Sample Category Title

Swiss SECO revised up growth and inflation forecasts, warned of escalation to trade war

In this Swiss State Secretariat for Economic Affairs report published today, the government painted a brighter picture of the economy. Growth forecasts for 2018 and 2019 were both revised up. Also, 2018 inflation forecast was revised notably higher. The report titled Economy continues dynamic recovery noted that "the economy to continue its dynamic recovery and anticipates strong GDP growth of 2.4% in 2018. The buoyant international economy is supporting foreign trade, while a favourable investment climate is stimulating domestic demand."

Here are the latest projections

- 2018 GDP forecast at 2.4%, revised UP from prior forecast at 2.3%.

- 2019 GDP forecast at 2.0%, revised UP from prior forecast at 1.9%.

- 2018 CPI forecast at 0.6%, revised notably up from prior forecast at 0.3%

- 2019 CPI forecast at 0.7%, unchanged from prior forecast at 0.7%

The tone of the report was very upbeat as it said "Switzerland's economy has not looked this healthy since the minimum euro exchange rate was discontinued in early 2015. The upturn gathered increasing momentum and became more broad-based in the second half of 2017."

Also, "the healthy global economy is boosting international demand for Swiss products and therefore driving foreign trade." And, "the Expert Group predicts that foreign trade will provide a significant boost to growth in 2018 especially but also in 2019." Regarding the job market, the reported noted that unemployment has been in " gradual decline since mid-2016, while employment also stepped up in the second half of 2017."

Regarding economic risks, SECO saw short-term positive and negative risks are "balanced". Upturn in global economy could help depreciate the Swiss Franc further and "give the Swiss economy a further boost". But warned that "protectionist measures recently announced in the US pose negative risks for the global economy." And, "any escalation to a trade war between the major economic zones would have a considerable dampening effect in the medium-term."

Besides, the report pointed to recent Italian election as "a certain political uncertainty remains on the international stage." Unclear Brexit terms and uncertainties in Switzerland's relationship with the EU are other risks mentioned. Domestically, there is risk of sharp correction in construction sector.

XAUUSD Intraday Analysis

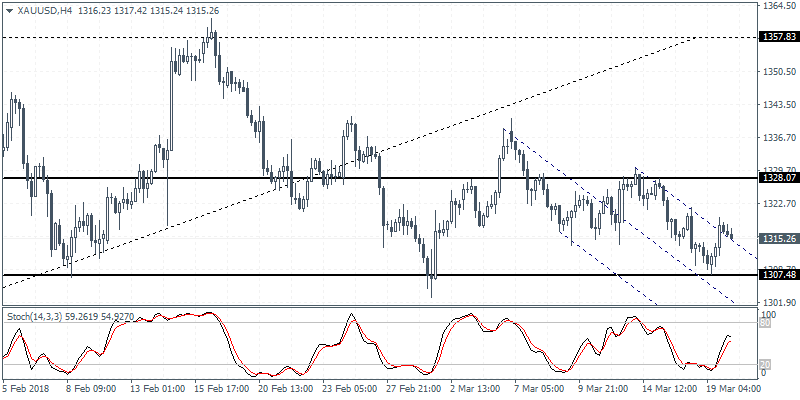

XAUUSD (1315.26): Gold prices were seen trading within the range after price action briefly touched down to 1307.80 level. We expect the downside bias to continue in the short term as gold prices could once again test this familiar support level. There is scope for price to potentially break down below 1307.80 region in which case, further declines could push gold prices to the 1300.00 round number followed by a test of support near the 1282 - 1274 level. To the upside, a close above the recent highs at 1319 could mean further gains toward 1328.00 level of resistance.

GBPUSD Intraday Analysis

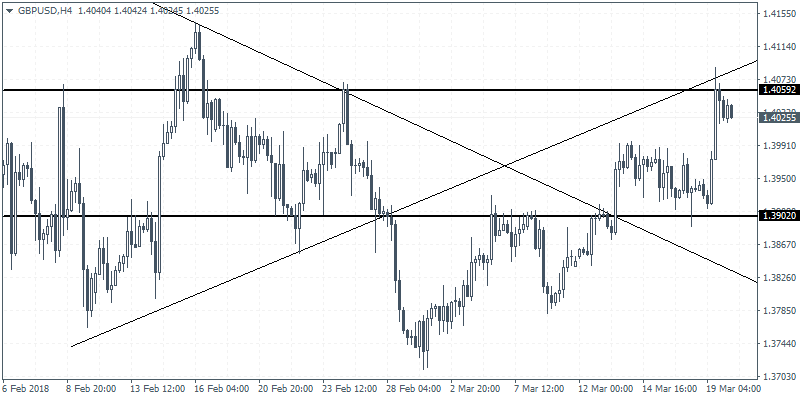

GBPUSD (1.4025): The British pound was seen posting strong gains on the day led by the developments on the Brexit talks which the market viewed as being positive for the GBP. The currency pair was seen trading above 1.4063 level but the gains stalled after the trend line was tested from below acting as resistance. The current consolidation could see further gains coming in. There is also the potential for GBPUSD to form an inverse head and shoulders pattern following the reversal at the resistance level of 1.4059.

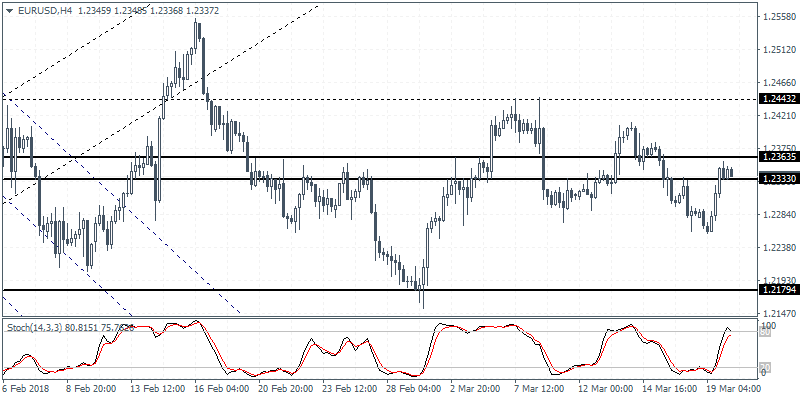

EURUSD Intraday Analysis

EURUSD (1.2337): The euro currency was seen posting strong gains yesterday as price action posted a reversal following last week's declines. However, the gains stalled near the resistance zone of 1.2363 - 1.2333 level. A reversal off this level could once again put the EURUSD back into the sideways range with the lower support at 1.2179 likely to be tested. With the Fed meeting due tomorrow, we expect to see the ranging price action continue. A breakout from either the resistance or the support level could potentially establish the direction in the currency pair.

EU-UK Strike Transitory Brexit Deal

The U.S. dollar was on the backfoot yesterday. The euro was seen retracing it’s the gains strongly which gains came amid investor uncertainty ahead of the FOMC meeting due on Wednesday.

Developments from Brexit included the EU and the UK striking a transitory deal. According to reports, the UK will remain in the EU until end of 2020 but with restricted powers. The British pound rallied on the news as the currency touched intraday highs of 1.4088.

Looking ahead, the economic calendar for the day will see the release of the inflation data for February from the UK. Economists forecast that inflation might have slowed down to 2.8% on a year over year basis in February. Core inflation is also expected to slow to 2.5% in February after rising 2.7% previously.

From the Eurozone, the German ZEW economic sentiment and the Eurozone ZEW economic sentiment reports will be released. Later in the day, the Eurozone consumer confidence data will also be coming out.

Tech Selloff Drags Down Global Equities

The steep losses in U.S. technology stocks were carried into Asian markets today with all major indices tracking Wall Street declines. Facebook made the headlines on Monday, as reports over the weekend claimed that data from 50 million users was accessed without their permission. The stock fell 6.8% and wiped out almost $37 billion from its market cap. The news will undoubtedly scare advertisers, especially if itleads to regulators changing Facebook’s business model in a way which may impact the company’s revenues.

Investors should not only be worried about the drop in Facebook equities, but also aboutFAANG stockswhich have been leading the bull market for many years. Alphabet dropped 3% yesterday, while Apple, Netflix, and Amazon declined 1.53%, 1.56% and 1.7% respectively. Though the fall in Facebook might have impacted the sector negatively, it does not explain the full picture. Concerns that the European Commission will impose new taxes on Tech firms in retaliation for U.S. steel and aluminum tariffs, is an early indication that the trade war should be taken more seriously. If markets decided to turn on FAANG stocks, we would likely see a similar reaction to last February’s correction.

Jay Powell Fed & the dots

The newly appointed Fed Chair, Jay Powell will hold his first press conference tomorrow, when the U.S. central bank is expected to raise interest rates for the first time in 2018. Markets have fully priced in a 25-basis point rate increase, so do not expect this to have any influence on the dollar’s direction.

The key to dollar traders is how Fed officials, led by the new Chair, will act on recent economic data and whether the fiscal stimulus will eventually lead to a tighter monetary policy in 2018. Market participants are split on whether the Fed will project four rate hikes in 2018 compared to three in the last meeting. An upward shift in the dot plot should support the dollar, although it is likely to lead to further flattening in the U.S. yield curve.

Brexit transition deal sends Sterling higher

The pound was the best performing currency on Monday, rising 0.6% against the USD to trade back above 1.40. The Brexit deal was thought to be more positive for Sterling, but given that no agreement was reached on the Irish border, gains were capped. I believe that Sterling may still have further room to appreciate against its peers, especially if Consumer prices today and wage data tomorrow provide new signs of inflationary pressure before Bank of England meet on Thursday.

EU And UK Agree Transition Deal

Following on from the list of retaliatory trade tariffs drawn up by the EU over the weekend, the risk-off sentiment deepened in markets yesterday, with the US 500 index breaking down out of its triangle and the NASDAQ breaking lower to form a bearish island reversal pattern. On a quiet day for data releases, there were plenty of headlines, with Brexit taking the early focus. The EU and UK agreed on a transition deal to maintain the status quo through to 2020. The GBP and EUR both strengthened on the news, with GBPUSD up to a high of 1.40878 from 1.39120 and EURUSD up to 1.23584 from 1.22621. The EUR was helped by reports that the ECB has shifted focus on to how quickly to raise rates after QE.

The G20 kicked off in Buenos Aires yesterday, with the main focus being the US Trade Tariffs. BOJ Governor Kuroda said that protectionist steps would backfire for countries that implement them by disrupting their own imports of necessary goods. He said that he didn’t think the policies would spread and that the global community understands the need to protect trade. “The G20 will likely continue calling on the importance of free trade”, he said. On cryptocurrencies, he said “there may be areas where regulations could be beefed up, such as consumer protection and money laundering. But we also need to make sure we don’t stifle new technology”.

New Zealand Westpac Consumer Survey (Q1) was 111.2 against a prior number of 107.4. This data beat the previous quarter and shows signs of confidence in the economy. NZDUSD moved higher from 0.72364 to 0.72438 after the data release.

RBA Meeting Minutes were published. The minutes said that low rates are playing a part in lowering unemployment and lifting inflation. The bank repeated that further progress on policy goals is likely to only be gradual. GDP growth is expected to exceed potential growth in 2018 and CPI inflation is expected to rise to a little above 2 pct this year. It also said that the rising AUD would slow pickup in economic growth and inflation. Strong employment had not yet led to a “definitive pick-up” in wage growth and high household debt levels added to the uncertainty over consumption and warranted careful attention.

Australian House Price Index (QoQ) (Q4) came in at 1.0% against an expected 0.0%, from -0.2% previously. This data point has managed to climb to 1.0% after slipping under 0.0% in the last quarter (Q3). This shows a slowing in the market overall, down from 4.1% in Q4 2016. AUDUSD moved higher from 0.77025 to 0.77170 due to this data release.

Japanese Leading Economic Index (Jan) came in at 105.6 against an expected 106.2, from 106.8 which was revised up from 104.8. Coincident Index (Jan) came in at 114.9 against an expected 119.1, from 119.7, which was revised up from 114.0. USDJPY fell from 106.392 to 106.250 as a result of this data release.

EURUSD is up 0.07% overnight, trading around 1.23439.

USDJPY is up 0.18% in early session trading at around 106.274.

GBPUSD is up 0.13% this morning, trading around 1.40418.

Gold is down -0.05% in early morning trading at around $1,315.99.

WTI is up 0.69% this morning, trading around $62.68.

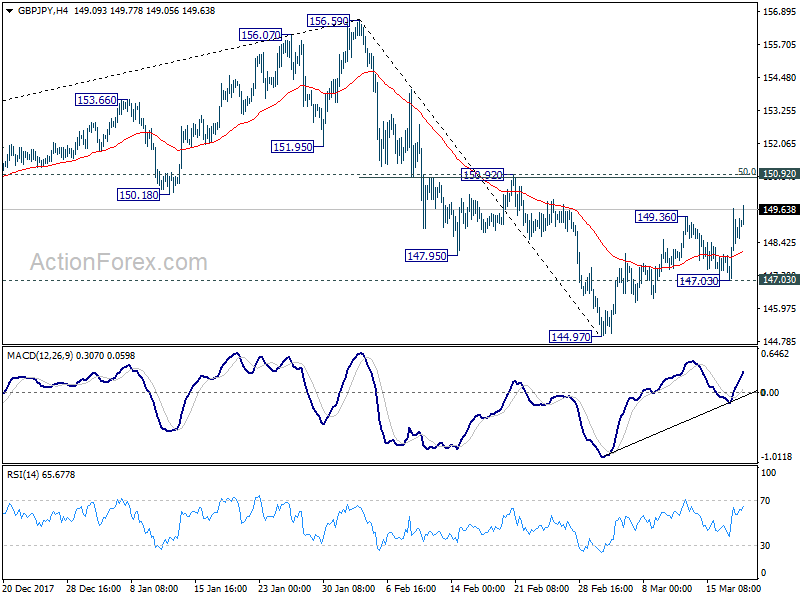

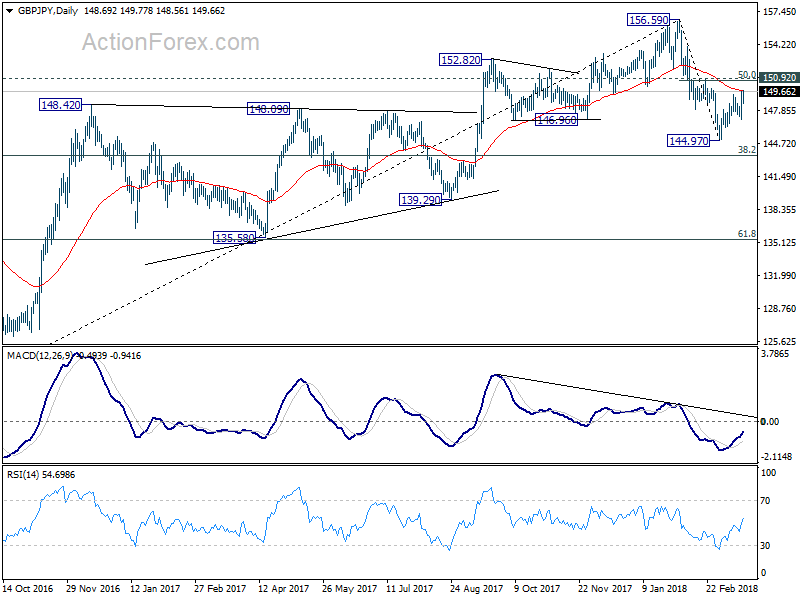

GBP/JPY Daily Outlook

Daily Pivots: (S1) 147.31; (P) 148.49; (R1) 149.94; More....

Intraday bias in GBP/JPY remains mildly on the upside as rebound from 144.97 extends. Further rise could be seen. But still, it's seen as a corrective move. Therefore, we'd expect strong resistance from 150.92 (50% retracement of 156.59 to 144.97 at 150.78) to bring fall resumption. On the downside, below 147.03 will bring retest of 144.97 low first. Break will extend the decline from 156.59 to 143.51 medium term fibonacci level next. However, sustained break of 150.92 will pave the way back to retest 156.69 high.

In the bigger picture, the case for medium term reversal continues to build up. There is bearish divergence condition in daily MACD. 146.96 support was taken out. And GBP/JPY was rejected by 55 month EMA. Break of 38.2% retracement of 122.36 to 156.59 at 143.51 will pave the way to 61.8% retracement at 135.43 and below. This will now be the preferred case as long as 150.92 resistance holds.

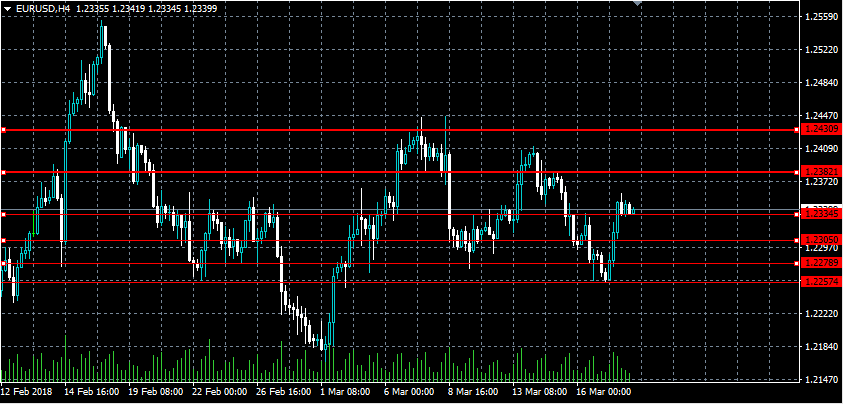

EURUSD Intraday Bullish ABove 1.2334 Level

The euro has reversed early week trading losses against the greenback, following dovish news coming out from the European Central Bank on Monday. The EURUSD pair quickly moved back above the 1.2305 level, after reports that ECB policymakers had shifted talks towards on how quickly the ECB can raise interest rates after ending QE. Traders now look to key economic data from the German economy, with monthly PPI inflation and ZEW survey numbers coming out during the European trading session.

The EURUSD pair is bullish whilst trading above the 1.2334 level, key technical resistance is now found at the 1.2382 and 1.2430 levels.

If the EURUSD pair falls below the 1.2334 support level, a price correction towards the 1.2305 and 1.2278 level may occur.

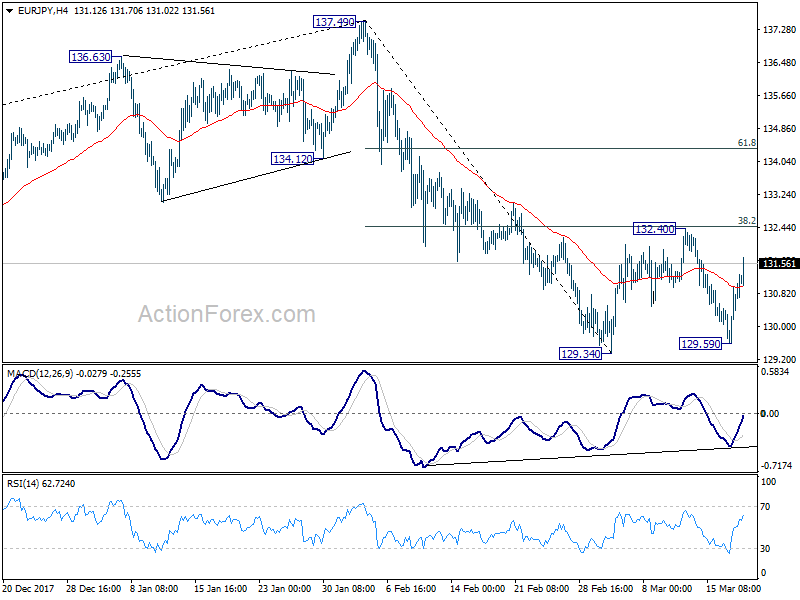

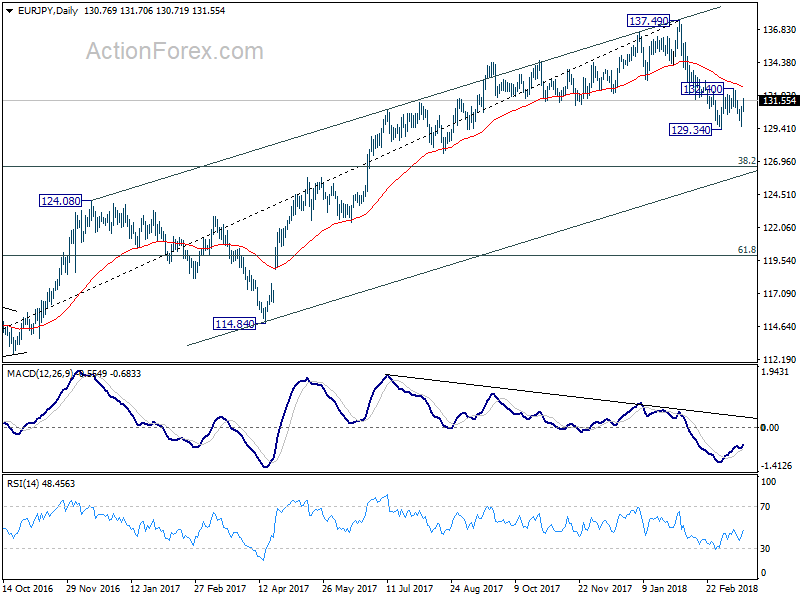

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.95; (P) 130.51; (R1) 131.41; More....

EUR/JPY's rebound from 129.59 extends to as high as 131.70 so far today. A this point, as the cross is staying in range above 129.34, intraday bias stays neutral first. Also, we'd expect strong resistance from 38.2% retracement of 137.49 to 129.34 at 132.45 to limit upside and bring fall resumption eventually. On the downside, decisive break of 129.34 will confirm resumption of whole fall 137.49 and target 126.61 medium term fibonacci level. However, firm break of 132.45 will target 61.8% retracement at 134.37 instead.

In the bigger picture, current development argues that rise from 109.03 (2016 low) has completed at 137.49, on bearish divergence condition in weekly MACD. Deeper fall should be seen to 38.2% retracement of 109.03 to 137.49 at 126.61 first. On the upside, break of 137.49 is needed to confirm medium term rise resumption. Otherwise, risk will now stay on the downside even in case of strong rebound.