Sample Category Title

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3964; (P) 1.4015; (R1) 1.4048; More....

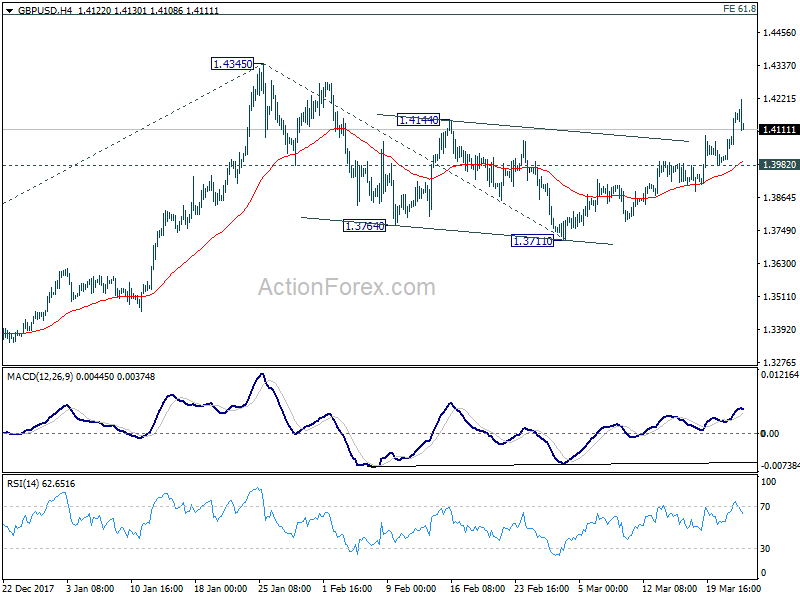

GBP/USD surges to as high as 1.4215 but retreats mildly since then. With 1.3982 minor support intact, intraday bias stays on the upside for further rally. Current development is consistent with our bullish view that correction from 1.4345 has completed at 1.3711 already. And larger up trend could be ready to resume. Further rise should be seen to retest 1.4345 high first. Break will target 61.8% projection of 1.3038 to 1.4345 from 1.3711 at 1.4519 next. On the downside, break of 1.3982 support is needed to signal completion of the rise from 1.3711. Otherwise, outlook will remain cautiously bullish in case of retreat.

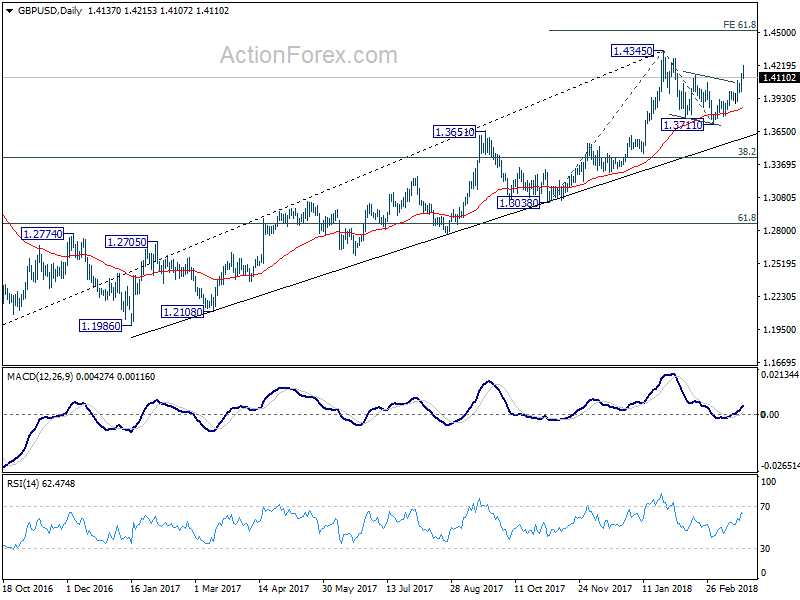

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9520; (P) 0.9544; (R1) 0.9588; More...

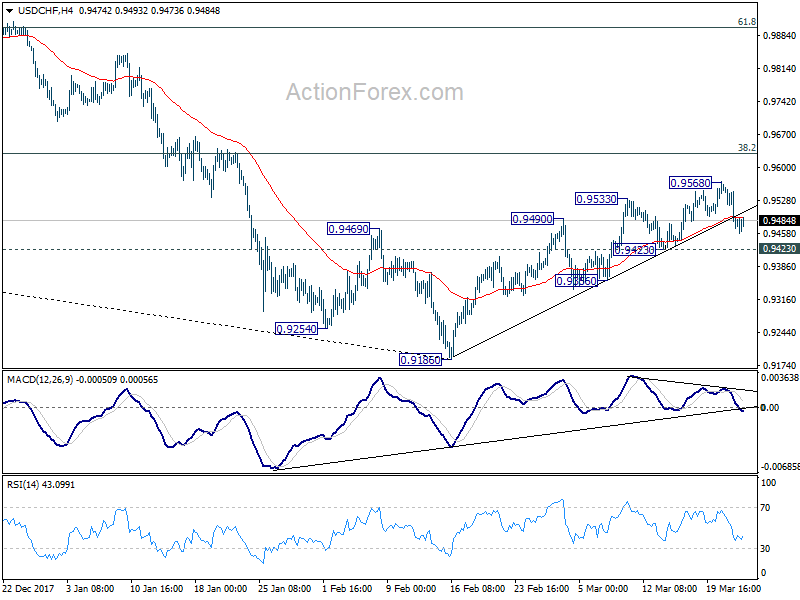

USD/CHF is staying in range between 0.9423 and 0.9568 and intraday bias remains neutral first. Rebound from 0.9186 could extend with another rise. But considering bearish divergence condition in 4 hour MACD, upside should be limited by 0.9626 key fibonacci level, to complete the rebound from 0.9186. Break of 0.9432 support will indicate near term reversal and turn bias to the downside for retesting 0.9186 low. Nonetheless, sustained break of 0.9626 will carry larger bullish implications.

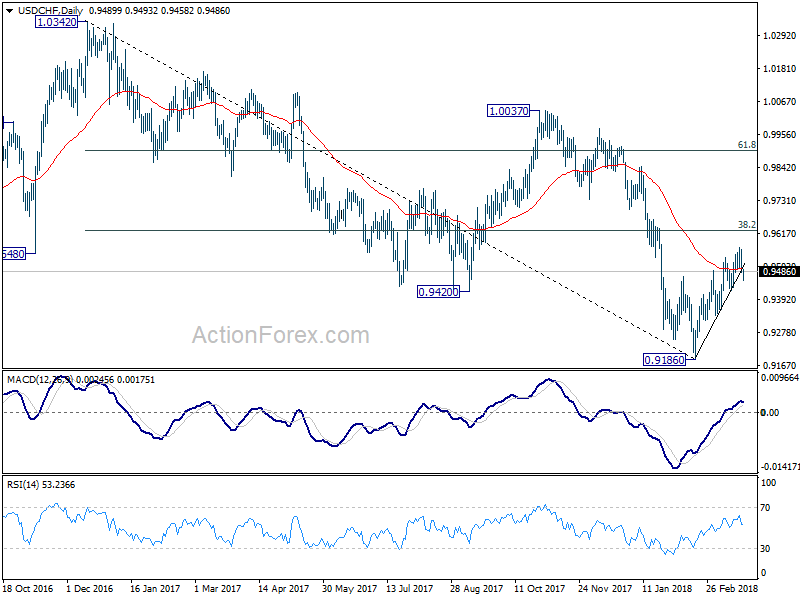

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Current development is raising the chance that it is completed. But there is no confirmation yet. Focus will now be back on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add much credence to the case of trend reversal and target 61.8% retracement at 0.9900 and above. However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

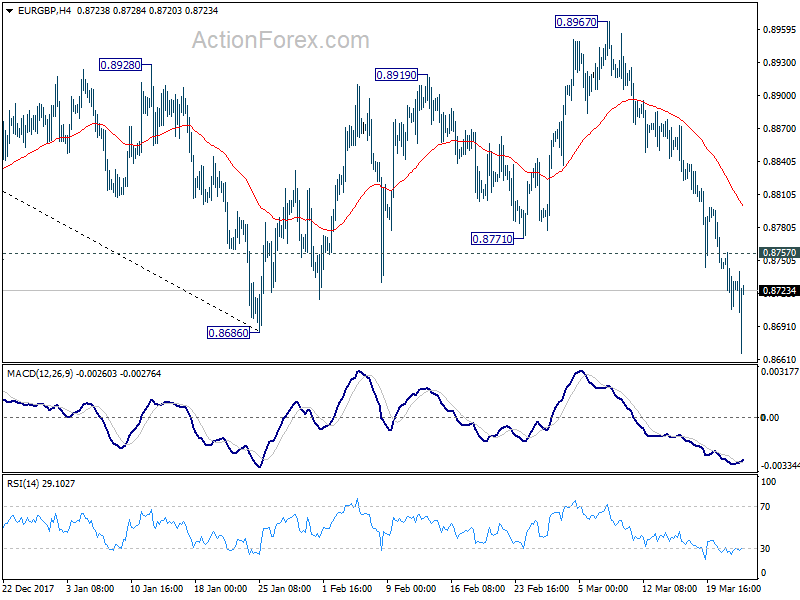

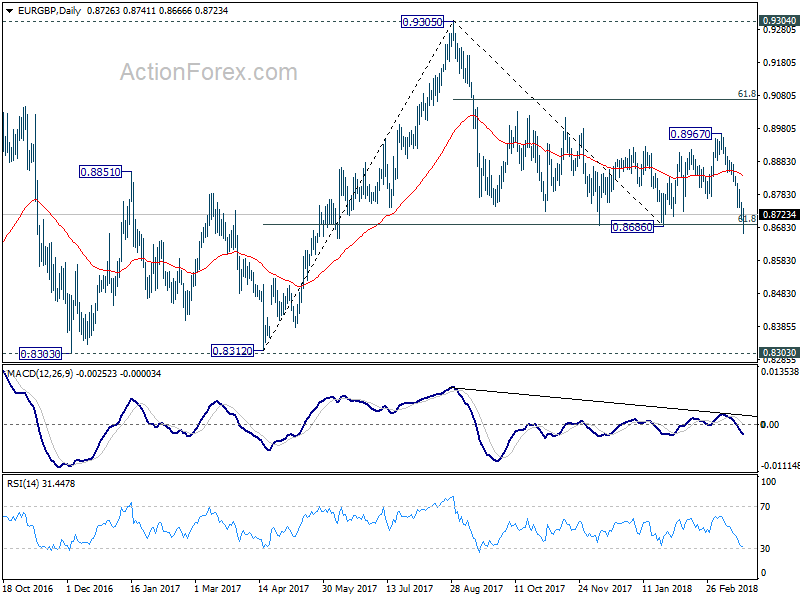

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8701; (P) 0.8730; (R1) 0.8753; More...

EUR/GBP dives to as low as 0.8666 today and breached 0.8686 briefly, before recovering. At this point, intraday bias stays on the downside with 0.8757 minor resistance intact, with focus on 0.8686 key support level. We'd be cautious on strong support from there to bring another rebound. But decisive break of 0.8686 will resume whole fall from 0.9305 and target 0.8303 key support next. On the upside, above 0.8757 minor resistance will turn bias back to the upside for recovery to 4 hour 55 EMA (now at 0.8802) and above.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Metal Prices Come Under Fire from Trump Tariffs; Aussie also Feels the Pressure

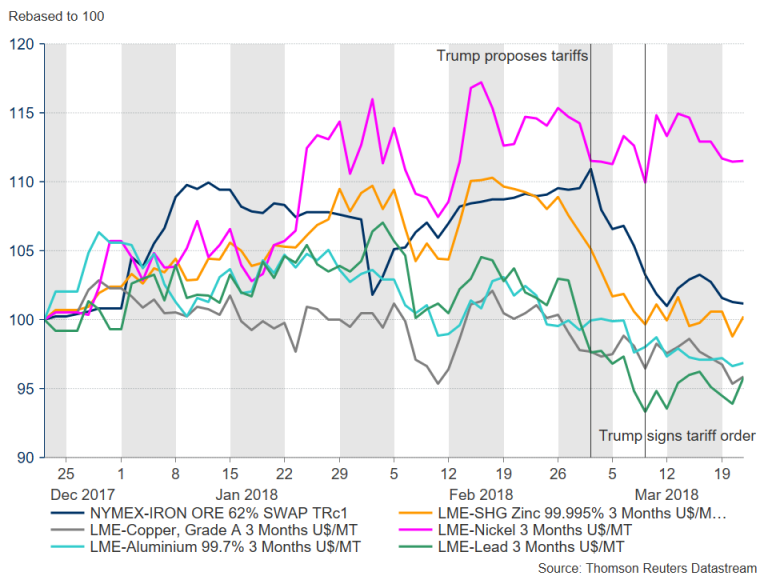

After an impressive two-year rally, industrial metal prices have been having a stormier time in 2018, being first swept over by the market turbulence caused by the sell-off in global equities and bonds, then by the announcement by US President Donald Trump that he is imposing tariffs on US imports of steel and aluminium. Commodity-linked currencies such as the Australian dollar have also been pulled lower by the market volatility and subsequent rise in risk aversion.

However, despite an international outcry by governments and industry leaders against the tariffs, which has stoked fears of a global trade war, there’s been no dramatic sell-off in industrial metals as of yet, with the declines being more attuned to a technical correction than signalling the start of a new bearish phase.

The announcement on March 8 that the United States will be slapping 25% tariffs on steel imports and 10% on aluminium was a hugely symbolic move by President Trump that he intends to see through his election campaign promises. But reaction in financial markets was far more restrained than one would have anticipated. Although the bigger sell-off actually came within the preceding days when reports of the tariffs first started circulating, events and developments after the announcement helped contain steeper declines.

Iron ore – the main alloy used in steel – has been one of the bigger casualties of the tariffs. It fell by around 7% in the days leading to the official announcement of the tariffs and has since declined by a further 2% to near three-month lows. However, iron ore’s troubles are part of a wider problem in the steel industry relating to overcapacity and rising inventories in China.

Iron ore – the main alloy used in steel – has been one of the bigger casualties of the tariffs. It fell by around 7% in the days leading to the official announcement of the tariffs and has since declined by a further 2% to near three-month lows. However, iron ore’s troubles are part of a wider problem in the steel industry relating to overcapacity and rising inventories in China.

Imports of iron ore by China fell sharply in February, contributing to the sell-off. However, China’s monthly trade figures were overall positive as exports surged by 44.5%, providing support to wider commodity prices. Other data out of China also surprised to the upside, including better-than-expected manufacturing PMI and industrial output in February, helping commodity prices stabilize. In addition, exemptions from the tariffs for some countries, including Australia, provided a further cushion for the market from a sharper sell-off.

There should be some support for iron ore prices too if the US tariffs push up steel prices in the short term. (US steel prices have already started to rise on the prospect of a higher import tax). However, longer-term gains are unlikely as higher prices would eventually start to dent demand. The impact on aluminium is expected to be even more limited given the smaller size of the tariff and the fact that US imports account for just 7% of global output.

What happens next though will not only depend on whether or not the trade tensions escalate into a more serious and wider global trade war, but on demand as well. The value of the US dollar is another factor to consider in this equation as a weaker greenback is generally positive for commodities. The weakening dollar in 2017 fuelled the rally in commodities that’s been mostly driven by the improving outlook of the global economy.

However, this bullish outlook appeared at risk even before the US tariffs came into play as rising prices have led to increased supply, with inventories of many base metals such as copper, zinc and aluminium recording strong gains at the start of the year. Even for metals like nickel where stocks have been falling, an expected supply increase and softer demand in China should curb any sharp rise in prices. While most base metals remain above their moving averages, they are at risk of entering bearish territory, and with a possible trade war hanging over the market, it may be difficult for investor sentiment to change in the near term.

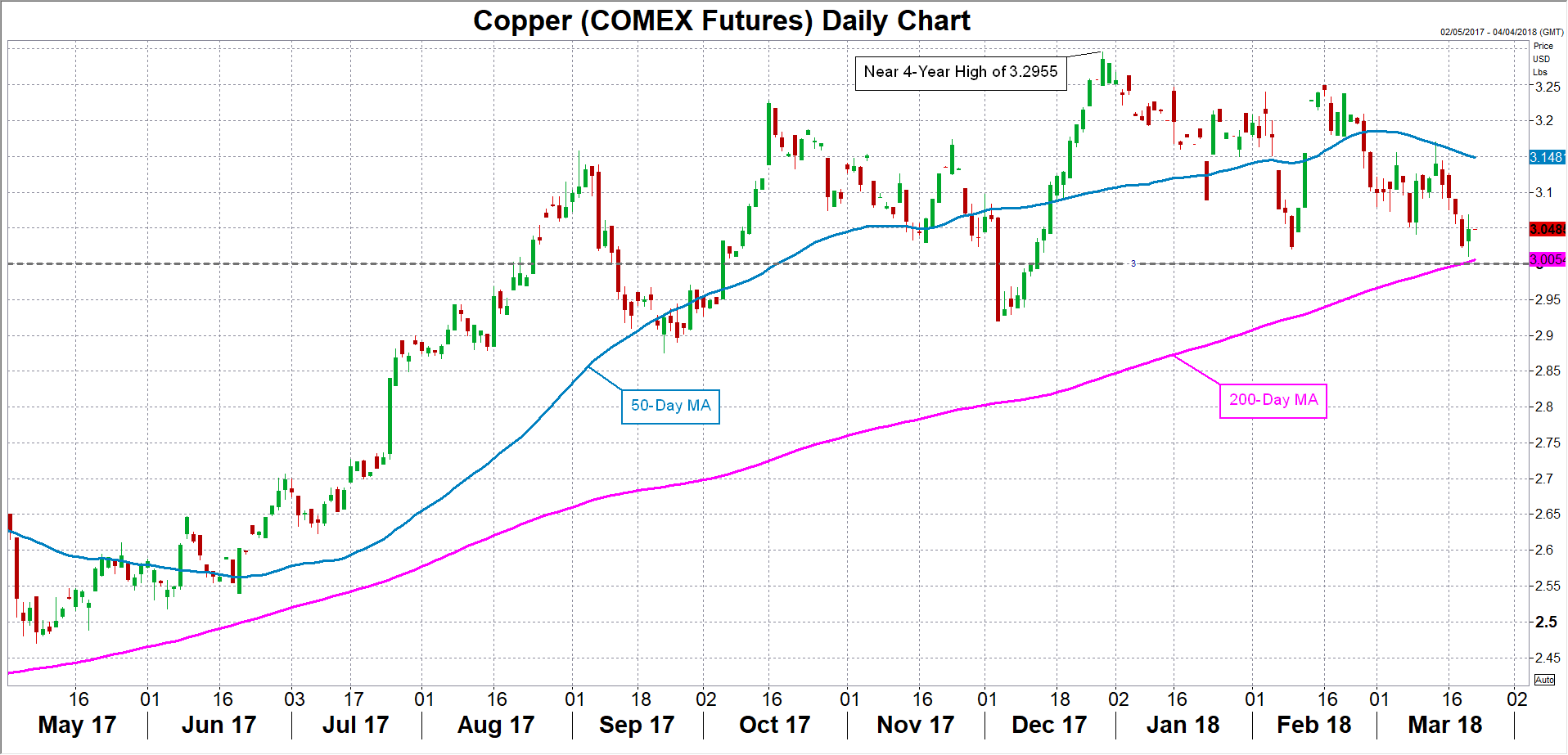

One of the most vulnerabe to a downside reversal is copper. The red metal is currently flirting with its 200-day moving average (MA). Failure to find support at the 200-MA just above the $3.00 per pound level could lead to deeper losses for copper. If the bearish sentiment was to spread to other metals, this could have a spill over effect in forex markets, particularly on the Australian dollar.

One of the most vulnerabe to a downside reversal is copper. The red metal is currently flirting with its 200-day moving average (MA). Failure to find support at the 200-MA just above the $3.00 per pound level could lead to deeper losses for copper. If the bearish sentiment was to spread to other metals, this could have a spill over effect in forex markets, particularly on the Australian dollar.

Australia is a major exporter of resources such as iron ore and copper, with China being the main destination. The demand outlook for industrial metals has already been dampened somewhat by expectations that growth in the world’s second largest economy and biggest consumer of commodities will slow in 2018. Should China engage in a trade war with the US, investors are likely to become more pessimistic about the demand outlook for metals, thus hurting the Australian currency.

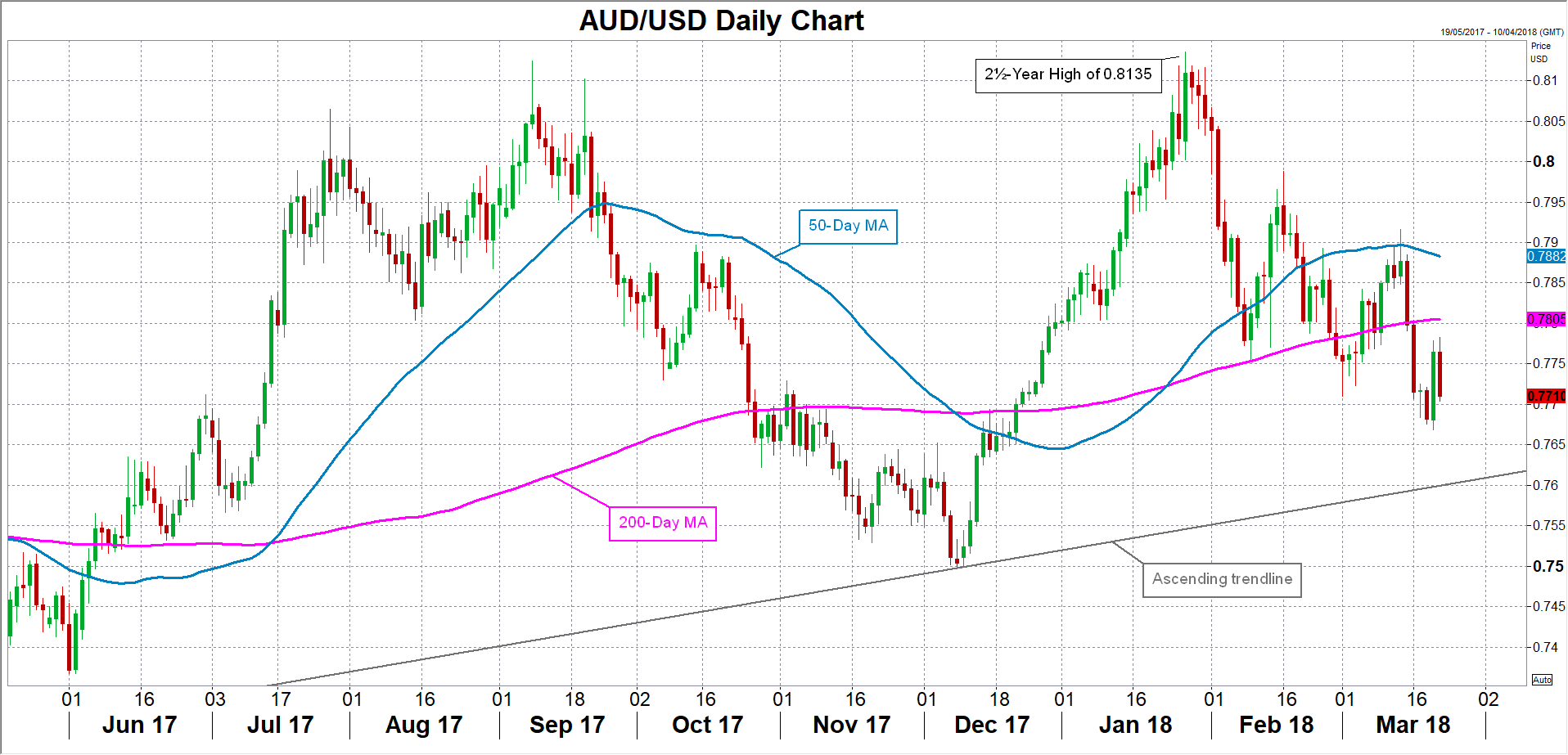

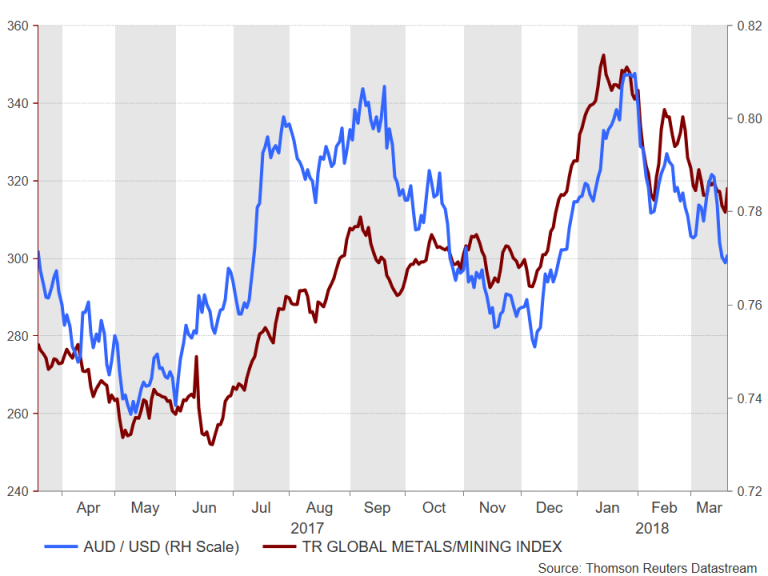

The aussie has been forming lower highs and lower lows since a two-month old rally came to a halt when it hit a 2½-year high of $0.8135 versus the US dollar in January. Whether this downtrend develops to a longer-term descent could depend to a great extent on how metals perform over the coming months. The Australian dollar has a historically strong correlation with the price of metals and mining stocks. A key support to watch in the coming weeks is the ascending trendline (currently around $0.76) that’s been evolving since early 2016. A breach of this trendline would be a bearish signal for the aussie/dollar.

The aussie has been forming lower highs and lower lows since a two-month old rally came to a halt when it hit a 2½-year high of $0.8135 versus the US dollar in January. Whether this downtrend develops to a longer-term descent could depend to a great extent on how metals perform over the coming months. The Australian dollar has a historically strong correlation with the price of metals and mining stocks. A key support to watch in the coming weeks is the ascending trendline (currently around $0.76) that’s been evolving since early 2016. A breach of this trendline would be a bearish signal for the aussie/dollar.

Traders could be tempted to push the pair to such levels if President Trump, as expected, announces on Thursday, additional tariffs, this time targeting Chinese technology and telecommunications products, as well as intellectual property. The big test will be how China responds to such a move. Retaliatory measures by China and other countries have the potential to damage global trade, and thus, weaken the global economy.

Traders could be tempted to push the pair to such levels if President Trump, as expected, announces on Thursday, additional tariffs, this time targeting Chinese technology and telecommunications products, as well as intellectual property. The big test will be how China responds to such a move. Retaliatory measures by China and other countries have the potential to damage global trade, and thus, weaken the global economy.

It is of course possible that Trump’s actions have the intended effect and compel China to offer more favourable trade terms to US companies. In such a scenario, investors would likely breathe a sigh of relieve and much of the risk-off generated sell-off could be reversed. However, were Trump’s tactics to succeed in achieving a more favourable trading environment for US firms and alleviate the trade war fears, the dollar would likely appreciate under such conditions, offsetting some of the potential gains for commodity prices and commodity-linked currencies.

This only goes to highlight the many headwinds facing the commodities market in 2018. One thing traders should be able to take comfort from however is that in a worst-case scenario, the increasingly solid fundamentals of the global economy should help prevent any downtrend from spiralling out of control.

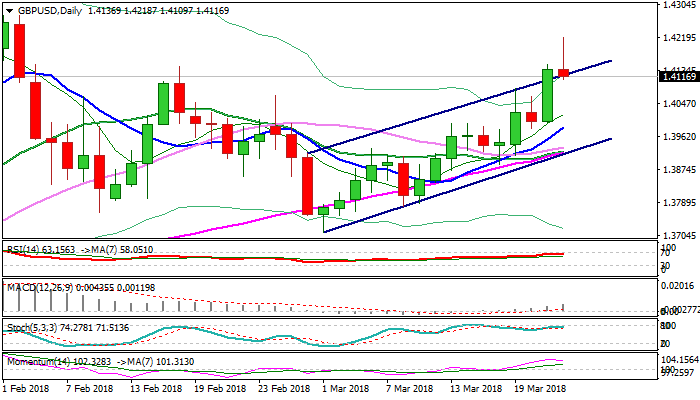

GBPUSD – Quick Pullback from Post-BoE Spike High Could form Negative Signal on Daily Chart

Sterling spiked to 1.4218, the highest since 02 Feb, after BoE kept interest rates unchanged on Thursday, but surprised markets by 7-2 voting results 9-0 expected, as two MPC members voted for rate hike.

New situation within policy makers improves the outlook, increasing hopes for central bank’s action as early as May.

Cable spiked in immediate reaction on BoE’s decision, but reversed gains on quick pullback which resulted in posting new daily low at 1.4112.

Strong upside rejection could be initial negative signal and could result in bearish daily candle with long upper shadow, which could increase risk of deeper pullback.

Another negative signal is forming on slow stochastic, where bearish divergence warns of further easing.

Profit-taking after strong gains in past couple of sessions could accelerate pullback, which currently probes below broken upper boundary of bull-channel and pressures supports at 1.4102/1.4092 (broken Fibo 61.8% of 1.4345/1.3711 descend/Fibo 38.2% of 1.3889/1.4218 upleg) .

Close below the latter would generate further negative signal for deeper correction and risk retest of psychological 1.40 support (former strong barrier).

Res: 1.4150; 1.4218; 1.4277; 1.4300

Sup: 1.4102; 1.4092; 1.4070; 1.4053

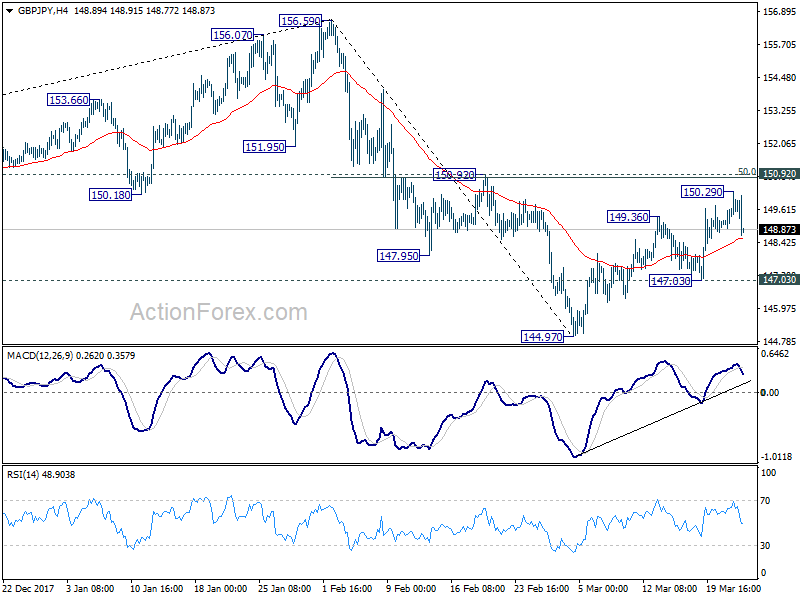

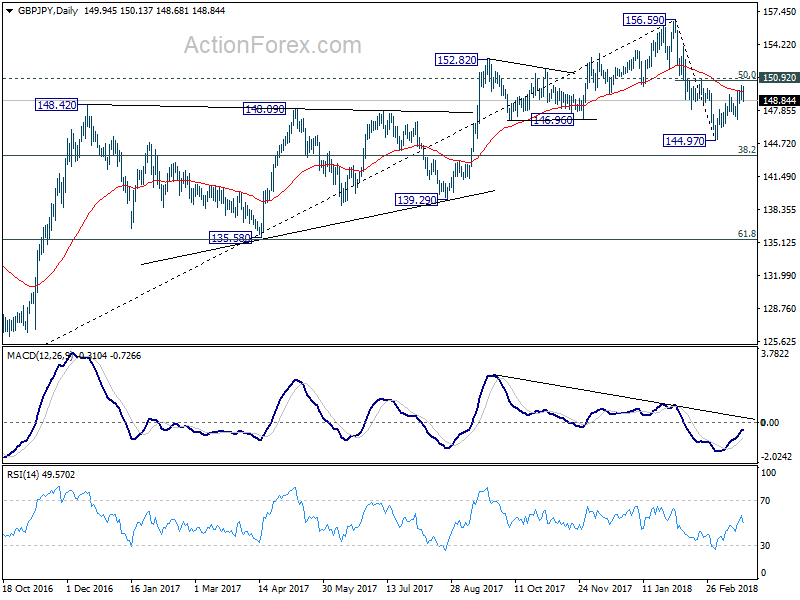

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.53; (P) 149.15; (R1) 149.75; More....

GBP/JPY drops sharply after hitting 150.29 but it's holding above 147.03 minor support so far. Intraday bias is neutral first. While another rise cannot be ruled out, we maintain the view that rebound from 144.97 is a corrective move. Therefore, strong resistance is expected from 150.92 (50% retracement of 156.59 to 144.97 at 150.78) to bring fall resumption. On the downside, below 147.03 will bring retest of 144.97 low first. Break will extend the decline from 156.59 to 143.51 medium term fibonacci level next. However, sustained break of 150.92 will pave the way back to retest 156.69 high.

In the bigger picture, the case for medium term reversal continues to build up. There is bearish divergence condition in daily MACD. 146.96 support was taken out. And GBP/JPY was rejected by 55 month EMA. Break of 38.2% retracement of 122.36 to 156.59 at 143.51 will pave the way to 61.8% retracement at 135.43 and below. This will now be the preferred case as long as 150.92 resistance holds.

Yen Steals the Show on Trade War Worries, Sterling Reversed after Brief BoE Spike

Sterling attempts to rally after BoE rate decisions but failed to sustain gain. On the other hand, Yen is quietly stealing the show on risk aversion. Investors are worried that the world is finally entering into the phase of trade war with US President Donald Trump's scheduled announce of tariffs against China. Australian Dollar remains the weakest one, for its tie with China, and as weighed down by weaker than expected job data. Euro follows as the second after a string of soft confidence indicators suggested that it's recent growth momentum has already peaked.

Trump to announce USD 50b tariffs against China, exempt EU from still tariffs

Trump is set to announce the tariffs on 100 different types of Chinese goods today, as follow up to the section 301 of the Trade Act of 1974 investigation. Bloomberg reported that the targeted amount would be at around USD 50b annually. White House official Raj Shah also said in a statement that "tomorrow the president will announce the actions he has decided to take based on USTR's 301 investigation into China's state-led, market-distorting efforts to force, pressure, and steal U.S. technologies and intellectual property." It's believed that the tariffs won't take effect immediately. And the list of targeted products will be finalized after industry input. But it's only confirmed when it's confirmed.

Jake Parker, vice president of China operations at the U.S.-China Business Council in Beijing, warned that "tariffs will do more harm than good in bringing about an improvement in intellectual property protection for American companies in China." And, he urged 'a focused effort to fix the problems is better than imposing sanctions that will bring collateral damage to American households, farmers, and manufacturers." Also, Parker questioned the purpose of the tariffs and asked "How will that fix the problem? What actions does the administration want China to take to improve IP protection and end forced technology transfer?" He hoped that Trump's administration will "spell this out".

Separately, EU has already secured temporary exception from the steel and aluminum tariffs. And Trump will announce it today to. That make us wonder, who else is still on the list?

Also from US, initial jobless claims rose 3k to 229k in the week ended March 17. Four-week moving average rose 2.25k to 223.75k. Continuing claims dropped -57k to 1.83m, lowest since December 1973. House price index rose 0.8% mom in January.

BoE stands pat, Brexit transition deal didn't change majority of MPC

BoE left bank rate unchanged at 0.50% and asset purchase target at GBP 435b as widely expected. Sterling initially spiked higher as known hawks Michael Saunders and Ian McCafferty dissented and voted for rate hike. These two have history of dissenting and pushing for tightening since last year. However, the Pound's strength was limited as apart from voting, today's announcement is not much different from the February's. Overall tone of the statement remained cautious. And, Brexit development was just briefly mentioned. The essential part regarding Brexit was totally unchanged. The was no acknowledgement of the Brexit transition deal.

Regarding the economic outlook, BoE maintained that the projected 1.75% GDP growth would be more than offset 1.5% supply growth. And small margin of excess demand was projected to emerge by early 2020. And that would push up domestic costs. Thus, "inflation remained above the 2% target in the second and third years of the MPC's central projection." BoE added that "ongoing tightening of monetary policy over the forecast period will be appropriate to return inflation sustainably to its target at a more conventional horizon." This suggests that it's more confident regarding tightening ahead. But BoE reiterated cautious that "any future increases in Bank Rate are likely to be at a gradual pace and to a limited extent.

Hence, Brexit development just unlocked the two known hawks out of the cage. But it didn't make BoE more likely to hike in May.

Also from UK, retail sales rose 0.8% mom in February, higher than expectation of 0.4% mom.

Eurozone PMI composite at 14-month low, Euro strengthen weighed on exports

Eurozone PMIs released today are generally disappointing. Eurozone PMI manufacturing dropped to 56.6 in March , down from 58.6, below expectation of 58.1. That's lowest in 8 months. Eurozone PMI services dropped to 55.0, down from 56.2, below expectation of 56.0. That's lowest in 5 months. Eurozone PMI composite dropped to 55.3 down from 57.1, lowest in 14 month.

Markit Chief Business Economist Chris Williamson noted in the statement that " the loss of momentum since the buoyant start to the year has been quite dramatic." One key factor is the strength in Euro which took an "increasing toll on export performance". Political uncertainty also "appears to have intensified, dampening demand".

After all, the average PMI readings still suggests 0.7-0.8% GDP growth in Eurozone in Q1. But Eurozone growth " peaked around the turn of the year and the region is settling into a slower, but still robust pace of expansion."

Meanwhile, German PMI manufacturing dropped to 58.4 in March, down from 60.6, below expectation of 59.8. That's an 8-month low. German PMI services dropped to 54.2 in March, down from 55.3 and missed expectation of 55.0. That's a 7-month low. France PMI manufacturing dropped to sharply to 53.6 in March, down from 55.9 and missed expectation of 55.6. France PMI services dropped to 56.8, down from 57.4 and missed expectation of 57.0.

German Ifo: Threat of protectionism dampened mood in the economy

Also from Eurozone, German Ifo business climate dropped to 114.7 in March, down from 115.4, slightly above expectation of 114.6. Ifo expectation dropped to 104.4, down from 105.4, met consensus. Ifo current assessment dropped to 125.9, down from 126.3, above expectation of 125.6. Ifo economist Klaus Wohlrabe "the protectionism debate is leaving its mark." And therefore, "export expectations have fallen to their lowest levels in more than a year." Ifo president Clemens Fuest also echoed that "the threat of protectionism is dampening the mood in the German economy."

Japan PMI manufacturing signalled weaker improvements in business conditions

Japan PMI manufacturing dropped to 53.2 in March, down from 54.1 and missed expectation of 54.3. Markit economist Joe Hayes noted in the release that the data signalled a "weaker improvement in overall business conditions in the manufacturing sector". In particular, output, new order and employment growth slowed. Nonetheless, new business grew for an eighteenth straight month. And businesses raised output prices in quicker pace. These are seen as "confidence in the demand climate and purchasing power of their clients".

Also from Japan all industry activity index dropped -1.8% mom in January.

Economists pushed back expectation on timing of BoJ exit

According to a Reuters poll in March 12-20, economists are pushing back their expectation on the timing of BoJ stimulus exit, due to Yen's appreciation and BoJ Governor Haruhiko Kuroda's recent cautious comments. 37 of 41 economists expected BoJ's next move to be exit but 4 expects further easing. The median of economists expect BoJ to keep interest rate at -0.1% and target JGB yield at zero at least till the end of 2019. 13 economists expected BoJ to taper asset purchases in the first half of 2019. 7 economists expected it to happy in the second half of 2019. 11 economists said tapering will only start sometime in 2020 or later.

RBNZ stands pat, Spencer said NZD in vicinity of fair value

NZD is relatively steady after RBNZ kept OCR unchanged at 1.75% as widely expected, and maintained a dovish stance. Outgoing Acting Governor Grant Spencer gave an interview before handing over to Adrian Orr. He noted that RBNZ shouldn't comment on NZD's exchange rate. And, he emphasized that "we should only comment on the currency if it's really pretty clear that it's out of alignment and you're wanting to have some impact, some sort of jaw-boning effect". Though, he acknowledged that "in the past we have got into this situation where we sort of had to make a statement about the currency and if we didn't the market was going to react." But then, he also said that NZD is "in the vicinity of fair value".

In the accompany statement, RBNZ maintained that "monetary policy will remain accommodative for a considerable period." It said, "inflation is expected to weaken further in the near term", before heading up to 2% target "over the medium term". And, "tradeable inflation is projected to remain subdued through the forecast period." At the same time, "non-tradables inflation is moderate but is expected to increase in line with a rise in capacity pressure." Regarding the economy, "growth is expected to strengthen, supported by accommodative monetary policy, a high terms of trade, government spending and population growth."

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.53; (P) 149.15; (R1) 149.75; More....

GBP/JPY drops sharply after hitting 150.29 but it's holding above 147.03 minor support so far. Intraday bias is neutral first. While another rise cannot be ruled out, we maintain the view that rebound from 144.97 is a corrective move. Therefore, strong resistance is expected from 150.92 (50% retracement of 156.59 to 144.97 at 150.78) to bring fall resumption. On the downside, below 147.03 will bring retest of 144.97 low first. Break will extend the decline from 156.59 to 143.51 medium term fibonacci level next. However, sustained break of 150.92 will pave the way back to retest 156.69 high.

In the bigger picture, the case for medium term reversal continues to build up. There is bearish divergence condition in daily MACD. 146.96 support was taken out. And GBP/JPY was rejected by 55 month EMA. Break of 38.2% retracement of 122.36 to 156.59 at 143.51 will pave the way to 61.8% retracement at 135.43 and below. This will now be the preferred case as long as 150.92 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 20:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% | 1.75% | |

| 00:30 | AUD | Employment Change Feb | 17.5K | 20.3K | 16.0K | 12.5K |

| 00:30 | AUD | Unemployment Rate Feb | 5.60% | 5.50% | 5.50% | |

| 00:30 | JPY | PMI Manufacturing Mar P | 53.2 | 54.3 | 54.1 | |

| 04:30 | JPY | All Industry Activity Index M/M Jan | -1.80% | -1.80% | 0.50% | 0.60% |

| 08:00 | EUR | France Manufacturing PMI Mar P | 54.2 | 55.5 | 55.9 | |

| 08:00 | EUR | France Services PMI Mar P | 56.8 | 57 | 57.4 | |

| 08:30 | EUR | Germany Manufacturing PMI Mar P | 58.4 | 59.8 | 60.6 | |

| 08:30 | EUR | Germany Services PMI Mar P | 54.2 | 55 | 55.3 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Mar P | 56.6 | 58.1 | 58.6 | |

| 09:00 | EUR | Eurozone Services PMI Mar P | 55 | 56 | 56.2 | |

| 09:00 | EUR | Eurozone Current Account (EUR) Jan | 37.6B | 30.2B | 29.9B | 31.0B |

| 09:00 | EUR | German IFO Business Climate Mar | 114.7 | 114.6 | 115.4 | |

| 09:00 | EUR | German IFO Expectations Mar | 104.4 | 104.4 | 105.4 | |

| 09:00 | EUR | German IFO Current Assessment Mar | 125.9 | 125.6 | 126.3 | |

| 09:00 | EUR | ECB Economic Bulletin | ||||

| 09:30 | GBP | Retail Sales M/M Feb | 0.80% | 0.40% | 0.10% | -0.20% |

| 12:00 | GBP | BoE Rate Decision | 0.50% | 0.50% | 0.50% | |

| 12:00 | GBP | BoE Asset Purchase Target Mar | 435B | 435B | 435B | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 2--0--7 | 0--0--9 | 0--0--9 | |

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0--0--9 | 0--0--9 | 0--0--9 | |

| 12:30 | USD | Initial Jobless Claims (MAR 17) | 229K | 225K | 226K | |

| 13:00 | USD | House Price Index M/M Jan | 0.80% | 0.40% | 0.30% | 0.40% |

| 13:45 | USD | US Manufacturing PMI Mar P | 55.7 | 55.5 | 55.3 | |

| 13:45 | USD | US Services PMI Mar P | 54.1 | 56 | 55.9 | |

| 14:00 | USD | Leading Index Feb | 0.60% | 0.50% | 1.00% | |

| 14:30 | USD | Natural Gas Storage | -88B | -93B |

BOE Voted 7-2 to Leave Bank Rate Unchanged at 0.50%

BOE voted 7-2 to leave the Bank rate at 0.50%. The members voted unanimously to leave to asset purchase program unchanged at 435B pound. The members were generally positive over the economic outlook, noting that "recent data releases are broadly consistent with the MPC's view of the medium-term outlook as set out in the February Inflation Report". Wage growth has been in line with BOE's expectations. This has raised the confidence that "growth in wages and unit labour costs would pick up to target-consistent rates". Sterling jumped initially after the announcement with GBPUSD rising to a 7-week high of 1.4216. Gains were pared shortly. The market has priced in over 60% chance of a +25 bps rate hike in May.

The direction of the monetary policy decision is up. As mentioned in the minutes, "given the prospect of excess demand over the forecast period, an ongoing tightening of monetary policy over the forecast period would be appropriate to return inflation sustainably to its target at a more conventional horizon". The members agreed that the pace of rate hikes would be gradual and to a limited extent. As noted in the minutes, "the best collective judgment of the MPC remained that, given the prospect of excess demand over the forecast period, an ongoing tightening of monetary policy over the forecast period would be appropriate".

For the majority of the members who favored keeping the powder this month, they prefer to wait for more information before another move. As noted in the minutes, they acknowledged that there were "surprises in recent economic data and the February Inflation Report projections, conditioned on a gently rising path of Bank Rate, had appeared broadly on track". Yet, they added that "the May forecast round would enable the Committee to undertake a fuller assessment of the underlying momentum in the economy, the degree of slack remaining and the extent of domestic inflationary pressures".

For the two dissents, Ian McCafferty and Michael Saunders, who opted for a hike this month, they believed that "slack was largely used up and that pay growth was picking up, presenting upside risks to inflation in the medium term. A modest tightening of monetary policy at this meeting could mitigate the risks from a more sustained period of above-target inflation that might ultimately necessitate a more abrupt change in policy and hence a greater adjustment in growth and employment".

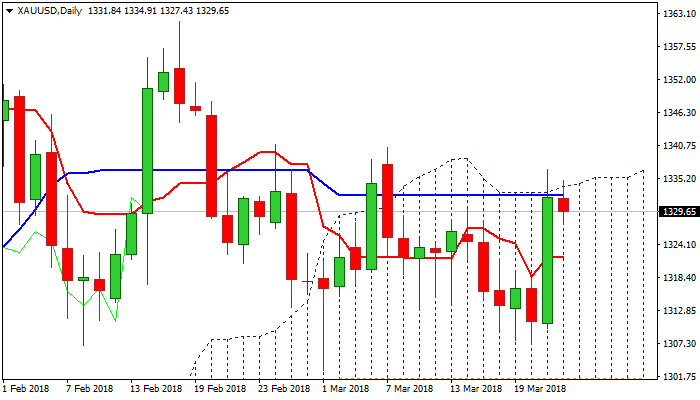

SPOT GOLD – Outlook Remains Bullish But Daily Cloud Top Limits Advance for Now

Spot Gold consolidates under new two-week high at $1336, after rallying strongly on Wednesday on less hawkish than expected Fed which hit the greenback. The yellow metal was additionally supported by growing concerns about trade war which increased demand for safe-haven assets.

Wednesday’s rally surged through strong $1320/29 resistance zone, provided by a cluster of MA’s, but faced strong headwinds from top of daily cloud ($1334) which was repeatedly dented but without clear break higher so far.

Current action so far looks as consolidation before final push through cloud top and extension towards next target at $1340 (07 Mar high).

Daily techs remain in full bullish configuration and supportive for further advance, as trade war fears underpin.

Alternative scenario requires return and close below $1320 to weaken near-term structure and risk further weakness.

Res: 1334; 1336; 1340; 1345

Sup: 1327; 1323; 1321; 1315

Canadian Dollar Rally Continues on NAFTA Optimism

The Canadian dollar continues to gain ground, and has inched higher in the Thursday session. Currently, USD/CAD is trading at 1.2894, down 0.08% on the day. On the release front, there are no Canadian data releases. In the US, unemployment claims rose to 229 thousand, higher than the forecast of 225 thousand. On Friday, the US releases durable goods and housing reports.

It’s been a good week for the Canadian dollar, which has gained 1.6 percent against the greenback. This has erased most of last week’s losses. There has been some good news on the NAFTA front, as the US appears to have softened its rigid negotiation position. The US had demanded far-reaching concessions from Canada and Mexico, threatening to withdraw from NAFTA if its demands were not met. NAFTA is critically important for the Canadian economy, and the specter of the free-trade agreement being cancelled has weighed on the Canadian dollar for months. However, there was good news this week as US has dropped its demand that vehicles produced in Canada or Mexico that are destined to the US, contain a minimum of 50% US content.This demand was one of the key sticking points in the negotiations, and its removal should speed up talks on the renegotiated NAFTA agreement. Another scare for Canadian policymakers was the US decision to slap tariffs on steel and aluminum products, as Canada is the largest exporter of steel to the US. Canada avoided a bullet as President Trump announced that the Canada and Mexico would be exempt from the tariffs, at least temporarily.

As widely expected, the Federal Reserve raised rates by a quarter-point on Wednesday, bringing the benchmark rate to a range between 1.50% and 1.75%. The markets were looking for any clues with regard to the pace of rate hikes in 2018 – currently the Fed is projecting three hikes, but a robust US economy could push the Fed to press the rate trigger four times. The rate statement did not directly address the issue, but there was a refreshing lack of Fedspeak from policymakers, who said that “the economic outlook has strengthened in recent months”. This phrase has not been used in previous rate statements, and if Fed policymakers reiterate positive sentiment towards the economy, could push the US dollar to higher ground.