Sample Category Title

Global Markets Crash, Yen Surge as US-China Trade War Starts

US stocks tumbled sharply in the final hour of trading overnight, taking out key support levels in the wake of the start of US-China trade war. DOW closed sharply lower by -724.42 pts or -2.93% at 23957.89 overnight as fear of trade war intensified. S&P 500 was down -68.24 pts or -2.52% at 2643.69. NASDAQ also dropped -178.61pts or -2.43% to 7166.68. Selling continues in Asia with Nikkei trading down -4.4%, or near -950 pts at the time of writing. Hong Kong HSI is also losing -3% or over -900 pts.

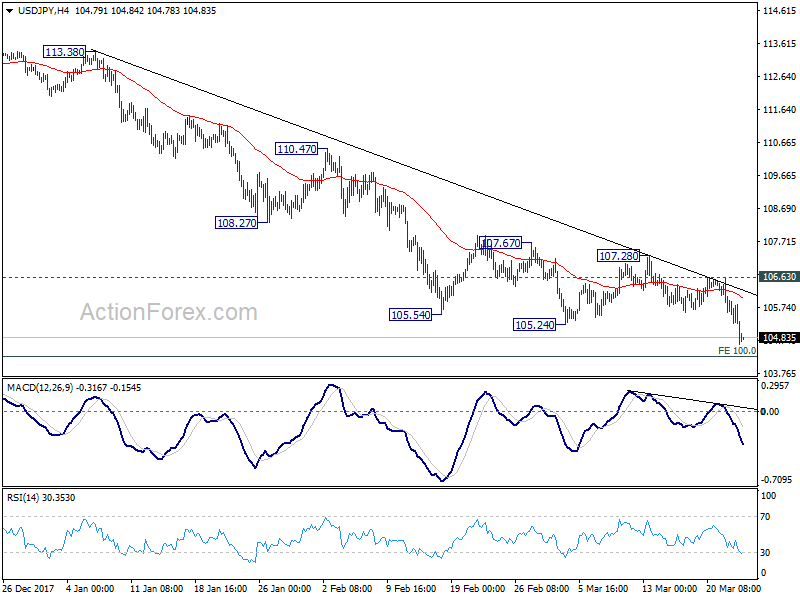

In the currency markets, Dollar is under broad based selling pressure and is trading all in red against others for the day and the week. Yen rides of strong risk aversion and is trading as the strongest one since yesterday. In particular, USD/JPY's firm break of 105.24 support now open up the case through 100 handle.

US-China trade war starts

Trump announced tariffs on USD 50-60b of annual imports from China. He noted that "this is the first of many". The White House added that it was also seeking to impose new investment restrictions on Chinese companies. Initial reaction was muted as what was announced was a big difference to rumor of USD 50b in tariffs. Nonetheless, the selloff in stocks and rally in Yen picked up momentum in the last trading hour, as traders dumped their position ahead of China's retaliation measures.

In Asian session, China's Ministry of Commerce announced measures countering US tariffs. But it should be noted that these measures are in response to Trump's steel and aluminum tariffs, not the USD 50b section 301 tariffs announced overnight. China also said it could take legal action regarding the steel tariffs under WTO rules. So far, it appears that China is trying to play by the book.

The MOFCOM proposed a list of 128 US imports with total value at over USD 3b in 2017. A 15% tariff will be imposed on the first group including wines, fresh fruit, dried fruit and nuts, steel pipes, modified ethanol, and ginseng. Then a 25% tariff could be imposed on the second group, including pork and recycled aluminium goods if both sides failed to reach a resolution through talks.

Trump exempted over 50% of steel imports from tariffs, but not Japan nor Taiwan

Separately, Trump also announced temporary suspension to the steel and aluminum tariffs, until May 1, 2018. The final result will depend on the discussions outcome. The countries that are temporarily exempted include Argentina, Australia, Brazil, Canada, Mexico, EU and South Korea.

According to Wood Mackenzie data, in 2017, the top 10 steel importer to US are Canada (16.7%), Brazil (13.2%), South Korea (9.7%), Mexico (9.4%), Russia (8.1%), Turkey (5.6%), Japan (4.9%), Germany (3.7%), Taiwan (3.2%), China (2.9%).

The total contribution of the exempted countries is 52.7%. Meanwhile, two notable absentees are Japan and Taiwan. Japanese's request for exemption seemed to have fallen on deaf ears. Both Japan and Taiwan are seen by many as the closest allies of the US in the far east.

Japan CPI core hit 1% for the first time since 2014

Japan national CPI core accelerated to 1.0% yoy in February, up from 0.9% yoy and met expectation. That's also the first time it hits 1% level since August 2014. The so called core-core CPI, CPI excluding fresh food and energy, rose to 0.5% yoy.

Newly appointed BoJ deputy governor Masazumi Wakatabe said in the parliament that the reading, especially the core-core CPI, showed that Japanese inflation expectation remain weak. He noted that "when compared to the United States or Europe, gains in Japan's core-core CPI are insufficient." He added that "what we can learn from this is that people still don't believe inflation will reach 2 percent." And, "inflation expectations are not anchored."

And he pledged to "maintain the regime and stance we have in place for monetary policy to meet 2 percent inflation and to strengthen it if possible."

BoE voted 7-2 to leave bank rate unchanged yesterday

While Sterling pared back much again after BoE rate decision yesterday, it's still among the strongest ones for the week. BOE voted 7-2 to leave the Bank rate at 0.50%. For the two dissents, Ian McCafferty and Michael Saunders, who opted for a hike this month, they believed that "slack was largely used up and that pay growth was picking up, presenting upside risks to inflation in the medium term. A modest tightening of monetary policy at this meeting could mitigate the risks from a more sustained period of above-target inflation that might ultimately necessitate a more abrupt change in policy and hence a greater adjustment in growth and employment". More in BOE Voted 7-2 to Leave Bank Rate Unchanged at 0.50%

Suggested reading on BoE: BoE Still on Track for a May Hike

Looking ahead

Canada CPI and retail sales will be the main focus today. Canadian Dollar has been strong this week on optimism over NAFTA renegotiation. But more is needed to solidify bullish momentum. US will also release durable goods orders and new home sales.

USD/JPY Daily Outlook

Daily Pivots: (S1) 104.99; (P) 105.53; (R1) 105.82; More...

USD/JPY dives to as low as 104.63 so far as decline accelerates. Firm break of 105.24 support confirms resumption of decline from 114.73. Such fall is part of the whole pattern from 118.65. Intraday bias now stays on the downside for 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. Sustained break there will pave the way to 98.97 (2016 low). On the upside, break of 106.63 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

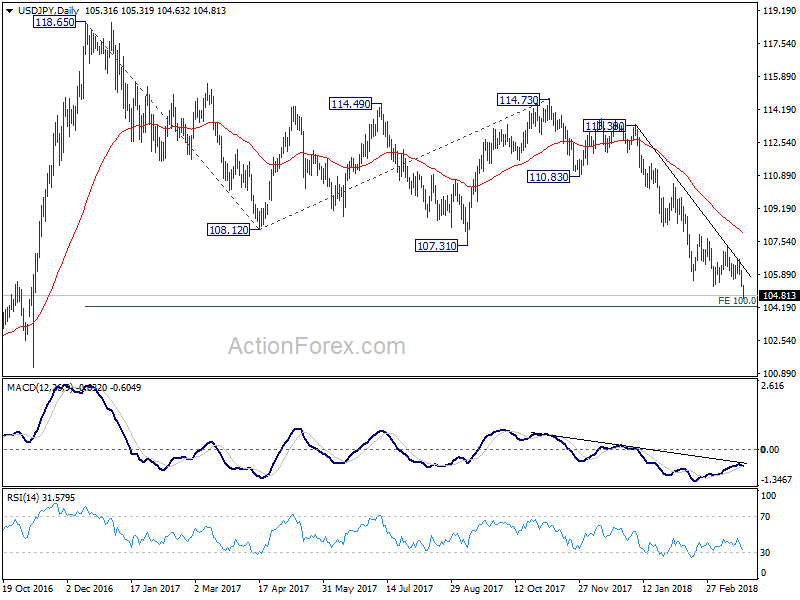

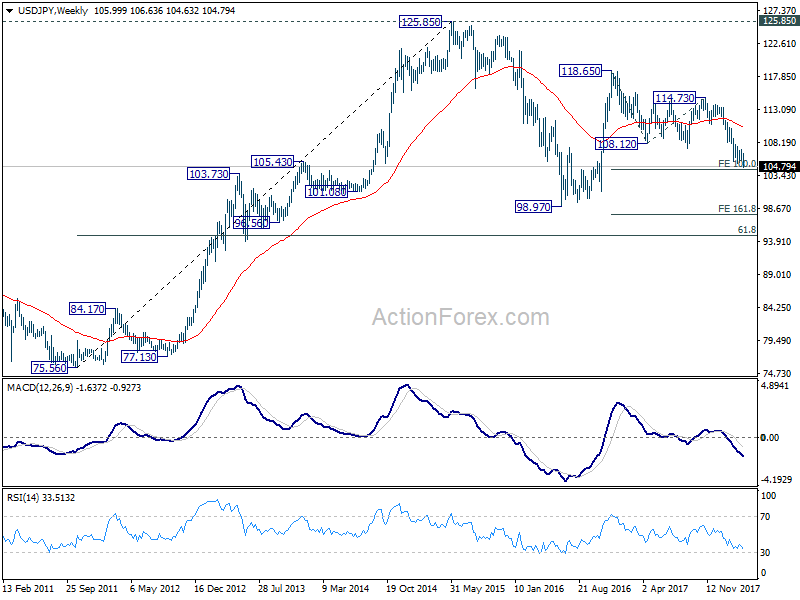

In the bigger picture, medium term down trend from 118.65 2016 high is still in progress and extending. Build up in downside momentum argues that it might be extending the whole corrective pattern from 125.85 (2015 high). 100% projection of 118.65 to 108.12 from 114.73 at 104.20 will be a key level to watch as firm break there could bring downside acceleration. And in that case, 98.97 key support level (2016 low) would at least be breached. This bearish case will now be favored as long as 108.12 support turned resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Feb | 1.00% | 1.00% | 0.90% | |

| 12:00 | GBP | BoE Quarterly Bulletin | ||||

| 12:30 | CAD | CPI M/M Feb | 0.50% | 0.70% | ||

| 12:30 | CAD | CPI Y/Y Feb | 2.00% | 1.70% | ||

| 12:30 | CAD | CPI Core Common Y/Y Feb | 1.90% | 1.80% | ||

| 12:30 | CAD | CPI Core - Median Y/Y Feb | 1.90% | |||

| 12:30 | CAD | CPI Core - Trim Y/Y Feb | 1.80% | |||

| 12:30 | CAD | Retail Sales M/M Jan | 1.20% | -0.80% | ||

| 12:30 | CAD | Retail Sales Ex Auto M/M Jan | 0.90% | -1.80% | ||

| 12:30 | USD | Durable Goods Orders Feb P | 1.70% | -3.60% | ||

| 12:30 | USD | Durables Ex Transportation Feb P | 0.50% | -0.30% | ||

| 14:00 | USD | New Home Sales Feb | 621K | 593K |

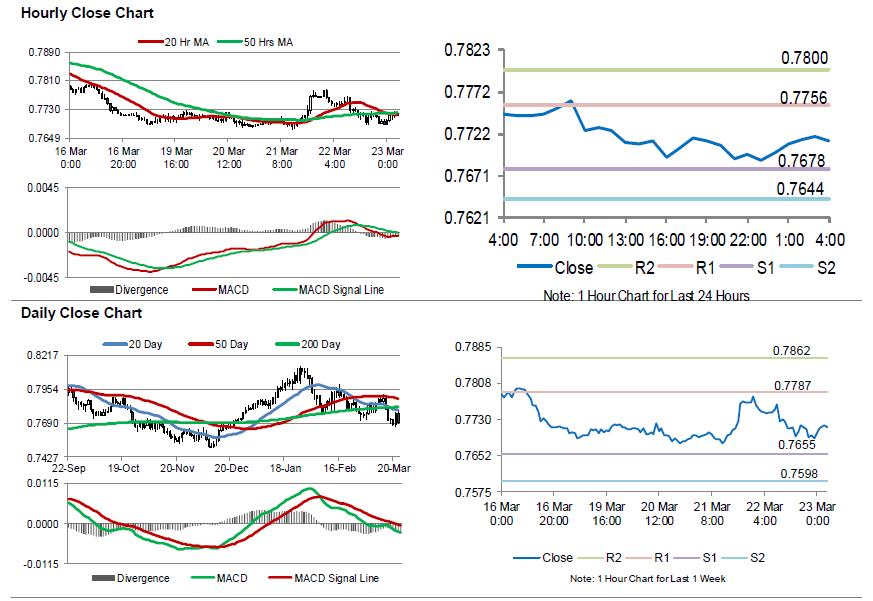

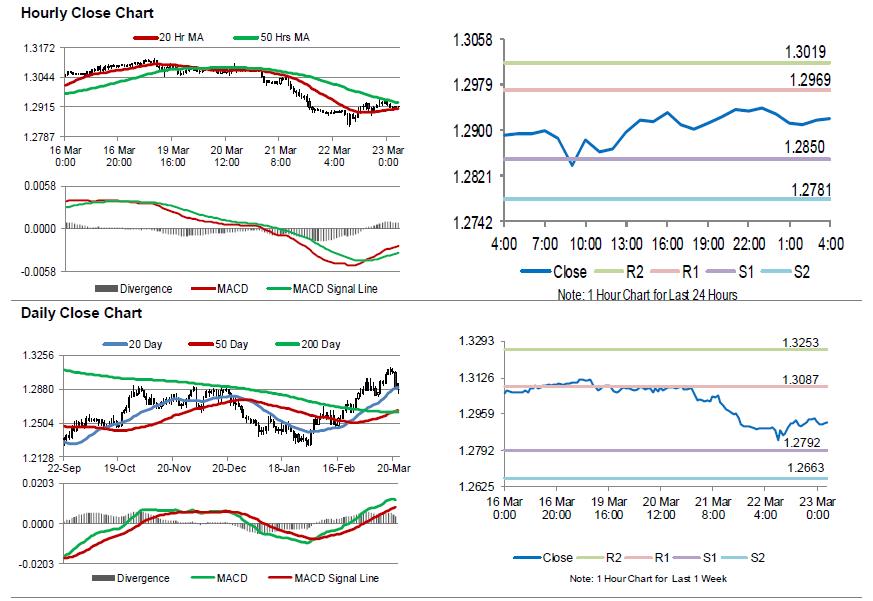

Aussie Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the AUD declined 0.75% against the USD and closed at 0.7689.

LME Copper prices declined 0.1% or $8.5/MT to $6746.5/MT. Aluminium prices declined 3.9% or $83.0/MT to $2059.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7713, with the AUD trading 0.31% higher against the USD from yesterday’s close.

The pair is expected to find support at 0.7678, and a fall through could take it to the next support level of 0.7644. The pair is expected to find its first resistance at 0.7756, and a rise through could take it to the next resistance level of 0.7800.

Going ahead, investors would eye Australia’s private sector credit data for February, the sole macroeconomic release next week.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Manufacturing Sector Growth Cooled To An 8-Month Low In March, While Services Sector Activity Eased To A 5-Month...

For the 24 hours to 23:00 GMT, the EUR declined 0.35% against the USD and closed at 1.2317, after the latest set of economic releases pointed to a moderation in economic activity across the Euro-zone.

Data revealed that the Euro-zone's flash Markit manufacturing PMI eased to a level of 56.6 in March, hitting its lowest level in 8 months. The PMI had registered a level of 58.6 in the prior month, while markets were expecting for a drop to a level of 58.1. Further, the region's preliminary Markit services PMI fell to a 5-month low level of 55.0 in March, more than market consensus for a drop to a level of 56.0. The PMI had registered a level of 56.2 in the prior month.

Separately, activity in Germany's manufacturing sector slowed more-than-expected to a level of 58.4 in March, touching its lowest level since July 2017. Market participants had envisaged the PMI to fall to a level of 59.8, after recording a reading of 60.6 in the previous month. Moreover, growth in the nation's services sector dropped to a level of 54.2 in March, expanding at its weakest pace in 7 months. The PMI had registered a reading of 55.3 in the previous month, while markets were expecting it to ease to a level of 55.0.

Another set of economic data revealed that Germany's Ifo business climate index declined to a level of 114.7 in March, less than market expectations for a fall to a level of 114.6. The index had recorded a reading of 115.4 in the prior month. Moreover, the nation's Ifo business expectations index dipped to a level of 104.4 in March, in line with market expectations. In the prior month, the index had registered a level of 105.4.

Macroeconomic data released in the US indicated that the flash Markit manufacturing PMI rose to a level of 55.7 in March, exceeding market expectations for a rise to a level of 55.5 and notching its highest level since March 2015. The PMI had registered a level of 55.3 in the previous month. On the other hand, the nation's flash Markit services PMI unexpectedly eased to a level of 54.1 in March, defying market expectations for an advance to a level of 56.0. In the previous month, the PMI had registered a reading of 55.9.

In other economic news, the US initial jobless claims recorded an unexpected rise to a level of 229.0K in the week ended 17 March, confounding market expectations for a fall to a level of 225.0K. Initial jobless claims had registered a level of 226.0K in the previous week. Meanwhile, the nation's leading indicator advanced 0.6% in February, compared to a revised gain of 0.8% in the previous month, while markets had envisaged for a rise of 0.5%.

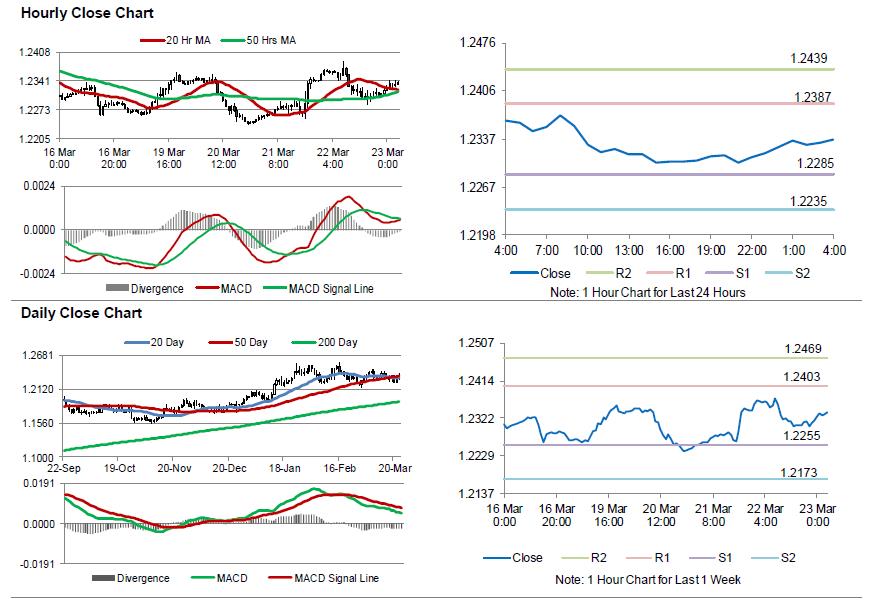

In the Asian session, at GMT0400, the pair is trading at 1.2336, with the EUR trading 0.15% higher against the USD from yesterday's close.

The pair is expected to find support at 1.2285, and a fall through could take it to the next support level of 1.2235. The pair is expected to find its first resistance at 1.2387, and a rise through could take it to the next resistance level of 1.2439.

Amid no macroeconomic releases in the Euro-zone today, investors would focus on the US flash durable goods orders and new home sales data, both for February, set to release later in the day.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

BoE Holds Interest Rate At 0.50%, Hints At May Rate Hike

For the 24 hours to 23:00 GMT, the GBP declined 0.39% against the USD and closed at 1.4105, after the Bank of England (BoE) reiterated that any future interest rate hikes would be gradual and limited.

The BoE, at its March monetary policy meeting, opted to keep the benchmark interest rate steady at 0.50% and its asset purchase facility at £435.0 billion, with two officials surprisingly voting for an immediate rate hike. The minutes of the meeting revealed that policymakers expressed the need for further gradual monetary policy tightening in order to bring inflation back to the central bank’s 2.00% target. Further, the central bank warned that an increase in protectionism could have a “significant negative impact” on global growth and could stoke inflation.

On the macro front, UK’s retail sales rose 0.8% on a monthly basis in February, topping market expectations for an advance of 0.4%. Retail sales had recorded a rise of 0.1% in the previous month.

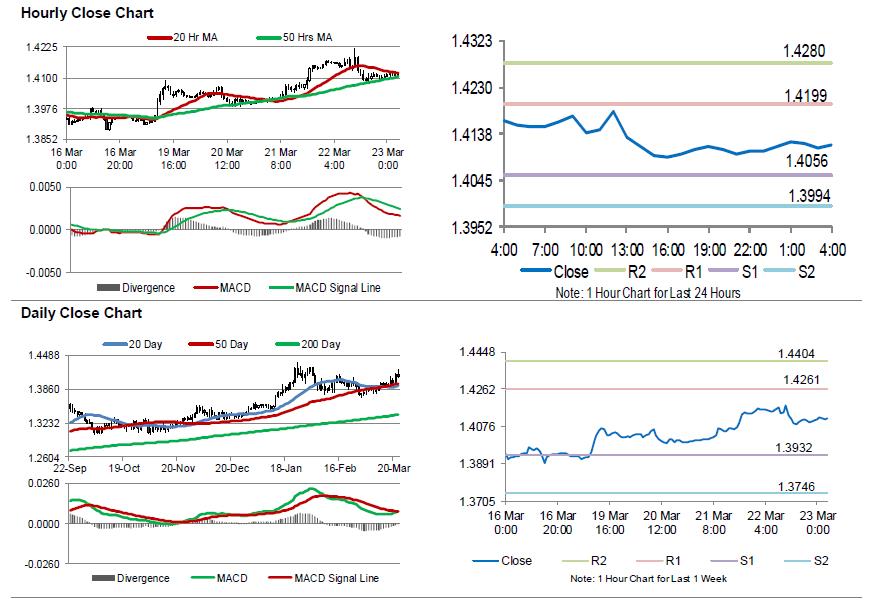

In the Asian session, at GMT0400, the pair is trading at 1.4117, with the GBP trading 0.09% higher against the USD from yesterday’s close.

The pair is expected to find support at 1.4056, and a fall through could take it to the next support level of 1.3994. The pair is expected to find its first resistance at 1.4199, and a rise through could take it to the next resistance level of 1.4280.

With no macroeconomic releases in UK today, investors would await the release of UK’s final 4Q GDP numbers, GfK consumer confidence index, mortgage approvals and net consumer credit data, all slated to release next week.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Japan’s Annual Inflation Advanced As Expected In February

For the 24 hours to 23:00 GMT, the USD declined 0.8% against the JPY and closed at 104.88.

The Japanese Yen gained ground against the USD, as investors piled into safe haven currency, after the US President, Donald Trump signed a $50.0 billion in trade tariffs on Chinese imports, thus sparking fresh fears of a trade war between the world's two biggest economies.

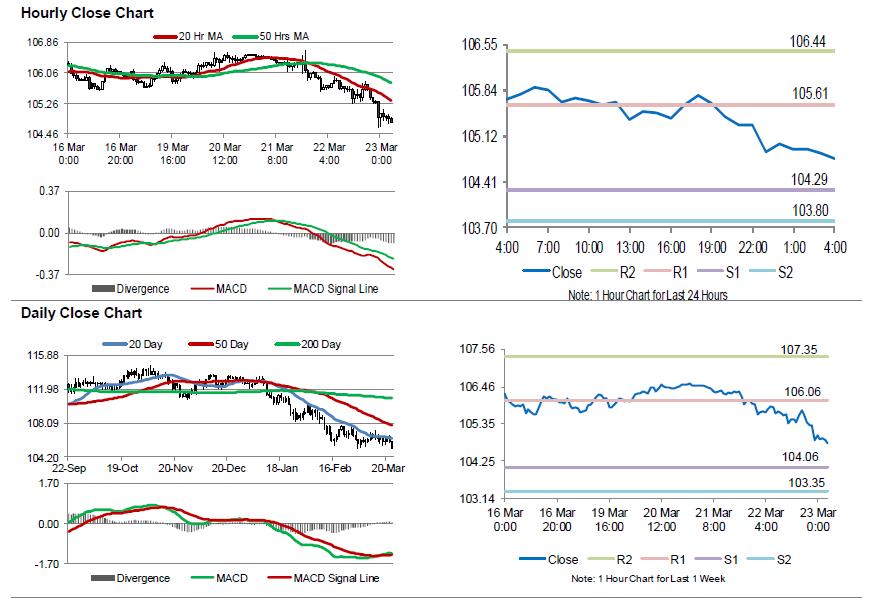

In the Asian session, at GMT0400, the pair is trading at 104.77, with the USD trading 0.1% lower against the JPY from yesterday's close.

Data released overnight showed that Japan's national consumer price index (CPI) rose 1.5% on an annual basis in February, in line with market expectations. In the previous month, the CPI had risen 1.4%.

The pair is expected to find support at 104.29, and a fall through could take it to the next support level of 103.80. The pair is expected to find its first resistance at 105.61, and a rise through could take it to the next resistance level of 106.44.

Next week, Japan's jobless rate, industrial production, retail trade and large retailers' sales data, all scheduled to release next week, will be on investors' radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD marginally declined against the CHF and closed at 0.9478.

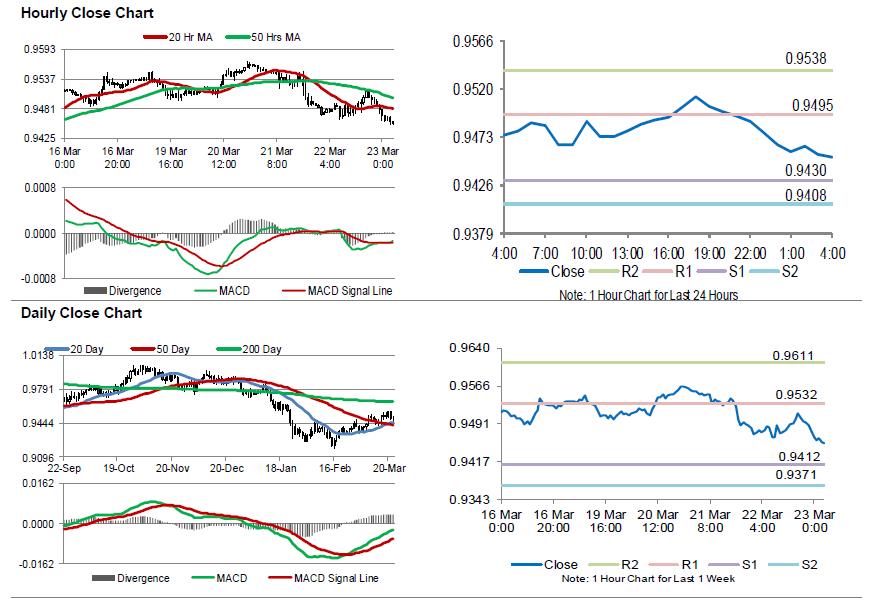

In the Asian session, at GMT0400, the pair is trading at 0.9453, with the USD trading 0.26% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.943, and a fall through could take it to the next support level of 0.9408. The pair is expected to find its first resistance at 0.9495, and a rise through could take it to the next resistance level of 0.9538.

Looking forward, investors would keep a close watch on Switzerland’s ZEW expectations index and KOF leading indicator data, both due to release next week.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Loonie Reverses Its Losses In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.34% against the CAD and closed at 1.2938.

In the Asian session, at GMT0400, the pair is trading at 1.2920, with the USD trading 0.14% lower against CAD from yesterday’s close.

The pair is expected to find support at 1.2850, and a fall through could take it to the next support level of 1.2781. The pair is expected to find its first resistance at 1.2969, and a rise through could take it to the next resistance level of 1.3019.

Later today, traders would closely monitor Canada’s consumer price inflation for February and retail sales data for January.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

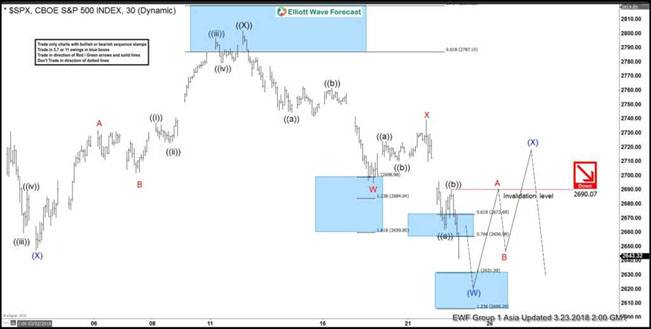

Elliott Wave Analysis: SPX Should See More Weakness

SPX rally to 2801.9 on 3.13.2018 ended Primary wave ((X)). Since then, the decline from there is unfolding as a double three Elliott Wave structure where Minor wave W ended at 2694.59 and Minor wave X ended at 2739.14. A double three is a WXY structure where the subdivision of each leg is corrective. Subdivision of Minor wave W unfolded as a zigzag Elliott Wave structure where Minute wave ((a)) ended at 2744.38, Minute wave ((b)) ended at 2761.85, and Minute wave ((c)) of W ended at 2694.59. Subdivision of Minor wave X unfolded as another zigzag where Minute wave ((a)) ended at 2724.22, Minute wave ((b)) ended at 2710.05, and Minute wave ((c)) of X ended at 2739.14.

Minor wave Y is currently in progress as a zigzag Elliott Wave structure where Minute wave ((a)) ended at 2661.78 and Minute wave ((b)) ended at 2690.07. Near term focus is on 2606.2 – 2631.59 area to complete Minute wave ((c)) of Y. The next move lower also should complete Intermediate wave (W) of higher degree and end cycle from 3.13.2018 high. Index should then bounce in Intermediate wave (X) to correct cycle from 3.13.2018 high in 3, 7, or 11 swing before the decline resumes.

SPX 1 Hour Elliott Wave Chart

Japan CPI core hit 1% for first time since 2014, BoJ Wakatabe said “inflation expectations are not anchored”

Japan national CPI core accelerated to 1.0% yoy in February, up from 0.9% yoy and met expectation. That's also the first time it hits 1% level since August 2014. The so called core-core CPI, CPI excluding fresh food and energy, rose to 0.5% yoy.

Newly appointed BoJ deputy governor Masazumi Wakatabe said in the parliament that the reading, especially the core-core CPI, showed that Japanese inflation expectation remain weak. He noted that "when compared to the United States or Europe, gains in Japan's core-core CPI are insufficient." He added that "what we can learn from this is that people still don't believe inflation will reach 2 percent." And, "inflation expectations are not anchored."

And he pledged to "maintain the regime and stance we have in place for monetary policy to meet 2 percent inflation and to strengthen it if possible."

Trump exempted over 50% of steel imports from tariffs, but not Japan nor Taiwan

Trump also announced temporary suspension to the steel and aluminum tariffs, until May 1, 2018. The final result will depend on the discussions outcome. The countries that are temporarily exempted include Argentina, Australia, Brazil, Canada, Mexico, EU and South Korea.

According to Wood Mackenzie data, in 2017, the top 10 steel importer to US are Canada (16.7%), Brazil (13.2%), South Korea (9.7%), Mexico (9.4%), Russia (8.1%), Turkey (5.6%), Japan (4.9%), Germany (3.7%), Taiwan (3.2%), China (2.9%).

The total contribution of the exempted countries is 52.7%!

Like some said, this is more political drama than anything as Trump announced a tariff and more than 50% is exempted.

Meanwhile, two notable absentees are Japan and Taiwan. Japanese's request for exemption seemed to have fallen on deaf ears. Both Japan and Taiwan are seen by many as the closest allies of the US in the far east.

Here is the statement:

President Trump Approves Section 232 Tariff Modifications

WASHINGTON - Today, based on ongoing dialogues, President Donald J. Trump authorized the modification of the Section 232 tariffs on steel and aluminum imports to suspend the tariffs for certain countries before they take effect. These suspensions are based on factors including ongoing discussions regarding measures to reduce global excess capacity in steel and aluminum production by addressing its root causes.

The tariffs on steel and aluminum imports from the following countries are suspended until May 1, 2018, pending discussions of satisfactory long-term alternative means to address the threatened impairment to U.S. national security:

Argentina;

Australia;

Brazil;

Canada;

Mexico;

the member countries of the European Union; and

South Korea.

By May 1, 2018, the President will decide whether to continue to exempt these countries from the tariffs, based on the status of the discussions. The European Union will negotiate on behalf of its member countries.

The President retains broad authority to further modify the tariffs, including by removing the suspensions or suspending additional countries. Any country not currently suspended remains welcome to discuss a possible suspension with the United States based on a shared commitment to addressing global excess steel and aluminum capacity and production.

The Administration will closely monitor imports of steel and aluminum imports from exempted countries, and the United States Trade Representative, in consultation with the Secretary of Commerce and the Director of the National Economic Council, may advise the President to impose quotas as appropriate. Further action by the President would be needed to implement any quota the President might decide to adopt.

The tariffs proclaimed in Presidential Proclamations 9704 and 9705 will go into effect on 12:01 a.m. on Friday, March 23, 2018.

The process for directly affected parties to apply for an exclusion for specific steel or aluminum products that they need remains in place, as announced in the two Presidential Proclamations and subsequent Federal Register notices by the U.S. Department of Commerce. Secretary Ross, in consultation with other Administration officials, will evaluate exclusion requests for products, taking into account national security considerations. In that evaluation, the Secretary will consider whether a product is produced in the United States of a satisfactory quality or in a sufficient and reasonably available amount.