The pair is expected to find its first resistance at 1.3422, and a rise through could take it to the next resistance level of 1.3479.

Looking ahead, investors would closely monitor UK's ILO unemployment rate and average weekly earnings, both for April, slated to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

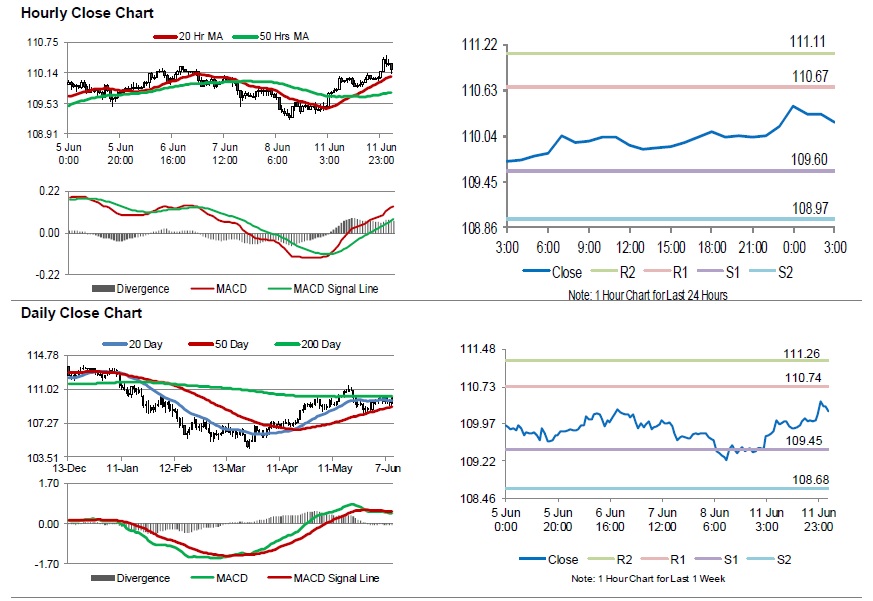

Japanese Yen Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.66% against the JPY and closed at 110.17.

On the data front, Japan’s flash machine tool orders advanced 14.9% on a yearly basis in May, following a rise 22.0% in the previous month.

In the Asian session, at GMT0300, the pair is trading at 110.22, with the USD trading 0.05% higher against the JPY from yesterday’s close.

The pair is expected to find support at 109.60, and a fall through could take it to the next support level of 108.97. The pair is expected to find its first resistance at 110.67, and a rise through could take it to the next resistance level of 111.11.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

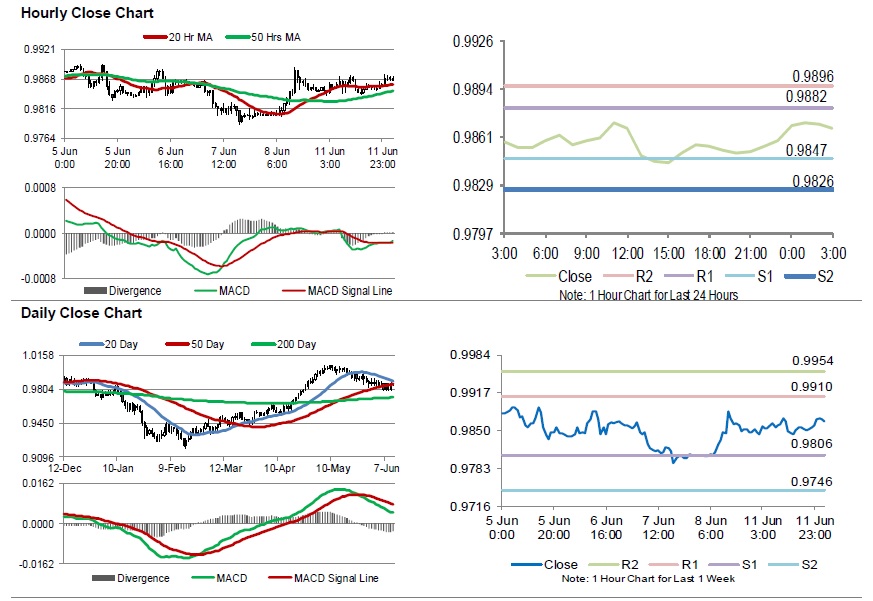

Swiss Franc Trading On A Weaker Footing In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.15% against the CHF and closed at 0.9859.

In economic news, Switzerland’s total sight deposits eased to a level of CHF576.3 billion in the week ended 08 June, from CHF576.5 billion in the previous week.

In the Asian session, at GMT0300, the pair is trading at 0.9867, with the USD trading 0.08% higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9847, and a fall through could take it to the next support level of 0.9826. The pair is expected to find its first resistance at 0.9882, and a rise through could take it to the next resistance level of 0.9896.

With no macroeconomic releases in Switzerland today, investors would look forward to global macroeconomic releases for further direction.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

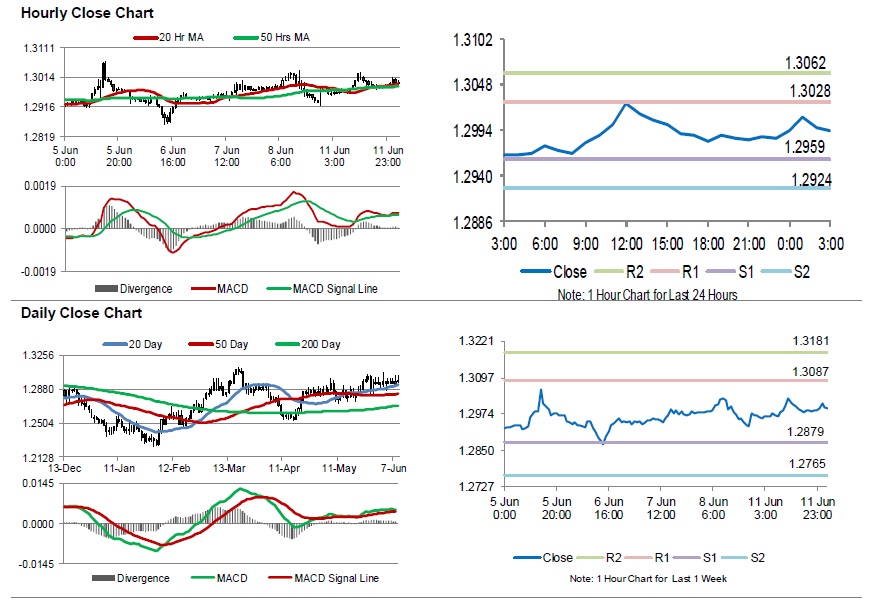

Loonie Trading Lower In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.19% against the CAD and closed at 1.2985.

In the Asian session, at GMT0300, the pair is trading at 1.2993, with the USD trading 0.06% higher against the CAD from yesterday’s close.

The pair is expected to find support at 1.2959, and a fall through could take it to the next support level of 1.2924. The pair is expected to find its first resistance at 1.3028, and a rise through could take it to the next resistance level of 1.3062.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

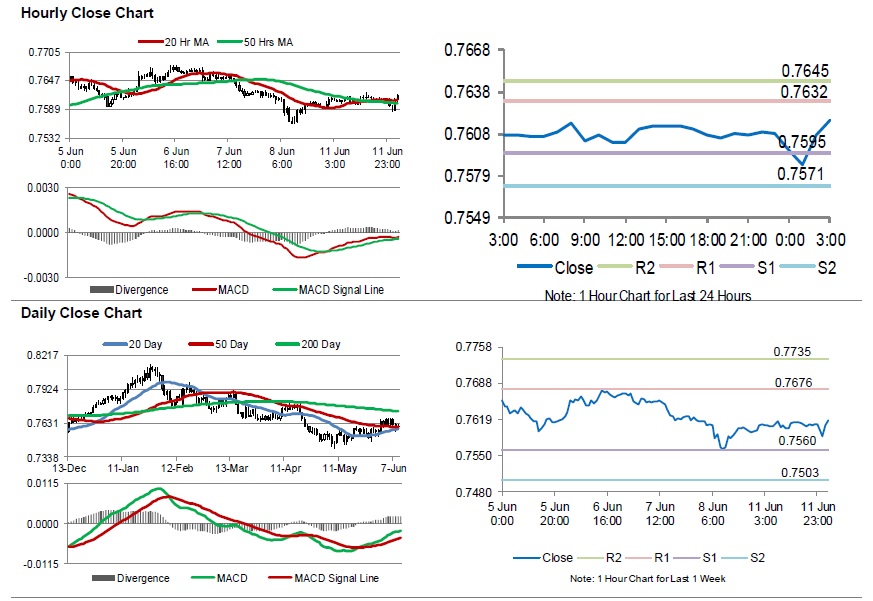

Australia’s NAB Business Confidence Eased In May

For the 24 hours to 23:00 GMT, the AUD slightly declined against the USD and closed at 0.7609.

LME Copper prices declined 0.54% or $39.0/MT to $ 7223.5/MT. Aluminium prices rose 0.55% or $12.5/MT to $2300.00/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7618, with the AUD trading 0.12% higher against the USD from yesterday's close.

Overnight data showed that Australia's NAB business confidence index registered a drop to a level of 6.0 in May, compared to a revised reading of 11.0 in the prior month. Additionally, the nation's NAB business conditions index eased to 15.0 in May, compared to a reading of 21.0 in the previous month.

The pair is expected to find support at 0.7595, and a fall through could take it to the next support level of 0.7571. The pair is expected to find its first resistance at 0.7632, and a rise through could take it to the next resistance level of 0.7645.

Going forward, traders would await Australia's Westpac consumer confidence for June, due to be released overnight.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

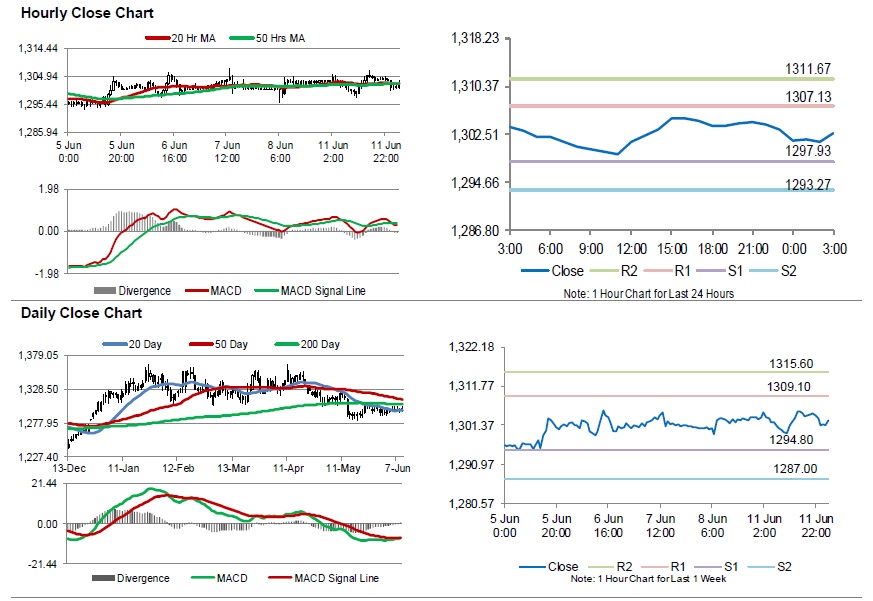

Gold: Yellow Metal Extends Its Losses In The Asian Session

For the 24 hours to 23:00 GMT, Gold declined 0.05% against the USD and closed at USD1304.00 per ounce.

In the Asian session, at GMT0300, the pair is trading at 1302.60, with gold trading 0.11% lower against the USD from yesterday’s close.

The pair is expected to find support at 1297.93, and a fall through could take it to the next support level of 1293.27. The pair is expected to find its first resistance at 1307.13, and a rise through could take it to the next resistance level of 1311.67.

The yellow metal is showing convergence with its 20 Hr and 50 Hr moving averages.