Sample Category Title

A Box Full Of Surprises GE14

Malaysia

Historical events unfolded overnight as in stunning fashion Pakatan Harapan(PH) won the hotly contested which is creating quite the stir with foreign investors trying to decipher the PH new mandate. The thinly traded one-month NDF markets have shot up on the election results above 4.05 in response to the anticipated knee-jerk weakening on Malaysian assets as indicated but the tumult on iShares MSCI Malaysia ETF.

But indeed, this election surprise has caught some off guard, and with the USD MYR pulling up 1.75 % in the pre-election run-up, but with the NDF now printing 4.075 the Ringgit is now sitting at the bottom of the regional currency pecking order.

Fortunately or unfortunately for some, the local cash markets will be closed May 10 and 11 in conjunction with the special public holiday which should provide time for investors to digest the fallout. Indeed if abolishing the GST and accelerating fiscal spending becomes the new government’s policy cornerstone this could be interpreted negatively given the drain on government coffers, this despite surging oil prices.

The BNM was due today but at this stage, it remains uncertain if they will go ahead with the policy meeting or take the weekend to rethink current policy which could also weigh on MYR sentiment due to indecision.

Currency Markets

Not to overcomplicate issues, after the recent wave of USD buying, profit taking has set in ahead of Thursdays Key CPI prints which will arguably be the most critical data release for the month. A solid print will underpin recent hawkishness building on the US economic view (and sequential Fed pricing). Whereas, a downside miss could stop the bubbling USD dead in its tracks. In other critical cross-asset markets, US 10y yield is back to 3.0%, WTI is enjoying the lofty levels above $ 71, equities are in the green while gold is in search of its next catalyst.

The correlation between rates and FX is picking up again, and the USDJPY continues to trade constructively. Suggesting we could finally bound clear of the 110 level on a robust US CPI print

Oil Markets

Unsurprisingly Crude continues to trade actively following the US pulling out of JCPOA as the decision poses significant supply risk in the context of the delicately balanced supply and demand matrix.

But putting today’s API inventories report into context( surprise draw), it confirms the general trend that US inventories are shrinking. Suggesting unless there are some production increases from the Opec/ Non-Opec accord to offset the drop in Venezuelan production, and the expected decline of the Iranian output, prices could be in for a significant leg higher. Of course, there is little indication that the accord will be looking to intervene, but the guessing game will intensify the closer we get to the June 21 OPEC meeting in Vienna

Gold Markets

Gold traders are desperately looking for a theme after putting the Iran announcement on the back burner for the time being. But there remains enough middle east risk, not to mention the looming Trump-Kim summit to keep gold dips tentatively supported in the face of the resurgent USD. The point, in fact, several sirens have sounded in the Golan Heights earlier, and Isreal defence is currently investigating while Israel’s army has ordered all communities there to prepare bomb shelter due to “irregular” Iranian activity in the region. The US Embassy has also issued a travel warning to the area.

However, unless an actual escalation in Middle East tension, Gold could be extremely vulnerable to an extension of the USD dollar rally.

BoE – Will They Or Won’t They?

Is a Rate Hold Nailed On Or Are Markets Positioned For a Shock?

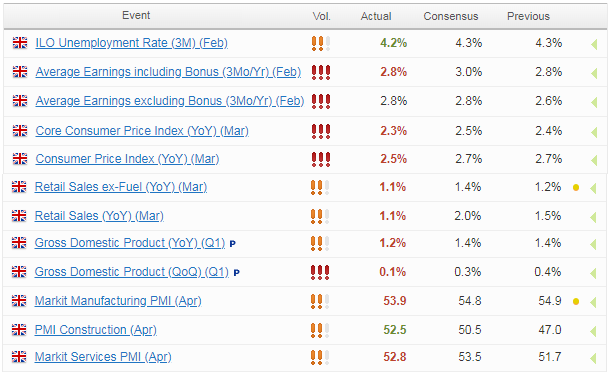

The Bank of England meets on Thursday and, despite spending months preparing markets for a rate hike, the central bank is widely expected to leave them on hold at 0.5%.

While markets don't always get fully on board with central bank efforts to prepare markets for a tightening of monetary policy – as the US Federal Reserve found in the early days of its cycle – I think the two are actually closely aligned on this particular occasion.

UK data casts doubt over a rate hike

Carney's change of tune prompts significant drop in expectations

Market reaction could be huge if BoE follows through on previous warnings

The economic data from the UK over the last month or so has been underwhelming at best and another drop off in the inflation readings has afforded the Monetary Policy Committee the space to take a little more time rather than rush into raising rates.

While much of the weak data could be attributed to the “Beast from the East”, the weaker PMI surveys and the fact that inflation is now only just above target after peaking above 3% in November gives the central bank little reason to raise interest rates, particularly against such an uncertain backdrop.

Brexit poses many risks for the UK economy and with less than a year to go until the country leaves the EU – meaning we should have more clarity on the outlook later this year – there seems little to be gained in rushing to raise interest rates when it may have to be reversed shortly after.

It's not just the data that has cast doubt on a rate hike on Thursday – the implied probability has fallen from around 70% a few weeks ago to only 13% now – Governor Mark Carney didn't want to get drawn on the timing of the next rate hike on 19 April, stressing he's conscious that there are other meetings over the course of the year, an apparent hint that May is no longer the certainty it was.

GBP/USD – British Pound Steady, Markets Expect BoE to Stand Pat

What is clear is that there is no real unanimous view on the correct timing for rate hikes on the MPC which should make the votes very interesting on Thursday. Ian McCafferty and Michael Saunders will likely stick with their gut in voting for a hike – especially if the latter's recent comments are anything to go by – but the question is whether the new forecasts will be enough to persuade others to follow.

The new economic forecasts will also be key in shaping the view on future rates hikes, as will the comments of Carney and his colleagues in the press conference shortly after which should make for a very interesting day for sterling, UK bonds and the FTSE. The pound has fallen more than 5% against the dollar over the last weeks as expectations of a hike have collapsed.

While Thursday looks a foregone conclusion, the BoE could still spring a surprise on the markets having previously laid the groundwork for such a move. If they do, the market reaction would likely be quite huge.

Gold Trading Sideways After Trump Bombshell

Gold is trading sideways in the Wednesday session. In North American trade, the spot price for an ounce of gold is $ 1313.48, down 0.08% on the day. On the release front, producer price inflation reports were soft. PPI dropped to 0.1%, shy of the estimate of 0.2%. Core PPI edged lower to 0.2%, matching the forecast. The focus remains on inflation on Thursday, as the US releases consumer inflation reports.

US President Trump delivered a major speech on Tuesday, announcing that the US would withdraw from the Iran nuclear deal. The bombshell announcement did not impact on gold prices, as demand for safe-haven assets remains muted. In his televised remarks, Trump blasted the agreement and said that the US would reimpose stiff sanctions on Iran. However, Britain, France and Germany have said they plan to remain in the deal, and will be holding a high-level meeting with Iranian leaders on how the agreement can be salvaged. With the US acknowledging that the White House does not have a ‘Plan B', it's unclear what happens next. Meanwhile, tensions between Israel and Iran are at a fever pitch, and any confrontation between the two could shake up the markets and send gold prices upwards.

The Federal Reserve's newest regional Fed president, Thomas Barkin, delivered a major speech on Monday, and his tone was decidedly upbeat. Barkin said that the economy is “remarkably strong: above-trend growth, low unemployment, inflation at target”. Barkin added that although the labor market is strong, it is not causing pressure on wages, but low unemployment should lead to an increase in inflationary pressures. As for upcoming rate increases, Barkin was careful to remain mum on how many rate hikes he expects this year. The Fed raised rates in March by a quarter-point and continues to forecast two additional increases this year. However, some policymakers are calling for three more hikes, given the strong health of the US economy.

Eco Data 5/10/18

[php_everywhere instance="1"]

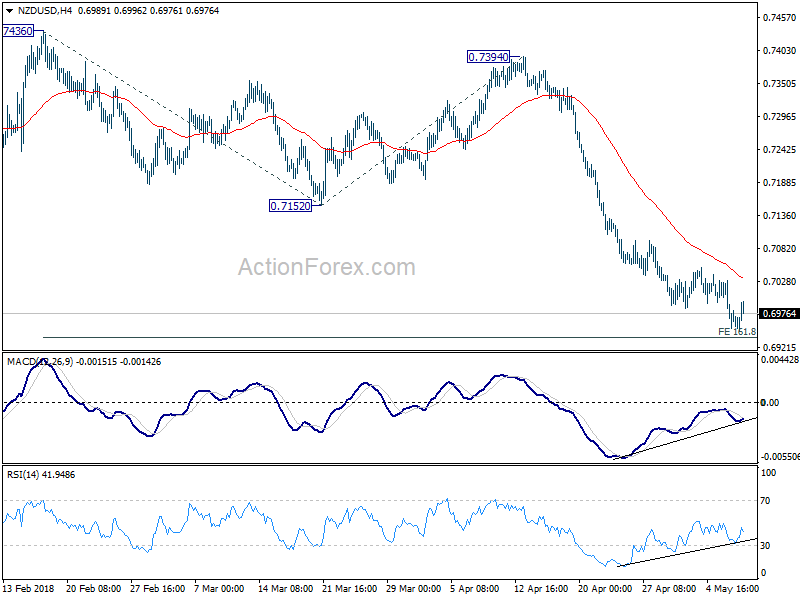

NZDUSD a counter trend candidate ahead of RBNZ

RBNZ rate decision is a major focus in the upcoming Asian session. It's widely expected to keep OCR unchanged at 1.75%. There is little to practically no chance of a surprise. The question is on how RBNZ view the sharp slow down in CPI to 1.1% in Q1. The reaction of NZD would very much depend on how dovish the new governor Adrian Orr is.

Take a look at NZDUSD Action Bias table, D row shows it's clearly in a down trend. However, 6H Action bias suggests that downside momentum is unconvincing. Adding to that, there is a few bard of upside blue H row, arguing that it's in a rebound.

Take a look at the 6H Action Bias chart, it's apparent, even with eyeballing, that the decline since mid April is losing momentum. The so many neutral bars since late April is consistent with this view. So, is it ready for a rebound?

Take a look at the regular bar chart, we see that NZD/USD reached as low as 0.6947 earlier today. It's now close to 161.8% projection of 0.7436 to 0.7152 from 0.7394 at 0.6934. Bullish convergence is seen in 4 hour RSI. There is possibility of bullish convergence in 4 hour MACD too. So, this is a good candidate for counter trend, or reversal trading.

We'd like to emphasize that the exact strategy is very personal. It has to suit one's temperament. Some traders like to catch tops and bottoms. Some traders like to grab quick profits on swing trades. Some like scalping. Some like to hold a position for a few weeks or more. While the strategies vary, the analytic process, to us, is pretty much the same. It's about deciding what to trade first, then see if it fits our style. To us, it has to be the "style" first, then "what", before "how" the actual system.

That is, for those who like counter trend trading (style), NZDUSD (what) is a candidate. And how? We'll buy on next dip, with a tight stop below 0.6934 projection level at 0.6900, target 0.7152 support turned resistance, and get out earlier if momentum of the rebound is weak. Other traders could have their own way based on their temperament.

British Pound Steady, Markets Expect BoE to Stand Pat

The British pound continues to show little movement this week. In North American trade, GBP/USD is trading at 1.3574, up 0.19% on the day. On the release front, there are no major British indicators. In the US, PPI dropped to 0.1%, shy of the estimate of 0.2%. Core PPI edged lower to 0.2%, matching the forecast. On Thursday, the UK releases Manufacturing Production, and the US will publish consumer inflation reports.

The currency markets are not showing much movement after President Trump’s dramatic speech on Tuesday. Trump announced that the US would withdraw from the Iran nuclear deal. Trump blasted the agreement and said that the US would impose stiff sanctions on Iran. However, Britain, France and Germany have said they plan to remain in the deal, and will be holding a high-level meeting with Iranian leaders on how the agreement can be salvaged. With the US acknowledging that the White House does not have a ‘Plan B’, it’s unclear what happens next. Meanwhile, tensions between Iran on one the one side, and US allies Israel and Saudi Arabia on the other are at a fever pitch, and any military confrontation involving these countries could shake up the markets.

Investors are keeping a close eye on the Bank of England, which will set the benchmark interest rate on Thursday. Just a few weeks ago, there were strong expectations that the bank was poised to raise rates by a quarter-point, but some weak releases have soured sentiment towards a rate hike. For example, Preliminary GDP in the first quarter gained only 0.1%, missing the forecast of 0.3 percent. The cautious BoE is expected to maintain rates at 0.50% on Thursday, as short-term interest rates are now pricing in less than a 10 percent probability of a rate increase. Analysts are circling August as the next likely date for a rate hike.

ECB Lane: Too early to tell if soft data is a demand issue, or just running out of room

ECB Governing council member Philip Lane said the policymakers need more data to decide whether the slowdown in Eurozone is due to global demand of a decrease in the amount of slack domestically.

He said:

"In terms of soft data and some of the hard data, the question is whether it is something just to acknowledge and accept as running out of room, versus a demand issue, which would trigger more questions,"

"But let's see. Let's see where we are. I think it's too early to tell."

"In June I think and next month possibly we will have much more recent data"

Sunset Market Commentary

Markets

Global core bonds lost more ground today with US Treasuries underperforming German Bunds ahead of tonight’s 10-yr Note auction. Higher oil prices in the wake of Trump’s rejection of the Iran deal continue to have only a marginal negative impact. FI, FX and stock markets’ reaction to his decision remain muted overall. Today’s eco calendar was empty apart from softer than expected US PPI data. However, the reaction to the report was very modest. Markets are looking forward to tomorrow’s CPI data. US yields increase by up to 3.0 bps (10-yr) at the time of writing. The US 10-yr yield passed the psychological 3% threshold again. The German yield curve bear steepens with yields up to 1.3 bp higher (30-yr). BTP’s slightly underperform, but the ‘damage’ remains limited. The Italian spread trades marginally wider compared to a slightly tighter spread for most other EMU countries. 5SM and Lega are trying to buy time to reach a government without triggering fresh elections.

Today, the USD rally shifted into a lower gear. This morning, it initially looked that combination of higher oil prices, higher US yields and a stronger dollar that regained of late would continue after president Trump decided to exit the Iran nuclear deal. EUR/USD touched a new ST correction low in the 1.1825 area. Interest rate differential also still widened slightly further in favour of the dollar. However, it was not enough to extend the USD rally. EUR/USD rebounded. We didn’t see a specific trigger for this intraday reversal. The EUR/USD filled offers just below the 1.19 big figure after the publication of softer than expected US PPI data. However, the impact of the report on USD trading was limited and short-lived. USD bulls probably await additional info from this evening’s US 10-y auction and even more from tomorrow’s US CPI release. Or is euro selling easing? Contrary to what was the case of late, USD/JPY outperformed USD/EUR today. The pair maintained most of this morning’s gain and trades in the 109.75 area. EUR/USD is changing hands in the 1.1875/80 area.

Today, sterling trading was modestly driven by technical considerations. If anything, the UK currency traded with a slightly positive bias. In this respect, investors ignored very weak April BRC retail sales published this morning. Sterling investors are looking forward to tomorrow’s BoE policy decision. Markets apparently prepare for a ‘hawkish hold’ scenario. The BoE might keep the door open for a rate hike later this year if the poor UK Q1 economic performance would prove to be temporary. EUR/GBP trades currently in the 0.8740/45 area. Cable rebounded to the 1.36 as the recent USD rally is running into resistance.

News Headlines

5SM leader Di Maio and Lega leader Salvini made a last-ditch effort to form a government together, asking President Mattarella to delay by 24 hours his plan to appoint a non-partisan premier.

Turkish President Erdogan summoned economy officials for a meeting at the palace in Ankara to discuss the slide of lira to a record low, according to two officials who declined to be identified due to sensitivity of the information. EUR/TRY dropped from 5.15 towards 5.05.

EUR/SEK declined from 10.45 to 10.35. The Swedish krona gained ground after April CPI data printed in line with forecasts (0.4% M/M & 1.9% Y/Y). The data further question the markets dovish reading of the previous Riksbank meeting. Yesterday’s Minutes of that meeting also supported the SEK for the same reason.

Japanese Yen Dips Despite Soft US Inflation Reports

After showing little movement early in the week, the yen has lost ground in the Wednesday session. In North American trade, USD/JPY is trading at 109.77, up 0.56% on the day. On the release front, the Bank of Japan releases the summary of opinion from the April policy meeting. As well, Japan’s current account surplus is expected to rise to JPY 1.62 trillion. In the US, PPI dropped to 0.1%, shy of the estimate of 0.2%. Core PPI edged lower to 0.2%, matching the forecast. On Thursday, the US will publish consumer inflation reports.

US President Trump dropped a bombshell on Tuesday, announcing that the US would withdraw from the Iran nuclear deal. However, the currency markets are not showing much movement in response to the speech. The Japanese yen has lost ground on Wednesday, as demand for safe-haven assets remained muted. In his televised remarks, Trump blasted the agreement and said that the US would reimpose stiff sanctions on Iran. However, Britain, France and Germany have said they plan to remain in the deal, and will be holding a high-level meeting with Iranian leaders on how the agreement can be salvaged. With the US acknowledging that the White House does not have a ‘Plan B’, it’s unclear what happens next. Meanwhile, tensions between Israel and Iran are at a fever pitch, and any confrontation between the two could shake up the markets.

Japanese consumer spending disappointed in March, according to a key indicator. Household Spending declined 0.2%, underscoring sluggish domestic demand and a pessimistic Japanese consumer. Although the employment market is very tight, consumers continue to hold tight to the purse strings, as companies have been reluctant to raise wages. However, Bank of Japan policymakers appear more confident in the Japanese economy, as the minutes from the March meeting were upbeat. The minutes said that the economy, as well as inflation, are likely to continue on an upward trend. Will the bank’s summary of opinions also be optimistic? The bank has long sought to reach an inflation target of around 2 percent, and if policymakers are correct and this goal is on its way to being achieved, the BoJ will be able to contemplate a reduction in its stimulus program, a move which could have a substantial impact on the yen. However, the cautious BoJ is likely to stick to current policy well into 2019, even if economic conditions improve and inflation moves closer to target.

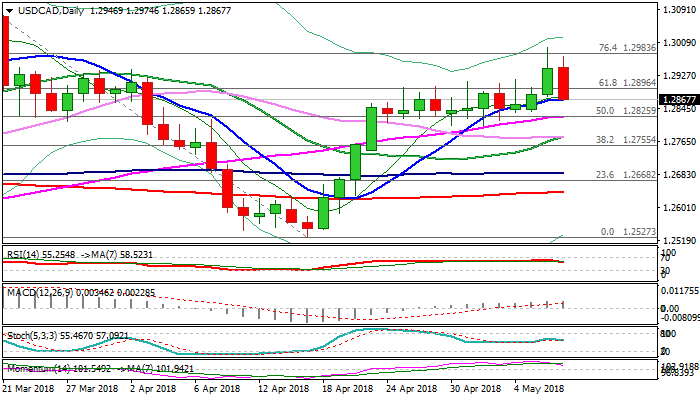

USDCAD Eases after Bulls Stalled Under 1.30 Barrier; Daily Cloud Top/10SMA Mark Key Supports

The USDCAD pair eased on Wednesday as the greenback eased from fresh highs posted after US decision on Iran while loonie was boosted by fresh rise in oil prices.

Tuesday’s rally which marked eventual break above two-week 1.2800/1.2915 range stalled just ticks under psychological 1.30 barrier and subsequent pullback cracked strong supports at 1.2880/70 (daily cloud top/rising 10SMA.

Daily techs show mixed signals as RSI and momentum are heading lower while MA’s remain in bullish setup.

Pair’s action at key points 1.2880/70 would provide fresh direction signals. Clear break lower would be negative signal for extension towards next key supports at 1.1817/15 (Fibo 38.2% of 1.2527/1.2997 rally/recent range floor).

Conversely, expectations for renewed attack at 1.30 barrier are expected to stay in play while 10SMA/cloud top hold dips.

Res: 1.2974; 1.3000; 1.3076; 1.3103

Sup: 1.2861; 1.2826; 1.2815; 1.2778