Sample Category Title

Market Morning Briefing: Euro Dipped After Seeing A High Near 1.2355

STOCKS

Dow (24727.27, +0.47%) and Dax (12307.33, +0.74%) have risen slightly yesterday. Dow looks bearish while below 25000 while Dax may come off while below 12500. The rejection from levels near 12500 has not produced a sharp rejection for Dax and the index is stuck in the 12200-12500 zone. A break on either side would determine the further directional course. Another dip if seen could take Dow towards 24200 and Dax towards 12200.

Nikkei (21380.97, -0.47%) has support just below current levels. While Dollar Yen remains ranged in the 107.50-106.0 region, Nikkei may trade above support with the upper limit near 22500 just now.

Shanghai (3309.83, +0.58%) seems to be trading in the 3350-3230 region and is likely to remain sideways for now.

Nifty (10124.35, +0.30%) has bounced back from levels near 10070 and if that sustains, the index could move up towards 10320 in the coming sessions. Sensex (32996.76, +0.22%) has also bounced a bit and could test 33250 on the upside. The trade region could narrow in the coming sessions.

COMMODITIES

Brent (67.63) has moved up sharply after the API reports suggested a surprise draw of 2.739 million barrels of United States crude oil inventories for the week ending March 16. News states an anticipation of 2.556 million barrels in crude oil inventories—a discrepancy of over 5 million barrels. Brent could test decent resistance near 68 which could produce a slight dip towards 66.

Nymex WTI (63.75) could also test resistance near 64 and come off towards 62.50 by the end of the week.

Gold (1312.80) is headed towards 1300 in the next few sessions. Near term looks weak.

Copper (3.0485) has broken below the support near 3.05 on the daily candle chart and could now come down further to test 3.00. In case 3.00 is able to produce a bounce, the index could head higher towards 3.10, else a break below 3.0, if seen would be vulnerable to a sharp fall in the medium term.

FOREX

Dollar index (90.303), against our expectation, has again moved up, breaching immediate resistance near 90.25-90.30 on the daily candles. It saw a high of 90.45 yesterday and is currently trading below that level, possibly indicating that resistance level on weekly candles near 90.5 could hold. However, at this stage there is also some room on the 3 day candles and daily line chart for the Dollar Index to rise towards resistance near 91.

We again highlight below the importance of the Fed meeting later today:

'A lot could depend on the US Fed meeting today, where a rate hike of 25 bps is expected. Whether a rate hike and a possible rise in US yields subsequently are positive for Dollar strength or not would have to be seen –the usually positive correlation between bond yields and currency strength has not worked for the Dollar in the past 3-4 months and whether this particular rate hike can reinstate the previous correlation would be something to watch out for in the coming weeks. Our preference is for the negative correlation to continue ie for the Dollar to see a dip.”

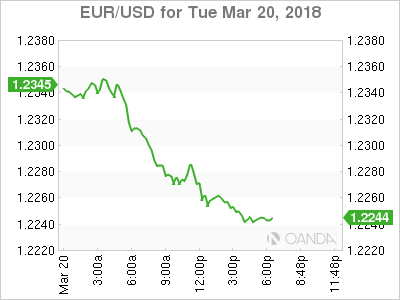

Euro (1.2256) – Against expectations, Euro dipped after seeing a high near 1.2355 yesterday and is currently testing support near 1.225 on the daily candles. There is crucial lower support on daily candles, 3 day candles, daily line chart and 3 day line chart near 1.2200-1.2175, which if broken would be bearish for the Euro in the medium term.

The Euro has been seeing sideways movement in the broad 1.215-1.255 zone for the last 8 weeks. We have been saying that a decisive breakout on the upside beyond higher resistance on 3 day candles near 1.255 could be on the cards within the next couple of weeks. The US Fed meeting later today could be the decider on that.

Dollar Yen (106.49) after having tested immediate resistance on daily candles near 106.5-106.6 might see a dip now. Resistance near current levels is also being provided by the 21 days moving average line on daily line chart and the 5 week moving average line on the weekly line chart. In the less preferred case of Dollar strength after the US Fed meeting today, the Dollar Yen could rise further towards resistance (earlier support) near 107 on the 3 day line chart.

We have been saying that the Dollar Yen might be about to turn bearish towards 105 and lower within the next 1-2 weeks. A break of 105, would be crucial since the Dollar Yen hasn’t been able to move below that level for more than a year.

Euro Yen (130.51) is seeing a dip after testing (and slightly breaching) immediate resistance on daily candles near 131.5. There is strong support visible now near 130 on daily, 3 day and weekly candles.

Pound (1.40) had bounced after testing support near 1.38 on 3 day candles last week. It might pause slightly in its upmove if there is re-emergence of global Dollar strength after the Fed meeting. However, in case the Dollar doesn’t strengthen, we could see the Pound test resistance near 1.44 on 3 day candles and line chart in the coming 1-2 weeks.

Dollar Rupee (65.195) is overall bullish while above 65.00. But, upside is limited to 65.40-60.

INTEREST RATES

Global bond yields are expected to react to the Fed meeting today. US yields have already started moving up in anticipation of a rate hike.

US 10 Yr Yield (2.8959), 30 Yr (3.13), 5 Yr (2.696), 2 Yr (2.344):

We repeat yesterday’s comment that: Data releases over the past week have put up a contrasting view of the US economy – CPI, Retail Sales, Wage Growth and Housing Starts data indicated a pause in growth while Capacity Utilization, unemployment claims, Industrial Production and Import Prices data indicated a surge in growth. We expect the US Fed to hike rates today but at the same time strike a balance by not being too hawkish in the press conference. We might be wrong and the Fed could surprise everyone - lets wait and watch.

In our Mar ’18 US Treasury report (available on demand), we keep an upside target of 3.075% for the 10 Year yield, 3.3% for the 30 Yr yield and 2.925% for the 5 Year yield in Apr’18. We also see yields again declining in May-Jun.

Let’s wait for the Fed meeting today to see how bond yields shape up.

GBP finds footing as UK employment data eyed

For now, Sterling is still trading as the second strongest major currency for the week despite yesterday's post CPI dip. Employment data will be a main focus today. Markets expect claimant counts to dropped -3.1k in February. ILO unemployment rate is expected to stay unchanged at 4.4% in January. A key focus is on wage growth as average weekly earnings is expected to rise 2.6% 3moy in January. Still, with CPI at 2.7% yoy, wage is still playing catch up.

Reaction to the job data could be muted though as the major focus is on tomorrow's BoE rate decision. BoE is widely expected to keep bank rate unchanged at 0.50% and asset purchase target at GBP 435b. No updated economic projections will be delivered as they were published back in February's Inflation Report already. Instead, eyes will be on whether BoE would turn more upbeat in the statement, given that a Brexit transition deal is already done. In addition, known hawks Michael Saunders and Ian McCafferty could come back with a vote on rate hike. All in all, focus in on gauging the chance of a May hike.

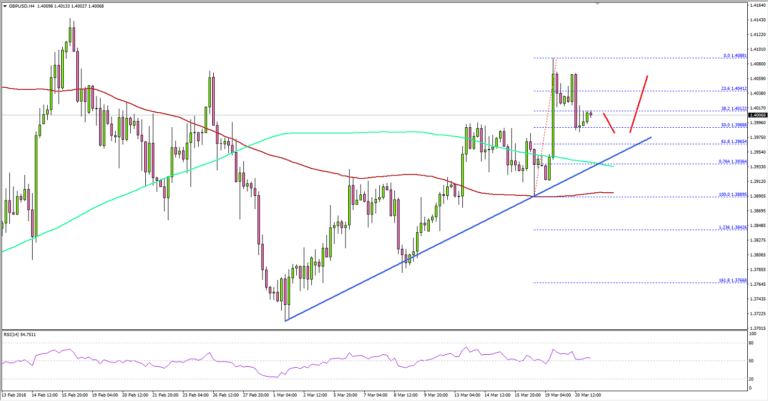

GBP/USD Downsides Remain Supported Above 1.3950

Key Highlights

- The British Pound recently made a short-term top at 1.4080 against the US Dollar.

- There is a crucial bullish trend line in place with support at 1.3950 on the 4-hours chart of GBP/USD.

- The UK CPI in Feb 2018 increased 0.4%, less than the forecast of +0.5% (MoM).

- Today, the UK Claimant Count Change for Feb 2018 will be released, which is forecasted to post -5K.

GBPUSD Technical Analysis

The British Pound climbed earlier this week and moved above 1.4000 against the US Dollar. The GBP/USD pair failed to move past 1.4080-1.4100 and started a downside correction.

It declined and tested the 50% Fib retracement level of the last wave from the 1.3889 low to 1.4088 high. However, there are many supports on the downside around the 1.3950-60 levels.

There is also a crucial bullish trend line in place with support at 1.3950 on the 4-hours chart. Furthermore, the 200 simple moving average (green, 4-hours) is at 1.3935, which is also a major support.

More importantly, the 61.8% Fib retracement level of the last wave from the 1.3889 low to 1.4088 high is at 1.3965. Therefore, the 1.3950-1.3960 area is a decent support region.

As long as the pair is above the 1.3950 level, it remains supported for more gains. On the upside, the pair may find is difficult to break the 1.4080 and 1.4100 resistance levels.

Recently in the UK, the Consumer Price Index (CPI) for Feb 2018 was released by the Office for National Statistics. The market was looking for a 0.5% rise in Feb 2018 compared with the previous month.

The real outcome was a bit below the forecast as the CPI increased by 0.4%. In terms of the yearly change, there was a rise of 2.7%, less than the forecast of 2.8% and previous 3%.

The report added that:

The largest downward contributions to the change in the rate came from transport and food prices, which rose by less than a year ago. Falling prices for accommodation services also had a downward effect. Rising prices for footwear produced the largest, partially offsetting, upward contribution.

Overall, the GBP/USD pair may consolidate above 1.3950 for some time before making the next move. However, today’s UK CPI release and the Fed interest rate decision could impact pairs like EUR/USD, GBP/USD, USD/JPY and AUD/USD in the near term.

Economic Releases to Watch Today

- UK Claimant Count Change Feb 2018 – Forecast -5.0K, versus -7.2K previous.

- UK ILO Unemployment Rate Jan 2018 (3M) – Forecast 4.4%, versus 4.4% previous.

- US Existing Home Sales for Feb 2018 (MoM) – Forecast +0.5%, versus -3.2% previous.

Feb Interest Rate Decision – Forecast 1.75%, versus 1.5% previous.

CAD rebounds as US dropped one of the toughest protectionist demand in NAFTA talks

Canadian Dollar rebounds strongly on news that US will drop contentious auto-content proposal in NAFTA talks. It's seen as clearing and important road block in NAFTA renegotiation. The Loonie is trading as the strongest major currency in Asian session.

There was a demand for vehicles made in Canada and Mexico for export to the US contain at least 50% US content. But Canada's Globe and Mail reported that this contentious demand was dropped during NAFTA meeting in Washington last week. This is seen by some as one of the US toughest protectionist demand.

CAD is now the strongest one as seen in heatmap for today, followed by Euro. NZD, AUD and USD are the weakest ones.

From Action Bias chart, 6H bias turned neutral after USD/CAD hit 1.3124. And H bias turned negative with current dip through 1.305. For now, it's more of a correction then a change in trend.

From Action Bias chart, 6H bias turned neutral after USD/CAD hit 1.3124. And H bias turned negative with current dip through 1.305. For now, it's more of a correction then a change in trend.

Trump to announce tariffs on Chinese goods on Thursday, but will seek industry input before finalizing

US President Donald Trump is set to announce the package of tariffs against Chinese goods on Thursday, a day earlier than rumored. It's believed that the total amount of targeted goods adds up to USD 30-60b. We believe that it will be on the higher side on the range. Additionally, there will be new restrictions on Chinese investments in the US. Treasury will be directed to outline the rules regarding Chinese investments.

But, it's reported that the tariffs won't take effect immediately. Instead, businesses are given a chance to comment on the list of tariffed products. The final decision will come after industry input. This is seen as an act of Trump bowing down to pressure from business leaders. Earlier this week, 45 of largest American trade groups wrote an open letter to Trump, warning Trump not to respond to unfair Chinese practices and policies by measures that will "harm U.S. companies, workers, farmers, ranchers, consumers, and investors."

Everything That Needs To Be Said Has Already Been Said

Everything that needs to be said has already been said

I'm not sure if there's anything I can say that hasn't already been said about this weeks Fed meeting, but with the multitude of notes and conjectures floating around one thing that is abundantly clear, with regards to forwarding guidance, no one knows what to expect.

What we do know, however, is this meeting has lots of eyes on it and not just because it's Jerome Powell's first post FOMC press conference, but there's likely to be some nuanced changes in the Fed statement.

Since the December meeting, inflation has shown signs of coming to life, although the latest round of data would challenge that view. But more significantly Fed speak has turned marginally more hawkish of late, suggesting we should expect some upgrade to the statement, at the minimum. But during the period the markets endured a colossal collapse in equity markets at the prospects of higher US interest rates, so the big question will be how does the Fed nudge rate hike expectations higher, without tipping the apple cart.

In typical fashion, however, traders are hedging for the possible extreme outcomes. While markets tend to overhype these events, but this time around the air is so thick with uncertainty, and the fear of the unknown is driving sentiment. But at the end of the day, will that extra dot, which is little more than a central bank projection, make that much of a difference in the global competition for investment dollars?

In general, much of the cross-asset price action was more a reflection of pre-FOMC positioning, as the markets reversed out Monday's dollar weakness and the US equity markets are finding support on the back of the energy sector, in spite of Facebooks continuing woes.

Oil Markets

In addition to the Middle East (geo) political issues and Venezuelan supply concerns, the American Petroleum Institute( API) report is providing a further fillip to oil prices, the API reported a surprise draw of 2.739 million barrels which is an enormous 5 million barrels disparity from analysts expectations. That's a vast delta and should support a short-term bid on dip mentality despite the longer term bearish implication of rising US shale production.

However, traders are looking over their shoulder at the worrying signs from the industrial commodity complex which is plunging on a waning global growth narrative, something that certainly doesn't bode well for oil producers either.

Gold Markets

The gold market's reversed out Monday's gains as the US dollar picked up steam ahead of Fed rate decision. While higher interest rates typically weigh on gold sentiment, I'm struggling to factor in just how much competition the possible one extra dot plot will have for Gold demand. Tail risk demand in the face of gusting headwinds from risk-appetite, heightened (geo) political tensions, inflation concerns, trade wars not to mention the runaway budget deficit spending which should serve to counteract the well-expected FOMC rate hike should keep the floor on gold prices intact.

Currency Markets

The markets should tie a string around their finger to remind themselves it's not uncommon for the dollar to recover from bearish extremes ahead of an FOMC meeting

The Euro

The markets went Dollar bid across the board after the latest Germany ZEW survey results came in worse than expected, which reversed out much of the ECB inspired Euro rally and more from the previous day. The obvious implications are the ZEW reading is implying the stronger EUR is weighing on Germany' s economy and by extension, the ECB will remain dovish.

The Japanese Yen

Little more than waiting and watching but some mild intrigue overnight after BOJ'S AMAMIYA: DON'T RULE OUT ADJUSTING RATES BEFORE HITTING 2%” (Bloomberg) inspired a brief spike lower but reversed out just a quickly.

While trader remains nervous about a pre-FOMC squeeze higher, provide there's not an out of the box response from Jerome Powel the market will likely initially fade any interest rate inspired move higher, as that strategy has served traders through a multitude of risk events this year.

The Malaysian Ringgit

Local Ringgit traders and investors are so preoccupied with FOMC's forward guidance and Fed fund rates dot-plot projection that MYR demand has dwindled. A steeper rate hike trajectory is keeping region markets apprehensive, and when you factor in the adverse domestic equity price action of late, the MYR continues to struggle short term. But for the Ringgit, we are miles away from a crossroads in sentiment as even in the face of a one-dot increase in the Fed projections the current account driven MYR should remain in favour regionally.

US Dollar Rises Ahead Of Fed Rate Announcement

The USD is higher against major pairs before the end of the March central bank meeting. The U.S. Federal Reserve will publish its Federal Open Market Committee (FOMC) statement on Wednesday, March 21 at 2:00 pm EDT. The US central bank will also release its economic projections for the quarter which could end up signalling more than the three interest rate hikes forecasted in December. The CME FedWatch tool shows a 94.4 percent probability of a 25 basis points rate hike taking the Fed funds rate to 1.50–1.75 percent. Chair Jerome Powell will host his first post-FOMC press conference at 2:30 pm EDT.

- The Fed is anticipated to raise rates by 25 bps

- The Fed will release its economic projections

- US crude oil inventories forecasting a buildup of 2.5 million barrels

The EUR/USD lost 0.63 percent in the last 24 hours. The single pair is trading at 1.2258 ahead of the U.S. Federal Reserve statement. The majority of market watchers anticipate a 25 basis points lift. Economic projections will take on more importance as investors look for clues on the Fed’s rate hike path. Jerome Powell’s press conference will add the most uncertainty to the proceedings as he kicks off his term at the head of the central bank. He is expected to follow on his predecessor direction and keep hiking interest rates, but unlike Yellen he has a more hawkish FOMC that might need tempering to avoid coming out too hawkish and sending the wrong signal to the market.

This week the USD has appreciated 0.31 percent versus the USD on the back of strong fundamentals and a supportive central bank despite the political drama in Washington. American growth is now expected to be on par or surpass European growth which is cooling even as the European Central Bank (ECB) continues to run a stimulus program with no rate hike in sight for 2018.

The US tax reform is one of the victories of the Trump administration and its impact will be considered by the Fed in updating its economic outlook. The case for adding a fourth rate lift in 2018 is one of the biggest questions that will be answered on Wednesday.

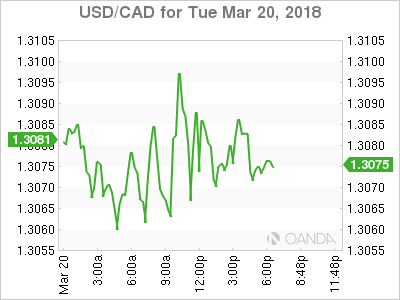

The USD/CAD rose 0.05 percent on Tuesday. The currency pair is trading at 1.3084. The Canadian dollar recovered slightly earlier in the week after touching 9 month lows last week. The CAD is down 4 percent since the start of the year after a slowdown in economic indicators and the protectionist trade rhetoric of the Trump administration.

Canadian Prime Minister Justin Trudeau has remained optimistic about the fate of NAFTA. The PM said on Monday that US President Donald Trump appears enthusiastic about agreeing to a trade deal renegotiation. The fact remains that after seven rounds of talks there has been little progress and the feeling of acceleration at this point could also be desperation as elections in the three nations could threaten to derail negotiations.

The announced US tariffs on steel and aluminum hit the Canadian currency, even though those tariffs were later revelled to not be applicable for Canada and Mexico. The last thing the team of NAFTA negotiations needed to hear was the US announcing tariffs just as they discuss the divisive trade agreement. The eight and final round of talks is yet to be scheduled but will take place in the United States in April.

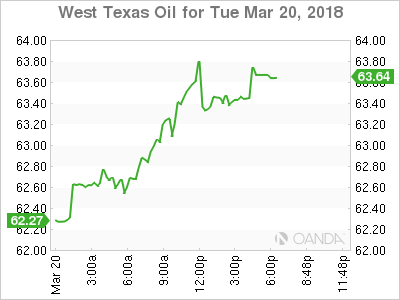

Oil prices rose on Tuesday. The West Texas Intermediate is trading at $63.44 on the back of rising concerns about the Iran nuclear deal. Saudi Crown Prince Mohammed bin Salman is visiting Washington with one of the items in the agenda is to ask US President Trump to toughen its sanctions against Iran. The political differences between the two Organization of the Petroleum Exporting Countries (OPEC) members has driven up prices before, but at this moment the OPEC production cut is one the biggest factors in current energy price stability.

US shale producers are forecasted to start ramping up production to take advantage of current prices. Weather and other disruptions has limited their production ability, but it is not expected to last. OPEC supply has been kept lower thanks to the agreement that runs until the end of 2018. Ongoing discord between members could end up breaking the agreement sooner although so far Russia the biggest non-OPEC participant has pledged its commitment to the deal until the end of the deadline and beyond if necessary.

US weekly inventories of crude will be published on Wednesday, March 21 at 10:30 am EDT. There is a forecasted buildup of 2.5 million barrels which is a slowdown from the higher 5 million buildup in the last report. US crude stocks have risen for the past three weeks and could add a fourth one as shale producers slowly ramp up production.

Market events to watch this week:

Wednesday, March 21

5:30am GBP Average Earnings Index 3m/y

10:30am USD Crude Oil Inventories

2:00pm USD FOMC Economic Projections

2:00pm USD FOMC Statement

2:00pm USD Federal Funds Rate

2:30pm USD FOMC Press Conference

4:00pm NZD RBNZ Rate Statement

8:30pm AUD Employment Change

Thursday, March 22

5:30am GBP Retail Sales m/m

8:00am GBP MPC Official Bank Rate Votes

8:00am GBP Monetary Policy Summary

8:00am GBP Official Bank Rate

Friday, March 23

8:30am CAD CPI m/m

8:30am CAD Core Retail Sales m/m

8:30am USD Core Durable Goods Orders m/m

G20 stressed importance of trade, urged further dialogue, nothing more

G20 finance ministers and central bank governors ended the summit in Buenos Aires with a joint communique that emphasized the importance of international trade. And they urged for the need for "further dialogue and actions". But the communique fell short of anything else to push back protectionism.

The communique noted "International trade and investment are important engines of growth, productivity, innovation, job creation and development." And, "we reaffirm the conclusions of our Leaders on trade at the Hamburg Summit and recognise the need for further dialogue and actions." They pledged to work to "strengthen the contribution of trade to our economies."

Below is the full communique covering areas like technology, infrastructure, global financial system, cross-border capital flow, debts, international tax system and even Cryto-assets. But trade wasn't mentioned beyond the first paragraph.

Communiqué

Finance ministers and central bank governors

March 20, 2018, Buenos Aires

The global economic outlook has continued to improve since we last met in October 2017, with the broadest synchronised global growth upsurge since 2010, and a pick-up in investment and trade. While we welcome this progress, recent market volatility despite sound fundamentals of the global economy is a reminder of risks and vulnerabilities. Downside risks persist and, over the medium term, challenges remain to raise growth and make it more inclusive. This is our moment to take action to address structural growth impediments, rebuild buffers, reduce excessive global imbalances, and mitigate risks. We discussed key risks to the outlook, including financial vulnerabilities that could be revealed with a faster than expected tightening of financial conditions and heightened economic and geopolitical tensions. We agree to continue using all policy tools to support strong, sustainable, balanced and inclusive growth. We will implement structural reforms to enhance our growth potential. Fiscal policy should be used flexibly and be growth-friendly, prioritise high quality investment, while enhancing economic and financial resilience and ensuring debt as a share of GDP is on a sustainable path. Strong fundamentals, sound policies, and a resilient international monetary system are essential to the stability of exchange rates, contributing to strong and sustainable growth and investment. Flexible exchange rates, where feasible, can serve as a shock absorber. We recognise that excessive volatility or disorderly movements in exchange rates can have adverse implications for economic and financial stability. We will refrain from competitive devaluations, and will not target our exchange rates for competitive purposes. International trade and investment are important engines of growth, productivity, innovation, job creation and development. We reaffirm the conclusions of our Leaders on trade at the Hamburg Summit and recognise the need for further dialogue and actions. We are working to strengthen the contribution of trade to our economies.

Technology, including digitalisation, is fundamentally reshaping the global economy given its borderless and intangible nature, and its increasing ability to automate cognitive tasks. We are developing a common understanding of the nature of the changes and their potential implications. Transformative technologies are expected to bring immense economic opportunities, such as new ways of doing business, new industries, new and better jobs, and higher GDP growth and living standards. At the same time, the transition creates challenges for individuals, businesses, and governments. These include changes to labour markets, the growing importance of skills and adaptability, and the risk of increased inequality within and between countries. Policy responses, including international cooperation, are needed to harness the opportunities and ensure the benefits are shared by all. We therefore agree to develop a menu of policy options for consideration at our meeting in July.

Infrastructure is critical to boost productivity, enhance connectivity, sustain long-term inclusive growth and provide our citizens with physical and digital access to the new economy. Despite its importance, a persistent infrastructure financing gap remains. Public financing of infrastructure is essential but mobilising additional private capital is needed to meet global infrastructure needs. To achieve this, we agree to promote the necessary conditions to help develop infrastructure as an asset class. To guide our work, we endorse the Roadmap to Infrastructure as an Asset Class which builds on the outcomes of past G20 presidencies and draws together the steps needed to achieve our ambition. The Roadmap identifies seven work streams, including regulatory frameworks and capital markets, as well as quality infrastructure. In 2018, our focus under the Roadmap will be to improve project preparation, move towards greater standardisation of contracts and infrastructure financing instruments, address data gaps, and improve risk mitigation, taking into account country-specific conditions. We look forward to continuing and deepening the dialogue with the private sector.

We note the report of the Independent Board of the Global Infrastructure Hub recommending renewal of its mandate. We call for coordination among current initiatives sponsored by MDBs and others to avoid duplication of efforts.

We reaffirm our commitment to further strengthening the global financial safety net with a strong, quota-based, and adequately resourced IMF at its centre. We are committed to concluding the 15th General Review of Quotas and agreeing on a new quota formula as a basis for a realignment of quota shares to result in increased shares for dynamic economies in line with their relative positions in the world economy and hence likely in the share of emerging market and developing countries as a whole, while protecting the voice and representation of the poorest members by the Spring Meetings of 2019 and no later than the Annual Meetings of 2019.

Cross-border capital flows offer significant benefits, but their size and volatility may pose policy challenges. We will continue to monitor capital flows and refine our understanding of the tools to improve the resilience of the international monetary system. We recognise the importance of macroprudential policies in limiting systemic risk. We continue to deepen our understanding of capital flow management measures and the conditions under which they might be effective, taking into account country-specific circumstances. We are looking forward to further work by the IMF, based on the IMF Institutional View on Capital Flow Management, that will help inform country actions and to the results of the Review of the OECD Code of Liberalisation of Capital Movement.

Rising debt levels in Low Income Countries (LICs) have led to concerns about debt vulnerabilities in these economies. We agree that building capacity in public financial management, strengthening domestic policy frameworks, and enhancing information sharing could help avoid new episodes of debt distress in LICs. We call for greater transparency, both on the side of debtors and creditors. We reaffirm our support to the ongoing work of the Paris Club, as the principal international forum for restructuring official bilateral debt, towards the broader inclusion of emerging creditors. We support the provision of technical assistance by the IMF and the World Bank Group (WBG) in debt recording and reporting in LICs, where needed, and look forward to the work of these institutions on debt transparency.

The global financial system must remain open, resilient and supportive of growth and grounded in agreed international standards. We will continue to closely monitor and, if necessary, address emerging risks and vulnerabilities in the financial system. We welcome the finalisation of Basel III, which completes main elements of the post crisis reforms. We remain committed to the full, timely and consistent implementation and finalisation of the reforms and their evaluation to help identify and address any material unintended consequences and ensure that the reforms accomplish their objectives. We look forward to the FSB-led evaluation of the reforms, including their effects on the financing of infrastructure investment and on incentives for central clearing of over-the-counter derivatives. We will continue to address the decline in correspondent banking relationships.

We acknowledge that technological innovation, including that underlying crypto-assets, has the potential to improve the efficiency and inclusiveness of the financial system and the economy more broadly. Crypto-assets do, however, raise issues with respect to consumer and investor protection, market integrity, tax evasion, money laundering and terrorist financing. Crypto-assets lack the key attributes of sovereign currencies. At some point they could have financial stability implications. We commit to implement the FATF standards as they apply to crypto-assets, look forward to the FATF review of those standards, and call on the FATF to advance global implementation. We call on international standard-setting bodies (SSBs) to continue their monitoring of crypto-assets and their risks, according to their mandates, and assess multilateral responses as needed.

We will continue our work for a globally fair and modern international tax system and welcome international cooperation and pro-growth tax policies. We remain committed to the implementation of the Base Erosion and Profit Shifting package and welcome progress to date. The impacts of the digitalisation of the economy on the international tax system remain key outstanding issues. We welcome the OECD interim report analysing the impact of the digitalisation of the economy on the international tax system. We are committed to work together to seek a consensus-based solution by 2020, with an update in 2019.

We have made substantial progress on tax transparency. Further steps to implement transparency standards and requirements for the exchange of information for tax purposes will take place this year. Jurisdictions scheduled to commence automatic exchange of financial account information for tax purposes in 2018 should ensure that all necessary steps are taken to meet this timeline. We call on all jurisdictions to sign and ratify the multilateral Convention on Mutual Administrative Assistance in Tax Matters. We look forward to the OECD's recommendations on how to further strengthen the criteria for assessing jurisdictions compliance with internationally agreed tax transparency standards. Defensive measures will be considered against listed jurisdictions. We continue to support assistance to developing countries to build their tax capacity. We welcome the first conference of the Platform for Collaboration on Tax and the efforts undertaken to help developing countries implement the new international tax standards. We also encourage countries to enhance tax certainty.

We commit to step up our fight against terrorist financing, money laundering and proliferation financing. We call for the full, effective and swift implementation of the FATF standards worldwide. We reaffirm our support for the FATF, as the global anti money laundering and counter terrorist financing standard-setting body, to further strengthen its institutional basis, governance and capacity. We call on FATF to enhance its efforts to counter proliferation financing.

Eco Data 3/21/18

[php_everywhere instance="1"]

Gold Dips, Investors Eye Fed Announcement

Gold has posted gains in the Monday session. In North American trade, the spot price for an ounce of gold is $1311.30, down 0.45% on the day. On the release front, there are no US indicators on the schedule. on Wednesday, the US releases Current Account and Existing Home Sales. As well, the Federal Reserve is expected to raise interest rates for the first time in 2018.

Traders should be prepared for some volatility from gold prices this week, with the Federal Reserve poised to raise interest rates on Wednesday. This would mark the first hike of 2018. According to the CME Group, the odds of a quarter-point raise stand at an impressive 91 percent. What can we expect from the Fed during the year? The current Fed projection remains at three hikes, but a robust US economy has raised speculation that the Fed could accelerate the pace to four hikes, which would be good news for the US dollar. Investors will be keeping a close eye on key US data, especially upcoming inflation indicators. If these numbers improve, we’re likely to see four rate hikes in 2018.

After months of rough rhetoric between Britain and the EU, the two sides announced that there would be a transition period following the UK’s departure from the EU in March 2019. The transition deal will kick in at that time, lasting until December 2020. The deal covers the rights and status of EU citizens in the UK and British citizens in the EU, and allows the UK to pursue new trade agreements during that time. There are still some issues to iron out, such as the Northern Ireland border. The transition period is a major, positive development, in that it will enable Britain to enjoy the benefits of the common market, albeit without a seat at the table.