Sample Category Title

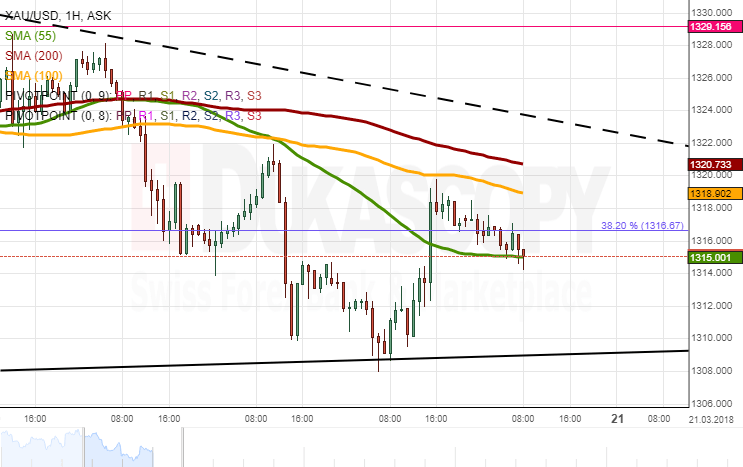

Gold Analysis: Stranded By SMAs

A reversal from the 1,310.00 territory early on Monday was followed by a sharp upside pressure for Gold, as the weakening of the US Dollar boosted demand for the commodity. As a result, the 55-hour SMA and the 38.20% Fibonacci retracement were breached.

The Asian session marked a slight decline in price, as traders are awaiting patiently the first Fed rate hike this year. In terms of technicals, Gold faces strong resistance of the 100– and 200-hour SMAs and a down-trend near the 1,320.00 mark.

It is likely that bulls fail to gather enough momentum in to push above this area this session. Thus, the yellow metal should push lower down to the 55-hour SMA. No additional support is provided until 1,310.00.

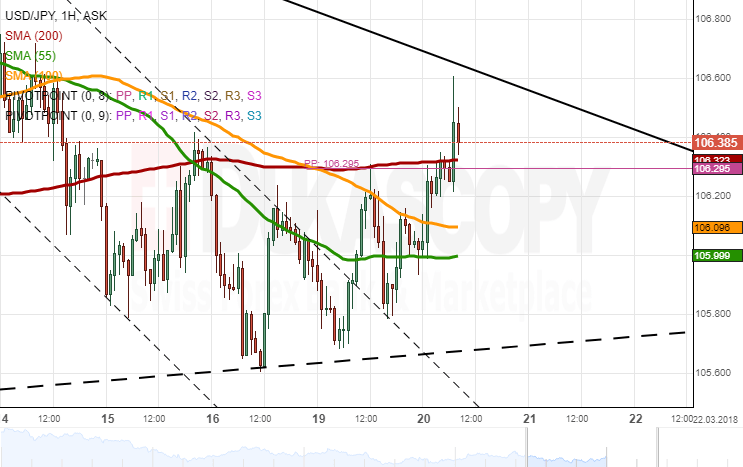

USD/JPY Analysis: Still Indecisive

The US Dollar continues to consolidate for the third consecutive session. During this time, a move above the 106.50 mark was restricted by the 200-hour SMA, while support was provided by a three-week up-trend.

The pair was testing the former at the time of this analysis. It is likely that the same lack of momentum also continues in this session, as traders are awaiting patiently the Fed policy statement released tomorrow at 1800GMT. Additional resistance is likewise provided by a medium trend-line near 106.50.

Given the rate's inability to move above this mark for the last few sessions, it is more likely that that the US Dollar targets the 2017/2018 low and the weekly S1 at 105.30 today. A fall below this level should not occur.

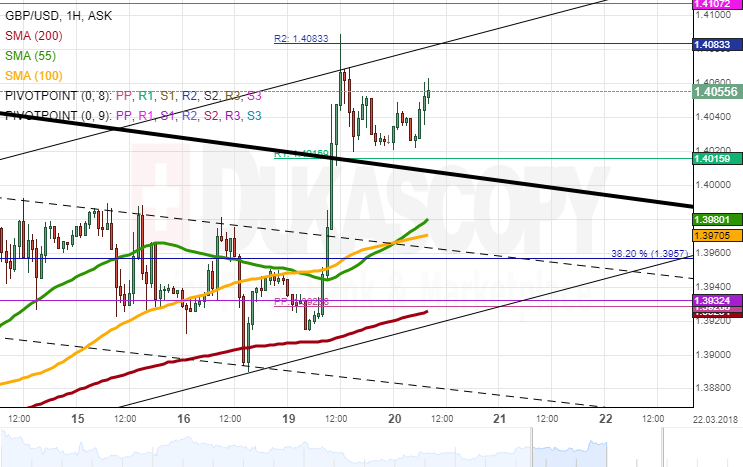

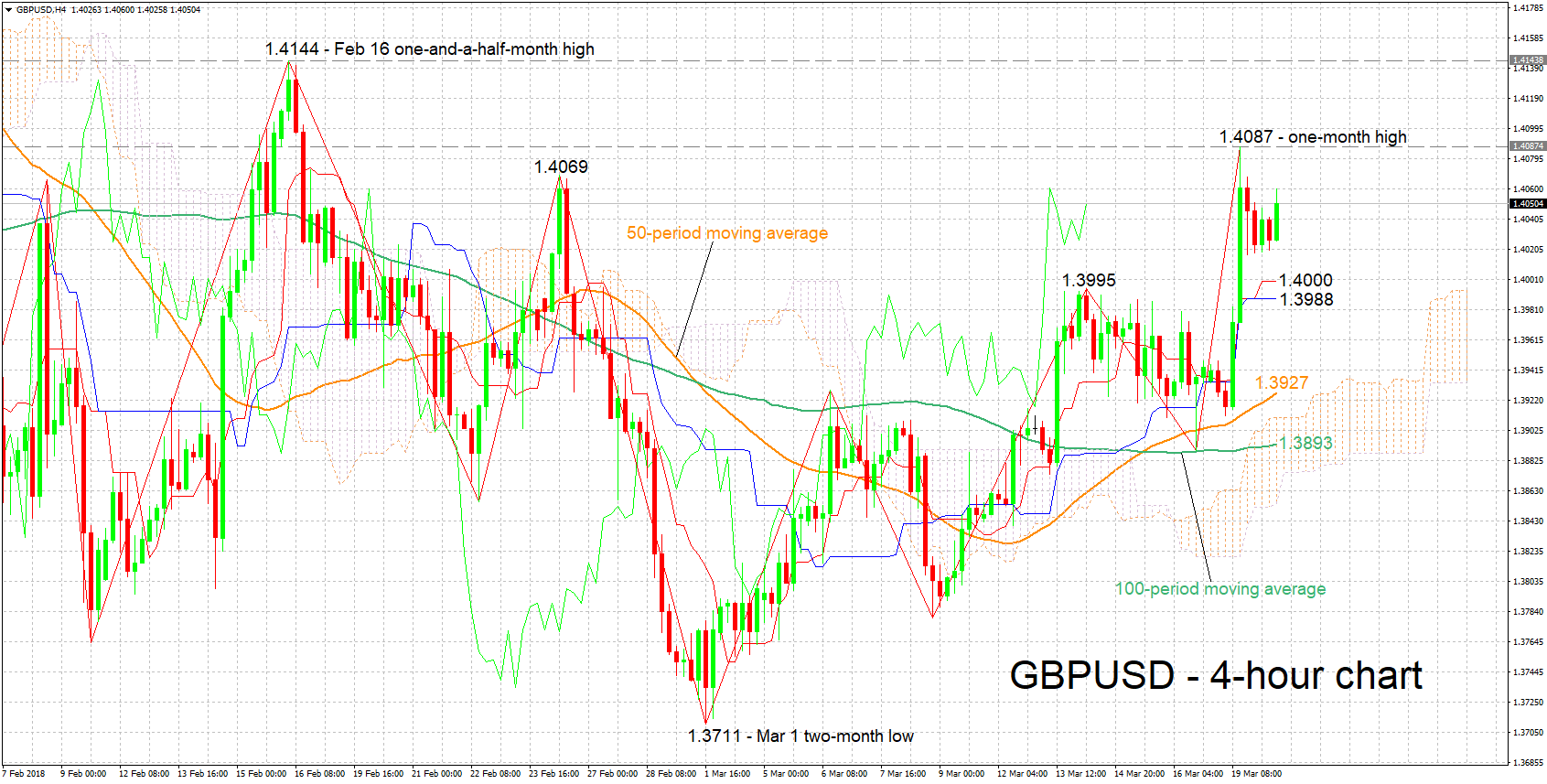

GBP/USD Analysis: Shoots Up To 1.4060

The British Sterling was bounded by moving averages during the first part of Monday, thus trading in line with a short-term channel down.

This lack of momentum changed significantly mid-session when a successful Brexit deal between the EU ad the UK shot up the rate by 1.03% within a couple of hours. As a result, the pair breached the prevailing senior channel and pushed as high as the weekly R2 at 1.4083.

Technical indicators still flash strongly bullish signals; however, their direction does show a tendency southwards. Thus, traders should see a bearish correction to the 1.40 area where the 55– and 100-hour SMAs are located.

In case no fundamentals shake the market today, it is unlikely that the 1.4080 is breached, thus paving the way for a slide south.

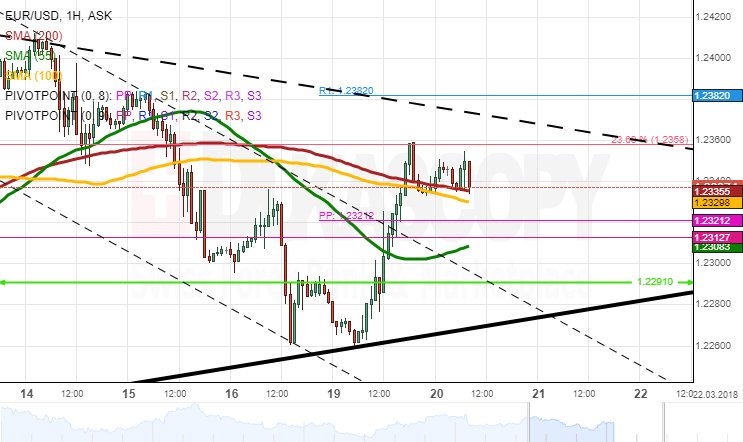

EUR/USD Analysis: Allays After Surge

The Euro rallied against the US Dollar on Monday, thus closing the session with a 55-pip gain. The most notable surge was apparent mid-session when a successful Brexit agreement gave additional bullish push.

The rate moved above the 200– and 100-hour SMAs and was therefore located near the 1.2360 area which has provided strong resistance during the previous weeks.

This breakout might be interpreted as a signal for a continuous advance north. However, the aforementioned resistance area could introduce some changes to this assumption and thus force the Euro lower down to the weekly PP and the 55-hour SMA circa 1.2310.

The main driver of volatility in this session should be G20 meetings. In case no surprises occur, the market is likely to consolidate prior to Fed statement tomorrow.

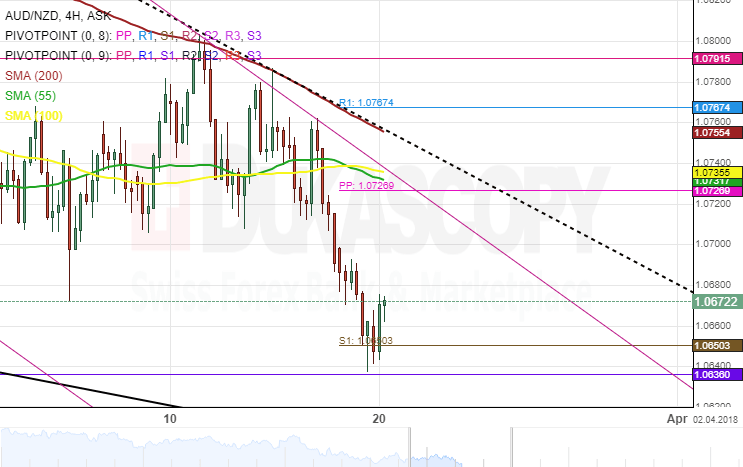

AUD/NZD 4H Chart: Bears Growing Stronger

The Australian Dollar has been constrained by several descending channels against the New Zealand Dollar since late October 2017. The upper boundary of a dominant channel was reached on October 24 and has since remained trading along this patterns.

The inability for the AUD/NZD pair to initiate new moves up indicates that it might breach the junior pattern as soon as possible. The combination of the 55– and 100 –hour SMAs was restricting the rate from making such upward wave.

Everything being equal, the currency exchange rate could plummet further during the following trading sessions. Meanwhile, technical indicators favour bears to grow stronger.

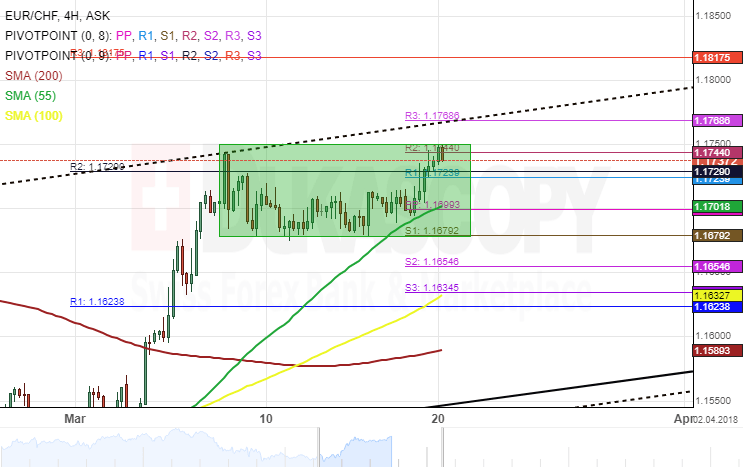

EUR/CHF 4H Chart: Flag Pattern Formed

The common European currency has appreciated substantially against the Swiss Franc since mid-June 2017.The upwards moves have been constrained in an ascending channel.

During the past few weeks, the Euro has failed to make any further movement north as the EUR/CHF pair encountered a period of consolidation. Due to this reason, a flag pattern has been formed as can be observed on the chart.

Technical indicators suggest that a breakout is likely to occur through the upper boundary of a rectangle during the following trading sessions. However, it is important to note that the nearest resistance that could hinder the exchange rate to make upside moves is located near 1.1768.

Euro, Sterling Build On Gains Versus The Greenback, UK Inflation And US-Saudi Meeting Eyed

Here are the latest developments in global markets:

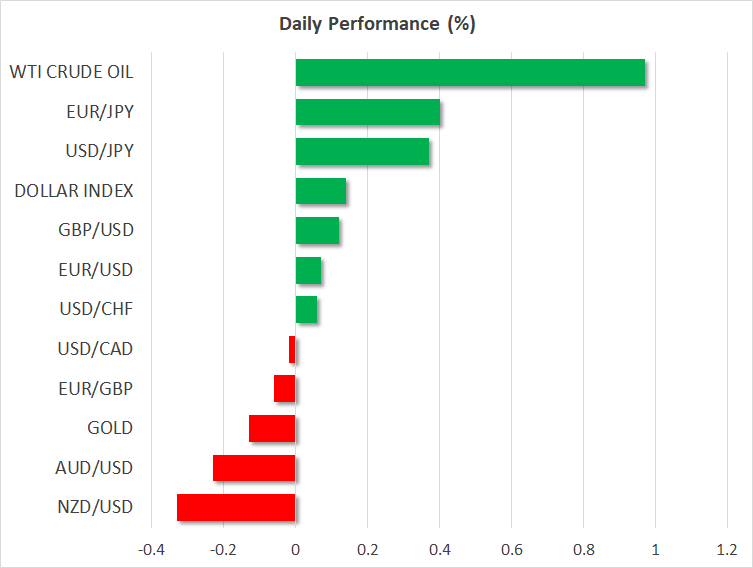

FOREX: The dollar edged higher versus a basket of currencies on Tuesday after retreating against the euro and sterling on Monday. The yen was losing considerable ground relative to other major currencies, while the antipodeans were trading not far above recent lows against the greenback.

STOCKS: US markets closed significantly lower yesterday, dragged down primarily by technology stocks, as a scandal involving Facebook raised speculation that tech firms may see increased regulation soon. The Nasdaq Composite led the charge lower, declining by 1.8%, while the S&P 500 and the Dow Jones followed closely in its tracks, falling by 1.4% and 1.35% respectively. Futures tracking the Dow and S&P are more or less flat at the time of writing, but those tracking the Nasdaq 100 are in negative territory, pointing to a lower open for the tech-heavy index. In Asia, Japan’s Nikkei 225 and Topix tumbled by 0.5% and 0.2% respectively, while in Hong Kong, the Hang Seng was down by less than 0.1%. Europe was a different story, as futures tracking all the major benchmarks were a sea of green today, suggesting these indices are likely to open higher.

COMMODITIES: Oil prices surged on Tuesday, with WTI and Brent crude climbing by 1.0% and 0.8% correspondingly. The spike higher is being attributed to concerns that oil output from Venezuela could fall notably in the near future, as well as due to increased tensions in the Middle East. In this respect, a meeting between the US President and the Saudi Crown Prince today will be closely watched, for any hints on whether a new round of sanctions on Iran is on the cards. The private API crude inventory data will also be in focus at 2030 GMT. In precious metals, gold traded around 0.2% lower today, unable to hold onto the gains it posted yesterday. The yellow metal continues to be unresponsive to the broader risk-aversion in markets lately, even despite the rising risk of a “trade war” that has helped other safe havens like the Japanese yen.

Major movers: Euro and pound build on gains versus the dollar, advances moderate though; yen retreats

The dollar’s index against a basket of currencies was up by around 0.2% at 89.91 after being weighed the previous day by strength in the euro and the British pound. The focus for the dollar now turns to the Federal Reserve’s two-day meeting which concludes on Wednesday and during which the delivery of a quarter percentage point interest rate hike is widely expected. Meanwhile, US Treasury yields were rising on Tuesday, adding to the greenback’s allure.

The yen, which started yesterday’s trading on a positive footing as polls showed Prime Minister Abe’s administration losing public support, was retreating versus majors including the dollar, euro and sterling. Versus the former two, the Japanese currency was down by 0.4%, while pound/yen traded higher by 0.6%, not far below a near three-week high of 149.78 hit earlier in the day.

Euro/dollar was 0.1% up at 1.2343, building on Monday’s gains that saw it rise by 0.4% on the back of rising speculation – spurred by a Reuters report based on ECB sources – that the ECB will further scale back its asset purchases in 2018 and deliver a rate hike around the middle of next year.

The pound also traded 0.1% higher versus the greenback at 1.4036, after adding 0.6% the previous day and recording a one-month high of 1.4087. The British currency was boosted after the UK and the EU agreed to a 21-month post-Brexit transition period as well as a potential solution to avoid a “hard border” for Northern Ireland. Euro/pound, which recorded losses on Monday, was 0.1% down at 0.8789, at 0729 GMT. This compares to yesterday’s one-and-a-half month low of 0.8742.

Lastly, the antipodean currencies extended their recent losses versus their US counterpart. Aussie/dollar was 0.2% down at 0.7699, not far above Monday’s three-month low of 0.7684, while kiwi/dollar was 0.3% lower at 0.7219 after yesterday recording a near three-week low of 0.7194. Cautiousness ahead of the FOMC meeting as well as fears of a global trade war were seen as hurting the currencies of the two commodity-exporting countries; US President Donald Trump is anticipated to unveil up to $60 billion in new tariffs on Chinese products by Friday. In addition, the aussie was hurt by softer iron ore prices, Australia’s top export earner, while the RBA minutes of its March meeting released earlier on Tuesday possibly weighed on the currency as well. The central bank reiterated its cautious stance on consumer spending, sending the message that interest rates may need to stay at record lows for longer.

Day ahead: UK inflation data and US-Saudi meeting in the spotlight; G20 trade message also of importance

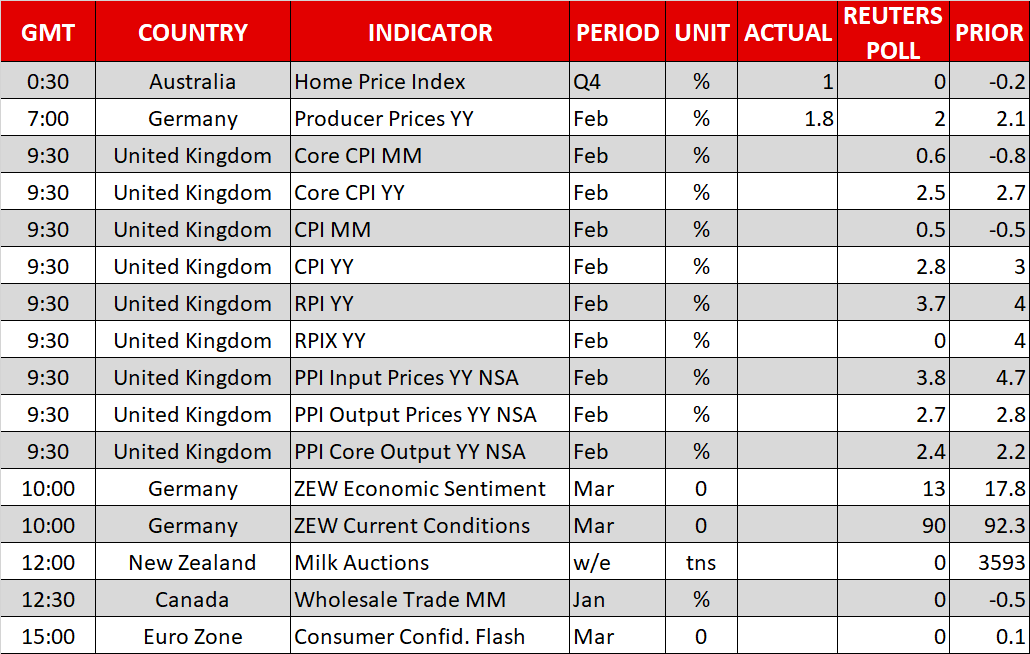

The most important release today will be the UK CPI data for February, due out at 0930 GMT. Both the headline and the core CPI rates are expected to have declined in yearly terms, but both are still anticipated to remain well-above the Bank of England’s (BoE) 2% target. In such case, slowing inflation would likely ease some of the pressure on the Bank to hike rates in the near-term. Markets currently see a 70% probability for the BoE to raise rates in May. A notable decline in the CPIs – particularly the core rate – could push that probability lower, and sterling alongside it. The Markit services PMI for February supports the forecasts, as it showed prices charged by service companies increasing at the weakest rate for six months. Data on producer prices (PPI) for February will also be made public at the same time.

In Germany, the ZEW survey for March will be in focus at 1000 GMT. Both the current conditions and the expectations indices are anticipated to decline. Even though falling sentiment among German financial experts would be a negative development for the ECB, policymakers are likely to focus more on the Markit PMIs that are due out on Thursday in order to gauge the momentum of eurozone’s economy. The bloc’s preliminary consumer confidence index for March is also coming out, at 1500 GMT.

In New Zealand, the bi-weekly milk auction will be held today. Given New Zealand’s status as a major dairy exporter, these data tend to impact the kiwi dollar. The time of this release is always tentative, though most calendars have it marked for 1200 GMT. Overall, the attention of NZD-traders remains on the RBNZ policy decision tomorrow, as it could determine the currency’s short-term direction.

In the US, the FOMC will begin its policy meeting today, which will conclude tomorrow at 1800 GMT.

In energy markets, besides the weekly API crude inventory data that will be released at 2030 GMT, investors will also keep their eyes on a meeting between US President Trump and Saudi Crown Prince Mohammad bin Salman in Washington. Media reports suggest the two will be discussing Iran and as such, attention will be on whether a new round of sanctions is to be imposed on the nation soon. Any hints suggesting as much could boost oil prices, on speculation that a large chunk of Iranian oil supply could be removed from the market in the foreseeable future.

Elsewhere, the G20 meeting between finance ministers and central bank governors will conclude today. The common statement on trade will be worth watching, as it could provide some signals on whether the “trade war” theme is set to intensify further.

Technical Analysis: GBPUSD bullish bias but positive momentum may be losing steam

GBPUSD is trading roughly 40 pips below Monday’s one-month high of 1.4087. The positively aligned Tenkan- and Kijun-sen lines are projecting a bullish bias, though the fact that the two lines have flatlined is an indication that positive momentum has lost part of its steam. UK inflation figures due later on Tuesday have the capacity to either refuel the positive momentum or alter it altogether, turning the pair to the downside.

Should CPI data be interpreted by markets as increasing the odds for a more aggressive tightening cycle by the Bank of England, then GBPUSD is likely to gain. Resistance in this case might come around yesterday’s high of 1.4087. Notice that the area around this point also encapsulates another top from the recent past at 1.4069, as well as the 1.41 handle that may be of psychological significance.

A downside deviation from inflation projections though is likely to push back expectations for more aggressive monetary policy normalization by the BoE, leading to weakness in GBPUSD. Support in this scenario could be met around the current level of the Tenkan-sen at 1.40. The range around this level also includes the Kijun-sen at 1.3988, as well as a previous peak at 1.3995.

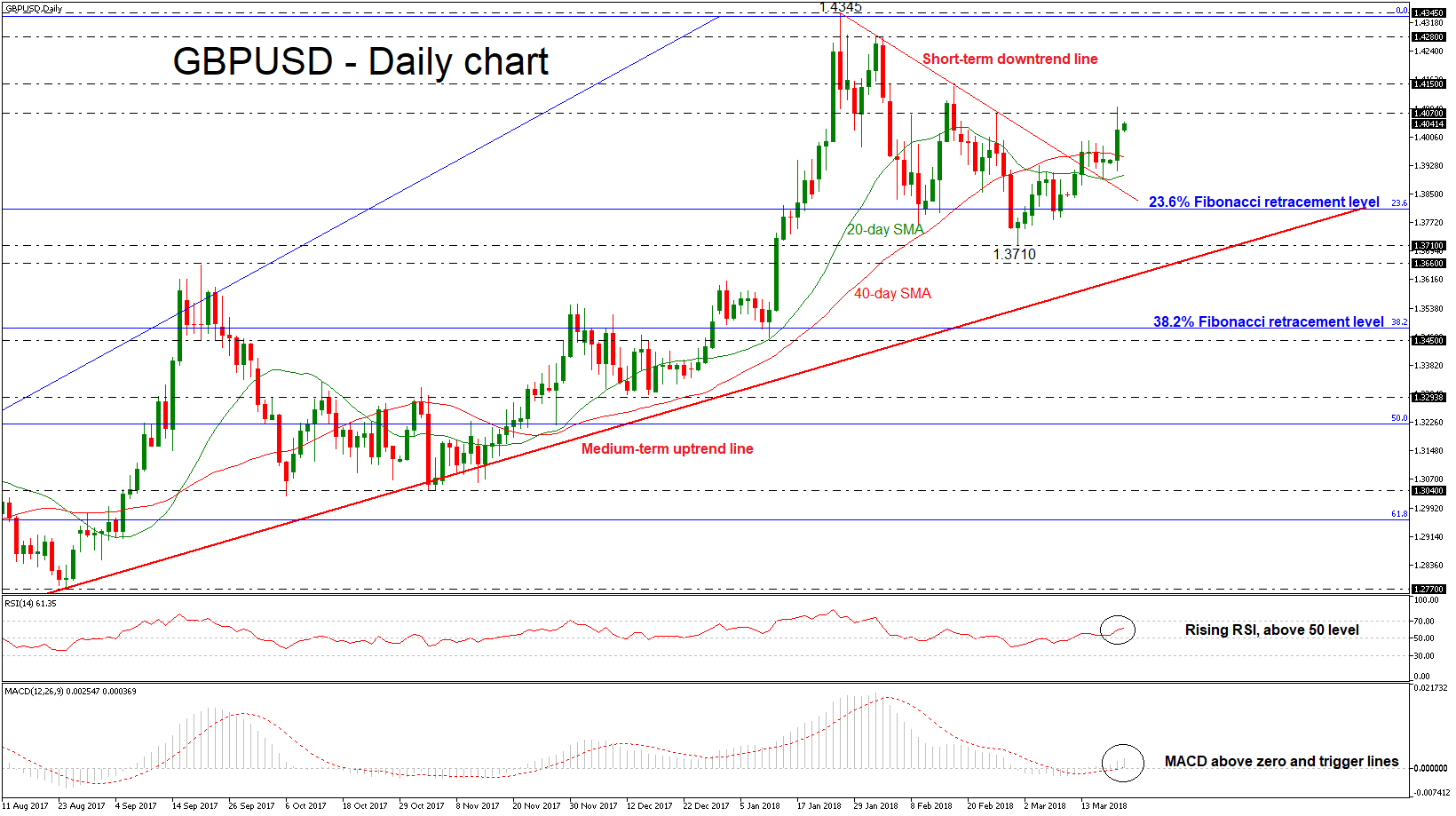

GBPUSD Edges Higher, Creates 1-Month High Below 1.4100

GBPUSD has advanced considerably during yesterday’s trading session, hitting a new one-month high of 1.4087. Over the last few days, the price climbed above the short-term descending trend line from the high on January 25, suggesting more upside bias. The technical picture also supports that the bullish move is likely to continue in the short-term.

It is worth mentioning that the pair has been trading within a strong ascending movement since March 2017 and tested the diagonal line several times in the past.

Looking at the daily timeframe, the RSI indicator has a clear upside direction above the threshold of 50, supporting that the market could keep moving higher. The MACD oscillator confirms this view in the positive territory and is currently moving above its trigger line.

Further gains above the 1.4070 resistance level, could see the February high of 1.4150 acting as the next major obstacle. A run above the latter level would endorse the bullish structure in the short-term and open the way towards the next key resistance of 1.4280.

In the wake of negative pressures, the market could meet support at the 23.6% Fibonacci retracement level near 1.3810 of the upleg from 1.2100 to 1.4345. A successful close below this level could see a retest of the previous low of 1.3710, while in case of steeper declines, the price could breach this level, diving to 1.3660, which holds near the uptrend line.

All Eyes On UK CPI Data As BOE Looms On Thursday

The G20 meeting continues today in Buenos Aires, where a range of global economic issues including the regulation of cryptocurrencies will be discussed. Headlines may affect any market depending on the context.

At 09:30 GMT, UK Consumer Price Index (YoY) (Feb) is expected out at 2.8% v 3.0% previously. Core Consumer Price Index (YoY) (Feb) is expected at 2.5% from 2.7% prior. Consumer Price Index (MoM) (Feb) is expected at 0.5% from -0.5% prior. Producer Price Index – Output (MoM) n.s.a. (Feb) is expected at 0.1% from 0.1% previously. Producer Price Index – Output (YoY) n.s.a. (Feb) is expected at 2.7% from 2.8% previously. Producer Price Index – Input (MoM) n.s.a. (Feb) is expected at -0.9% from 0.7% previously. Producer Price Index – Input (YoY) n.s.a. (Feb) is expected at 3.8% from 4.7% previously. Retail Price Index (MoM) (Feb) is expected at 0.8% against -0.8% previously. Retail Price Index (YoY) (Feb) is expected to be 3.7% from 4.0% prior. These data points show CPI slipping on a year-on-year basis but the monthly figure is expected to show some growth. The yearly CPI figure has remained above the Bank of England’s 2% target since March of 2017 due to the change in the value of the pound after Brexit. However, the BOE says that inflation is likely to move back to 2% in 2018. GBP crosses may be moved by the data released at this time.

At 10:00 GMT, German ZEW Survey – Current Situation (Mar) is expected at 90.0 against a prior 92.3. ZEW Survey – Economic Sentiment (Mar) is expected to be 13.0 from 17.8 previously. These data points are expected to soften, as the strengthening in the Euro affects business. The deteriorating trade environment is also a headwind for business outlook. EUR crosses may be affected by this data.

Tentative, New Zealand GDT Price Index is expected to be released with a previous reading of -0.6%. This data shows the change in the average price of dairy products sold at auction. As this is an important part of the New Zealand economy, NZD crosses may be impacted by the result.

Note: Wednesday is a Bank Holiday in Japan, banks will be closed, and there will be no trading activity due to the Vernal Equinox Day Bank Holiday.

Currencies: EUR/USD Balance Restored After Hawkish ECB Rumours

Rates: Fragile balance ahead of tomorrow's FOMC meeting

Initial losses on core bond markets were undone by a sell-off on US stock markets. Fragile risk sentiment and the possibility of a hawkish shift at tomorrow's Fed meeting, keep bonds currently in balance. The US Note future keeps underperforming the German Bund.

Currencies: EUR/USD balance restored after hawkish ECB rumours

A downside test of EUR/USD was blocked yesterday by the EU/UK transition deal and by comments on the ECB ending APP this year. Today, markets might shift into wait-and-see modus ahead of tomorrow's Fed decision. However, there is plentiful potential event risk that might unsettle (currency) markets.

The Sunrise Headlines

- US stock markets lost up to 1.85% yesterday (Nasdaq) on reports of a digital tax by the EU. Facebook also dragged the index lower after a data breach claim. Asian equities opened weak, but sentiment improves during dealings. They are mixed with China and Japan underperforming (-0.5%).

- The Washington Post reports that US President Trump prepares to hit China with $60bn in tariffs by Friday, doubling aides' earlier proposal in an escalation of trade tensions.

- ECB Mersch, one of the more hawkish officials, said everything is in place for the return of stable euro-area inflation, putting the central bank on course to halt its bond-buying program later this year.

- Saudi Arabia called the 2015 nuclear deal between Iran and world powers a "flawed agreement", on the eve of a meeting between the Saudi crown prince and US President Trump who have both been highly critical of Iran.

- A majority in Norway's parliament signaled it will try to oust the nation's justice minister after a controversial Facebook post, in a move that will probably force PM Solberg to put her whole cabinet up for a vote.

- Chinese President Xi Jinping warned self-ruled Taiwan that it will face the "punishment of history" for any attempt at separatism, offering his strongest warning yet to the island claimed by China as its sacred territory.

- Today's eco calendar contains UK inflation, German ZEW investor confidence and EMU consumer confidence. Germany holds a 2-yr Schatz auction

Currencies: EUR/USD Balance Restored After Hawkish ECB Rumours

EUR/USD balance restored after ‘ECB rumours'

Two factors changed fortunes for the euro yesterday. First, the UK and the EU agreed on a transition deal giving UK firms access to the common market till end 2020. This propelled sterling and, to a lesser extent the euro (against the dollar). Second, the rhetoric on the ECB turned less dovish on a Reuters article that there is consensus within the ECB to end APP by the end of this year. EUR/USD traded near 1.2260 yesterday morning, gained almost one big figure and closed the session at 1.2335. The equity sell-off had only a limited impact on the dollar. USD/JPY closed the session little changed at 106.10.

Sentiment in Asia remains risk-off this morning, but the losses are modest compared to WS yesterday. USD/JPY stays relatively well bid. The pair is said to be supported by importer related buying. EUR/JPY buying after yesterday's ECB rumors might also be in play. EUR/USD maintains yesterday's gains, but stabilizes near yesterday's close. The RBA minutes gave a balanced view on the economy and inflation with little impact on the AUD/USD which holds in the low 0.77 area.

German ZEW investor sentiment and the EC consumer confidence will be published. Some easing is expected for both indicators. They will probably only be of intraday significance, at best. Last week, the euro ceded modest ground on soft ECB talk, highlighting ongoing low inflation. However, the balance between the euro and dollar looks restored after yesterday's Reuters' comments. This morning's constructive performance of USD/JPY despite a global risk-off context suggests some USD buying interest going into the FOMC meeting. However, this probably won't help EUR/USD bears. Yesterday's rejected test of the 1.2260 area propelled EUR/USD back in the established consolidation pattern. There is probably a really hawkish Fed-message needed for new downside test. The trade tariffs debate and equity sentiment remain (tentatively negative) wildcards for the dollar.

Sterling jumped yesterday after the EU/UK transition deal. Headline UK inflation is expected to ease from 3.0% to 2.8% today. (Inflation) data might get some more weight for GBP-trading.as Brexit moves to the background. Especially an upside surprise might reinforce BoE rate hike expectations and push EUR/GBP further south in the 0.8950/0.8690 trading range. We don't anticipate a downside break yet.

EUR/USD returns higher in established range as ECB is said to end APP this year