Sample Category Title

BoE Seen Preparing Markets For A May Rate Hike, Risk Appetite Wanes Ahead Of Trump Chinese Tariff Announcement

Notes/Observations

- Major European Manufacturing PMI data (France, Germany and Euro Zone) all miss expectations as they retreat from recent cycle high levels

- German Mar IFO Survey registers a slight beat but continues to move off recent record highs registered back in Jan

- BoE seen preparing markets or a May rate hike; Focus will be on policy vote to see if there are any dissenters

Asia:

- New Zealand Central Bank (RBNZ) left its Official Cash Rate (OCR) unchanged at 1.75% (as expected). monetary policy to remain accommodative for a considerable period

- Australia Feb Employment Change: +17.5K v +20.0Ke; Unemployment Rate: 5.6% v 5.5%e

- Japan Mar Preliminary PMI Manufacturing slowed for 2nd straight month (53.2 v 54.1 prior)

- PBoC raised its 7-Day Reverse Repo by 5bps to 2.55% (tracks Wed's 25bps rate hike by US Fed, as speculated)

Europe:

- EU Leaders summit draft to remind UK that nothing was agreed to yet regarding Brexit and that Ireland and Gibraltar commitments must be respected

- Germany Finance Ministry Monthly Report: Indicators suggest German economic growth slowed at start of 2018. Uncertainties resulting from US decision to impose tariffs on imports pose a risk to German exports

- Catalan Parliament expected to meet on Thursday, Mar 22nd and nominate Jordi Turull as the new President

Americas:

- FOMC raised its Target Rate Range by 25bps to 1.50-1.75% (as expected). Dots suggest 2 more hikes this year for total of 3.

- Fed Chair Powell stated during his press conference that decision to hike was another step in gradual process. FOMC expected job market to remain strong. Economic outlook strengthened in recent months. Shortfall of inflation reflected unusual price declines from last year. Inflation might be above or below 2% at times. Balance sheet reduction program proceeding smoothly and did not intend to alter

- Brazil Central Bank (BCB) cut its Selic Rate by 25bps to 6.50% (as expected)

- Canada PM Trudeau: Seems to be a certain momentum around NAFTA talks; remained optimistic about ability to get a good deal on NAFTA

- White House: President Trump to sign memo on China trade at 12:30 PM EST on Thursday, Mar 22nd (Insight: White did not provide any no indication on size or scope of tariffs) Reports circulated that Trump was prepared to announce ~$50Bin tariffs against China over intellectual property violations and targeting over 100 different types of Chinese goods. The value of the tariffs based on US estimates of economic damage caused by intellectual property theft

Economic Data:

- (MY) Malaysia Mid-Mar Foreign Reserves: $103.9B v $103.7B prior

- (FR) France Mar Business Confidence: 109 v 109e; Manufacturing Confidence: 111 v 111e, Production Outlook Indicator: 27 v 28e, Own-Company Production Outlook: 11 v 16e

- (TW) Taiwan Feb Unemployment Rate: 3.7% v 3.7%e

- (FR) France Mar Preliminary Manufacturing PMI: 53.6 v 55.5e (18th month of expansion and lowest since Mar 2017); Services PMI: 56.8 v 57.0e, Composite PMI: 56.2 v 57.0e

- (PH) Philippines Central Bank (BSP) leaves Overnight Borrowing Rate unchanged at 3.00%, as expected

- (DE) Germany Mar Preliminary Manufacturing PMI: 58.4 v 59.8e (39th month of expansion and lowest since July); Services PMI: 54.2 v 55.0e; Composite PMI: 58.4 v 57.0e

- (HK) Hong Kong Q4 Current Account: $15.2B v $58.8B prior; Overall Balance of Payments (BoP) $73.5B v $55.6B prior

- (EU) Euro Zone Mar Preliminary Manufacturing PMI: 56.6 v 58.1e; Services PMI: 55.0 v 56.0e, Composite PMI: 55.3 v 56.8e

- (EU) Euro Zone Jan Current Account (Seasonally Adj): €37.6B v €31.0B prior; Current Account NSA (unadj): €12.8B v €46.8B prior

- (DE) Germany Mar IFO Business Climate: 114.7 v 114.6e; Current Assessment: 125.9 v 125.6e, Expectations Survey: 104.4 v 104.4e

- (IT) Italy Jan Current Account: -€1.3B v €6.2B prior

- (IS) Iceland Feb Wage Index M/M: 0.4% v 0.4% prior; Y/Y: 7.2% v 7.3% prior

- (UK) Feb Retail Sales (Ex Auto Fuel) M/M: 0.6% v 0.4%e; Y/Y: 1.1% v 1.2%e

- (UK) Feb Retail Sales (Including Auto Fuel) M/M: 0.8% v 0.4%e; Y/Y: 1.5% v 1.4%e

- (TW) Taiwan Central Bank (CBC) left its Benchmark Interest Rate unchanged at 1.375%, as expected

- (ID) Indonesia Central Bank (BI) left its 7-Day Reverse Repo unchanged at 4.25%

Fixed Income Issuance:

- None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -0.7% at 372.1, FTSE -0.6% at 6993, DAX -1.1% at 12170, CAC-40 -1.0% at 5189, IBEX-35 -0.8% at 9556, FTSE MIB -1.0% at 22600 , SMI -0.8% at 8713, S&P 500 Futures -0.8%]

- Market Focal Points/Key Themes: European Indices trade lower across the board tracking US futures lower following the FOMC rate decision yesterday and the BoE rate decision later today. Earnings were the dominant theme on the corporate front with IG Group outperforming following strong quarterly results, with Ted Baker, Lamprell trading lower. German names Hella, United Internet, Zooplus and HeidelbergerCement also trade lower after results. Reckitt Benckiser outperforms after dropping its interests in Pfizers Consumer health unit, with CA Immobilien Anlagen and Immofinanz also higher after Starwood takes a stake. Looking ahead we continue to see retailers reporting, with Darden, GIII apparel and Cato reporting alongside Accenture.

Movers

- Consumer Discretionary [ Hella Kgaa [HLE.DE] -1.5% (Earnings), Zooplus [ZO1.DE] -6.8% (Earnings), CTS Eventim [EVD.DE] -2.6% (Earnings)]

- Energy [Lamprell [LAM.UK] -4.6% (Earnings)]

- Industrials [HeidelbergerCement [HEI.DE] -1.7% (Earnings)

- Healthcare [ Reckitt Benckiser [RB.UK] +6.2% (Drops interest in Pfizer's consumer health unit), Ted Baker [TED.UK] -6% (Earnings) ]

- Technology [United Internet [UTDI.DE] -7.4% (Earnings)]

- Financial [ IG Group [IGG.UK] +4.7% (Earnings), Wendel [MF.FR] -1.1% (Earnings)]

Speakers

- ECB Economic Bulletin: Developments supported the notion of a gradual upward trend in wage growth and gradual buildup in domestic cost pressures. Reiterates that an ample degree of monetary policy accommodation remained necessary

- ECB’s Nouy (SSM chief): Need to improve bank governance framework. Some banks had too many Board members

- SNB Annual Report noted that it had spent CHF48.2B on FX intervention in 2017

- Sweden Central Bank (Riksbank) Dep Gov Floden: Still a concern that inflation pressure was low. Reiterated view that domestic growth was good with underlying strength. Surprised by the big decline in unemployment suspecting it might be due to seasonal factors. Reiterated Riksbank view that Sweden could likely raise rates before the ECB

- German Fin Min Scholz: Domestic economy was doing well. Reiterated Govt stance that Germany needed a balanced budget and was in Germany’s national interest to safeguard EU's future. Germany could not solve banking union problems alone

- Italy acting PM Gentiloni could resign once Parliamentary speakers were designated

- German IFO Economists commented that it would maintain its current 2018 GDP growth forecast but was not expecting new growth records export expectations had fallen to its lowest level in over a year

- Philippines Central Bank policy statement noted that inflation to meet its target in 2018 and 2019 and would monitor rising inflation expectations as it saw upside risks. Domestic demand was firm and saw liquidity as adequate

- Philippine Central Bank Deputy Gov Guinigundo: Ready to tighten policy if needed; BSP is not behind the curve

- BOJ's Wakatabe: Fiscal policy is up to the govt and Parliament. Synergy between fiscal and monetary policy was important. Reiterated that BOJ could not buy foreign bonds to influence the FX rate

- Taiwan Central Bank Central Bank gov Perng saw stronger domestic demand in 2018 but the output gap remained negative. Financial conditions index had loosened while the inflation outlook remained mild

- Indonesia Central Bank (BI) Gov Martowardojo pre-rate decision press conference: Q1 GDP growth seen better compared t prior quarters. To guard IDR currency (Rupiah) to be in-line with fundamentals and monitor all risks from global markets

Currencies

- The USD continued with its softer tone in the aftermath of the Fed rate decision. Fed had executed a hawkish hike. However, markets appeared to have given it a dovish spin. Dealers noted of elevated hawkish expectations going into the meeting on Wed and concluded that economic dots did not necessarily justify a faster hiking cycle this year at this time.

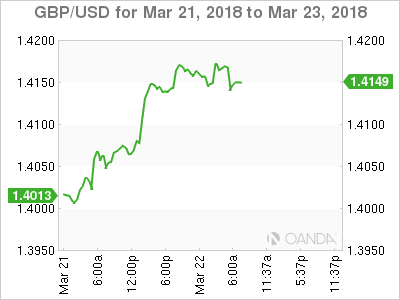

- The GBP/USD was higher by 0.2% at 1.4160 as and the BoE was seen as likely preparing for a May rate hike later today. Retail sales data was mixed with mostly a beat on the front month readings while the back month was revised lower.

- EUR/USD still well-contained within its 2018 trading range but slightly firming in today’s session. The pair was about 30 pips off its best levels as European data continued to move off recent cycle highs.

Fixed Income

- Bund Futures trade 34 ticks higher at 158.34 extending the move higher after regional PMI data misses expectations across the board and German IFO continues to come off the record highs seen in January. Upside targets 158.75, while a return lower targets the157.25 level.

- Gilt futures trade at 122.26 up 25 ticks following the move in US Treasury's. Support continues to stand at 120.75 then 120.15, with upside resistance at 122.85 then 123.35.

- Thursday's liquidity report showed Wednesday's excess liquidity dropped to €1.806T from €1.842T prior. Use of the marginal lending facility fell from €200M to €55M.

Looking Ahead

- (EU) EU leaders begin 2-day Summit in Brussels

- (IT) Italian parliament reconvenes after general election

- (CO) Colombia Feb Retail Confidence: No est v 21.8 prior; Industrial Confidence: No est v 0.0 prior

- (AR) Argentina Mar Consumer Confidence: No est v 43.8 prior 0

- 06:00 (EU) Daily Euribor Fixing

- 06:30 (HU) Hungary Debt Agency (AKK) to sell 12-month Bills

- 06:30 (HU) Hungary Debt Agency (AKK) to sell Floating Bonds

- 07:00 (CZ) Czech Republic to sell Bills

- 07:00 (RO) Romania to sell 4.75% 2019 Bonds

- 07:00 (IE) Ireland Feb PPI M/M: No est v -1.2% prior; Y/Y: No est v -4.9% prior

- 07:00 (IE) Ireland Jan Industrial Production M/M: No est v 3.0% prior; Y/Y: No est v 3.0% prior

- 07:00 (ZA) South Africa Jan Retail Sales M/M: -0.1%e v -2.6% prior; Y/Y: 5.9%e v 5.3% prior

- 07:30 (TR) Turkey Mar Real Sector Confidence (seasonally adj): No est v 110.8 prior; Real Sector Confidence (unadj): No est v 110.8 prior

- 07:30 (TR) Turkey Mar Capacity Utilization: No est v 77.8% prior

- 07:30 (IS) Iceland to sell Bills - 07:45 (US) Daily Libor Fixing

- 08:00 (UK) Bank of England Bank (BOE) Interest Rate Decision: Expected to leave Interest Rates unchanged at 0.50%

- 08:00 (UK) Bank of England Bank (BOE) Mar Minutes

- 08:30 (US) Initial Jobless Claims: 225Ke v 226K prior; Continuing Claims: 1.870Me v 1.879M prior

- 08:30 (US) Weekly USDA Net Export Sales

- 09:00 (US) Jan FHFA House Price Index M/M: 0.4%e v 0.3% prior

- 09:00 (PL) Poland Feb M3 Money Supply M/M: +0.5%e v -1.1% prior; Y/Y: 5.0%e v 4.8% prior

- 09:00 (RU) Russia Gold and Forex Reserve w/e Mar 16th: No est v $455.2B prior

- 09:05 (US) Baltic Dry Bulk Index

- 09:45 (US) Mar Preliminary Markit Manufacturing PMI: 55.5e v 55.3 prior; Services PMI: 56.0e v 55.9 prior; Composite PMI: No est v 55.8 prior

- 10:00 (US) Feb Leading Index: 0.5%e v 1.0% prior

- 10:00 (BE) Belgium Mar Business Confidence: 1.2e v 1.9 prior

- 10:30 (US) Weekly EIA Natural Gas Inventories

- 11:00 (US) Mar Kansas City Fed Manufacturing Activity: 17e v 17 prior

- 11:30 (US) Treasury announcement for upcoming 2-year, 5-year and 7-year note auctions during week of Mar 26th

- 12:00 (UK) BOE’s Ramsden in London

- 12:30 (US) President Trump expected to sign China tariffs

- 13:00 (US) Treasury to sell 10-Year TIPS Reopening

- 15:00 (CA) Bank of Canada (BOC) Dep Gov Wilkins speech

- 15:00 (AR) Argentina Q4 Current Account: -$8.0Be v -$8.7B prior

- 15:00 (CO) Colombia Jan Economic Activity Index (Monthly GDP) Y/Y: 1.8%e v 1.3% prior

- 19:30 (JP) Japan Feb National CPI Y/Y: 1.5%e v 1.4% prior; CPI (Ex-fresh food) Y/Y: 1.0%e v 0.9% prior; CPI (Ex-fresh food/energy) Y/Y: 0.5%e v 0.4% prior

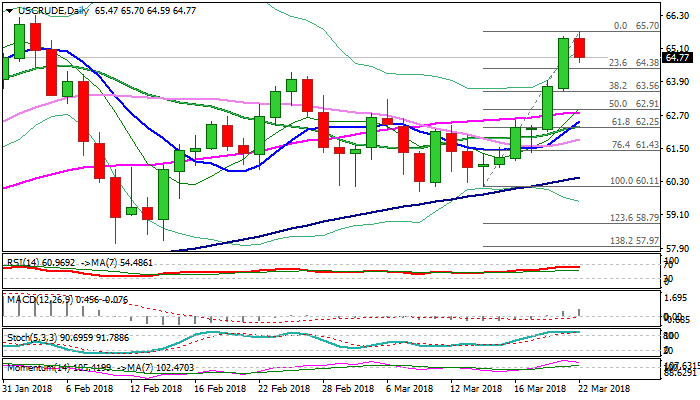

Technical Outlook: WTI OIL Eases After Six-Day Rally, Risk Of Stronger Weakness On Trade War Concerns

WTI oil price eases on Thursday after hitting marginally higher high at $65.70 (the highest since early Feb) in uninterrupted six-day rally.

Strong bullish sentiment could be soured by rising concerns about import tariffs on China, which could trigger stronger correction of $60.11/$65.70 ascend.

Overall structure remains firmly bullish and current easing could be seen as corrective action on overbought conditions (slow stochastic reverses in deep overbought territory).

Initial supports at $64.38/22 (Fibo 23.6% of $60.11/$65.70 rally / 26 Feb former high) are still intact, with deeper dips expected to find ground at $63.56 (Fibo 38.2% / Wednesday’s low) to keep bullish structure intact for fresh attempts higher and final push towards target at $66.64 (25 Jan peak).

Conversely, close below $63.56 would generate negative signal and risk further easing towards rising 55SMA at $62.79.

Res: 65.23, 65.53, 65.70, 65.85

Sup: 64.38, 64.22, 63.56, 63.26

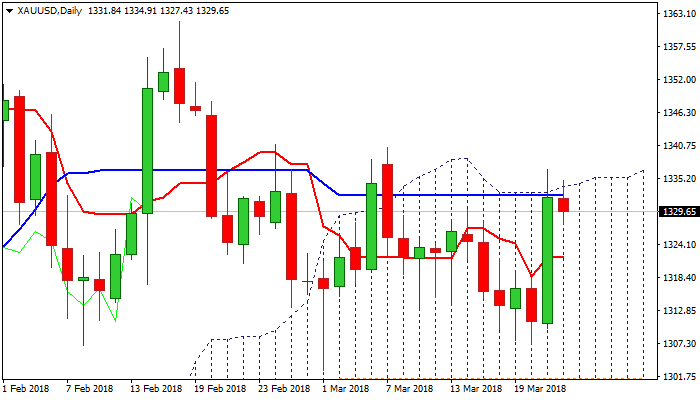

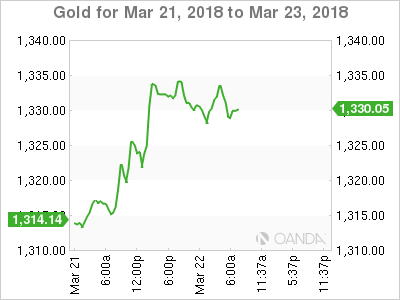

Technical Outlook: SPOT GOLD – Outlook Remains Bullish But Daily Cloud Top Limits Advance For Now

Spot Gold consolidates under new two-week high at $1336, after rallying strongly on Wednesday on less hawkish than expected Fed which hit the greenback. The yellow metal was additionally supported by growing concerns about trade war which increased demand for safe-haven assets.

Wednesday’s rally surged through strong $1320/29 resistance zone, provided by a cluster of MA’s, but faced strong headwinds from top of daily cloud ($1334) which was repeatedly dented but without clear break higher so far.

Current action so far looks as consolidation before final push through cloud top and extension towards next target at $1340 (07 Mar high).

Daily techs remain in full bullish configuration and supportive for further advance, as trade war fears underpin.

Alternative scenario requires return and close below $1320 to weaken near-term structure and risk further weakness.

Res: 1334, 1336, 1340, 1345

Sup: 1327, 1323, 1321, 1315

Euro Shrugs Off Soft Manufacturing PMIs

EUR/USD has paused on Thursday, after gains on the Wednesday session. Currently, the pair is trading at 1.2327, down 0.10% on the day. On the release front, eurozone and Germany Manufacturing PMIs missed their estimates. Eurozone Manufacturing PMI dropped to 56.6, down from 58.1 points. The German release slowed to 58.4, compared to the estimate of 59.8 points. German Ifo Business Climate also dipped to 114.7, matching the estimate. In the US, the key indicator is unemployment claims, which is expected to edge lower to 225 thousand. On Friday, the US releases durable goods and housing reports.

As widely expected, the Federal Reserve raised rates by a quarter-point on Wednesday, bringing the benchmark rate to a range between 1.50% and 1.75%. The markets were looking for any clues with regard to the pace of rate hikes in 2018 – currently the Fed is projecting three hikes, but a robust US economy could push the Fed to press the rate trigger four times. The rate statement did not directly address the issue, but there was a refreshing lack of Fedspeak from policymakers, who said that “the economic outlook has strengthened in recent months”. This phrase has not been used in previous rate statements, and if Fed policymakers reiterate positive sentiment towards the economy, could push the US dollar to higher ground.

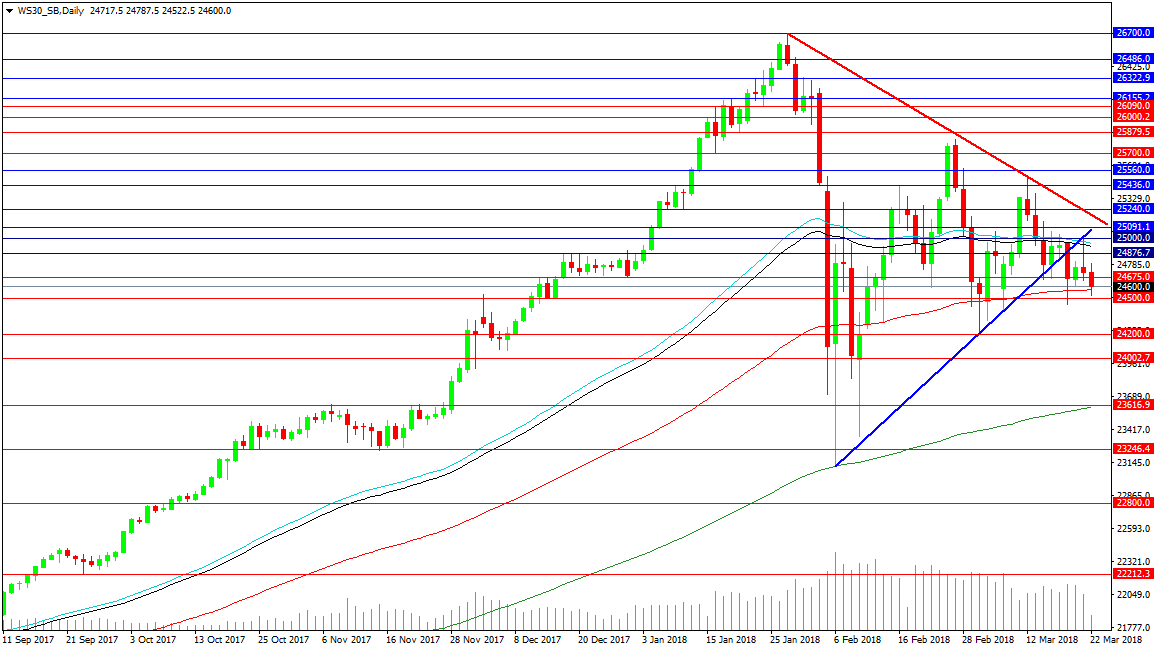

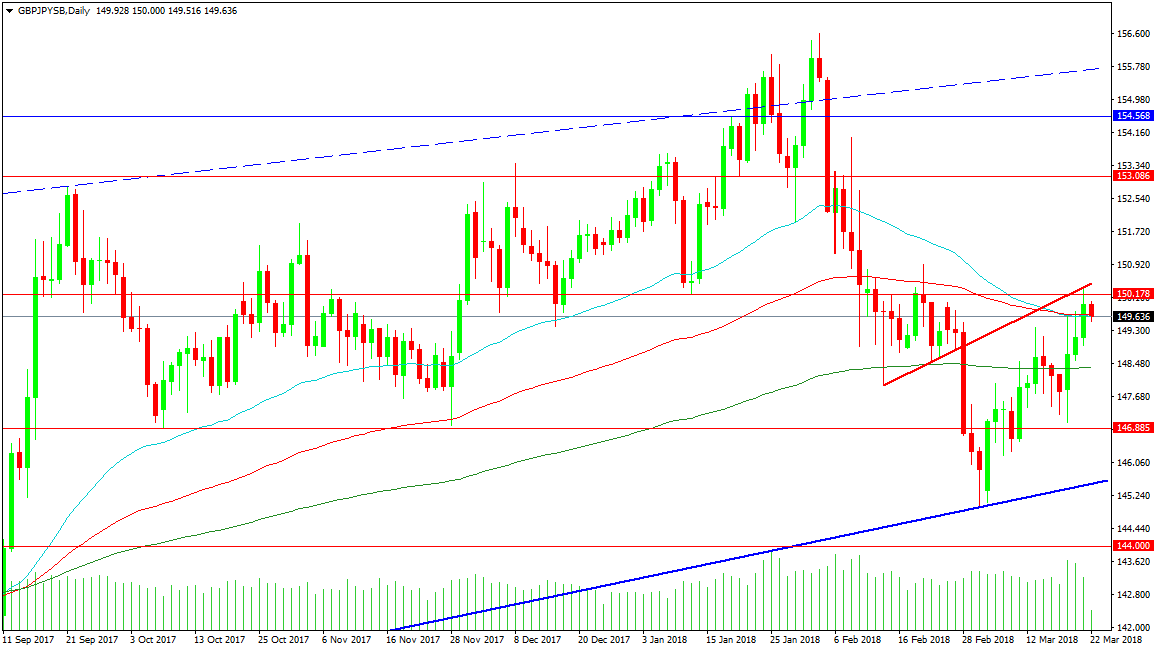

Forex Analysis: US 30 And GBPJPY Analysis

After the FOMC yesterday, the US 30 index initially moved higher to test towards 25000.00 but failed, as it ran into the blue trend line resistance and faded down to a low of 24679.5, which has been taken out this morning. Today’s low is extending to 24522.2. This paints a bearish picture for the index, as the tech industry gets hit and risk sentiment is weak. Major support is found at 24200.0, with a loss here creating a lower low and putting the February low of 23108.0 in focus. The rising 200 DMA is located at 23600.0 today and may see buyers step back into the market, for a repeat of the February rally. Failure to do so puts a question mark over the market, which is already trading flat on the year.

Should bulls find support, a rally above the falling red tend line at 25184.0 is needed to wrest control from bears. The 50 DMA is located at 24950.0, with further resistance at 25500.0 and 25821.0. A move above these levels targets 26200.0 and the high at 26700.0.

GBPJPY

The GBPJPY pair will be actively traded today, as the BOE decides on its Monetary Policy and Rates. Price rose to test broken support as red trend line resistance yesterday and pulled back today to the combined 50 and 100 DMAs at 149.695. The inability to stay above 150.000 is a concern for long traders, with resistance firming around this area. There is further resistance at 150.500, as the trend line rises. The next level of resistance comes at 151.920, followed by 153.086 and 154.568 above. The rising broken blue resistance trend line is at 155.675, with the high of 156.597 overhead.

Support can be found at the 149.366 level and the 200 DMA at 148.398. A drop under there puts the 146.885 level in focus, as a loss of it creates a lower low and targets the low at 144.975. The rising blue support trend line, which originates at the April 2017 low, is located at 145.500 and contains 3 touches.

Risk Appetite Fades Ahead Of Trump Chinese Tariff Announcement

Thursday March 22: Five things the markets are talking about

Ahead of the U.S open, Treasuries prices have rallied, the once ‘mighty’ dollar has extended its losses and Euro equities are under pressure as the market assesses the implications of higher borrowing costs in the U.S and in China, alongside global trade tensions.

Note: The Whitehouse administration is set to announce trade tariffs against China later today (12:30 EDT).

Overnight, the People’s Bank of China (PBoC) increased short-term interest rate just hours after the Fed announced its first interest-rate increase for this year. The PBoC raised the rate by +0.05% for the seven-day tenor.

Yesterday, Fed officials, meeting for the first time under new Chairman Jerome Powell, as expected raised the benchmark lending rate +25 bps and forecasted a steeper path of hikes in 2019 and 2020, citing an improving economic outlook.

Nevertheless, the market was disappointed as they had expected U.S officials to live up to some predictions that it would lean towards four rate hikes this year, instead of the three that had been communicated yesterday (dots suggest 2 more hikes this year for total of 3).

1. Stocks mixed results

In Japan, the Nikkei share average rallied overnight despite a stronger yen (¥105.68) with retail investors purchasing recently battered stocks. The Nikkei ended +1.0% higher, while the broader Topix was up +0.7%.

Down-under, Aussie shares fell on Thursday, as early gains from solid jobs data were erased by losses amongst financials. The S&P/ASX 200 index slipped -0.2%. The benchmark had advanced +0.2% on Wednesday. In S. Korea, the Kospi stock index surged to a seven-week high on a less ‘hawkish’ than anticipated Fed. At the close it was up +0.44%.

In Hong Kong, tech firms drag down regional shares as trade war fears weigh. At close of trade, the Hang Seng index was down -1.1%, while the Hang Seng China Enterprises index fell -0.8%.

In China, stocks were also under pressure on concerns over a potential trade war between the world’s two largest economies. At the close, the Shanghai Composite index was down -0.5%, while the blue-chip CSI300 index was down -1%.

In Europe, regional indices trade lower across the board, tracking U.S futures lower following the FOMC rate decision yesterday and the BoE rate decision this morning.

U.S stocks are set to open deep in the ‘red’ (-0.8%).

Indices: Stoxx600 -0.7% at 372.1, FTSE -0.6% at 6993, DAX -1.1% at 12170, CAC-40 -1.0% at 5189, IBEX-35 -0.8% at 9556, FTSE MIB -1.0% at 22600, SMI -0.8% at 8713, S&P 500 Futures -0.8%

2. Oil under pressure as U.S output to disrupt markets, gold higher

Oil prices are under pressure as the rise in U.S crude production threatens to undermine efforts led by OPEC to tighten the market.

Brent crude futures are at +$69.34 per barrel, down -13c, or -0.2% from their last close. U.S West Texas Intermediate (WTI) crude futures are at +$65.13 a barrel, down -4c from their previous settlement.

Note: Both benchmarks yesterday hit their highest levels since early February, having risen around +10% from its March lows.

Any confidence in the oil market is being tempered by U.S crude production – last week it climbed to a new record of +10.4m bpd, putting the U.S ahead of top exporter Saudi Arabia and within reach of Russia’s +11m bpd.

Note: Yesterday’s EIA report showed that U.S crude inventories had a drawdown of -2.6m barrels in the week ended March 16 to +428.31m barrels.

Ahead of the U.S open, gold prices trade atop of its two-week high on a weaker dollar after the Feds rate view. Spot gold has rallied +0.1% to +$1,332.77 per ounce. Prices rose to a two-week high of +$1,336.59 yesterday, and also registered their biggest single-day percentage gain since May of last year.

3. Yields fall on ‘dovish’ Fed

This morning, the Bank of England (BoE) is expected to keep interest rates and its asset-purchase program unchanged at 08:00 EDT. Attention will be on the language and the odds for a May hike, now seen as increasingly likely despite softer-than-expected inflation. U.K inflation fell to +2.7% in February, but remains well above the BoE’s +2.0% target.

Down-under, the NZD/USD (N$0.7233) jumped by +1.1% after the FOMC statement, but had little reaction to its own central bank’s comments yesterday afternoon. The RBNZ left its official cash rate unchanged at +1.75%, as widely expected.

Note: New RBNZ Governor, Adrian Orr, starts work next Tuesday.

Elsewhere, the yield on U.S 10’s has decreased -3 bps to +2.85%, the biggest dip in three weeks. In Germany, the 10-year Bund yield has fallen -2 bps to +0.57%, the lowest in almost two-months.

4. Dollar under intense pressure

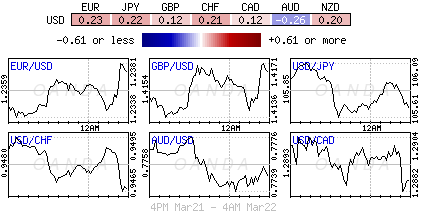

The once ‘mighty’ USD continues with its softer tone after yesterday’s Fed decision. The Fed had executed a ‘hawkish’ hike, but fixed income dealers have given it a dovish spin as they expected four hikes in 2018, not the dot planned three.

The markets focus now shifts to sterling (£1.4140). GBP rallied to a seven-week high outright of £1.4181, helped by a broad-based weakening of the dollar as well as above-forecast U.K. retail sales data (see below). Market will be looking closely at the BoE’s statement – a “hawkish” tone [which means a 8-1 or 7-2 vote] may tilt the balance in favour of a rate hike as early as May.

Elsewhere, the EUR/USD (€1.2326) remains contained within its 2018 trading range, but a tad firmer in today’s session.

5. U.K retail sales rebounded in February

Data from the ONS this morning showed that U.K retail sales rebounded last month, but the underlying picture stayed weak, signalling that the British consumer remains cautious.

Sales grew by +0.8% on month in February, compared with a monthly decline of +0.2% in January. The headline print was double the markets expectations.

Digging deeper, with the exception of non-food stores, all retail sectors saw growth in the month. This, however, came after a -0.3% downward revision to January’s monthly growth.

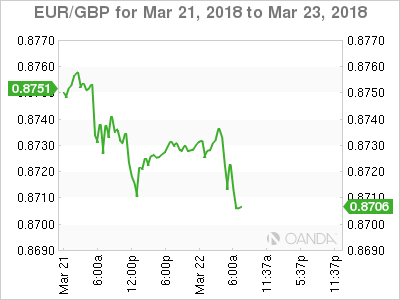

Euro broadly lower after data miss, Sterling mixed ahead of BoE, EUR/GBP an interesting one to watch

Euro suffers broad based selling in the current 4H bar as seen in heatmap. It's triggered by a string of data misses, that started from France PMIs, Germany PMIs and Eurozone PMIs. While German Ifo business climate beat expectation, it did dropped from 115.4 to 114.7 in March. Just as Markit economist said, growth in Eurozone should have peaked around the turn of the year already.

Meanwhile, Sterling is mixed ahead of BoE rate decision as traders turn a bit cautious. But it's still generally firm as markets are anticipating a hawkish turn that might signal a May hike.

EUR/GBP will be an interesting one to watch in the come 2 hours. 6H action bias chart indicate clear downside momentum with the fall from 0.8967. However, D action bias chart showed that it's just starting turn red in the last few bars. Also, as mentioned in our technical outlook reports, 0.8686 is a key support level, bottom of the multi-month range. It's still unsure whether this level would be taken out. BoE will be the key.

BoE To Follow In The Footsteps Of The Fed?

- Investors Anxious About Pace of Tightening and Trade Wars;

- BoE Expected to Signal May Rate Hike Today.

Investors Anxious About Pace of Tightening and Trade Wars

US futures are coming under pressure once again ahead of the open on Thursday, as investors continue to display an anxiety about the path of interest rates against a backdrop of escalating trade conflicts.

The Federal Reserve announcement on Wednesday went, broadly speaking, as many anticipated with the central bank raising growth and inflation forecasts and, with that, expectations for interest rates in the coming years. While the central bank still only expects three rate hikes this year, an extra is now forecast for next year and it’s expected to reach 3.4% in 2020, up from 3.1% in December.

This faster pace of tightening is primarily being driven by the fiscal stimulus from tax reforms which were passed late last year. There was plenty of debate about whether this was necessary and while markets responded positively at the time – likely driven largely by corporation tax changes – we’re now seeing the negative impact, with investors fearing the impact more rate hikes could have on the wider economy.

On top of that, Donald Trump seems intent on starting trade wars, most notably with China, which could trigger a wave of protectionism and drive up prices in the US and likely weigh on the growth momentum. How the central bank deals with this will be very interesting given the already fast pace of hikes. Policy makers may well be feeling very happy with the decision to get ahead of the curve with tightening as it affords them the ability to maintain gradual hikes now.

BoE Expected to Signal May Rate Hike Today

On the other side of the pond, attention will be on the Bank of England monetary policy decision, as it prepares to raise interest rates from post-financial crisis emergency levels for the first time in nine years. The rate hike towards the end of last year was simply a reverse of the post-Brexit referendum cut a year earlier, taking the rate back to 0.5% where it had spent the seven and a half years previously.

While a rate hike is not expected today, it is heavily priced in for May when the central bank will also release its inflation report containing new macro-economic projections. The Monetary Policy Committee has become notably more hawkish recently and the reference to rate hikes needing to come "somewhat earlier and by a somewhat greater extent" than it expected in November, last month was a clear reference to an upcoming meeting. If the MPC is still planning to raise in May, I would expect another clear hint from the central bank today.

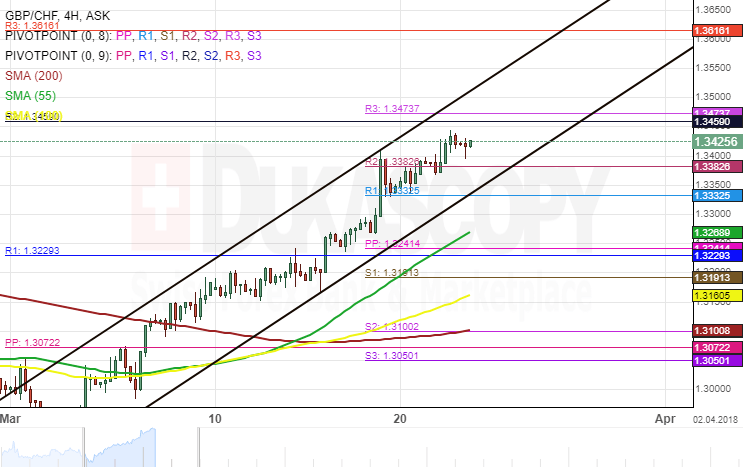

GBP/CHF 4H Chart: Trading In A Narrow Channel

The British Pound has been appreciating substantially against the Swiss Franc. The pair bounced off the lower boundary of a junior ascending channel on March 2 and has since trade bullish.

The GBP/CHF currency pair has been trading in a narrow channel since the beginning of March. Due to the fact that the channel is too narrow, it is likely going to be broken in the nearest future.

Technical indicators demonstrate that the rate could continue moving upward within this session. However, this surge is likely going to encounter a resistance cluster set by the monthly R2 and the weekly R3 near 1.3473.

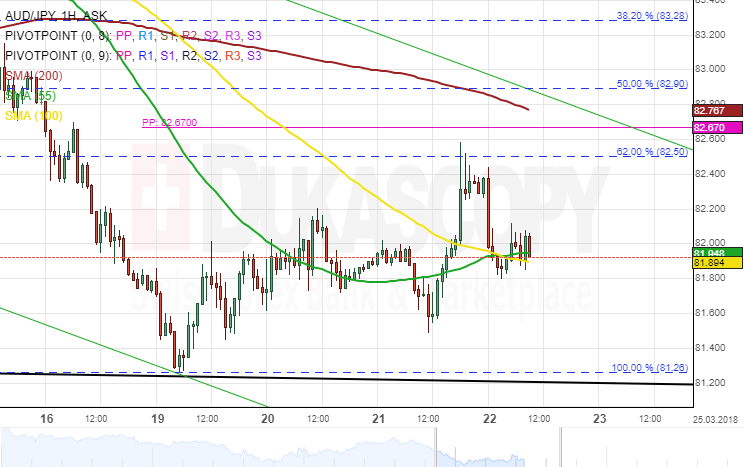

AUD/JPY 4H Chart: Bears Marke

The Australian Dollar has been strained in several channels down against the Japanese Yen. The exchange rate tested the upper boundary of a junior channel at 88.39 being followed by a strong period of decline. In the one-hour time frame, the currency pair breached the 62.80% Fibonacci retracement level and slowly moving south. This retracement can be measured by connecting the low at 81.26 and the high at 84.53. Everything being equal, the AUD/JPY exchange rate might continue trading in a descending channel because technical indicators suggest bears is likely to grow stronger during the following days.