Sample Category Title

France PMI indicates softening in private sector growth again

France PMI manufacturing dropped to sharply to 53.6 in March, down from 55.9 and missed expectation of 55.6.

France PMI services dropped to 56.8, down from 57.4 and missed expectation of 57.0.

Markit titled the release as "Private sector growth softens again, but remains marked".

Quote from the release by Alex Gill, Economist at IHS Markit:

"Growth slowed in the French private sector economy during March, with the headline composite output figure down for the second successive month. At 56.2, however, the rate of expansion remained elevated by historical levels, while the Q1 average of 57.7 is consistent with a robust GDP number.

"Strong client demand in both domestic and foreign markets continues to support output and employment. Meanwhile, a further robust degree of business confidence combined with a sharp and accelerated accumulation of outstanding business suggests further growth in the coming months."

XAUUSD Intraday Analysis

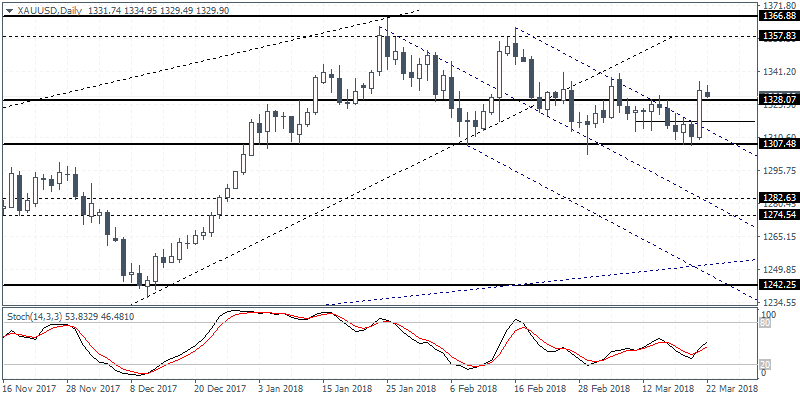

XAUUSD (1329.90): Gold prices broke out to the upside with price closing above the 1328 handle. The near term declines could be seen supported with a retest of 1328 level. As long as this level holds, gold prices could be seen pushing higher, potentially targeting the 1357 level as the next upside target. To the downside, in the event that 1328 fails to hold as support, we expect gold prices to settle back into the range trading within the 1328 and 1307 levels in the near term.

GBPUSD Intraday Analysis

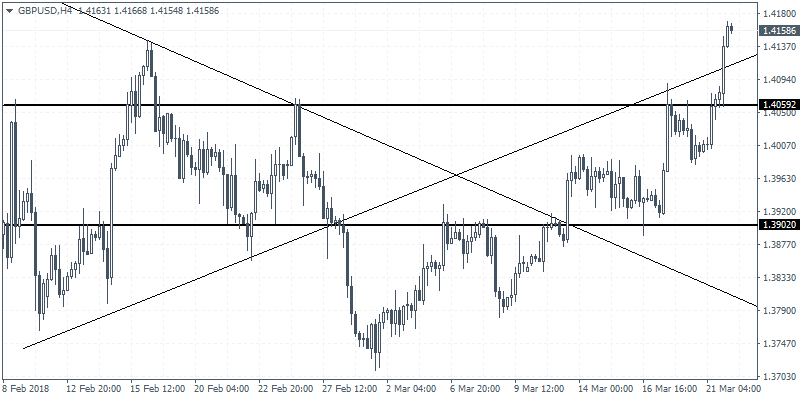

GBPUSD (1.4158): The British pound posted strong gains with early trading today sending the currency pair to a fresh two month high at 1.4170. The gains came amid a better than expected jobs report which saw wages finally catching up as inflation cooled. The GBPUSD breached the trend line which served as resistance and could be seen pushing higher ahead of the Bank of England meeting. The BoE is expected to give a hawkish forward guidance a today's meeting with the markets now pricing in the next BoE rate hike in the month of May. A near term dips could be seen supported by the trend line which could now act as support.

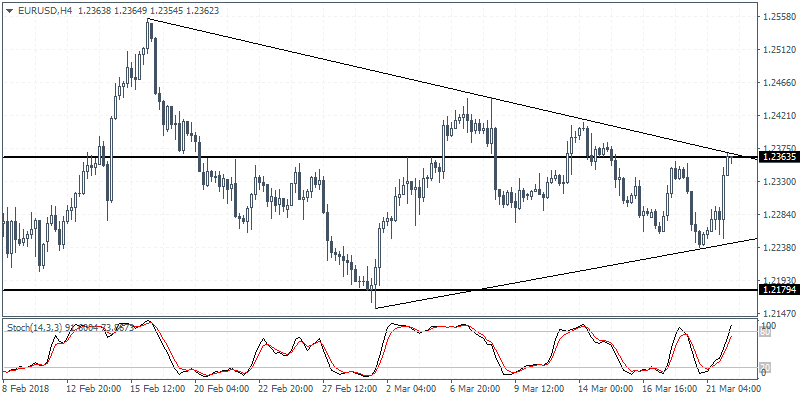

EURUSD Intraday Analysis

EURUSD (1.2362): The euro currency reversed the declines as price was seen pushing higher on the day. The euro gained 0.77% on the day but price action was confined to Wednesday's range. The bounce in the common currency sent the euro to trade back at the 1.2363 level of resistance which also coincides with a medium term trend line. A reversal at this level is quite likely but overall, the EURUSD is expected to maintain a sideways range within the 1.2363 and 1.2180 levels of resistance and support.

Powell Starts With Modest Hawkish Shift

- Fed hikes policy rate by 25 bps to 1.5%-1.75%

- Economic outlook has strengthened, despite setback in Q1 2018

- More confidence in hitting dual mandate

- Median FOMC rate projection rose in 2019, 2020 and long run

- Muted market reaction; odds of 4 rate hikes this year increased

The Fed hiked its policy rate as widely anticipated by 25 bps from 1.25%‐1.50% to 1.50%‐1.75% at Jerome Powell’s inaugural meeting as Fed governor. In its statement, the Fed admitted that growth moderated at the start of the year coming from a very strong Q4 2017. Looking forward though, the FOMC says that the economic outlook has strengthened. The US economy benefits from accelerating global growth and domestic fiscal policy changed from head wind into tail wind. This economic optimism translates in upward revisions to GDP forecasts for this year (2.7% from 2.5%) and next year (2.4% from 2.1%). The 2020 GDP projection remains unchanged at 2%.

The FOMC upgraded its assessment of the labour market. Job gains have been strong in recent months and the unemployment rate has stayed low. New forecasts indicate that the central bank thinks there is room for a further decline in the unemployment rate to 3.8% in 2018 (from 3.9%), and 3.6% in both 2019 & 2020 (from 3.9% and 4% respectively). The FOMC lowered its forecast for the NAIRU from 4.6% to 4.5%.

The appraisal of the US central bank’s other policy goal, price stability, remained broadly unchanged. In January, the FOMC expected inflation to move up “this year” and to stabilize around the Committee’s 2% objective in the medium term. The wording in the statement slightly changed to move up “in coming months” before stabilizing. PCE inflation forecasts remained unchanged in 2018 (1.9%) and 2019 (2%). The FOMC increased the 2020 forecast from 2% to 2.1%.

Upward shift dot plot, close call in 2018

The more upbeat economic assessment and increased confidence in hitting its dual mandate of maximum employment and price stability triggered changes in the FOMC’s dot plot which is used as a benchmark for the US central banks’ expected rate path. The new median forecast suggests 2 more rate hikes this year (to 2%‐2.25%), 3 hikes in 2019 (to2.75%‐3%) and 2 hikes in 2020 (to 3.25%‐3.5%). This scenario includes 1 additional hike in 2019 and 2020 compared with the December 2017 dots.

However, there’s more to the picture than meets the eye. The median forecast for this year remained unchanged, but the average projection increased by 0.17%! Six out of 15 governors expect 2 more hikes this year (only 2 more dovish dots), whereas six others pencil in 3 more hikes. Three months ago, this balance was still clearly tilted to the “cautious” side with a 6‐3 split (out of 16; with 6 more dovish dots). More specifically, it now takes only one Fed governor to change his mind in order to trigger an increase in the median forecast for this year. This probably helps explain why the market implied probability of 3 more rate hikes this year hardly changed compared to before the FOMC meeting (37% from 38%). The market attaches an 80% probability to a new 25 bps rate hike in June, also unchanged from before the meeting.

Finally, we take note of the increase in the Fed’s median forecast for the long term neutral, equilibrium rate, from 2.75% to 2.875%. Fed governor Powell at the press conference suggested that Fed participants believed that higher investment and productivity could be among the benefits from the new fiscal policy. This reasoning suggests that a further increase in the median forecast for the neutral rate is possible at one of the next FOMC meetings, especially as the situation is comparable with the 2018 dots. Only one governor needs to increase his projection to 3% to lift the median as well. That would be a break with history as the estimation of the neutral rate was almost consistently downgraded from 4.25% in March 2012 to 2.75% at the final two meetings of 2017. A higher neutral rate could flag a new sell‐off at the long end of the US yield curve in the MT

New Fed dot plot (green) and Fed Funds future curve (blue): increase of 2019, 2020 and LT median projections

Overall, we conclude that the Fed’s statement and dot plot turned more hawkish compared to December 2017. The unchanged forecast for this year and (limited) increase in the neutral rate, even if they were close calls, suggest that some FOMC members want more economic evidence that the central bank will reach its dual mandate. We keep our forecast for 4 rate hikes this year unchanged. Marvin Goodfriend will probably attend the June policy meeting, filling one of the vacant Washington‐based governors’ seat. His vote can already be enough to tilt the balance.

A final takeaway from Powell’s first press conference is that it seems that he will– more than his predecessors – actually try to be data dependent. Two months of good/bad eco data could have implications in both directions. Q2 eco data and the June policy meeting will show whether this hunch proved to be right or wrong

Dollar and yields correct slightly lower

Yesterday’s muted market reaction suggests that investors keep such scenario in the back of their heads. The US yield curve bull steepened with yields 4 bps (2‐yr) to 1.1 bp (30‐ yr) lower. The correction at the front end shouldn’t surprise given the huge front running we’ve witnessed this year. Additionally, some expected a 50 bps rate hike. The loss of interest rate support weighed on the dollar with EUR/USD rising from 1.2260 to 1.2340. The trade‐weighted dollar fell from 90.20 to 89.70. US stock markets trade volatile, but could live with the fact that the worst possible outcome (very hawkish Fed) was avoided. Main indices closed around 0.2% lower on a daily basis

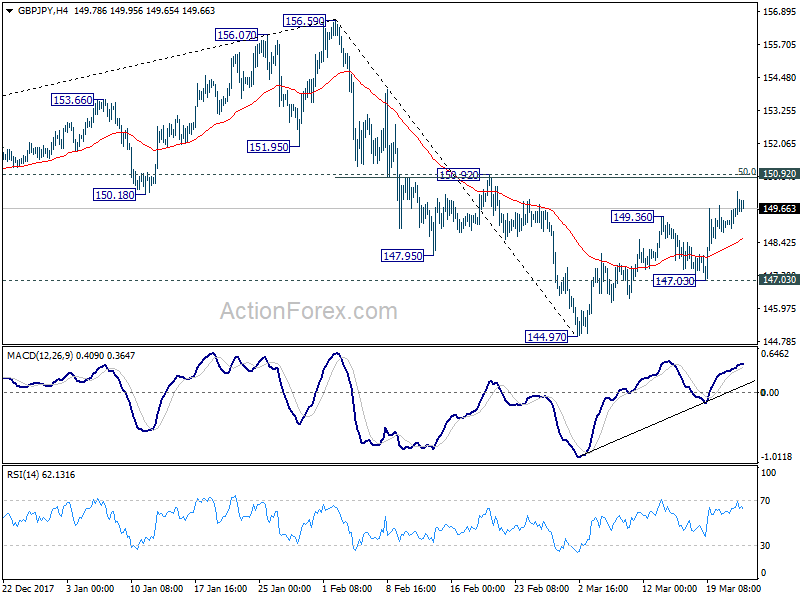

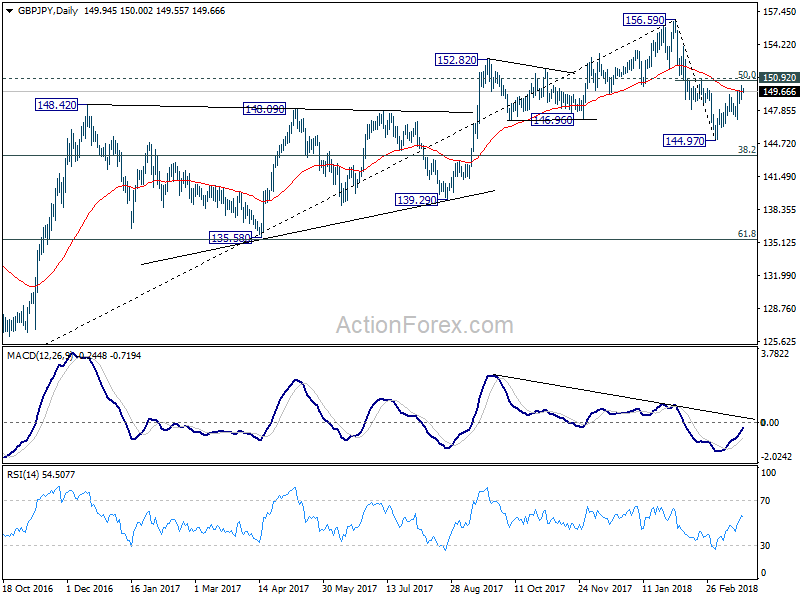

GBP/JPY Daily Outlook

Daily Pivots: (S1) 148.53; (P) 149.15; (R1) 149.75; More....

GBP/JPY's recovery from 144.97 is still in progress and further rise could be seen. But again, such rise is viewed as a corrective move. And hence, strong resistance is expected from 150.92 (50% retracement of 156.59 to 144.97 at 150.78) to bring fall resumption. On the downside, below 147.03 will bring retest of 144.97 low first. Break will extend the decline from 156.59 to 143.51 medium term fibonacci level next. However, sustained break of 150.92 will pave the way back to retest 156.69 high.

In the bigger picture, the case for medium term reversal continues to build up. There is bearish divergence condition in daily MACD. 146.96 support was taken out. And GBP/JPY was rejected by 55 month EMA. Break of 38.2% retracement of 122.36 to 156.59 at 143.51 will pave the way to 61.8% retracement at 135.43 and below. This will now be the preferred case as long as 150.92 resistance holds.

USD Falls On Fed Rate Hike, BoE Meeting Up Next!

It was a busy day for the markets with key events lined up that included the UK jobs data, the U.S. Federal Reserve meeting and the RBNZ monetary policy meeting.

Data from the UK showed that the unemployment rate fell to 4.3% on the month beating estimates of an unchanged print of 4.4%. Wage growth surprised to the upside rising 2.8% on the month which beat estimates of 2.6% and accelerating from a revised 2.7% seen previously.

The Federal Reserve hiked the 30-day Fed funds rate to 1.75% as widely expected by the markets. The Fed stuck to its baseline scenario of three rate hikes this year while upgrading its economic assessment. However, the hawkish statement was offset by a dovish press conference chaired by the new Fed Governor Jerome Powell.

The U.S. dollar fell sharply on the day with the biggest gains coming from commodities such as WTI crude oil and gold.

The RBNZ's meeting was clearly overshadowed by the FOMC meeting. The RBNZ held the overnight cash rate unchanged at 1.75%. The monetary policy statement did not deviate from the previous monetary policy meeting which saw the NZD playing more to the Fed's narrative than the RBNZ.

Looking ahead, focus turns to the UK as the Bank of England will be holding its monetary policy meeting today. Based on the recent dip in inflation and a pickup in wage growth, expectations ride high for the next BoE rate hike in May. With the recent tides of uncertainty from Brexit abating due to the transitory deal, the Bank of England is expected to push forward with the next rate hike.

The UK retail sales report will be coming up ahead of the BoE meeting. Economists forecast that retail sales increased 0.4% on the month, accelerating from 0.1% previously.

In the Eurozone, flash manufacturing and services PMI data for March will be released.

BOE To Leave Rates Unchanged But Watch For Signal Of May Hike

The Bank of England is expected to leave rates unchanged today at 0.5% but will potentially lay the groundwork for a hike of rates in May. Market analysts will look to the Monetary Policy Summary for guidance indicating any hawkish tone on the back of Brexit progress and a pickup in economic data this week. The MPC vote will also be key, as any indication that members vote to hike rates will be seen as rubberstamping a May hike, which the market is fully pricing in. Failure to do so will disappoint traders and may lead to a reversal in prices if market expectations go unmet.

President Trump is expected to announce Trade Tariffs on Chinese goods and services to the value of $50 Billion later today. China has said it resolutely opposes US unilateralism and protectionism. It said it will take all necessary measures to resolutely protect its interests.

UK Average Earnings excluding Bonus (3Mo/Yr) (Jan) was as expected at 2.6%, from 2.5% previously. Claimant Count Change (Feb) was 9.2K v an expected -5.0K, from a previous reading of -7.2K, which was revised up to -1.6K. ILO Unemployment Rate (3M) (Jan) was 4.3% v an expected 4.4%, versus 4.4% previously. Average Earnings including Bonus (3Mo/Yr) (Jan) was 2.8% v an expected 2.6%, from 2.5% previously which, was revised up to 2.7%. Claimant Count Rate (Feb) was 2.4% against 2.3% previously. Public Sector Net Borrowing (Feb) was £-0.272B v an expected £0.00B, from £-11.62B prior, which was revised down to £-11.719B. Wage growth ticked up after stabilizing at 2.5% for the past three months. The Unemployment rate fell, showing more people at work and putting further pressure on wages, which have not declined for nine straight months now. The BOE will study wage data to see any indication of a pickup, indicating they need to maintain their hawkish tone. GBPUSD spiked higher from 1.40218 to 1.40749 and EURGBP sold off from 0.87515 to 0.87227 after this data release.

US Existing Home Sales (MoM) (Feb) came in at 5.54M v an expected 5.40M, against 5.38M previously. After reaching a seven-year high in November, this data point has slipped lower over the last two months, signalling a little softness in the sector. But this could be down to seasonal factors and this current beat on the consensus is already showing a pickup, which usually lasts into autumn. USDCAD moved higher from 1.29704 to 1.29916 after this data came out.

The US Fed’s Monetary Policy Statement and Interest Rate Decision were released and rates were raised to 1.75% from 1.5%. This hike in rates had been more or less priced into markets and marks the first in a series of expected increases in 2018. Inflation on a 12-month basis is expected to move up in the coming months. Jobs growth has been strong and the vote to increase was unanimous. The dot plots showed that the Fed is likely to hike three times in 2018 and three times in 2019, against the market consensus, which expected three, maybe four, in 2018 and two in 2019. USDJPY spiked up and down but eventually went higher to 106.635.

The FOMC Press Conference took place, as the new Chairman, Jerome Powell, addressed the audience. He said: Job growth has been ‘well above’ pace needed to sustain labour force and he expects the job market to remain strong. Raising rates too slowly would raise the risk of having to tighten too quickly later. FOMC members noted they heard concerns about future trade action and the effect on the future outlook. We will know that the labour market is getting tight when we see more wage inflation. Low productivity explains some of the weakness in wages. USDJPY reversed the earlier move after the rate hike and fell to a low of 105.574 in the following hours. Stocks faded the early spike higher, with the S&P 500 down to 2711.60 and the Dow down to 24679.5 from a high of 24986.0. Gold moved up to 1336.80.

The Reserve Bank of New Zealand Interest Rate Decision left rates unchanged at 1.75%. The Rate statement and the Monetary Policy Statement said monetary policy will remain accommodative for a considerable period. The domestic economy is projected to strengthen and long-term inflation expectations are well anchored around 2%. GDP was weaker than expected in Q4 and labour market conditions continue to tighten. CPI inflation is expected to weaken further near-term due to softness in food and energy prices. NZDUSD moved higher from 0.72240 to 0.72447 after this event.

EURUSD is up 0.11% overnight, trading around 1.23511.

USDJPY is down -0.16% in early session trading at around 105.881.

GBPUSD is up 0.04% this morning, trading around 1.41462.

USDCAD is down -0.02% in early trade at around 1.29001.

Gold is down -0.16% in early morning trading at around $1,330.00.

WTI is down -0.58% this morning, trading around $65.11.

Will BoE Lay The Foundations For May Rate Hike?

Brexit, trade wars, slow economic growth and heightened tensions with Russia, not exactly the ideal environment for a central bank to consider raising interest rates. Yet, that's exactly what the Bank of England is doing and on Thursday, they may signal and intention to do just that at the next meeting in May.

It is worth pointing out firstly that this is only half the story. The country is also experiencing high inflation, a 43-year low in unemployment and rising wages against a backdrop of strong global growth. The central bank is not exactly in an enviable position.

To make matters more confusing, inflation has fallen from its highs and was lower than expected in February, with the core number only 0.4% above target. Wage growth is improving but from a low base and remains moderate. And finally Brexit talks are progressing, with the transition deal at the start of the week another major hurdle that's been overcome. It's no wonder people can't agree on the correct course of action.

That said, one thing that has appeared clear is that the BoE wants to raise interest rates, and soon. The language from policy makers is becoming increasingly hawkish and last month it claimed that tightening (rate hikes) would have to come "somewhat earlier and by a somewhat greater extent" that it expected in November.

It's because of this that market expectations of a rate hike in May – when the next inflation report is released – are so high. Clearly the central bank is trying to provide clear guidance that interest rates will rise in the near future and May would represent a logical time to do so.

Investors are even looking past small changes in the data that may ordinarily make the BoE question their decision to hike rates – inflation falling more than expected – because the central bank will want to avoid credibility questions arising again if it changes its mind.

Taking all of the above into consideration, it's logical then that the Monetary Policy Committee will make clear in Thursday's minutes its intention to raise interest rates in May, which is what traders will be looking for. Any indication that it may be having doubts could hit the pound, given how priced in a May rate hike now is.

The interesting thing with the charts is that, with all the good Brexit transition news now priced in – subject to sign off by EU leaders later in the week – and a rate hike also priced in, I wonder how much more upside the pound will see and whether we may instead see profit taking shortly after the release. The pound has certainly rallied strongly recently in anticipation of it all, particularly against the euro but I wonder what it has left in the tank.

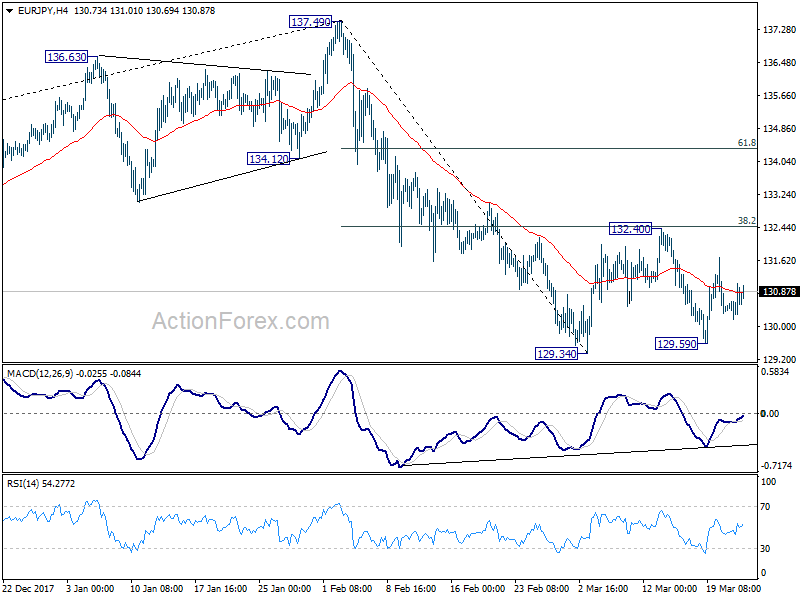

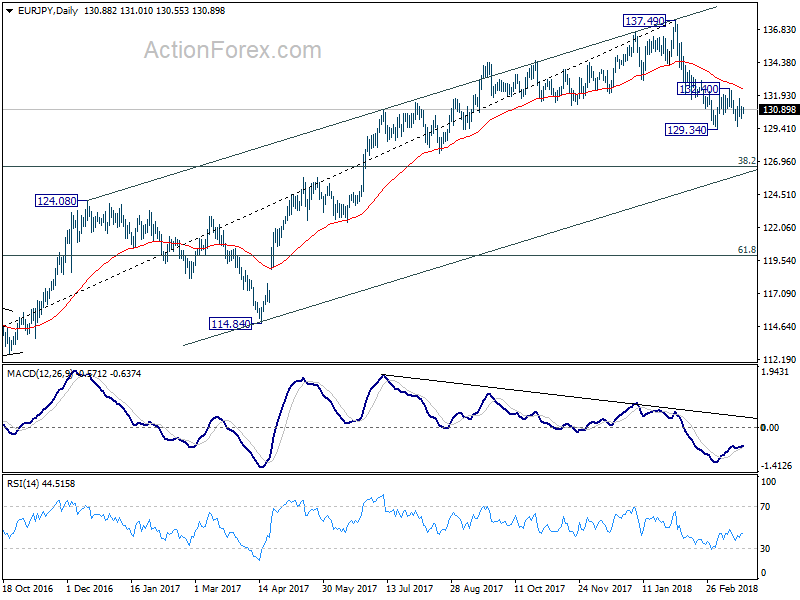

EUR/JPY Daily Outlook

Daily Pivots: (S1) 130.33; (P) 130.69; (R1) 131.20; More....

EUR/JPY continues to gyrate in range of 129.34/132.40 and intraday bias remains neutral first. Overall, we'd expect upside of the consolidation to be limited by 38.2% retracement of 137.49 to 129.34 at 132.45 to bring fall resumption eventually. On the downside, decisive break of 129.34 will confirm resumption of whole fall 137.49 and target 126.61 medium term fibonacci level. However, firm break of 132.45 will target 61.8% retracement at 134.37 instead.

In the bigger picture, current development argues that rise from 109.03 (2016 low) has completed at 137.49, on bearish divergence condition in weekly MACD. Deeper fall should be seen to 38.2% retracement of 109.03 to 137.49 at 126.61 first. On the upside, break of 137.49 is needed to confirm medium term rise resumption. Otherwise, risk will now stay on the downside even in case of strong rebound.