Sample Category Title

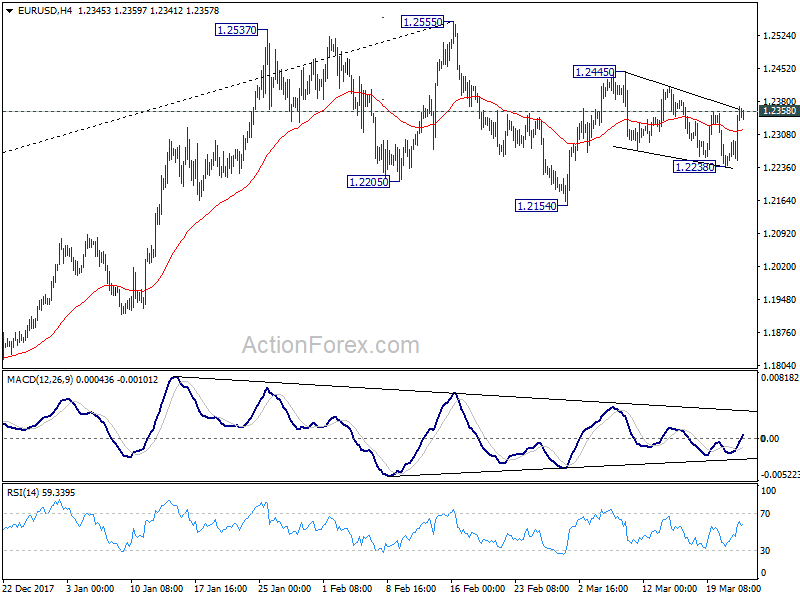

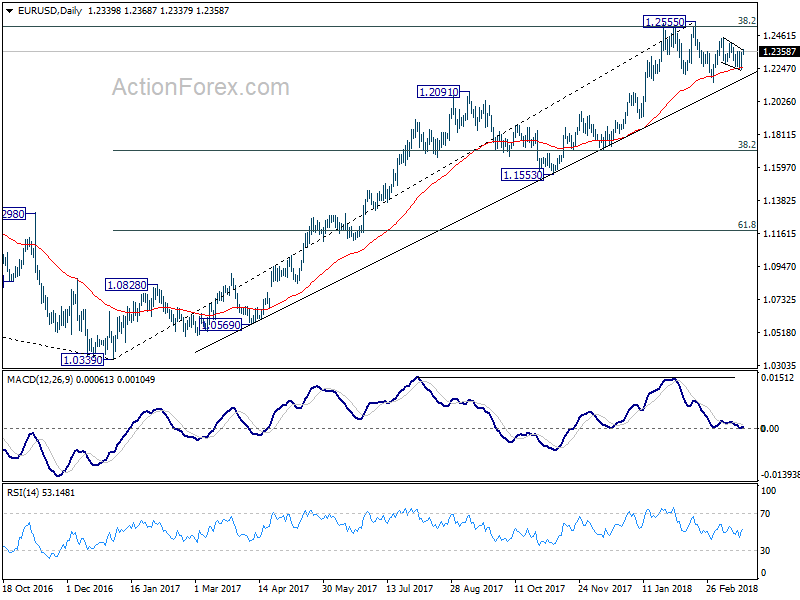

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2268; (P) 1.2309 (R1) 1.2378; More....

EUR/USD's strong rebound and breach of 1.2358 minor resistance affirm our bullish view. That is, price actions from 1.2445 is a corrective pattern in form of falling wedge. And, it might be completed at 1.2238 already. Intraday bias is now on the upside for 1.2445 first. Break will resume whole rebound from 1.2154 and target 1.2555 high, which is close to 1.2516 key long term fibonacci level. On the downside, however, firm break of 1.1238 will turn bias back to the downside, to resume the fall from 1.2555 through 1.2154.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Asian Market Update: Nikkei Rises After Recent Holiday

Headlines/Economic Data

General Trend:

- Tencent declines after Q4/FY17 results; some analysts issue cautious commentary

- China Mobile FY17 earnings beat ests, Revs below

- Japan Exchange raises FY guidance on higher forecast for daily trading value and volumes

- USD trades generally weaker in aftermath of Fed amid focus on 2018 rate path

- Reserve Bank of New Zealand (RBNZ) does not mention currency in statement

- China and Hong Kong raise rates after US Fed

- Hong Kong reiterates currency peg to US dollar

- Short-term rates move higher in Australia and Hong Kong

- Aussie employment rises for 17th straight month in Feb, misses estimates; Unemployment rate rises as participation hits highest since Dec 2010

- US budget situation again in focus

Australia/New Zealand

- ASX 200 opened -0.4%; closed -0.2%

- ASX 200 Telecom Index -1.7%, Utilities -1.2%, REIT -1%, Financials -0.4%; Resources +1.9%, Energy +1.4%

- (AU) AUSTRALIA FEB EMPLOYMENT CHANGE: 17.5K V 20.0KE; UNEMPLOYMENT RATE: 5.6% V 5.5%E

- (NZ) NEW ZEALAND CENTRAL BANK (RBNZ) LEAVES OFFICIAL CASH RATE (OCR) UNCHANGED AT 1.75%, AS EXPECTED

China/Hong Kong

- Shanghai Composite opened flat, Hang Seng +0.5%

- Hang Seng Information Tech Index -2.9%, Services -1.2%, Consumer Goods -0.7%, Property/Construction -0.6%, Financials -0.5%; Energy +0.8%

- Shanghai Composite Property index declines over 1%

- Sportswear company Li Ning [2331.HK] rises over 3% after earnings report

- (CN) PBOC RAISES RATE ON 7-DAY REVERSE REPO BY 5BPS TO 2.55% FROM 2.50% (tracks Wed's 25bps rate hike by US Fed, as speculated)

- (HK) Hong Kong Monetary Authority (HKMA) raises base rate by 25bps to 2.0% (tracks Fed, as expected)

- (CN) China said to increase the net profit requirement for IPO applications - Chinese Press

- (CN) China Dalian City said to begin home purchase restrictions – US financial press

- (US) Follow Up: White House: President Trump to sign memo on China trade at 12:30 PM EST on Thursday [Reminder: Earlier on Wednesday, White House spokesperson Shah confirmed that Trump would announce trade actions on China intellectual property on Thursday]

- (CN) China said to name Guo Shuqing (current CBRC Chairman) as head of new regulator for banking and insurance sectors

- (CN) China PBoC sets yuan reference rate at 6.3167 v 6.3396 prior

- (HK) Hong Kong Monetary Authority (HKMA) Chan: HKD will 'very soon' hit lower end of trading band at 7.85; to buy HKD when currency touches weak end of trading band (HK$7.75-7.85)

- (CN) Moody's: US tariffs have limited impact on China so far, but broad-ranging measures would pose greater challenges

Japan

- Nikkei 225 opened -0.1% (closed prior session for holiday); closed +1%

- TOPIX Electric Appliances Index +0.9%, Real Estate +0.6%; Securities -0.4%, Iron/Steel -0.3%

- (JP) Japan 3-month basis swap rate rises to highest since 2014

- (JP) Japan MAR Preliminary PMI Manufacturing: 53.2 v 54.1 prior (slows for 2nd straight month)

- (JP) Japan Jan All Industry Activity Index M/M: -1.8% v -1.8%e

- Looking Ahead: Japan Feb National CPI due for release on Friday

- (JP) New BoJ Dep Gov Wakatabe to appear in parliament at 5:14 PM local time on Thursday (4:14 AM EST)

Korea

- Kospi opened +0.4%

- (KR) South Korea President Moon said to propose lowering the voting age by 1 year to 18, proposed two 4-year presidential terms vs one 5-year term currently; The proposals are part of the constitutional amendment bill. - US financial press

- (KR) Bank of Korea Gov Lee: Sees little market impact from Fed interest rate hike; Don't see capital outflow on rate gap in recent moves

- (KR) Hana Financial says Bank of Korea (BoK) may raise rates in May and H2 2018 – US financial press

North America

- US equity markets ended mostly lower: Dow -0.2%, S&P500 -0.2%, Nasdaq -0.3%, Russell 2000 +0.6%

- S&P500 Consumer Staples -1.2%; Energy +2.6%

- (US) DOE CRUDE: -2.6M V +2.5ME;

- (US) US House and Senate leaders said to agree on $1.3T omnibus spending bill; Republicans said to expect vote during Thursday afternoon - financial press

- (US) The House Republican Freedom Caucus said that it is opposed to the spending measure.

- (US) FOMC RAISES TARGET RATE RANGE 25BPS TO 1.50-1.75% (AS EXPECTED); Affirms Median forecast for end-2018 rate 2.125% (prior 2.125%)

- Summary of Comments from Fed Chair Powell’s Post Rate Decision Press Conference

- Overall financial conditions remain accommodative

- Trying to take middle ground on rate hikes, consisting of further gradual rate hikes as long as economy remains on path

- Rate path could become more or less gradual depending on how economy is doing

- Cannot give exact number on how far they might allow inflation to rise above 2% target but goal is keeping around 2% level;

- No sense in data that we are on the cusp of an inflation acceleration

- There's no thought that changes in trade policy should have any effect on current outlook;Trade policy has become a concern for businesses

Europe

- (EU) US Commerce Dept: EU and US have agreed to begin discussion on trade issues; Talks will include discussions of steel and aluminum - joint statement with EU's Malmstrom

- (EU) EU Council Pres Tusk: economy continues to grow above expectations; Cautiously optimistic about receiving exemption from US aluminum/steel tariffs

- (GE) Germany Finance Ministry Monthly Report: Feb Tax Rev +8.1% y/y; Indicators suggest German economic growth slowed at start of 2018

- (ES) Catalan Parliament expected to meet tomorrow and nominate Turull as the new President – press

- Looking Ahead: Bank of England (BoE) rate decision due later today

Levels as of 01:00ET

- Hang Seng -0.5%; Shanghai Composite -0.6%; Kospi +0.5%

- Equity Futures: S&P500 +0.1%; Nasdaq100 +0.1%, Dax +0.1%; FTSE100 flat

- EUR 1.2337-1.2370 ; JPY 105.57-106.10; AUD 0.7736-0.7787 ;NZD 0.7222-0.7246

- Feb Gold +0.6% at $1,329/oz; Feb Crude Oil +0.1% at $65.25/brl; Mar Copper -0.1% at $3.076/lb

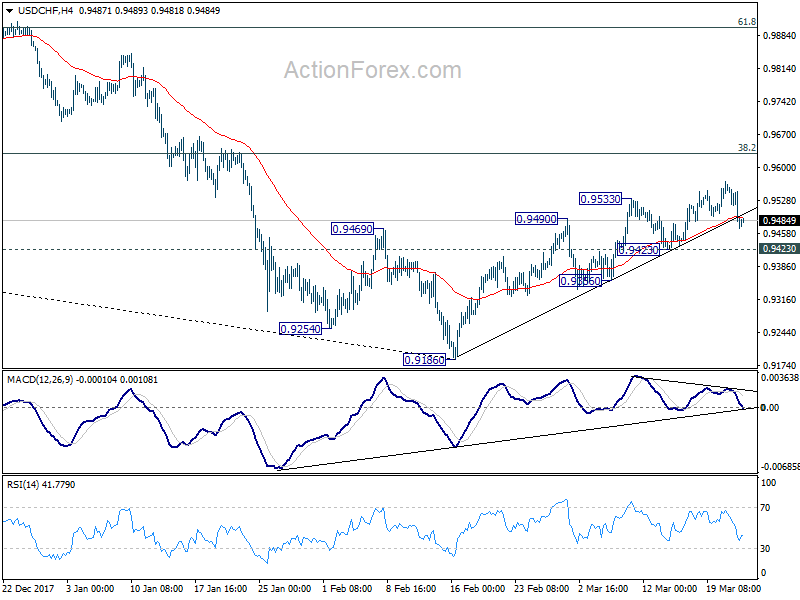

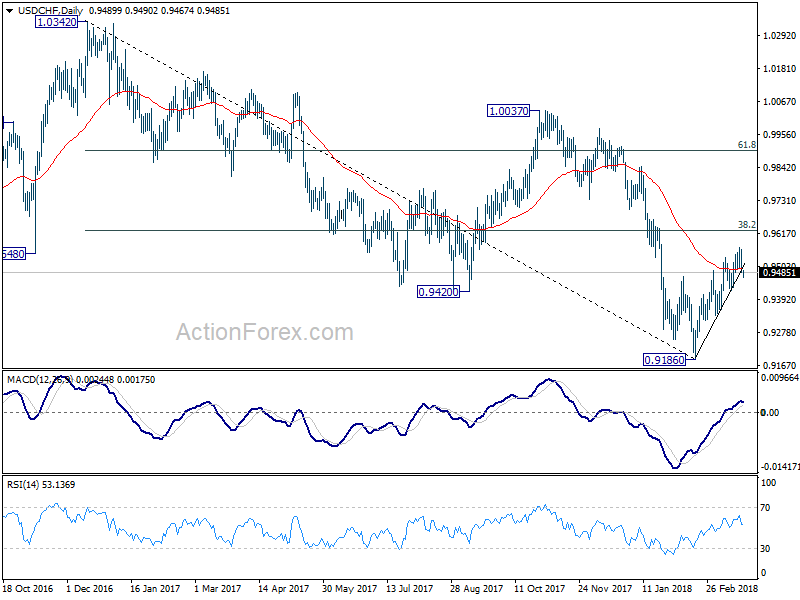

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9520; (P) 0.9544; (R1) 0.9588; More...

Intraday bias in USD/CHF remains neutral at this point. Another rise cannot be ruled out yet. But considering bearish divergence condition in 4 hour MACD, upside should be limited by 0.9626 key fibonacci level, to complete the rebound from 0.9186. Break of 0.9432 support will indicate near term reversal and turn bias to the downside for retesting 0.9186 low. Nonetheless, sustained break of 0.9626 will carry larger bullish implications.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Current development is raising the chance that it is completed. But there is no confirmation yet. Focus will now be back on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add much credence to the case of trend reversal and target 61.8% retracement at 0.9900 and above. However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

USD/JPY Daily Outlook

Daily Pivots: (S1) 105.73; (P) 106.18; (R1) 106.49; More...

USD/JPY continues to gyrate in range of 105.24/107.67 and outlook is unchanged. Intraday bias remains neutral. With 107.67 resistance intact, near term outlook remains bearish and further decline is expected. The corrective price actions since 105.24 support this. On the downside, break of 105.24 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. On the upside, firm break of 107.67 resistance will indicate near term reversal, on bullish convergence condition in 4 hour MACD. In such case, outlook will be turned bullish for 110.47 resistance next.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

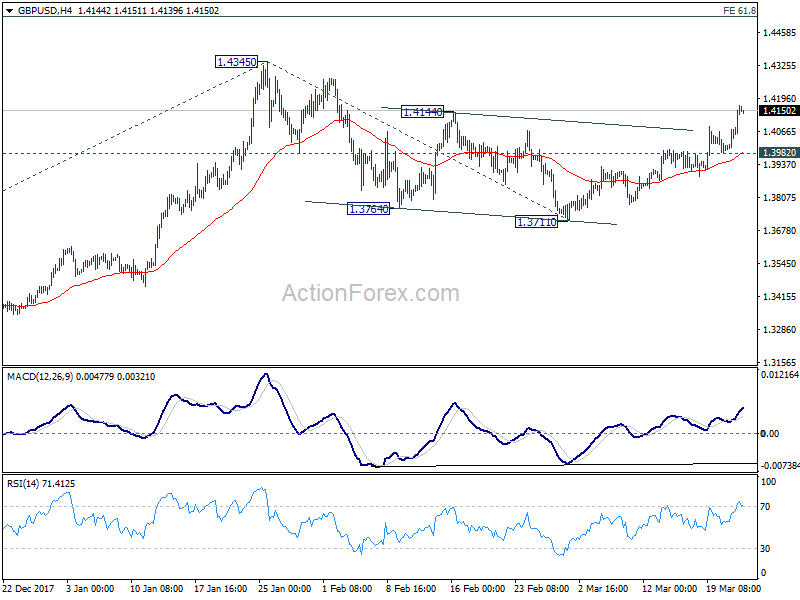

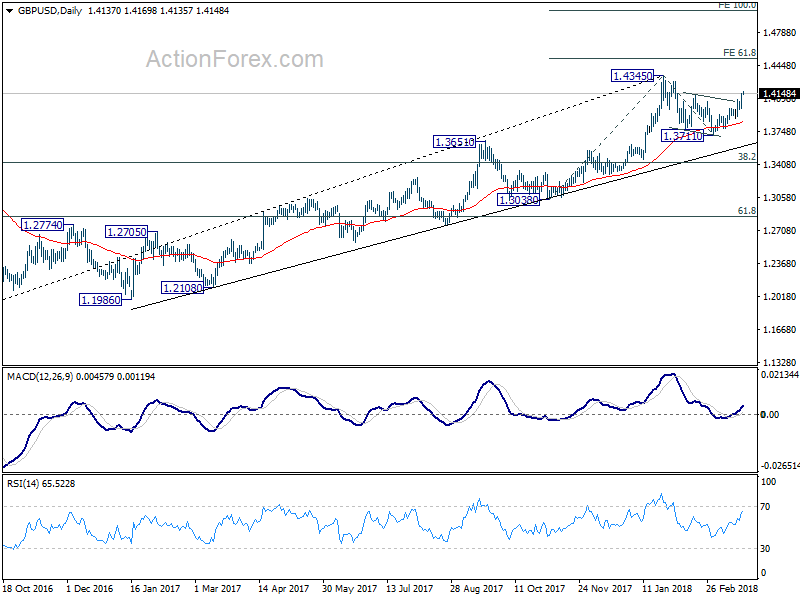

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3964; (P) 1.4015; (R1) 1.4048; More....

GBP/USD's rally resumed after brief retreat and reaches as high as 1.4169 so far. The break of 1.4144 resistance should confirm our bullish view that correction from 1.4345 has completed at 1.3711 already. Intraday bias is now on the upside for 1.4345 high next. Break will resume larger up trend to 61.8% projection of 1.3038 to 1.4345 from 1.3711 at 1.4519 first. On the downside, break of 1.3982 support is needed to signal completion of the rise from 1.3711. Otherwise, outlook will remain cautiously bullish in case of retreat.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

Dollar Broadly Pressured after FOMC, Sterling Strong ahead of BoE

Dollar stays broadly pressured today as post FOMC selloff extends. While Fed delivered the widely anticipated rate hike, it maintained the forecast of a total of three hikes in 2018 only, not four. Aussie is the only failing to join the party against Dollar today after weaker than expected job data. Sterling remains the strongest major currency for the week even though it turns slightly cautious against Euro and Yen today. BoE rate decision is the main event to watch and any hawkish twist in the announcement would propel Sterling further higher. In addition, Eurozone will release PMIs and German Ifo. US President Donald Trump will also finally announce his tariffs against China.

BoE to stand pat but may indicate a May hike

BoE is widely expected to keep the bank rate unchanged at 0.50% today. The asset purchase target will also be held at GBP 435b. After this week's events, the announce has become very lively. The announcement that UK and EU has reached the Brexit transition deal has given the pound a strong boost. It still has to go through EU summit at the end of the week but that should just a matter of formality only. The development also cleared an important uncertainty for BoE in its monetary policy consideration.

Sterling's strength was somewhat limited later by disappointing inflation data. CPI slowed more than expected to 2.7% yoy in February, versus consensus of 2.8% yoy. Core CPI also slowed to 2.4% yoy, below expectation of 2.5% yoy. But later, the pound was lifted again by employment data as unemployment rate dipped to 4.3% from 4.4%. More importantly, wage growth showed acceleration with average weekly earnings including bonus jumped to 2.8% 3moy.

On the one hand, Brexit development would remove an excuse for BoE doves to urge for patience. On the other hand, the strength in wage growth now gives BoE hawks a bullet to push for rate hike. Sterling could be shoot up again if BoE announcement today signals that it's getting closer for a May hike. That could be come by a twist in the language of the statement. Or, it could be signaled by some votes for hike by hawks like Michael Saunders and Ian McCafferty

More readings on BoE:

- UK And EU Reached Transition Deal, Erasing Key Uncertainty Of BOE's Rate Hike Path

- Will BoE Lay the Foundations For May Rate Hike?

- Brexit Transition Deal Gives BoE Go-Ahead For May Rate Hike But UK Data Poses Dilemma

Trump to announce USD 50b tariffs on China today, China fights back… verbally… for now

Trump is set to announce the tariffs on 100 different types of Chinese goods today, as follow up to the section 301 of the Trade Act of 1974 investigation. Bloomberg reported that the targeted amount would be at around USD 50b annually. White House official Raj Shah also said in a statement that "tomorrow the president will announce the actions he has decided to take based on USTR's 301 investigation into China's state-led, market-distorting efforts to force, pressure, and steal U.S. technologies and intellectual property." It's believed that the tariffs won't take effect immediately. And the list of targeted products will be finalized after industry input. But it's only confirmed when it's confirmed.

On the other hand, China is readying retaliation measures. But before that, China's Ministry of Commerce pointed to WTO ruling against the Obama-era anti-subsidy tariffs. Back in 2012, China went to WTO to challenge U.S. anti-subsidy tariffs on Chinese exports including solar panels, wind turbines, steel cylinders and aluminum extrusions. And, the WTO ruled the United States had not fully complied with a 2014 ruling against its anti-subsidy tariffs on a range of Chinese products

The MOFCOM criticized that the US has "violated WTO rules, repeatedly abused trade remedy measures, which has seriously damaged the fair and just nature of the international trade environment and weakened the stability of the multilateral trading system." The MOFCOM also pledged to oppose "protectionism by the US ahead of any possible trade measures against China" and to " take all necessary measures to resolutely protect its interests"

Separately, a former vice commerce minister and now an executive deputy director of the China Center for International Economic Exchanges, Wei Jianguo, warned that "if Trump really signs the order, that is a declaration of trade war with China." Wei said "China is not afraid, nor will it dodge a trade war." And, there are "plenty of measures to fight back, in areas of automobile imports, soybean, aircraft and chips.

Dollar broadly lower as Fed maintained projection of 3 hikes in total this year

FOMC's rate hike of 25 bps to 1.50-1.75% was fully expected. . What caught market attention the most was the median dot plot (which continued to project 3 rate hikes in 2018) and the upgrades in the economic projections. US dollar plunged from almost a three-week higher after the announcement. The message delivered in the accompanying statement and by Fed Chair Powell at the press conference was not as hawkish as some had expected. In particular, the median dot plot continues to point to 3 rate hikes this year (two more to come), rather than a total of 4 hikes in 2018. More in FOMC Projects Two More Rate Hikes This Year, Followed By Three In 2019.

Further readings on FOMC:

- USD Suffers Selloff after FOMC and Powell, Worst against GBP and CAD

- Fed maintains forecast of three hikes in 2018, expects one extra in 2019

- Increasingly Confident Fed Raises Rates, and Growth Forecasts

- FOMC Review: Only Slightly Steeper Rate Path Due To Trumponomics

- Fed Recap: Dollar Sinks Despite Higher Fed Forecasts

- The Fed Remains Resolute, Even in the Face of Softer Data

- FOMC Raises the Fed Funds Rate to 1-1/2 to 1-3/4

RBNZ stands pat, Spencer said NZD in vicinity of fair value

NZD is relatively steady after RBNZ kept OCR unchanged at 1.75% as widely expected, and maintained a dovish stance. Outgoing Acting Governor Grant Spencer gave an interview before handing over to Adrian Orr. He noted that RBNZ shouldn't comment on NZD's exchange rate. And, he emphasized that "we should only comment on the currency if it's really pretty clear that it's out of alignment and you're wanting to have some impact, some sort of jaw-boning effect". Though, he acknowledged that "in the past we have got into this situation where we sort of had to make a statement about the currency and if we didn't the market was going to react." But then, he also said that NZD is "in the vicinity of fair value".

In the accompany statement, RBNZ maintained that "monetary policy will remain accommodative for a considerable period." It said, "inflation is expected to weaken further in the near term", before heading up to 2% target "over the medium term". And, "tradeable inflation is projected to remain subdued through the forecast period." At the same time, "non-tradables inflation is moderate but is expected to increase in line with a rise in capacity pressure." Regarding the economy, "growth is expected to strengthen, supported by accommodative monetary policy, a high terms of trade, government spending and population growth."

On the data front

Australia employment was a disappointment to the markets. Australian economy added 17.5k job in February, below expectation of 20.3k. Unemployment rate also rose to 5.6%, above expectation of 5.5%. Japan PMI manufacturing dropped to 53.2 in March, below expectation of 54.3. Japan all industry activity index dropped -1.8% mom in January.

Looking ahead, while BoE is the major focus, there are other key features in the calendar too. Eurozone will release PMIs and German Ifo business climate. ECB will release monthly bulletin. UK will also release retail sales. Later in the day, US will release jobless claims, house price index, PMIs and leading indicator.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3964; (P) 1.4015; (R1) 1.4048; More....

GBP/USD's rally resumed after brief retreat and reaches as high as 1.4169 so far. The break of 1.4144 resistance should confirm our bullish view that correction from 1.4345 has completed at 1.3711 already. Intraday bias is now on the upside for 1.4345 high next. Break will resume larger up trend to 61.8% projection of 1.3038 to 1.4345 from 1.3711 at 1.4519 first. On the downside, break of 1.3982 support is needed to signal completion of the rise from 1.3711. Otherwise, outlook will remain cautiously bullish in case of retreat.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 20:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% | 1.75% | |

| 0:30 | AUD | Employment Change Feb | 17.5K | 20.3K | 16.0K | 12.5K |

| 0:30 | AUD | Unemployment Rate Feb | 5.60% | 5.50% | 5.50% | |

| 0:30 | JPY | PMI Manufacturing Mar P | 53.2 | 54.3 | 54.1 | |

| 4:30 | JPY | All Industry Activity Index M/M Jan | -1.80% | -1.80% | 0.50% | 0.60% |

| 8:00 | EUR | France Manufacturing PMI Mar P | 55.5 | 55.9 | ||

| 8:00 | EUR | France Services PMI Mar P | 57 | 57.4 | ||

| 8:30 | EUR | Germany Manufacturing PMI Mar P | 59.8 | 60.6 | ||

| 8:30 | EUR | Germany Services PMI Mar P | 55 | 55.3 | ||

| 9:00 | EUR | Eurozone Manufacturing PMI Mar P | 58.1 | 58.6 | ||

| 9:00 | EUR | Eurozone Services PMI Mar P | 56 | 56.2 | ||

| 9:00 | EUR | Eurozone Current Account (EUR) Jan | 30.2B | 29.9B | ||

| 9:00 | EUR | German IFO Business Climate Mar | 114.6 | 115.4 | ||

| 9:00 | EUR | German IFO Expectations Mar | 104.4 | 105.4 | ||

| 9:00 | EUR | German IFO Current Assessment Mar | 125.6 | 126.3 | ||

| 9:00 | EUR | ECB Economic Bulletin | ||||

| 9:30 | GBP | Retail Sales M/M Feb | 0.40% | 0.10% | ||

| 12:00 | GBP | BoE Rate Decision | 0.50% | 0.50% | ||

| 12:00 | GBP | BoE Asset Purchase Target Mar | 435B | 435B | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | 0--0--9 | 0--0--9 | ||

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0--0--9 | 0--0--9 | ||

| 12:30 | USD | Initial Jobless Claims (MAR 17) | 225K | 226K | ||

| 13:00 | USD | House Price Index M/M Jan | 0.40% | 0.30% | ||

| 13:45 | USD | US Manufacturing PMI Mar P | 55.5 | 55.3 | ||

| 13:45 | USD | US Services PMI Mar P | 56 | 55.9 | ||

| 14:00 | USD | Leading Index Feb | 0.50% | 1.00% | ||

| 14:30 | USD | Natural Gas Storage | -93B |

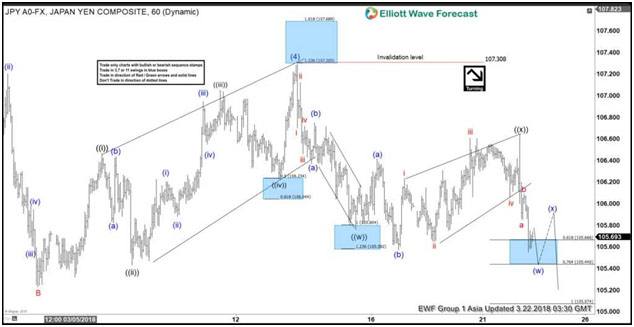

Elliott Wave Analysis: USDJPY Resumes Lower To 104

USDJPY Elliott Wave view suggests that the decline from 11.6.2017 high is unfolding as a 5 waves impulse Elliott Wave structure. Down from 11.6.2017 high (114.73), Intermediate wave (1) ended at 110.84, Intermediate wave (2) ended at 113.75, Intermediate wave (3) ended at 105.55, and Intermediate wave (4) ended at 107.3. Intermediate wave (5) is in progress as an Ending Diagonal Elliott Wave structure.

Down from 107.3, Minute wave ((w)) ended at 105.76 and Minute wave ((x)) ended at 106.64. Subdivision of Minute wave ((w)) unfolded as a zigzag Elliott Wave structure where Minutte wave (a) ended at 106.37, Minutte wave (b) ended at 106.75, and Minutte wave (c) of ((w)) ended at 105.76. Subdivision of Minute wave ((x)) unfolded as an Expanded Flat Elliott Wave structure where Minutte wave (a) ended at 106.41, Minutte wave (b) ended at 105.57, and Minutte wave (c) of ((x)) ended at 106.64. Near term, expect pair to bounce in Minutte wave (x) to correct cycle from 106.64 high, then as far as pivot at 3.13.2018 high (107.3) stays intact, expect pair to extend lower towards 104 area.

USDJPY 1 Hour Elliott Wave Chart

The PMI Figures For March Will Be Released Today

Market movers today

There are a number of interesting data releases today. Furthermore, financial markets will also look out for new trade measures from the US versus China and possible counteraction by the Chinese authorities.

In the US , Markit PMIs for March are due for release. We expect the manufacturing PMI to stabilise at a relatively high level of around 55 after having fallen back a bit last month. Optimism remains high as consumer confidence rose further in February, which in our view, suggests that the services PMI could rise further from 55.9 to 56.4.

In the euro area, the PMI figures for March will be released today. For two consecutive months, we have seen manufacturing PMI decline. After peaking at 60.6 in December 2017, it declined to 58.6 in February. We expect to see a further decline to 57.6 in March from 58.6 in February given the negative order-inventory indicator and impact of the 2017 euro appreciation. The Services PMI is also expected to decline in March to 55.7 from 56.2 in February.

We expect the German Ifo expectations to have fallen further in March to 105.0 from 105.4 in February, thereby increasing the downward trend seen since November last year.

In the UK, eyes will be on the Bank of England (BOE) meeting today, although we do not expect any major policy shifts and on the EU summit, where we are looking for further details on the tentative deal that seemed to have been reached between UK and EU earlier this week.

Selected market news

As we expected, the Fed delivered a "dovish hike" by maintaining the rate hike signal at two additional hikes this year (although it was close to being revised up to one more hike, supporting the view that risk is probably skewed towards a total of four hikes this year) while raising the 2019 median dot from slightly more than two hikes to three hikes (for more details see our FOMC review: Only slightly steeper rate path due to Trumponomics ). As markets had speculated about the signal being revised up for this year, we have seen the EUR/USD moved higher and US Treasury yields moved lower after the meeting. Asian equities are more mixed as the boost from the 'dovish' Fed hike is mitigated by concerns about new US trade actions

This concern comes after the media yesterday reported that Trump might already announce new tariffs targeted China today (was not expected until tomorrow). The stories suggest Trump will impose tariffs on goods imported from China for a value of USD50bn but that the administration will try to limit the impact on US consumers. US Trade Representative Robert Lighthizer also threatened China with retaliation against any Chinese retaliation measures, especially on agricultural products. In the same interview, he said that the US trade deficit with the EU is a big problem. For our take on the threat of global trade war, see Symbolic protectionism with limited impact on growth and inflation but risks remain and 10 areas where China could retaliate vs US measures .

Why The Dollar Sank On The Fed

The market expected something more hawkish from the FOMC on Wednesday. Instead, the dot plot continued to show three hikes and the US dollar stumbled. In early Asia-Pacific trading, the RBNZ left rates unchanged. A new Premium GBP trade was issued. Here is a tweet posted 7 hours before the Fed decision.

A Fed hike was entirely priced in on Wednesday so the market was more focused on signals about what is coming later in the year, particularly the debate about three or four rate hikes. Many thought the dot plot would move higher to indicate four hikes this year but it remained at three and the instant reaction in the US dollar was to slide. In case you missed Ashraf's Fed preview explaining why predicted the Fed will still stick with signalling 3 hikes, here is the video and here is the article.

Initially that was balanced out by a fresh line the statement that said economic growth has strengthened in recent months. Later, in the press conference, Powell chose not to highlight better growth prospects and instead noted the slow pace of wage gains. That might have been a reflection of the questions he was asked but the hawks were still left with little to get excited about.

In addition, the market was leaning towards something hawkish in the lead-up to the announcement. As seen by the rise in Treasury yields and the dollar beforehand. Much of that reversed in the hours after the statement.

In particular, GBP limbed above the mid-February high in a strong move ahead of Thursday's BOE rate decision and UK retail sales report. If Carney delivers a hint about a rate hike in May, a return to the February highs is likely. A recurring message about GBP Ashraf has been sending over the past 9 months to subscribers is that the Bank of England is more eager to contain inflation via talking up the pound than via actual rate hikes. Alluding to a potential May stands among the ways to jawbone the currency without actually pulling the rate trigger.

Another big move Wednesday came in the Canadian dollar as officials in Canada and the US highlighted progress on NAFTA talks. USD/CAD dropped more than 150 pips on the day. Tradewise, the Premium short in USDCAD survived the 1.3120 stop before re-entering the green, while the CADJPY short was closed for 200-pip gain at the right shoulder.

The New Zealand dollar emerged from the RBNZ decision relatively unscathed. There was no move on rates as was expected with Grant Spencer's interim term as Governor wrapping up next week. Some m odest NZD selling came on a line in the statement saying that CPI inflation will weaken further in the near term but that was balanced by the absence of anti-NZD jawboning.

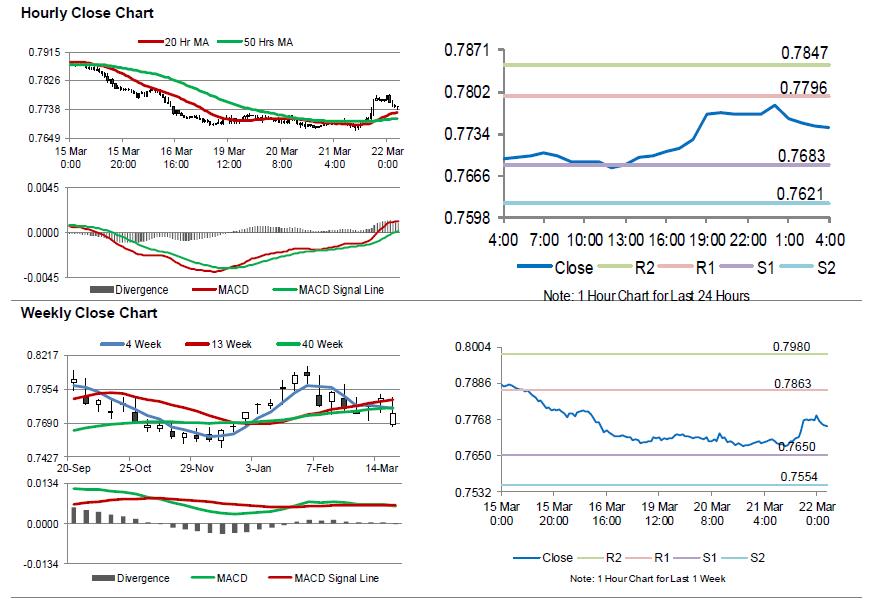

Australia’s Unemployment Rate Unexpectedly Climbed In February

For the 24 hours to 23:00 GMT, the AUD rose 0.98% against the USD and closed at 0.7766.

LME Copper prices declined 2.4% or $163.0/MT to $6675.0/MT. Aluminium prices declined 5.1% or $111.5/MT to $2056.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7745, with the AUD trading 0.27% lower against the USD from yesterday's close, after Australia's seasonally adjusted unemployment rate recorded an unexpected rise to 5.6% in February, confounding market expectations for a steady reading. In the previous month, unemployment rate had recorded a reading of 5.5%.

The pair is expected to find support at 0.7683, and a fall through could take it to the next support level of 0.7621. The pair is expected to find its first resistance at 0.7796, and a rise through could take it to the next resistance level of 0.7847.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.