Sample Category Title

EUR/USD Mid-Day Outlook

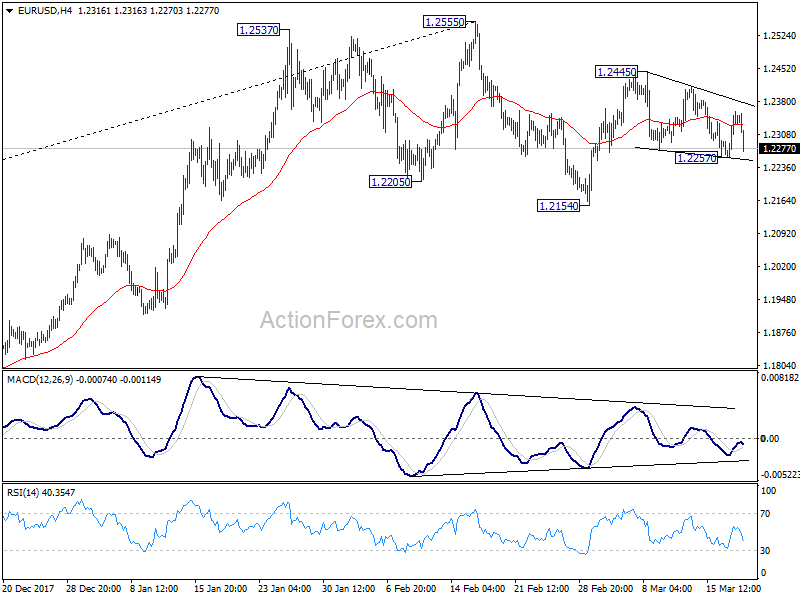

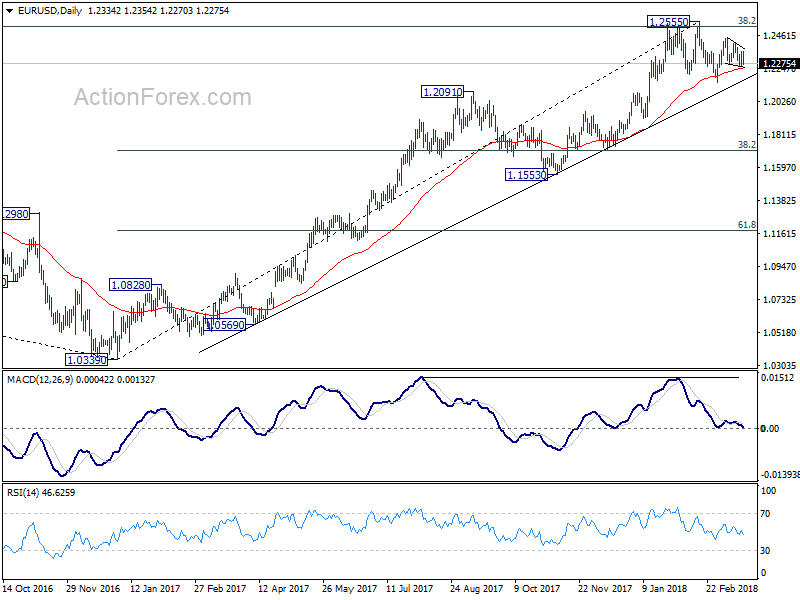

Daily Pivots: (S1) 1.2275; (P) 1.2316 (R1) 1.2376; More....

EUR/USD's sharp fall today now put 1.2257 support back into focus. Intraday bias is turned neutral first. For the moment, we're slightly favoring the case that price actions from 1.2445 are corrective in nature. And 1.2257 support should hold even in case of a brief breach. Another rise is expected and break of 1.2445 will target a test on 1.2555 key resistance. However, sustained break of 1.2257 will dampen this bullish view. In that case, intraday bias will be turned back to the downside, to resume the fall from 1.2555 through 1.2154.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Euro Reverses as Germany Outlook Worsened Considerably, Sterling Pare Gains after CPI Miss

Euro and Sterling trade notably lower today as economic data missed expectation. Sterling remains relatively firm and stays as the strongest major currency for the week. The CPI miss was just 0.1% yoy, and Brexit transition deal should still give BoE policy makers a confidence boost. Euro, on the other hand, is much more troubled as deterioration in German ZEW was quite considerable. The trades mildly generally firmer today as markets await FOMC rate hike tomorrow. Before that, eyes will be on whether G20 leaders would come up with something against protectionism and trade war in their joint communique.

UK CPI slowed to 2.7% yoy, missed expectation

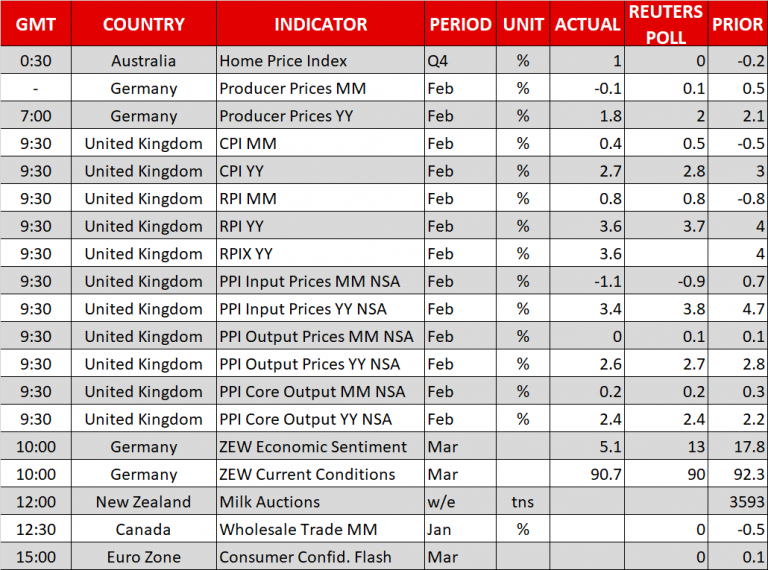

UK headline CPI slowed to 2.7% yoy in February, down from 3.0% yoy and missed expectation of 2.8% yoy. Core CPI slowed to 2.4% yoy, down from 2.7% yoy and missed expectation of 2.5% yoy. The reading doesn't give any added pressure for BoE to rate interest rate in May. Nonetheless, CPI stays above the mid-point of 2-3% target range. BoE board members should still view the Brexit transition deal as a relief to businesses. And investors could come back with, at least, part of the uncertainties cleared. Known hawks like Michael Saunders and Ian McCafferty could still start pushing for rate hike during this week's meeting.

Also from UK, PPI input dropped -1.1% mom, rose 3.4% yoy versus expectation of -0.9% mom, 3.8% yoy. PPI output rose 0.0% mom, 2.6% yoy versus expectation of 0.1% mom, 2.7% yoy. PPI output core rose 0.2% mom, 2.4% yoy versus expectation of 0.2% mom, 2.4% yoy, house price index rose 4.9% yoy in January below expectation of 5.0% yoy.

German ZEW indicates "Economic Outlook Worsens Considerably"

German ZEW economic sentiment dropped to 5.1 in March, down from 17.8, below expectation of 13.0. Current situation gauge dropped to 90.7, down from 92.3, above expectation of 90.0. Eurozone ZEW economic sentiment also dropped sharply to 13.4, down from 29.3, missed expectation of 28.1.ZEW titled the release as "Economic Outlook Worsens Considerably" which is an indication of how bad things turned. ZEW President Professor Achim Wambach noted that "concerns over a US-led global trade conflict have made the experts more cautious in their prognoses. The strong euro is also hampering the economic outlook for Germany, a nation reliant on exports." But he added that "combined with the experts' continued positive assessment of the current situation, however, the outlook is still largely positive."

Also from Germany, PPI dropped -0.1% mom, rose 1.8% yoy in February.

Swiss SECO revised up growth and inflation forecasts, warned of escalation to trade war

In the Swiss State Secretariat for Economic Affairs report published today, the government painted a brighter picture of the economy. Growth forecasts for 2018 and 2019 were both revised up. Also, 2018 inflation forecast was revised notably higher. The report titled Economy continues dynamic recovery noted that "the economy to continue its dynamic recovery and anticipates strong GDP growth of 2.4% in 2018. The buoyant international economy is supporting foreign trade, while a favourable investment climate is stimulating domestic demand."

The tone of the report was very upbeat as it said "Switzerland's economy has not looked this healthy since the minimum euro exchange rate was discontinued in early 2015. The upturn gathered increasing momentum and became more broad-based in the second half of 2017." "The Expert Group predicts that foreign trade will provide a significant boost to growth in 2018 especially but also in 2019."

Regarding economic risks, SECO saw short-term positive and negative risks are "balanced". But it warned that "protectionist measures recently announced in the US pose negative risks for the global economy." And, "any escalation to a trade war between the major economic zones would have a considerable dampening effect in the medium-term."

More about the report here.

Also from Swiss, trade surplus widened to CHF 3.14b in February, above expectation of CHF 1.87b.

Little surprise from RBA minutes

The RBA minutes for the March contained little surprise. Policymakers remained concerned about the soft inflation outlook, noting faster wage growth is needed to assure a stronger and more sustainable improvement on inflation. As suggested in the minutes, "employment had grown strongly and the unemployment rate had fallen over the preceding year. However, the improvement in overall conditions had not yet translated into a definitive pick-up in wages growth, which remained low". It added that "further progress on these goals [reducing the unemployment rate and bringing inflation closer to target] was expected over the period ahead, but this process was likely to be gradual". Also from Australia, house price index rose 1.0% qoq in Q4 versus expectation of 0.0% qoq.

More on RBA minutes in RBA Minutes Reiterated The Impacts Of Low Wage Growth On Inflation.

New BoJ deputies Wakatabe and Amamiya sound cautious in inaugural press conference

The two new BoJ Deputy Governors spoke in the inaugural news conference today.

Masazumi Wakatabe said that BoJ sounded cautious as he said BoJ should avoid premature shift in monetary policy. Also, in his view, the central bank shouldn't hesitate to ease monetary policy further if needed. Nonetheless, she acknowledged that various economic data already showed the positive impacts of current and past ultra loose policy.

Masayoshi Amamiya, also emphasized the importance to continue with powerful monetary easy, for achieving improvements in the output gap. He acknowledged that Japan is no longer in deflation. But BoJ hasn't meet its 2% inflation target yet.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2275; (P) 1.2316 (R1) 1.2376; More....

EUR/USD's sharp fall today now put 1.2257 support back into focus. Intraday bias is turned neutral first. For the moment, we're slightly favoring the case that price actions from 1.2445 are corrective in nature. And 1.2257 support should hold even in case of a brief breach. Another rise is expected and break of 1.2445 will target a test on 1.2555 key resistance. However, sustained break of 1.2257 will dampen this bullish view. In that case, intraday bias will be turned back to the downside, to resume the fall from 1.2555 through 1.2154.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | House Price Index Q/Q Q4 | 1.00% | 0.00% | -0.20% | |

| 00:30 | AUD | RBA March Meeting Minutes | ||||

| 06:45 | CHF | SECO Economic Forecasts March | ||||

| 07:00 | EUR | German PPI M/M Feb | -0.10% | 0.10% | 0.50% | |

| 07:00 | EUR | German PPI Y/Y Feb | 1.80% | 2.00% | 2.10% | |

| 07:00 | CHF | Trade Balance (CHF) Feb | 3.14B | 1.87B | 1.32B | |

| 09:30 | GBP | CPI M/M Feb | 0.40% | 0.50% | -0.50% | |

| 09:30 | GBP | CPI Y/Y Feb | 2.70% | 2.80% | 3.00% | |

| 09:30 | GBP | Core CPI Y/Y Feb | 2.40% | 2.50% | 2.70% | |

| 09:30 | GBP | RPI M/M Feb | 0.80% | 0.80% | -0.80% | |

| 09:30 | GBP | PPI Input M/M Feb | -1.10% | -0.90% | 0.70% | 0.40% |

| 09:30 | GBP | PPI Input Y/Y Feb | 3.40% | 3.80% | 4.70% | |

| 09:30 | GBP | PPI Output M/M Feb | 0.00% | 0.10% | 0.10% | |

| 09:30 | GBP | PPI Output Y/Y Feb | 2.60% | 2.70% | 2.80% | |

| 09:30 | GBP | PPI Output Core M/M Feb | 0.20% | 0.20% | 0.30% | |

| 09:30 | GBP | PPI Output Core Y/Y Feb | 2.40% | 2.40% | 2.20% | |

| 09:30 | GBP | House Price Index Y/Y Jan | 4.90% | 5.00% | 5.20% | 5.00% |

| 10:00 | EUR | German ZEW (Economic Sentiment) Mar | 5.1 | 13 | 17.8 | |

| 10:00 | EUR | German ZEW Current Situation Mar | 90.7 | 90 | 92.3 | |

| 10:00 | EUR | Eurozone ZEW (Economic Sentiment) Mar | 13.4 | 28.1 | 29.3 | |

| 12:30 | CAD | Wholesale Trade Sales M/M Jan | 0.10% | 0.40% | -0.50% | |

| 15:00 | EUR | Eurozone Consumer Confidence Mar A | 0 | 0.1 |

Euro and Sterling post data selloff accelerate as delayed reaction

Euro and Sterling enter US session as the weakest ones. Economic data from Eurozone and UK missed expectation. But the selloffs accelerate as delayed reactions. Aussie, on the other hand, picks up some strength togther with Dollar, with help from selloff in EUR/AUD.

For the week, Sterling is still the strongest one so far. But Euro is turning mixed.

For the week, Sterling is still the strongest one so far. But Euro is turning mixed.

Dollar on the Rise as FOMC Gathers; European Stocks Step Lower

Here are the latest developments in global markets:

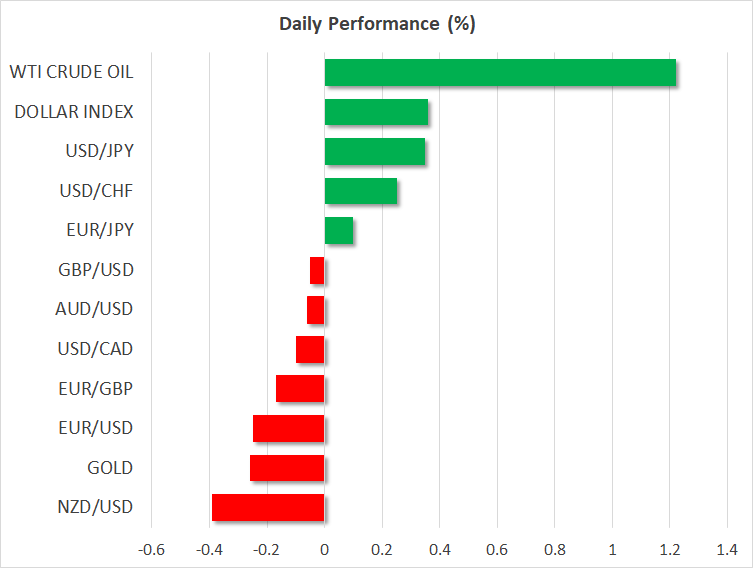

FOREX: The US dollar traded higher today, reversing some of its losses in the previous days as investors were preparing their positions ahead of Wednesday’s Federal Reserve rate decision, where expectations are for the FOMC board members to raise interest rates for the first time this year. Dollar/yen rose towards 106.52 (+0.35%) after touching a session low of 106.00 earlier today and the US dollar index edged higher by 0.35%, breaking slightly above the 90.00 level. Earlier today, the Bank of Japan welcomed two new board members, who pledged to meet the central bank’s 2% inflation target as soon as possible. The British pound moved lower after the release of the UK CPI which fell to 2.7% y/y in February from the 3% in the previous month, missing expectations of a 2.8% increase. It was the lowest rate since July last year. Pound/dollar remained in the green but near to its opening level of 1.4030. Recall that on Monday, sterling posted a strong rally on the news that the UK and the EU had reached an agreement on the Brexit transition deal. This period will be between March 2019 and December 2020. Euro/dollar dropped to 1.2285 after the German ZEW economic sentiment appeared strongly lower than forecasted. Moreover, the commodity-linked currencies remained virtually unchanged during early European afternoon. Aussie/dollar hovered near a three-month low of 0.7685, being 0.04% down on the day. Kiwi/dollar remained under pressure near three-week lows, losing 0.37%, while dollar/loonie weakened by 0.05% to 1.3073 after it hit a 9-month high of 1.3124 on Monday.

STOCKS: Following a plunge in the US and Asian indices triggered by a sell-off in technology shares, the European equities started the day on a softer tone. The blue-chip Euro Stoxx 50 was up by 0.15% at 1030 GMT, the German DAX 30 rose by 0.28% and the British FTSE 100 climbed by 0.34%.

COMMODITIES: Oil rose to its highest level this month, due to tensions in the Middle East and the possibility of further fall in Venezuelan output. WTI crude oil rose by 1.13% to $62.51 a barrel and Brent crude oil surged by 1.17% to $66.84 a barrel. In precious metals, gold traded lower by 0.25% as the dollar awaits the Fed to shed some light on the path of US interest rates at the conclusion of its two-day policy meeting on Wednesday.

Day ahead: FOMC board members begin policy meeting; G20 meeting concludes

Day ahead: FOMC board members begin policy meeting; G20 meeting concludes

In the absence of major economic releases out of the US, the focus is turning to the Fed which starts its two-day monetary policy meeting today. It will be chaired by Jerome Powell for the first time since his nomination, with the rate announcement and fresh projections on the path of interest rates, economic growth, unemployment rate and inflation expected to be made on Wednesday at 1800 GMT. While a rate hike is a widely anticipated outcome with the CME Federal Reserve tool indicating an almost 95% probability of this happening, investors will be closely looking for any clues that could signal four rate hikes this year instead of three currently priced in the markets.

Given the latest upbeat evidence on the US economic performance and the potential positive effects stemming from the new tax overhaul, policymakers could back the scenario of ‘faster rate hikes than previously expected’, with the Fed Funds futures implying a probability of 35% of four or more rate rises in 2018 compared to less than 10% three months ago. However, the persisting softness in inflationary pressures could persuade policymakers to reiterate only gradual interest rate rises. Speaking on Monday in Philadelphia, Janet Yellen, the former Fed chair, said that a slower tightening could overheat the market, while a faster tightening could restrict inflation from reaching the Fed’s 2.0% target.

On the trade front, the G20 meeting concludes today and any valuable news out of the event could move the dollar. In case statements disappoint, fuelling concerns of a potential global trade war, the dollar could slip into losses, while a milder response could ease tensions and provide support to the greenback. Meanwhile, on Monday sources said that the US President is preparing to impose a $60 billion package of annual import tariffs on Chinese products to punish China for intellectual property theft, with the plan expected to be unveiled by Friday.

In terms of data releases, the economic calendar features January’s wholesale trade figures out of Canada later in the day at 1230 GMT and Eurozone flash estimates on consumer confidence for the month of March at 1500 GMT. New Zealand will see the results of the bi-weekly milk auctions today at a tentative time which could bring fresh volatility to the kiwi. Investors, though, could pay greater attention to the RBNZ policy meeting held on Thursday.

In energy markets, the American Petroleum Institute will publish readings on the US crude inventories at 2030 GMT. A meeting between the US President, Donald Trump, and the Saudi Arabian Crown Prince, Mohammed Bin Salman, could attract some attention as well, as both countries seem to be looking for ways to impose tougher measures against Iran’s nuclear program. Note that Saudi Arabia – US relations have been improving after tensions under the previous US administration. Therefore any intention between the countries to deliver a new round of sanctions against Iran could lift oil prices as this could weigh on Iranian oil supply.

Canadian Dollar Subdued, Wholesale Sales Next

The Canadian dollar is unchanged in the Tuesday session. Currently, USD/CAD is trading at 1.3083, up 0.04% on the day. On the release front, Canadian Wholesale Sales is expected to improve to 0.1%. For a second straight day, there are no US indicators. On Wednesday, the Federal Reserve will set the benchmark interest rate and release a rate statement.

The Canadian dollar is steady, after enduring a dismal week. The currency suffered its worst week since May 2016, sliding 2.7 percent. The week ended on a sour note, as Canadian Manufacturing Sales declined for the third time in four months. The key indicator declined 1.0%, missing the estimate of -0.8%. USD/CAD pushed above the 1.31 level on Monday, for the first time since June.

With the Federal Reserve widely expected to raise rates on Wednesday to a range of between 1.50% and 1.75%, the Canadian dollar could face strong pressure. According to the CME Group, the odds of a quarter-point raise stand at an impressive 94 percent. What can we expect from the Fed during the year? The current Fed projection remains at three hikes, but a robust US economy has raised speculation that the Fed could accelerate the pace to four hikes, which would be good news for the US dollar. Investors will be keeping a close eye on key US data, especially upcoming inflation indicators. If these numbers improve, we're likely to see four rate hikes in 2018.

Canadian policymakers continue to cast a nervous eye towards the Trump White House. The latest worry is the steel tariffs that the US has imposed, with the European Union threatening to retaliate against a host of US products. Although Canada was exempted from the tariffs, this could prove temporary, and the threat of a global trade war is not good news for Canada. Added to this mix is rising uncertainty over the NAFTA agreement. The US is demanding far-reaching concessions from Canada and Mexico, and the protectionist Trump administration could decide to exit NAFTA, which has been a key driver of economic growth for Canada. With the Federal Reserve expected to raise rates at least three times in 2018, the fragile Canadian dollar could find itself mired in more headwinds.

DAX Rebounds, Shrugs Off Soft Economic Sentiment Reports

The DAX index has posted gains in the Tuesday session, after losses of 1.0% in the Monday session. Currently, the DAX is trading at 12,270, up 0.44% on the day. On the release front, Germany PPI surprised the markets with a decline of 0.1%, shy of the estimate of +0.1%. This marked the first decline since May. German ZEW Economic Sentiment plunged to 5.1 points, down from 17.8 a month lower. This reading was well off the forecast of 13.1 points and marked the lowest reading since September 2016. Eurozone ZEW Economic Sentiment followed the same trend, dropping to 13.4, compared to a forecast of 28.1 points. The markets will be keeping a close eye on the Federal Reserve, which will set the benchmark rate and release a rate statement.

It was a rough start to the week for European stock markets, and the DAX suffered sharp losses of 1.0% on Monday. European technology stocks were sharply lower on the news that Micro Focus, one of Britain’s largest tech firms, saw its shares plunge by 55 percent after it lowered its revenue forecast and its CEO resigned. However, the DAX has rebounded on Tuesday, posting modest gains.

There have been plenty of setbacks in the Brexit negotiations, but there was some good news on Monday, as the two sides announced that there would be a transition period following the UK’s departure from the EU in March 2019. The transition deal will kick in at that time, lasting until December 2020. The deal covers the rights and status of EU citizens in the UK and British citizens in the EU, and allows the UK to pursue new trade agreements during that time. There are still issues to iron out, such as the Northern Ireland border. The transition period is a major, positive development, in that it will enable Britain to enjoy the benefits of the common market, although Britain will be out of the EU and won’t have any voting rights in the club.

The Federal Reserve is poised to raise interest rates on Wednesday, which would mark the first hike of 2018. According to the CME Group, the odds of a quarter-point raise stand at 94 percent. What can we expect from the Fed during the year? The current Fed projection remains at three hikes, but a robust US economy has raised speculation that the Fed could accelerate the pace to four hikes, which would be good news for the US dollar. Investors will be keeping a close eye on key US data, especially upcoming inflation indicators. If these numbers improve, we’re likely to see four rate hikes in 2018.

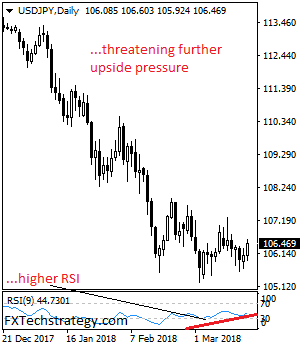

USDJPY – Strengthens, Continues To Trade Above Key Resistance

USDJPY - The pair looks to extend its recovery higher as it continues to strengthen further above its key support located at 106.24. On the downside, support lies at the 106.00 level where a break if seen will aim at the 105.50 level. A cut through here will turn focus to the 105.00 level and possibly lower towards the 104.50 level. On the upside, resistance resides at the 107.00 level. Further out, we envisage a possible move towards the 107.50 level. Further out, resistance resides at the 108.00 level with a turn above here aiming at the 108.50 level. On the whole, USDJPY faces further upside pressure

Market Update – European Session: Trade Concerns Continue To Have Risk Appetite Stay Offered, UK CPI Registers A Slight...

Notes/Observations

- G20 communique to reflect fears of protectionism. Disagreement remained over whether to address trade friction through a bilateral or multilateral framework

- Trade escalation seen entering its next stage with the US administration considering imposing a $60B tariff on China's $510B of exports into the US.

- UK Feb CPI comes in below expectations (YoY: 2.7% v 2.8%e); but unlikely to sway expectations that next BOE rate hike could come as soon as May

Asia:

- Japan Vice Fin Min Kihara: Told G20 recent market volatility did not reflect global economic fundamentals; communique likely to note concerns over inward looking policies. Told its G20 counterparts that protectionism benefited no country and was among key risks to the global economy as it would shrink trade

- Japan Trade Min Seko: High chance Japan would secure some exemptions from US tariffs on steel and aluminum on per-item basis

- RBA March Meeting Minutes reiterated low rates were playing a part in lowering unemployment and lifting inflation. Reiterated stance that the steady monetary policy would be consistent with sustainable growth in the economy and achieving the inflation target over time. Financial market pricing continued to imply that the cash rate was expected to remain unchanged during 2018, with a 25 basis point increase expected in the first half of 2019

- China Premier Li stated that was fully confident in achieving 2018 economic targets. Reiterated view that did not hope to see relatively big trade surplus with US and that a trade war would not be beneficial and hoped it would be avoided

Europe:

- ECB's Mersch (Luxembourg): economic recovery in the euro area had developed better than expected and employment had increased significantly; Reiterated Council view that have become more confident that inflation is on the right track

- ECB’s Weidmann (Germany) indicated rift at G20 regarding trade. Officials talked about the risks of a trade war and what it could mean for economic growth.

- Italy President Mattarella to allow several months for coalition talks on forming govt

Americas:

- President Trump said to be readying $60B package of China tariffs that could be announced by Friday, Mar 23rd (China Commerce Ministry (MOFCOM) did not comment but urged US to correct abuse of trade measures)

Energy:

- Trump-Saudi meeting scheduled for Tuesday, Mar 20th. Saudi Arabia had previously called the 2015 nuclear deal between Iran and world powers a “flawed agreement

Economic Data:

- (DE) Germany Feb PPI M/M: -0.1% v +0.1%e; Y/Y: 1.8% v 2.0%e

- (CH) Swiss Feb Trade Balance (CHF): 3.1B v 2.1B prior, Real Exports M/M: +2.3% v -4.8% prior, Real Imports M/M: -9.5% v +4.7% prior

- (DK) Denmark Mar Consumer Confidence Indicator: 8.5 v 7.5e

- (ZA) South Africa Jan Leading Indicator: 106.1 v 105.8 prior

- (FI) Finland Feb Unemployment Rate: 8.6% v 8.8% prior

- (TR) Turkey Mar Consumer Confidence: 71.3 v 72.3 prior

- (TW) Taiwan Feb Export Orders Y/Y: -3.8% v +3.5%e

- (ZA) South Africa Feb CPI M/M: 0.8% v 0.9%e ; Y/Y: 4.0% v 4.1%e

- (ZA) South Africa Feb CPI Core M/M: 1.1% v 1.1%e; Y/Y: 4.1% v 4.1%e

- (ZA) South Africa Q4 Current Account (ZAR): -137B v -106Be; C/A to GDP ratio: -2.9% v -2.0%e

- (HU) Hungary Jan Average Gross Wages Y/Y: 13.8% v 12.0%e

- (HK) Hong Kong Feb CPI Composite Y/Y: 3.1% v 2.2%e

- (UK) Feb CPI M/M: 0.4% v 0.5%e; Y/Y: 2.7% v 2.8%e; CPI Core Y/Y: 2.4% v 2.5%e; CPIH Y/Y: 2.5% v 2.6%e

- (UK) Feb RPI M/M: 0.8% v 0.8%e; Y/Y: 3.6% v 3.7%e, RPI-X (ex-mortgage interest payment) Y/Y: 3.6% v 3.6%e, Retail Price Index: 278.1 v 278.3e

- (UK) Feb PPI Input M/M: -1.1% v -0.9%e; Y/Y: 3.4% v 3.8%e

- (UK) Feb PPI Output M/M: 0.0% v 0.1%e; Y/Y: 2.6% v 2.7%e - (UK) Feb PPI Output Core M/M: 0.2% v 0.2%e; Y/Y: 2.4% v 2.4%e

- (UK) Jan ONS House Price Index Y/Y: 4.9% v 5.0%e

Fixed Income Issuance:

- (ID) Indonesia sold total IDR8.9T vs. IDR8.0T target in 6-month Islamic Bills, 2-year, 4-year, 7-year and 15-year Project-based Sukuk (PBS)

- (ZA) South Africa sold total ZAR3.3B vs. ZAR3.3B indicated in 2023, 2031, 2037 and 2048 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -0.1% at 373.3, FTSE +0.1% at 7051, DAX -0.2% at 12198, CAC-40 -0.2% at 5211, IBEX-35 -0.5% at 9618, FTSE MIB -0.1% at 22608 , SMI -0.4% at 8776, S&P 500 Futures -0.2%]

- Market Focal Points/Key Themes: European Indices drift into negative territory tracking US futures lower, with the Nasdaq continuing to underperform with Facebook remaining in focus following privacy backlash. On the corporate front solid earnings from Tom Tailor, Partners Group and Bellway saw shares higher, while John Wood Group, Ocado, 888 Holdings were some of the names lower after results. In the M&A space Fenner trades sharply higher after its to be acquired by Michelin for £1.2B, whilst Rio Tinto trades higher after divesting its interest in Hail Creek coal mine. Looking ahead notable earnings include Children's Place and Duluth holdings.

Movers

- Consumer Discretionary [ Fingerprint Cards [FINGB.SE] -6.9% (New CFO), 888 Holdings [888.UK] -5.8% (Earnings), Ocado [OCDO.UK] -1.4% (Trading update), Mears Group [MER.UK] -1.4% (Earnings) ]

- Industrials [ John Wood Group [WG.UK] -1.6% (Earnings) ) ]

- Financials [ Partners Group [PGHN.CH] +2.3% (Earnings) ]

- Technology [Fingerprint Cards [FINGB.SE] -6.9% (New CFO), Delarue [DLR.UK] -11% (Earnings) ]

- Energy [ BKW [BKW.CH] +4% (Earnings)]

- Real Estate [ Bellway [BWY.UK] +2.7% (Earnings)]

Speakers

- Swiss SECO March 2018 Economic Forecasts raised both 2018 and 2019 GDP growth forecasts but warned the US protectionism stance was a risk to the global economy

- Bundesbank Dombret (ECB SSM member): Brexit banks should file license applications by June

- EU Parliamentary official Huebner: Saw support for giving ECB clearing oversight

- South Africa Hawks police unit: No investigation of Gordhan (refutes new speculation)

- Bank of Korea (BOK) Feb Minutes: One member saw the need for a rate hike but the timing was uncertain while another member noted that reaching the 2% inflation target looked unclear

- Japan said to consider summit with South Korea and China after Golden Week

- BOJ Dep Gov Amamiya stated that the country was not in deflation but still far from inflation target. Would do the utmost to end deflation. Needed to continue with easing persistently. Challenges included exit and side effect of current policy. No need to consider rate hike at this time; didnot rule out adjusting rates before hitting inflation target (in-line with Gov Kuroda views)

- BOJ Dep Gov Wakatabe: Had no preconceptions on policy as aim was to hit price target asap. Did have tools for more easing. Needed to avoid any premature shift in policy but should not hesitate to add to easing if needed. Various data showed positive impact of easing. Benefits of monetary easing had yet to spread through economy

- S&P affirmed Hong Kong sovereign rating at AA+; outlook stable

- OPEC/Non-Opec committee said to see market re-balancing by Q3

Currencies

- The focus has been on trade over the past 24 hours as G20 meets in Argentina. Dealers note that an escalation on trade issues was now seen entering its next stage with the US administration considering imposing a $60B tariff on China's $510B of exports into the US by the end of the week.

- The USD/JPY pair moved higher as the session began after a Japanese official noted that the country would secure some exemptions from US tariffs on steel and aluminum on per-item basis. The pair peaked at 106.60 after the new BOJ Dep Govs Amamiya and Wakatabe touted the BOJ standard rhetoric. Both new members noted that they saw no need to consider rate hike at this time but did not rule out adjusting rates before hitting inflation target

- EUR/USD maintained some legs after reports circulated on Monday that the ECB policymakers had begun shifting the debate towards the steepness of the rate path with even the most dovish members accepting that QE should end this year. The pair was steady at 1.2340 and still well-contained with the 4 big figure range that has enveloped the pair this year.

- The GBP/USD was building to its gains in the aftermath of an agreement on the Brexit transition ahead of the EU Leaders summit this week. Focus was on key inflation data ahead of Thursday’s BOE rate decision. UK Feb CPI came in below expectations (YoY: 2.7% v 2.8%e); but was viewed as unlikely to sway expectations that

Fixed Income

- Bund Futures trade 16 ticks lower at 157.99 ahead of the March German ZEW survey. Upside targets 158.75, while a return lower targets the157.25 level.

- Gilt futures trade at 122.62 down 14 ticks after softer than expected UK inflation. Support continues to stand at 120.75 then 120.15, with upside resistance at 122.85 then 123.35.

- Tuesday’s liquidity report showed Monday's excess liquidity fell to €1.824T from €1.834T prior. Use of the marginal lending facility stayed steady at nil.

Looking Ahead

- G20 Meeting continues in Argentina

- (PL) EU update on Poland Rule of Law (no decision expected)

- Saudi Crown Prince Mohammed bin Salman meets President Trump in Washington

- (IL) Israel Mar 12-month CPI Forecast: No est v 0.8% prior

- (AR) Argentina Feb Budget Balance (ARS): No est v 3.9B prior

- 06:00 (DE) Germany Mar ZEW Current Situation: 90.0e v 92.3 prior; Expectations Survey: 13.0e v 17.8 prior

- 06:00 (EU) Euro Zone Mar ZEW Expectations Survey: No est v 29.3 prior

- 06:00 (IT) Italy's Berlusconi gathers newly-elected lawmakers

- 06:00 (EU) Daily Euribor Fixing

- 06:15 (CH) Switzerland to sell 3-month Bills - 06.30 (UK) Weekly John Lewis LFL sales data

- 06:30 (EU) ECB allotment in 7-Day Main Refinancing Tender (MRO)

- 06:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills;

- 06:30 (DE) Germany to sell €4.0B in 0% Mar 2020 Schatz

- 07:00 (IL) Israel Jan Manufacturing Production M/M: No est v -0.5% prior

- 07:00 (TR) Turkey to sell 2019 and 2028 bonds

- 07:30 (EU) ESM to sell €2.0B in 6-month bills

- 07:45 (US) Weekly Goldman Economist Chain Store Sales

- 07:45 (US) Daily Libor Fixing

- 08:00 (RU) Russia announces weekly OFZ bond auction

- 08:30 (CA) Canada Jan Wholesale Trade Sales M/M: +0.1%e v -0.5% prior

- 08:30 (NZ) Fonterra Global Dairy Trade Auction

- 08:55 (US) Weekly Redbook Sales

- 09:05 (US) Baltic Dry Bulk Index

- 10:00 (EU) Weekly ECB Forex Reserves

- 10:30 (CA) Canada to sell 3-month, 6-month and 12-month bills

- 10:45 (UK) BOE APF Gilt purchase operation (over 15-years)

- 11:00 (EU) Euro Zone Mar Advance Consumer Confidence: 0.0e v 0.1 prior

- 11:00 (CO) Colombia Jan Trade Balance: -$0.6Be v +$0.5B prior; Total Imports: $3.8Be v $3.6B prior

- 11:30 (US) Treasury to sell 4-Week Bills

- 15:00 (AR) Argentina Q4 Unemployment Rate: 7.5%e v 8.3% prior

- 15:00 (CO) Colombia Central Bank Interest Rate Decision: Expected to leave Overnight Lending Rate unchanged at 4.50%

- 15:00 (MX) Mexico Citibanamex Survey of Economists

- 16:30 (US) Weekly API Oil Inventories

- 17:00 (CL) Chile Central Bank (BCCH) Interest Rate Decision: Expected to leave Overnight Rate Target unchanged at 2.50%

Sterling Slips On Inflation Slowdown, Oil Rises

The British Pound immediately weakened against the Dollar on Tuesday morning after UK inflation fell more than expected in February.

Consumer price inflation eased to a 7-month low at 2.7% in February, down from 3% in January, as the impact of Sterling’s Brexit-fuelled selloff faded. Today’s weaker than expected inflation figures are unlikely to budge market expectations of the Bank of England raising UK interest rates in May. However, if wage growth figures published on Wednesday print in line with forecasts at 2.6%, this could ease some pressure on the BoE to take further action beyond May. With the British Pound still noticeably sensitive to monetary policy speculation, bears exploited the fall in inflation to drag the GBPUSD towards 1.4020.

From a technical perspective, the GBPUSD still remains at risk of sinking lower if bulls are unable to maintain control above the 1.4000 level. A breakdown and daily close below 1.4000 could invite a decline towards1.3930 and 1.3850, respectively.

Dollar steady ahead of FOMC meeting

The Dollar was steady against a basket of major currencies ahead of the heavily anticipated Federal Reserve policy meeting under the new Fed Chairman, Jerome Powell.

With the central bank widely expected to raise interest rates in March, much focus will be directed towards the “dot plots” and Powell’s first press conference. Investors are likely to closely scrutinize the policy statement and conference for clues on whether the Fed will raise interest rates 3 or 4 times this year. King Dollar could be exposed to downside risks if Powell comes across less hawkish than market expectations. Although speculation of higher rates has the ability to support the Greenback, political uncertainty in Washington remains an invitation for bears to attack.

Focusing on the technical picture, the Dollar Index is at risk of trading lower if prices are unable to keep above the 90.00 level. Repeated weakness below 90.00 could encourage a decline towards 89.50. If bulls are able to maintain control above 90.00, then the Dollar Index has scope to challenge 90.30 and 90.50, respectively.

Global stocks gripped by caution

Global equity markets were a sea of red on Monday, as the unsavoury combination of US interest rate jitters and lingering tradewar fears eroded risk appetite.

In Asia, stocks stumbled in Tuesday’s trading session following an overnight decline on Wall Street. Although European markets opened on a firmer note, investors still remained guarded ahead of the Fed meeting. With Wall Street suffering painful losses on Monday thanks to a Facebook-led tech selloff, U.S stocks remain vulnerable to further downside amid the growing caution this afternoon. Political uncertainty in Washington coupled with heightened fears over global trade tensions has clearly left market sentiment fragile. Stock markets are likely to remain exposed to downside shocks, as uncertainty encourages investors to scatter away from riskier assets to safe-haven investments.

Commodity spotlight – WTI Oil

Oil prices have appreciated as continued tensions in the Middle East stimulated concerns over potential supply disruptions.

While news of the United States potentially re-imposing sanctions on Iran could fuel the current upside, growing fears of rising U.S production are likely to create headwinds for bulls down the road. With the oversupply concerns still a major theme impacting oil prices, WTI Crude remains vulnerable to heavy losses.

Focusing purely on the technical picture, WTI experienced a technical breakout above the $62.00 l

New BoJ deputies Wakatabe and Amamiya sound cautious in inaugural press conference

The two new BoJ Deputy Governors spoke in the inaugural news conference today.

Masazumi Wakatabe said that BoJ sounded cautious as he said BoJ should avoid premature shift in monetary policy. Also, in his view, the central bank shouldn't hesitate to ease monetary policy further if needed. Nonetheless, she acknowledged that various economic data already showed the positive impacts of current and past ultra loose policy.

Masayoshi Amamiya, also emphasized the importance to continue with powerful monetary easy, for achieving improvements in the output gap. He acknowledged that Japan is no longer in deflation. But BoJ hasn't meet its 2% inflation target yet.