Sample Category Title

GBP rally held back by lack of aknowledgement of Brexit negotiation progress by BoE

More on BoE, apart from Saunders and McCafferty, there seems to be nothing worth noting in today's announcement. Overall tone of the statement remained the same as February's. Brexit development was just briefly mentioned. The essential part regarding Brexit was totally unchanged.

BoE maintained that the projected 1.75% GDP growth would be more than offset 1.5% supply growth. And small margin of excess demand was projected to emerge by early 2020. And that would push up domestic costs. Thus, "inflation remained above the 2% target in the second and third years of the MPC's central projection."

BoE added that "ongoing tightening of monetary policy over the forecast period will be appropriate to return inflation sustainably to its target at a more conventional horizon." This suggests that it's more confident regarding tightening ahead. But BoE reiterated cautious that "any future increases in Bank Rate are likely to be at a gradual pace and to a limited extent.

Overall, the lack of acknowledge of Brexit negotiation progress, and the cautious tone of the statement is holding back Sterling bulls.

Dollar Holds Weak Ahead Of Trump’s Chinese Tariffs, BoE Decides On Interest Rates

Here are the latest developments in global markets:

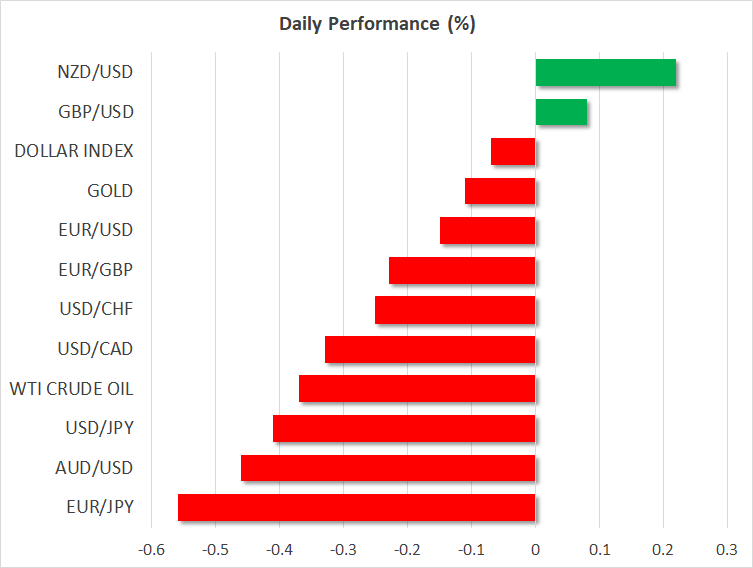

FOREX: The US dollar index was falling by 0.03% against a basket of major currencies during early European afternoon and dollar/yen remained under pressure, losing 0.39%. The fall in the dollar came in after the Fed raised interest rates, as was widely anticipated, but stayed on course for three rate hikes this year, disappointing those who hoped for the famous dot plot to signal four rises for 2018. The euro managed to hit a one-week high of 1.2387 early on Thursday but the gains were short-lived, with euro/dollar moving lower towards 1.2317 (-0.15%) afterwards. Sterling will be in focus today as the Bank of England (BoE) is expected to announce its rate decision later today. Meanwhile, pound/dollar stretched up to 1.4180, the highest peak reached in seven weeks before it returned to 1.4148 (+0.07%). The Reserve Bank of New Zealand's monetary policy announcement did not have a significant impact on the New Zealand dollar. Kiwi/dollar was last up by 0.26% on the day, while aussie/dollar was weaker by 0.44%. Dollar/loonie was unable to recover after a 200 pips fall on Wednesday, last seen at 1.2863 (+0.31%).

STOCK: European stocks posted strong declines on Thursday as trade concerns over a potential retaliation against Trump's punitive import tariffs loomed in the background. The blue-chip Euro STOXX 50 plunged by 0.98% at 1100 GMT, the British FTSE 100 was down by 0.54%, while the German DAX 30 and the Spanish IBEX 35 were weaker by 0.86% and 0.91% respectively. US stock futures were in the red, poised to open lower.

COMMODITIES: WTI crude and Brent managed to recoup part of yesterday's losses, but remained down on the day. The former climbed to $65.16 (- 0.05%), while the latter edged up to $69.40 a barrel. (-0.12%) Gold slipped to $1,329.40 per ounce (-0.18%), hovering near two-week highs hit late on Wednesday on the back of a weaker dollar.

Day ahead: Bank of England to leave rates unchanged; Trump set to announce tariffs on China

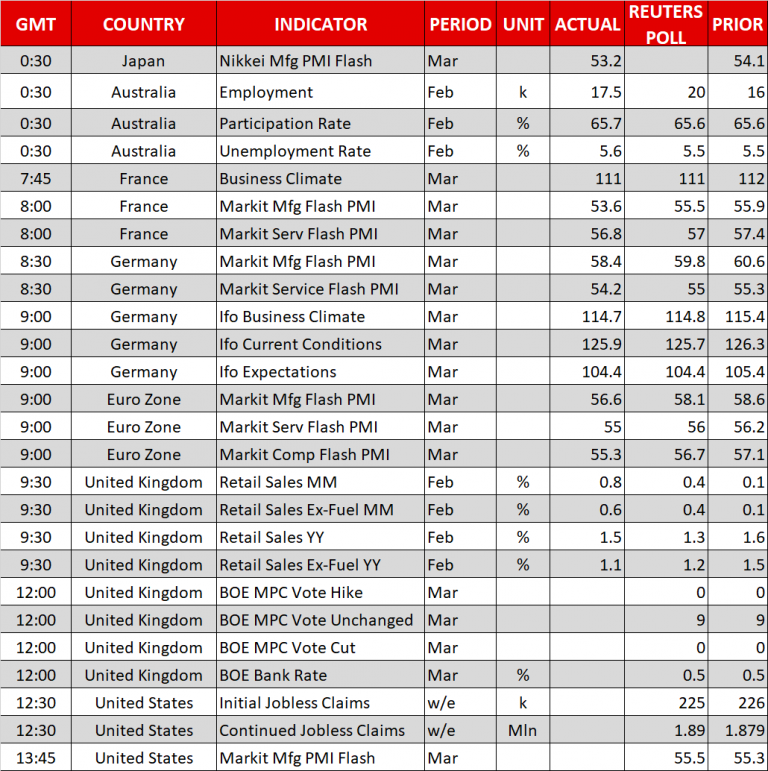

Following its US and New Zealand counterparts, the Bank of England (BoE) is next in line to decide on interest rates. However, unlike its US peer, the BoE is not expected to deliver any rate hike today at 1200 GMT, but according to market chatter, it may signal that a rise in borrowing costs from their current level of 0.5% could emerge in May. Yesterday, employment data out of the UK showed that the unemployment rate eased unexpectedly to 4.3% in January, while an improvement in wage growth was a bigger surprise after the numbers showed that average earnings jumped to a 2 ½-year high of 2.8%, fueling hopes that monetary policy could tighten in May when policymakers revise their economic projections. Therefore, if the BoE sounds more optimistic today, probably expressing satisfaction about the UK's employment trends and the recent encouraging Brexit developments, the pound could extend gains as investors would be more confident that the BoE would raise rates in May. On the other hand, a cautious stance could send the pound lower. Investors will also keep a close eye on the vote count. Forecasts are for a unanimous 9-0 vote to stay on hold. However, if the most hawkish members, McCafferty and Michael Saunders, call for a tightening, turning the no-change vote to 7-2, the pound could post a stronger rally.

On the Brexit front, the EU summit takes place today in Brussels and any updates could be also important for the pound. While a two-year transitional period is a done deal following Monday's agreement on transitional arrangements, any details on the terms that are not publicly known could pressure the currency.

In the US, according to a White House official, the US President, Donald Trump, will announce new import tariffs on China, amounting to $50 billion as rumors support, in an effort to punish the country for intellectual property theft, probably around 1630 GMT. Yesterday, the U.S. Trade Representative Robert Lighthizer said that the country would target China's high-technology sector and impose restrictions on Chinese investments in the United States. In this event, a global trade war is what frightens investors as China is not expected to stay behind but respond accordingly, activating its own restrictive measures. Consequently, the aussie and the kiwi which are sensitive to China's economic developments could lose ground in the wake of the news, while the risk-off sentiment could harm stocks and provide support to safe havens such as the yen and the Swiss franc.

Looking at today's remaining data releases, initial jobless claims and Markit manufacturing PMI's will be noted in the US at 1230 GMT and 1300 GMT respectively. During early Asian session, at 2330 GMT, Japanese inflation readings for the month of February will come into view as well. Regarding the latter, projections are for the headline and the core CPI to inch up by 0.1 percentage points to 1.0% and 1.5% on a yearly basis respectively.

In equities, the footwear maker Nike is expected to announce a decline in third-quarter profits on Thursday due to changes in the US tax code.

Finally, in terms of speakers, we will hear from Norges Bank Governor Oystein Olsen at 1615 GMT, as well as BoE Deputy Governor Dave Ramsden, at 1700 GMT. Bank of Canada Deputy Governor Carolyn Wilkins is also due to deliver remarks, at 1845 GMT.

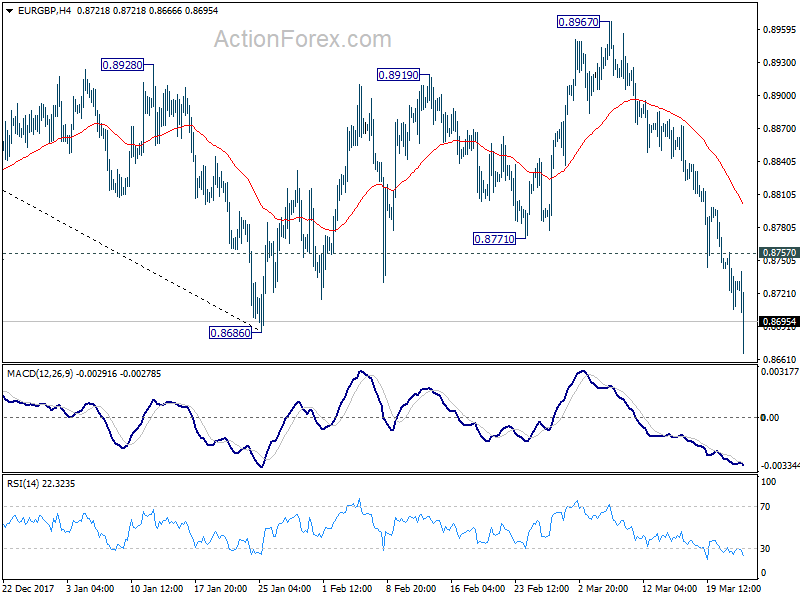

GBP spikes high, EUR/GBP breaks key support as McCafferty and Saunders voted for BoE hike

BoE stands pat as widely expected. And just as we anticipated, Ian McCafferty and Michael Saunders come back with votes for rate hike. This feels like the irresistable nature of hawks.

Sterling spikes higher broadly after the release. And EUR/GBP dives through key support level at 0.8686 to as low as 0.8666. Now, let's see if it can sustain below this key support level.

Below is BoE's full statement.

Below is BoE's full statement.

Bank Rate Maintained at 0.50%

Our Monetary Policy Committee has voted by a majority of 7-2 to maintain Bank Rate at 0.50%. The committee also voted unanimously to maintain the stock of corporate bond purchases and UK government bond purchases.

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 21 March 2018, the MPC voted by a majority of 7-2 to maintain Bank Rate at 0.5%. The Committee voted unanimously to maintain the stock of sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves, at £10 billion. The Committee also voted unanimously to maintain the stock of UK government bond purchases, financed by the issuance of central bank reserves, at £435 billion.

In the MPC's most recent projections, set out in the February Inflation Report, GDP was expected to grow by around 1¾% per year on average over the forecast period. While modest by historical standards, that growth rate was expected to exceed the diminished rate of supply growth of the economy, which was projected to be around 1½% per year. As a result, a small margin of excess demand was projected to emerge by early 2020 and build thereafter. That pushed up on domestic costs, although CPI inflation fell back gradually as the effects of sterling's past depreciation faded. Inflation remained above the 2% target in the second and third years of the MPC's central projection.

Recent data releases are broadly consistent with the MPC's view of the medium-term outlook as set out in the February Report. The prospects for global GDP growth remain strong, and financial conditions continue to be accommodative, with little persistent effect from the recent financial market volatility. UK GDP growth in the fourth quarter was revised down slightly, to 0.4%, with the composition of demand implying less rotation towards net trade and business investment than anticipated at the time of the February Report. However, early estimates of the expenditure components of GDP are prone to revision, and other indicators of exports and investment point to a stronger picture. The latest activity indicators suggest that the underlying pace of GDP growth in the first quarter of 2018 remains similar to that in the final quarter of 2017.

CPI inflation fell from 3.0% in January to 2.7% in February. Inflation is expected to ease further in the short term although to remain above the 2% target. Pay growth continued to pick up. The unemployment rate remained low in the three months to January. The firming of shorter-term measures of wage growth in recent quarters and a range of survey indicators suggest pay growth will rise further in response to the tightening labour market. This provides increasing confidence that growth in wages and unit labour costs will pick up to target-consistent rates.

Developments regarding the United Kingdom's withdrawal from the European Union – and in particular the reaction of households, businesses and asset prices to them – remain the most significant influence on, and source of uncertainty about, the economic outlook. In such exceptional circumstances, the MPC's remit specifies that the Committee must balance any significant trade-off between the speed at which it intends to return inflation sustainably to the target and the support that monetary policy provides to jobs and activity. The steady absorption of slack has reduced the degree to which it is appropriate for the MPC to accommodate an extended period of inflation above the target.

As in February, the best collective judgement of the MPC remains that, given the prospect of excess demand over the forecast period, an ongoing tightening of monetary policy over the forecast period will be appropriate to return inflation sustainably to its target at a more conventional horizon. All members agree that any future increases in Bank Rate are likely to be at a gradual pace and to a limited extent. In light of these considerations, seven members thought that the current policy stance remained appropriate to balance the demands of the MPC's remit.

DAX Slides As Hawkish Powell Sends Markets Lower

The DAX index has recorded sharp losses in the Thursday session. Currently, the DAX is trading at 12,169, down 1.14% on the day. On the release front, eurozone and Germany Manufacturing PMIs missed their estimates. Eurozone Manufacturing PMI dropped to 56.6, down from 58.1 points. The German release slowed to 58.4, compared to the estimate of 59.8 points. German Ifo Business Climate also dipped to 114.7, matching the estimate.

The markets had priced in a rate hike from the Federal Reserve, and policymakers complied with a quarter-point increase on Wednesday, bringing the benchmark rate to a range between 1.50% and 1.75%. The markets were looking for any clues with regard to the pace of rate hikes in 2018 – currently the Fed is projecting three hikes, but a robust US economy could push the Fed to press the rate trigger four times. The rate statement did not directly address the issue, but there was a refreshing lack of Fedspeak from policymakers, who said that “the economic outlook has strengthened in recent months”. This phrase has not been used in previous rate statements, and the hawkish terminology helped send US markets lower on Wednesday, with the trend continuing on Thursday in European markets.

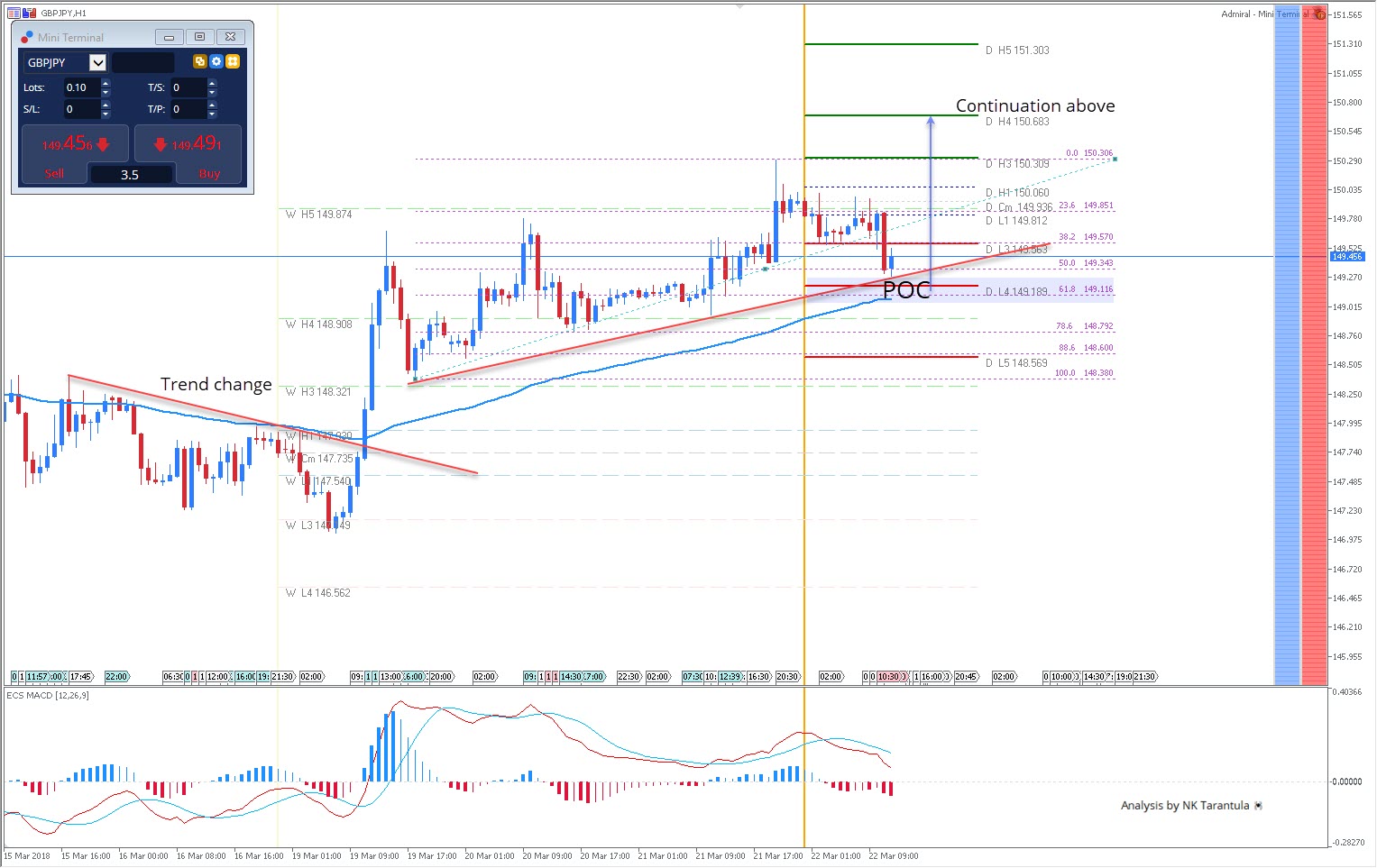

GBP/JPY Bullish Zig-Zag After The Trend Change

The GBP/JPY has gone through a trend change after the price broke a descending trendline above 147.90. Subsequently the price has made a bearish zig-zag so buying the dip could be possible. 149.10-149.30 is the zone to watch for as the price might bounce from POC targeting 149.89 and 150.00. Only above 150.00, 150.68 will be the target. Strong 1h candle or 4h candle above 150.68 is needed for the price to proceed further above towards 151.30.

However if the price drops below 148.55, the trend might become neutral to bearish.

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

GBP/USD: UK Retail Sales

The British Pound strengthened against the Greenback, following the UK retail sales report on Thursday. The GBP/USD currency pair gained only four pips, or 0.03%, in the first minute after the release. However, the GBP/USD currency pair showed growth only in the first two minutes and continued to decline afterwards.

The Office for National Statistics revealed better-than-expected retail sales data, but that was not enough to cause a significant move on the market. British retail sales grew 0.8% in February, exceeding the forecasts of 0.4%. Despite the fact that retail sales grew, doubts about consumer purchase power remained, as the Bank of England plans on raising interest rates.

(BOE) Bank Rate Maintained at 0.50%

Our Monetary Policy Committee has voted by a majority of 7-2 to maintain Bank Rate at 0.50%. The committee also voted unanimously to maintain the stock of corporate bond purchases and UK government bond purchases.

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 21 March 2018, the MPC voted by a majority of 7-2 to maintain Bank Rate at 0.5%. The Committee voted unanimously to maintain the stock of sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves, at £10 billion. The Committee also voted unanimously to maintain the stock of UK government bond purchases, financed by the issuance of central bank reserves, at £435 billion.

In the MPC's most recent projections, set out in the February Inflation Report, GDP was expected to grow by around 1¾% per year on average over the forecast period. While modest by historical standards, that growth rate was expected to exceed the diminished rate of supply growth of the economy, which was projected to be around 1½% per year. As a result, a small margin of excess demand was projected to emerge by early 2020 and build thereafter. That pushed up on domestic costs, although CPI inflation fell back gradually as the effects of sterling's past depreciation faded. Inflation remained above the 2% target in the second and third years of the MPC's central projection.

Recent data releases are broadly consistent with the MPC's view of the medium-term outlook as set out in the February Report. The prospects for global GDP growth remain strong, and financial conditions continue to be accommodative, with little persistent effect from the recent financial market volatility. UK GDP growth in the fourth quarter was revised down slightly, to 0.4%, with the composition of demand implying less rotation towards net trade and business investment than anticipated at the time of the February Report. However, early estimates of the expenditure components of GDP are prone to revision, and other indicators of exports and investment point to a stronger picture. The latest activity indicators suggest that the underlying pace of GDP growth in the first quarter of 2018 remains similar to that in the final quarter of 2017.

CPI inflation fell from 3.0% in January to 2.7% in February. Inflation is expected to ease further in the short term although to remain above the 2% target. Pay growth continued to pick up. The unemployment rate remained low in the three months to January. The firming of shorter-term measures of wage growth in recent quarters and a range of survey indicators suggest pay growth will rise further in response to the tightening labour market. This provides increasing confidence that growth in wages and unit labour costs will pick up to target-consistent rates.

Developments regarding the United Kingdom's withdrawal from the European Union – and in particular the reaction of households, businesses and asset prices to them – remain the most significant influence on, and source of uncertainty about, the economic outlook. In such exceptional circumstances, the MPC's remit specifies that the Committee must balance any significant trade-off between the speed at which it intends to return inflation sustainably to the target and the support that monetary policy provides to jobs and activity. The steady absorption of slack has reduced the degree to which it is appropriate for the MPC to accommodate an extended period of inflation above the target.

As in February, the best collective judgement of the MPC remains that, given the prospect of excess demand over the forecast period, an ongoing tightening of monetary policy over the forecast period will be appropriate to return inflation sustainably to its target at a more conventional horizon. All members agree that any future increases in Bank Rate are likely to be at a gradual pace and to a limited extent. In light of these considerations, seven members thought that the current policy stance remained appropriate to balance the demands of the MPC's remit.

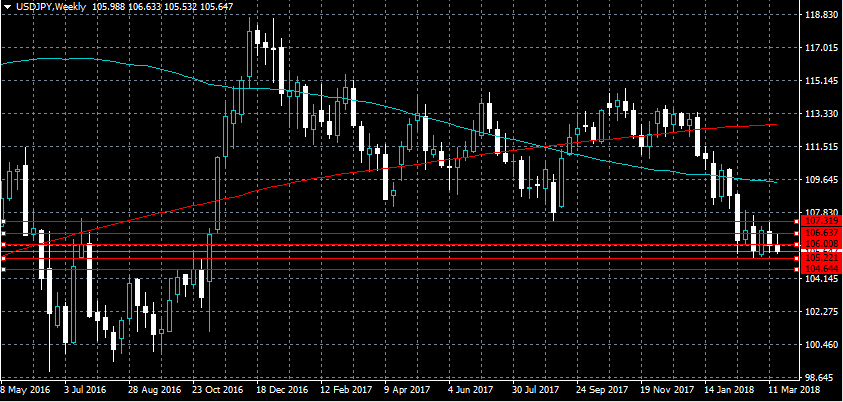

USDJPY Further Bearish Below 105.22 Level

The U.S dollar is moving towards the lowest levels of 2018 against the Japanese yen currency, as global trade war concerns help to underpin risk-off trading sentiment. The USDJPY pair is currently trading around the crucial 105.50 level, with sellers likely to target the pairs yearly price-low, at 105.22. Moving into the U.S session, USDJPY traders await further news on the Trump administrations latest plans to impose trade tariffs on Chinese exports.

The USDJPY pair is likely to encounter further intraday losses below the 105.50 level, key technical support is then found at the 105.22 and 104.64 levels

Should the USDJPY pair hold above the 105.50 support level, a technical correction back towards the 105.78 and 106.00 levels may occur.

GBPUSD Price Correction Looms Below 1.4179

The British pound has edged marginally lower against the greenback during the European trading session, following a mixed UK Retail Sales report. The GBPUSD pair initially spiked to 1.4179, following a better than expected February UK Retail Sales headline number, but soon reversed direction as the previous month's figures were downgraded. The pair currently trades back below the key 1.4046 level, with the 1.4179 to 1.4088 trading-range in focus, ahead today's Bank of England's interest rate decision.

The GBPUSD pair retains a bullish bias whilst trading above the 1.4088 level, key technical resistance is now found at the 1.4179 and 1.4279 levels.

Should GBPUSD price-action move below the 1.4088 support level, a technical correction back toward the 1.4045 and 1.4000 support levels may occur.

USD Takes A Hit Amid Cautious Fed

Fed's caution disappoints markets

As broadly expected the FOMC lifted the Feds fund rate targets by 25bps to 1.50% - 1.75%. Fed members adjusted their forecast so that they reflect their more optimistic view of the US economy. The press statement also underwent changes, all positive. However, despite these efforts, the US dollar has been under heavy selling pressure since yesterday evening. The dollar index fell 89.3 following the announcement and kept losing ground on Thursday morning to reach 89.40 as investors seemed disappointed.

The Committee raised its growth forecast once again. The US economy should grow 2.7% in 2018, an increase from its forecast of 2.5% in December and 2.1% in September last year. On the employment front, the unemployment rate should end the year at 3.8% (3.9% in December and 4.1% in September). However, Fed members left roughly unchanged inflation projections. The Core PCE forecast for 2018 stays at 1.9% but was slightly increase from 2% to 2.1% for 2019. Finally, the Federal Funds rate forecast remains at 2.1% for year-end but was revised higher for 2019, from 2.7% to 2.9%. It means that the Fed should hike rates two more times this year and two times next year.

Looking at the FX market, it seems that investors were expecting a much more aggressive path of tightening from the Federal Reserves. There were a lot of talking about a potential fourth rate hike this year but according to the dot-plots, it won't happen. The Fed has started to unload its massive balance sheet just a few months ago. It will be done gradually and take many years, but still, there will consequences for borrowing costs. We believe that the cautiousness displayed by the Fed could be explained by the willingness to avoid disturbing financial markets further. Trump's recent political decisions could only widen the budget gap. The US government is facing the threat of a shutdown every two weeks these days (I am exaggerating slightly) and the trade tariff situation is not helping to improve the market Sentiment. I believe that the Fed is waiting to get further clarity regarding the effects of the balance sheet unwinding and wants to avoid increase the burden on the government by limiting to some extent the increase of borrowing costs.

Trump 'fly by policy' strokes trade war fears

Markets are once again bracing for US Trump trade policy 'on the fly'. With Rex Tillerson out of the way, Larry Kudlow supporting punitive actions against China and Peter Novara and Wilder Ross steady daring Trump on just about anything could happen today. White House officials indicate that Trump will announce tariffs on Chinese imports this afternoon. The objective according to now turned narrative it Trump titter policy is aimed at curbing theft of US technology. There has been limited indications on size and scope of the tariffs, which indicated in our view a making it up as he goes strategy. We find it hard to think of any actions that accomplish the desired effect.

However, most likely triggering rapid and possible more influential retaliations actions. We doubt Beijing will sit quietly this time around which has significantly increased the risk of a global trade war. USD remains sensitive to protectionism actions, indicated the greenback will unlikely walkway from this one unscathed. Should Trump announced a significant escalations we would rotated into European G10 (SEK, NOK and CHF). Higher US yields have not support USD and unlikely to protect from geopolitical tensions.