Sample Category Title

French FM Le Drian: Trump’s decision was “isolationist, protectionist and unilateral logic.

French Foreign Minister Jean-Yves Le Drian criticized Trump's decision to withdraw from the Iran deal as "isolationist, protectionist and unilateral logic." And he added, "this is a break with international commitment and France deeply regrets this decision."

But Le Drian emphasized that the Iran nuclear deal "is not dead", and pledged to "bring businesses together in the coming days to try and preserve them as much as possible from the US measures." And, "we must talk about Iran's impressive ballistic missiles. Let's talk about this with Iran, let's put everything on the table but let's stay in the accord, the accord is a good thing for the stability in the region and for our security."

French President Emmanuel Macron would call Iranian President Hassan Rouhani today. And representatives from France, the UK and Germany would meet with Iranian counterparts on Monday.

Iran Uncertainty Pushing Up Oil And US Yields

Notes/Observations

- Iran uncertainty pushing up oil and US yields, USD benefits

- France production data continued the theme of moderation of EU data during Q1

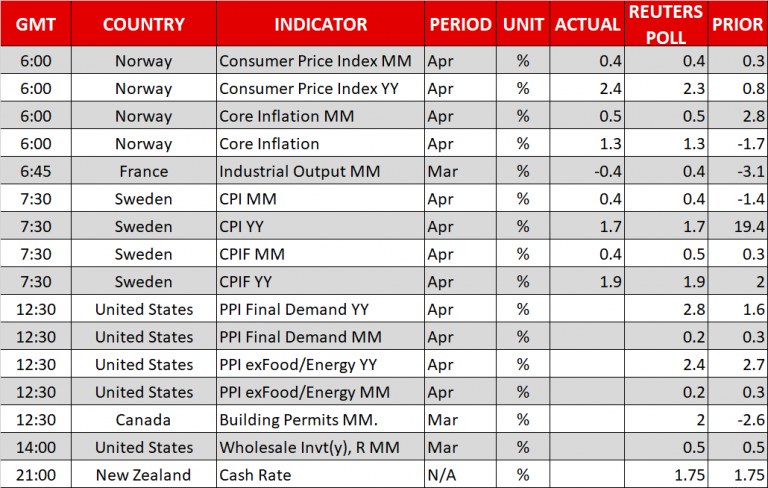

- Swedish, Norwegian and Hungarian CPI data roughly in-line with expectations; concerns of prolong low inflation seem to be abating

Asia:

- Japan Mar Labor Cash Earnings saw its fastest annual rise since June 2003 (YoY: 2.1% v 1.0%e); Real Cash Earnings rose for the 1st time in 4 months (y/y: +0.8% v -0.5%e)

Europe:

- ECB's Vasiliauskas (Lithuania): ending QE in Dec was a realistic scenario. A 6 to 9 month period between end of QE and first rate hike seemed logical. Reiterated MPC view that there was no reason to dramatize the recent economic slowdown

- Forza Party's Berlusconi said to have denied he was considering stepping aside to allow 5-Star/Northern League to form government

- UK House of Lords voted in favor of Brexit amendment that would allow the UK to participate in EU agencies after leaving the union (another defeat of PM May's govt Brexit strategy)

- UK PM May could bypass her Brexit Cabinet by asking the full Cabinet to back her plans for a customs partnership with the EU

- France Pres Macron: France, Germany and UK regret the US decision to leave Iran deal; To work collectively on a wider Iran agreement. Iran framework will cover ballistic missiles, the post-2025 period

- EU's Mogherini: EU vows to uphold Iran nuclear accord despite Trump decision. Intended to protect its economic investments in Iran

- Russia foreign ministry: deeply disappointed with Trump decision to leave the Iran nuclear deal; US move was a violation of the deal

Americas:

- President Trump: US to withdraw from Iran nuclear agreement; to reinstate highest level of economic sanctions on Iranian regime

- Former President Obama: Trump's decision to withdraw from the Iran deal was misguided and a serious mistake

Energy:

- Weekly API Oil Inventories: Crude: -1.9M v +3.4M prior

Economic Data:

- (NL) Netherlands Mar Manufacturing Production M/M: -0.1% v -0.2% prior; Y/Y: 3.5% v 4.2% prior; Industrial Sales Y/Y: -1.8% v +6.9% prior

- (NO) Norway Apr CPI M/M: 0.4% v 0.4%e; Y/Y: 2.4% v 2.3%e

- (NO) Norway Apr CPI Underlying M/M: 0.5% v 0.5%e; Y/Y: 1.3% v 1.4%e

- (NO) Norway Apr PPI (including Oil) M/M: 3.3% v 0.5% prior; Y/Y: 12.2% v 6.4% prior

- (DK) Denmark Mar Current Account Balance (DKK): 13.9B v 13.5B prior; Trade Balance: 5.1B v 6.9B prior

- (FR) France Mar Industrial Production M/M: -0.4% v +0.4%e; Y/Y: 1.8% v 2.8%e

- (FR) France Mar Manufacturing Production M/M: 0.1% v 0.9%e; Y/Y: 0.4% v 2.1%e

- (ES) Spain Mar Industrial Output NSA Y/Y: -3.6% v +3.0%e; Industrial Output SA Y/Y: 5.1% v 3.6%e, Industrial Production M/M: +1.2% v -0.1%e

- (CZ) Czech Mar National Trade Balance (CZK): 18.7B v 21.3Be

- (HU) Hungary Apr CPI M/M: 0.7% v 0.7%e; Y/Y: 2.3% v 2.3%e

- (SE) Sweden Apr CPI M/M: 0.4% v 0.4%e; Y/Y: 1.7% v 1.7%e; CPI Level: 327.10 v 327.24e

- (SE) Sweden Apr CPIF M/M: 0.4% v 0.4%e; Y/Y: 1.9% v 1.9%e

- (SE) Sweden Mar Household Consumption M/M: 0.5% v 0.5% prior; Y/Y: 3.3% v 1.7% prior

- (CZ) Czech Apr International Reserves: $147.0B v $149.7B prior

- (IT) Italy Mar Retail Sales M/M: -0.2% v 0.0%e; Y/Y: 2.9% v 0.1%e

Fixed Income Issuance:

- (IN) India sold total INR150B vs. INR150B indicated in 3-month, 6-month and 12-month bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.3% at 391.2, FTSE +0.6% at 7608, DAX +0.3% at 12953, CAC-40 flat at 5522, IBEX-35 flat at 10167, FTSE MIB +0.8% at 24328, SMI +0.1% at 8949, S&P 500 Futures -+0.5%]

- Market Focal Points/Key Themes: European Indices trade higher across the board, trending upwards through the session on the back of rising US futures following earnings and Geo political developments. Siemens trades higher after results and raised guidance, with AB Inbev, Imperial Brands, Dialog Semi among other gainers after earnings. Meanwhile Greggs drops sharply in the UK after a drop in profits, with Compass Group and Skanska also lower after earnings. In the M&A Space Vodafone acquired the select European assets from Liberty Global in a €18.4B deal, with Bruberry lower after Groupe Bruxelles Lambert sells its stake for £498M, in the US its reported Walmart has acquired 75% stake in Flipkart for $15B. Looking ahead notable earners include Coty, Mylan and Groupon.

Movers

- Consumer Discretionary [ Ahold Delhaize -1.8% (Earnings), Greggs [GRG.UK] -15% (Earnings), G4S [GFS.UK] -4% (Earnings), Burberry [BRBY.UK] -6% (Groupe Bruxelles Lambert sells stake) ]

- Industrials [Skanska [SKAB.SE] -4.7% (earnings), Fraport [FRA.DE] +1.4% (Earnings) ]

- Consumer Staples [ Imperial Brands [IMB.UK] +4% (Earnings), Compass Group [CPG.UK] -5.7% (Earnings) ]

- Telecom [ Vodafone [VOD.UK] +1.3% (Acquires certain European assets from Liberty Global)]

- Technology [Siemens [SIE.DE] +4.7% (Earnings), Dialog Semi [DLG.DE] +7.3% (Earnings)]

Speakers

- Brazil Central Bank Gov Goldfajn: Focus remained on inflation, strong USD was a global issue (not just exclusive for Brazil)

- Turkey Fin Min Agbal said to announce a tax amnesty for overseas repatriation

- Turkey Central Bank increases size of Lira FX swap auction size to $1.5B from $1.25B

- Turkey President Erdogan to have meeting with Economic officials regarding the exchange rate

- Russia Foreign Min lavrov stated that its govt remains committed to the Iranian nuclear accord.

- Iran Parliament to vote on motion to call for 'proportional and reciprocal' action by govt in the aftermath of the US withdrawal from the nuclear accord

Currencies

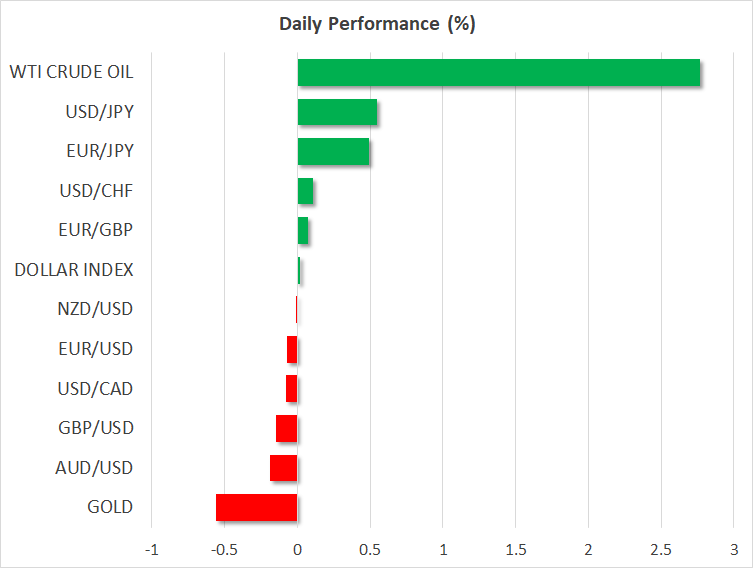

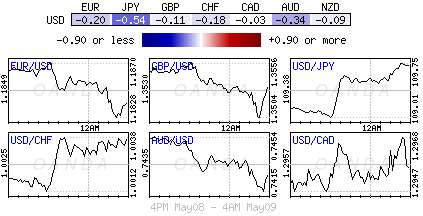

- USD continued its firm tone as geopolitical and trade issues remain in focus and remain at its best level for the year against the major pairs. Trump’s announcement to withdraw from the Iran nuclear accord providing some uncertainty and helping to push up oil prices and US yields.

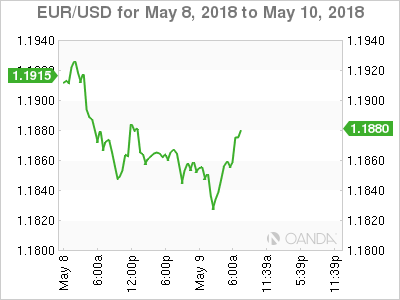

- EUR/USD tested the 1.1822 level before consolidating its losses.

- USD/JPY making another approach toward the 110 handle, which has proven to be stubborn resistance in recent weeks.

- GBP/USD initially tested below the 1.35 handle before recovering the bulk of its losses. Again the focus was turning towards Thursday’s BOE decision. The Times shadow MPC had 6 of the 9 members vote for a 25bps hike tomorrow despite recent weak economic data with 2 of the members saying QE should start to be wound down. Nonetheless the market seemed to be on the lookout for a hawkish hold by the central bank.

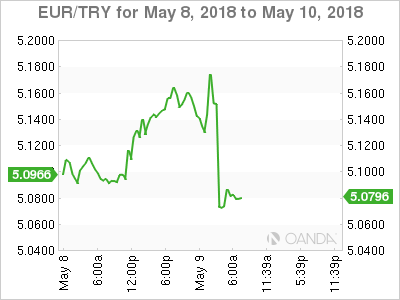

- Emerging market currencies continues to struggle. Turkey announces a few measures to combat the lira weakness. The TRY currency reversed its initial losses in the session after reports circulated that President Erdogan would hold a meeting on exchange rates.

Fixed Income

- Bund Futures trade 28 ticks lower at 158.63 as Euro Zone money markets price in roughly 75% chance of a 10bps ECB rate hike by June 2019, after fully pricing a move two weeks ago. Upside targets 159.75, while a return lower targets the 157.25 level.

- Gilt futures trade at 121.87 lower by 26 ticks, coming off the highs made in March. Support continues stands at 120.85 then 120.25, with upside resistance at 123.35 then 123.85.

- Wednesday’s liquidity report showed Tuesday's excess liquidity rose to €1.900T from €1.892T prior. Use of the marginal lending facility increased from €25M to €14M.

- Corporate issuance saw 7 issuers raise $15B in the primary market

Looking Ahead

- 05:30 (ZA) South Africa Apr Sacci Business Confidence: No est v 97.6 prior

- 05.30 (UK) Weekly John Lewis LFL sales data

- 05:30 (DE) (DE) Germany to sell €1.5B in 1.25% Apr 2048 Bunds

- 05:30 (UK) DMO to sell £2.75B in 1.625% Oct 2028 Gilts

- 05:30 (PT) Portugal Debt Agency (IGCP) to sell €1.0-1.25B in 2023 and 2028 OT bonds

- 06:00 (PT) Portugal Q1 Unemployment Rate: No est v 8.1% prior - 06:00 (IE) Ireland Mar Property Prices M/M: No est v 1.1% prior; Y/Y: No est v 13.0% prior

- 06:00 (CZ) Czech Republic to sell CZK15B in bonds

- 06:45 (US) Daily Libor Fixing - 07:00 (RU) Russia to sell OFZ bonds

- 07:00 (US) MBA Mortgage Applications w/e May 4th: No est v -2.5% prior

- 07:00 (TR) Turkey President Erdogan to have meeting with Economic officials regarding the exchange rate

- 08:00 (HU) Hungary Central Bank's Apr Minutes

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) Apr PPI Final Demand M/M: 0.2%e v 0.3% prior; Y/Y: 2.8%e v 3.0% prior

- 08:30 (US) Apr PPI Ex Food and Energy M/M: 0.2%e v 0.3% prior; Y/Y: 2.4%e v 2.7% prior

- 08:30 (US) Apr PPI Ex Food, Energy, Trade M/M: 0.2%e v 0.4% prior; Y/Y: No est v 2.9% prior

- 08:30 (CA) Canada Mar Building Permits M/M: +2.2%e v -2.6% prior

- 09:00 (MX) Mexico Apr CPI M/M: -0.3%e v +0.3% prior; Y/Y: 4.6%e v 5.0% prior, CPI Core M/M: 0.2%e v 0.3% prior

- 10:00 (US) Mar Final Wholesale Inventories M/M: 0.5%e v 0.5% prelim, Wholesale Trade Sales M/M: No est v 1.0% prior

- 10:30 (US) Weekly DOE Crude Oil Inventories

- 13:00 (US) Treasury to sell 10-Year Notes

- 13:15 (US) Fed’s Bostic (FOMC voter, dove) on economic outlook and monetary policy

- 17:00 (NZ) New Zealand Central Bank (RBNZ) Interest Rate Decision: Expected to leave Official Cash Rate unchanged at 1.75%

Japan, South Korea and China agreed on security and economic cooperations

Japanese Prime Minister Shinzo Abe, South Korean President Moon Jae-in and Chinese Premier Li Keqiang met in Tokyo today for the first trilateral summit since 2015. The three leaders agreed to work together on denuclearization of North Korea. IN particular, Moon said that the actual steps to achieve it could be difficult. But the three countries will work together out the necessary steps needed. Li and Abe also oversaw the signing of a pact to set up a security hotline within 30 days.

Also, a Japanese official said that the leaders agreed to work on a free trade pact among the three countries. And, they will also work towards the proposed Regional Comprehensive Economic Partnership with Southeast Asian countries too.

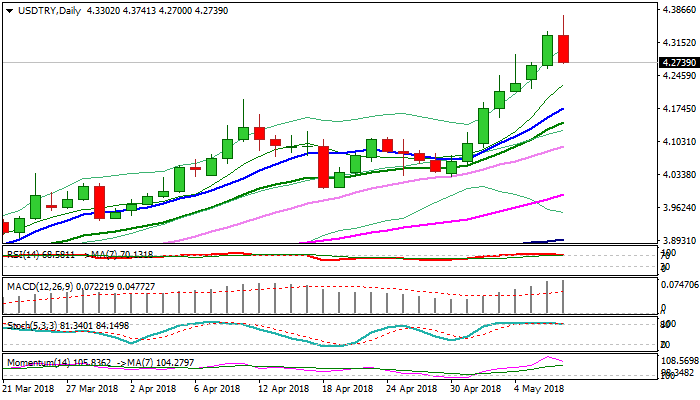

Turkish Lira Bounces From New Record Low On Signals The CBRT May Take An Extraordinary Action

The Turkish lira hit new record low at 4.3741 against US dollar on Wednesday, in fresh extension after decision of US President Trump to pull the US from international nuclear deal with Iran boosted dollar. Gains proved to be short lived as lira subsequently bounced on comments that Turkish President Erdogan would discuss about the currency with his economy team which raised hopes for an extraordinary tightening action from the central bank. The unscheduled meeting of Erdogan and the economic team is due today and may result in some new and unexpected steps from the central bank, which was so far unable to deal with double-digit inflation. Turkish lira bounced around ten figures in immediate reaction on the news and currently trading around 4.28 handle. Daily techs also started to generate bearish signals on RSI / slow stochastic reversal from overbought territory and momentum turned south after peaking earlier today. Technical signals need to be confirmed by the action of the central bank, or at least signals that the CBRT is on track to do some changes and stop recent sharp fall of lira. Extension and close below 4.2424 (Fibo 38.2% of 4.0294/4.3741 upleg) is needed to signal reversal and put bulls on hold. Stronger recovery could be signaled on lira's rally through rising 10SMA (4.1748). Conversely, mild reaction from the central bank would risk fresh weakness of Turkish lira.

Res: 4.3000, 4.3382, 4.3500, 4.3741

Sup: 4.2700, 4.2600, 4.2424, 4.2176

Oil Highest Since 2014 As US Pulls Out Of Iran Deal

It's been a relatively positive start to trading in Europe on Wednesday, with much of the attention falling on US President Donald Trump's decision to withdraw from the Iran nuclear deal.

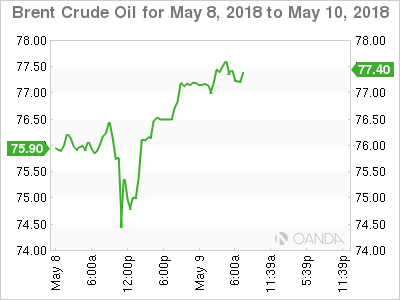

Oil is back trading at three and a half year highs this morning after Trump confirmed that the US will be withdrawing from the Iran nuclear deal and sanctions will be restored. The question now is how restrictive the sanctions will be on the Iranian economy and its ability to produce and export oil given that the UK, Germany, France, China and Russia remain committed to the deal.

Oil has been rallying for days in response to rumours that Trump would announce the withdrawal, which clearly suggests that traders believe the sanctions will further tighten global supply at a time when some of the world's largest producers have already significantly reduced inventories. There is clearly the potential for these countries to fill the void left by the sanctions but if it aids their cause then they'll likely opt against it.

The EIA inventory data will be of particular interest today given the attention that the oil market is already getting as a result of the sanctions. The numbers have been quite volatile for much of the year, following seven months of constant declines which brought the inventories back towards their five year average, as per the intentions of the deal between OPEC and some non-OPEC nations. The question now is how much further they'll go to lift prices.

US futures are currently around half a percentage point higher, with gains likely being driven by energy stocks which are leading the way in Europe currently. Brent and WTI crude are almost 3% up on the day so far which is naturally beneficial for oil and gas companies and is therefore contributing strongly to the gains. While this is providing near-term support for US indices, I wonder whether it will help in the longer-term with the US' decision to pull out potentially increasing geopolitical risk.

This comes at a time when stock markets already look quite vulnerable having failed to recover in any significant way from their lows. Despite the occasion positive days, the momentum looks very much with the bears right now and a break below this year's lows – which have been tested a few times now – could trigger further sell-offs.

Safe Havens Gain Little Despite Rising Iran-US Tensions, RBNZ Rate Decision Next

Here are the latest developments in global markets:

FOREX: Safe-haven currencies did not gain much after Trump announced the withdrawal of the US from the 2015 Iran nuclear deal and expressed his plans to impose stricter sanctions on the country. Although investors were worried that political tensions between Europe, the US, and the Middle East could escalate, they did not increase their stakes on safe-haven investments much. Instead, they remained optimistic on the dollar as they are widely expecting the Fed to proceed with further monetary tightening later this year. In notable movements, dollar/yen touched a one-week high of 109.80 (+0.55%), dollar/swissie hit a one-year high of 1.01 (+0.07%), while the dollar index reached a fresh 4 ½-month high of 93.41. The euro and the pound were on the back foot for another day in the face of a strengthening dollar, with euro/dollar and pound/dollar edging down to 1.1855 (-0.08%) and 1.3537 (-0.04%) respectively. Pound traders were also eagerly waiting for the BoE to cancel what was previously thought as a planned rate hike on Thursday. Dollar/loonie inched down to 1.2937 (-0.08%), as rising oil prices continued to underpin the commodity-linked loonie. Aussie/dollar remained near 11-month lows, last seen at 0.7439 (-0.15%) and kiwi/dollar continued to fluctuate around 0.6960, at near four-month troughs ahead of the RBNZ rate decision later today.

STOCKS: A boost in oil prices following Trump’s decision to leave the Iranian nuclear deal helped European stocks to open higher on Wednesday, with the pan-European STOXX 600 and the blue-chip STOXX 50 being up by 0.31% and 0.58% respectively at 0900 GMT, as energy stocks were on the rise. The German DAX 30 rose by 0.21%, with the German industrial giant Siemens leading the gains after the company raised its full-year earnings per share outlook. The French CAC 40 remained flat as shares of Iran-exposed car makers such as Renault and Peugeot fell. The Italian FTSE MIB moved up by 0.80%, while the British FTSE 100 gained 0.61%. Futures tracking US stock indices were in the green, pointing to a positive open.

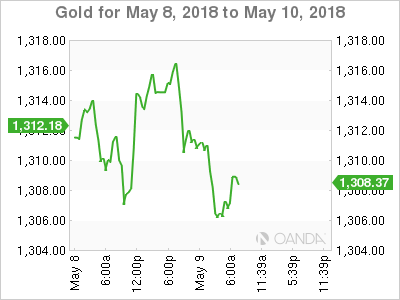

COMMODITIES: Oil prices hit fresh 3 ½-year highs during the early European session on fears that the US President would impose the “highest level of sanctions” against Iran, the third largest exporter within OPEC. Under the expectation that sanctions would tighten oil supply even further, WTI crude touched a new top at $71.17 per barrel before it slipped to $70.96 (+2.75%), while Brent hit a new peak at $77.20/barrel before it fell to $76.82 (+2.61%). In precious metals, gold extended losses towards $1,307.52/ounce (-0.50%).

Day Ahead: US delivers PPI data; RBNZ decision in focus

Next on the day’s agenda, the US Bureau of Labor Statistics will release figures on producer prices at 1230 GMT, with analysts projecting the PPI for the month of April to inch down by 0.1 percentage points to 0.2% m/m. Meanwhile, the core monthly PPI is anticipated to reflect a slowdown in the pace of growth, standing at 0.2% m/m as well. Year-on-year, the headline PPI figure is forecasted to decline by 0.2% percentage points to 2.8% in April from 3.0% in the previous month.

In Canada, a report on the growth of building permits in March will be available at 1230 GMT, with analysts predicting the gauge to tick higher to 2.0% from a contraction of 2.6% in the preceding month.

In energy markets, investors will look at the weekly EIA report on US crude oil inventories after Trump’s decision to leave the 2015 Iran nuclear accord yesterday added substantial gains to crude oil prices. According to forecasts, US crude inventories are expected to fall by 0.719 million barrels in the week ending May 4 compared to a rise of 6.218m in the prior week. It would be interesting to see whether oil prices will reach fresh tops today in case the numbers unexpectedly reflect a larger decline in oil inventories or whether they will pull back in the event of an upward surprise.

In terms of public appearances, Atlanta Fed President Raphael Bostic will be talking about the US economic outlook and monetary policy at 1715 GMT.

As for central bank meetings, the Reserve Bank of New Zealand (RBNZ) will announce its rate decision later in the day, at 2100 GMT. Policymakers are widely anticipated to keep interest rates unchanged at 1.75% and as such, attention will turn to the phrasing of the accompanying statement as well as the updated economic forecasts.

U.S Dollar Rises On Higher Yields, EM Pairs Suffer

Wednesday May 9: Five things the markets are talking about

The threat of an increase in geopolitical tension in the Middle East is weighing on global sentiment just as concern spread over the implications of higher U.S Treasury yields and a stronger dollar.

Overnight, the 'big' dollar has rallied for a fourth consecutive session, pressurizing emerging-markets pairs and mudding the picture for commodities as investors digest President Trump's announcement yesterday to walk away from the Iran nuclear deal.

Elsewhere, U.S bond yields again have penetrated the psychological +3% handle as the market prepares to take down another +$73B of new U.S debt product this week.

Global equities have produced mixed results, while most metals are trading under pressure.

1. Stocks 'mixed bag'

In Japan, stocks fell overnight as global tensions flared after President Trump pulled the U.S out of the nuclear deal with Iran. The Nikkei ended down -0.4%, while the broader Topix was down -0.3%.

Down-under, Aussie shares ended slightly higher on Wednesday, as gains across a number of sectors following an optimistic budget were offset by financials. The S&P/ASX 200 index rose +0.26%. In S. Korea, the Kospi fell -0.24%.

In Hong Kong, stocks rallied, led by the energy sector after Trump pulled out of the Iran nuclear deal, sparking fears about global oil supplies. The Hang Seng index rose +0.4%, while the China Enterprises Index gained +0.3%.

In China, equities ended a tad lower overnight as losses in the financial and property shares outweighed gains in energy stocks. The blue-chip CSI300 index fell -0.2%, while the Shanghai Composite Index dipped -0.1%.

In Europe, regional indices trade higher across the board, trending upwards on the back of rising U.S futures following earnings and geopolitical events.

U.S stocks are set to open in the 'black' (+0.5%).

Indices: Stoxx600 +0.3% at 391.2, FTSE +0.6% at 7608, DAX +0.3% at 12953, CAC-40 flat at 5522, IBEX-35 flat at 10167, FTSE MIB +0.8% at 24328, SMI +0.1% at 8949, S&P 500 Futures -+0.5%

2. Oil jumps to highest since 2014 after U.S. quits Iran deal, gold lower

Oil prices have rallied more than +3% overnight, hitting a four-year high, after the U.S walked away from the Iran nuclear deal and announced the “highest level” of sanctions against the OPEC member.

Brent crude oil is trading at its highest in three-years at +$77.20 a barrel. The benchmark contract was up +$2.15 a barrel, or more than +2.8%. U.S light crude is up +$1.90 a barrel, or almost +2.9%.

Note: In China, the biggest single buyer of Iranian oil, Shanghai crude futures hit their strongest since they were launched in late March.

Iran is the third-biggest exporter of crude within OPEC, behind Saudi Arabia and Iraq. Walking away from the nuclear deal means that the U.S will re-impose sanctions against Iran after 180 days.

The oil supply/demand is somewhat currently 'balanced' and it could turn to a complete supply shortage. Nevertheless, Saudi Arabia this morning said it would work with other producers to lessen the impact of any shortage in crude supplies.

Note: Saudi Arabia has been leading efforts since last year to withhold production to prop up prices.

Ahead of the U.S open, gold prices are trading under pressure, atop of their weekly lows, as the 'big' dollar strengthened after U.S's decision out of the Iran nuclear deal boosted energy prices and pushed Treasury yields higher. Trump said he would reimpose U.S economic sanctions on Iran that had been lifted under the 2015 agreement.

Spot gold has fallen -0.65% to +$1,305.16 an ounce, its lowest since May 3, while U.S gold futures for June delivery are down -0.6% at +$1,305.70 per ounce.

3. U.S yields back up to old territory

Stateside, today brings with it a +$25B auction of 10-year U.S notes and the market is waiting to see if the new bonds will carry a +3 % coupon for the first time in nearly seven-years.

Currently, the yield on U.S 10-year Treasuries has climbed +3 bps to +3.00% in the overnight session, the highest in two-weeks on the biggest increase in almost three weeks.

Elsewhere, in Germany, the 10-year Bund yield has climbed +1 bps to +0.58%, the highest in a week, while in the U.K, the 10-year Gilt yield has increased +2 bps to +1.444%, the highest in almost two-weeks.

In Sweden, Norway and Hungry, CPI data this morning came roughly in-line with expectations and any concerns of “prolong low inflation” seem to be abating.

4. Turkey's CBRT makes its move

TRY ($4.2858) has reversed its earlier losses outright after their central bank (CBRT) this morning took additional liquidity measures in a move to prop up the currency. The CBRT has increased the daily amount of currency swap auctions from +$1.25B to +$1.5B. The sale position of forward foreign exchange auctions may increase from $5.3 billion to $7.1 billion by the end of June, the central bank said. President Erdogan would hold a meeting on exchange rates.

Note: The record high USD/TRY print was a tad above $4.37.

In Sweden, the krona (+0.80% to $8.7528) has rallied after April inflation data came in line with market expectations, up +0.4% m/m, and higher than last month's +0.3% rise. EUR/SEK has fallen to a two-week low of €10.4102 from around €10.4635 beforehand.

Note: The krona lost ground between late January and early May after the Riksbank twice postponed a first rate increase in years due to the fact that the underlying inflation trend had turned lower.

Elsewhere, the Bank of England (BoE) could help boost the pound (£1.3531) if it raises interest rates tomorrow. However, the central bank has communicated before that a rate rise is not a given, which has led the fixed income market to price out a May rate increase. The consensus is for the BoE to stand pat, but most believe that a summer hike is in the works.

Similar to the Argentinian peso, Indonesia's rupiah has fallen to a fresh 29-month low on worries about capital outflows from emerging markets.

Note: Argentina's reliance on U.S dollar funding, coupled with the depreciation of its own currency is sending the country in to the all-too-familiar direction: financial turmoil.

5. French Industrial Production fell unexpectedly

Data this morning from France's official statistics agency INSEE showed that French industrial production fell unexpectedly in March, reflecting a sharp manufacturing drop in the mining, energy and utilities industries.

INSEE said industrial production fell by -0.4% in March m/m, after rising +1.1% in February. The figure for the previous month had been revised down from a preliminary reading of +1.2%.

Note: Market consensus was expecting a +0.4% rise, with estimates rising from -1.0% to +1.5%.

DAX Shrugs Off Trump Bombshell On Iran Nuclear Deal

The DAX index remains subdued in the Wednesday session, after showing little movement on Tuesday. Currently, the DAX is at 12,916 points, up 0.03% on the day. It’s a quiet day on the release front, with no major indicators in the eurozone. On Wednesday, the ECB releases an economic bulletin, and the US will publish consumer inflation reports.

Germany has posted some soft numbers recently, which could have major ramifications for ECB fiscal policy. The ECB cut its stimulus package at the start of the year from EUR 60 billion to 30 billion, while at the same time it extended the program to September. However, soft eurozone numbers, especially in Germany, have raised concerns that the bank may decide to again extend stimulus into 2019. German Factory Orders posted a second decline in the past three months, and the most recent PMIs in the services and manufacturing sectors also headed lower. On Tuesday, German indicators bounced back after a weak start to the week. Industrial Production climbed 1.0%, beating the estimate of 0.8% and ending a nasty streak of three straight declines. As well, Germany posted a trade surplus of EUR 22.0 billion, easily beating the estimate of EUR 19.9 billion. This marked a 4-month high.

European stock markets are showing a muted reaction to President Trump’s dramatic speech on Tuesday. Trump announced that the US would withdraw from the Iran nuclear deal. Trump blasted the agreement and said that the US would impose stiff sanctions on Iran. However, Britain, France and Germany have said they plan to remain in the deal, and will be holding a high-level meeting with Iranian leaders on how the agreement can be salvaged. With the US acknowledging that the White House does not have a ‘Plan B’, it’s unclear what happens next. Meanwhile, tensions between Israel and Iran remain high, after several Israeli airstrikes in Syria caused Iranian casualties. Any confrontation between the two could shake up the markets.

EUR/USD – Lack Of Fundamentals Leaves Euro Trading Sideways

EUR/USD is showing little movement in the Wednesday session. Currently, the pair is trading at 1.1858, down 0.07% on the day. In economic news, there are no major events in the eurozone. The US will release key inflation reports, with PPI and Core PPI both expected to drop from 0.3% to 0.2%. On Wednesday, the ECB releases an economic bulletin, and the US will publish consumer inflation reports.

The currency markets are not showing much movement after President Trump’s dramatic speech on Tuesday. Trump announced that the US would withdraw from the Iran nuclear deal. Trump blasted the agreement and said that the US would impose stiff sanctions on Iran. However, Britain, France and Germany have said they plan to remain in the deal, and will be holding a high-level meeting with Iranian leaders on how the agreement can be salvaged. With the US acknowledging that the White House does not have a ‘Plan B’, it’s unclear what happens next. Meanwhile, tensions between Israel and Iran are at a fever pitch, and any confrontation between the two could shake up the markets.

Germany has posted some soft numbers recently, which could have major ramifications for ECB fiscal policy. The ECB cut its stimulus package at the start of the year from EUR 60 billion to 30 billion, while at the same time it extended the program to September. However, soft eurozone numbers, especially in Germany, have raised concerns that the bank may decide to again extend stimulus into 2019. German Factory Orders posted a second decline in the past three months, and the most recent PMIs in the services and manufacturing sectors also headed lower. On Tuesday, German indicators bounced back after a weak start to the week. Industrial Production climbed 1.0%, beating the estimate of 0.8% and ending a nasty streak of three straight declines. As well, Germany posted a trade surplus of EUR 22.0 billion, easily beating the estimate of EUR 19.9 billion. This marked a 4-month high.

The Federal Reserve’s newest regional Fed president, Thomas Barkin, delivered a major speech on Monday, and his tone was decidedly upbeat. Barkin said that the economy is “remarkably strong: above-trend growth, low unemployment, inflation at target”. Barkin added that although the labor market is strong, it is not causing pressure on wages, but low unemployment should lead to an increase in inflationary pressures. As for upcoming rate increases, Barkin was careful to remain mum on how many rate hikes he expects this year. The Fed raised rates in March by a quarter-point and continues to forecast two additional increases this year. However, some policymakers are calling for three more hikes, given the strong health of the US economy.

It Would Be A Mistake To Be Overly Bullish On Oil

- France, Germany and the U.K. - all implored Trump to remain in the landmark deal

- A mammoth amount of oil exports finds its way to countries like China

- Iranian oil production is bound to go down under the current situation

- Lower supply would be taken by other members

Trump is out of the Iran nuclear deal, Trump is in: confusing headlines created unnecessary volatility in the oil market yesterday. Algorithms lost control of things, there was no clear message until President Trump took things in hand and announced that he is undoing all the hard work done to stop Iran from becoming a nuclear power.

His decision to pull out of the Iranian nuclear deal could have much larger widespread implications than only an increase in the oil price. His decision would not only increase Iranian ambitions to become a nuclear power, but also damages the US relationship with its allies. France, Germany and the U.K. - all implored Trump to remain in the landmark deal forged under Barack Obama’s administration. The French president has already shown his frustration yesterday by saying that all the three allies regret the US decision to leave the JCPOA.

Trump is pushing the limits of his allies’ restraint. They are already sour over recent trade tariffs, and you can only ruffle feathers for so long before there is pushback. When the trade tariffs (25 percent on foreign steel and 10 percent on foreign aluminium) were introduced, the European Commissioner, Jean Claude Juncker gave a strong response and warned the US, in so many words, to stop pushing it before European patience ran out.

Iran has an important role to play here: it is the third biggest oil producer of OPEC cartel, and leading up to this event, we have witnessed panic amidst traders who pushed the price of oil higher. OPEC members had to work day and night to balance the supply and demand equation, and it is under threat now because other nations in OPEC could use this situation as an excuse to produce higher quantity than they should be producing. The Saudis, to take one example, want the oil price to reach $80b/pd and only a lower supply could help them to achieve that.

Russia, China, Turkey and EU

Currently, Iran's oil production stands at 4 million barrels per day. The country’s production took a nose dive from 3.8 million barrels per day in April 2010, to 2.5 million in May 2013 due to US and European sanctions. This time we are unlikely to have that effect, as only US sanctions are presently likely to be restored. A mammoth amount of oil exports finds its way to countries like China, India, Korea, Turkey, and Europe where Iran has strong relationships. China, Russia and Turkey all have not only strong ties with Iran and contune to respect its compliance with the nuclear agreement; the EU is on the same page when it comes to this argument. Therefore, the prospects of cast supply cut are next to none.

However, Trump vowed yesterday that he will institute even stronger economic sanctions on Iran and if the full force of previous sanctions is brought to bear it would make it incredibly difficult for companies to stay in business with Tehran. Iran’s aim was to raise $200 billion of investment to help its energy sector, but due to the continued pressure from Trump administration, oil firms have been very slow and wary in conducting business in Iran. Out of all the oil companies, it was a French company - Total SA - which returned to Iran with meaningful investment. Although, with the current situation, Russian oil companies could benefit from the situation and build their presence in a more prominent way. Hence, the equation of oil production for Iran is a little unknown here.

Spare Capacity

Iranian oil production is bound to go down under the current situation and questions remain over which country would use its spare capacity to make up for the shortfall. OPEC has curbed its production to 1.8 million barrels per day, and Saudi Arabia is the largest oil producer. At the same time, it is in the Saudis’ interest to let the supply shrink because that would likely bring the oil price to their target level. So, unless a spat breaks out – which is likely, a one thing the OPEC members are good at is fighting for their oil share - oil prices may continue to rise.

Let's say that Iran’s oil production does go down by half a million barrel per day, which would impact the price more positively – so, even with lower production, Iran may not be in such a bad position because of the higher oil price. Most importantly, Iran learned how to work with sanctions and the country is in a much stronger position politically and economically to work with other major players in the region to find a solution which fits all. Hence, there may be no point in becoming a massive bull on oil (I do not see any bigger impact on the oil supply), or hold a massive bearish position on Iranian currency or the equity market.