Sample Category Title

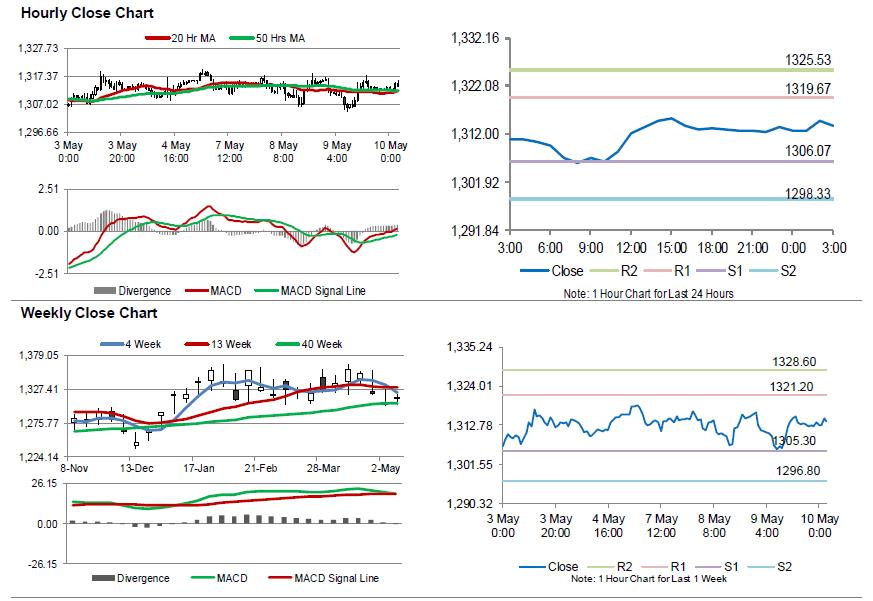

Gold: Yellow Metal Reverses Its Losses In The Asian Session

For the 24 hours to 23:00 GMT, Gold declined 0.26% against the USD and closed at USD1312.40 per ounce, amid strength in the greenback.

In the Asian session, at GMT0300, the pair is trading at 1313.80, with gold trading 0.11% higher against the USD from yesterday’s close.

The pair is expected to find support at 1306.07, and a fall through could take it to the next support level of 1298.33. The pair is expected to find its first resistance at 1319.67, and a rise through could take it to the next resistance level of 1325.53.

The yellow metal is trading above its 20 Hr and 50 Hr moving averages.

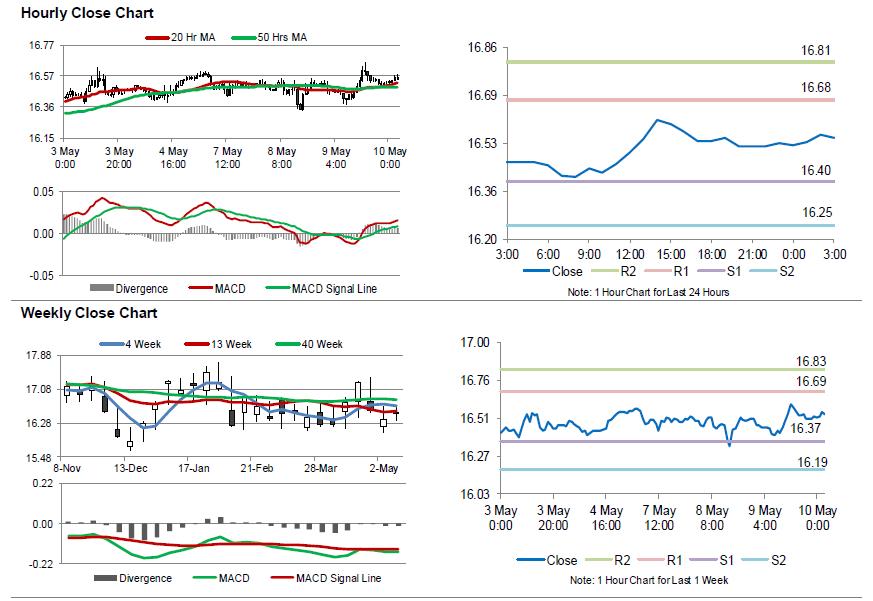

Silver: White Metal Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, Silver rose 0.06% against the USD and closed at USD16.53 per ounce.

In the Asian session, at GMT0300, the pair is trading at 16.55, with silver trading 0.12% higher against the USD from yesterday’s close.

The pair is expected to find support at 16.40, and a fall through could take it to the next support level of 16.25. The pair is expected to find its first resistance at 16.68, and a rise through could take it to the next resistance level of 16.81.

The white metal is trading above its 20 Hr and 50 Hr moving averages.

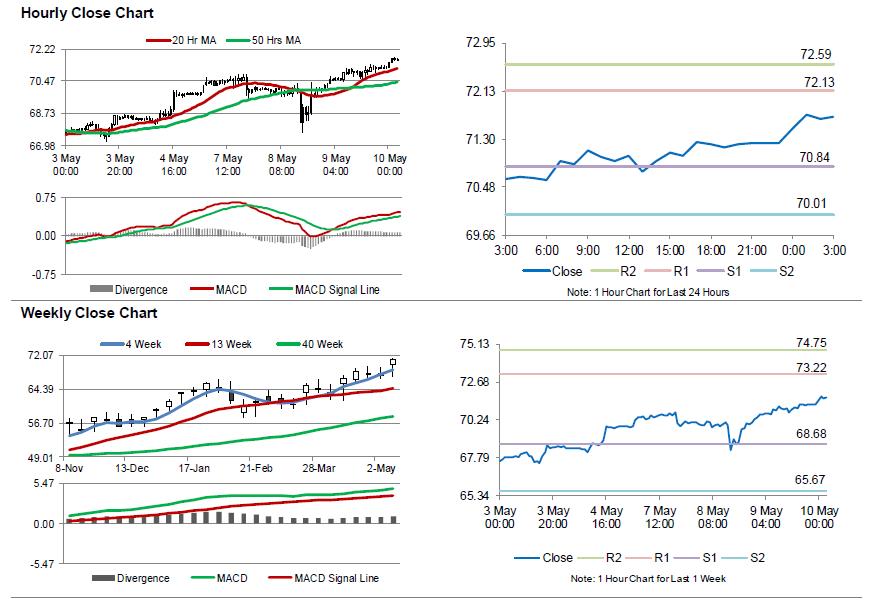

Crude Oil: Oil Extends Gains In The Morning Session

For the 24 hours to 23:00 GMT, Crude Oil rose 1.61% against the USD and closed at USD71.23 per barrel, extending its previous session gains, after the US decided to quit a nuclear deal with Iran.

Gains in crude prices were boosted further, after the Energy Information Administration (EIA) reported that US crude oil inventories fell by 2.2 million barrels to 433.8 million barrels in the week ended 04 May.

In the Asian session, at GMT0300, the pair is trading at 71.68, with oil trading 0.63% higher against the USD from yesterday’s close.

The pair is expected to find support at 70.84, and a fall through could take it to the next support level of 70.01. The pair is expected to find its first resistance at 72.13, and a rise through could take it to the next resistance level of 72.59.

Crude oil is trading above its 20 Hr and 50 Hr moving averages.

BoJ Kuroda: Inflation expectations may not rise smoothly if there is strong uncertainty

BoJ Governor Haruhiko Kuroda said today that the central could debate stimulus exit if policy makers see increasing chance of hitting the 2% inflation target. He noted that "when the possibility of achieving our price target heightens, conditions of an exit would fall into place. The BOJ's policy board could then discuss conditions for an exit."

However, he emphasized that "With achievement of our price target still distant, it will create market confusion if we explain specific means and timing of an exit (from the easy policy) now." Also, he warned that "if there is strong uncertainty about future growth, firms will hesitate to raise wages." He added that "even if firms' wage- and price-setting stance becomes more proactive, inflation expectations may not rise smoothly."

RBNZ Turns Dovish, Downgrading Growth and CPI Forecasts

RBNZ left the OCR unchanged at 1.75% in May. The message delivered by the central bank came in slightly more dovish than expected, sending NZDUSD to a fresh 5-month low. In his first meeting in the capacity of the RBNZ Governor, Adrian Orr made some changes in the policy statement, of which the reference that “the direction of our next move is equally balanced, up or down. Only time and events will tell” has caught the most attention.

Policymakers remained positive over the economic developments, noting that “growth and employment in New Zealand remain robust, near their sustainable levels”. The central bank attributed the recent growth in demand to the unprecedented increase in employment. It acknowledged the rise in number of willing workers and participation of net immigration in the labor market. Yet, the central bank slightly lowered its GDP growth forecast to +3.3% for end-2018, down from +3.4% projected previously, and to +3.2% for end-2019, down from +3.5% prior. Growth would then slow further to +3% by end-2020, unchanged from previous forecast.

Inflation remained subdued, staying below the +2% mid-point of the target, as a result of “recent low food and import price inflation” and “subdued wage pressures”. RBNZ revised lower its inflation forecasts slight for coming quarters slightly. It does not expect CPI to reach 2% until 4Q20, compared with 3Q20 prior.

On the monetary policy outlook, the members expect the policy rate would stay at “expansionary level for a considerable period of time”, in order to achieve the goal of maximum and sustainable employment, and low and stable inflation. As mentioned above, RBNZ indicated “the direction of our next move is equally balanced, up or down”. When we compared it to the reference in March that “Monetary policy remains easy in the advanced economies but is gradually becoming less stimulatory”, the current tone is obviously more dovish. The latest projections signal that while the next move will be a rate hike, it should not occur before late-2019. The path thereafter would also be gradual.

Market Morning Briefing: Euro Rose Towards 1.1897

STOCKS

Dow (24542.54, +0.75%) has finally closed above 24500, breaking above the near term range. While the index continues to rise, it could head towards 25000 in the next 1-2 sessions.

Dax (12943.06, +0.24%) is in an uptrend and is headed towards 13200 in the near term.

Nikkei (22440.44, +0.14%) is trapped in the 22400-22600 region. It is difficult to say if this is a short pause before a sharp upmove. Immediate resistance near 22600 is holding for now. There are equal chances of the index moving on either side.

Shanghai (3168.81, +0.31%) looks bullish in the near term while above 3150 and could test 3200-3250 soon. Near term looks bullish.

Nifty (10741.70, +0.22%) could have some scope of testing upside limits of 10800-10850 levels in the near term. Support at 10600 is holding well. Sensex (35319.35, +0.29%) is likely to move up towards 35500-35750 levels.

COMMODITIES

US Crude production has risen to 10.7mln barrels/day from 10.62 mln a week earlier (EIA report). The EIA has now raised its US crude production outlook to rise by 1.14mln barrels/day for the next year (revised from the earlier projection of 750,000 bpd).

EIA's estimate of a reduction in US crude inventory by 2.2mln barrels last week has aided to a rise in the crude prices. Brent (77.73) and Nymex WTI (71.68) are trading just below resistances near 78 and 72 respectively. If WTI breaks above 72, it could target 74 in the medium term while a rejection would see a short dip to 70-69 again. Brent could also come down to 76 if 78 holds, else a sharp upmove is likely in the near to medium term.

Gold (1314, +0.08%) could test 1320 before again dipping back to 1300. For now Gold could trade sideways in the range of 1325-1300. A break below 1300, if seen would open up chances of testing 1280 on the downside.

Copper (3.0720, +0.4%) may test 3.10-3.12 on the upside before again dipping back to 3.07.

FOREX

Dollar index (92.99) saw a slight dip yesterday from levels near 93.3-93.4 towards 92.8-92.9. It should rise back up towards 93.5 again by tomorrow (maybe after seeing another dip to 92.75 today). As we mentioned yesterday, the Dollar Index (on the 1 hour chart) could be in the last leg of its 5 wave upmove from 89.23 (17th Apr onwards). This last leg could possibly end near 93.70-94.50. Our projection of the Dollar Index coming close to its medium term target of 94-95 in the next 1-2 weeks might well come out to be true. (the level 94-95 corresponds to the 5th wave starting point of the downmove since Dec ’16).

Euro (1.1863) rose towards 1.1897 yesterday and also saw a low near 1.1823. It could move up again today and test 1.19. However, after that we expect it to dip lower (and possibly test 1.18) by this week’s end / early next week. Repeating yesterday’s comment: corresponding to the Dollar Index’s upmove towards 93.70-94.50, the Euro could have its current downmove restricted till 1.1775-1.1655, after which it could again start rising after a couple of weeks. If the Dollar Index tests 95, Euro could simultaneously test 1.160-1.158.

Dollar Yen (109.72) has continued rising from support (near 108.75) on the upward trendline on daily candles and has seen a high near 109.99. It could be in the last leg of the 5 wave upmove starting from near 104.6 in March end. This current upmove could take it higher towards 110.5-111.0 (earlier max mentioned as 110.75) in the near term. The broader uptrend looks capped till 110.50-111.0, after which Dollar Yen could turn bearish.

Euro Yen (130.17) as per our expectation is currently respecting support on weekly candles near 129.3-129.2 and might continue doing so for a few days till the Dollar Yen continues its upmove towards 110.5-111.0. After that, as the Dollar Yen turns bearish, we could see Euro Yen break below 129.

Pound (1.3562): As per our expectation, Pound again rose above 1.354-1.355 yesterday to see a high near 1.36 (1.3607). It is currently trading lower but could possibly again test higher levels near 1.36-1.37 in the next couple of days before moving lower. If it breaks below 1.352, it could then move down quickly towards 1.325.

Dollar Rupee (67.265): Dollar Rupee may test support near 67.12, upside is open towards 67.60/70.

INTEREST RATES

The US CPI data release later today has assumed a lot of significance for the US 10 year yield. Analysts expect a 2.5% y-o-y increase in Headline inflation and a 2.2% y-o-y increase in core inflation. If the datat release meets or surpasses these expectations, it could well act as a trigger for a bond selloff, which could thereby take the 10 Year yield beyond 3% decisively. The 10 year yield has tested 3% twice over the past few days but the psychologically important level has continued acting as a resistance.

Yesterday, Trump’s withdrawal from the Iran deal took crude prices higher and also took the 10 Year yield towards 3%. However, it wasn’t enough to bring about a decisive breach of 3%.

The Fed in their last week’s meeting had expressed some hawkishness in its stance. In the near term, we are expecting US yields to start rising towards their medium term targets (see below) as the June Fed meeting comes closer (where a rate hike is widely expected).

The medium term targets for US yields in our Apr ’18 US Treasury report (available on demand) are as follows: 3.2%-3.3% (10 Year), 3.4%-3.5% (30 Year), 3.15% (5 Year) and 2.75% (2 Year). A breach of the 3% level by the 10 year yield would be vital for these targets to be achieved by June. A rate hike is expected in the June Fed meeting, which might start getting factored later this month and could henceforth lead to a rally in yields towards these medium term targets. We also expect some more yield curve flattening in the next month followed by steepening after that, as yields bounce from long term supports.

US 10 Yr Yield (2.99%), 30 Yr (3.15%), 5 Yr (2.83%), 2 Yr (2.53%):

The 2 year yield saw a high near 2.55% and could continue its upmove towards our medium target of 2.75%. We expect this level to be tested later this month or in mid June.

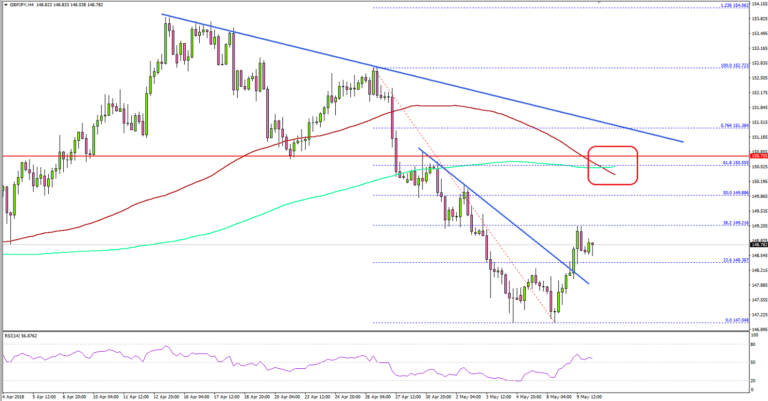

GBP/JPY Could Gain Further, BOE’s Rate Decision Next

Key Highlights

- The British Pound found support near 147.00 and recovered sharply against the Japanese Yen.

- There was a break above a key bearish trend line with resistance at 148.20 on the 4-hour chart of GBP/JPY.

- Japan's Current Account posted a trade surplus of ¥3,122.3B in March 2018, compared with the ¥3,009.2B forecast.

- Today, the BOE Interest Rate Decision is lined up, and the central bank is likely to keep rates at 0.5%.

GBPJPY Technical Analysis

The British Pound found a strong support near 147.00 after a major decline against the Japanese Yen. The GBP/JPY pair is currently correcting higher and is placed nicely above 148.40.

Looking at the 4-hours chart, the pair started a decent upward move and broke the 23.6% Fib retracement level of the last decline from the 152.72 high to 147.04 low.

More importantly, there was a break above a key bearish trend line with resistance at 148.20 on the same chart. To the topside, there are many hurdles for buyers around the 150.00 and 150.50 levels.

Both the 100 (red) and 200 (green) simple moving averages are positioned near 150.50. Moreover, the 61.8% Fib retracement level of the last decline from the 152.72 high to 147.04 low is at 150.55. Therefore, if the pair continues to move higher, it is likely to face sellers near the 150.50 level.

An intermediate resistance is around 150.00 and the 50% Fib retracement level of the last decline from the 152.72 high to 147.04 low. On the downside, the 148.40 level is a decent support, followed by 148.00.

Today, there are many high risk events lined up in the UK and US, including BOE Interest Rate Decision, UK's Production report, US Initial Jobless Claims and US CPI. These events are likely to impact the market, and pairs like EUR/USD, GBP/USD, USD/JPY and NZD/USD may become volatile.

Economic Releases to Watch Today

- UK Industrial Production for March 2018 (MoM) – Forecast +0.2%, versus +0.1% previous.

- UK Manufacturing Production for March 2018 (MoM) – Forecast -0.2%, versus -0.2% previous.

- UK Trade Balance non-EU for March 2018 – Forecast £-3.34B, versus £-2.24B previous.

- BoE Interest Rate Decision – Forecast 0.50%, versus 0.50% previous.

- US Initial Jobless Claims – Forecast 218K, versus 211K previous.

- US Consumer Price Index April 2018 (MoM) – Forecast +0.3%, versus -0.1% previous.

- US Consumer Price Index April 2018 (YoY) – Forecast +2.5%, versus +2.4% previous.

- US Consumer Price Index Ex Food & Energy April 2018 (YoY) – Forecast +2.2%, versus +2.1% previous.

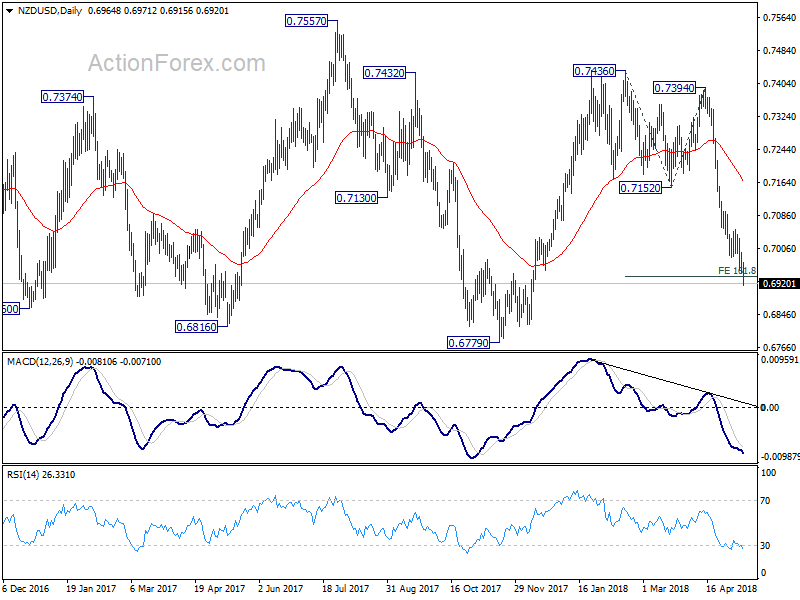

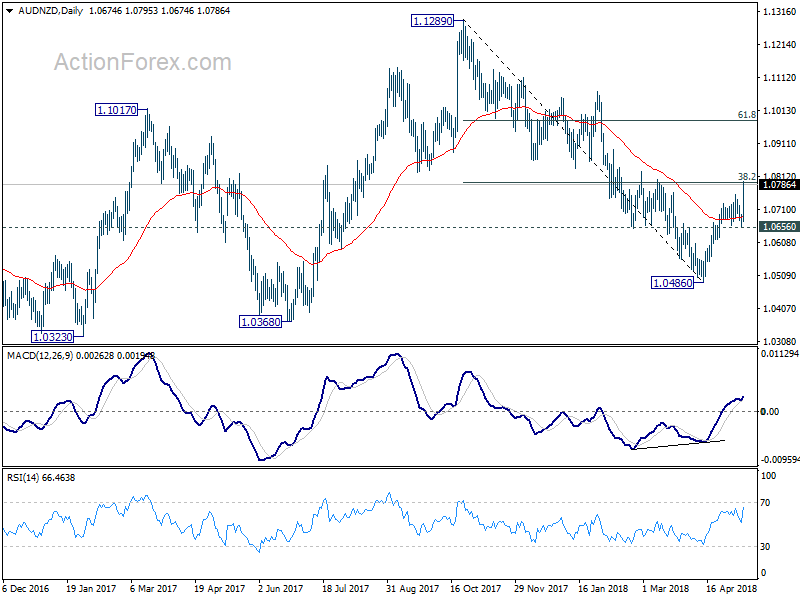

A look at NZDUSD and AUDNZD after post RBNZ selloff

The RBNZ rate decision turned out to be much more dovish than expected. Governor Adrian Orr's statement indicated there is no rush to lift interest rate. And the central bank downgraded inflation forecast for 2019 and 2020. The downgrade of 2019 and 2020 GDP forecasts was quite significant too. RBNZ is now expected to stand pat at least until mid-2019.

Given that, NZD tumbled broadly after the release. NZD/USD drops to as low as 0.6915 so far. 161.8% projection of 0.7436 to 0.7152 from 0.7394 at 0.6934 is firmly taken out. And our counter trend long position mentioned here will likely be stopped out with a loss. NZD/USD would now target 0.6779 low after sustaining below 0.69 handle.

AUD/NZD surges to as high as 1.0795 and hit 38.2% retracement of 1.1289 to 1.0486 at 1.0793. Based on current momentum, rise from 1.0486 will now likely extend to 61.8% retracement at 1.0982 and above. As AUD/NZD is, after all, staying in long term range trading, strong resistance could be seen above 1.0982 to bring reversal to extend the range pattern.

RBNZ downgraded both GDP growth and inflation forecasts

The overall RBNZ monetary policy decision is rather dovish. OCR is left unchanged at 1.75% for a 19th straight month as widely expected. Governor Adrian Orr noted in the statement that growth and employment remain "robust" and near their "sustainable levels". But CPI remains below the 2% mid-point of target. And, the best way to see inflation moving back to target would be "to keep the OCR [overnight cash rate] at this expansionary level for a considerable period of time". RBNZ is clearly is no rush to raise interest rates.

Adding to that, the GDP growth and inflation forecasts were also downgraded for the period ahead. The downgrade in GDP forecasts were quite significant in 2019 and 2020. CPI is still projected to hit 2.0% target 2021 but is expected to be lower in both 2019 and 2029.

GDP is projected to grow 2.8% (2018), 3.1% (2019), 3.3% (2020), 3.1% (2021). Back in February, GDP projections were 2.9% (2018), 3.3% (2019), 3.5% (2020), 3.1% (2021).

CPI is projected to be at 1.1% (2018, 1.6% (2019), 1.8% (2020), 2.0% (2021). Back in February, CPI projections were 1.1% (2018), 1.7% (2019), 1.8% (2020), 2.0% (2021).

This is May's forecast summary.

This is February's forecast summary.

And here is the press conference:

And here is the press conference:

https://www.youtube.com/watch?v=eobtG1NneD4

(RBNZ) Official Cash Rate unchanged at 1.75 percent

Statement by Reserve Bank Governor Adrian Orr:

Tena koutou, katoa, welcome all.

The Official Cash Rate (OCR) will remain at 1.75 percent for some time to come. The direction of our next move is equally balanced, up or down. Only time and events will tell.

Economic growth and employment in New Zealand remain robust, near their sustainable levels. However, consumer price inflation remains below the 2 percent mid-point of our target due, in part, to recent low food and import price inflation, and subdued wage pressures.

The recent growth in demand has been delivered by an unprecedented increase in employment. The number of willing workers continues to rise, especially with more female and older workers choosing to participate. Likewise net immigration has added to the supply of labour, and the demand for goods, services, and accommodation.

Ahead, global economic growth is forecast to continue supporting demand for New Zealand's products and services. Global inflation pressures are expected to rise but remain contained.

At home, ongoing spending and investment, by both households and government, is expected to support economic growth and employment demand. Business investment should also increase due to emerging capacity constraints.

The emerging capacity constraints are projected to see New Zealand's consumer price inflation gradually rise to our 2 percent annual target.

To best ensure this outcome, we expect to keep the OCR at this expansionary level for a considerable period of time. This is the best contribution we can make, at this moment, to maximising sustainable employment and maintaining low and stable inflation.

Our economic projections, assumptions, and key risks and uncertainties, are elaborated on fully in our Monetary Policy Statement.

Meitaki, thanks

Read the Monetary Policy Statement.