Sample Category Title

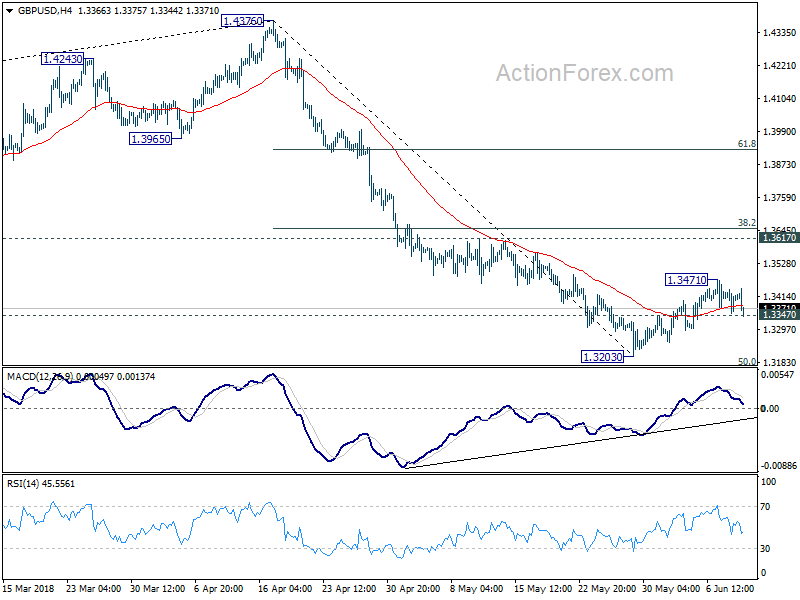

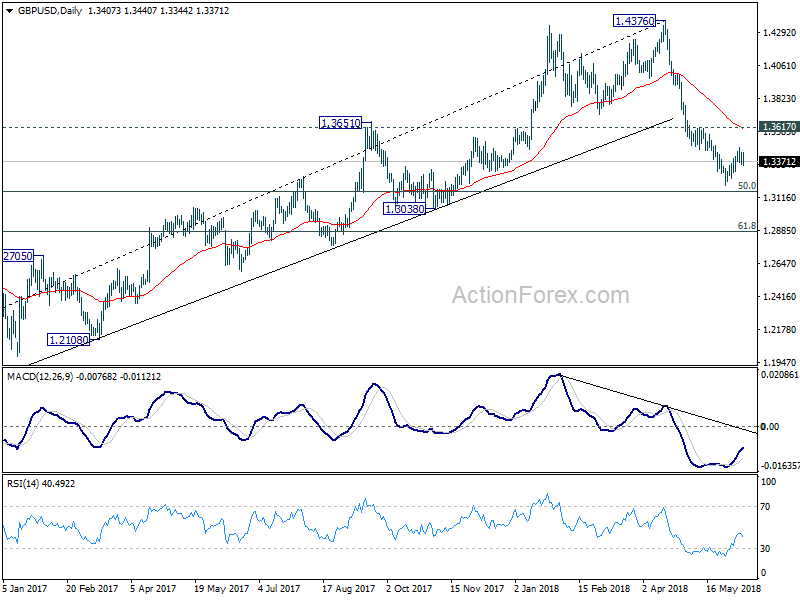

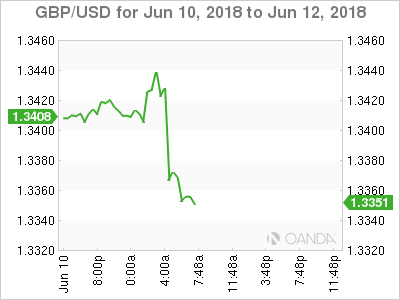

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3364; (P) 1.3402; (R1) 1.3448; More...

GBP/USD dips notably today but it's staying above 1.3347 minor support so far. Intraday bias remains neutral first. On the downside, firm break of 1.3347 will confirm completion of the corrective rise from 1.3203. Intraday bias would be turn to the downside. And fall from 1.4376 should resume through 1.3203 to 50% retracement of 1.1946 to 1.4376 at 1.3161 first, and 61.8% retracement at 1.2875 next. In case of another rally, upside should be limited by 1.3617 resistance to bring reversal.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3617 resistance holds, even in case of strong rebound.

Sterling Weakens after Poor Economic Data, More to Care than Kim-Trump Summit for Traders

While the spats between US and G6 countries made a lot of headlines, they're not much bothered by the market-smart investors who know what are important. The summit between North Korean Leader Kim Jong-un and US president Donald Trump is currently in the spotlight. But it will likely fade into darkness quickly too. There are a number of important events this week. And Sterling is already hit but a batch of weaker than expected data. Euro, on the other hand, is the strongest one as risk of Italian existing Eurozone receded. But there is no clear follow through buy, not even in EUR/GBP, as ECB risks loom. Dollar is also mixed ahead of FOMC rate decision, economic projections and press conference.

Technically, 1.3347 in GBP/USD will be a focus in the US session. The pair breached this level but recovered quickly. Firm break of 1.3347 should confirm completion of the corrective rise from 1.3203. And by then, we could see downside accelerate through 1.3203 low.0.8844 in EUR/GBP is another level to watch as firm break there will finally confirm resumption of near term rebound from 0.8620.

Sterling dips as trade balance and production missed, more tests ahead

Sterling trades lower again Euro and Dollar today after a string of weaker than expected data. Visible trade deficit widened to GBP -14.0B in April, from GBP -12.0B, missed expectation of GBP -11.5B. Industrial production at -0.8% mom 1.8% yoy in April , versus expectation of 0.1% mom 2.7yoy and prior 0.1% mom 2.9% yoy. Manufacturing production at -1.4% mom 1.4% yoy, versus expectation of 0.3% mom 2.9% yoy, and prior -0.1% mom 2.9% yoy. Construction output rose 0.5% mom in April versus expectation of 2.4% mom and prior -2.3% mom.

NIESR said UK GDP is estimated to have grown 0.2% in the three months ending May, following 0.1% grow in the three months ending April. Amit Kara, Head of UK macroeconomic forecasting, said, growth slowed "materially" since the start of the year and remains weak. In additional to severe weather in March, latest data also showed slowdown in manufacturing, driven by both domestic and external conditions. Accommodative monetary policy would help to strength the economy ahead. But risks are "weighed to the downside". Brexit is the most important risk but there were also "escalation of tensions in international trade and a potential flare-up in uncertainty in the Euro Area because of political developments in Italy."

The real tests will lie in tomorrow's employment data and Wednesday's inflation data. Average weekly earnings including bonus are expected to grow 2.6% 3moy in April. Weekly earnings excluding bonus are expected to growth 2.9% 3moy. Both are unchanged from March's readings. CPI is expected to rise back to 2.5% yoy in May, up from 2.4% yoy. CPI core is expected to be unchanged at 2.1% yoy. For now, a BoE August hike is still on the table. But after the data, we'll pretty know if there is still such a chance. Retail sales will be featured later in the week but that's less important.

FOMC and ECB meeting the highlight of the week

There are more things to care in the week than the Kim-Trump summit. A rate hike of 25 bps at the upcoming FOMC meeting this week is a done deal as the market has for months priced in over 90% chance of its occurrence. Recent macroeconomic developments indicate such rate hike is totally justified. The focuses are on the forward guidance on the future path of normalization and the updated economic projections. We expect the members to upgrade the economic growth and inflation assessment. It is also prudent to make some changed on the forward guidance, to illustrate that the rate- hike process since the end of 2015 has taken the policy more closely to "neutral" than years ago. More in FOMC Preview – Fed's Rate Hike A Done Deal, Focus Turned to Forward Guidance.

The recovery in euro since late-May gathered momentum last week after ECB Chief Economist and executive board member Peter Praet signaled the central bank would discuss QE tapering at this week's meeting. We are not surprised by this as it is appropriate for the members to communicate with the market its next week after the current asset purchases end in September. We believe July would be a better time for the announcement as the members could assess more indicators before making a decision. This is particularly important at the current period of economic growth slowdown, rising protectionism from the US and ongoing political uncertainty in the peripheral Eurozone. More in ECB Preview – Members to Discuss QE Tapering This Week, Attention Moves to Rate Hike Path and Forward Guidance.

Mexican Guajardo to engage strongly in July on NAFTA

Mexican Economy Minister Ildefonso Guajardo said Mexico, Canada and the US will be "engaging strongly" later in July to work on a NAFTA agreement that 's "feasible, workable and benefits the three nations involved."

He added that "the only way we will find that solution is if countries involved have sufficient flexibility to be able to find that narrow strip where we have to land."

And he warned that "an agreement that does not give us certainty, does not give us rules that have to be obeyed and mechanisms to settle disputes will not be of help for the business community."

New Zealand Parker: None of us can beat globalization

New Zealand Trade Minister David Parker urged the world to stand up to defend rules-based trade system. And he added that "none of us can beat globalization". He noted that "what's happening in the world worries me. But the world is already developing alternatives like CPTPP".

The Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), also known as TPP-11, was an advanced version of the Trans-Pacific Partnership (TPP) that was signed in March. The US was originally in the TPP but Trump pulled out of it immediately after taking office.

Malaysian PM Mahathir renews push for EAEC as US become isolationist again

Malaysian Prime Minister Mahathir Mohamad said the Trans Pacific Partnership needs to be renegotiated because "smaller countries would have the chance to compete because they would be given certain handicaps." He emphasized "small countries cannot compete on the same terms as bigger countries."

Mahathir, aged 92 and became Prime Minister for the second time last month, would also like to have a second push to his favored broad trade pact such as the East Asian Economic Caucus (EAEC), which he proposed during his previous administration. He noted that "yes, I am still in favor of EAEC. In the past, of course, we were not able to do this due to the objections of America, but now America seems to become isolationist again so it is not in a position to demand that we cannot form EAEC."

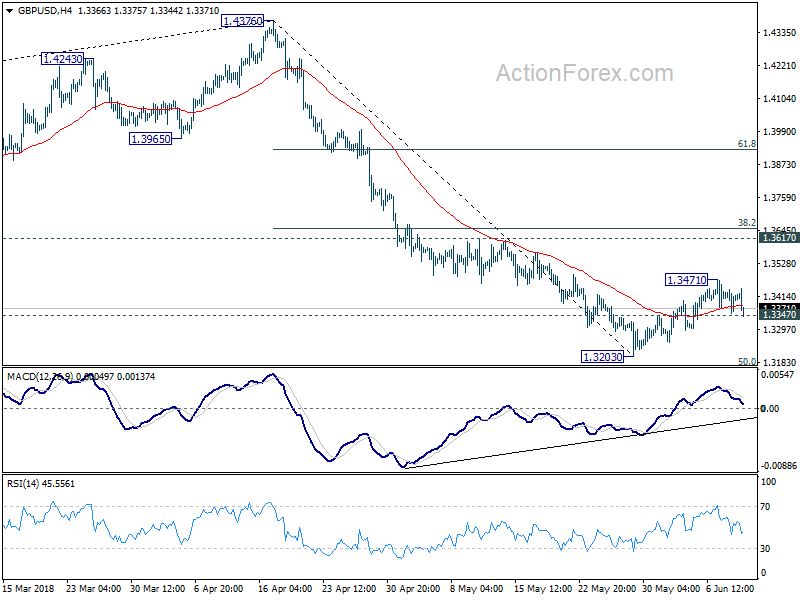

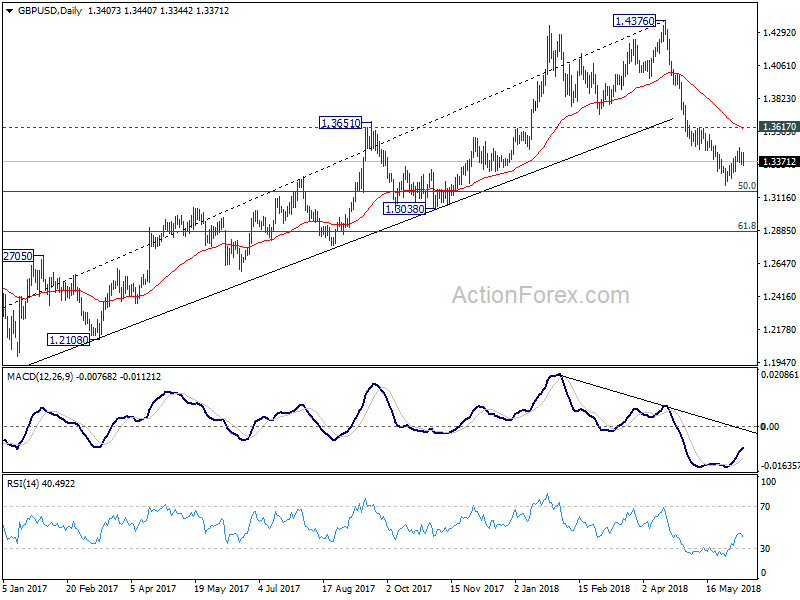

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3364; (P) 1.3402; (R1) 1.3448; More...

GBP/USD dips notably today but it's staying above 1.3347 minor support so far. Intraday bias remains neutral first. On the downside, firm break of 1.3347 will confirm completion of the corrective rise from 1.3203. Intraday bias would be turn to the downside. And fall from 1.4376 should resume through 1.3203 to 50% retracement of 1.1946 to 1.4376 at 1.3161 first, and 61.8% retracement at 1.2875 next. In case of another rally, upside should be limited by 1.3617 resistance to bring reversal.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3617 resistance holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Manufacturing Activity Q1 | 0.60% | 2.80% | 2.60% | |

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y May | 3.20% | 3.30% | 3.30% | 3.20% |

| 23:50 | JPY | Machine Orders M/M Apr | 10.10% | 2.50% | -3.90% | |

| 6:00 | JPY | Machine Tool Orders Y/Y May P | 14.90% | 22.00% | ||

| 8:30 | GBP | Visible Trade Balance (GBP) Apr | -14.0B | -11.5B | -12.3B | -12.0B |

| 8:30 | GBP | Industrial Production M/M Apr | -0.80% | 0.10% | 0.10% | |

| 8:30 | GBP | Industrial Production Y/Y Apr | 1.80% | 2.70% | 2.90% | |

| 8:30 | GBP | Manufacturing Production M/M Apr | -1.40% | 0.30% | -0.10% | |

| 8:30 | GBP | Manufacturing Production Y/Y Apr | 1.40% | 2.90% | 2.90% | |

| 8:30 | GBP | Construction Output M/M Apr | 0.50% | 2.40% | -2.30% | |

| 11:00 | GBP | NIESR GDP Estimate May | 0.20% | 0.10% |

Dismal UK Data As Manufacturing Production Registers Its Largest Monthly Decline In Over 5 Years

Notes/Observations

- UK Manufacturing data misses expectations to register its largest monthly decline in over 5 years; trade deficit also larger than consensus

- Norway CPI lags forecasts; keeps finger on trigger for Norges on its 1st potential rate hike until after summer

- Kim Jong Un and Trump will discuss peace, denuclearization; look to manage expectations

Asia:

- China May CPI M/M: -0.2% v -0.2% prior; Y/Y: 1.8% v 1.8%e; PPI Y/Y: 4.1% v 3.9%e

Europe:

- Italy Econ Min Tria gives markets reassurance that govt had no intention of leaving the Euro

- Swiss voters reject Vollgeld Referendum (as expected). Reject motion to abolish traditional bank lending and allow only money to be created by the central bank. SNB responded to vote outcome: A "yes" vote would have made its work “considerably more difficult”.

- UK PM May expected to urge potential Tory rebels to get behind the party ahead of crucial votes on the EU Withdraw Bill. Wants to overturn a series of amendments made by the House of Lords but faces defeat if Conservative Remainders side with Labour

- PM May to hold Brexit talks with ministers at her country residence following the June EU summit and would finalize Brexit policy paper post June EU summit

- German Chancellor Merkel: EU has prepared counter measures against the US tariffs on steel and aluminum; We would not allow us being ripped off over and over again, we would also act then

Americas:

- G7 Official Communique (with support from all but the US): We acknowledge free, fair and mutually beneficial trade is key engine for growth and jobs; We strive to reduce tariffs

Economic Data:

- (NO) Norway May CPI M/M: 0.1% v 0.3%e; Y/Y: 2.3% v 2.5%e

- (NO) Norway May CPI Underlying M/M: 0.2% v 0.3%e; Y/Y: 1.2% v 1.4%e

- (NO) Norway May PPI (including Oil) M/M: 1.2% v 3.3% prior; Y/Y: 14.4% v 12.2% prior

- (DK) Denmark Apr Current Account (DKK): 1.4B v 11.7B prior; Trade Balance: 6.0B v 4.6B prior

- (DK) Denmark May CPI M/M: 0.2% v 0.2%e; Y/Y: 1.1% v 1.1%e

- (DK) Denmark May CPI EU Harmonized M/M: 0.2% v 0.3%e; Y/Y: 1.0% v 1.1%e

- (JP) Japan May Preliminary Machine Tool Orders Y/Y: 14.9% v 22.0% prior

- (FR) Bank of France (Industrial) Sentiment: 100 v 102e

- (SE) Sweden Jun SEB Housing Price Indicator: 7 v 11 prior

- (CZ) Czech May CPI M/M: 0.5% v 0.3%e; Y/Y: 2.2% v 2.0%e

- (TR) Turkey Apr Current Account Balance: -$5.4B v -$5.1Be

- (TR) Turkey Q1 GDP Q/Q: 2.0% v 0.8%e; Y/Y: 7.4% v 7.0%e

- (IT) Italy Apr Industrial Production M/M: -1.2% v -0.7%e; Y/Y: +6.7% v -1.1% prior; Industrial Production WDA Y/Y: 1.9% v 3.6%e

- (CH) SNB Total Sight Deposits for Week Ended Jun 8th (CHF): 576.3B v 576.5B prior

- (UK) Apr Visible Trade Balance: -£14.0B v -£11.4Be; Overall Trade Balance: -£5.3B v -£2.5Be; Trade Balance Non-EU: -£5.4B v -£3.2Be

- (UK) Apr Industrial Production M/M: -0.8% v 0.1%e; Y/Y: 1.8% v 2.7%e

- (UK) Apr Manufacturing Production M/M: -1.4% v +0.3%e (biggest monthly decline in 5 ½ years); Y/Y: 1.4% v 3.1%e

- (UK) Apr Construction Output M/M: 0.5% v 2.2%e; Y/Y: -3.3% v -1.4%e

Fixed Income Issuance:

- None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 +0.6% at 3,465, FTSE +0.8% at 7,738, DAX +0.5% at 12,834, CAC-40 +0.2% at 5,460; IBEX-35 +0.6% at 9,806, FTSE MIB +2.0% at 21,784, SMI +0.9% at 8,590 , S&P 500 Futures +0.1%]

- Market Focal Points/Key Themes: European indexes opened broadly higher and maintained trend as the session progressed; financials supported following assurances from Italy not interested in leaving Euro; Italy best performer; Portugal underperformer, dragged down by Altri correction; G7 controversy leaves markets largely unaffected; materials and energy sectors under pressure; risk sentiment supported on the back of less geopolitical concerns; focus on upcoming North Korea talks; Colombia closed for holiday; earnings expected during the US session include Optical Cable and RF Industries

Equities

- Consumer discretionary: BCA Marketplace BCA.UK +8.8% (rejects takeover offer), CD Projekt Red 7CD.DE -7.4% (title release), Ferguson FERG.UK +0.5% (share consolidation)

- Financials: Bollore BOL.FR -1.2% (analyst action), Intesa Sanpaolo ISP.IT +4.3% (talks with Blackrock)

- Industrials: Rolls Royce RR.UK -0.8% (Package B engines issue)

- Telecom: Eutelsate TEL.UK +2.1% (analyst action), Inmarsat ISAT.UK +12.9% (rejects takeover offer), SES SESG.FR +1% (analyst action)

Speakers

- Italy PM Conte: NATO and EU needed to cooperate more on immigration and security. Russia's role was key in regional crisis

- Spain's bad bank (SAREB) said to have placed €30B of planned asset sales on hold until it receives fresh approval from the new govt

- ESM's Regling stated that the Portuguese banking sector was now more resilient. Govt needed to keep up the reform momentum

Currencies

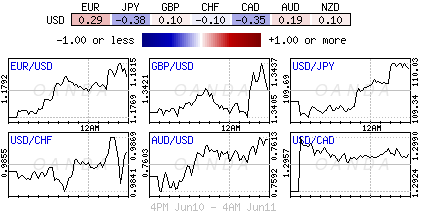

- EUR/USD moved back above the 1.18 level for a good portion of the session after Italy Econ Min Tria gave the markets more reassurances that the new govt had no intention of leaving the Euro. Italian 10-year BTP yield fell by almost 25bps as a result to trade around 2.85%. Pair still well contained in its 1.15-1.20 trading range. Key focus will be the ECB statement on Thursday for hints of when the QE bond buying program would end.

- GBP/USD saw its earlier gains slip away after disappointing trade and production data for April. GBP/USD slipped from 1.34 20 to test below 1.3375 after the data miss. Focus turning to the political front as PM May was expected to urge potential Tory rebels to get behind the party ahead of crucial votes on the EU Withdraw Bill this week.

- The NOK was softer after Norway CPI lagged forecasts. The data miss would likely to keep the central bank on hold until later this summer for its 1st potential rate hike

Fixed Income

- Bund Futures trade 24 ticks lower at 160.07 following the move lower in Treasuries. Upside targets 161.75 followed by 162.50, while a return lower targets the 159.25 level.

- Gilt futures trade at 121.72 lower by 105 ticks following disappointing production data. Support continues stands at 120.75 then 119.25, with upside resistance at 122.85 then 123.35.

- Monday’s liquidity report showed Friday’s excess liquidity rose from €1.924T to €1.924T. Use of the marginal lending facility decreased from €92M to €M.

- Corporate issuance saw 1 issuer raise $255M in the primary market

Looking Ahead

- (MX) Mexico May ANTAD SSS Y/Y: No est v -0.2% prior

- (IL) Israel Central Bank (BOI) May Minutes

- 05:30 (DE) Germany to sell €3.0B in 6-month Bubills

- 06:00 (IL) Israel May Consumer Confidence: No est v 124 prior

- 06:00 (RO) Romania to sell Bonds

- 06:00 (IL) Israel to sell Bonds - 06:45 (US) Daily Libor Fixing

- 07:00 (UK) May NIESR GDP Estimate: 0.3%e v 0.1% prior

- 07:00 (BR) Brazil Jun IGP-M Inflation (1st Preview): 1.5%e v 1.2% prior

- 07:00 (CZ) Czech Central Bank to comment on CPI data

- 07:25 (BR) Brazil Central Bank Weekly Economists Survey

- 07:30 (TR) Turkey Jun Central bank TCMB Survey of Expectations

- 08:05 (UK) Baltic Dry Bulk Index

- 08:00 (ES) Spain Debt Agency (Tesoro) announces of upcoming issuance

- 08:00 (IN) India announces details of upcoming bond sale (held on Fridays)

- 08:55 (FR) France Debt Agency (AFT) to sell combined €3.8-5.0B in 3-month, 6-month and 12-month BTF Bills

- 09:00 (MX) Mexico Apr Industrial Production M/M: No est v -2.4% prior; Y/Y: +3.6%e v -3.7% prior, Manufacturing Production Y/Y: +4.5%e v -2.4% prior

- 09:30 (EU) ECB announces Covered-Bond Purchases

- 09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

- 11:00 (DE) German Chancellor Merkel with IMF chief Lagarde

- 11:30 (US) Treasury to sell 3-month and 6-month Bills

- 11:50 (RU) Russia Foreign Min Lavrov in Berlin on Ukraine

- 12:30 (DE) German Fin Min Scholz on panal in Berlin

- 13:00 (US) Treasury to sell 3-Year Notes

- 13:00 (US) Treasury to sell 10-Year Notes Reopening

- 16:00 (US) Weekly Crop Progress Report

- 21:00 (SG) President Trump and North Korea Leader Kim hold Summit

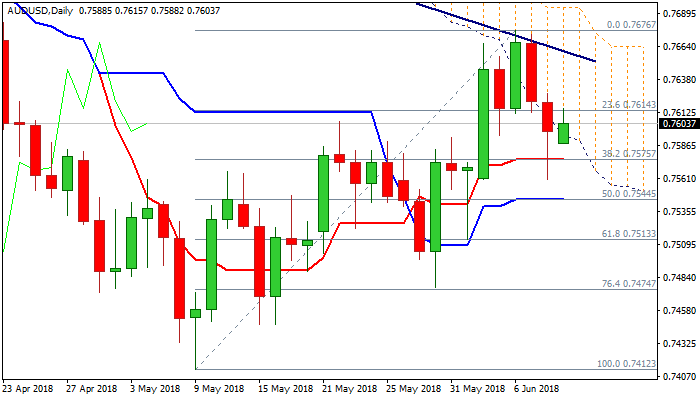

Fresh Risk Sentiment Drives Aussie Back Into Daily Cloud, US/NK Summit In Focus

The Aussie dollar probes breaks into daily cloud on Monday, supported by fresh risk appetite ahead of historical US/NK summit on Tuesday.

Repeated close below daily cloud on Thu/Fri was bearish signal, but pullback from 0.7676/73 tops (where main bear-trendline repeatedly capped upside attempts) was contained by rising 20SMA on Friday’s spike to 0.7560.

Strengthening momentum is supportive but falling daily cloud continues to weigh and keep the downside at risk.

Another close below cloud will be bearish signal and could risk retest of 20SMA (0.7567), break of which is needed to confirm reversal, as 20SMA is reinforced by Fibo 38.2% of 0.7412/0.7676 rally (0.7575).

Bullish scenario requires close in the clod and also close above falling 55 SMA to sideline immediate downside threats.

Res: 0.7607, 0.7621, 0.7658, 0.7676

Sup: 0.7588, 0.7567, 0.7547, 0.7513

USDJPY Intraday Bullish Above 109.60

The US dollar has moved back towards the key 110.00 level against the Japanese yen currency, as the greenback recovers Friday’s heavy losses. The USDJPY pair was met with strong buying interest from the 109.40 level earlier today, after finding support from the 109.19 level. USDJPY buyers will look for further upside above the 110.00 level, while sellers will try to push the price back below the 109.60 support level.

The USDJPY pair is intraday bullish while trading above the 109.60 level, key resistance is found at the 110.26 and 110.48 levels.

If the USDJPY pair falls below the 109.60 level, key intraday support is found at the 109.19 and 109.00 levels.

GBPUSD Now Intraday Bearish Below 1.3400

The British pound has reversed lower against the US dollar, following the release of much weaker than expected monthly Industrial Production and Manufacturing numbers from the United Kingdom economy. The GBPUSD pair currently trades around the 1.3365 level, with further intraday losses likely if the key 1.3352 support level is broken. Traders now look towards a key bond auction in the United States and the upcoming talks between US President Trump and the North Korean leader Kim Jong-un.

The GBPUSD pair is intraday bearish while trading below the 1.3400 level, key support is located at the 1.3352 and 1.3300 levels.

If the GBPUSD pair moves above the 1.3400 level, key technical resistance is found at the 1.3425 and 1.3450 levels.

Forex Analysis: S&P 500 And Nasdaq 100

US equities ended last week with solid gains ahead of what turned out to be a turbulent G7 summit. President Trump has fired off a string of angry tweets criticising Canada and the EU over trade adding that “Fair trade is now to be called fool trade”. Attention will now turn to the historic talks between the Trump and Kim Jong Un in Singapore with headlines likely to induce market volatility over the coming days.

Facebook stock will react to new data-sharing revelations regarding specials deals with companies that granted access to user data well past 2015 when they claimed that third party developers were barred from access. Also this week, video game makers such as Electronic Arts and Activision Blizzard will be in focus as The Electronic Entertainment Expo kicks off.

S&P 500

On the daily chart, the S&P500 (SPX) has continued to make gains after breaking 2760. The index is now approaching a major zone of resistance between 2785-2800. A break of 2800 is needed for a continuation towards 2820 and then new all time highs. Any retracement will find support 2760 and then 2740.

Nasdaq 100

On the daily chart, the Nasdaq 100 (NDX) broke to new all time highs last week. The index is now trading in a potential ascending wedge and if broken could lead to a correction. A break 7100 could open the door to a move lower to support at 7000 followed by 6870. However, as long as 7100 holds, another test of high at 7228 is possible and a break should see the index push towards the Fibonacci extension at 7340.

Geopolitics And Rate Calls To Dominate Busy Week

Monday June 11: Five things the markets are talking about

Investors’ focus now shifts from last weekend’s disastrous G7 meeting in Canada to tomorrows Trump-Kim summit in Singapore and a plethora of major central bank rate announcements later this week.

Market mood remains cautiously ‘risk-on’ as we begin one of the busiest weeks of the calendar year. Global equities are tentatively trading in the ‘black’ as sovereign bond prices fall. The EUR and Italian bonds have jumped after the country’s new finance minister over the weekend confirmed his commitment to the common currency.

Despite the market noise, investors are preparing themselves for more geopolitics to dominate this week’s market activity – Trump is somewhat confident about tomorrow’s summit with Kim Jong-Un. Mind you, he implied that in Quebec on the weekend at the G7, before his Twitter rant, which ended with deepening tensions over U.S tariffs and saw a dispute erupt between the U.S and Canada.

After that, investors shift their focus to a number of Tier I central banks monetary policy decisions – on Wednesday, the Federal Open Market Committee (FOMC) is expected to hike interest rates, while the European Central Bank (ECB) officials are poised to hold the first formal talks on ending it’s bond-buying program (QE) Thursday, while the Bank of Japan (BoJ) meets early Friday, with no change to policy expected.

1. Stocks see the light

In Japan, stocks gain in thin trade as markets await the U.S-N. Korea summit. The Nikkei share average rallied +0.5%, while the broader Topix advanced +0.3%, but volume was low, with only +1b shares changing hands, the lowest level in two-weeks.

Down-under, Aussie markets were closed due to a bank holiday, while in S. Korea, the Kospi rallied +0.7%.

In Hong Kong, shares rose slightly overnight, ahead of tomorrow’s historic U.S-North Korea summit that the market hopes might pave the way for an end to the nuclear standoff on the Korean peninsula. The Hang Seng index rose +0.3%, while the China Enterprises Index gained +0.1%.

In China, stocks closed lower for a third consecutive session overnight, on investor concerns over the liquidity conditions in the market. The Shanghai Composite Index touched its lowest level since last May before closing down -0.5%, while the blue-chip CSI300 index was unchanged.

In Europe, Euro indexes opened broadly higher and have maintained that trend ahead of Wall St. open. Euro financials are well-supported following assurances from Italy over the weekend that they are not interested in leaving the Euro.

U.S stocks are set to open in the ‘black’ (+0.1%).

Indices: Stoxx50 +0.6% at 3,465, FTSE +0.8% at 7,738, DAX +0.5% at 12,834, CAC-40 +0.2% at 5,460; IBEX-35 +0.6% at 9,806, FTSE MIB +2.0% at 21,784, SMI +0.9% at 8,590, S&P 500 Futures +0.1%

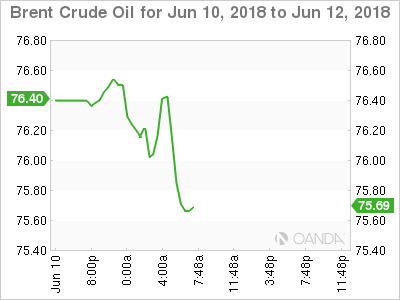

2. Oil prices slip, as U.S. and Russian supplies grow, gold unchanged

Oil prices are under pressure starting the week, pulled down by rising Russian production and the highest U.S. drilling activity in more than three-years, but supported by concerns over future Iranian and Venezuelan output.

Benchmark Brent is down -15c at +$76.31 a barrel, while U.S light crude (WTI) is -10c lower at +$65.64.

Data on Friday showed that the number of new rigs drilling for oil in the U.S rose by one last week to +862, it’s highest since March 2015, according to Baker Hughes. This would suggest that U.S crude output, already at a record high of +10.8m bpd, could climb even further.

Analysts expect higher U.S. output to offset supply curbs by the Organization of the Petroleum Exporting Countries, which have been in place for 18 months and have pushed up prices significantly over the last year.

Nevertheless, dealers remain concerned by falling supply from Venezuela and the potential of lower exports from Iran.

Note: Venezuelan production is falling due to sanctions, economic crisis and mismanagement, while Iran faces U.S sanctions over its nuclear program that are likely to curb exports in the next few months.

OPEC and its partners are due to meet on June 22-23 in Vienna.

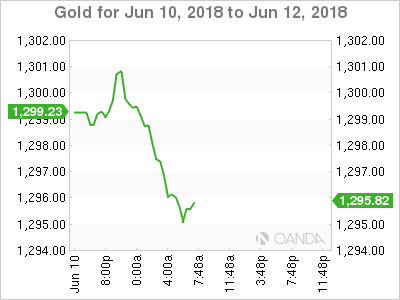

Ahead of the U.S open, gold is trading steady overnight with investors awaiting key central bank policy meetings and the U.S/N. Korea summit this week for direction. Spot gold is steady at +$1,297.75 per ounce, while U.S gold futures for August delivery are -0.1% lower at +$1,301.60 per ounce.

3. Sovereign yields back up in risk-on mood

In early trade, German Bund yields have backed up, signalling risk-on sentiment despite a spat between the U.S and its G7 allies over the weekend. The 10-year Bund yield is trading at +0.47%, up +3 bps. Also providing some bond price pressures is the reassuring statement by Italy’s new finance minister over the weekend that a euro exit is out of question. Italian 10-year BTP yield has fallen by almost -25 bps as a result to trade around +2.85%.

Next up, bond investors will be eyeing the ECB’s meeting Thursday, which will potentially offer fresh information regarding the end of QE. If so, it should be EUR positive and partly counterweigh the potentially more ‘hawkish’ Fed meeting expected on Wednesday.

Elsewhere, the yield on 10-year Treasuries has advanced +2 bps to +2.96%, while the U.K 10-year Gilt yield increased +3 bps to +1.388%, the highest in almost three weeks.

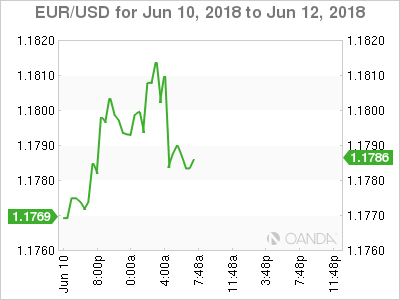

4. Dollar in a flux

EUR/USD (€1.1788) temporarily traded above the psychological €1.1800 for a good portion of this morning early session after Italian Economic Minister Tria gave the markets more reassurances that the new government had no intention of leaving the Euro. The pair has been well contained in its €1.15-1.20 trading range. Investors’ key focus will be the ECB statement on Thursday for hints of when the QE bond-buying program would end.

GBP/USD (£1.3368) saw its earlier gains slip away after disappointing trade and production data for April (see below). GBP/USD slipped from £1.3420 to new intraday lows atop of €1.3360 after the data miss. Market focus again turns to the political front as PM May is expected to urge potential Tory rebels to get behind the party ahead of crucial votes on the E.U Withdraw Bill tomorrow.

The NOK ($8.0625) is a tad softer ahead of the U.S open after Norway CPI lagged forecasts (+0.1% vs. +0.3%e m/m). The data miss would likely to keep Norges bank on hold until later this summer for its first potential rate hike.

5. U.K factory output tumbles at steepest in six-years

Data this morning showed that U.K factory output fell in April at the steepest monthly pace in six-years, which would suggest that weakness the U.K economy witnessed in Q1, has firmly extended into Q2.

Today’s report provides further proof that the U.K economy’s slow start to the year had deeper causes than a patch of bad weather, and should add to market doubts that the BoE will raise interest rates again this year.

British manufacturing output declined -1.4% in April compared with March, and the largest monthly fall since October 2012 according to the ONS.

Digging deeper, output fell across the board, in sectors including auto production, metals and electrical machinery.

Overall industrial production declined -0.8% on the month, as a pickup in oil and gas output partly offset the poor performance of manufacturing.

Note: The U.K economy has been lagging its counterparts as uncertainty over the country’s future ties to the E.U continues to weigh on activity and investment.

DAX Moves Higher, Shrugs Off G-7 Fireworks

The DAX index has started the week with gains. In the Monday session, the DAX is at 12,824, up 0.45% on the day. There are no German or eurozone events on the schedule. On Tuesday, Germany and the eurozone release ZEW Economic Sentiment.

European stock markets are in positive territory on Monday, despite a remarkably acrimonious G-7 meeting. The summit in Quebec lived up to the negative hype, as the “G-6 +1” was the scene of sharp disagreements between U.S President Trump and the other six leaders. Trump openly clashed with the other leaders over his recent tariffs against the European Union and Canada and pulled back his endorsement of the traditional post-summit statement put out by the other members. The undiplomatic Trump also tweeted that Canadian Prime Minister Trudeau, who hosted the summit, was “dishonest and weak”. Canada and the EU are furious over recent US tariffs, especially because of Trump pushed them through on the basis of ‘national security’. The glaring cracks in G-7 unity could cast a long shadow on trade relations between the U.S and the “G-6”, with business confidence and capital spending at risk if the tariff spat continues.

The ECB hold its next policy meeting on Thursday, and the markets will be looking for any clues with regard to the ECB’s asset-purchase program. Currently, the bank is purchasing EUR 30 billion/mth, and the scheme is scheduled to wind up in September. However, some ECB policymakers want to phase out the program slowly, rather than turn off the tap completely in September. ECB Chief Economist recently said that the ECB board members would conduct a detailed discussion about the fate of the stimulus package at the June meeting. The head of the German central bank, Jens Weidmann, weighed into the discussion last week, saying that the markets expected the stimulus program to wind down before the end of the year and that such expectations were “plausible”. ECB head Mario Draghi will likely make mention of the program at his press conference following the Thursday meeting, so traders should be prepared for some volatility from EUR/USD on Thursday.

Euro Edges Higher In Light Fundamentals Session

EUR/USD has posted gains in the Monday session. Currently, the pair is trading at 1.1791, up 0.19% on the day. It’s a very quiet start to the week on the release front, with no major events. On Tuesday, Germany releases ZEW Economic Sentiment and the US publishes CPI reports.

The markets were braced for a bumpy meeting between the Group of Seven leaders on Friday, but the sharp disagreements between President Trump and the other six members were far worse than expected. Trump openly clashed with the other leaders over his recent tariffs against the European Union and Canada and pulled back his endorsement of the traditional post-summit statement put out by the other members. The undiplomatic Trump also tweeted that Canadian Prime Minister Trudeau, who hosted the summit, was “dishonest and weak”. Canada and the EU are furious over recent US tariffs, especially because of Trump pushed them through on the basis of ‘national security’. The glaring cracks in G-7 unity could cast a long shadow on trade relations between the U.S and the “G-6”, with business confidence and capital spending at risk if the tariff spat continues.

The ECB hold its next policy meeting on Thursday, and the markets will be looking for any clues with regard to the ECB’s asset-purchase program. Currently, the bank is purchasing EUR 30 billion/mth, and the scheme is scheduled to wind up in September. However, some ECB policymakers want to phase out the program slowly, rather than turn off the tap completely in September. ECB Chief Economist recently said that the ECB board members would conduct a detailed discussion about the fate of the stimulus package at the June meeting. Mario Draghi will likely make mention of the program at his press conference, so traders should be prepared for some volatility from EUR/USD on Thursday.