Sample Category Title

GBP/USD Continued Rise

GBP/USD continues its rise, breaking hourly resistance at 1.4151 (05/02/2018) and heading along the 1.42 range. The short-term bullish pattern is maintained. Hourly support and resistance remain at 1.3765 (09/02/2018 low) and 1.4345 (25/01/2018 high). The technical structure suggests continued short-term increase.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is moving to 2016 highs. Long-term support and resistance are given at 1.1841 (07/10/2017 low) and 1.5018 (24/06/2016 high).

EUR/USD Increasing

EUR/USD is bouncing back following slight decline at 1.2342. Expected to increase along the 1.2380 range. Hourly support and resistance are given at 1.2165 (17/01/2018 low) and 1.2537 (31/01/2018 high). The technical structure suggests continued short-term upward moves.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2886 (15/10/2014 high) while strong support lies at 1.1554 (08/11/2017 low).

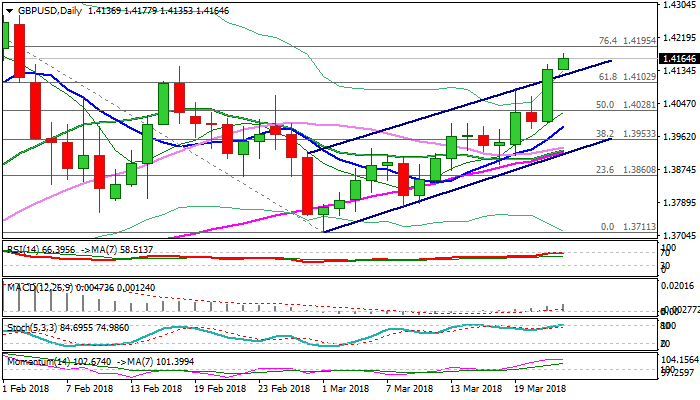

Technical Outlook: GBPUSD – Post-Fed Acceleration Broke Above Bull-Channel, BoE MPC Decision Eyed For Fresh Signals

Sterling continues to advance, supported by positive news about Brexit negotiations and additionally boosted by less hawkish than expected Fed, which sent the greenback lower.

Wednesday's rally generated bullish signal on close above important barriers at 1.4102 (Fibo 61.8% of 1.1345/1.3711 descend) and bull-trendline at 1.4122 (the upper boundary of bull-channel from 1.3711.

Positive sentiment is additionally supported by bullish daily techs, keeping strong bullish bias.

Extension above 1.42 barrier (near Fibo 76.4%) would open way towards double top at 1.4277 (01/02 Mar) and bring in focus key short-term barrier at 1.4345 (the highest traded since Brexit vote in June 2016).

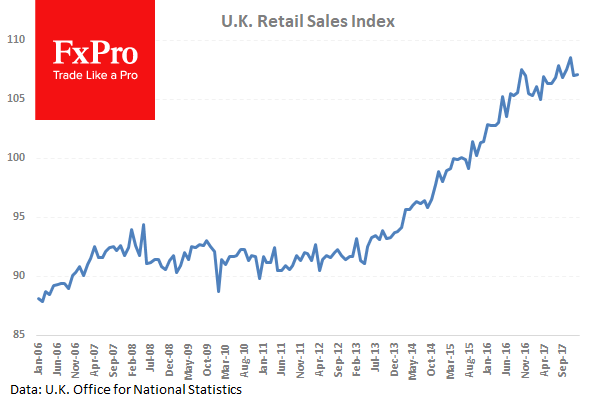

Two key events for sterling are in focus today. UK retail sales are forecasted higher in Feb, with BoE MPC rate decision and minutes following.

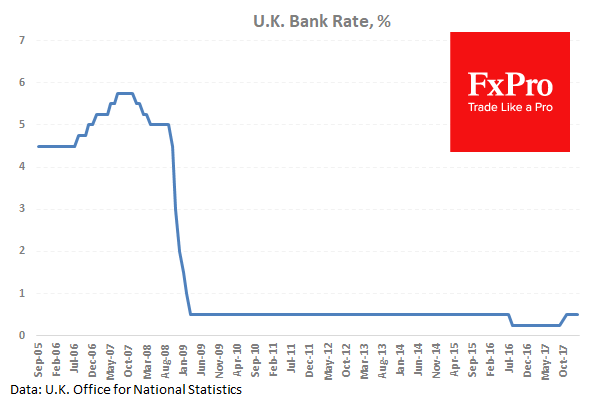

The UK central bank is expected to keep rates unchanged at 0.50% on today's meeting but voting results will be closely watched and hawkish outcome would further boost expectations for May rate hike and send pound higher.

Res: 1.4177, 1.4195, 1.4277, 1.4300

Sup: 1.4134, 1.4102, 1.4070, 1.4028

Dollar Dips On Dot-Plot Disappointment, BoE In Focus

The Federal Reserve has lifted interest rates to their highest level since the financial crisis, but Dollar bulls are clearly unamused.

Although on Wednesday, as widely expected, US interest rates were raised by 0.25% to a new band of 1.5%-1.75%, investors were more concerned with the dot-plot and Powell’s press conference. While the policy statement was generally positive and US economic growth was revised higher for 2018 and 2019, a crucial ingredient for hawks was missing. There is a suspicion that the Fed heavily disappointed markets by leaving the dot-plot unchanged for 2018 at a grand total of three hikes. Although there was a small upgrade to the dot-plot forecast for 2019 and 2020, this did little to support King Dollar. Jerome Powell’s noticeable caution during his conference and statement on how there was no clear indication in data of an accelerating inflation, encouraged investors to attack the Dollar further.

Taking a look at the technical picture, the Dollar Index was vulnerable to heavy losses after the Federal Reserve turned out to be less hawkish than anticipated. The breakdown below 90.00 could invite a decline towards 89.50 and 89.00, respectively.

Sterling higher ahead of BoE

The main event risk for Sterling today will be the Bank of England monetary policy decision, which is widely expected to conclude with interest rates left unchanged at 0.5%.

Investors will direct their attention towards the language of the statement for any fresh insights about potential timings of a change in UK interest rates this year. A sense of optimism over the Brexit transition deal, coupled with the fact that wage growth accelerated at the fastest pace in over two years, has boosted speculation of a rate hike in May. Sterling could receive a further boost if BoE policymakers mirror these expectations by adopting a hawkish stance and signalling a rate hike in May.

Focusing on the technical perspective, the GBPUSD extended gains on Thursday with prices hitting a fresh one-month high at 1.4170 as of writing. The combination of Dollar weakness following Wednesday’s dot-plot disappointment and Sterling strength has brought GBPUSD bulls back into the game. A breach above 1.4180 could encourage an appreciation towards 1.4260 and 1.4300.

Commodity spotlight – Gold

It’s remarkable how Gold prices soared on Wednesday despite the Federal Reserve raising interest rates. The reason behind Gold’s incredible rebound could be linked to the fact the Federal Reserve was less hawkish than anticipated, which simply weakened the Dollar. With the Dollar tumbling after the US Federal Reserve disappointed investors, Gold found itself back in fashion. The yellow metal could build on the current upside momentum, if political uncertainty in Washington and lingering trade war fears support the flight to safety. From a technical standpoint, Gold has broken above the $1330 resistance level. Previous resistance at $1330 could transform into a dynamic support that encourages an incline higher towards $1340. Alternatively, a failure for bulls to keep above $1330 could invite a decline back towards $1314.

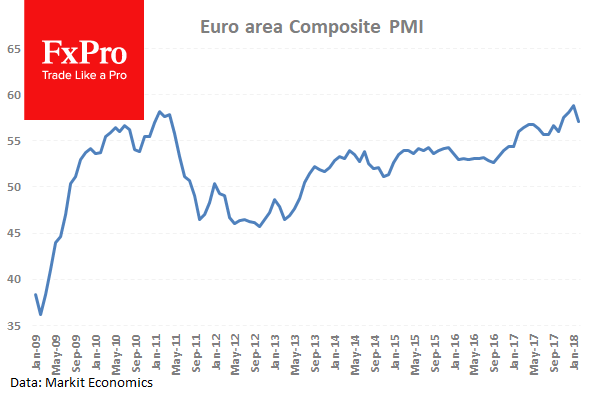

Eurozone PMI composite at 55.3, 14-month low; Growth peaked around the turn of the year

Eurozone PMI manfucturing dropped to 56.6 in March , down from 58.6, below expectation of 58.1. That's lowest in 8 months.

Eurozone PMI services dropped to 55.0, down from 56.2, below expectation of 56.0. That'st lowest in 5 months.

Eurozone PMI composite dropped to 55.3 down from 57.1, loweset in 14 month.

Here is ther release Eurozone expansion slows to weakest since start of 2017

Quote from Makit Chief Business Economist Chris Williamson:

"While the first quarter average PMI reading remains relatively robust, indicative of GDP rising by 0.7-0.8%, the loss of momentum since the buoyant start to the year has been quite dramatic.

"At least some of the slowing may be ascribed to bad weather in some northern regions and, perhaps more importantly, 'growing pains' resulting from the strength of the recent growth spurt. Supply chain delays and raw material shortages were often reported to have stymied production in manufacturing (delays in German supply chains are currently more widespread than at any time in the survey's 22-year history), and both manufacturing and services sectors also saw activity being curtailed by growing incidences of skill shortages. Backlogs of work continue to rise as a result of these growth constraints.

"However, other factors are clearly at play. The fact that export order book growth has more than halved since the end of last year suggests the stronger euro is taking an increasing toll on export performance. Survey responses also highlighted how political uncertainty also appears to have intensified, dampening demand.

"The data therefore suggest that eurozone growth peaked around the turn of the year and the region is settling into a slower, but still robust pace of expansion. Price pressures have meanwhile also eased slightly, in part linked to cheaper imports arising from the euro's recent strength, but remain elevated."

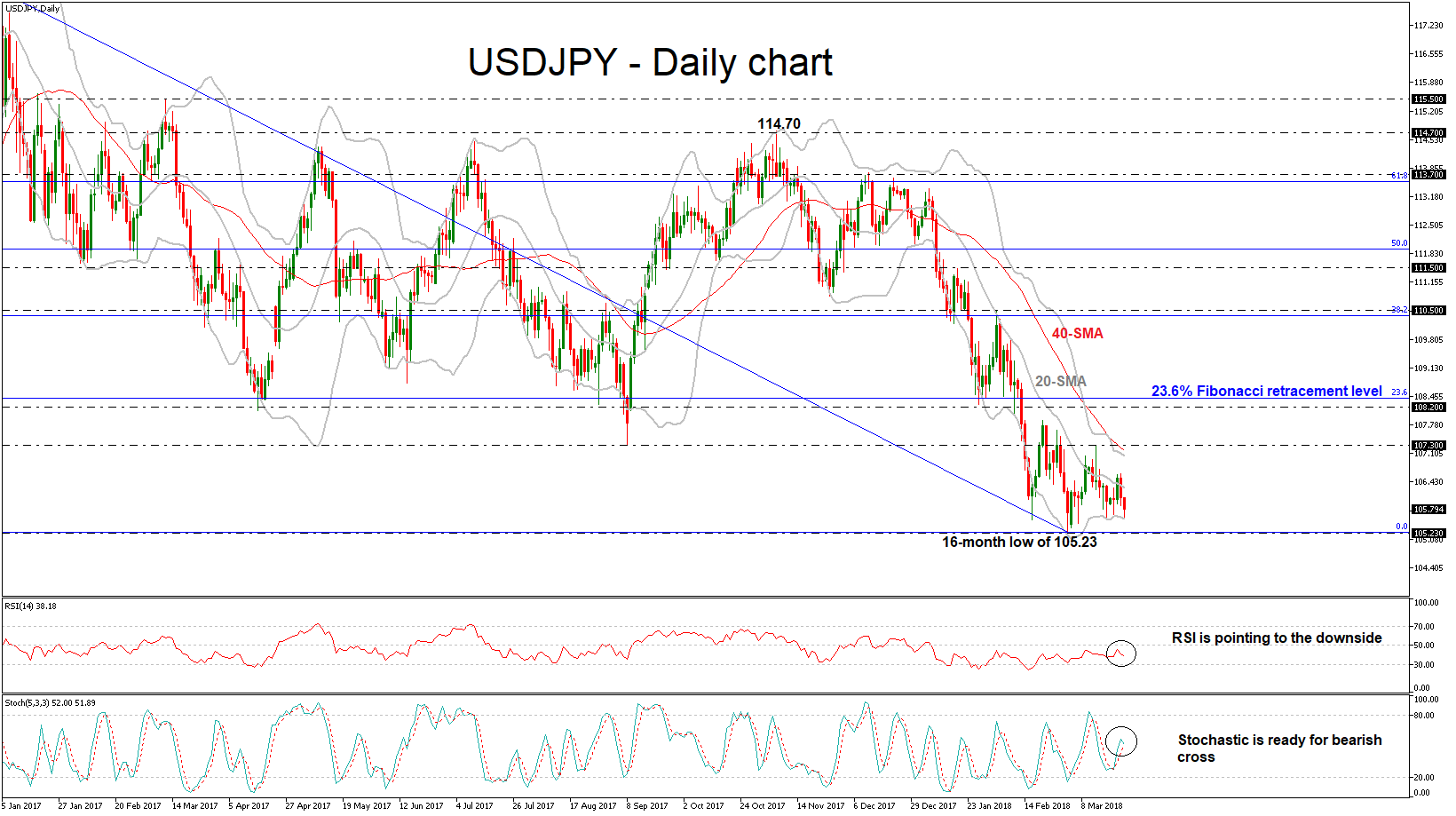

USDJPY Stands Around 2-Week Low, Bearish In Short- And Medium-Term

USDJPY fell as low as 105.57 during today’s Asian session and reached a two-week low. Over the last three weeks, the pair is posting neutral sessions as it failed several times to jump above the 107.30 key resistance level but managed to hold above the 16-month low of 105.23. Price action is at the moment taking place not far above this low.

From the technical point of view, in the daily timeframe, the price hit the lower Bollinger band and rebounded on it, while it is trading below the 20-day simple moving average (SMA). The RSI indicator is sloping to the downside approaching the threshold of 30. Also, the stochastic oscillator is ready to create a bearish cross with the %K and %D lines.

For the time being, 106.00 holds as resistance for USD/JPY, but a move below the aforementioned 16-month low could open the way towards the next significant handle of 101.00 taken from the low of November 2016.

On the flip side, should an upside reversal take form, the next pause could be on the 40-day simple moving average near 107.20, which moves near the upper Bollinger Band before it touches the 107.30 barrier. A break above this area could shift the short-term outlook to a bullish one with the next resistance coming from the 23.6% Fibonacci retracement level at 108.40 of the downleg from 118.60 to 105.23.

German PMI, BOE Rate Decision And US Jobless Claims

At 08:30 GMT, German Markit Manufacturing PMI (Mar) is expected to come in at 59.8 from 60.6 previously. Markit Services PMI (Mar) is expected at 55.0 v 55.3 previously. Markit PMI Composite (Mar) is expected to be 57.0 from 57.6 prior. The expectation is for a slip in these data points, suggesting that the December reading was a short-term high. For Manufacturing, it was the highest since before the financial crisis and for Services, it was the highest since June 2011. EUR traders will be closely following this data release.

At 09:00 GMT, Eurozone Markit Manufacturing PMI (Mar) is expected to come in at 58.1 from 58.6 previously. Markit Services PMI (Mar) is expected at 56.0 v 56.2 previously. Markit PMI Composite (Mar) is expected to be 56.7 from 57.1 prior. This data is also expected to soften from highs in December. EUR crosses may see a spike in volatility should the actual released data differ from the expected consensus.

At 09:30 GMT, UK Retail Sales (YoY) (Feb) is expected to be 1.3% from 1.6% previously. Retail Sales (MoM) (Feb) is expected at 0.4% against a prior 0.1%. Retail Sales Ex-Fuel (YoY) (Feb) is expected to be 1.2% from 1.5% previously. Retail Sales Ex-Fuel (MoM) (Feb) is expected at 0.4% against a prior 0.1%. This data series will be the last available to the BOE before they decide on monetary policy ahead of their 12:00 GMT announcements. It is a volatile data set but it does give a view on consumer spending. GBP crosses may experience an increase in volatility following this data release.

At 12:00 GMT, the Bank of England Interest Rate Decision is expected to be left unchanged at 0.5%. The BOE Minutes, BOE Quarterly Inflation Report and the Monetary Policy Statement will also be released at the same time. BOE Asset Purchase Facility is expected to come in unchanged at £435B. While no change in rate is expected, the tone and language used will be examined for hints that the Bank is gearing up to increase rates in future. GBP crosses may see a spike in volatility after this data is released.

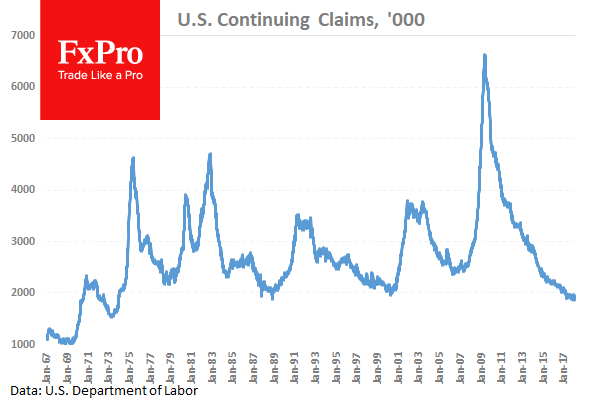

At 12:30 GMT, US Initial Jobless Claims (Mar 16) is expected to be 225K from 226K previously. Continuing Jobless Claims (Mar 9) is expected to be 1.890M from 1.879M previously. Jobless Claims data has been in a downtrend since the high after the financial crisis. It is expected to fall further today, as job creation is sustained and more individuals resume work. Continuing Jobless claims is expected to tick up a little. USD crosses could be moved by this data.

At 13:00 GMT, US House Price Index (MoM) (Jan) is expected at 0.5% v 0.3% previously. This data is expected to tick up a little after falling over the last few months in what has become a seasonal move. Statistically, this reading is one of the worst for House prices in the US as it represents the January data. USD crosses may be heavily traded as a result of this data.

At 13:45 GMT, US Markit Manufacturing PMI (Mar) is expected to come in at 55.5 from 55.3 previously. Markit Services PMI (Mar) is expected at 55.8 v 55.9 previously. Markit PMI Composite (Mar) is expected to be 55.7 from 55.8 prior. Manufacturing is expected to maintain its strong improvement since a low in May 2016. Services data is expected to soften a little. USD crosses may be heavily traded as a result of this data.

At 17:00 GMT, the BOE’s Ramsden is due to deliver closing remarks at the International FinTech Conference, in London. Comments may cause moves in GBP pairs.

At 18:45 GMT, the BOC’s Wilkins is due to speak at the Rotman School of Management, in Toronto. Comments may cause moves in CAD crosses.

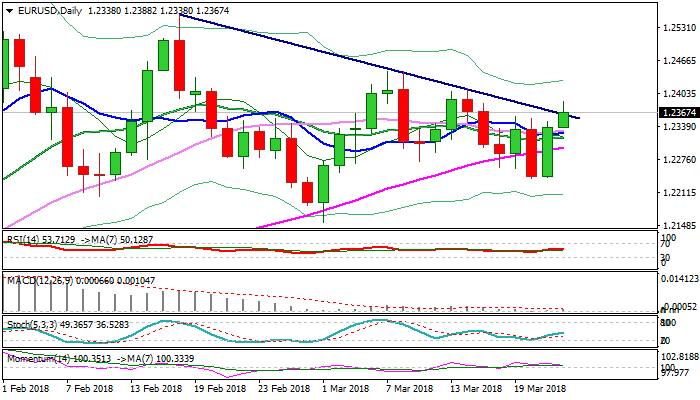

Technical Outlook: EURUSD – Extended Recovery Needs Clear Break Above Cracked Trendline Resistance

The Euro extends post-Fed rally on Thursday and hit one-week high at 1.2388 on probe above trendline resistance at 1.2356 (bear-trendline drawn off 16 Mar high at 1.2555).

The Fed disappointed markets on less hawkish than expected announcement after increasing interest rates by 0.25%, as widely expected. The US central bank forecasted two more rate hikes in 2018, remaining in line with forecast for total of three hikes this year and remained upbeat on economy outlook, though low inflation continues to be the main obstacle.

The dollar remains at the back foot across the boards after Fed and rising concerns about coming announcement about US tariffs.

Daily techs returned to full bullish mode on fresh acceleration which emerged above thickening daily cloud which underpins recovery.

Sustained break above cracked bear-trendline is needed to generate fresh bullish signal for extension of recovery leg from 1.2240 (20/21 Mar double top) towards highs at 1.2412 (14 Mar) and 1.2446 (08 Mar).

Broken 10 SMA offers support at 1.2327 which is expected to keep the downside protected and guard lower pivot at 1.2295 (daily cloud top).

Res: 1.2388,1.2412,1.2446,1.2495

Sup: 1.2355,1.2327,1.2295,1.2240

Germany PMI: Private sector pulled back sharply, but Q1 still robust

German PMI manufacturing dropped to 58.4 in March, down from 60.6, below expectaiton of 59.8. That's an 8-month low.

German PMI services dropped to 54.2 in March, down from 55.3 and missed expectation of 55.0. That's a 7-month low.

Here is the full release: Germany PMI drops to eight-month low in March.

Quote from Phil Smith, Principal Economist at IHS Markit:

"Growth in Germany's private sector has pulled back sharply since the start of the year, with the pace of expansion in March well below January's near seven-year high.

"However, with the strong expansions seen at the end of last year and in the opening months of 2018 already baked in, official numbers are expected to show robust GDP growth in the opening quarter. Latest IHS Markit forecasts show growth picking up from the somewhat disappointing 0.6% seen in the fourth quarter of 2017.

"Interestingly, the survey's anecdotal evidence also found an unusually high prevalence of staff sickness affecting business activity, to suggest that the extent of the slowdown in March might be partly due to temporary factors.

"It is manufacturing that has lost the most momentum, with growth in goods production slowing particularly sharply to its weakest since the start of 2017. The headline manufacturing PMI, however, is somewhat supported by the suppliers' delivery times component, which has hit a fresh record-low – its third in the past four months.

"Capacity pressures remain a theme, with firms noting not only bottlenecks in supply chains but also a solid and accelerated increase in backlogs of work. This bodes well for strong job creation continuing in the months ahead."

Currencies: Fed Not Hawkish Enough To Trigger Further USD Gains

Rates: Fed makes modest hawkish shift; markets slightly 'disappointed'

The US yield curve correctively bull steepened after yesterday's FOMC meeting. The hawkish shift by the Fed just failed to meet the market's hurdle. The median rate projections for 2019, 2020 and the neutral rate increased while the 2018 'dot' was unchanged, even if it was a close call.

Currencies: Fed not hawkish enough to trigger further USD gains

Of late, the dollar profited from a 'hawkish' market positioning ahead of the FOMC meeting. The Fed governors raised their dots, but not enough to trigger further USD gains. For now, the stalemate in EUR/USD trading persists. Today, the focus turns to (softer?) EMU confidence data and to president Trump's announcement of tariffs on Chinese imports

The Sunrise Headlines

- US stock markets traded volatile after the Fed's verdict and eventually closed around 0.2% lower. Asian risk sentiment is mixed.

- The Fed raised its policy rate by 25 bps to 1.50%-1.75% at Powell's inaugural meeting. The dot plot signalled more rate hikes ahead as the economic outlook strengthened and with more confidence in hitting its dual mandate.

- Congressional leaders reached an agreement on a spending bill that would fund the government until October, ending a protracted negotiation that left lawmakers little time to pass it before the current funding expires at week's end.

- The Reserve Bank of New Zealand flagged a temporary dip in price growth as it held interest rates at record lows, its last decision before an expected deviation from its trademark pure inflation target mandate.

- Australian employment data were mixed. Net employment change (+17.5k) was slightly below consensus, but full employment added a very strong 64.9k. The unemployment rate ticked up to 5.6%, but was matched by an increase in the participation rate to a 7-yr high (65.7%).

- President Trump will announce tariffs on Chinese imports today ($50bn), a White House official said, in a move aimed at curbing theft of US technology and likely to trigger retaliation from Beijing and stoke fears of a global trade war.

- Today's eco calendar contains German Ifo business confidence, EMU PMI's, UK retail sales and US weekly jobless claims. The Bank of England holds its policy meeting. The EU Summit on Brexit starts and the ECB publishes its bulletin.

Currencies: Fed Not Hawkish Enough To Trigger Further USD Gains

Fed not hawkish enough to support the dollar

The dollar traded in wait-and-see modus yesterday ahead of the Fed policy decision. EUR/USD hovered in the upper half of the 1.22 big figure. USD/JPY held well north of 106. The Fed as expected raised its policy rate by 25 basis points. The median Fed forecast for the 2019/20 rate path was upwardly revised and there was also upward drift in the 2018 forecast and the neutral rate. However, this change was just not hawkish enough to meet recent market anticipation. For an in depth analysis of the FOMC decision. Short-term yields and the dollar reversed part of the recent rise. EUR/USD jumped back north of 1.23 (close 1.2338). USD/JPY closed the day at 106.05.

Asian equities don't find a clear direction overnight. The PBOC raised a shortterm reverse repo rate by 5 bps. Regional markets look forward to the trade tariffs announcement of US president Trump. China and Korean markets slightly underperform the region. EUR/USD trades near 1.2350. USD/JPY is holding below the 106 mark. AUD/USD reversed a small part of the post-Fed rebound on mixed labour data.

German IFo business confidence and the March EMU PMI are published today. Recently, EU business confidence eased off record levels. This drift is expected to continue. The data still point to solid growth. Even so, another negative surprise might be slightly euro negative. Later, US president Trump is expected to announce tariffs on Chinese imports. Markets try to assess the potential retaliation. A risk-off reaction might weigh on USD/JPY. The impact on EUR/USD is less clear. Yesterday's Fed decision didn't break the stalemate in EUR/USD trading. For now, we assume that the downside of the dollar/topside in EUR/USD remains rather well protected, but there is no trigger for a substantial USD up-leg. For that to happen, good US data are needed. The 1.2155-1.2446 trading range remains in place. We slightly favour a sell-on upticks bias. UK retail sales will be published today and the BoE announces its policy decision. A modest rebound after two months of soft sales is expected. The BoE is expected to keep the door open for a May rate hike even as February inflation was slightly softer than expected. EUR/GBP recently drifted south in the 0.9033/0.8688-52 trading range. A downside test is possible, but we don't expect a clean break yet.

EUR/USD stalemate persists as Fed confirms 'gradual' policy normalization