Sample Category Title

Powell Likely to Be Quizzed on New Projections and Trade War Risks in First Press Conference

- US Rate Hike Priced in, Economic Projections Key;

- Powell Likely to Be Quizzed on New Projections and Trade War Risks in First Press Conference;

- Sterling Rallies as Jobs Data Supports Case For May Rate Hike;

US Rate Hike Priced in, Economic Projections Key

US futures are currently pointing to a flat open on Wednesday as we await the latest economic projections from the Federal Reserve, which is likely to come alongside the first rate hike of 2018.

The Fed concludes is two day meeting later on today, after which it is widely expected to raise interest rates by 25 basis points. The hike is 94% priced in according to CME Group and so any reaction to this could be relatively muted. What will be of much more interest to investors is the economic projections which, aside from offering updated growth and inflation forecasts, will offer crucial insight into how policy makers see interest rates moving.

The central bank had previously indicated – back in December – that it saw three rate hikes this year but since then Trump’s tax reforms have provided an additional tailwind for the economy, one that could lift inflationary pressures and force the central bank to tighten at a slightly faster pace. The comments that we’ve had from some policy makers since then suggest some are now anticipating a fourth rate hike this year, which should be reflected in the dot plot. How many now fall into that camp will determine how markets respond.

As it is, markets are already pricing in around three rate hikes this year – 79% priced in according to CME Group – so they’re pretty much on the same page as the central bank. A number of policy makers forecasting a fourth may lift this a little as that is only 39% priced in but it may not make a huge difference so any dollar upside could be both limited and short-lived.

Powell Likely to Be Quizzed on New Projections and Trade War Risks in First Press Conference

The announcement will also be followed by Jerome Powell’s first press conference as Fed Chairman, during which he will likely be quizzed on any updates to the projections. In the current environment, he will also likely be questioned on the downside risks to the forecasts, most notably a trade war that US President Donald Trump appears so at ease engaging in.

The prospect of a trade war has taken its toll on sentiment in financial markets, with the week having got off to another weaker start. Stocks appeared to be making a strong comeback from the correction in early February but trade war fears have stalled the recovery, with indices currently on course to record a third losing week in the last four, although it’s worth noting that due to the strong rally a couple of weeks ago, this would leave indices not far below where they closed four weeks ago.

Sterling Rallies as Jobs Data Supports Case For May Rate Hike

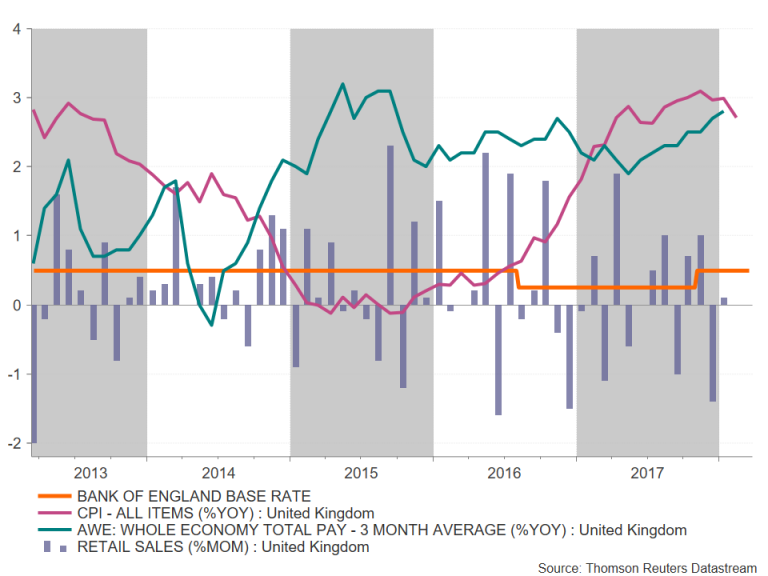

The Fed is not the only central bank in the spotlight this week. The Bank of England will announce its latest monetary policy decision tomorrow, before which we’ll get more data on the economy. Yesterday’s UK inflation did little to shake the belief that a rate hike is likely in May, while this morning’s jobs numbers were very much favourable for one. Unemployment fell to 4.3% in the three months to January, its lowest level since June 1975, while wages including bonuses rose 2.8%, offering further evidence that the labour market is tightening.

The question for many is whether higher wages are a reflection of a tighter labour market or the higher cost of living in the aftermath of the Brexit referendum, something the BoE doesn’t appear too concerned with. The rally in the pound in response to the data would suggest traders are instead seeing the data and further supportive the case for a rate hike in May.

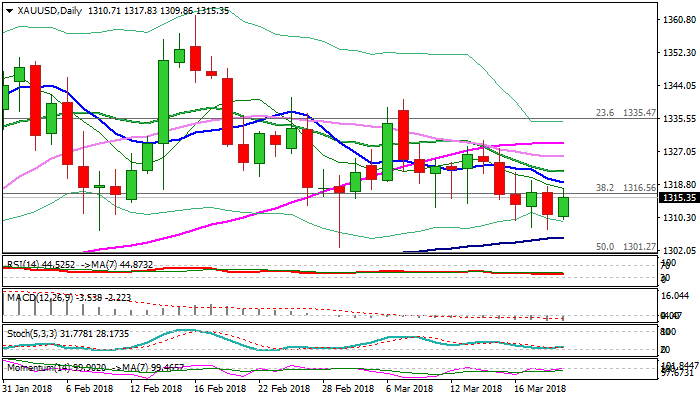

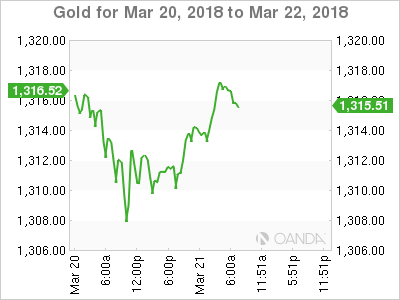

Spot Gold Bounces after Bears Approached Key Supports at $1305/02; Fed Decision is in Focus for Fresh Direction Signals

GOLD

Spot Gold trades higher on Wednesday after hitting three-week low at $1307 on Tuesday, where broader bears stalled on approach to key supports at $1305 (100SMA) and $1302 (01 Mar spike low).

Overall structure remains bearish and looks for eventual break through pivotal $1300 support zone, which also marks the mid-point of larger $1226/$1366 ascend.

Today’s bounce could be seen as positioning for fresh downside as Fed is widely expected to increase interest rates on its two-day meeting which ends today. However, traders will be looking for hints about Fed’s next steps, as hawkish tone would signal more aggressive approach to the interest rate policy and possible four hikes in 2018, compared to projected three hikes, which would boost the greenback and send gold price lower.

Softer tone from Fed would ease current bearish pressure on the yellow metal and open way for stronger recovery and test of a cluster of MA barriers which lies between $1319 and $1329.

Firm break here will be needed to sideline existing bears and signal stronger recovery.

Res: 1319; 1322; 1325; 1329

Sup: 1307; 1305; 1302; 1300

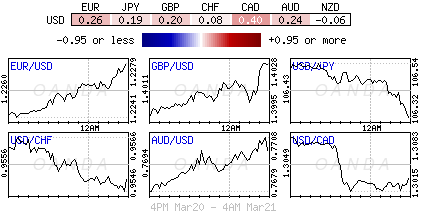

NZDUSD at the early stage of decline ahead of RBNZ rate decision

USD suffers some selling today as markets await FOMC rate hike. But NZD and AUD are performing even worse as seen in daily heatmap. On the other hand, solid UK job data, with fall in unemployment rate to 4.3%, and acceleration wage growth, keeps Sterling buoyed. Indeed, GBP is staying as the strongest one for the week ahead of tomorrow's BoE rate decision. Canadian Dollar follows as the strongest for the day.

In between FOMC and BoE, RBNZ will also announce rate decision in the upcoming Asian session. RBNZ is widely expected to keep the Official Cash Rate OCR unchanged at 1.75%. In the prior statement, RBNZ noted that "monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain and policy may need to adjust accordingly." That's clearly seen as easing bias by the markets. We're not expecting any change in the OCR, nor the slightly dovish stance in tomorrow's announcement.

In between FOMC and BoE, RBNZ will also announce rate decision in the upcoming Asian session. RBNZ is widely expected to keep the Official Cash Rate OCR unchanged at 1.75%. In the prior statement, RBNZ noted that "monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain and policy may need to adjust accordingly." That's clearly seen as easing bias by the markets. We're not expecting any change in the OCR, nor the slightly dovish stance in tomorrow's announcement.

Looking at the 6H action bias chart, NZD/USD is clearly in a persisting near term down move, just came out of brief consolidation.

Looking at the 6H action bias chart, NZD/USD is clearly in a persisting near term down move, just came out of brief consolidation.

From the D action bias chart, NZD/USD is staying to increase downside bias after taking out 0.7176 support (Feb 6). It's likely just the start of a bigger downward move given the developments.

Brexit Transition Deal Gives BoE Go-Ahead For May Rate Hike But UK Data Poses Dilemma

Bets for a Bank of England rate hike in May received a major boost this week after the United Kingdom and the European Union reached a deal on a 21-month transition period that would come into effect when Britain officially leaves the bloc at the end of March 2019. The positive development is likely to sway BoE policymakers in favour of signalling a rate increase in May when they convene on Wednesday and Thursday for a two-day monetary policy meeting. No change in interest rates or to the quantitative easing program is expected on Thursday.

The Bank struck a hawkish tone at the February policy meeting with Governor Mark Carney saying that rates would need to be raised “somewhat earlier and to a somewhat greater extent than we had thought in November”. There was more hawkish rhetoric at the inflation hearing before Parliament's Treasury Select Committee on February 21. The normally dovish Andy Haldane, the Bank's chief economist, warned that the balance of risks to the path of interest rates needed to return inflation to target is to the upside.

A transition deal is an important component in the Bank's decision making as it would maintain the status quo for British firms to remain in the single market until at least the end of 2020, helping businesses plan forward. But with that uncertainty now seemingly lifted, the focus has shifted solely on economic indicators.

Annual inflation in the UK moderated by slightly more than forecast to 2.7% in February from 3.0% in January, according to data released on Tuesday. This suggests the spike in inflation generated by the plunge in sterling after the Brexit vote is now starting to drop out of the calculations. Consequently, this is raising some eyebrows among some market analysts about the BoE's overly hawkish inflation outlook.

The Bank's main worry is that the limited slack available in the economy and the tightening labour market will keep inflation above its 2% target without some gradual rate increases over the next 2-3 years. However, wage growth remains muted by historical standards even after firming to 2.8% in the three months to January, as per Wednesday's data. The decline in the number of EU migrants heading to the UK since the Brexit vote may be accentuating the upside risks to wages at a time when the jobless rate is running at a four-decade low (4.3% in January). But like in the United States, there is yet to be any convincing evidence of a more sustained pick-up in wages.

The final piece of data the Monetary Policy Committee (MPC) will have to analyse before their policy decision on Thursday will be the retail sales figures for February. After slumping by 1.5% in December and stalling in January, sales are expected to have rebounded in February, rising by 0.4% over the month. A worse-than-expected figure could weaken the MPC's growth outlook in the medium term given that private consumption accounts for about 65% of UK GDP, while a stronger rebound would underscore the Bank's view that the economy should continue expanding at a moderate rate.

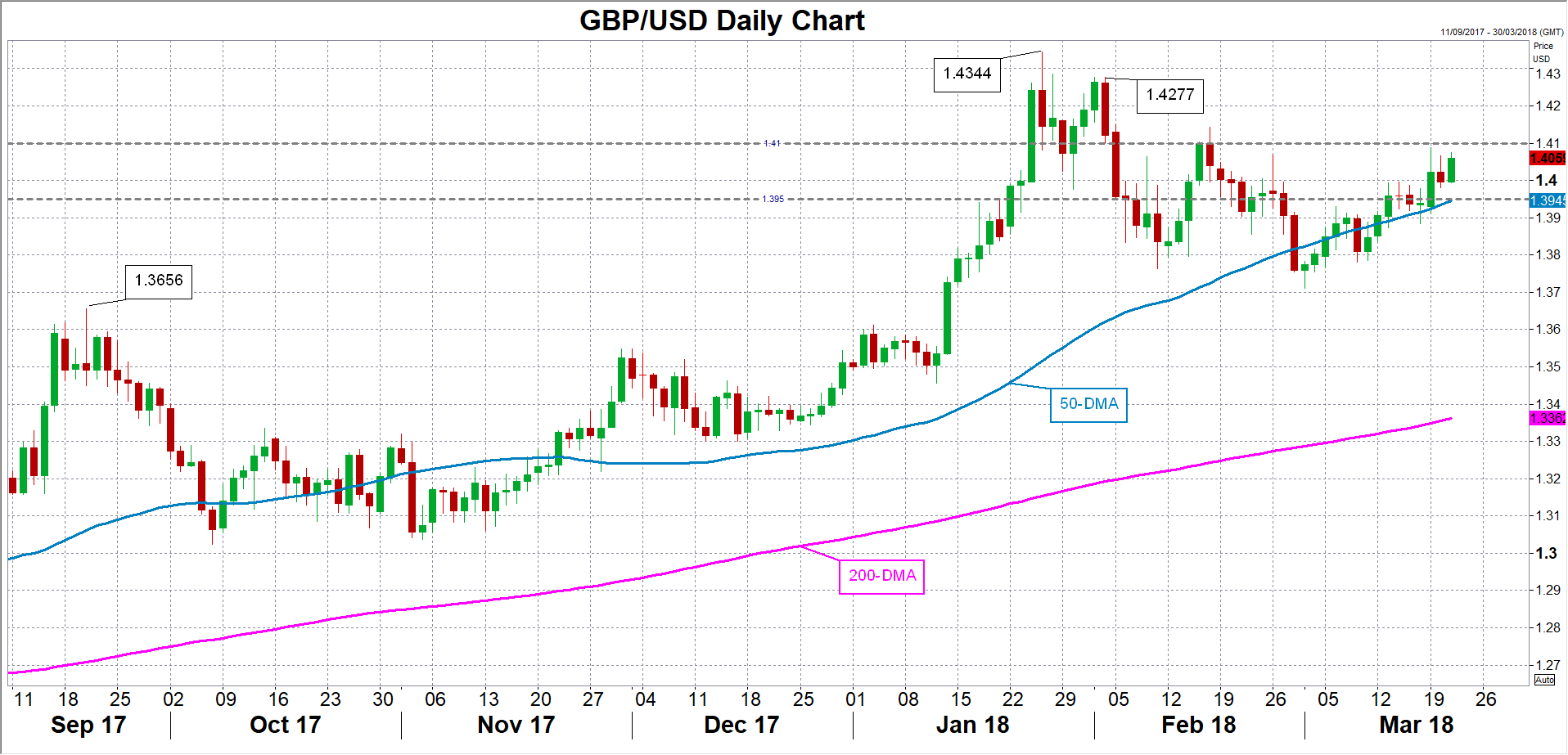

Sterling, which rallied to a one-month high after Monday's announcement of a transition deal but met resistance just below the $1.41 level, could break above the aforementioned key handle if the BoE confidently flags a rate hike at its next meeting in May. A climb above $1.41 would bring into scope the February peak of $1.4277. However, should the Bank opt for a more cautious stance and fail to clearly signal a Spring move, the pound could drop back below the $1.40 level towards the 50-day moving average around $1.3950.

Many analysts think the BoE has backed itself into a corner by communicating a rate hike path at a time when UK growth is lagging its European peers and when the Brexit negotiations are ongoing. Should the UK and the EU fail to reach a post-Brexit trade deal, the Bank may be forced to undo its rate hikes. But even in the event of a positive conclusion to the Brexit talks, many economists don't see the need for monetary tightening at the current pace of economic expansion. In support of the Bank, however, is the improvement in real incomes. As earnings head for 3% annual growth and inflation falls towards 2%, rising real wages should drive consumption higher over the coming months, shifting the risks clearly to the upside

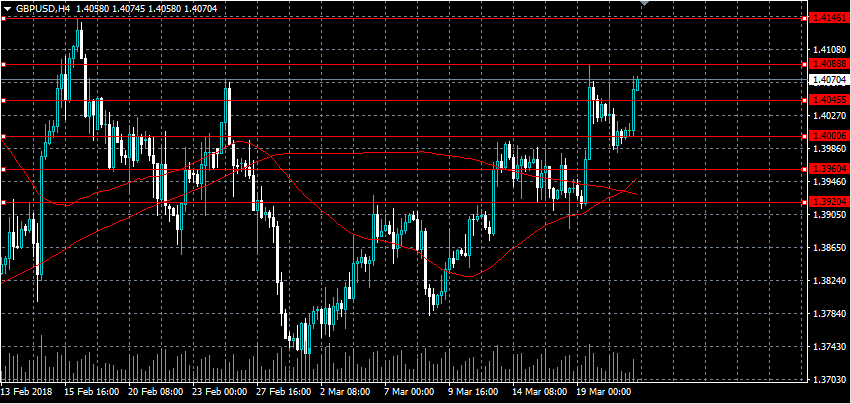

GBPUSD Strongly Bullish Above 1.4045 Level

The British pound has moved back towards the trading highs of the week against the U.S dollar, after data from the United Kingdom showed UK wages growing at the fasted pace since 2016. The GBPUSD pair currently trades around the 1.4060 level, with pound sentiment also receiving a boost from a fall in the official UK unemployment rate. A technical break above the 1.4088 level may encourage further gains towards the 1.4146 level, whilst key daily support for the pair is found at the 1.3960 level.

The GBPUSD pair remains strongly bullish whilst trading above the 1.4045 level, further gains towards the 1.4088 and 1.4146 levels seem possible.

If price-action on the GBPUSD pair moves below the 1.4045 level, a correction back towards the 1.4000 and 1.3960 levels may occur.

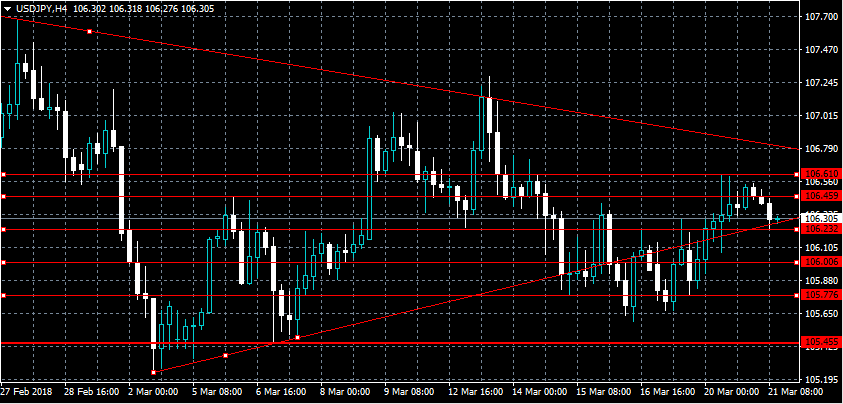

USDJPY Breakout Looms Ahead Of Fed Decision

The U.S dollar continues to consolidate above the 106.00 handle against the Japanese yen, with a technical breakout looming ahead of today’s Federal Reserve interest rate. The USDJPY pair is trading in tight price-range, with price-action now pulling back from the weekly price-high, found at the 106.61 level. A clear breach of the 106.80 resistance area should encourage further gains above the 107.00 level, whilst key weekly technical support is found at the 105.45 level.

The USDJPY pair remains bullish while trading above the 106.00 level, key upside resistance is now found at the 106.80 and 107.50 levels.

Should the USDJPY pair declines below the 106.00 support levels, key support is found at the 105.45, 105.22 and 104.60 levels.

Forex Analysis: USDCAD And USDMXN

The US has agreed to drop its proposed Auto Content from NAFTA, opening the way for progress to be made on the trade agreement. USDCAD dropped on the news, breaking through trend line support down to 1.30097 but has moved back to the current levels around 1.30395. Resistance is found near the broken trend line at 1.30704, with the previous high at 1.31241. US FOMC is expected to hike interest rates to 1.75% later today and signal up to four rates hikes for 2018.

Support can be found at 1.30000, close to the rising 50-period MA, if the market resumes its moves lower. However, the trend is for higher prices and only a move under trend line support at 1.28850 would upset proceedings. Until then, support can be seen at 1.29608 and 1.29200, close to the rising 100-period MA. The 200-period MA is on track to reach 1.28000 later, with a test to this level wiping out long positions and creating a lower low.

USDMXN

The USDMXN pair has also taken a dip on the NAFTA news and is approaching trend line support at 18.5364. A break under this area would hit support at 18.4377 initially but could push lower to test the recent lows at 18.3000. A loss of this area would create a lower low and target 18.0495, followed by the red trend line support at 17.6950.

The resistance comes in at yesterday’s highs and the moving average cluster at 18.7148, followed by the trend line at 18.8334. The 18.9028 level, located above the trend line, and recent highs at 18.9697 block a move to 19.0000 and 19.3633. The December high comes in at 19.9000.

Technical Outlook: GBPUSD Rises On Upbeat UK Earnings But Key 1.41 Barrier Is Still Intact, Focus Turns To FOMC

Sterling jumped above Tuesday’s high at 1.4066, boosted by better than expected UK earnings data and pressures strong barriers at 1.4088 (Monday’s spike high) and 1.4102 (Fibo 61.8% of 1.4345/1.3711 descend).

Upbeat UK earnings (including bonus) in Jan (2.8% vs 2.6% f/c and upward-revised 2.7% in Dec) supports hawks who are looking for more rate hikes in 2018 and maintain positive outlook for sterling, which was boosted by recent news of positive movements in Brexit talks.

Additional support comes from Unemployment rate which dipped back to four decade low at 4.3%, but positive impact was overshadowed by increase in jobless claims which rose by 9.2K in Feb vs -3.1K forecast and previous month’s downward-revised result at -1.6K.

Positive UK data came as support for bullish techs (daily MA’s in bullish setup and formed multiple bull-crosses) and 14-d momentum continues to head north in positive territory.

Also, daily Ichimoku cloud is thickening and continues to underpin the action.

Bulls need firm break above 1.41 zone to signal continuation and expose initial barrier at 1.4144 (16 Feb lower top) with extension higher to look for 1.4195 (Fibo 76.4% of 1.4345/1.3711 fall).

Broken Fibo 50% barrier marks initial support at 1.4028, guarding strong support at key 1.40 zone, which is expected to keep the downside protected.

Focus now turns towards FOMC verdict which is next key event today and expected to provide strong direction signals.

Res: 1.4088, 1.4102, 1.4144, 1.4195

Sup: 1.4028, 1.4000, 1.3961, 1.3946

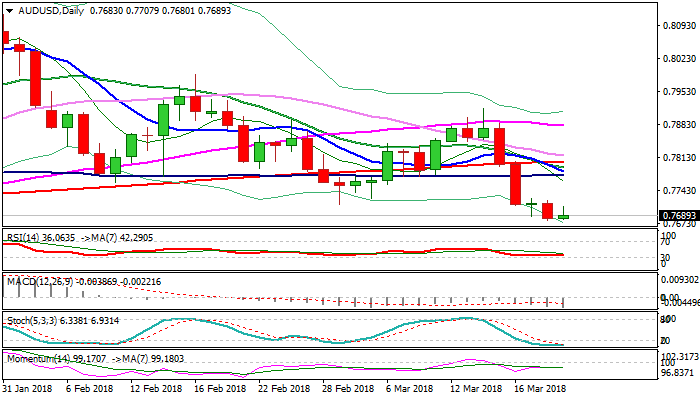

Technical Outlook: AUDUSD – Recovery Attempts Stalled At 0.77 Barrier, Fed Decision Eyed For Fresh Signals

Recovery attempts on Wednesday from new three-month low at 0.7678 (posted on Tuesday) were so far short-lived.

Bunce stalled on probe above initial barrier at 0.7700 and subsequent fall kept immediate focus at the downside.

Firm bearish setup of daily techs, with multiple death-crosses (10/200 and 20/200SMA’s and 10/20 SMA bear-cross) maintain bearish pressure.

Meanwhile, bears could be further delayed as slow stochastic turned sideways deeply in oversold territory and may generate positive signal on reversal.

FOMC policy decision is due later today and eyed for stronger signal, as wide expectations go for hawkish stance of the US central bank which would further boost the greenback.

On the other side, softer tone from Fed would weaken dollar bulls and send Aussie higher.

Former key support, provided by 100SMA , now acts as strong resistance (0.7773) and close above it is need to undermine dollar’s bulls and allow for stronger correction of 0.7916/0.7678 bear-leg.

Res: 0.7707, 0.7725, 0.7742, 0.7773

Sup: 0.7678, 0.7650, 0.7626, 0.7600

USD/CAD – Canada’s Loonie Gets A NAFTA Lift

Wednesday March 21: Five things the markets are talking about

Global equities have traded mixed overnight despite the U.S dollar operating under pressure as the market waits for the Federal Reserve's first policy decision since Jerome Powell took the wheel. Treasuries prices have rallied and oil has touched a six-week high.

At 02:00 pm ETD the market will tune in to Jerome Powell's first Federal Open Market Committee (FOMC) meeting as chairman, with close scrutiny of whether monetary policy might become more “hawkish” under his tenure. Also of interest will be the future guidance given by him during his scheduled press conference (02:30 am EDT).

Recent U.S data and Fed speeches would suggest the median of FOMC participants' assessment of the appropriate pace of policy firming (the dots) will unite around +2.125% or three-hikes for 2018, with an outside risk the median dot will move to +2.375%.

Elsewhere, the Bank of England (BoE) is expected to keep interest rates and its asset-purchase program unchanged tomorrow (8:00 am EDT). Attention will be on language and the odds for a May hike.

Also, down-under, the Reserve Bank of New Zealand (RBNZ) has a monetary policy decision today at 04:00 pm EDT.

1. Stocks mixed results

In Japan, many investors have stayed on the sidelines ahead of today's Japanese public holiday and the two-day Fed meeting expected to produce a rate hike.

Down-under, Australia's ASX closed +0.2% higher, while indexes in Indonesia and India rose by +1% and +0.7%, respectively. In New Zealand, the main benchmark closed +1.4% higher at a record high.

In Hong Kong, stocks were little changed overnight, as the market braces itself for Fed Chair Powell's first policy meeting and amid concerns that President Trump could impose additional punitive trade measures against China. The Hang Seng index rose +0.1%, while the China Enterprises Index lost -0.5%.

In China, stocks erased early gains and ended lower, weighed down by start-up firms, as investors booked profits mostly in the tech sector. At the close, the Shanghai Composite index was down -0.3%, while the blue-chip CSI300 index was down -0.38%.

In Europe, regional indices trade mostly lower across the board led by the FTSE 100 which trades lower on a stronger pound (£1.4074) on the back of stronger jobs data (see below) out of the U.K.

U.S stock futures are pointing to a -0.1% fall for the S&P 500 and the Dow.

Indices: Stoxx600 -0.2% at 375.0, FTSE -0.5% at 7026, DAX -0.1% at 12298, CAC-40 -0.3% at 5235, IBEX-35 +0.1% at 9688, FTSE MIB +0.1% at 22829, SMI -0.2% at 8834, S&P 500 Futures -0.1%

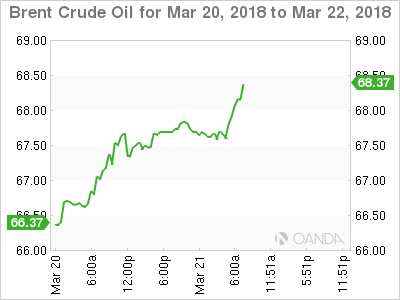

2. Oil prices edge higher on Middle East tension, gold supported

Oil prices are better bid, lifted by a mixed dollar, tensions in the Middle East and concerns of a further fall in Venezuelan output.

Brent crude futures are at +$67.56 per barrel, up +14c, or +0.2%, while U.S West Texas Intermediate (WTI) crude futures are at +$63.69 a barrel, up +15c, or +0.2% from Monday's close.

The IEA said last week that Venezuela, where an economic crisis has cut oil production by almost -50% to well below +2m bpd was “clearly vulnerable to an accelerated decline”, and that such a disruption could tip global markets into deficit.

Capping prices somewhat is U.S crude oil production, which has risen by more than a fifth since mid-2016, to +10.38m bpd.

Note: U.S output is now higher than that of top exporter Saudi Arabia. Only Russia produces more, at around +11m bpd, although U.S output is expected to overtake Russia's later this year.

Ahead of the U.S open, gold prices gains on the ‘big' dollar decline as market awaits the Feds rate outlook. Spot gold is up +0.4% at +$1,315.84 per ounce. Prices fell to a nearly three-week low of +$1,306.91 in yesterday's session.

3. Sovereign yield to be guided by Fed decision

U.S government bond prices fell yesterday as investors look forward to the conclusion of today's Fed meeting and clear space in their portfolios for new corporate bond offerings.

Note: As often happens in the lead-up to Fed meetings, yields have been trending higher. Fed officials are widely expected to lift short-term interest rates by +25 bps this afternoon.

There is the risk that the Fed will sound a little bit more ‘hawkish.' Nevertheless, the majority is anticipating that the Fed's median projection of rate increases for this year will remain at three. There is a slight possibility that officials could lift their projections for 2019, 2020 and over the longer term

The yield on U.S 10-year Treasuries -1 bps to +2.88%, the first retreat in a week. In Germany, the 10-year Bund yield fell less than -1 bps to +0.58%. In the U.K, the 10-year Gilt yield has declined -1 bps to +1.482%.

4. The dollar's mixed results

FX markets remain mostly in a “wait-and-see mode” ahead of today's Fed meeting decision.

The USD is a tad softer against the major pairs and has moved off its recent three-week highs.

GBP/USD (£1.4074) is firmer todays after stronger than anticipated U.K wage data (see below) has given the MPC more latitude to display a more ‘hawkish” tone after yesterday's disappointing CPI print.

The EUR/USD is higher by +0.3%, just shy of the psychological €1.2300 level, while USD/JPY is off by -0.3% at ¥106.29

Elsewhere, constructive NAFTA news that the U.S government is contemplating dropping demand on Canada and Mexico autos in NAFTA talks saw the MXN and CAD currencies firm up. The CAD (C$1.3040) dollar has rallied overnight, hitting its best levels in about a week.

5. U.K data in focus

Data this morning, across the pond, showed that the U.K unemployment rate held steady in January, while wage growth ticked a tad higher.

The jobless rate in the three-months through January was +4.3%, the same rate as the previous three-months and lower than the +4.7% for the same period a year earlier.

Other data showed that annual wage growth accelerated to +2.6%, from +2.5% previously, driven by higher pay settlements in construction and manufacturing.

Today's U.K wage data keeps door ajar for a possible B0E hike in May.