Sample Category Title

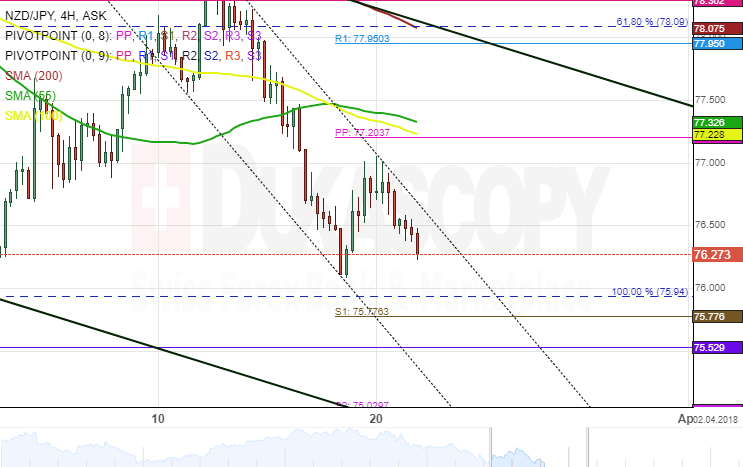

NZD/JPY 4H Chart: Expected To Decline Further

During the past three months, the New Zealand Dollar has depreciated substantially against the Japanese Yen in a descending channel. The NZD/JPY pair has provided several confirmations on both sides that the rate is likely to continue falling, the latest of which occurred last week.

After reaching the 50.00% Fibonacci retracement level, the exchange rate made a U-turn south and has since remained bearish. This retracement can be measured by connecting the low at 75.94 and the high at 81.57.

Everything being equal, the currency exchange rate is likely to decline further until it finds support cluster set by the weekly S1 and the monthly S1 near the 75.77 area. In addition, technical indicators flash sell signals.

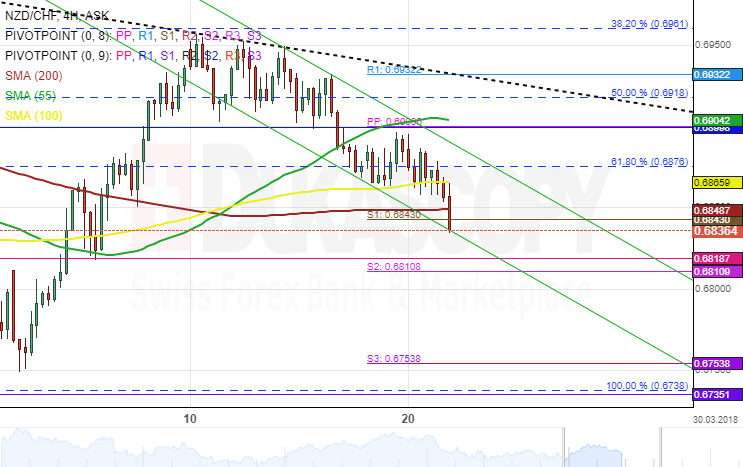

NZD/CHF 4H Chart: Trading In Narrow Channel

The New Zealand Dollar has been moving in a descending channel against the Swiss Franc since late July 2017. The upper boundary of a dominant channel was tested on July 31 and that was followed by a new wave down.After hitting the 38.20% Fib

onacci retracement level, the NZD/CHF exchange rate took a dive south and has since been trading in a narrow junior channel. This retracement can be measured by connecting the low at 0.6738 and the high at 0.7099.As for n

earest future, bears are likely to grow stronger until it breaches a support cluster set by the 200-hour simple moving average and the weekly S1 at 0.6843 where the lower boundary of the narrow channel is located.

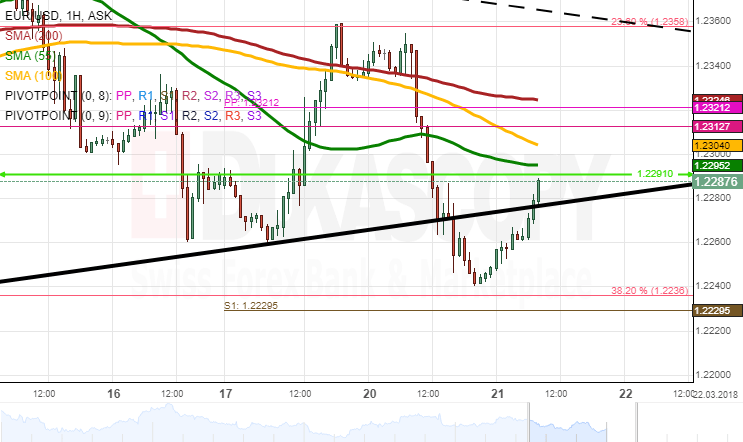

EURUSD Analysis: Bounces Off 38.20% Fibo

The US Dollar grew stronger on Tuesday, thus pushing the EUR/USD exchange rate considerably lower.

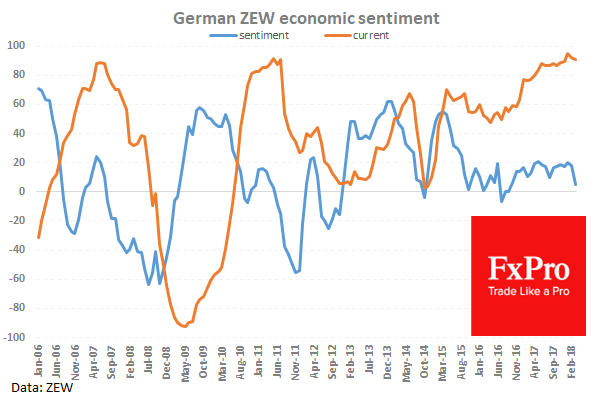

The pair started to edge south mid-session and consequently plunged 110 pips within a couple of hours, thus breaching all three moving averages and the senior channel along the way. This strong downside momentum was caused by the dismal ZEW survey which showed that German confidence fell to an unexpected low of 5.1 in February.

The first part of the day should mark a move closer to 1.2320 where several important resistance levels are located; however, it is unlikely to be surpassed. The Fed is the main focus today.

An interest hike is seemed to be priced in the market, presumably having a positive impact on the pair. Conversely, improved rate forecasts are likely to pressure the rate lower.

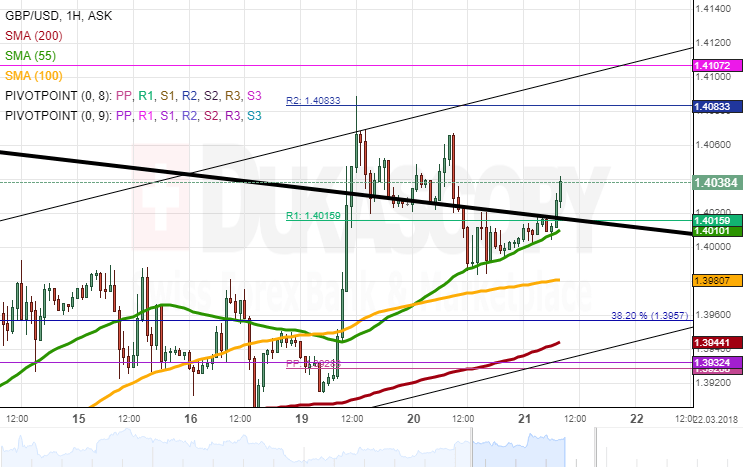

GBPUSD Analysis: Moves Along 55-Hour SMA

The Sterling was generally steady against the US Dollar on Tuesday, as traders were awaiting patiently for the Fed monetary policy statement at 1800GMT.

The only volatility during the day was introduced by the British CPI which showed sluggish performance during the previous month. Bears pressured the Pound lower for a few hours until the 55-hour SMA near 1.40 was reached.

The pair has been subsequently guided by this line, suggesting that the same situation might continue during the first part of the day when the rate might push for the weekly R2 at 1.4083. By and large, the Fed is very likely to end this still movement and elicit notable reaction.

The 1.3930 mark should restrict bearish momentum due to strong support levels. Conversely, upside potential is up to 1.4150.

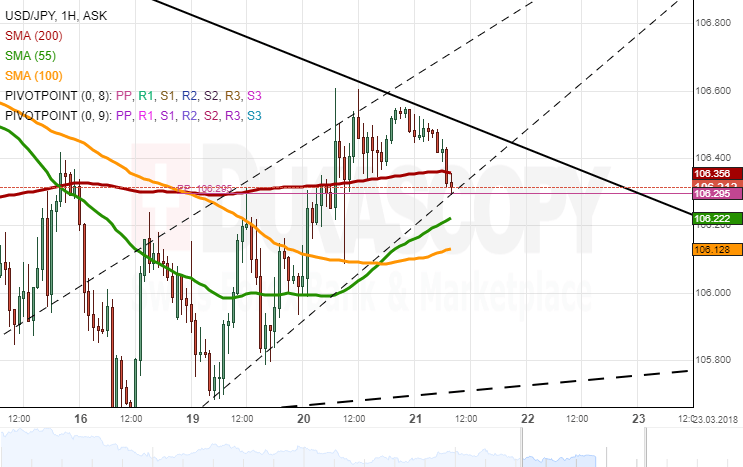

USDJPY Analysis: Consolidates Circa 106.60

Demand for the US Dollar increased on Tuesday which was boosted by positive growth in the US Treasury bonds. As a result, bulls pushed the rate past the 200-hour SMA and bounded it between this moving average and a trend-line near the 106.50 area.

Technical indicators favour the prevalence of the bearish sentiment today, as already indicated by a slight period of consolidation. From purely technical point of view, the Greenback should continue fluctuating between two trend-lines and thus target the 105.80 area within the following days. However, it is likely that traders are reluctant to breach the 200-, 55– and 100-hour SMAs prior to the FOMC statement at 1800GMT.

Given today's fundamentals, a possible trading range is relatively wide, i.e., between 106.00 and 107.00.

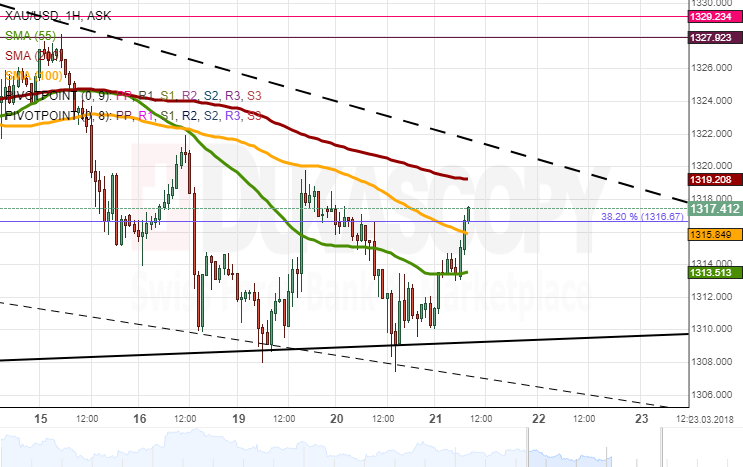

Gold Analysis: Is Moving Towards 1,320.00

Gold was generally bearish against the US Dollar on Tuesday even though it managed to regain some of the lost positions by Wednesday morning. The pair's fall during the first part of the day was stopped by a trend-line at 1,310.00 which allowed to re-acquire its position above the 55-hour SMA.

The apparent upside potential until the 1,320.00 area could be realised during the first part of the day; however, an uneventful period of consolidation is as likely prior to the FOMC statement at 1800GMT. This fundamental release is very likely to introduce volatility in the market and even direct the rate's subsequent movement.

Gains should be capped at 1,324.00, while the 50.0% Fibonacci retracement is expected to provide an unbreakable support.

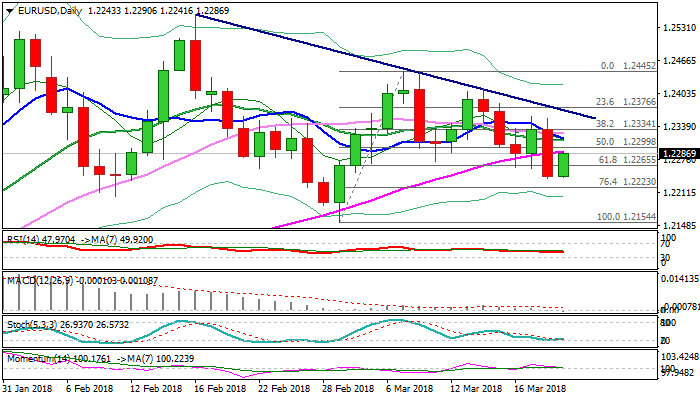

Technical Outlook: EURUSD – Close Below Cloud Top/55SMA Was Bearish Signal/ Fed Decision Would Be Next Strong Driver

The Euro bounces from three-week low at 1.2240 on Wednesday, after suffering heavy losses the day before, on fall from 1.2354 to 1.2240.

Tuesday's penetration of thick daily cloud and close below key points at 1.2295/65 (cloud top/55SMAand Fibo 61.8% of 1.2154/1.2445 rally), was bearish signal.

Bearish daily techs favor further weakness, with current upside action seen as positioning.

The action is expected to stay capped by daily cloud top/55SMA to keep bearish structure (reinforced by formation of 10/30 and 10/20SMA bears crosses) intact.

Break through initial supports at 1.2240 (Tuesday's low) and 1.2223 (Fibo 76.4% of 1.2154/1.2445) is needed to open way towards 1.2154 (01 Mar low), with stronger acceleration to look for test of 1.2068 (rising 100SMA).

Conversely, close above cloud top/55SMA would ease bearish pressure, but stronger bullish signals could be expected on close above cluster of MA's (10/20/30) at 1.2315/26 zone.

US Federal Reserve is ending its two-day monetary policy meeting today and will announce its decision later today.

Markets widely expect Fed to increase interest rates by 0.25%, on central bank's first policy meeting under new chair person Jerome Powell, but focus will be on the press conference, as traders look for more signals about Fed's next steps.

Fed announced three rate hikes in 2018, but strong signals about more aggressive approach have been sent and markets will be looking for signs possible four hikes this year.

Res: 1.2295, 1.2315, 1.2326, 1.2355

Sup: 1.2265, 1.2240, 1.2223, 1.2205

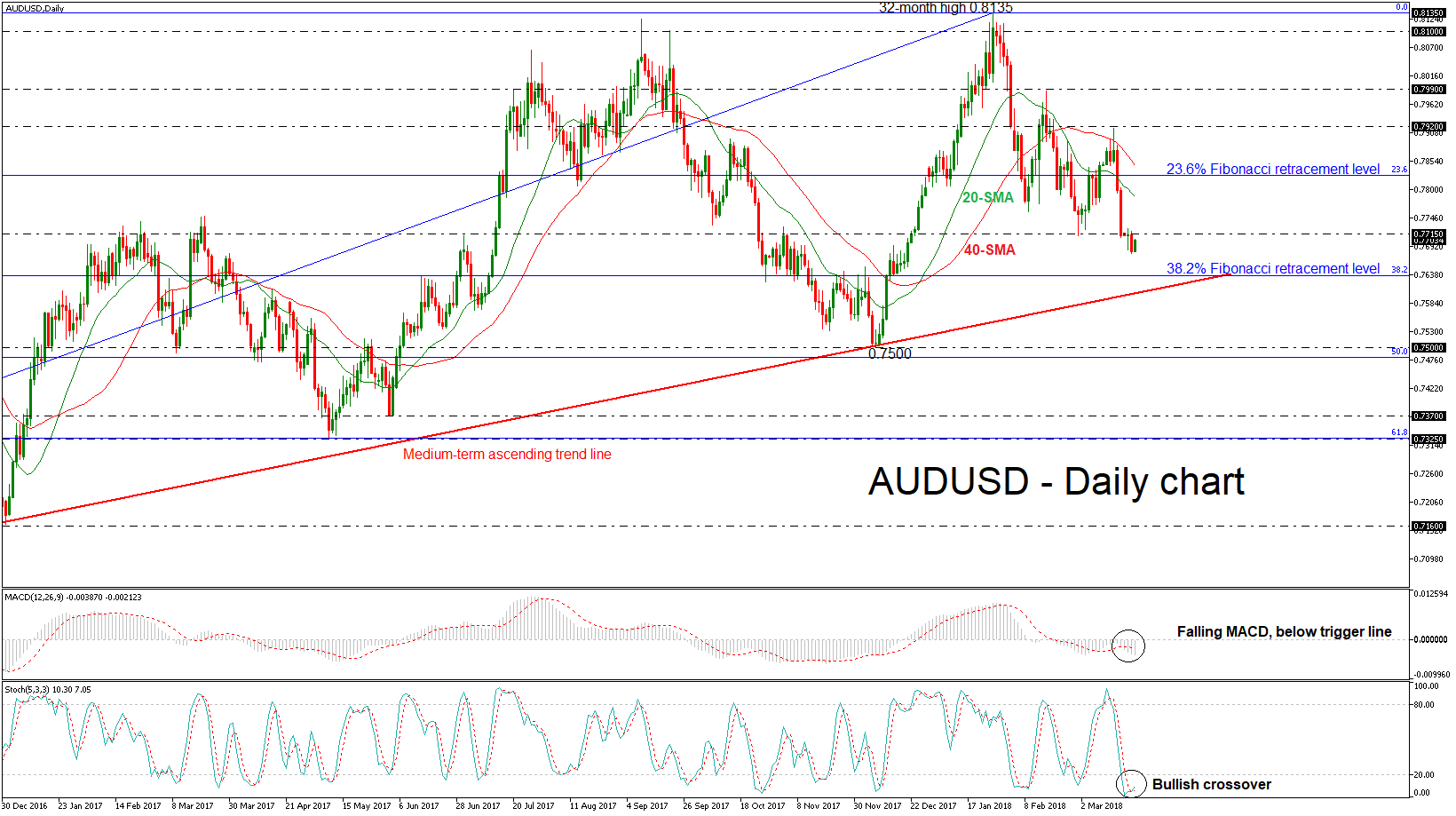

AUDUSD In Strong Sell-Off, Ascending Trend Line Eyed As Next Level

AUDUSD recorded relative strong bearish sessions in the previous week before the pull-back on the 0.7920 resistance level. The price plunged below the 0.7715 key level and posted a fresh three-month low of 0.7677. The bearish structure in the short-term remains intact, however, stochastics signal for a bullish correction.

In the daily timeframe, the MACD indicator is well below the zero and trigger lines and is falling, while the stochastic oscillator is creating a bullish crossover within the %K and %D line in the oversold zone, suggesting that the latest downswing may be running out of steam and that the risk for a continuation of the upward tendency is high.

In the wake of negative movements, the market could meet the immediate support at 38.2% Fibonacci retracement level near 0.7640 of the upleg with the low of 0.6820 to the high of 0.8135. This level stands near the medium-term ascending trend line, which has been holding since January 2016. A successful close below this area could increase chances for further losses until the 0.7500 handle and the trend would shift to bearish.

On the flip side, a move to the upside could see immediate resistance at the 20-day simple moving average (SMA) at 0.7788 but should the market push the price higher towards the 23.6% Fibonacci mark near 0.7830. A strong barrier, could be found at the 0.7920 resistance level taken from the high on March 14.

Currencies: Fed ‘Dot-Plot’ To Support A Further USD Rebound?

Rates: Hawkish Fed and sell-off at long end?

The Fed will hike its policy rate, but we also expect changes to the dot plot: a higher estimation of the neutral rate (3% from 2.75%) and a potential shift already in 2018 (4 from 3) and/or 2019 dots. Markets partly frontrunned on the short term shift, but don't anticipate a higher neutral rate. Therefore, we mainly expect a sell-off a the longer end of the US yield curve.

Currencies: Fed 'dot-plot' to support a further USD rebound?

EUR/USD easily reversed Monday's ECB' driven rise yesterday. Focus turns to the Fed policy decision today. Powell and Co indicating four rate hikes this year and lifting the neutral rate back to 3.0% might trigger a further USD rebound. Sterling traders will look out whether the UK labour data confirm the case for a May BoE rate hike.

The Sunrise Headlines

- US stock markets slightly rebounded after Tuesday's heavy sell-off, but Facebook continued to lag behind. Asian stock markets rebound as well with Japan closed for Vernal Equinox Day.

- The Fed will hike rates at Fed Powell's inaugural meeting at the helm of the central bank. We also expect a more upbeat economic assessment and a hawkish shift in the new dot plot, including a higher neutral rate.

- The Trump administration has dropped a demand that all vehicles made in Canada and Mexico for export to the US contain at least 50% US content, the Globe and Mail report, citing sources with knowledge of the NAFTA talks.

- The White House is preparing to crack down on what it says are improper Chinese trade practices by making it significantly more difficult for Chinese firms to acquire advanced US technology or invest in American companies, individuals involved in the planning said.

- The world's financial leaders (G20) rejected protectionism and urged "further dialogue" on trade, but failed to diffuse the threat of a trade war days before Washington is to announce measures against China.

- Fitch affirmed its A+ rating on China, and said tighter regulations have curbed financial risks without jeopardising growth targets, but warned that it remains to be seen if Beijing would stay committed to debt stabilisation.

- Apart from the Fed meeting, today's eco calendar contains the UK labour market report, a German Bund auction and the RBNZ's policy decision

Currencies: Fed 'Dot-Plot' To Support A Further USD Rebound?

New Fed 'dot-plot' to support the dollar?

The focus of FX traders turned again to the Fed after an 'ECB-driven' rally of the euro on Monday. Interest rate differentials widened in favour of the dollar. Currency investors apparently didn't want to be positioned short USD. EUR/USD reversed Monday's rise and closed the day at 1.2242 (from 1.2335). The gain of USD/JPY was more modest. Still, the pair closed at 106.53, well off the recent lows.

Overnight, Asian risk sentiment isn't too bad as investors look forward to the Fed's policy decision. Japanese markets are closed. BOJ deputy governor Amamiya indicated that one can't rule out the BOJ to adjust rates before the 2% target is reached, but that there is no reason to consider a rate hike now. USD/JPY lost a few ticks after the Amamiya headlines. EUR/USD also regains slightly ground.

Today, all eyes are on the Fed's policy decision. A 25 bps rate hike is discounted. Markets will mainly look at the new Fed forecasts (dots) and at Chairman Powell's assessment at its first press conference. For an in depth analysis, see the Fixed income part of this report. We assume that the Fed dots will signal four rate hikes in 2018. We also closely monitor whether the Fed raises the neutral rate back to 3.0%. If so, it could be important for global markets and for the dollar. Yesterday's price action was already USD constructive. Monday's EUR/USD rise was easily reversed. This suggests that the market still found itself a bit too much euro long/USD short. If our dotsscenario materializes, there is room for a ST USD rebound. EUR/USD 1.2155 is the first important support. A break opens the way to the 1.20 area. The gain in USD/JPY might be more modest than in USD/EUR.

Sterling gained further ground against a declining euro yesterday and held stable against the dollar despite softer CPI data. UK labour data take center stage today. Modest labour growth is expected, but average earnings are expected to rise slightly to 2.6% Y/Y. We don't have much reason to take a different view from the consensus. However, a positive surprise might reinforce BoE rate hike expectations and be slightly supportive for sterling. A test of the EUR/GBP 0.8690 support might be on the cards, especially if EUR/USD declines after the Fed

EUR/USD Fed to open the way for further USD gains?

Forex Analysis: NAFTA Progress As US Drops Auto Content Proposal

Note: Wednesday is a Bank Holiday in Japan, banks will be closed, and there will be no trading activity due to the Vernal Equinox Day Bank Holiday.

Progress has been made on NAFTA, as the US has backed down and dropped the demand that all vehicles made in Canada and Mexico that are sold into the US contain at least 50% US made parts. This is a big step, as much was made of the proposal by President Trump and his team during early negotiations. It is also a subtle indication that the President will play hardball during initial negotiations but will compromise to sign a deal in the end. USDCAD broke lower from 1.30692 down to 1.30097 on the news and USDMXN fell from 18.7519 to 18.6104. This news broke in after-hours trading so there could be substantial carry through into the North American session later today.

The communiqué from the G20 meeting over the last couple of days removed the reference to fighting protectionism and inward-looking policies. Instead, the following line was put in its place, “We reaffirm the conclusions of our leaders on trade at the Hamburg Summit and recognize the need for further dialogue and actions. We are working to strengthen contribution of trade to our economies.” But another line was also included that said attendees “recognize the role of legitimate trade defence instruments” and “are aware of the developing trade environment”. On crypto, it was said that crypto assets could have stability implications at some point and they should continue to be monitored by international standard-setting bodies.

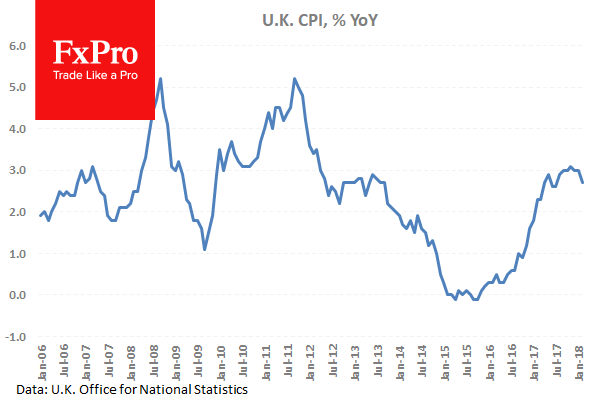

UK Consumer Price Index (YoY) (Feb) was 2.7% v an expected 2.8%, from 3.0% previously. Core Consumer Price Index (YoY) (Feb) was 2.4% v an expected 2.5%, from 2.7% prior. Consumer Price Index (MoM) (Feb) was 0.4% v an expected 0.5%, from -0.5% prior. Producer Price Index – Output (MoM) n.s.a. (Feb) was 0.0% v an expected 0.1%, from 0.1% previously. Producer Price Index – Output (YoY) n.s.a. (Feb) was 2.6% v an expected 2.7%, from 2.8% previously. Producer Price Index – Input (MoM) n.s.a. (Feb) was -1.1% v an expected -0.9%, from 0.7% previously, which was revised down to 0.4%. Producer Price Index – Input (YoY) n.s.a. (Feb) was 3.4% v an expected 3.8%, from 4.7% previously, which was revised down to 4.5%. Retail Price Index (MoM) (Feb) was as expected at 0.8%, against -0.8% previously. Retail Price Index (YoY) (Feb) was 3.6% v an expected 3.7%, from 4.0% prior. Most of the data came in softer than expected. These data points show CPI slipping on a year over year basis. The yearly figure has been above the Bank of England’s 2% target since March of 2017, due to the change in the value of the pound after Brexit. However, the BOE says that inflation is likely to move back to 2% in 2018, after peaking at 3%. GBPUSD fell from 1.40528 down to 1.39852 in the hours after this data release.

German ZEW Survey – Current Situation (Mar) was 90.7 v an expected 90.0, against a prior 92.3. ZEW Survey – Economic Sentiment (Mar) was 5.1 v an expected 13.0, from 17.8 previously. These data points softened quite a lot from previous reads, as the strengthening in the Euro affects business. The deteriorating trade environment is also a headwind for business outlook and a looming trade war damages sentiment. Germany is one of the countries likely to be hit badly by steel tariffs. EURUSD fell from 1.23165 to 1.22627 in the hours after this data came out.

New Zealand GDT Price Index was released at -1.2%, with a previous reading of -0.6%. This data shows that the change in the average price of dairy products sold at auction is slipping. As this makes up an important part of the New Zealand economy, NZDUSD rose from 0.71885 to 0.72003 as a result.

EURUSD is up 0.25% overnight, trading around 1.22720.

USDJPY is down -0.11% in early session trading at around 106.416.

GBPUSD is up 0.11% this morning, trading around 1.40132.

USDCAD is down -0.39% in early trading at around 1.30206.

Gold is up 0.30% in early morning trading at around $1,314.95.

WTI is down -0.13% this morning, trading around $63.68.