Sample Category Title

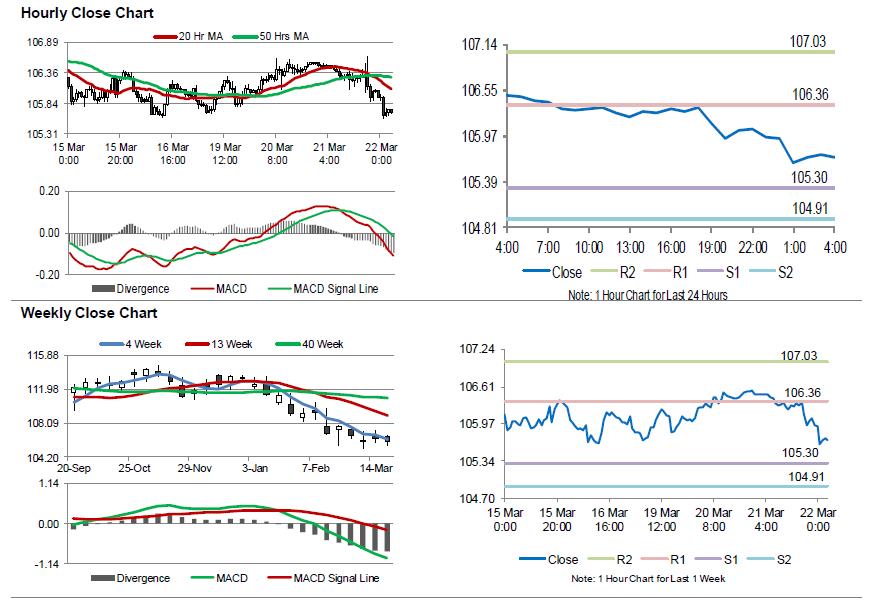

Japan’s Manufacturing Sector Growth Cooled In March

For the 24 hours to 23:00 GMT, the USD declined 0.50% against the JPY and closed at 105.95.

In the Asian session, at GMT0400, the pair is trading at 105.69, with the USD trading 0.25% lower against the JPY from yesterday's close.

Overnight data revealed that Japan's flash Nikkei manufacturing PMI declined to a level of 53.2 in March, compared to a level of 54.1 in the prior month.

Early morning data showed that the nation's all industry activity index eased 1.8% MoM in January, in line with market expectations. The index had advanced by a revised 0.6% in the prior month.

The pair is expected to find support at 105.30, and a fall through could take it to the next support level of 104.91. The pair is expected to find its first resistance at 106.36, and a rise through could take it to the next resistance level of 107.03.

Moving forward, Japan's national consumer price index (CPI) for February, slated to release overnight, will be eyed by market participants.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

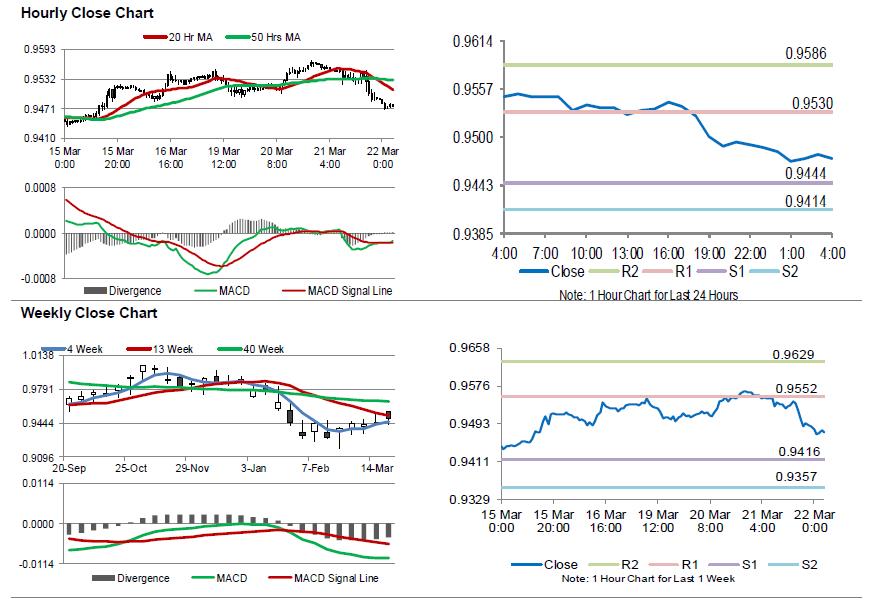

Swiss Franc Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.7% against the CHF and closed at 0.9488.

In the Asian session, at GMT0400, the pair is trading at 0.9475, with the USD trading 0.14% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9444, and a fall through could take it to the next support level of 0.9414. The pair is expected to find its first resistance at 0.9530, and a rise through could take it to the next resistance level of 0.9586.

With no major macroeconomic releases in Switzerland today, investor sentiment would be governed by global macroeconomic news.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

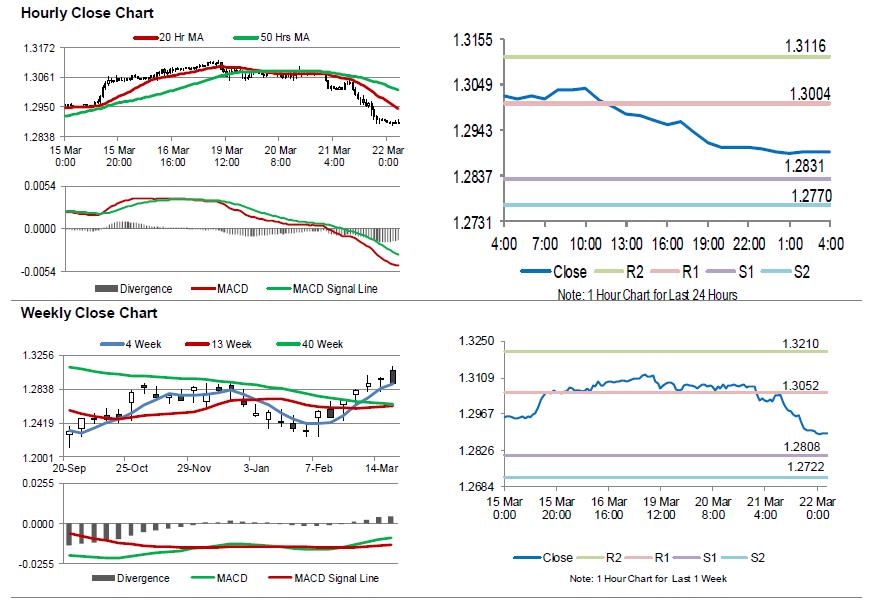

Loonie Extends Its Gains In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.98% against the CAD and closed at 1.2900.

In the Asian session, at GMT0400, the pair is trading at 1.2893, with the USD trading 0.10% lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.2831, and a fall through could take it to the next support level of 1.2770. The pair is expected to find its first resistance at 1.3004, and a rise through could take it to the next resistance level of 1.3116.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Trump to announce USD 50b tariffs on China today, China fights back… verbally… for now

Trump is set to announce the tariffs on 100 different types of Chinese goods today, as follow up to the section 301 of the Trade Act of 1974 investigation. Bloomberg reported that the targeted amount would be at around USD 50b annually. White House official Raj Shah also said in a statement that "tomorrow the president will announce the actions he has decided to take based on USTR's 301 investigation into China's state-led, market-distorting efforts to force, pressure, and steal U.S. technologies and intellectual property." It's believed that the tariffs won't take effect immediately. And the list of targeted products will be finalized after industry input. But it's only confirmed when it's confirmed.

On the other hand, China is readying retaliation measures. But before that, China's Ministry of Commerce pointed to WTO ruling against the Obama-era anti-subsidy tariffs. Back in 2012, China went to WTO to challenge U.S. anti-subsidy tariffs on Chinese exports including solar panels, wind turbines, steel cylinders and aluminum extrusions. And, the WTO ruled the United States had not fully complied with a 2014 ruling against its anti-subsidy tariffs on a range of Chinese products

The MOFCOM criticized that the US has "violated WTO rules, repeatedly abused trade remedy measures, which has seriously damaged the fair and just nature of the international trade environment and weakened the stability of the multilateral trading system." THe MOFCOM also pledged to oppose "protectionism by the US ahead of any possible trade measures against China" and to " take all necessary measures to resolutely protect its interests"

Separately, a former vice commerce minister and now an executive deputy director of the China Center for International Economic Exchanges, Wei Jianguo, warned that "if Trump really signs the order, that is a declaration of trade war with China." Wei said "China is not afraid, nor will it dodge a trade war." And, there are "plenty of measures to fight back, in areas of automobile imports, soybean, aircraft and chips.

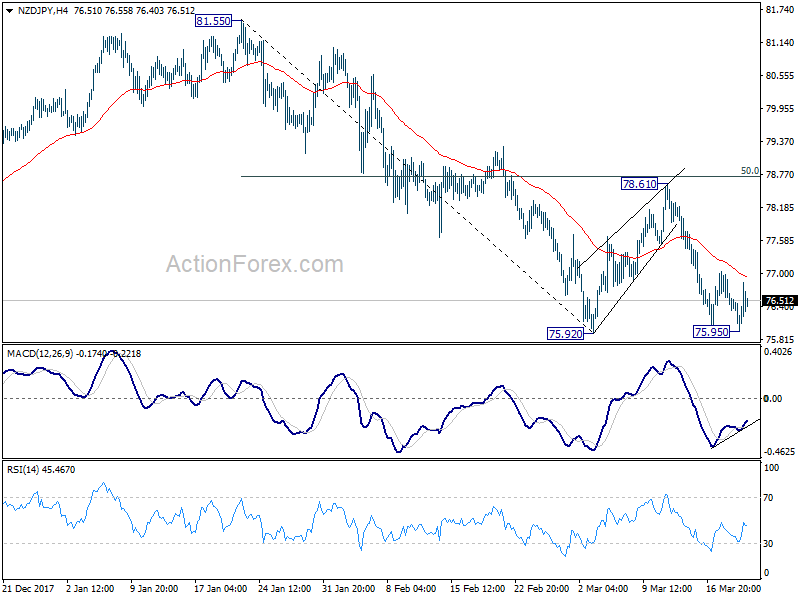

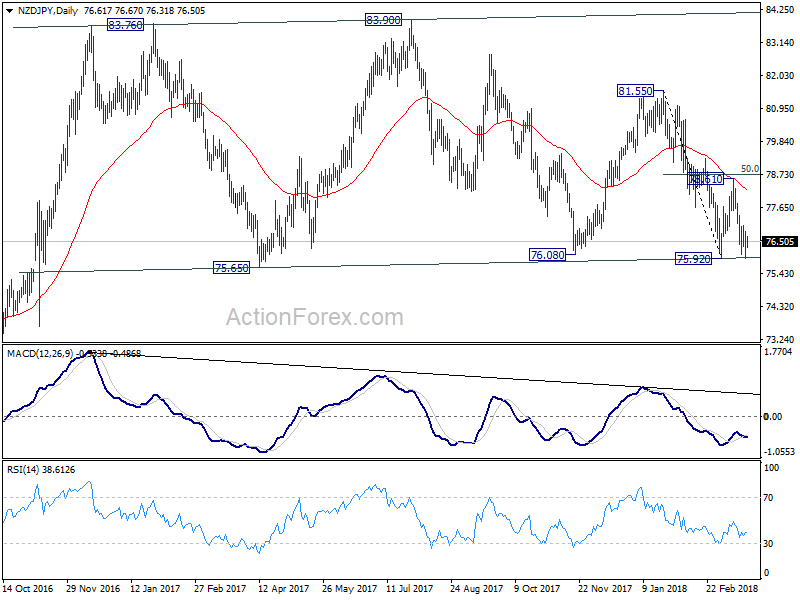

RBNZ Spencer: NZD in vicinity of fair value, NZD/JPY defended 76

NZD is relatively steady after RBNZ kept OCR unchanged at 1.75% as widely expected, and maintained a dovish stance. Outgoing Acting Governor Grant Spencer gave an interview before handing over to Adrian Orr. He noted that RBNZ shouldn't comment on NZD's exchange rate. And, he emphasized that "we should only comment on the currency if it's really pretty clear that it's out of alignment and you're wanting to have some impact, some sort of jaw-boning effect". Though, he acknowledged that "in the past we have got into this situation where we sort of had to make a statement about the currency and if we didn't the market was going to react." But then, he also said that NZD is "in the vicinity of fair value".

In the accompany statement, RBNZ maintained that "monetary policy will remain accommodative for a considerable period." It said, "inflation is expected to weaken further in the near term", before heading up to 2% target "over the medium term". And, "tradeable inflation is projected to remain subdued through the forecast period." At the same time, "non-tradables inflation is moderate but is expected to increase in line with a rise in capacity pressure." Regarding the economy, "growth is expected to strengthen, supported by accommodative monetary policy, a high terms of trade, government spending and population growth."

NZD/JPY's recovery from 75.59, with mild bullish convergence condition in 4 hour MACD, suggest that immediate threat of breaking 75.92 is over. NZD/JPY's near term outlook is rather mixed as momentum is clearly bearish. As it's held comfortably below falling 55 day EMA. But at the time time, 75.65/76.08 is a very important long term support zone. For now, there is little reason for sustainable rebound. But NZD/JPY bears will take more time and stimulus to take out this 75.65/76.08 support zone. So, range trading is likely the way to go.

FOMC Projects Two More Rate Hikes This Year, Followed By Three In 2019

FOMC's rate hike of +25 bps is not news. What caught market attention the most was the median dot plot (which continued to project 3 rate hikes in 2018) and the upgrades in the economic projections. US dollar plunged from almost a three-week highe after the announcement. The message delivered in the accompanying statement and by Fed Chair Powell at the press conference was not as hawkish as some had expected. Powell indicated he was not concerned about an overheating economy despite higher fiscal spending. Rather, he added that trade policies have become a rising concerns among policymakers.

On the updated economic forecasts, the staff raised the GDP growth forecast to +2.7% (previous +2.5%) and +2.4% (previous: +2.1%) for 2018 and 2019 respectively, as a result of tax reform and the Federal budget plan. Policymakers acknowledged that the economy “has strengthened in recent months”. The staff revised lower the unemployment rate to 3.8% for 2018 (previous: 3.9%) and 3.6% for both 2019 and 2020 (previous: 3.9% and 4.0% respectively). The long-term unemployment rate NAIRU was also taken down by -0.1 percentage point to 4.5%These numbers are almost a full percentage point below the Fed's latest estimate of NAIRU. On inflation, core PCE stayed unchanged for this year but was increased by a tenth each in 2019 and 2020 to 2.1%, signaling inflation might overshoot the +2% target.

While staying confident at the growth outlook, Powell at the press conference noted that “a number of participants did bring up the issue of tariffs". While he believed that “there's no thought that changes in trade policy should have any effect on the current outlook”, Powell added that "a number of participants reported that about their conversations with business leaders around the country and reported that trade policy has come a concern going forward for that growth".

The median dot plot continues to point to 3 rate hikes this year (two more to come). Yet, there are now 7 members expecting more than 3 rate hikes this year, compared with 4 in December. The median member expects an average federal funds rate of 2.9% and 3.4% in 2019 and 2020, respectively, up from 2.7% and 3.1%, suggesting that 3 rate hikes (compared with 2 previously)would come in 2019 and 2 (compared with 1.5 previously) for 2020. The market has now priced in 85% chance of another rate hike in June.

Bullish developments in GBPUSD and EURUSD after FOMC

USD's post FOMC selloff extends in Asia session, except versus AUD. Aussie pares back some gains after disappointment from its own employment data.

For the week, USD remains the worst performing one, followed by JPY. GBP and CAD remain nearly equally strong.

For the week, USD remains the worst performing one, followed by JPY. GBP and CAD remain nearly equally strong.

Two technical developments are worth noting after FOMC.

Two technical developments are worth noting after FOMC.

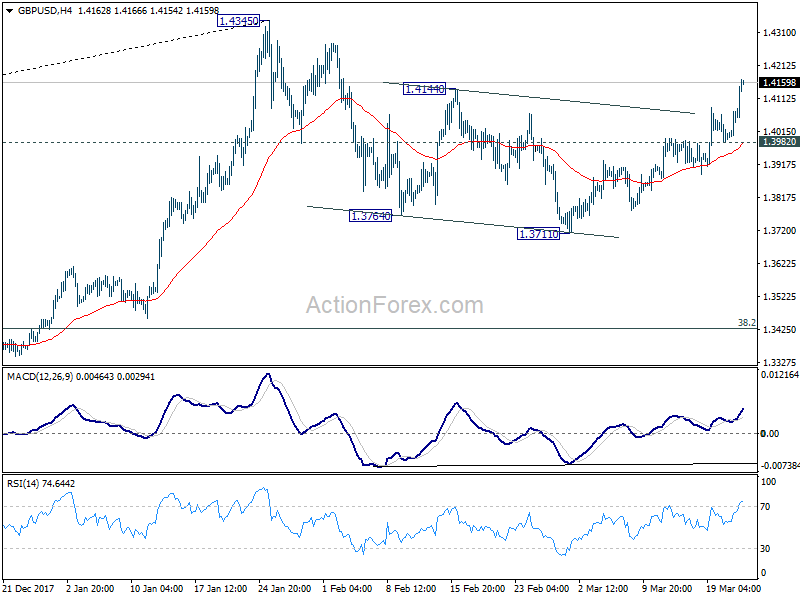

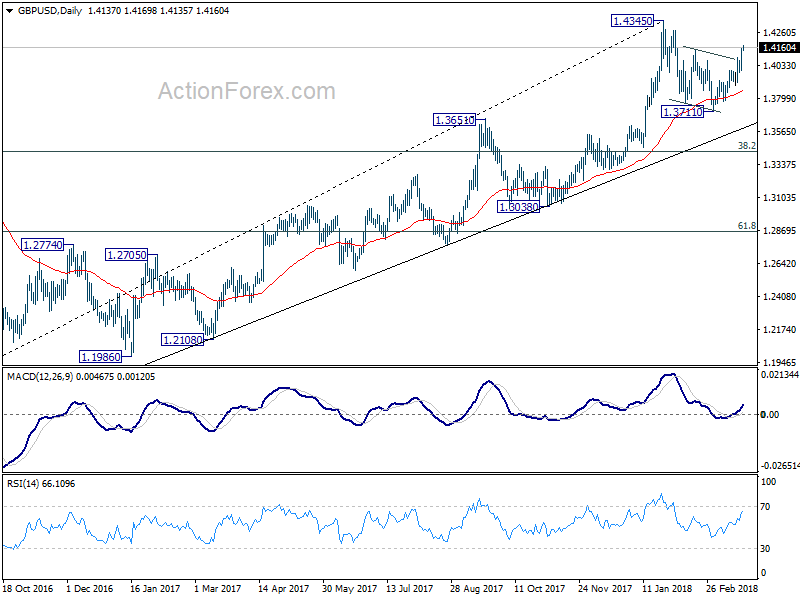

Firstly GBP/USD has now surged past 1.4144 resistance. The development further solidify the case that correction from 1.4345 has completed at 1.3711, as supported by 55 day EMA. And it's held above 1.3651 resistance turned support. That, thus, keep GBP/USD well supported in the healthy medium term up trend. Current rise should now extend to 1.4345 resistance technically. But of course, that will be subject to the outcome of today's BoE rate decision. While there is practically no change for BoE to hike, any hawkish twist of the language, or votes for hike, could shoot GBP/USD up through 1.4345.

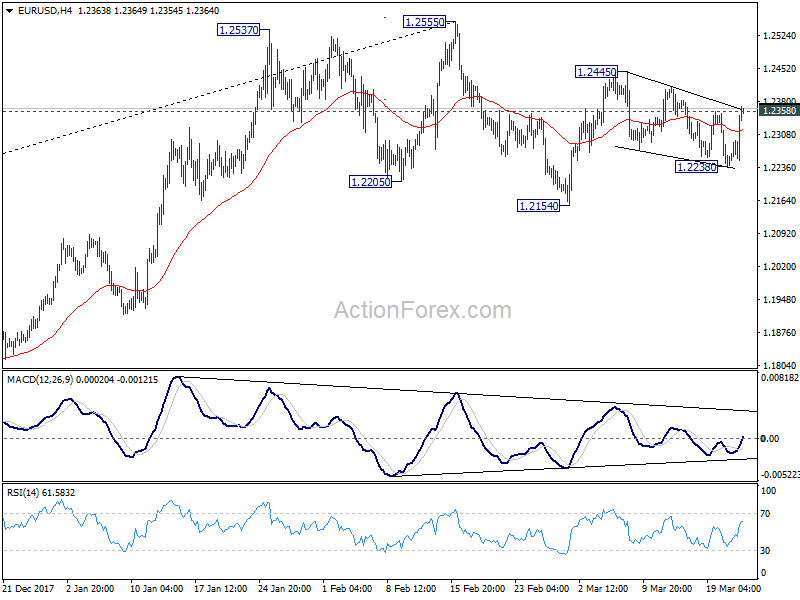

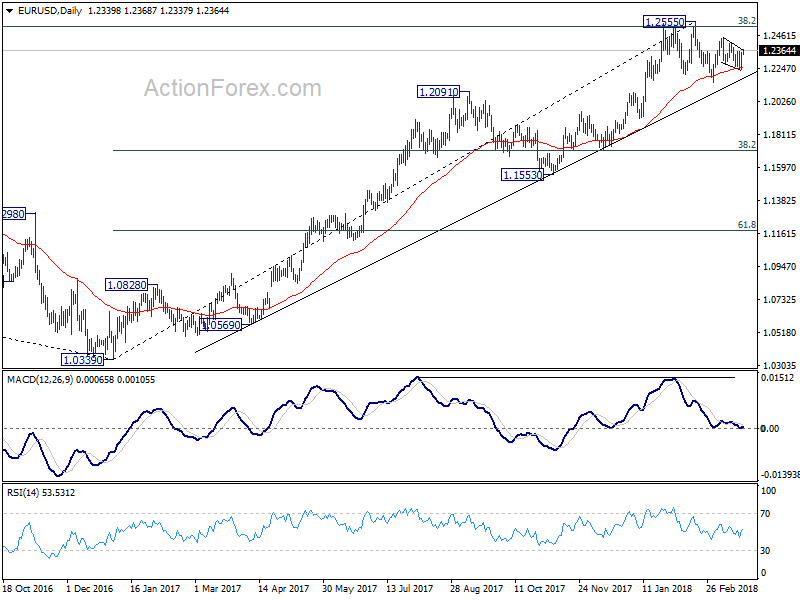

Euro is actually the third strongest for the week, following Sterling and Canadian Dollar. EUR/USD's breach of 1.2358 following FOMC also affirms the case that price action from 1.2455 are corrective. And the pattern could have completed at 1.2238 already. Further rise is now expected to 1.2445. Break will target 1.2555, the real key resistance level. So far, EUR/USD is also staying in healthy up trend as supported by rising 55 day EMA and above 1.2091 resistance turned support. Just that 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is an important hurdle to overcome.

Euro is actually the third strongest for the week, following Sterling and Canadian Dollar. EUR/USD's breach of 1.2358 following FOMC also affirms the case that price action from 1.2455 are corrective. And the pattern could have completed at 1.2238 already. Further rise is now expected to 1.2445. Break will target 1.2555, the real key resistance level. So far, EUR/USD is also staying in healthy up trend as supported by rising 55 day EMA and above 1.2091 resistance turned support. Just that 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is an important hurdle to overcome.

Increasingly Confident Fed Raises Rates, and Growth Forecasts

Highlights:

- The target range for the fed funds rate was raised to 1.50-1.75% in a unanimous decision.

- The statement noted the economic outlook has strengthened in recent months, though recent data point to a slightly softer start to the year for growth.

- The median GDP growth forecast was revised up by 1/2 percentage points over the next two years, likely reflecting fiscal stimulus. Unemployment was in turn revised lower.

- The median inflation projection now shows core prices rising slightly faster than the Fed’s 2% objective in 2019 and 2020.

- The ‘dot plot’ showed committee members are roughly split on whether two or three additional rate hikes will be appropriate this year. The median projection added one 25 basis point hike by the end of next year.

Our Take:

Today’s rate hike was no surprise and a slightly more upbeat tone in the policy statement was consistent with Governor Powell’s recent remarks. While acknowledging a somewhat softer start to the year for growth—which we think might reflect some of the same seasonal adjustment issues seen in years past—the statement echoed Powell’s assertion that the economic outlook has improved since December. That was reflected in the committee’s projections showing stronger growth over the next two years and a lower unemployment rate. There was also a slight nod to the inflationary impact of tight economic conditions with core inflation now projected at 2.1% in 2019 and 2020. Alongside those changes there was only a slight shift in the much-anticipated ‘dot plot’—just one extra rate hike over the next two years compared with December’s projection. For 2018, the committee is now almost evenly split on whether two or three further rate hikes will be appropriate. We think it will be the latter. As the Fed’s forecasts underline, fiscal stimulus is likely to keep the economy growing faster than its longer-run potential, lending some upside risk to the inflation outlook. Once-a-quarter rate hikes, still considered a ‘gradual’ pace, are appropriate.

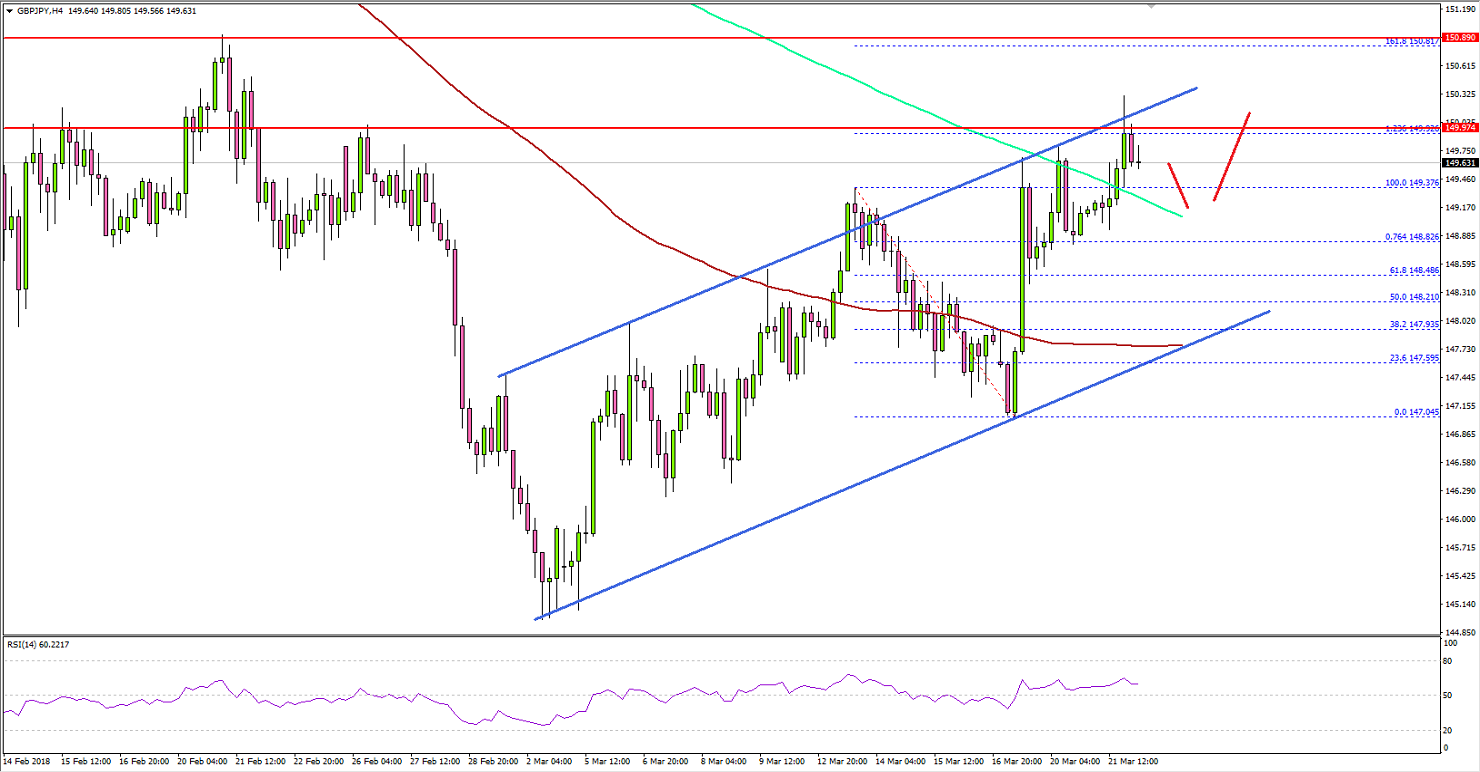

Can GBP/JPY Continue Trading Higher?

Key Highlights

- The British Pound made a nice upside move and traded above 149.00 against the Japanese Yen.

- There is a major ascending channel forming with support at 148.20 on the 4-hours chart of GBP/JPY.

- The UK Claimant Count Change came in at 9.2K in Feb 2018, compared with the forecast of -5.0K.

- Today, the BOE interest rate decision is scheduled and the market is looking for no change in rates from 0.50%.

GBPJPY Technical Analysis

The British Pound started a decent uptrend from the 147.04 low against the Japanese Yen. The GBP/JPY pair climbed above 148.50 and it seems like the pair may continue to move higher.

Looking at the 4-hours chart of GBP/JPY, the pair is trading well above the 149.00 pivot level and the 100 simple moving average (red, 4-hours). It broke the last swing high of 149.37 and it tested the 1.236 Fib extension of the last drop from the 149.37 high to 147.04 low.

On the positive side, there is a major ascending channel forming with support at 148.20 on the 4-hours chart of GBP/JPY. If the pair succeeds in moving above the 150.00 barrier, there may perhaps be a test of the 150.80 resistance.

The mentioned 150.80 resistance also represents the 1.618 Fib extension of the last drop from the 149.37 high to 147.04 low. On the flip side, if there is a downward correction, the pair is likely to find support near 148.50 and then around the channel support.

Recently in the UK, the Claimant Count Change report for Feb 2018 was released by the Office for National Statistics. The market was looking for a change of -5.0K compared with the previous -7.2K.

The real outcome was disappointing since there was no decline in the count, but instead there was a rise of 9.2K. Moreover, the last reading was revised to -1.6K. On the positive note, the ILO Unemployment Rate dropped from 4.4% to 4.3%.

The report added that:

The unemployment rate (the proportion of those in work plus those unemployed, that were unemployed) was 4.3%, down from 4.7% for a year earlier and the joint lowest since 1975.

The market sentiment broadly favored the British Pound. However, today’s BOE interest rate decision and retail sales report in the UK could impact both GBP/USD and GBP/JPY in the near term.

Economic Releases to Watch Today

- Germany’s Manufacturing PMI for March 2018 (Preliminary) – Forecast 59.8, versus 60.6 previous.

- Germany’s Services PMI for March 2018 (Preliminary) – Forecast 55.0, versus 55.3 previous.

- Euro Zone Manufacturing PMI March 2018 (Preliminary) – Forecast 55.5, versus 55.5 previous.

- Euro Zone Services PMI for March 2018 (Preliminary) – Forecast 55.0, versus 55.3 previous.

- US Manufacturing PMI for March 2018 (Preliminary) – Forecast 58.1, versus 58.6 previous.

- US Services PMI for March 2018 (Preliminary) – Forecast 55.8, versus 55.9 previous.

- US Manufacturing PMI for March 2018 (Preliminary) – Forecast 55.5, versus 55.3 previous.

- UK Retail Sales for Feb 2018 (YoY) – Forecast +1.3%, versus +1.6% previous.

- UK Retail Sales for Feb 2018 (MoM) – Forecast +0.4%, versus +0.1% previous.

- BoE Interest Rate Decision – Forecast 0.50%, versus 0.50% previous.

Market Morning Briefing: The US Fed Raised The Benchmark Funds Rate From 1.5% To 1.75%

STOCKS

Dow (24682.31, -0.18%) was stuck in the 25000-24600 region yesterday mostly in the whipsaw mode, unable to decide on which direction to take. While below 25000, the index looks bearish for the next couple of sessions targeting 24400 on the downside.

Dax (12309.15, +0.01%) has not been able to break on either side of the 12200-12400 region and may continue so for this week. While below 12400, medium term looks bearish and may eventually lead the index towards 12100 or lower.

Nikkei (21475.50, +0.44%) came down to re-test the immediate support levels also led by a stronger Yen. The support near 21000 is not able to create a sharp upmove beyond 22500 and while the Yen continues to strengthen, there could be some scope for Nikkei to come below 21000 soon.

Shanghai (3252.84, -0.86%) has fallen sharply and could gradually come down towards 3200. Near to medium term looks bearish.

Nifty (10155.25, +0.31%) is likely to remain stuck in the 10260-10020 region for a few sessions. Bias is towards a down move.

Sensex (33136.18, +0.42%) is also likely to face some resistance near 33500 and may come off from there towards 32750 in the near term. Thereafter a break on the downside looks more probable.

COMMODITIES

After the API report, it was now the EIA report yesterday which confirmed a fall by 2.6mln barrels in the US crude inventories last week to 428.31mln barrels. This further boosted the crude prices pushing them higher. Also note that the current weakness in the Dollar if continues could lead to a potential rise in the demand for crude.

Brent (69.51) and Nymex WTI (65.23) both rose sharply breaking the immediate resistance on the daily candles. Current levels are corresponding to the previous highs but if the oil prices sustains to break above current levels, we could see some more upside for the week before a corrective dip sets in.

Gold (1330.50) came up from levels near 1300 but only on a rise above 1340 we may focus higher levels of 1350-1375 region. .

Copper (3.0710) has bounced from just above 3.00 levels and we need to see if that sustains. If the price falls back towards 3.0 in the coming sessions, it could indicate some weakness in the coming sessions.

FOREX

The US Fed raised the benchmark funds rate from 1.5% to 1.75% and also struck a less hawkish tone in the press conference which followed, by signaling only 2 more rate hikes in 2018 (as opposed to the anticipation for 3 more hikes this year). As we had been expecting, this moderation in hawkishness has caused the Dollar to weaken.

Dollar index (89.533) has broken below support near 89.75-89.80 on the daily candles and is now near support on weekly line chart near 89.3-89.5. As we have mentioned earlier, this is a crucial support level whose break could lead to medium term bearishness for the Dollar. The next target on the downside (in case a break of 89.3-89.5 happens) would be support on daily candles near 88.5.

Euro (1.2360) again bounced from support on daily candles near 1.225 yesterday and is now testing immediate resistance on daily candles near 1.236-1.237. A breach of this resistance would take the Euro towards higher resistance level on 3 day candles near 1.255-1.260. This is a crucial level, whose breach could imply medium term bullishness for the Euro.

Dollar Yen (105.65), as per our expectation, dipped yesterday after testing resistance on daily candles near 106.5-106.6. It could now dip further towards support near 105 on daily candles. We have been saying that the Dollar Yen might be about to turn bearish towards 105 and lower in the next 1-2 weeks. A break of 105, if it happens, would be crucial since the Dollar Yen hasn’t been able to move below that level for more than a year.

Euro Yen (130.58) has immediate resistance on daily candles near 131 which should push it down again towards crucial support level of 130. Both Euro and Yen could strengthen further against the Dollar in the coming weeks (as mentioned above) – which might thereby keep the Euro Yen ranged above 130.

Pound (1.4159) as per our expectation, saw some bullishness and rose towards 1.42 from levels near 1.40 yesterday. It could attempt a test of 1.44 (seen as resistance on 3 day candles and 3 day line charts) in the coming 1-2 weeks.

Dollar Rupee (65.21) - Immediate support seen at 65.05/06 with lower supports at 65.0-64.80. An upmove in Dollar Rupee above 65.25 could take it higher towards 65.40/60.

INTEREST RATES

The US Fed’s rate hike of 25 basis points was supplemented by a moderation of its hawkish stance (via signaling of only 2 more rate hikes this year as opposed to the much anticipated 3 more hikes). However, the Fed now signals 3 rate hikes in 2019 instead of the earlier 2. Against our expectation, bond yields haven’t seen a significant rise post the rate hike yet. Our Treasury report for Mar’18 (available on demand) predicts a decline in yields after an initial upmove in the days post the rate hike. Looks like the decline might happen without the initial upmove – let’s wait and watch.

US 10 Yr Yield (2.87%), 30 Yr (3.10%), 5 Yr (2.66%), 2 Yr (2.295%) : US 2 Year yield has dropped below 2.3% while the other longer term yields continue to move around levels seen in the past week. On the short term chart, the 30 yr yield could move up towards 3.2% after having tested support near 3.05%. The 10 Yr yield is in a downward channel, which if not broken, would mean that it could dip towards 2.8% again.

The targets for Apr’18 mentioned in our Treasury report are 3.075% for the 10 Year yield, 3.3% for the 30 Yr yield and 2.925% for the 5 Year yield. We might revisit these if the decline in yields happens earlier than expected.