Sample Category Title

China retaliates US steel tariffs, not the US 50b IP tariffs yet

China's Ministry of Commerce announced measures countering US tariffs. But first thing first. The measures announced are in response to Trump's steel and aluminum tariffs, not the USD 50b section 301 tariffs announced overnight. China also said it could take legal action regarding the steel tariffs under WTO rules. So far, it appears that China is trying to play by the book.

The MOFCOM proposed a list of 128 US imports with total value at over USD 3b in 2017. A 15% tariff will be imposed on the first group including wines, fresh fruit, dried fruit and nuts, steel pipes, modified ethanol, and ginseng. Then a 25% tariff could be imposed on the second group, including pork and recycled aluminium goods if both sides failed to reach a resolution through talks.

Here is the statement (in simplified Chinese if you're interested).

Some analysts try to compare US tariffs on USD 50b of China import, and China tariff on USD 3b of American imports. But that is wrong. We'll repeat here that the MOFCOM's announcement was in response to the steel and aluminum tariff. And, depending on the data source, China was either the 10th or 11th largest steel importer to the US, contributing to less than 3%.

That is, China hasn't showed their hands regarding yesterday's announcement by Trump yet.

Market Morning Briefing: The US President Announced More Than 50 Billion Dollars Worth Of Import Curbs On China Last...

STOCKS

Dow (23957.89, -2.93%) has fallen sharply as Trump's plan for heavy import tariffs on China raises concerns for the US companies. This has been the sharpest fall since Feb, almost a d cline of 10% in a single session. This brings Dow to the correction region and while the index trades below 24000, it looks bearish for the medium term targeting 22000 on the downside.

Dax (12100.08, -1.70%) has also fallen testing 12100 mentioned yesterday. The index looks bearish for the next week as well targeting lower levels of 11900-11800 in the medium term.

Nikkei (20827.92, -3.54%) came down with a stronger Yen as mentioned yesterday. Dollar Yen slumped to 104.61 levels after the tensions over China and US trade resurfaced bringing down Nikkei sharply below 21000. This opens up a fall towards 20200 in the coming sessions.

Shanghai (3168.23, -2.92%) has fallen too along with the major indices and could test 3100 on the downside before trying to move up again in the medium term.

Nifty (10114.75, -0.40%) and Sensex (33006.27, -0.39%) may also fall a bit today keeping in line with the globally bearish sentiment. A break below 10020-10000 and 32750 on the Nifty and Sensex respectively would be an indication of further dip in the next week. Near to medium term looks bearish just now.

COMMODITIES

Brent (69.46) has medium term resistance near 71.50-70.00 which does not look very likely to break on the upside just now. A small dip from current levels is possible towards 68 by early next week. Nymex WTI (64.92) could also come off towards 63.60 in the coming sessions. 66-67 is important and is likely to produce some rejection pushing the price to lower levels in the near term.

Gold (1338.40) has risen and while that continues, it may attempt a test of 1345/50. If the ,momentum is strong, we may expect 1260 in the next week from where a corrective dip is possible.

Copper (3.0090) has come down as the Chinese stocks decline. A break below 3, if seen could open p chances of a fall towards 2.95-2.90 in the near term. Support is visible near current levels on the 3-day charts. Ned to see if price manages to bounce back from current levels or falls further in the next few sessions.

FOREX

The US President announced more than 50 billion dollars worth of import curbs on China last night, raising fears of a possible trade war. The implication of this move has already been seen on the Yen which has strengthened to a 17 months high. Whether this move leads to further weakening of the Dollar would have to be seen in the days ahead.

Dollar index (89.59) for now is trading near levels seen yesterday. There is immediate resistance near current levels on 3 day candles which could push it down further. The 1st downside target is support on weekly line chart near 89.3-89.5. As mentioned earlier, this is a crucial support level whose break could lead to medium term bearishness for the Dollar. The next target on the downside (in case a break of 89.3-89.5 happens) would be support on daily candles near 88.5.

Euro (1.2336) saw a high of 1.2390 yesterday thereby breaching immediate resistance near 1.236-1.237 on daily candles but has now again dipped below the resistance. Another breach of this resistance could take the Euro towards higher resistance level on 3 day candles near 1.255-1.260. This is a crucial level, whose breach could imply medium term bullishness for the Euro. On the downside, there is immediate support near 1.2275 on daily candles.

Dollar Yen (104.82), post Trump’s announcement, has dipped to a 17 months low and is testing support near 104.80 on daily candles. If this break of 105 sustains, the next downside target is seen on 3 day candles and weekly line chart near 103.75. This would be another crucial long term support level.

Euro Yen (129.30) as per expectation, has been pushed down by immediate resistance on daily candles near 131. However, contrary to expectation, it has broken the crucial support level of 130. If the Euro continues to respect resistance near 1.2375 and the Dollar Yen continues to be bearish towards 103.75, we could expect Euro Yen to turn very bearish in the medium term.

Pound (1.4117) has paused slightly after seeing a significant upmove (from 1.40 to 1.4220) yesterday. There could be some resistance near 1.43 on daily candles. If 1.43 is breached, it could attempt a test of 1.44 (seen as resistance on 3 day candles and 3 day line charts) in the coming 1-2 weeks.

Dollar Rupee (65.1050) -Watch intra-week Support at 65.00. We may see 64.90-80 if that breaks.

INTEREST RATES

After the US Fed didn’t put up a sufficiently hawkish stance for US yields to move up, Trump’s announcement of import curbs on China has made investors move away from stocks towards safer bonds, thereby pushing yields down even further.

As mentioned yesterday as well, our Treasury report for Mar’18 (available on demand) predicted a decline in yields after an initial upmove in the days post the rate hike. It looks like the decline has started happening without the initial upmove.

US 10 Yr Yield (2.7953%), 30 Yr (3.045%), 5 Yr (2.59%), 2 Yr (2.2621%) : As mentioned yesterday, on the short term chart, the 10 Yr yield has dipped towards channel support near 2.8% again, from where there should be a bounce if the support holds.

The 30 yr yield instead of moving up towards 3.2% has again dropped to support near 3.05%. It should see a rise now if the support holds.

The 5 year yield has also dipped to support near 2.6% and could see a bounce.

Japan 10 year yield (0.028) has broken crucial support near 0.0375-0.0400 on short term charts. Let’s see if it rises back up from these levels.

DOW lost -724 pts in delayed reaction to start of US-China trade war

DOW closed sharply lower by -724.42 pts or -2.93% at 23957.89 overnight as fear of trade war intensified. S&P 500 was down -68.24 pts or -2.52% at 2643.69. NASDAQ also dropped -178.61pts or -2.43% to 7166.68. Selloff continues in Asian session with Nikkei down -3.6% and HK HSI down -2.7% at the time of writing.

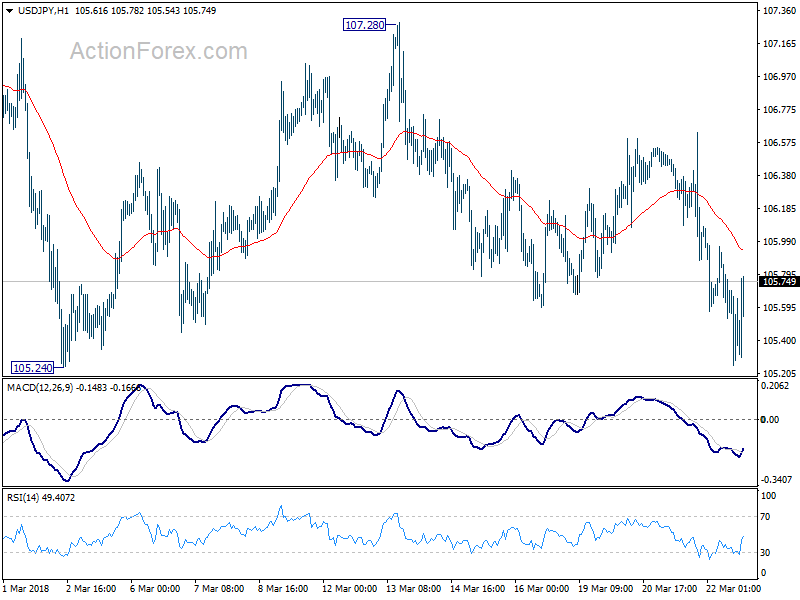

Initial reaction to Trump's announcement on tariffs against Chinese imports was very muted. Trump is targeting to impose tariffs on USD 50b worth of goods from China. That's a big difference to the rumor of USD 50b in tariffs. Nonetheless, the selloff picked up momentum in the last trading hour, as traders dumped their position ahead of China's retaliation measures. (China responded in Asian morning and that will be covered in another note). USD/JPY followed by breaking through 105 handle.

It initially looked like DOW could defend support zone between 23.6% retracement of 26616.71 to 23360.29 at 24128.80 and 24217.76. But the late intensified selling powered the index through this zone. Further fall is now expected in near term to 23360.29 support level.  In the bigger picture, we're maintaining the view that price action from 26616.71 is a medium term correction pattern that's correcting, at least, whole up trend from 2016 low at 15450.56. That means, 38.2% retracement of 15450.45 to 26616.71 at 22351.24 is the first target when the correction extends.

In the bigger picture, we're maintaining the view that price action from 26616.71 is a medium term correction pattern that's correcting, at least, whole up trend from 2016 low at 15450.56. That means, 38.2% retracement of 15450.45 to 26616.71 at 22351.24 is the first target when the correction extends.

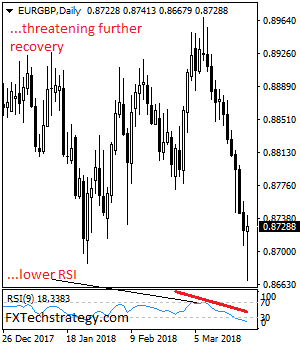

EURGBP – Hesitates, Backs Off Lower Prices

EURGBP - The pair backed off lower prices during Thursday trading session. This has opened the door for more recovery higher. Support lies at the 0.8700 level where a violation will turn focus to the 0.8650 level. A break will expose the 0.8600 level. Conversely, resistance resides at the 0.8800 level where a violation if seen will turn risk towards the 0.8850 level. Further up, resistance resides at 0.8900 level followed by the 0.8950 level. All in all, EURGBP remains biased to the downside but with caution of a recovery.

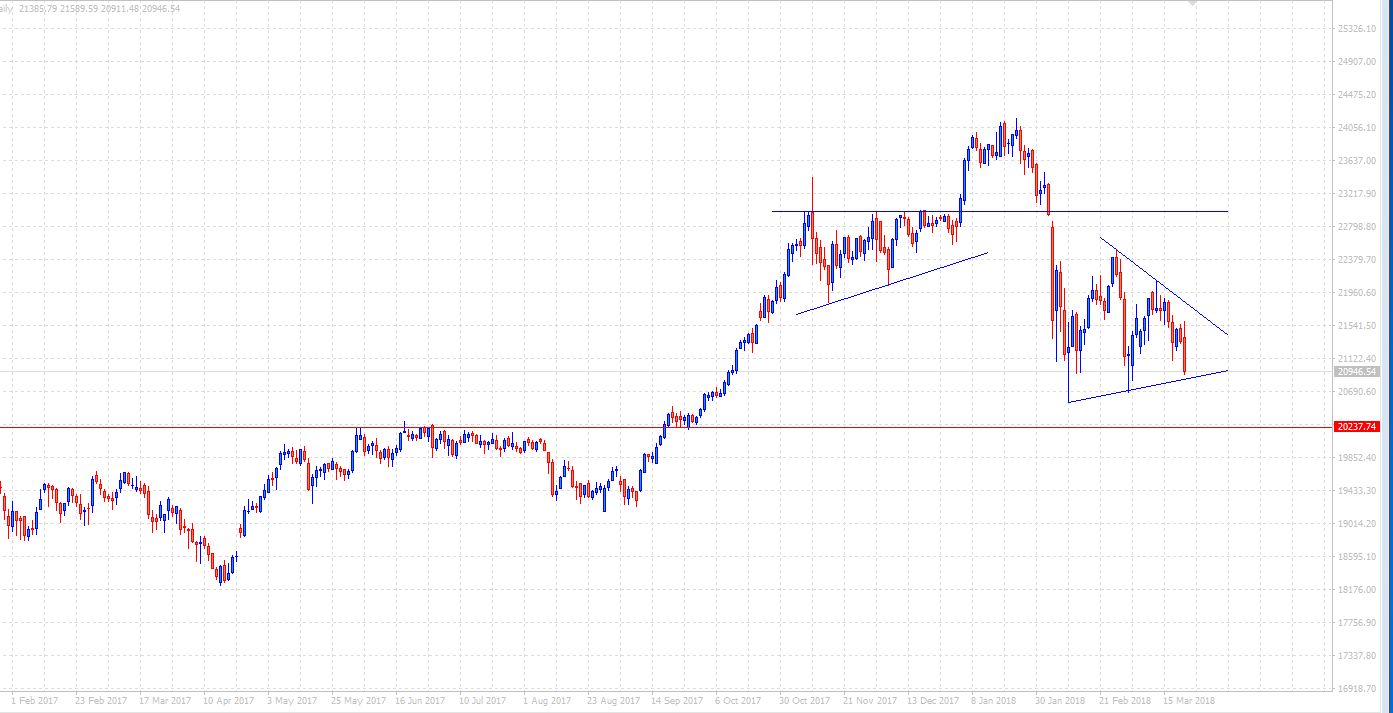

Symmetrical Triangle Forming On The Nikkei

Flipping through the charts last night, I came across this and wondered, is the sun setting on the Nikkei?

What we're seeing here is a symmetrical triangle pattern forming on the daily chart. Now, ideally i'd like to see a few more touches of the trendline, but the pattern is still valid. While symmetrical triangles are relatively unbiased in direction, this overall does look bearish.

China Is Not Backing Down , And Why Should They ?

China is not backing down, and why should they?

A confluence of market ruinous variables has triggered the intersection of short, medium and long-term investors who are taking for the sideline for fear of a market trainwreck.

US equity markets tumbled overnight as investors headed for the relative safety of Bonds as the US is on the cusp of a full-blown trade war with China. And with China unlikely to back down and to readying the retaliatory tariff salvos, markets are looking immensely fragile today. Strap in as a tit for tat tariff tiff is about to start.

Fortunately for the US, however, US bond markets remain the only game in the town for China, and while the may use pulling out of US bond markets as a lever in the trade war, it’s implausible they will follow through for fear of irreparably eroding the values of their enormous US holdings.

But the global economy is also looking incredibly more brittle this morning in the wake of the disappointing Eurozone, German and France PMIs, so this data also explains some of the market jitters.

Trump’s revolving door remains in full swing as John Dowd, Donald Trump’s lead lawyer and 'strongman'in the Mueller investigation into Russian election interference handed in his walking papers after the President is purportedly turning to Fox news for legal advice. The president’s erratic nature continues to generate credibility issues. But it doesn’t stop there as General McMaster was also handed his marching orders today.

The Facebook data controversy is showing few signs of abating and continues to have far-reaching implication not only for the social network but the tech sector in general.

All this has translated into a massive risk-off correction with steep falls in global equity markets and broader USD strength as investors head for the safety of US bonds.

Finally, the storm called 'Daniels 'is expected to hit landfall on Sunday night. CBS has announced they will air a telltale highlighting Porn Star 'Stormy Daniels 'infidelities with President Trump. While probably more tabloid fodder than anything else, nasty sex scandals have had a negative influence on past presidents approval ratings. But given GOP strongholds in the Bible Belt, these revelations could be particularly damaging to the GOP.

Currency Markets

While traders were debating the level of FOMC hawkishness after 'Jittery Jay'nudged the longer term FOMC dots higher, they were utterly overwhelmed by risk aversion and all but gave up on the currency strategy and followed the flow.

If pressed for a view, short USDJPY continues to be the easiest and quickest road to the bank. But despite the dollar gaining some momentum vs the broader G-10 landscape, the continuation of easy money policy and the Fed turtling on 2018 monetary policy adjustments is a nasty cocktail and should lead to the resumption of more widespread dollar weakness over the short term.

The Japanese Yen

The Yen continues to be the beneficiary of global risk aversion, and even as we melt through the 105 level like a hot knife through butter, there remain very few reasons not to be short USDJPY in this environment. Normally crowded trades get worrisome entering a weekend, but the USDJPY traders are on autopilot this morning.

The Euro

The Euro is being weighted down by the general risk-off malaise but is having just as much trouble regaining composure after the downtrodden EU PMI prints.

The Malaysian Ringgit

With a possible escalation of a trade war between China and the USA is denting regionals sentiment. Buckle in as there will be some short-term pain given the enormous export-oriented nature of the regional economies .. And while Malaysia is nowhere near as dependent on US exports as other regional currencies, it will be difficult to avoid the short-term fall out from a local association perspective. But the far more reaching implications for regional currency markets is that this could lead to the markets pricing out future rate hike premiums and in some cases, moving to rate cut probabilities.

Given the massive wave of risk aversion gripping markets, I would expect the USDMYR, considered a riskier currency, to gravitate towards the higher end of the current range.

Oil Markets

Oil prices are coming off pressured by US production and the waves of risk aversion cratering equity market;

Also weaker data out of Europe and the real prospect of a trade war will weigh on global growth sentiment.

Traders are looking over their shoulder at the worrying signs from the industrial commodity complex which is plunging on a shaky global growth narrative, something that certainly doesn’t bode well for oil producers either.

Gold Markets

We’re in a flat our risk-averse mode with looming trade wars pressuring global equity markets and providing a fillip to gold prices as investors are rotating out of equity positions into Gold. However, the USD remains on edge but tentatively holding up against the broader G-10 complex ( outside of JPY ) which is keeping top side Gold momentum in check so far.

Trade Turmoil

A series of waivers of US steel and aluminum tariffs eased trade worries on one front but escalated them on another Thursday as stock markets were battered. The yen was the top performer while the Australian dollar lagged in a classic risk-off move. Japanese CPI is due up next. The Premium DAX30 short was closed at 11980 for 360 pt-gain.

The US trade position is increasingly clear. Levying tariffs against some of its closest trading partners was part of a negotiating strategy. They were a threat designed to bring them to the table, where the US gave them an ultimatum: take our side against China or face the consequences.

Leaks from EU tariff negotiations showed that support for the US against China at the WTO stood among the conditions. At the same time, the US hit China with fresh tariffs Thursday on imports of intellectual property.

So what had looked like a US-against-the-world trade spat may be the-world-against-China, led by the US. That puts the China in a tough spot but leaves them with several options: 1) play the long game by accepting the tariffs and wait for Trump to leave office, 7 more years if necessary. 2) Try to sway countries on the US side. 3) Try to hurt the US in swing states head of the US mid-terms.

At the moment, the third option is the most likely but markets will be watching China's next move very closely. The S&P 500 closed on the lows and narrowly below the worst levels of March. Technically, the picture is deteriorating.It's much the same in the yen crosses – many of which never recovered from the plunge in February anyway.

Going into the weekend, the market will be wary of negative headlines and risk aversion will probably continue. Yen traders will we watching for headlines from Japanese CPI at 2330 GMT. The consensus is for a 0.5% y/y rise ex-fresh food and energy.

Eco Data 3/23/18

[php_everywhere instance="1"]

Trump announced tariffs on USD 60b of Chinese imports; No, not USD 60b of tariffs!

Trump finally announce his plan to tariff as much as USD 60b in Chinese imports to safeguard technological development of the US and its future.

Sorry, can you elaborate on what do you mean?

Well, Trump said, "this has been long in the making," and "we have a tremendous intellectual property theft situation going on" with China affecting hundreds of billions of dollars in trade each year".

Sorry, but... are you talking about USD 60b tariffs annually?

No. And apparently no. The tariff is only on USD 60b of Chines imports!

So how much is the tariff?

We here don't know yet. What we only know is that Trump complained that "We've lost, over a fairly short period of time 60,000 factories." And, he complained that China has been steal our jobs, stealing our technology. Yet, Trump said today that he view these thieves "as a friend"?!!

Anyway, reactions from the financial market is clear. USD/JPY recovers ahead of 105.24 near term support, without breaking.

DOW also recovers after after dipping to as low as 24175.49.

The markets' message is clear. Don't bother me until you're doing something significant!

BoE Still on Track for a May Hike

The Bank of England maintained monetary policy unchanged but two BoE members (Ian McCafferty and Michael Saunders) voted for an immediate rate hike (vote count 7-2 for an unchanged Bank Rate). While Mark Carney has already revealed that the BoE no longer wants to pre-commit to a hike, this was as close to a pre-commitment as we could get.

Looking at the meeting summary and minutes, there were no major shifts in the policy signal from the Bank of England, as economic data have been in line with the projections in the February Inflation Report. The BoE says 'ongoing tightening of monetary policy' is needed over the forecast horizon.

While the positive contribution to CPI inflation from GBP depreciation is fading, the BoE thinks domestic cost pressure is increasing, as slack has been more or less absorbed. In order to avoid a more persistent CPI inflation overshoot, it is appropriate to raise rates. The BoE still expects growth to remain above potential GDP growth over the forecast horizon.

With respect to Brexit, the Bank of England did not alter its communication despite the agreement on transition. Based on Mark Carney's comments at a press conference after the February meeting, the BoE had already pencilled in a high expectation of a Brexit transition agreement so it does not really alter the outlook for the BoE.

We still believe the BoE is heading for a May hike and we also believe another hike in November is likely, which is more than the one BoE hike forecast by consensus. As we argued back in February after the last meeting, the BoE seems to have launched a regular hiking cycle and this meeting has not changed our view. Markets have priced in approximately 42bp hikes this year, so we are more hawkish than both other houses and market pricing.

Although the Brexit transition deal is, other things being equal, positive news, it is in our view not a game-changer for EUR/GBP in the short-run and we forecast 0.87 in 3M. The negotiations on what the future relationship looks like are going to be much more complicated, not least with respect to the Irish border. We still think EUR/GBP will move lower in 6-12M on Brexit clarification and higher UK interest rates. We target EUR/GBP at 0.86 in 6M and 0.84 in 12M.