Sample Category Title

UK CPI release given more significance after Brexit transition deal

According to a Bloomberg survey, majority of economists expected BoE to vote 9-0 to keep interest rate unchanged at 0.50% later this week on Thursday. And, 54% of economists expected BoE to hike interest rate in May. That's a slight adjustment from 51% at prior survey. However, the data was taken as of March 19. And it's unsure how much regarding the Brexit transition deal was taken into consideration. And that could only be reflected in the next survey.

The BoE rate decision this Thursday becomes lively as the transition deal is done. UK CPI data to be released today will be the first key factor. Headline CPI is expected to slow from 3.0% yoy to 2.8% yoy in February. Core CPI is expected to slow from 2.7% yoy to 2.5% yoy.

On the one hand, the deal should give BoE policymakers some comfort to restart lifting interest rate from the current ultra low level at 0.50%. On the other hand, any upside surprise in today's inflation data would indeed give some pressure for BoE to act again.

And for the meeting, ahead, while BoE is still expected to stand pat, the statement could turn more relaxed and optimistic given that the Brexit picture is slightly clearer. And more importantly hawks like Ian McCafferty and Michael Saunders might come back to vote for rate hike.

Little surprise from RBA minutes

The RBA minutes for the March contained little surprise. Policymakers remained concerned about the soft inflation outlook, noting faster wage growth is needed to assure a stronger and more sustainable improvement on inflation. As suggested in the minutes, "employment had grown strongly and the unemployment rate had fallen over the preceding year. However, the improvement in overall conditions had not yet translated into a definitive pick-up in wages growth, which remained low". It added that "further progress on these goals [reducing the unemployment rate and bringing inflation closer to target] was expected over the period ahead, but this process was likely to be gradual".

Trump to announce USD 60b tariff against China on Friday, China Premier Li pledges to open market

It's known that Trump is preparing to impose a package of USD 60b in tariffs against China. It's reported that the package would apply to over 100 products. These products are believed by Trump to use trade secretes stolen from US companies, or forced to hand over in exchange for market access. The theme appears to be consistent with Section 301 intellectual property theft investigation and actions. But no one knows how relevant is that until there a a published list of products. Trump is planning to announce the action by Friday.

China Premier Li Keqiang said today after a press conference that there is no forced transfer of technology. But he pledged that China will better protect intellectually property. Also, China will further open up the economy, lower import tariffs and allow foreign and domestic companies to compete on equal ground. China commerce ministry said that there is WTO ruling against tariffs directed only at them. And it urged the US to correct the abuse of trade measures. But the MOFCOM didn't comment directly on the reported USD 60b tariff package.

EU Moscovici at G20: We must absolutely avoid trade wars

European Economics Commissioner Pierre Moscovici he's "cautiously optimistic" that there could be an agreement on the language on trade out of G20 meeting. And he hoped that the G20 communique will show that "how that protectionism is not the solution and we must absolutely avoid that." He warned that "the first risk is the risk of inward looking policies and protectionism."

Regarding US requests to omit the term "multilateral" from there statement, Moscovici blasted that "avoiding multilateralism in a multilateral organization makes no sense." He further added that "a trade war would be stupid. There would be damage on both sides of the Atlantic." Moscovici also reiterated that EU is prepared for counter-measures to US if it's not exempted from the steel and aluminum tariffs. Moscovici noted "but we think the best is to avoid a scale up" because "we must absolutely avoid trade wars."

On the other hand, US Treasury Secretary Steven Mnuchin emphasized in an email statement that "The trip to the G-20 will focus on advancing the Trump administration's global economic agenda to level the playing field for U.S. companies and workers."

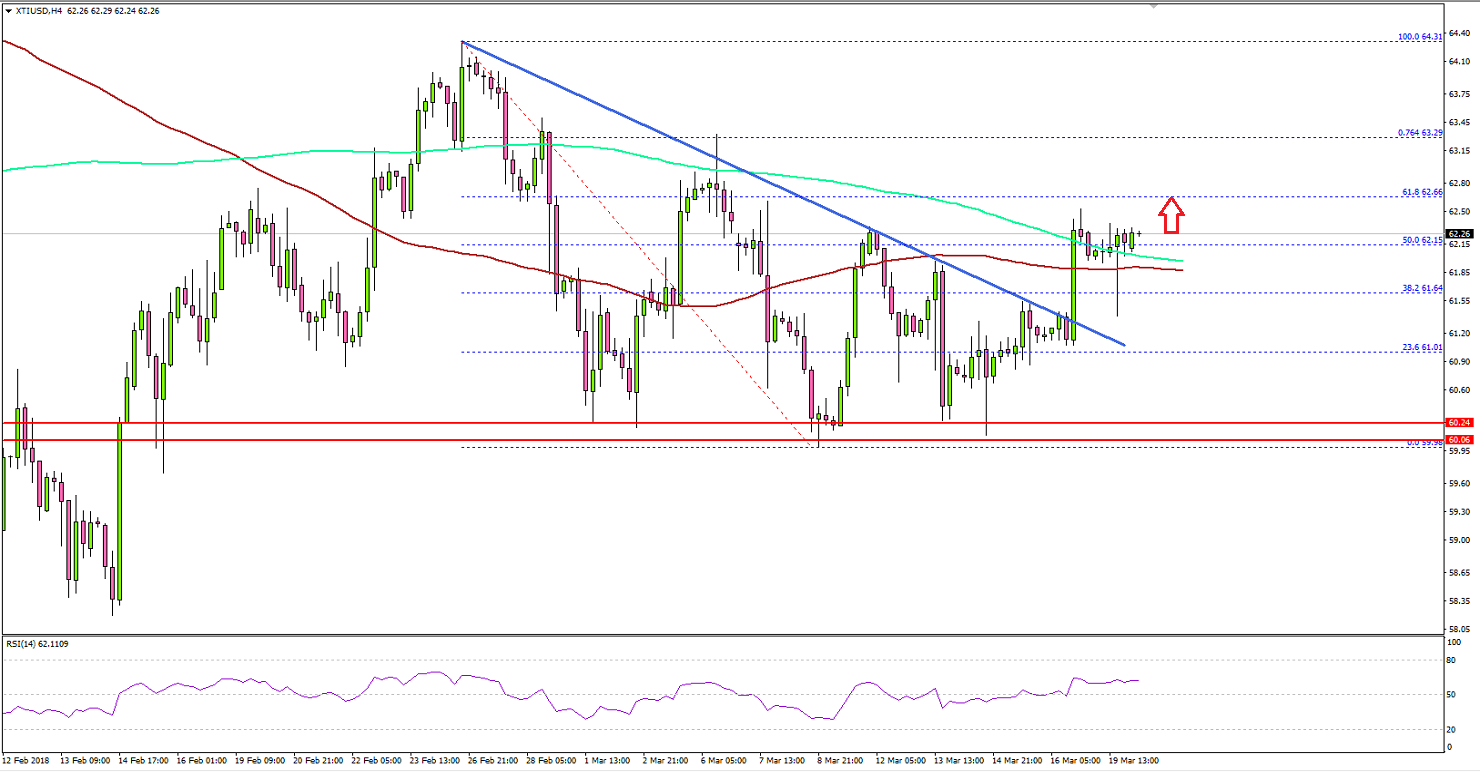

Crude Oil Price Moved Into Bullish Zone Above $61.50

Key Highlights

- Crude oil price formed a major support at $60.20 and moved higher against the US dollar.

- There was a break above a major bearish trend line with resistance near $61.25 on the 4-hours chart of XTI/USD.

- The price is now trading nicely above the $62.00 resistance and in a positive zone.

- Today in the UK, the CPI report for Feb 2018 will be released, and the market is looking for a 2.8% rise in the CPI (YoY).

Crude Oil Price Technical Analysis

There was a solid support base formed above $60.00 in crude oil price against the US dollar. As a result, there was a steady upside move and the price broke a major resistance near $61.20.

Looking at the 4-hours chart of XTI/USD, sellers made many attempts to push the price below $60.00. However, they failed and the price started an upside move above the $61.00 level.

During the upside, there was a break above the 23.6% Fibonacci retracement level of the last decline from the $64.31 high to $59.98 low.

More importantly, there a break above a major bearish trend line with resistance near $61.25 on the same chart. The price moved above the $62.00 handle and the 38.2% Fibonacci retracement level of the last decline from the $64.31 high to $59.98 low.

These all are positive signs above $62.00. On the upside, the next major resistance sits near the $62.50-60 area. Above $62.60, the price may attempt a move towards the $64.00 level.

On the downside, an initial support is around $62.00 level. However, the most important support is near the broken resistance near $61.20-25, which will most likely act as a decent support zone.

Economic Releases to Watch Today

- UK Retail Price Index Feb 2018 (YoY) – Forecast +3.7%, versus +4.0% previous.

- UK Producer Price Index Feb 2018 (YoY) – Forecast +3.8%, versus +4.7% previous.

- UK Producer Price Index Feb 2018 (MoM) – Forecast +0.1%, versus +0.1% previous.

- UK Consumer Price Index Feb 2018 (YoY) – Forecast +2.8%, versus +3.0% previous.

- UK Core Consumer Price Index Feb 2018 (YoY) – Forecast +2.5%, versus +2.7% previous.

- German ZEW Business Economic Sentiment Index for March 2018 – Forecast 13.0, versus 17.8 previous.

ECB Mersch: Prerequisites there for inflation, but easy policy still needed

ECB Executive Board member Yves Mersch sounded upbeat on his comments yesterday. He said that "all prerequisites for a sustainable adjustment of inflation to our objective are given."

The central bank could continue to cut down its asset purchases gradually as inflation outlook improves. He's concerned that there could be excessive market reactions if the asset purchases are reduced too quickly. And that would undo ECB's hard work in the past few years.

Overall, for the time being, easy monetary policy is still needed to support inflation.

AUD in strong near term downisde bias

While JPY is the worst performer this week so far, AUD is doing much better. Aussie is trading down versus all for the week except versus Dollar and Yen.

Looking at the Action Bias charts, note that 6H bias is all red downside in the last 9 bars of AUD/JPY. It's clear that it's in a near term downside momentum with solid momentum. The blue upside bars in hourly chart merely represents correction. And the decline is set to return after the correction completes.

Looking at the Action Bias charts, note that 6H bias is all red downside in the last 9 bars of AUD/JPY. It's clear that it's in a near term downside momentum with solid momentum. The blue upside bars in hourly chart merely represents correction. And the decline is set to return after the correction completes.

Similarly, GBP/AUD had strong upside momentum after the range breakout as seen in 6H bias chart. The neutral bias in H bias chart mere indicates it's in consolidation. The absence of red downside bar in H bias chart suggests that all consolidations were shallow and upside momentum has been strong.

Similarly, GBP/AUD had strong upside momentum after the range breakout as seen in 6H bias chart. The neutral bias in H bias chart mere indicates it's in consolidation. The absence of red downside bar in H bias chart suggests that all consolidations were shallow and upside momentum has been strong.

Many Moving Parts

Many Moving Parts

The various evolving narratives and lots of moving parts contributed some vibrant price action overnight. While international trade relations and the FOMC continue to lurk, markets took note of positive news regarding Brexit, yet another possible ECB policy shift and a tech-driven decline in the US and global equities markets.

Primary US stock index joined Global markets in the red Monday after Facebook share prices tanked over improper data use weighed on the tech sector. Cambridge Analytica was able to tap the profiles of more than 50 million Facebook users without their permission which could be an isolated issue or the symptom of broader matters at Facebook. This security breach could end up being a significant turning point for the social media and network portal.

Asia markets were already plumbing the depths on the prospects of Apple ‘s continued move to vertically integrate by both producing and manufacturing the new MicroLED technology in-house.

All in all global equities are mired in their worst run since November

Currency Markets

While the overwhelming focus remains on the FOMC, G-10 traders applauded the constructive Brexit news overnight and with most investors underweighted GBP assets; there was a scramble for topside exposure with the Pound punching well above its recent weight. As for the dollar fortunes, it all comes down to whether or not a steeper shift in dot plots is in the cards as the packed in March interest rate hike in itself is not sufficient enough to extend the USD’s recent appeal.

The Euro

The Euro was trading at dovish extremes entering the weekend but has bounced back with a vengeance after ” ECB sources” suggest the doves on the ECB board acknowledge QE should end this year and are okay with the market pricing in a 2019 rate hike. The single currency rallied 1.2260 towards 1.2360 in quick order on Monday as short-term Traders were caught out of line triggering some near-term stops.

The Japanese Yen

The USDJPY continues to trade heavy as this pair should be the most prominent beneficiary of the re-emergence of the weaker USD narrative even more so in this hyper risk-averse market. Abe political noise and equity market declines continue to dent sentiment.

The Malaysian Ringgit

EM and commodity currency continue to underperform in this risk-averse environment. But with the markets starting to price in a close call on Fed to shift to four rate hikes in 2018, the market has been paring back short USD MYR and $ASIA positions, so the Ringgit continues to struggle in this environment

The prospect of a faster pace of Fed policy normalisation and a risk-averse market provides a toxic backdrop for near-term Ringgit sentiment.

Oil Markets

At one point overnight OIl prices came off very aggressively as Wall street caved. But the downside susceptibility is also a cause and effect of the increase in US shale drilling where weaker speculative longs remain quite fragile to global risk sentiment

However, tensions between Saudi Arabia and Iran, as well as concerns over Venezuelan crude production, continued to underpin prices and the markets have recovered soundly. Iran nuclear tensions are not leaving the picture anytime soon, and the possible reimposition of US Oil sanctions should the keep Oil bulls charging near term.

Gold Markets

After knocking on crucial support level doors overnight, Gold prices bounced higher amid equity weakness and heightened geopolitical tensions between Saudi Arabia and Iran.

While gold investors remain incredibly nervous at the prospect of a shift in the Fed dot plots fearing of possible FOMC induced knee-jerk lower. However, since risk aversion is not expected to decrease anytime soon and with President Tump beating the trade war drums, demand for haven assets should remain firm over the medium term, even more so with core Gold investors.

While gold prices have bounced admirably over the past few US rate hikes, but those were interpreted as a dovish rate increase. This time around everyone is more apt to defend against a hawkish narrative.

Gold Starts Week With Gains, Fed Rate Hike Ahead

Gold has posted gains in the Monday session. In North American trade, the spot price for an ounce of gold is $1318.29, up 0.30% on the day. On the release front, there are no US indicators on the schedule.

On Friday, US numbers were mixed. Construction data disappointed, as Building Permits dropped to 1.30 million, shy of the estimate of 1.30 million. Housing Starts followed a similar trend, falling to 1.24 million and missing the forecast of 1.29 million. There was better news from consumer confidence, as UoM Consumer Sentiment improved to 102.0, beating the estimate of 99.3 points. This marked the first time that the indicator has been over the symbolic 100 level since October 2017.

Traders should be prepared for some volatility from gold prices this week, with the Federal Reserve poised to raise interest rates on Wednesday. This would mark the first hike of 2018. According to the CME Group, the odds of a quarter-point raise stand at an impressive 91 percent. What can we expect from the Fed during the year? The pressing question is how many rate hikes will we see in 2018. The current Fed projection remains at three hikes, but a robust US economy has raised speculation that the Fed could accelerate the pace to four hikes, which would be good news for the US dollar. Investors will be keeping a close eye on key US data, especially upcoming inflation indicators. If these numbers improve, we’re likely to see four rate hikes in 2018.

Brexit Deal Boosts GBP

A Brexit transition deal cleared a major hurdle for Theresa May and the Bank of England on Monday. GBP was the top performer while JPY lagged. RBA meeting minutes are due up next. The FTSE100 Premium short was closed for a 235-pt gain after CADJPY and GBPAUD hit their final targets for 200 and 290 pips respectively.

Brexit negotiators from the UK and EU announced a preliminary deal on a transition package that will extended to the end of 2020. That timeline will encourage UK business to make investment decisions and give confidence to the BOE that the trajectory of the UK economy is improving.

Cable climbed as high as 1.4088 from 1.3925 before sliding back 50 pips.The euro also got a lift from an ECB sources report showing that doves have relented and that the debate is moving on to how quickly to hike rates and how to communicate them. That boosted the euro up to 1.2350 from a low of 1.2260.

The stock market, meanwhile, suffered on as tech stocks dipped. A broader story about data abuse at Cambridge Analytica sparked a rout on Facebook that spread. Jitters about Trump and the FBI added to the worries. Critical questions about elections will continue to circulate but aside from companies directly involved, it isn't likely to an economic story.

Another key driver for markets is the tariff decision from White House with exemptions due before Friday's deadline. Comments from various European policymakers were upbeat on Monday and details of US requests showed the focus is tilted towards China. That makes it more likely exemptions will be granted as the US forms a 'coalition of the (reluctantly) willing' in a slow march to a trade war with China.

In the short-term, the Australian dollar is in focus. It rebounded to finish higher Monday after breaking down to the lowest levels of the year. Iron ore prices continue to slide but the immediate focus will be the RBA minutes at 0030 GMT and comments from the RBA's Bullock at 0415 GMT.