Sample Category Title

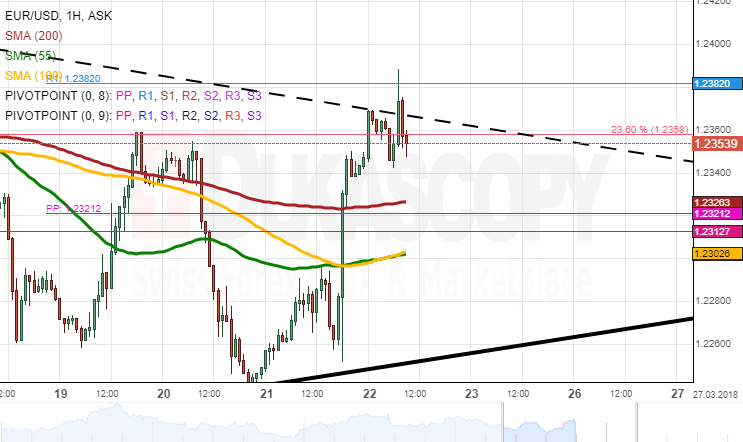

EUR/USD Analysis: Likely To Go For Correction South

The Euro spent most of Wednesday in a positive note, thus approaching the combined resistance of the 55– and 100-hour SMAs at 1.23.

Strong upside risks started to prevail in the market late in the evening when the FOMC announced a 0.25% increase in its benchmark rate. Volatility was introduced in both directions; however, Euro bulls eventually took the dominant hand in response to a decrease in rate hike projections. The pair shot up 48 pips in one hour and subsequently reached a one-week high of 1.2370.

It is expected that the given upward momentum allays in this session, thus allowing for a minor decline. This likely fall should not exceed 1.23, as this level is supported by the 55– and 100-hour SMAs. In the meantime, gains should be capped near 1.2450.

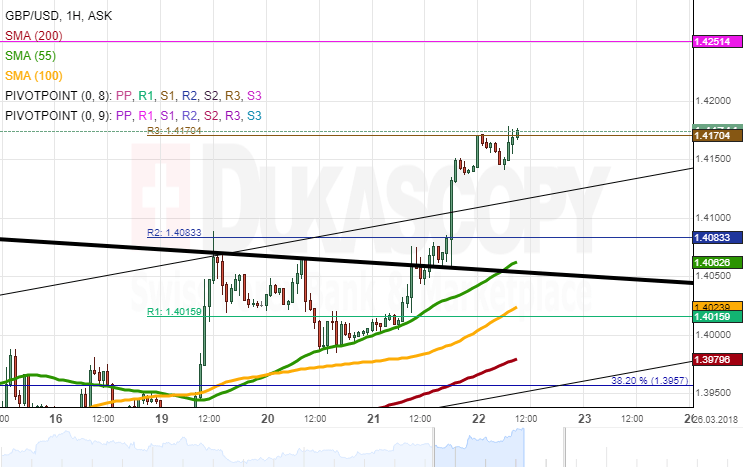

GBP/USD Analysis: Calm After Surge

GBP/USD was guided primarily by the 55-hour SMA during the first part of Wednesday which allowed to reach a three-week resistance of 1.4080.

Bullish strength was added late in the evening when the Fed increased its benchmark rate to 1.75%, but did lower the number of projected hikes to three this year. This caused a significant weakening of the US Dollar across all major currencies and thus paved the way for the Sterling to test the weekly R3 at 1.4170.

Technical indicators are starting to retrace from their high positions. This points to possible depreciation during the following hours, at least.

Volatility is likely to increase mid-session when the BOE is to release its Monetary Policy Summary at 1200GMT. Downside potential today is the 1.40 area, while strong resistance is set at 1.4250.

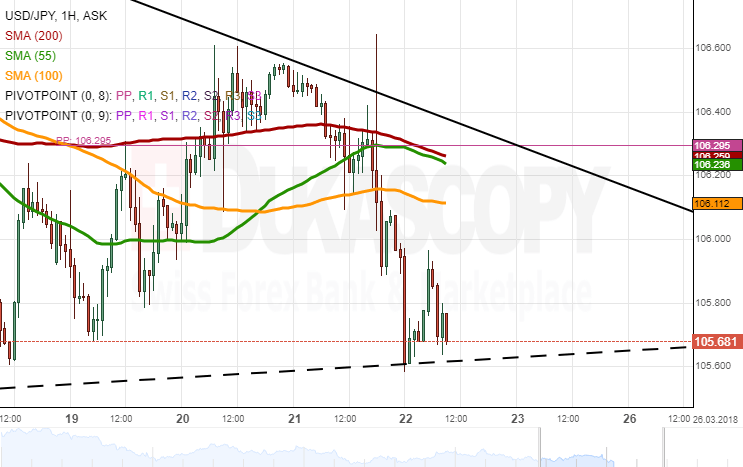

USD/JPY Analysis: Could Be Guided By Fundamentals Today

The US Dollar has still failed to gain strength against the Japanese Yen, thus lingering slightly above the 2017/2018 low of 105.35.

The most recent weakness was caused by trade rhetoric between the US and China which weighted heavily on the pair during the first part of Wednesday. As a result, the US Dollar dashed through the strong support of the 200-, 55– and 100-hour SMAs. The FOMC policy decision strengthened the bearish pressure, thus pushing the rate down to the 105.60 mark.

The pair is likely to be affected by fundamental events today, such as a tariff announcement by Trump, and is unlikely to move past the 55– and 200-hour SMAs and the weekly PP at 106.30 in this session. Meanwhile, the nearest support is set by the aforementioned low and the weekly S1 circa 105.30.

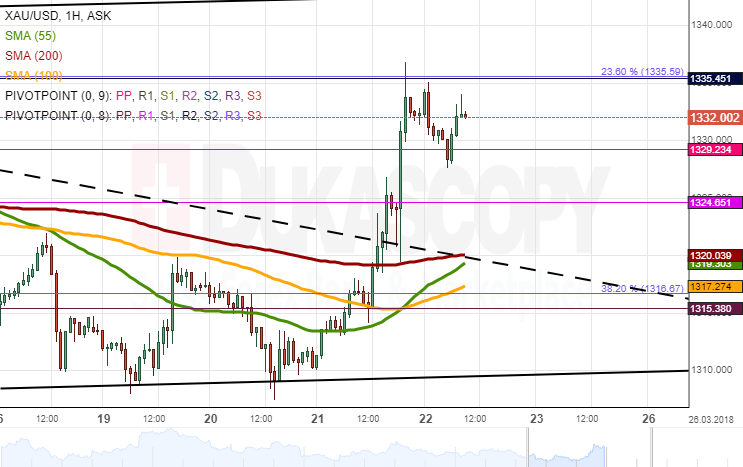

Gold Analysis: Bearish Today

The yellow metal was guided by strong upside risks on Wednesday. It hindered near the resistance of the 55-, 100– and 200-hour SMAs, but eventually managed to push through these lines and the prevailing five-week trend-line circa 1.320.00.

Additional push was given by the FOMC policy statement at 1800GMT. As a result, the pair closed the session at a two-week high of 1,335.00. The 23.60% Fibonacci retracement is likewise located nearby.

The current positioning of the rate suggests that some correction south is likely to occur in this session. However, a move below the previously-breached resistance of 1,320.00 is unlikely.

This area is likely to mark a reversal that would allow the pair to resume its upward movement in the senior channel.

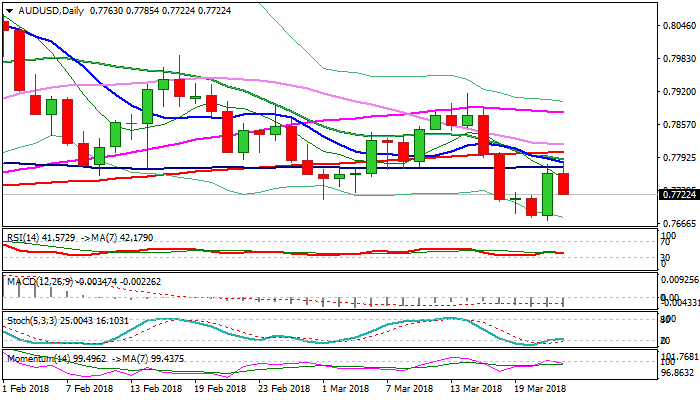

Technical Outlook: AUDUSD – Cluster Of Strong Barriers Capped Recovery, Fears Of Trade War Weigh On Aussie

The Aussie dollar pulled back from post-Fed recovery highs on Thursday after repeated attacks failed to break above initial barrier at 0.7775 (100SMA).

Positive impact from Fed could be offset by increasing fears about trade war, as President Trump is expected to announce tariffs on Chinese imports today.

Plethora of MA barriers between 0.7775 and 0.7818 weighs heavily and marks strong obstacle (reinforced by the base of thick daily cloud) where recovery attempts may stall, as the structure weakened on trade war fears and he notion is supported by negative momentum studies.

Today’s pullback already retraced 50% of Wednesday’s rally, with further weakness and close below 0.7715 (Fibo 61.8%) would confirm reversal and shift near-term focus lower.

Conversely, bullish scenario requires surge through 0.7775/0.7818 resistance zone and close above to neutralize downside risk and signal further recovery.

Res: 0.7775, 0.7785, 0.7804, 0.7818

Sup: 0.7715, 0.7699, 0.7672, 0.7641

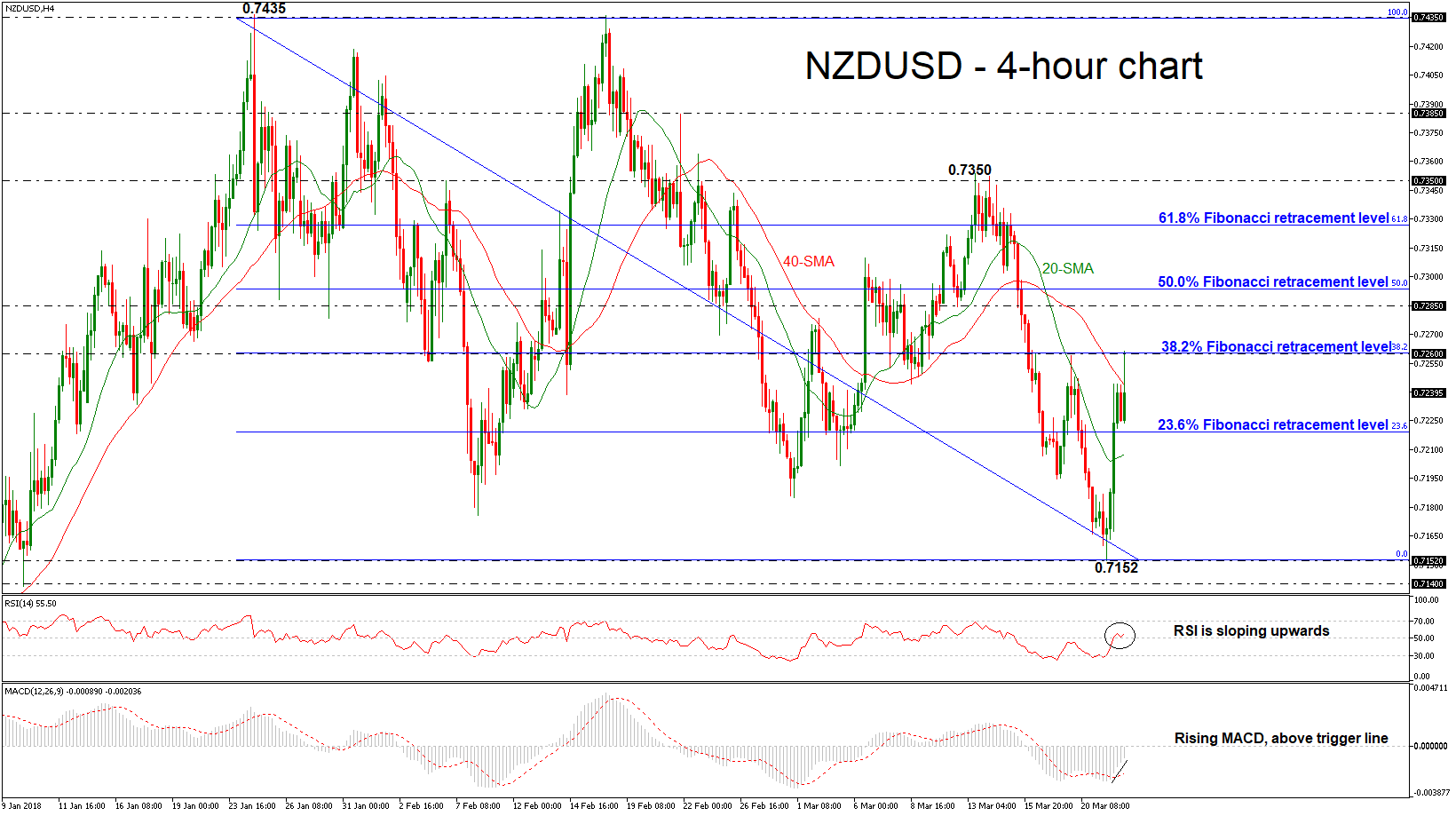

NZDUSD Advances Following The Rebound On 0.7152, Bullish Correction On The Way

NZDUSD skyrocketed over the last couple of hours and jumped above the 0.7260 critical level which overlaps with the 38.2% Fibonacci retracement level of the downleg from 0.7435 to 0.7152, posting a one-week high.

The rebound on the 0.7152 support barrier helped the price to create a strong bullish day surpassing the 20 and 40 simple moving averages (SMAs) in the 4-hour chart. Having a look at the momentum indicators, the RSI and the MACD seem to be in agreement with the bullish scenario. The RSI indicator is pointing north above the 50 level, while the MACD oscillator is rising in the negative territory and surged above its trigger line.

Further gains should see the 0.7285 barrier acting as a major resistance as this also slightly below the 50.0% Fibonacci mark near 0.7293. A jump above this level would reinforce the bullish structure in the short-term and open the door towards the next key level of the 61.8% Fibonacci of 0.7367.

In the event of a downside reversal, the 23.6% Fibonacci level could act as a barrier before the pair would be able to re-challenge the 20-SMA around the 0.7200 handle. A break below this level would shift the short-term outlook to a more neutral to bearish one as it would take the price near the 0.7152 support.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.2374

The break through 1.2300 has reinstated the positive bias and currently the pair is heading towards 1.2460 major resistance. The rise from 1.2240 should be considered a final leg of the whole rebound above 1.2160 before drowning towards 1.2090 zone. Key intraday support lies at 1.2330, followed by 1.2300.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2300 | 1.2460 | 1.2230 | 1.2160 |

| 1.2460 | 1.2560 | 1.2160 | 1.2090 |

USD/JPY

USD/JPY

Current level - 105.68

The intraday bias is bearish after the recent peak at 106.60, for a tight test of 105.20 lows. My outlook here is neutral.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 106.60 | 108.30 | 105.20 | 105.20 |

| 108.00 | 110.40 | 105.20 | 102.40 |

GBP/USD

GBP/USD

Current level - 1.4165

The uptrend is intact and there is a risk of a further rise to 1.4280 before reversal and completion of the whole upmove since 1.3710. Initial intraday support lies at 1.4080 and crucial on the downside is 1.3980.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.4180 | 1.4280 | 1.4080 | 1.3710 |

| 1.4280 | 1.4340 | 1.3980 | 1.3620 |

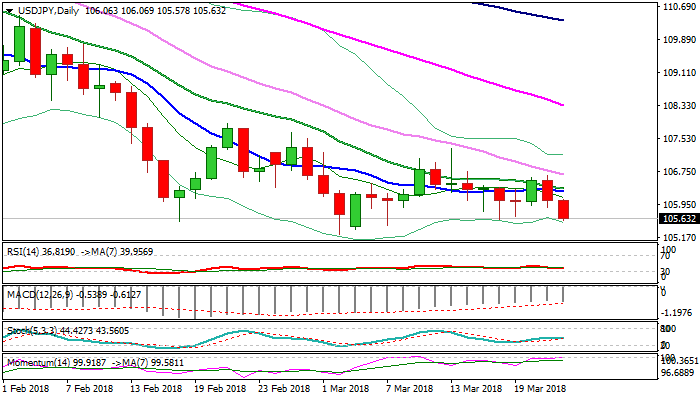

Technical Outlook: USDJPY – Bearish Bias Remains Intact After Repeated Rejection Under 30SMA, Scope For Retest Of 2018 Low...

Repeated rejection under falling 30SMA triggered fresh weakness which accelerated after disappointing Fed to probe below last week's low at 105.60 on Thursday.

Daily MA's returned to full bearish setup, as momentum remains in negative territory and maintains bearish bias.

Close below 105.60 would be negative signal for retest of 105.24 (02 Mar low) and possible extension towards psychological 105 support.

Broken 10SMA marks resistance at 106.26 which should limit upticks and guard pivotal barrier at 106.66 (falling 30SMA).

Res: 106.06, 106.26, 106.43, 106.66

Sup: 105.45, 105.24, 105.00, 104.46

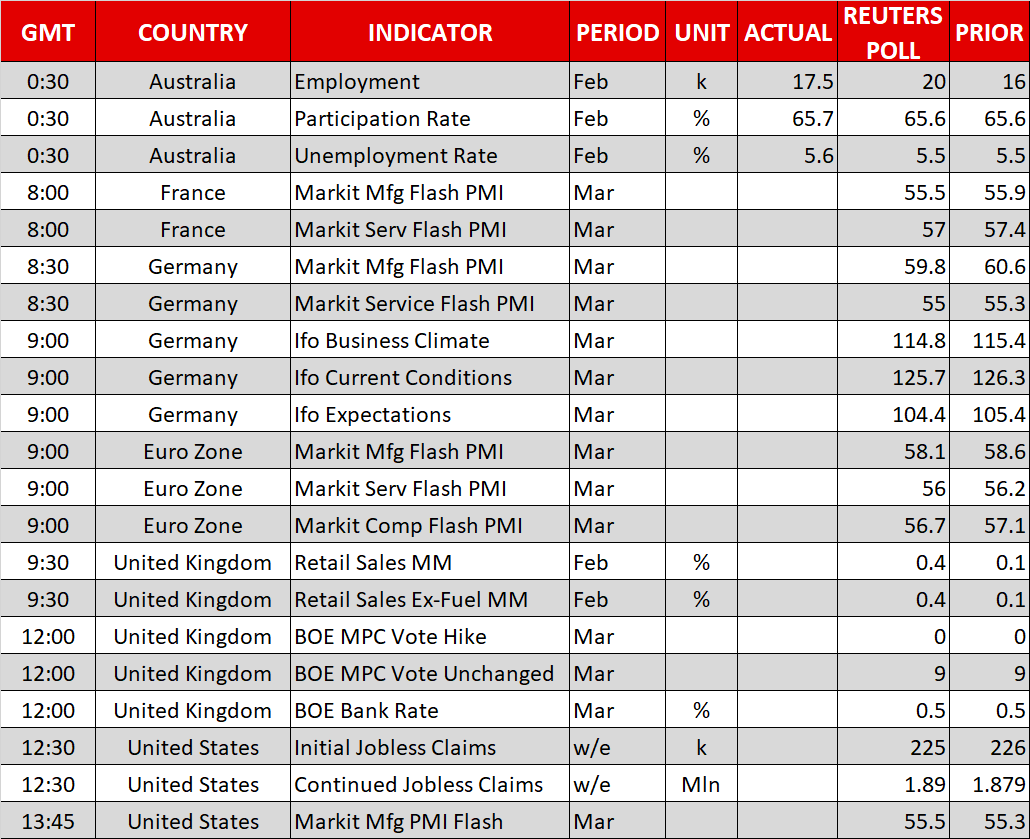

German Ifo business climate dropped to 114.7 as threat of protectionism dampended mood in the economy

German Ifo business climate dropped to 114.7 in March, down from 115.4, slightly above expectation of 114.6.

Ifo expectation dropped to 104.4, down from 105.4, met consensus.

Ifo current assesment dropped to 125.9, down from 126.3, above expectation of 125.6.

Ifo economist Klaus Wohlrabe "the protectionism debate is leaving its mark." And therefore, "export expectations have fallen to their lowest levels in more than a year."

Ifo president Clemens Fuest also echoed that "the threat of protectionism is dampening the mood in the German economy,"

Dollar Extends Declines As FOMC Sticks To 3 Hikes, BoE And US Tariffs Decision In Focus

Here are the latest developments in global markets:

FOREX: The dollar extended its declines from yesterday on Thursday, touching its lowest in nearly two weeks versus a basket of currencies. FOMC policymakers' decision to continue signaling three hikes in total for 2018 was seen as the catalyst behind the US currency's decline.

STOCKS: US markets closed a little lower yesterday in the aftermath of the Fed decision, as the upward revision in the rate projections for 2019 and 2020 raised concerns that this tightening cycle would last longer than previously anticipated. The Nasdaq Composite dropped by 0.3%, while both the S&P 500 and the Dow Jones closed 0.2% lower. Moreover, futures tracking the Dow, S&P, and Nasdaq 100 are all well-into negative territory, pointing to a lower open today, possibly due to reports the US will unveil new tariffs against China today. In Asia, Japan's Nikkei 225 and Topix indices gained 1.0% and 0.65% respectively on their first day back from a public holiday, but in Hong Kong, the Hang Seng was down by more than 0.9%. In Europe, futures tracking all the major indices are currently flashing red.

COMMODITIES: Oil prices traded somewhat lower today, with WTI and Brent crude being 0.1% and 0.2% lower respectively, both benchmarks giving back some of the notable gains they posted yesterday. Both WTI and Brent rose to levels last seen in early February on Wednesday, after the weekly EIA crude inventory data surprisingly showed a drawdown in stockpiles, signaling that US demand remains healthy. The decline in the US dollar was also positive for oil prices yesterday. In precious metals, gold surged yesterday on the back of a declining greenback, reaching its highest level since early March. A weaker US currency makes the dollar-denominated metal appear more appealing for investors using foreign currencies.

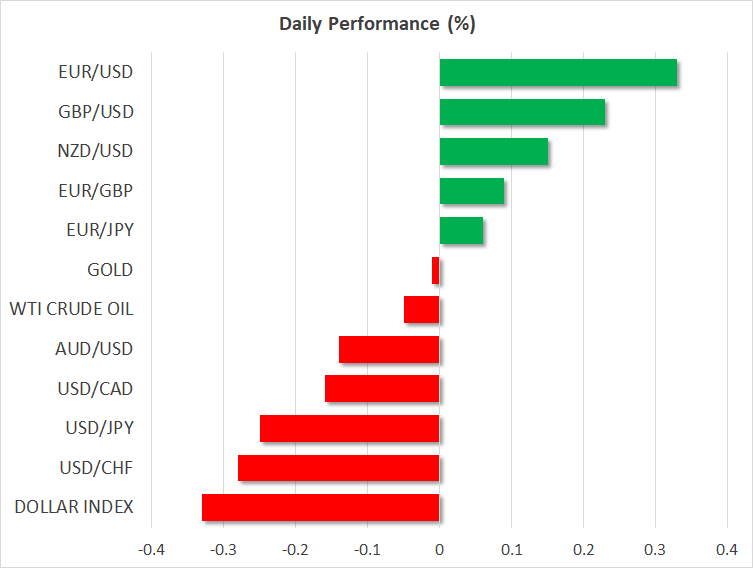

Major movers: Dollar broadly weaker in the aftermath of Fed meeting

The dollar's index against a basket of currencies traded 0.35% lower at 89.47, after losing 0.65% on Wednesday. Earlier on Thursday, the index touched 89.45 at its lowest, a level last tested on March 8. The fall in the dollar came after FOMC members continued to project three interest rate hikes in total for 2018 upon completion of the Fed's meeting on monetary policy on Wednesday. In an environment of rising expectations for four hikes, this was viewed as dollar-negative for market participants who in turn sold off the greenback. Meanwhile, as widely expected, the Fed did raise rates yesterday for the Fed funds rate to enter a target band between 1.50-1.75%.

Interestingly, the dollar was not supported by Fed policymakers' decision to revise upwards their expectations of the number of hikes for 2019 and 2020 on the back of an improving economic outlook according to their view.

Indicative of dollar weakness, the yen, euro and sterling were all building on yesterday's notable gains. At 0732 GMT, dollar/yen was down by 0.25% at 105.74, around a yen below Wednesday's one-week high, while it also recorded a two-week low of 105.55. Euro/dollar was up by 0.35% at 1.2379, recording an eight-day high of 1.2388 previously. Pound/dollar traded higher by 0.25% at 1.4173, close to the one-and-a-half-month high of 1.4177 posted earlier in the day; sterling will be in focus later on Thursday as the Bank of England will be completing its meeting on monetary policy.

Commodity-linked currencies, including the loonie, aussie and the kiwi, which took a beating recently on the back of concerns over global trade, also recorded hefty gains versus the US currency overnight. On Thursday, dollar/loonie traded lower by 0.15% and not far above a nine-day low of 1.2873 hit earlier in the day. Aussie/dollar was 0.15% down after previously posting a six-day high of 0.7783, while kiwi/dollar was up by 0.15%. Australia has strong economic ties with China and an anticipated US tariff announcement on Chinese imports later on Thursday likely weighed on the currency. Meanwhile, data on Australian employment growth were relatively strong – the unemployment rate did rise but that was due to more individuals entering the labor force – while the Reserve Bank of New Zealand held rates steady at the record low of 1.75% as it completed its meeting on monetary policy, providing very few fresh signals on policy.

In emerging markets, dollar/yuan hit a one-week low of 6.3020. The Chinese currency benefitted from the overall weaker greenback but also a firmer fixing of the exchange rate by the PBOC which also proceeded with raising a key short-term interest rate on Thursday.

Day ahead: BoE decides on interest rates, while US prepares to unveil new tariffs

Today, sterling traders will likely focus on the Bank of England's (BoE) rate decision at 1200 GMT. No change in policy is expected, and since this is one of the 'smaller' gatherings without a press conference, investors will probably scrutinize the accompanying statement and the meeting minutes for updated signals on policy. Specifically, for any hints regarding the likelihood of a rate hike at the May meeting, something markets seem to consider very probable judging by the 70% implied probability for such action, according to the UK overnight index swaps.

Any signs suggesting as much – for instance an optimistic assessment of the latest acceleration in wages – could push the May probability higher, alongside the British pound. Conversely, a more cautious stance by the Bank that downplays the likelihood for a near-term hike could spell bad news for sterling. The vote count will also be important. It is forecast to be a unanimous 9-0 for staying on hold, but if some of the more hawkish members like Ian McCafferty dissent and vote for a hike, the pound could rally immediately on the news. The nation's retail sales for February are also due out a few hours ahead of the decision, at 0930 GMT.

Those will not be the only events for the pound though, as the two-day EU summit will also commence today. A transitional Brexit deal has already been largely agreed, and it is simply expected to be formalized at this meeting. Still, many of the details of that deal have not been publicized yet, and the specifics could prove cause for volatility in the pound, as can any comments from the various officials at the summit.

Elsewhere, the 'trade war' narrative is about to get a new chapter, as media reports suggest the Trump administration will unveil new tariffs against Chinese goods as early as today. Besides the details of these tariffs, what will be equally important is the response from Chinese authorities. China noted that it will retaliate in kind to any US tariffs, to which US Trade Representative Robert Lighthizer responded that any Chinese retaliation will be met with new US measures, further amplifying concerns of a tit-for-tat escalation. In case the risk of a trade war increases further, the most vulnerable G10 currencies appear to be the aussie and the kiwi, given that the economies of Australia and New Zealand are highly reliant on commodity exports. Stock indices would probably take a serious hit as well, particularly Japanese benchmarks like the Nikkei 225. Meanwhile, safe havens such as the yen and the Swiss franc could extend their gains.

As for economic data, eurozone's preliminary Markit manufacturing and services PMIs for March will be in focus at 0900 GMT. Expectations are for these indices to decline somewhat, but to still remain safely above the critical 50 barrier, signaling continued expansion in those sectors. In Germany, the Ifo survey for March is due out at 0900 GMT as well, with forecasts pointing to a decline in both the current conditions and the expectations indices.

In the US, the preliminary Markit manufacturing PMI for March and initial jobless claims for the week ended March 16 are due for release.

In equities, Nike will be among companies releasing quarterly results on Thursday.

Finally, in terms of speakers, we will hear from Norges Bank Governor Oystein Olsen at 1615 GMT, as well as BoE Deputy Governor Dave Ramsden, at 1700 GMT. Bank of Canada Deputy Governor Carolyn Wilkins is also due to deliver remarks, at 1845 GMT.

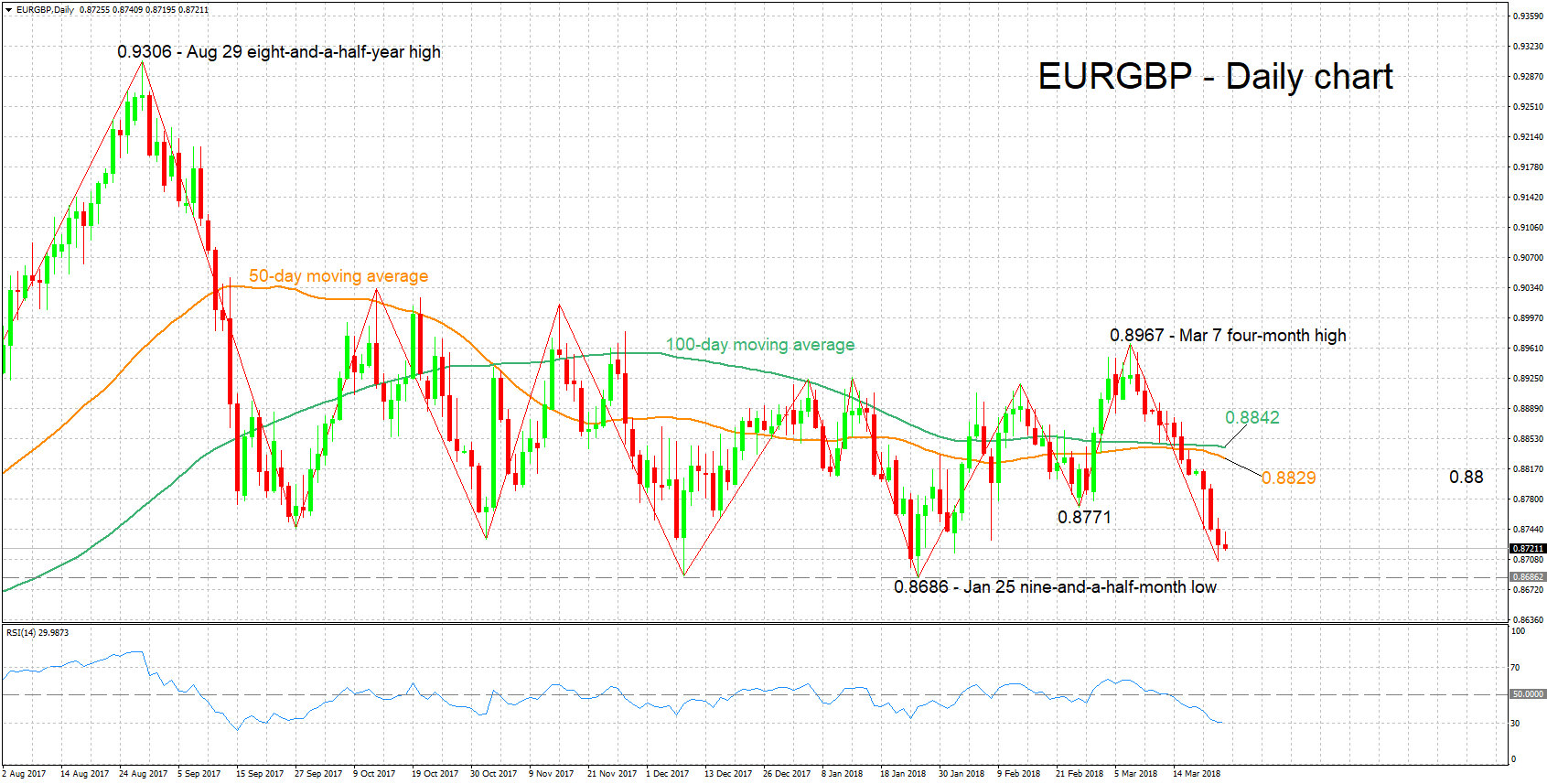

Technical Analysis: EURGBP short-term bearish; trades not far above 2-month low

EURGBP has experienced considerable declines in recent weeks. Specifically, the pair has retreated in all but three of the twelve trading days that followed after it recorded a four-month high of 0.8967 on March 7, while on Wednesday it touched a two-month low of 0.8706. The RSI is declining, pointing to a negative short-term picture; notice also that the indicator has just marginally crossed below the 30 oversold level.

A hawkish stance by the Bank of England later today is likely to see the pair extending its declines. Initial support in this case might come around yesterday's low of 0.8706, with a downside violation turning the focus to the nine-and-a-half-month low of 0.8686 recorded in late January, and even steeper declines shifting the attention to the 0.86 handle that may hold psychological importance.

A cautious tone by the central bank on the other hand, could see the pair advancing. The range around a previous bottom at 0.8771, which also encapsulates the 0.88 round figure and was congested recently, might offer resistance in the event of gains. A barrier to stronger bullish movement could come around the 50- and 100-day moving average lines at 0.8829 and 0.8842 respectively.