Sample Category Title

China preparing quick, targeted retaliations to Trump’s $60b tariffs

The WSJ reported that China is preparing to hit back at US President Donald Trump's targeted tariffs against it. Trump is set to unveiled to list of products tomorrow, which could add up to as much as USD 60b of annual tariffs.

It's not really news that China is preparing counter measures. But what WSJ said is that China's tit-for-tat tariffs would target Trump's support base. That is, they will be aimed at agricultural exports from Farm Belt states.

That raises a question on whether China views it as trade war with the US, the Republicans, or Trump himself. Trump war might be easy to win for a sized economy against smaller ones. It's much tougher between two economies of comparable size.

Would there be a chance if the trade war is between a political party, a family, or even a person, against a sized economy?

Remember that it's an authoritarian government in China. What they'd do very much depends on how their leader Xi Jinping views it. If Xi sees the provocation as from Trump only, rather than the whole of the US, then good luck to the latter.

Merkel pledges unambiguous counter measures against Trump’s unlawful tariffs

German Chancellor Angela Merkel talked to lawmakers in Bundestag today covering a number of topics.

Regarding Brexit, Merkel said the EU-UK relationship cannot not be as close as it is now after Brexit. However, she still emphasized that EU wants "friendly relationship" with UK. Also, she was "deep, detailed" free trade accord between EU and UK.

On the other hand, Merkel blasts US President Donald Trump's steel and aluminum tariffs as "unlawful". EU and Germany will continue talks with the US. However, Merkel emphasized that if necessary "we will take unambiguous counter measures".

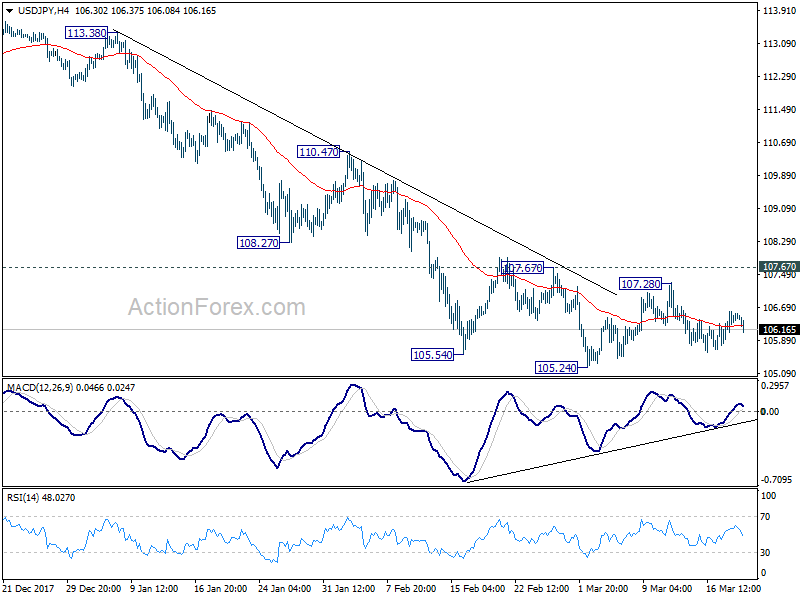

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 106.10; (P) 106.35; (R1) 106.78; More...

At this point, USD/JPY is still staying in sideway trading in range of 105.24/107.67. Intraday bias remains neutral. With 107.67 resistance intact, near term outlook remains bearish and further decline is expected. On the downside, break of 105.24 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. On the upside, firm break of 107.67 resistance will indicate near term reversal, on bullish convergence condition in 4 hour MACD. In such case, outlook will be turned bullish for 110.47 resistance next.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

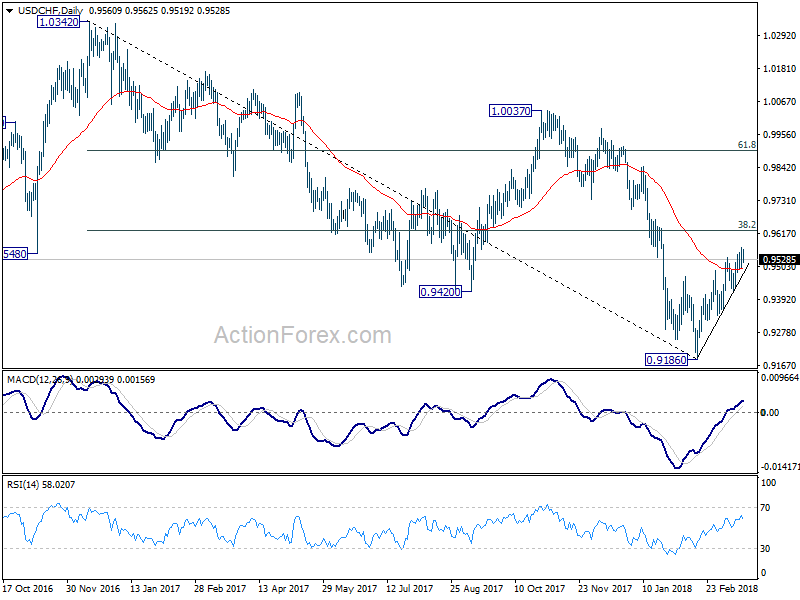

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9520; (P) 0.9544; (R1) 0.9588; More...

USD/CHF lost momentum again after hitting 0.9568. But for the momentum, further rise is still expected to 0.9626 fibonacci level. We'd be cautious on strong resistance from 0.9626 to limit upside. Nonetheless, sustained break of 0.9626 will carry larger bullish implications. On the downside, break of 0.9423 will indicate completion of the rebound from 0.9186. And intraday bias would then be turned back to the downside for 0.9356 support and below.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Current development is raising the chance that it is completed. But there is no confirmation yet. Focus will now be back on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add much credence to the case of trend reversal and target 61.8% retracement at 0.9900 and above. However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

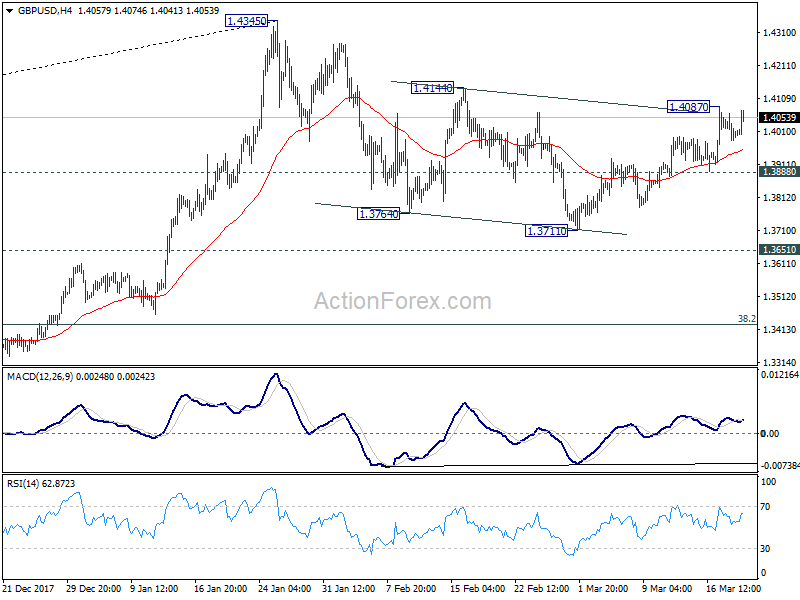

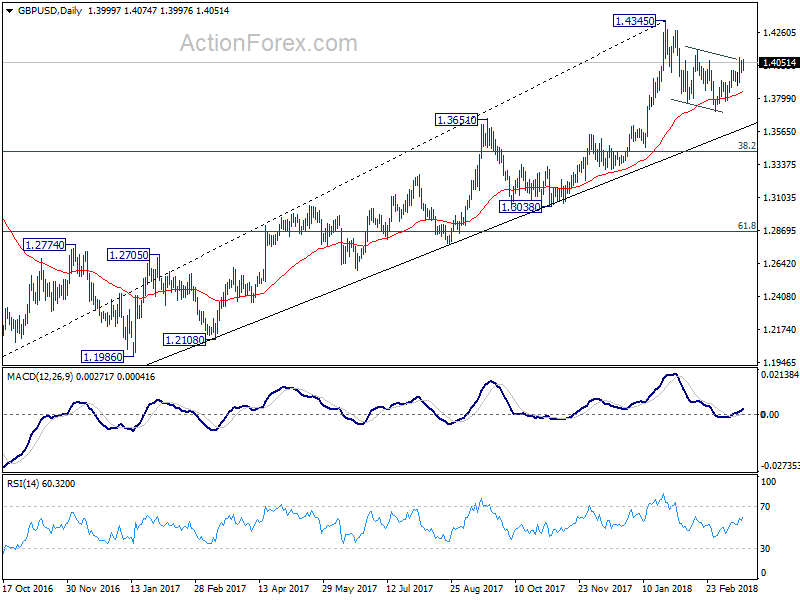

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3964; (P) 1.4015; (R1) 1.4048; More....

GBP/USD recovery well ahead of 4 hour 55 EMA but stays below 1.4087 temporary top. Intraday bias remains neutral first. As long as 1.3888 minor support holds, further rally is expected. As noted before, correction from 1.4345 could have completed at 1.3711 already. Above 1.4087 will target 1.4144 resistance first. Firm break there should confirm this bullish view and target 1.4345 and above. On the downside, however, break of 1.3888 minor support will dampen this bullish view. Intraday bias would be turned back to the downside to extend the decline from 1.4345 through 1.3711 instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

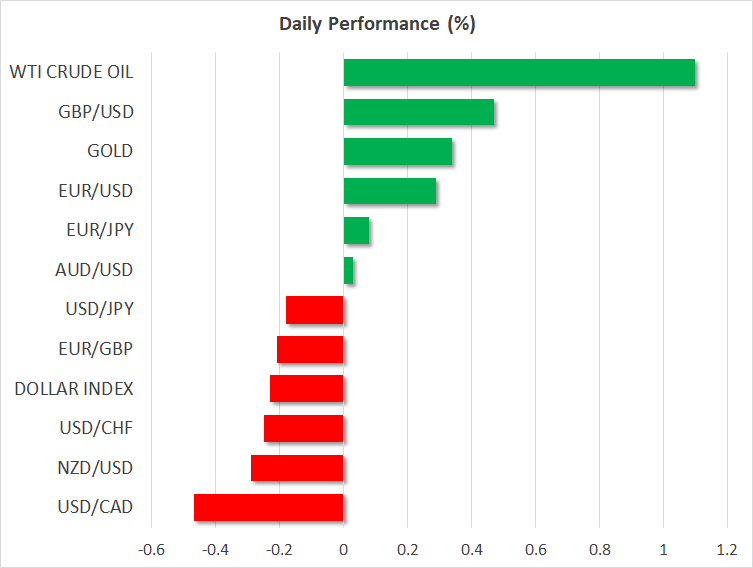

Dollar on the Backfoot ahead of Fed Rate Decision

Here are the latest developments in global markets:

FOREX: Dollar/yen was falling by 0.18% and the dollar index was also under pressure, losing 0.25% at the time of writing as investors were preparing their positions ahead of the Fed interest rate announcement later in the day. While the dollar was struggling to gain ground, the euro managed to recover some losses, with euro/dollar moving higher towards 1.2278 (+0.23%). Pound/dollar touched an intraday high of 1.4074 before it slipped to 1.4043 (+0.34%) after the UK’s unemployment rate came in better than expected in February, falling from 4.4% to 4.3%. It is worth mentioning that the Bank of England is expected to keep interest rates unchanged on Thursday, but deliver a rate hike probably in May. Dollar/loonie extended losses for the third day, last trading at 1.2979 (-0.67%). Aussie/dollar held near its today’s opening level, around 0.7690, while kiwi/dollar declined to 0.7160 (-0.31%). Note that the RBNZ will also decide on monetary policy today but the central bank is anticipated to stand pat on interest rates.

STOCK: European stocks were mixed at 1055 GMT. The blue-chip Euro STOXX 50 was flat, the British FTSE 100 was down by 0.37%, while the German DAX 30 and the Spanish IBEX 35 were up by 0.17% and 0.07% respectively. US stock futures were pointing to a negative open.

COMMODITIES: Oil prices advanced considerably as markets feared that tensions between Saudi Arabia, US and Iran could disrupt supply in the Middle East. WTI crude oil surged by 1.13% towards a fresh three-week high of $64.26 a barrel. Brent crude oil climbed to a six-week high of $68.27, gaining 1.26% at the time of writing. In precious metals, gold increased by 0.34% to $1,314.95 an ounce. Given that oil and gold are depended on the US dollar, they are likely to react to the FOMC decision later today. A strong dollar could drive commodities lower, whilst a weaker dollar could push them higher.

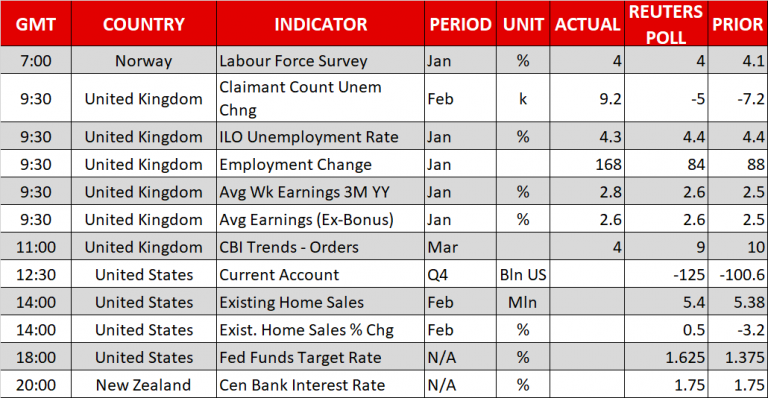

Day ahead: FOMC announcement on interest rates; RBNZ also gathers to decide on monetary policy

Day ahead: FOMC announcement on interest rates; RBNZ also gathers to decide on monetary policy

The Federal Open Monetary Committee concludes its two-day policy meeting today under the lead of Jerome Powell for the first time after his nomination as the new Fed chair. The decision on interest rates will be announced at 1800 GMT and markets have no doubt that policymakers will deliver another 25bps rate hike. However, the question for the jury will be whether the Fed will alter its forecasts for the pace of monetary tightening this year, and hence all eyes will be on the Fed dot plot to identify any change in the distribution of the dots. If the median dot is placed higher, hinting that four rate hikes are now on the cards, dollar bulls could take control. On the other hand, if the picture remains unchanged, this could add some pressure to the greenback as the news could be taken as dovish by investors, potentially hinting that the US economy is not strong enough to support stricter credit constraints. Policymakers could embrace a positive outlook on the economy when they release their fresh economic projections today, considering the benefits arising from the new tax overhaul, the weaker dollar, and stronger global growth. However, the persisting softness in inflation and wage growth under a tighter labor market could keep them cautious and unwilling to change their plans for gradual rate rises for now. A press conference by Powell at 1830 GMT will give more insight into the central bank’s way of thinking.

Two hours later, at 2000 GMT, the Reserve Bank of New Zealand will also make an announcement on interest rates. But in this case, no change is expected, with projections being for the central bank to hold rates at a record low of 1.75%. Inflation readings came in worse than expected in the fourth quarter of 2017 and business sentiment remains at levels seen during the 2008 financial crisis, while a potential global trade war in the face of Trump’s import tariffs are likely to put the country’s terms of trade at risk. If the monetary policy statement following the decision uses a cautious tone, probably highlighting the risks above, the kiwi could extend its recent losses.

Meanwhile, in Australia, investors will be waiting for the Australian Bureau of Statistics to publish February’s employment data early in the Asian session on Thursday (0030 GMT). Expectations are for job growth to post the longest run of employment gains in the survey’s history and the unemployment rate to remain unchanged at 5.5%. It would be interesting to see though, whether job creation is skewed to part-time positions as was the case in January. Such an outcome would be a negative spot on the report.

Turning to today’s remaining data, existing home sales for the month of February out of the US at 1400 GMT might turn positive after two months of falling, while earlier, at 1230 GMT, the US current account deficit during the fourth quarter of 2017 is anticipated to widen.

In energy markets, oil prices might experience some volatility after the release of the Energy Information Administration’s weekly report on US oil inventories for the week ending March 16. Crude oil inventories are anticipated to have risen by 2.600 million barrels, less than the 5.022m seen in the preceding week. If this is the case, that would be the fourth week of consecutive rises. Gasoline inventories and distillate stocks are expected to continue falling.

Legislative developments will also attract attention during the week after US Congressional Republicans failed to unveil their government spending plans on Tuesday, pointing possibly to a third government shutdown on Friday if they do not approve the bill by midnight. Also on Friday, Trump is likely to announce further tariffs on China.

Canadian Dollar Improves as US Eases on NAFTA Demands

The Canadian dollar has posted considerable gains in the Wednesday session. Currently, USD/CAD is trading at 1.2986, down 0.66% on the day. On the release front, there are no Canadian indicators on the schedule. In the US, the current account deficit widened to $128 billion, above the estimate of $125 billion. On the housing front, Existing Home Sales is forecast to rise to 5.41 million. All eyes are on the Federal Reserve, which is expected to raise the benchmark rate to a range of between 1.50% and 1.75%. On Thursday, the US releases unemployment claims.

A protectionist president in Washington continues to keep policymakers in Ottawa up late at night, as some 80% of Canadian exports head to its southern neighbor. The latest scare for Canada has been the US decision to slap tariffs on steel and aluminum products, as Canada is the largest exporter of steel to the US. Canada avoided a bullet as President Trump announced that the Canada and Mexico would be exempt from the tariffs, but the specter of the US involved in trade wars has weighed on the fragile Canadian dollar. There was some positive news earlier on Wednesday, with a report that the US has dropped its demand that vehicles produced in Canada or Mexico that are destined to the US, contain a minimum of 50% US content. This demand was one of the key sticking points in the negotiations, and its removal should speed up talks on the renegotiated NAFTA agreement.

The markets are keeping a close eye on the Federal Reserve, which will release a rate statement later in the day. The Fed is expected to raise rates for the first time in 2018, and Fed Chair Jerome Powell will preside as chair of the FOMC for the first time, followed by Powell’s first post-FMOC press conference. The Fed has sounded marginally more hawkish recently – will this trend continue in the rate statement? The Fed rate projection remains at three rates for 2018, but with the US economy continuing to perform well, this forecast could be revised upwards to four rates. If the rate statement is unexpectedly hawkish, the US dollar could respond with gains.

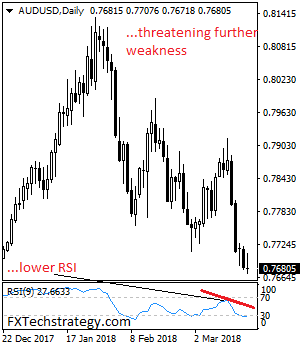

AUDUSD: Faces Further Downside Pressure On Bearishness

AUDUSD - The pair looks to weaken further lower following its Tuesday losses. On the downside, support resides at the 0.7650 level where a breach will aim at the 0.7600 level. Below that level will set the stage for a run at the 0.7550 level with a cut through here targeting further downside pressure towards the 0.7500 level. Its daily RSI is bearish and pointing lower suggesting further weakness. On the upside, resistance lies at the 0.7750 level. A cut through here will turn attention to the 0.7800 level and then the 0.7850 level where a violation will set the stage for a retarget of the 0.78500 level. On the whole, AUDUSD faces further bear threats.

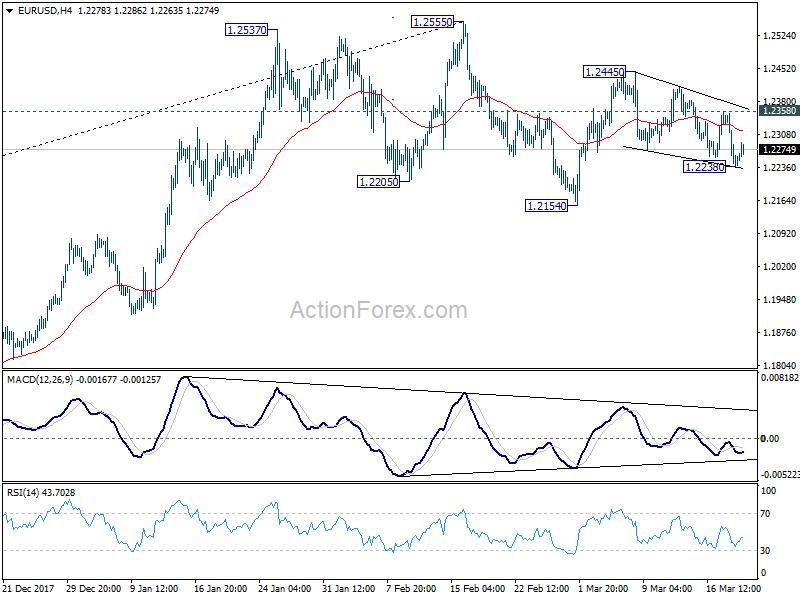

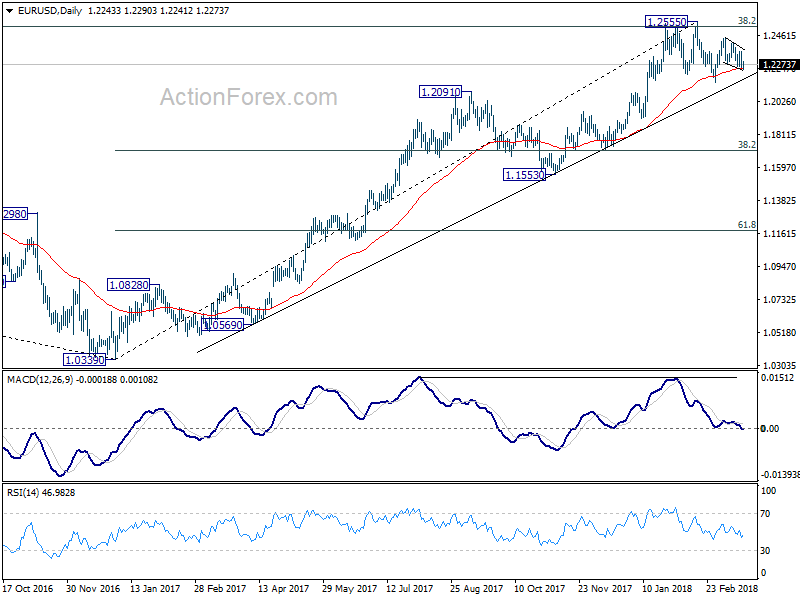

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2202; (P) 1.2278 (R1) 1.2317; More....

No change in EUR/USD's outlook that price action from 1.2445 are forming a corrective pattern, possibly a falling wedge. For the momentum, further rise remains mildly in favor. Break of 1.2358 resistance will revive the bullish case. That is, pull back from 1.2445 has completed. Intraday bias will be turned back to the upside for 1.2445 and then 1.2555 key resistance. However, firm break of 1.1238 will now turn bias back to the downside, to resume the fall from 1.2555 through 1.2154.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

USD and NZD Weak ahead of FOMC and RBNZ, Sterling lifted by Job Data

Sterling is staying in the spotlight today as the set of job and wage data boosts the chance of a May BoE hike. The central bank's announce tomorrow is now rather important as some hawks could come back flexing their muscles. Similar strong for today is Canadian Dollar, riding on positive news regarding NAFTA. On the other hand, Dollar, Aussie and Kiwi are under broad based pressure. FOMC and RBNZ will announce rate decision within a few hours from now. While one is expected to hike and the other is expected to stay dovish, the fate of them doesn't differ much, at least for today.

Fed to hike, new projections and Powell's press conference watched

Fed is widely expected to raise federal funds rate by 25bps to 1.50-1.75% today. There is practically no chance for a surprise in it. The main question in everybody's mind is whether Fed will hike a total of three times this year, or four. As usual with a March FOMC meeting, new economic projections will be released. Given that the Republican's tax cuts were done, there could be upward revisions in growth. Unemployment rate forecast might be left unchanged. PCE core at 1.5% in January, is still way off Fed's median projection of 1.9% in 2018. There is little chance of a change in that figure. Meanwhile, any slight change in the federal funds rate projection would be market moving. The event also bears additional significance as it's Powell's first press conference as Fed chair. Powell might maintain an upbeat tone today and indicate his confidence in continuing the tightening cycle.

More on FOMC in an earlier comment

Suggested readings on FOMC:

- Powell Likely to Be Quizzed on New Projections and Trade War Risks in First Press Conference

- Trading The Fed's Interest Rate Decision

- FOMC Preview: Connecting The Dots

- US Dollar Rises Ahead Of Fed Rate Announcement

- Fed Widely Expected To Hike Rates, Forward Guidance To Move The Dollar

Sterling boosted as unemployment rate fell, wage growth accelerated

Sterling jumps notably as positive response to UK job data. Unemployment rate dropped to 4.3%, down from 4.4%, and beat expectation of 4.4%. Average weekly earnings exclude bonus rose 2.6% 3moy, accelerated from 2.5% 3moy. More surprisingly, Average weekly earnings include bonus rose 2.8% 3moy, accelerated from 2.7% 3moy and beat expectation of of 2.6% 3moy. Claimant count, on the other hand, rose 9.2k versus expectation of -5k.

The set of data overall should be more than welcomed by BoE hawks. In particular, wage growth is picking up pace and would add to their argument of a May hike. Be ready and we might see a hawk or two vote for a hike in the announcement tomorrow. In particular, UK has the Brexit transition deal in pocket already.

Also released from UK, public sector net borrowing dropped GBP -0.3b in February.

Ifo forecast German economy to grow 2.6% in 2018, 2.1% in 2019

Ifo Institute forecasts German economy to grow 2.6% in 2018, then slow to 2.1% in 2019. It's head of f Economic Forecasting Timo Wollmershaeuser noted that the calculations "confirm figures from our December forecast.: However, "underlying forces have shifted somewhat." In particular, forecast for household consumption expenditure was scaled by by 0.5% in 2018, because of lower than expected spending back in 2H 2017. Government spending forecast was raised by 0.5% in 2018, as new government policy will provide a stimulus. Export growth was revised up by 0.5% in 2018, thanks to upturn in Eurozone economy and US tax cuts.

Regarding risks, "the debate over the introduction and/or increase in tariffs on transatlantic trade and the appreciation of the euro are weakening sentiment among German companies." Also, the new coalition government is "disappointing in terms of reforming the tax and social security system." In particular, Wollmershaeuser said that was no response to US, France and UK tax cuts.

CAD rebounded as NAFTA renegotiation cleared a major hurdle

Canadian Dollar rebounds strongly on news that US will drop contentious auto-content proposal in NAFTA talks. It's seen as clearing and important road block in NAFTA renegotiation. The Loonie is trading as the strongest major currency in Asian session. There was a demand for vehicles made in Canada and Mexico for export to the US contain at least 50% US content. But Canada's Globe and Mail reported that this contentious demand was dropped during NAFTA meeting in Washington last week. This is seen by some as one of the US toughest protectionist demand.

RBNZ to stand pat and maintain dovish bias

RBNZ will announce rate decision in the upcoming Asian session. RBNZ is widely expected to keep the Official Cash Rate OCR unchanged at 1.75%. In the prior statement, RBNZ noted that "monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain and policy may need to adjust accordingly." That's clearly seen as easing bias by the markets. We're not expecting any change in the OCR, nor the slightly dovish stance in tomorrow's announcement.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2202; (P) 1.2278 (R1) 1.2317; More....

No change in EUR/USD's outlook that price action from 1.2445 are forming a corrective pattern, possibly a falling wedge. For the momentum, further rise remains mildly in favor. Break of 1.2358 resistance will revive the bullish case. That is, pull back from 1.2445 has completed. Intraday bias will be turned back to the upside for 1.2445 and then 1.2555 key resistance. However, firm break of 1.1238 will now turn bias back to the downside, to resume the fall from 1.2555 through 1.2154.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Feb | 0.30% | -0.24% | -0.30% | |

| 9:30 | GBP | Jobless Claims Change Feb | 9.2K | -3.1K | -7.2K | |

| 9:30 | GBP | Claimant Count Rate Feb | 2.40% | 2.30% | ||

| 9:30 | GBP | Average Weekly Earnings 3M/Y Jan | 2.80% | 2.60% | 2.50% | 2.70% |

| 9:30 | GBP | ILO Unemployment Rate 3Mths Jan | 4.30% | 4.40% | 4.40% | |

| 9:30 | GBP | Public Sector Net Borrowing Feb | -0.3B | -0.4B | -101B | -11.6B |

| 14:00 | USD | Existing Home Sales Feb | 5.41M | 5.38M | ||

| 14:30 | USD | Crude Oil Inventories | 5.0M | |||

| 18:00 | USD | FOMC Rate Decision | 1.75% | 1.50% | ||

| 18:30 | USD | FOMC Press Conference | ||||

| 20:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% |