Sample Category Title

Flurry of UK Data and Brexit Developments to Move Sterling as the Week Unfolds

UK employment data for April will be made public on Tuesday at 0830 GMT, with May’s inflation numbers scheduled for release at the same time the following day. The relevant prints would constitute the last releases before the Bank of England concludes a monetary policy meeting next week, and thus might carry more weight in investors’ minds. On top of the various releases, this is a relatively important Brexit-week, something which overall brings sterling pairs to the spotlight.

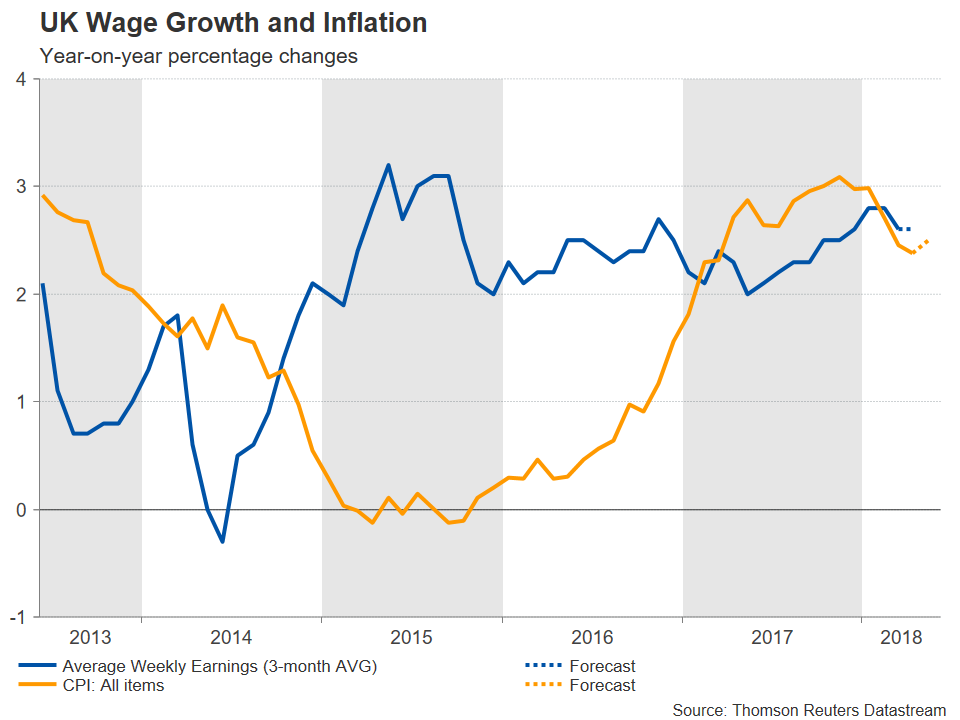

Tomorrow’s jobs data are projected to show April’s unemployment rate remaining at the multi-decade low of 4.2% for the third straight month. Meanwhile, employment is expected to rise by 110k in the three months to April, down from March’s robust figure of 197k, but still at relatively healthy levels. Most attention though, might fall on wage growth numbers, which despite being on the rise overall during the last few months, they still remain subdued given that the unemployment rate is standing at its lowest in 42 years. In this respect, the three-month average of weekly earnings is forecast to grow by 2.6% y/y, the same as in March. Excluding bonuses, average earnings are anticipated to grow by 2.9%, again the same pace as in March. In the meantime, the number of unemployment claimants during May will be released at 0830 GMT as well.

Despite less-than-stellar pay increases, if earnings growth meets expectations, April would constitute the third consecutive month wage growth would exceed price increases as gauged by the consumer price index (CPI), thus translating into a positive contribution to purchasing power for UK consumers. May’s inflation numbers due on Wednesday though, are projected to show CPI accelerating to 2.5% y/y, from April’s 2.4% which marked the third month in a row of slowing annual CPI; the BoE’s target for annual inflation stands at 2%. A CPI-beat is likely to stoke market expectations for a Bank of England rate hike sooner rather than later, consequently boosting sterling relative to other currencies. However, if the forecasted increase in price pressures is not met by (at least) an equivalent expansion in wages during May, then BoE policymakers may again need to factor in the squeeze in households’ spending power caused by inflation growing faster than wages; a factor weighing on the odds for a rate hike to be delivered soon.

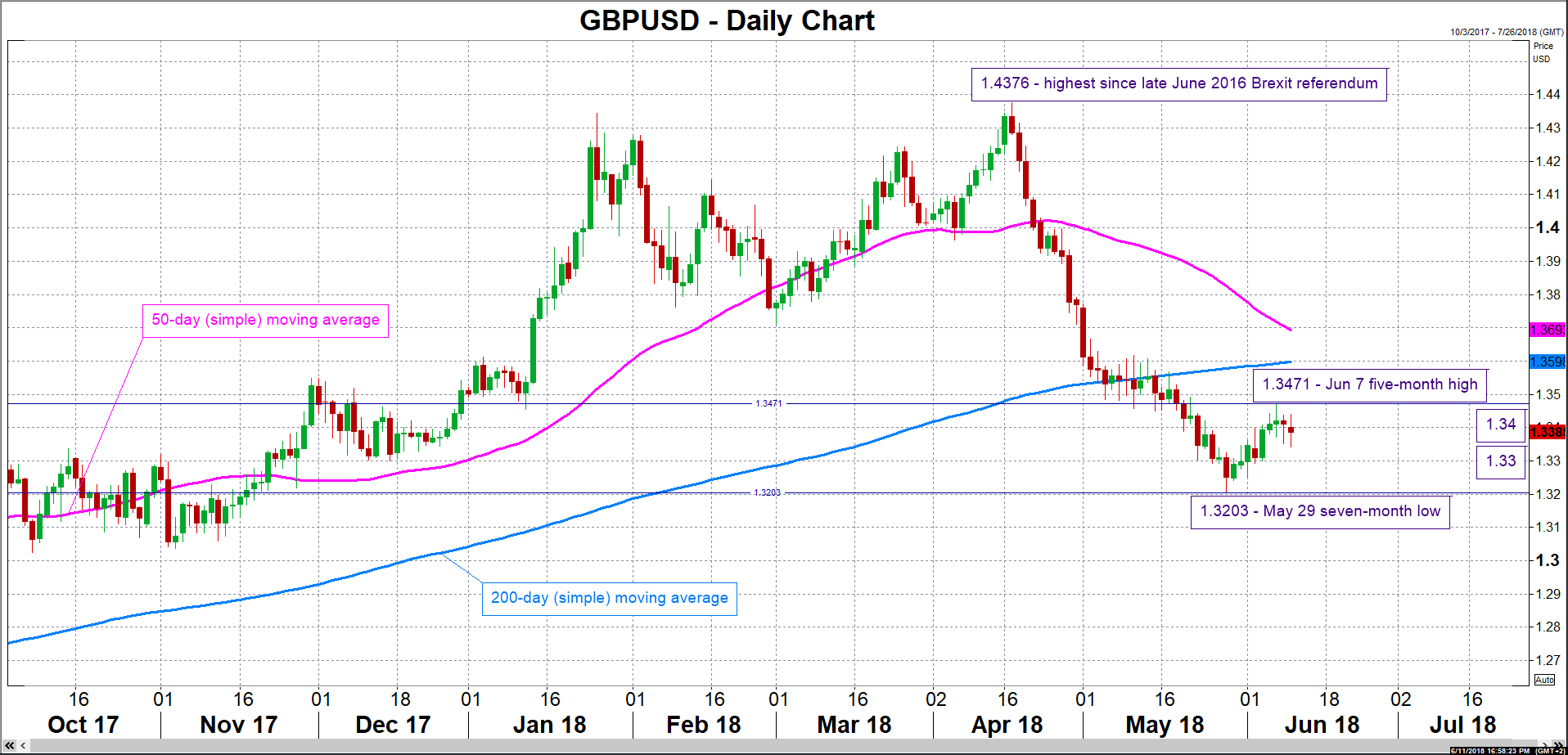

Data releases supporting a more aggressive tightening cycle by the BoE, such as upbeat earnings numbers, are anticipated to boost sterling. Focusing on GBPUSD, a first-line of resistance to price gains could come around the 1.34 round figure which failed to provide support earlier on Monday and may instead act as a barrier to the upside. Stronger bullish movement would shift the focus to Thursday’s five-month high of 1.3471, with the 1.35 handle lying not far above. Conversely, poorer-than-forecasted numbers are likely to exert downside pressure on the pair. The 1.33 handle may offer psychological support, with the attention increasingly turning to the seven-month low of 1.3203 from late May in the event of steeper losses.

Meanwhile, Brexit developments are likely to rank high on the agenda of sterling traders. Specifically, PM Theresa May will be facing votes in parliament tomorrow that could push forward a softer Brexit than envisaged by her administration. The situation is “delicate” in terms of positioning though. On the one hand, whenever a soft Brexit gains traction, sterling tends to gain. However, such an outcome is likely to be linked with a weaker May, raising fresh doubts on her leadership; political uncertainty of this sort has in the past acted to the detriment of the British currency. Investors would thus need to balance the situation based on developments and act accordingly. Still, some pound volatility could emerge around the vote.

In terms of reaction in GBPUSD, it should also be kept in mind that the US will be on the receiving end of important data during the week, including CPI and PPI numbers on Tuesday and Wednesday respectively, and retail sales on Thursday. Moreover, a Fed rate decision is on the agenda on Wednesday, while “Trump risk” might also play out in light of trade deliberations (the Trump administration said it will release a list of $50 billion of Chinese goods that will be subject to another 25% tariff for alleged intellectual property violations by June 15) and the US-North Korea summit taking place in Singapore on Tuesday.

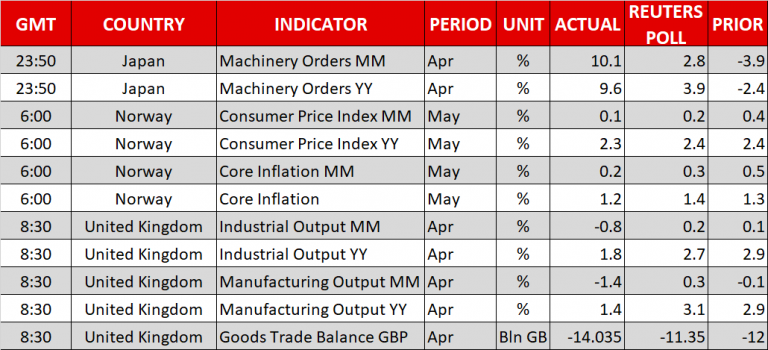

Other important UK data as the week unfolds are Thursday’s retail sales for the month of May. For the record, market participants do not expect a move by the BoE when it completes its meeting on monetary policy on June 21. In particular, UK overnight index swaps put the odds for such an outcome at slightly less than 9%; weaker than expected industrial and manufacturing output figures for April released earlier on Monday further weighed on the relevant probability. At the moment, markets have mostly priced in a 25bps rate increase during Q4.

US Inflation Data in Sight as Fed Gathers

As Fed policymakers kick off their two-day policy meeting on Tuesday, the US will also release its inflation readings for May, at 1230 GMT. Forecasts point to a further acceleration in price pressures, something that could amplify speculation for a more hawkish set of rate-path projections by policymakers and thereby, enhance the dollar’s appeal ahead of the actual rate decision.

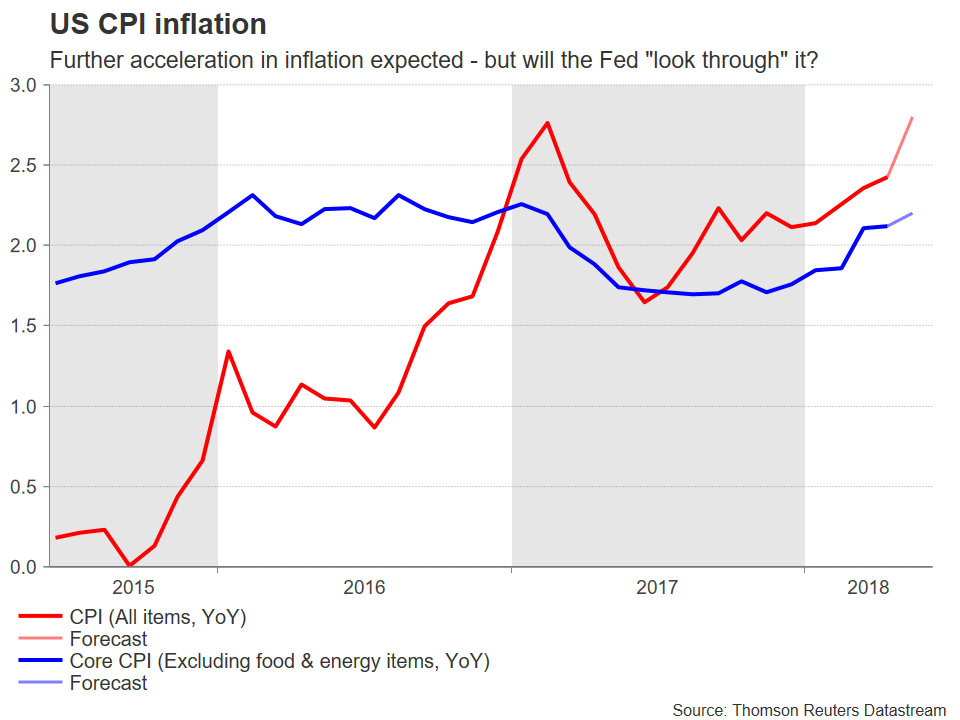

US inflation has been steadily picking up speed over past months, fueled by robust gains in the labor market, one-off effects that pulled inflation down last year filtering out of the yearly calculation now, and the latest surge in energy prices. Both the headline and core CPI inflation readings now stand above the Fed’s 2% goal, while the central bank’s preferred measure – the core PCE price index – rests just below, at 1.8%.

Forecasts suggest this trend is likely to continue in May. The headline CPI rate is projected to climb to 2.8% in yearly terms from 2.5% in April, something that would bring it to its highest point since 2012. The core figure, which excludes volatile food and energy items, is anticipated to reach 2.2% from 2.1% previously. Adding credence to these forecasts are the nation’s Markit manufacturing and services PMIs for May. The former showed that although selling price inflation eased slightly, it was still the second-fastest since June 2011, while the latter found prices charged by service firms rising at the quickest pace in three months.

Should the actual prints meet the forecasts, then the key question for dollar traders becomes whether a further speed-up in inflation will cause the Fed to adopt a more hawkish stance and hint at faster rate hikes moving forward. Recall that policymakers recently signaled they are comfortable allowing price pressures to overshoot 2% for a while, so it’s questionable whether even an upside surprise in inflation will nudge them towards further action. Especially so if such an upturn is fueled mostly by energy-related effects, which are considered transitory. Against this backdrop, a strong beat in the core rate is likely needed to amplify expectations for a more aggressive Fed.

Back in March, the individual rate projections of FOMC officials – the so-called “dots” – pointed to a total of three 25bps rate hikes being delivered this year. Crucially though, it was a very close call. If just one more member raises her/his “dot” to four hikes at the upcoming meeting, then the median “dot” would move higher to signal four hikes in total for 2018. It’s probably going to be a close call once again, and a strong set of inflation data would increase the odds of such a hawkish revision taking place, thereby enhancing the dollar’s allure ahead of the rate decision.

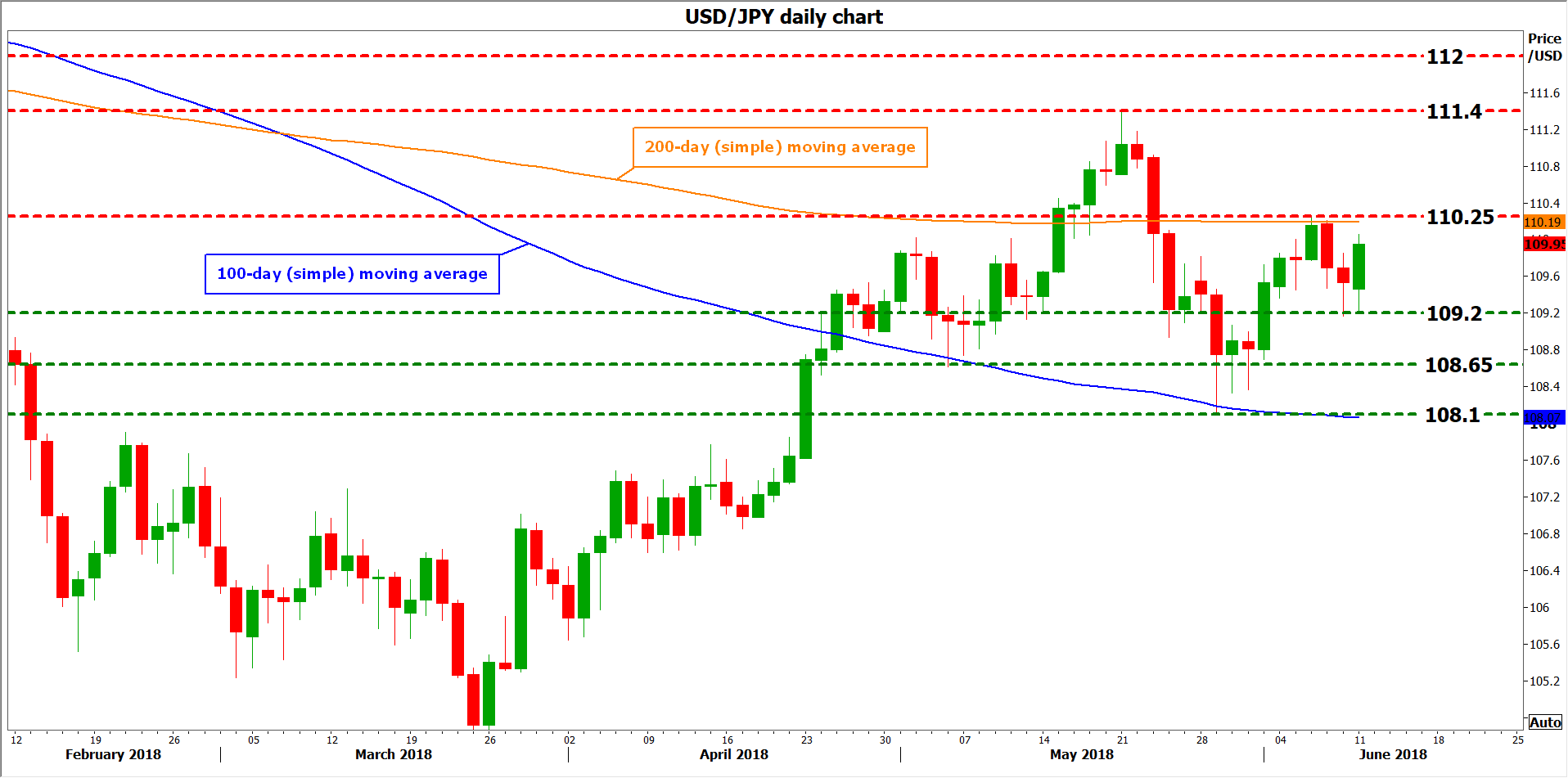

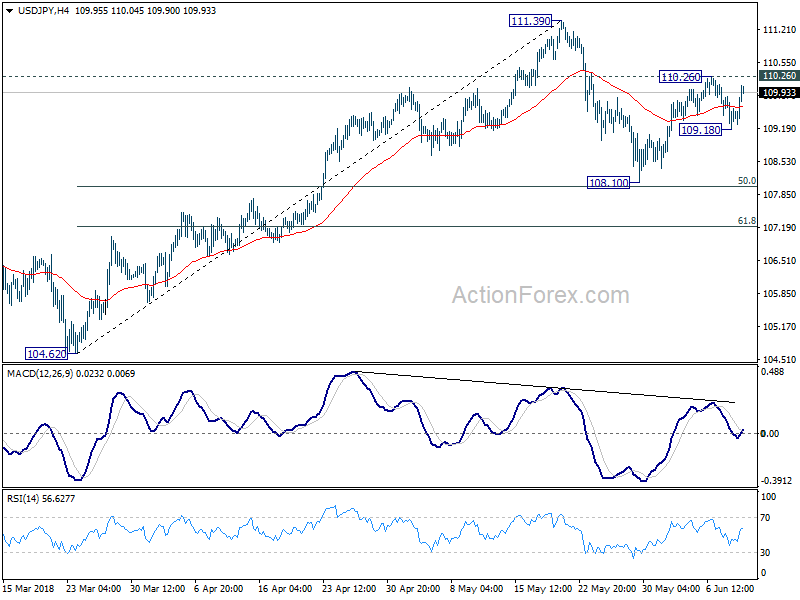

Technically, looking at dollar/yen, immediate resistance to advances could come at the 110.25 barrier, the high of June 6. The area around it also encapsulates the pair’s 200-day moving average, at 110.19. An upside break would shift attention to the 111.40 territory, which halted the pair’s climb on May 21. Even higher, the round figure of 112.00 would increasingly come into focus.

On the downside – and in case a disappointment in the CPI prints curbs speculation for a more aggressive Fed – then support may be found around 109.20, the low of June 8. Further below, declines may stall initially near the May 4 trough of 108.65, and subsequently at 108.10, the May 29 low – note that the 100-day day moving average lies just below, at 108.07.

Sunset Market Commentary

Markets:

Global core bonds lost some ground today. The tumultuous G7 meeting didn’t impact general risk sentiment (main European indices post small gains), but the car sector for example underperforms because of the boiling trade conflict. German Bunds underperform US Treasuries in a catch-up move. Italian outperformance on intra-EMU bond markets is probably also at play. Italian assets rise following this weekend’s commitment by Italian FM Tria to the euro. The Italian 10-yr yield spread vs Germany drops by 32 bps. Greek (-24 bps), Portuguese (-13 bps) and Spanish (-7 bps) spreads narrow as well. The negative bias of core bonds might also be related to this week’s event risk. We expect the ECB to announce the next phase in its normalization process (tapering in Q4 2018 with December 2018 as end date) while the Fed could indicate to step up its tightening cycle. Both firm the bottom below European/US rate markets. The German yield curve trades 3.7 bps (10-yr) to 4.5 bps (5-yr) higher. The US yield curve bear flattens with yields rising by 2.1 bps (2-yr) to 1.4 bps (30-yr).

Trading in the major euro and USD cross rates was mainly driven by market positioning ahead of the key Fed and ECB meetings later this week. At the same time, all kind of political event risk is also still in play. Risk sentiment wasn’t too bad this morning given the noise after the G7 meeting. Constructive comments from Italian Fin Min Tria added to positive sentiment on European markets and supported the euro. EUR/USD rebound north of 1.18. However, with the Fed meeting looming, there was little appetite to push EUR/USD beyond first resistance at 1.1830/40. EUR/USD soon returned to the 1.1775/1.18 area. The rise in core US and European yields and a constructive risk sentiment is also weighing on the yen as the BOJ is not expected to change course anytime soon. USD/JPY filled bids just north of 110. EUR/JPY challenged the 130 barrier. For now both cross rates failed to take out these levels a sustainable way. Even so, the yen is at risk to stay in the defensive going into the Fed and ECB policy meetings.

This week might also be key for UK markets. The House of Commons will vote on a series of amendments to the Brexit/withdrawal bill. The outcome might have important political consequences. Additionally, eco data will give an update on the health of the UK economy. UK April production and construction data and the trade balance figures all missed the consensus by quite a big margin today, with production nose-diving and the trade deficit widening. Both domestic and foreign demand weighed on UK activity. The data question the hypothesis that the disappointing Q1 performance was temporary. For now, there is little reason to preposition for an August BoE rate hike. Poor data in a context of political uncertainty were sterling negative. EUR/GBP jumped back beyond the 0.88 barrier. Cable dropped back to the mid 1.33 area, but is currently trading off the intraday low. EUR/GBP is nearing the 0.8840/50 area, the top of the ST consolidation pattern. A break above this level would be a further negative for sterling ST.

News Headlines:

After business warning that creating UK benchmarks would increase costs, Business secretary Greg Clark has announced that the UK wants to remain a full member of European standard setting bodies. This is again a slap in the face for hard Brexiteers.

The Turkish economy grew in the first quarter of this year by 2% Q/Q (vs 0.8% Q/Q consensus) following 1.7% Q/Q in the final quarter of 2017. These strong growth numbers don’t come cheap. The current account deficit has reached $5.426bn in April (up from $4.8bn in March) and expected inflation hit 10.47% for the coming twelve months. These results strengthens the concern of economists that the Turkish economy is overheating.

German retaliation to US steel tariffs coul take effect by July 1

German Chancellor's spokesman Steffen Seibert said EU is ready to take action against the US steel and aluminum tariffs, which are illegal under WTO rules. Germany's countermeasures can take effect on July 1. And it stands by resolving the standoff through international forums.

Germany Economy Minister Peter Altmaier told broadcaster Deutschlandfunk that a "win-win situation is still possible" on trade talk between the EU and the US.

However, he added that at the moment, "it seems that no solution is in sight, at least not in the short term." He pointed to the G7 summit and said "we have not made any progress in the last few days, but rather, as we saw with the rejection of the summit declaration, we have gone backwards."

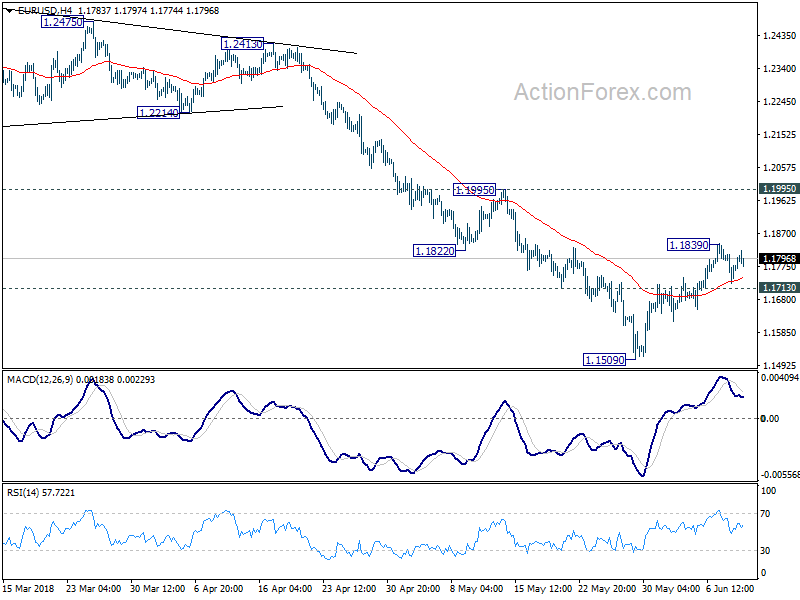

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1727; (P) 1.1769 (R1) 1.1811; More.....

EUR/USD is staying in range below 1.1839 and intraday bias remains neutral first. Rise from 1.1509 could extend higher. But still, it's seen as a correction and upside should be limited by 1.1995 resistance to bring reversal. On the downside, break of 1.1713 minor support will likely resume larger fall from 1.2555 through 1.1509 to 50% retracement of 1.0339 to 1.2555 at 1.1447.

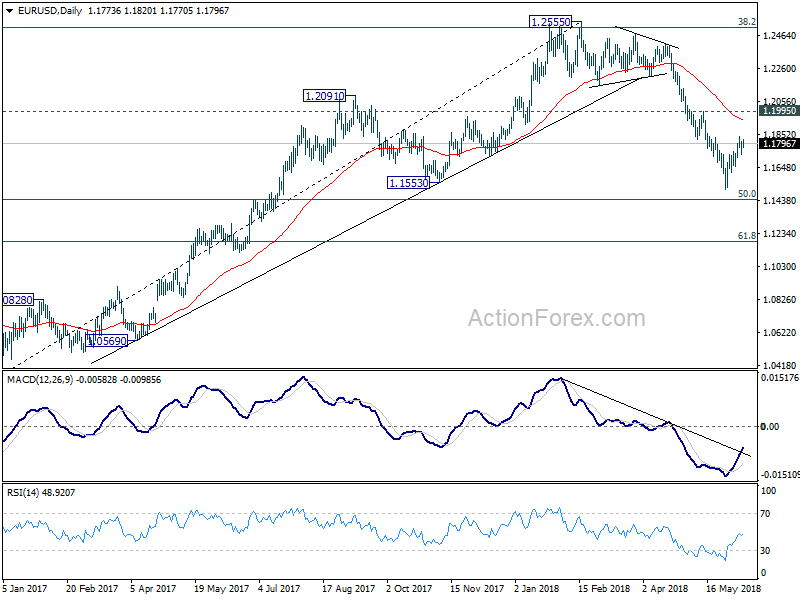

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

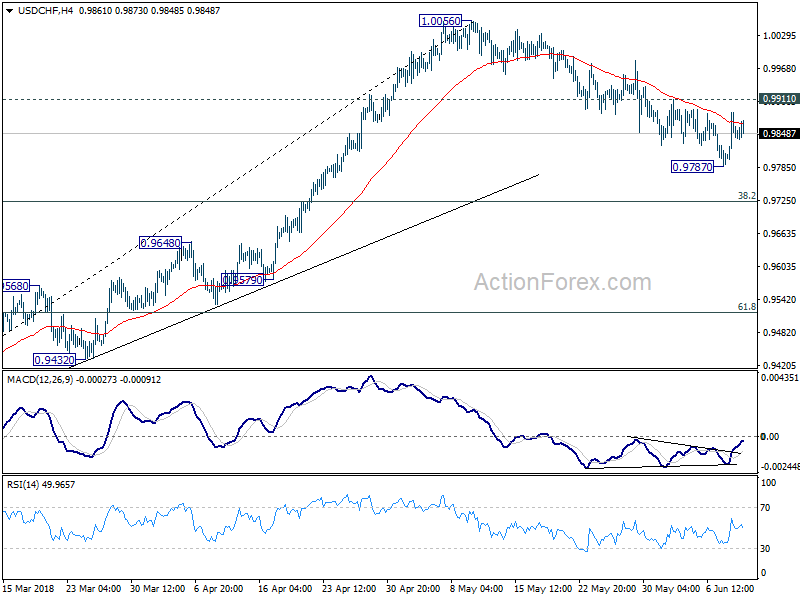

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9798; (P) 0.9843; (R1) 0.9895; More...

Intraday bias in USD/CHF stays neutral for the moment. Corrective decline from 1.0056 could still extend lower. But in that case, we'd expect strong support from 0.9724 fibonacci level to contain downside and bring rebound. On the upside, break of 0.9911 will argue that the pull back from 1.0056 has completed. In such case, intraday bias will be turned back to the upside for retesting 1.0056.

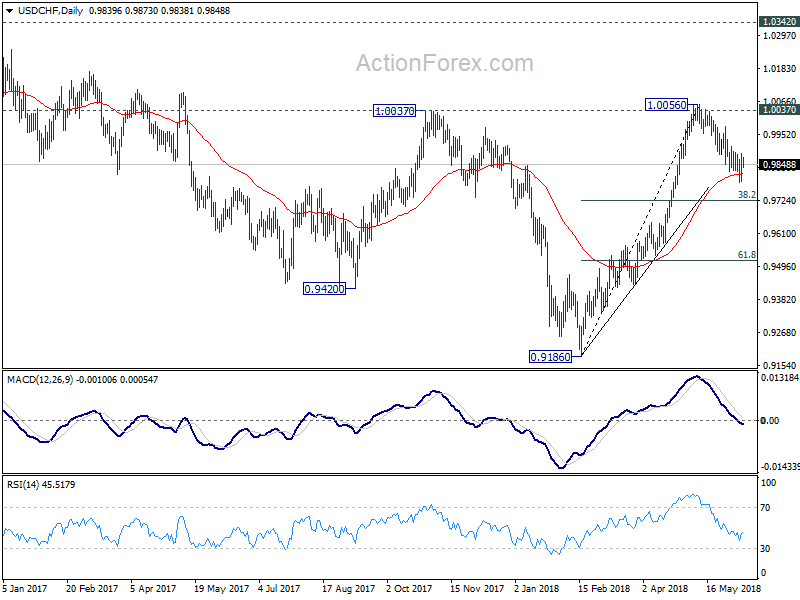

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.20; (P) 109.53; (R1) 109.87; More...

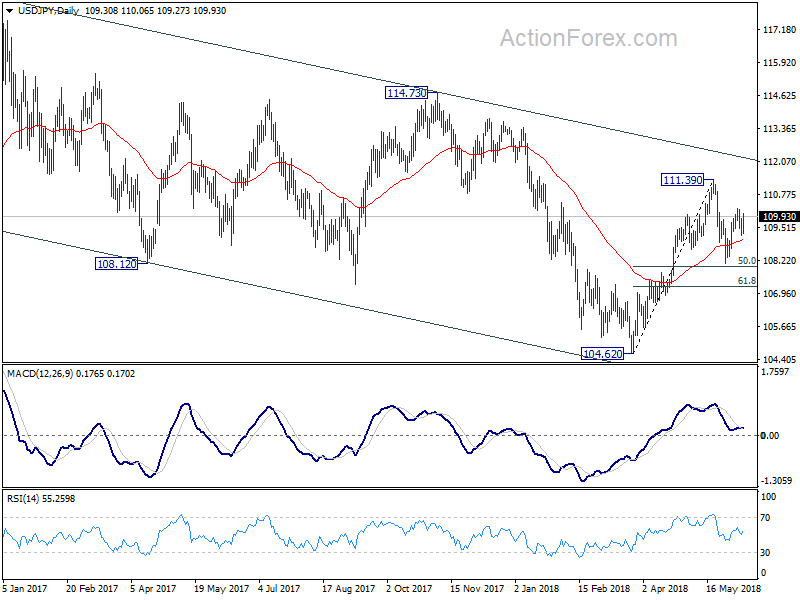

Intraday bias in USD/JPY remains neutral with focus on 110.26 minor resistance. Break there will resume the rebound from 108.10 for a test on 111.39 high. On the downside, below 109.18 will bring another fall to 108.10 or below. Overall, price actions from 111.39 are viewed as a corrective pattern which might extend. But in case of deeper fall, we'd expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

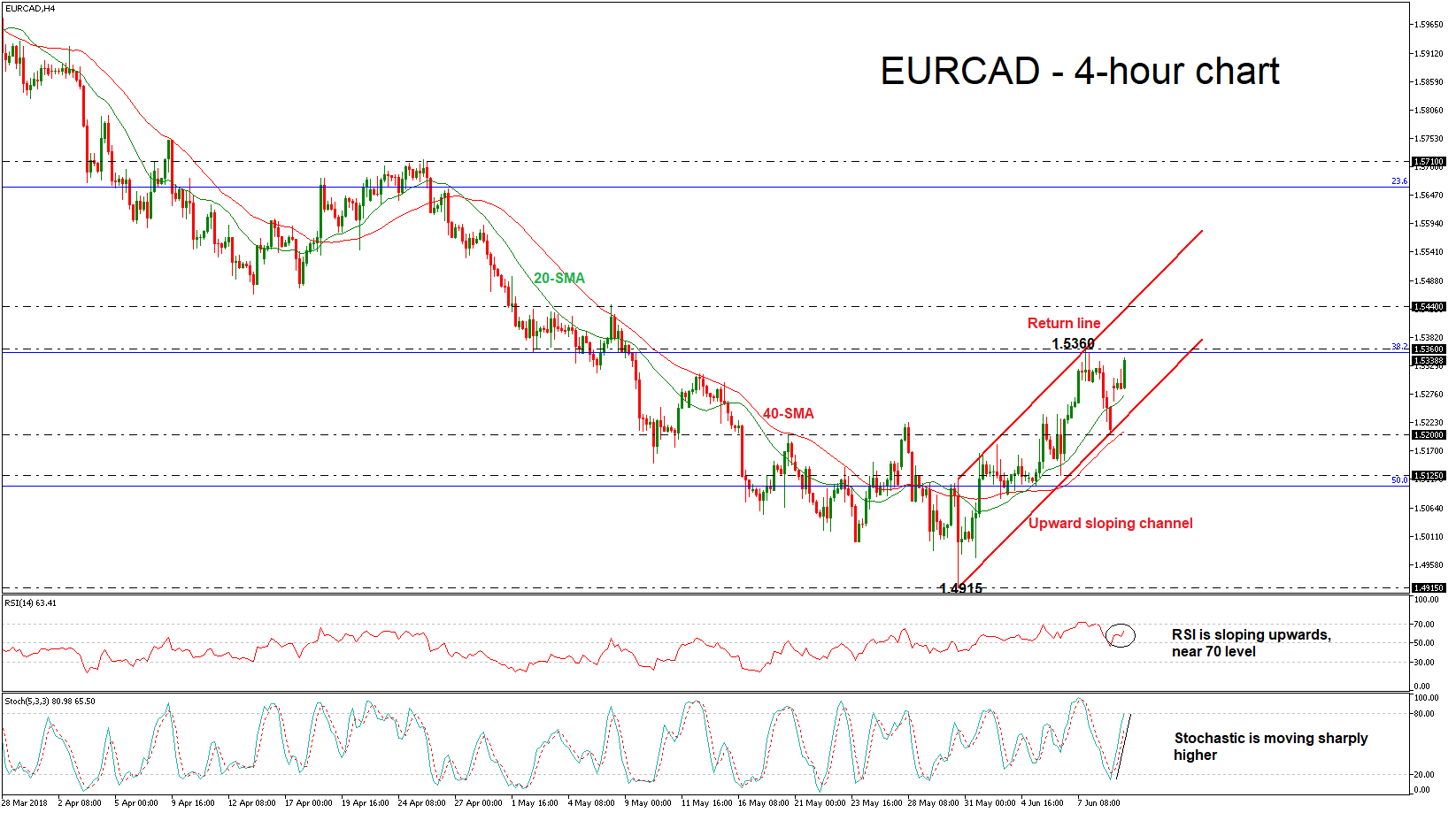

EURCAD Extends Gains in Near Term; Holds in Upward Sloping Channel

EURCAD moved higher so far on Monday and jumped above the 20- and 40-simple moving averages (SMAs) in the 4-hour chart. The pair has been consolidating within an upward sloping channel since May 30 and is in progress to turn the medium-term outlook from negative to positive.

From the technical point of view, the RSI indicator is sloping upwards in the bullish territory and is approaching the 70 level, while the %K line of the stochastic oscillator is ready to enter the overbought zone with strong momentum.

If the bulls maintain their movement, the next level to have in mind is the 38.2% Fibonacci retracement level of the upleg from 1.4050 to 1.6150, around the 1.5360 resistance barrier. If the price overcome this area, it could open the door for the 1.5440 hurdle, identified by May 8.

On the flip side, a dip below the 20-SMA could drive the pair to re-challenge the 1.5200 handle, which coincides with the 40-SMA in the near-term. If that level does not hold and the price breaks it to the downside, it would shift the focus south again and hit the 1.5125 support level.

Overall, EURCAD is extending its gains and is on the way to post a bullish correction in the short-term timeframe.

Dollar Enjoys Gains as Attention Shifts to Geopolitics and Monetary Policy

Here are the latest developments in global markets:

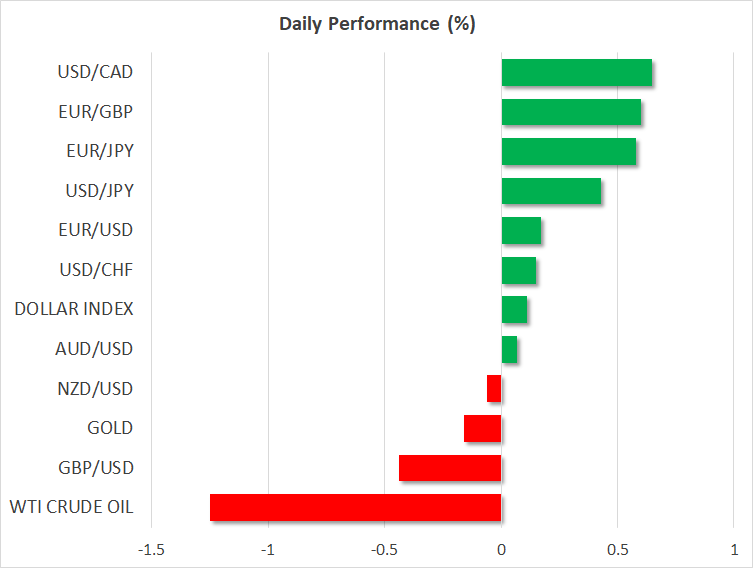

FOREX: The US dollar managed to cross slightly above the 110.00 key level against the Japanese yen on Monday to reach an intraday high of 110.06 ahead of a historic summit between the US President and the North Korean leader on Tuesday and the conclusion of the two-day FOMC policy meeting on Wednesday. The US dollar index which measures the greenback’s performance against a basket of six major currencies moved slightly higher by 0.07% today. Euro/dollar edged up by 0.21%, posting gains after Italy’s new finance minister pledged to keep the euro currency. Pound/dollar slid by 0.34% following the release of downbeat manufacturing and industrial production readings. Manufacturing production decreased by 1.4% m/m from a 0.1% fall in the previous month, posting the fastest drop since March 2013, while industrial production declined by 0.8% versus a contraction of 0.1% seen previously. Euro/pound jumped to 0.8813 (+0.42%). Turning to antipodean currencies, aussie/dollar climbed marginally by 0.09% to 0.7607 as Australian markets were shut for a holiday (Queen’s Birthday), while kiwi/dollar stood lower at 0.7025 (-0.10%). Dollar/loonie moved higher by 0.47% to 1.2983 as the G7 meeting concluded with renewed trade threats.

STOCKS: European equities were a sea of green on Monday although the G7 summit failed to break the trade deadlock over the weekend. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.51% and 0.48% respectively at 1100 GMT. The German DAX 30 edged up by 0.46%, the French CAC 40 climbed by 0.23%, UK’s FTSE 100 moved up by 0.91% and the Spanish IBEX 35 gained 0.77%. The Italian FTSE MIB was the best performer, surging by 2.17% after Italy’s new finance minister showed commitment to remain in the single currency. Futures tracking US stock indices were all in the green after two consecutive bullish days, pointing to a positive open.

COMMODITIES: Oil prices extended losses after Friday’s Baker Hughes readings showed a rise in the number of active US oil drillings, while news announcing a pick up in Russian production on Monday pressured prices even further. The market is also pricing in that OPEC would publicize an output hike at its policy meeting on June 22-23 amid rising US production. West Texas Intermediate (WTI) crude and Brent were developing lower at $64.92 per barrel (-1.25%) and $75.64 per barrel (-1.07%) respectively. In precious metals, gold was in the negative ground, trading lower at $1,295.20 per ounce (- 0.21%).

Day ahead: Focus switches to Geopolitics and monetary policy

Monday’s economic calendar will be relatively quiet in terms of major data releases in the remainder of the day, giving some time to investors to prepare their positions ahead of high-spot events later this week.

Early in the Asian session, traders will see the release of electronic card retail sales out of New Zealand at 2245 GMT, while at 2350 GMT Japan will issue PPI readings.

However, since the above data have a small capacity to spread volatility to the markets, the focus will turn to Singapore where the US President, Donald Trump, will be holding a historic summit with the North Korean leader, Kim Jong Un at 1700 GMT, a proposal made unexpectedly by the latter but initially cancelled by Trump. The two leaders, who will finally meet in person after exchanging war of words in 2017, will push efforts to find a common ground on North Korea’s future nuclear program after Kim showed the willingness to give up its nuclear weapons. Should the discussion prove fruitful, US trade restrictions could turn softer against the isolated peninsula, while the Korean War could also take a formal shape. However, if the meeting fails to deliver progress, the US could take a stricter stance against North Korea, bringing a fresh wave of uncertainty to the markets. Note that this would be the first meeting between a sitting US President and a North Korean leader.

Meanwhile in the US, the Federal Open Market Committee is scheduled to start its two-day policy meeting on Tuesday, with analysts widely expecting policymakers to hike interest rates for the second time this year and remain hawkish on the face of the US improving economic performance. The European Central Bank and the Bank of Japan will also decide on interest rates this week, on Thursday and Friday respectively, however, no rate rises are anticipated to be approved in these cases. Yet, the ECB policy meeting could attract a greater attention as the central bank could give direction on its QE program that expires in December. Particularly analysts wait to see whether policymakers will end or expand their bond-buying program after its expiration day.

Trade headlines would remain under the spotlight as the G7 meeting in Quebec Canada during the weekend was unable to unite the US with its closest allies on the trade front, with investors now looking for further clues to see whether rising trade tensions could unleash a global trade war.

Canadian Dollar Slips to 1.30, G-7 Summit Ends in Disarray

The Canadian dollar has started the dollar with losses. On Monday, USD/CAD is trading at 1.3004, up 0.62% on the day. In economic news, it’s a very quiet start to the week. There are no Canadian indicators and the sole US event is the 10-year bond yield. On Tuesday, the US releases CPI reports.

The markets were braced for a bumpy meeting between the Group of Seven leaders on Friday, but the sharp disagreements between President Trump and the other six members were far worse than expected. Trump openly clashed with the other leaders over his recent tariffs against the European Union and Canada and pulled back his endorsement of the traditional post-summit statement put out by the other members. The undiplomatic Trump also tweeted that Canadian Prime Minister Trudeau, who hosted the summit, was “dishonest and weak”. Canada and the EU are furious over recent US tariffs, especially because of Trump pushed them through on the basis of ‘national security’. The glaring cracks in G-7 unity could cast a long shadow on trade relations between the U.S and the “G-6”, with business confidence and capital spending at risk if the tariff spat continues.

All eyes were on last week’s election in Ontario, the most populous province in Canada. Although there was a sharp shift to the right, the Canadian dollar yawned and continued to hug the symbolic 1.30 level. The Conservatives won a decisive majority of seats, as the business sector sighed in relief. With the Conservatives and the left-wing NDP running neck-and-neck in the polls, there had been concerns that the NDP could win the election, or at least deny the Conservatives a majority. The new premier, Doug Ford, is a former businessman and investors can expect the new government to have a pro-business platform. This should translate into gains for Canadian stock markets as well as the Canadian dollar.