Sample Category Title

Pound Dips Despite Sharp Retail Sales

The British pound has headed lower in the Thursday session. In North American trade, GBP/USD is trading at 1.4091, down 0.36% on the day. On the release front, British Retail Sales impressed with a strong gain of 0.8%, beating the estimate of 0.4%. As expected, the Bank of England maintained the benchmark rate at 0.50%. In the US, unemployment claims rose to 229 thousand, higher than the forecast of 225 thousand. On Friday, the US releases durable goods and housing reports.

The Bank of England kept interest rates at 0.50% at its policy meeting on Wednesday. The markets were expecting this, with investors anticipating a rate move at the May moving. This sentiment has gained traction, following the release of the votes cast by MPC members. The markets had expected a unanimous decision to maintain rates at 0.50%, but two of the nine members voted in favor of immediately raising rates. The language of policymakers has become increasingly hawkish, and the MPC votes is another signal that there is a strong likelihood that the BoE will press the rate trigger come May. Earlier in the week, CPI, the primary gauge of consumer inflation, dropped to 2.7% in February. This is good news for consumers, who have seen their purchasing power steadily deteriorate, with inflation levels of around 3% in recent months.

On Wednesday, the Federal Reserve raised rates for the first time this year, in a move that was widely expected. The rate increase of a quarter-point brings the benchmark rate to a range between 1.50% and 1.75%. The markets were looking for any clues with regard to the pace of rate hikes in 2018 – currently the Fed is projecting three hikes, but a robust US economy could push the Fed to press the rate trigger four times. The rate statement did not directly address the issue, but there was a refreshing lack of Fedspeak from policymakers, who said that “the economic outlook has strengthened in recent months”. This phrase has not been used in previous rate statements, and if Fed policymakers reiterate positive sentiment towards the economy, could push the US dollar to higher ground.

Gold Dips Lower After Bullish Fed Statement

Gold has posted strong losses in the Thursday session, after recording strong gains on Wednesday. In North American trade, the spot price for an ounce of gold is $1327.54, down 0.35% on the day. On the release front, unemployment claims rose to 229 thousand, higher than the forecast of 225 thousand. On Friday, the US releases durable goods and housing reports.

Gold propelled to 2-week highs on Wednesday, following gains of over 1 percent. The base metal has reversed directions on Thursday, as the markets digest the Federal Reserve rate statement, which was somewhat hawkish. The Fed raised rates by a quarter-point on Wednesday, marking the first rate hike in 2018. he markets were looking for any clues with regard to the pace of rate hikes in 2018 – currently the Fed is projecting three hikes, but a robust US economy could push the Fed to press the rate trigger four times. The rate statement did not directly address the issue, but there was a refreshing lack of Fedspeak from policymakers, who said that “the economic outlook has strengthened in recent months”. This phrase has not been used in previous rate statements, and underscores a more hawkish stance from the Fed. The markets are expecting the Fed not to skip a beat, with the CME Group pricing another rate hike in May at 96%. This could translate into gains for the US dollar, at the expense of gold and other currencies.

Canada’s CPIs and Retail Sales May Help the Loonie Regain Some Poise

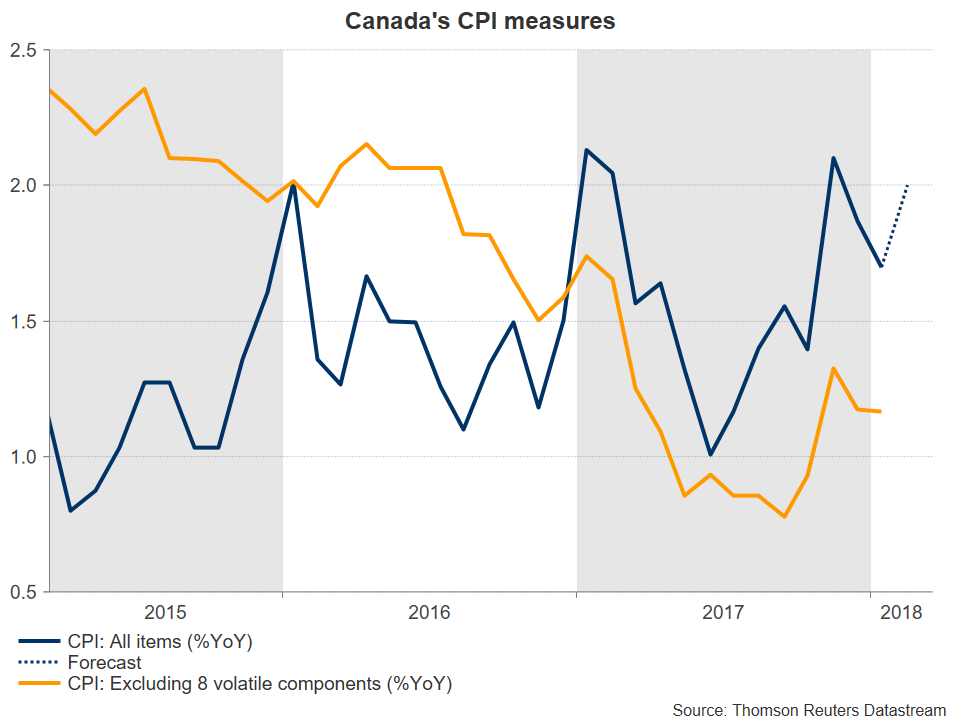

Canada will see the release of its inflation and retail sales data on Friday at 1230 GMT, with forecasts pointing to an acceleration in price pressures and a sharp rebound in consumer spending. While such prints would be pleasant news for the Bank of Canada (BoC) and could benefit the loonie, the currency’s broader direction will also depend to a large degree on how the NAFTA talks progress in the coming weeks.

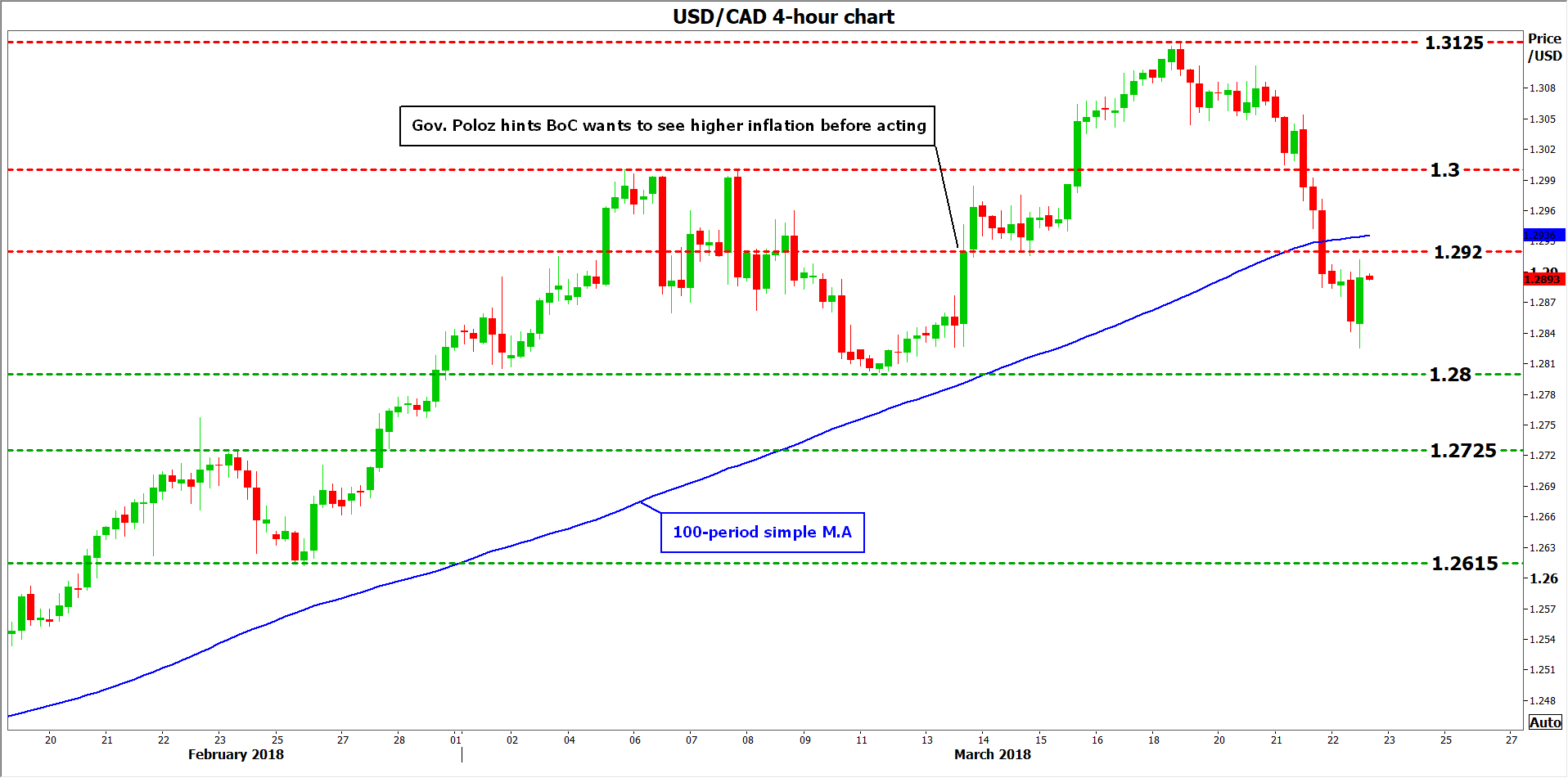

The BoC has gone to great lengths to appear as cautious as it can recently, even while raising interest rates three times since July. While strong economic growth and robust employment gains have encouraged the Bank to begin normalizing its policy, concerns over record-high household debt and the future of free trade agreements like NAFTA have remained a major source of uncertainty for policymakers. As for inflation, even though it has largely remained short of its 2% mark, the Bank has worked under the assumption it will pick up relatively soon. However, recent comments from Governor Poloz suggest policymakers are not particularly convinced this will actually occur soon, and instead prefer to see higher inflation materialize before raising rates more aggressively.

The Bank’s cautious thinking puts all the more emphasis on the upcoming set of inflation and retail sales data. In February, the headline CPI rate is projected to have risen to 2.0% year-on-year from 1.7% previously, while no forecast is available for the core print. As for retail sales, they are anticipated to have risen by 1.1% in January on a monthly basis, after a 0.8% decline previously, while the core figure is also expected to have rebounded sharply. Taken together, such prints would probably be encouraging news for the BoC, as they could signify both that inflation is moving in the desired direction, and that consumer spending did not stall as much as December’s numbers would lead one to believe.

The Bank’s cautious thinking puts all the more emphasis on the upcoming set of inflation and retail sales data. In February, the headline CPI rate is projected to have risen to 2.0% year-on-year from 1.7% previously, while no forecast is available for the core print. As for retail sales, they are anticipated to have risen by 1.1% in January on a monthly basis, after a 0.8% decline previously, while the core figure is also expected to have rebounded sharply. Taken together, such prints would probably be encouraging news for the BoC, as they could signify both that inflation is moving in the desired direction, and that consumer spending did not stall as much as December’s numbers would lead one to believe.

At the time of writing, markets see a 60% probability that the BoC will raise rates again at its May policy meeting, according to Canada’s overnight index swaps. In case these data come in strong, especially on the inflation front, investors may price in a higher probability for a May hike and thereby, help the loonie to recover some of its recent losses. Dollar/loonie could fall back down for a test of the 1.2800 territory, identified by the lows of March 12, while steeper declines may aim for the 1.2725 zone, marked by the February 23 highs. A downside break of that area as well could open the way for the 1.2615 barrier, the February 26 low.

On the flip side, a disappointment in these data could diminish expectations for a near-term rate increase and thereby, bring the loonie under renewed selling interest. Dollar/loonie would likely surge and challenge the 1.2920 zone, which is the 50.0% Fibonacci retracement of the May-September 2017 pullback. If the bulls overcome that hurdle, resistance may be found near the psychological 1.3000 obstacle, while even further advances could bring the 1.3125 area into focus, the pair’s recent highs.

As for which outcome is more probable, gauges of inflation were quite optimistic in February. Canada’s Markit manufacturing PMI for February showed that factory gate price inflation held close to its highest seen for seven years, supporting the forecast for an acceleration in consumer prices.

As for which outcome is more probable, gauges of inflation were quite optimistic in February. Canada’s Markit manufacturing PMI for February showed that factory gate price inflation held close to its highest seen for seven years, supporting the forecast for an acceleration in consumer prices.

In the bigger picture, besides speculation around the BoC, the loonie’s broader direction will also depend to a large extent on how the “protectionism theme” plays out and how the NAFTA negotiations progress. The next round of NAFTA talks is tentatively scheduled for mid-April, while the next BoC meeting is planned for the 18th of April. Unless there is substantial progress in the trade talks that alleviates some uncertainty by then, the loonie may find it difficult to rally even if the BoC strikes a hawkish tone.

Yen Rally Continues as Dollar Broadly Weaker

The Japanese yen has posted considerable gains in Thursday trade. In the North American session, USD/JPY is trading at 105.41, down 0.62% on the day. Japanese data was a disappointment. Flash Manufacturing PMI slowed to 53.2, missing the estimate of 54.3 points. As well, All Industries Activity declined 1.8%, shy of the estimate of -1.7%. Later in the day, Japan releases National Core CPI, which is expected to tick higher to 1.0%. In the US, unemployment claims rose to 229 thousand, higher than the forecast of 225 thousand. On Friday, the US releases durable goods and housing reports.

On Wednesday, the Federal Reserve raised rates for the first time this year, in a move that was widely expected. The rate increase of a quarter-point brings the benchmark rate to a range between 1.50% and 1.75%. The markets were looking for any clues with regard to the pace of rate hikes in 2018 – currently the Fed is projecting three hikes, but a robust US economy could push the Fed to press the rate trigger four times. The rate statement did not directly address the issue, but there was a refreshing lack of Fedspeak from policymakers, who said that “the economic outlook has strengthened in recent months”. This phrase has not been used in previous rate statements, and if Fed policymakers reiterate positive sentiment towards the economy, could push the US dollar to higher ground.

There are some new faces in the senior management of the Bank of Japan, but the “hold the course” mantra remains the same. On Tuesday, two new deputy governors, Masayoshi Anamiya and Masazumi Wakatabe, were elected to 5-year terms. On Wednesday, Anamiya said that “conceptually and theoretically, we haven’t hasn’t ruled out the possibility of adjusting the yield curve”, leaving the door open to raising rates even if inflation remains shy of the 2 percent target. However, Anamiya added that the Bank has not reached the point of having to make such a decision. In other words, the markets should not expect any changes in the bank’s ultra-accommodative policy for the foreseeable future.

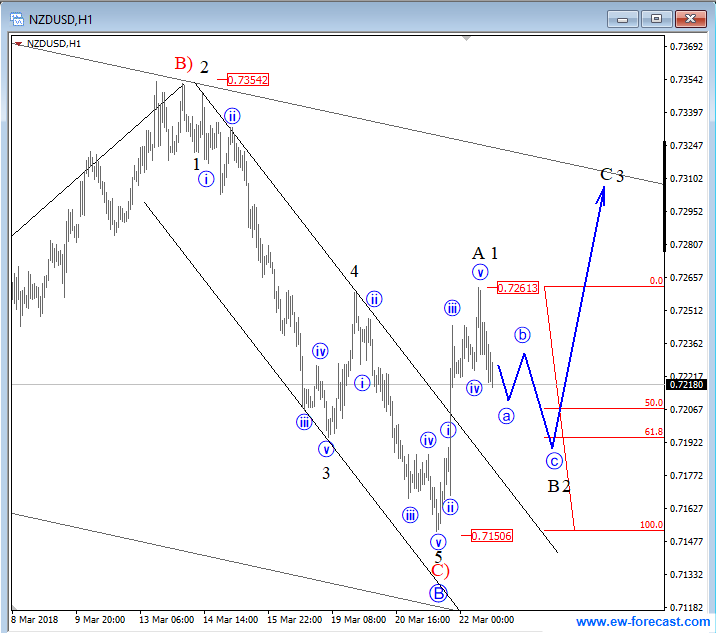

Elliott Wave Analysis: NZDUSD Showing A Sign For More Bullish Activity

NZDUSD made a strong and sharp breach recently, out of a Elliott wave channel, which we see it as a confirmation that higher degree red wave C) is completed, and that a change in trend from bearish to bullish can be here. As such we expect a minimum three-wave reversal to follow, with wave A or 1 leading the way. That said, we can see that wave A or 1 is completed at the 0.7261 level so current minor drop can be a temporary correction labeled as wave B or 2 in progress, which can see support and a bounce near the 0.7206-0.7192 region.

NZDUSD, 1H

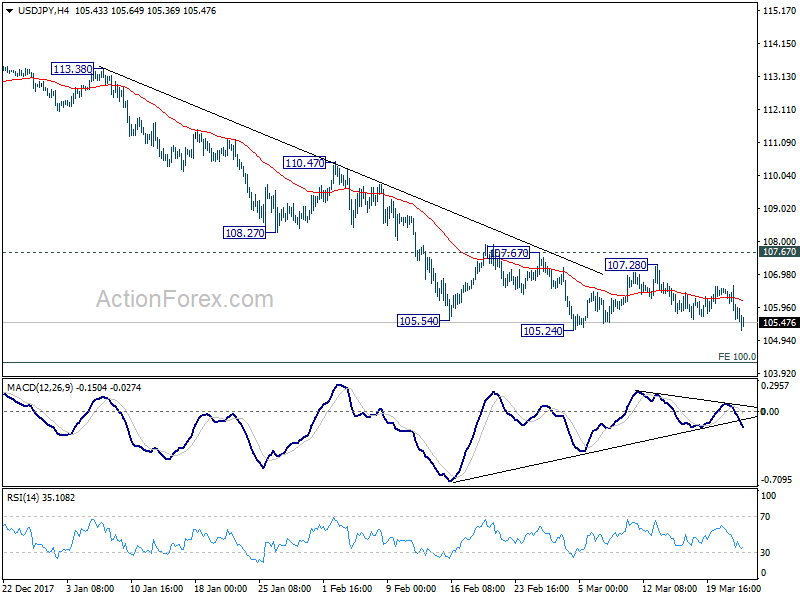

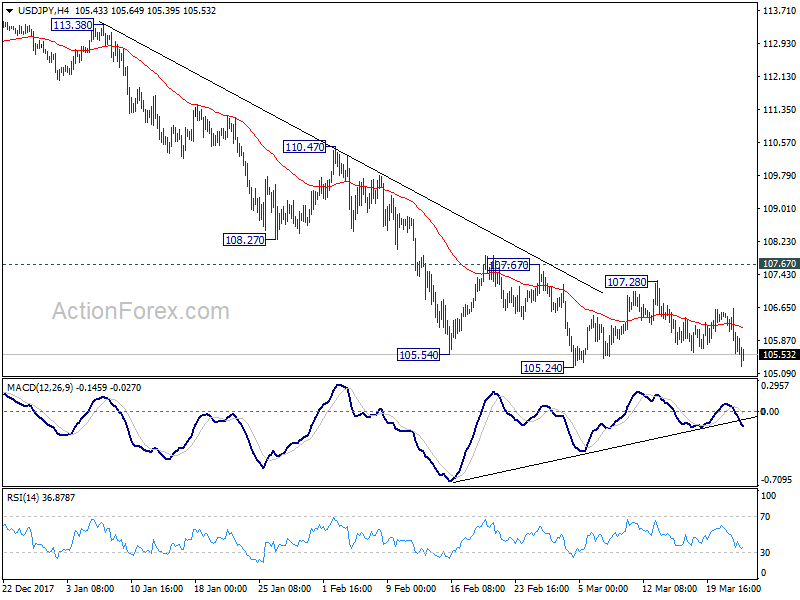

USDJPY Stands Ticks ahead of 105.24 Support, Awaiting US Tariff Announcement

Bears took full control on Thursday and the pair extended weakness into second straight day, hitting session low at 105.26, two ticks above key support at 105.24 (02 Mar low).

Firm bearish setup of daily techs is reinforced by dollar’s negative sentiment after Fed and rising demand for safe haven yen on strong trade war concerns.

All eyes are on announcement of US tariffs on China, which could spark stronger fall of USDJPY pair on risk aversion.

Firm break of key 105.24/00 supports would expose 104.04 (Fibo 76.4% of 99.53/118.60 ascend) and could expose psychological 100 support on stronger bearish acceleration, depending on decision of the US regarding import tariffs.

Falling Tenkan-sen line marks solid resistance at 106.27, while descending 30SMA remains pivotal barrier (currently at 106.65) and only firm break here would neutralize bearish threats.

Res: 105.57; 105.96; 106.27; 106.65

Sup: 105.24; 105.00; 104.46; 104.04

Sunset Market Commentary

Markets:

Global core bonds extended yesterday's rebound, but for different reasons. The corrective bull steepening after yesterday's FOMC meeting didn't continue in Asian dealings or at the start of European trading. Disappointing EMU PMI's nevertheless generated a new bid in core bonds, with this time mainly the longer end of the curve profiting. The move accelerated after investors added the stock market sell-off to the equation. Risk sentiment deteriorated ahead of US President Trump's expected announcement of additional tariffs against China. The uncertain nature of China's reply is worrisome as well. The US yield curve bull flattens at the time of writing with yields 2.3 bps (2-yr) to 6.3 bps (30-yr) lower. The US 10-yr yield approaches 2.8% support. German yields drop between 2.1 bps (2-yr) and 5.5 bps (10-yr). 10-yr yield spread changes versus Germany widen up to 2 bps with Portugal (+8 bps) and Greece (+12 bps) underperforming.

EUR/USD briefly rallied further at the start of European dealing as a slight 'disappointment' on the Fed's rate hike commitment weighed on the dollar. However, dollar negativism eased soon as markets realized that Fed policy normalization remains firmly in place. EMU PMI's again missed the consensus by a big margin, capping potential euro gains. EUR/USD drifted lower in the 1.23 big figure. Risk sentiment turned further negative. This was neutral for EUR/USD (currently 1.2325 area). USD/JPY declined to the 105.25/30 area, but regained a few ticks later. EUR/JPY dropped temporary below 130, but yen buying eased as US equities tried to fight back after initial losses.

The UK calendar contained two interesting features today: February retail sales and the BoE's policy decision. Retail sales were slightly stronger than expected at 0.8% M/M, but the January release was downwardly revised and December was also very weak. So, Q1 private consumption looks rather poor. Sterling tried a cautious up-tick, but the move stalled soon. The BoE as expected left is policy rate (0.5%) and the stock of asset purchases unchanged, but two members voted to raise the base rate (7-2 vote). Sterling spiked higher on the announcement. EUR/GBP tested 0.8688 support, but a sustained break didn't occur. EUR/GBP trades in the 0.8725/30 area. The MPC minutes retained the assessment of the February inflation report that excess demand growth during the policy horizon warrants a gradual, but limited tightening. The BoE left the door open for a May rate hike, but this wasn't really a surprise anymore. Today's price action confirms that the 0.8688/52 support doesn't give away that easily.

News Headlines:

The Bank of England kept interest rates steady, but two policymakers unexpectedly voted for a hike, boosting confidence among investors that borrowing costs will rise in May for only the second time since the 2008 financial crisis. The statement and Minutes largely resembled the February inflation report. UK retail sales rose more than expected in February as spending at supermarkets jumped, but a poor month for non-food stores suggests the squeeze on living standards is continuing to weigh on consumers.

The euro area's private-sector economy grew at the slowest pace in 14 months in March, as service providers and factories struggled to keep up with demand. The EMU composite PMI slid to 55.3 from 57.1 (vs 56.8 consensus). On a national level, both German and French PMI's disappointed. German Ifo investor confidence faced a small setback in March, both in the expectations and current assessment components, but the outcome was near forecasts.

The Polish central bank's next move in interest rates might be a cut, central banker Zyzynski said, adding there was currently no reason to change the level of interest rates. Zyzynski's comments reflect the stance of central bank Governor Glapinski.

DOW gaps lower as Trump is ready to start trade war, USD/JPY pressing 105.24 support

DOW gaps lower today and selling then intensifies in the second hour. The index is now trading down -1.5% at the time of writing. Worry on trade war is seen as a major bearish factor for stocks. And risk aversion also a major reason for Yen's broad based strength for today. Trump is set to announce his tariffs targeted at China today. Testifying to Senate finance committee, Trade Representative Robert Lighthizer said the US has done a study on Intellectual Property theft problem of China. And the trade department is looking into at building a better fairer system.

For DOW, it's on course for support zone between 23.6% retracement of 26616.71 to 23360.29 at 24128.80 and 24217.76. This zone will be key to determine DOW's near term direction. Rebound from there will change the prior triangle like pattern into a sideway range. And there would then be prospect of revisiting 25000 and above soon. However, sustained break of this support zone will argue that it's now in the third wave of the pattern from 26616.71 and should have a test on 23360.29 support and below. For the moment, we're favoring the latter scenario.

USD/JPY is at a tricky point close to 105.24 support now. 4 hour MACD suggests that it's on verge of breakout. And, firm break there will at least extend recent decline to medium term projection level of 100% projection of 118.65 to 108.12 from 114.73 at 104.20.

USD/JPY is at a tricky point close to 105.24 support now. 4 hour MACD suggests that it's on verge of breakout. And, firm break there will at least extend recent decline to medium term projection level of 100% projection of 118.65 to 108.12 from 114.73 at 104.20.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.73; (P) 106.18; (R1) 106.49; More...

USD/JPY drops to as low as 105.25 so far and is set to test 105.24 low. As noted before, near term outlook is bullish with 107.67 resistance intact. Firm break of 105.24 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. On the upside, break of 107.67, however, will indicate near term reversal and turn outlook bullish for stronger rebound to 110.47.

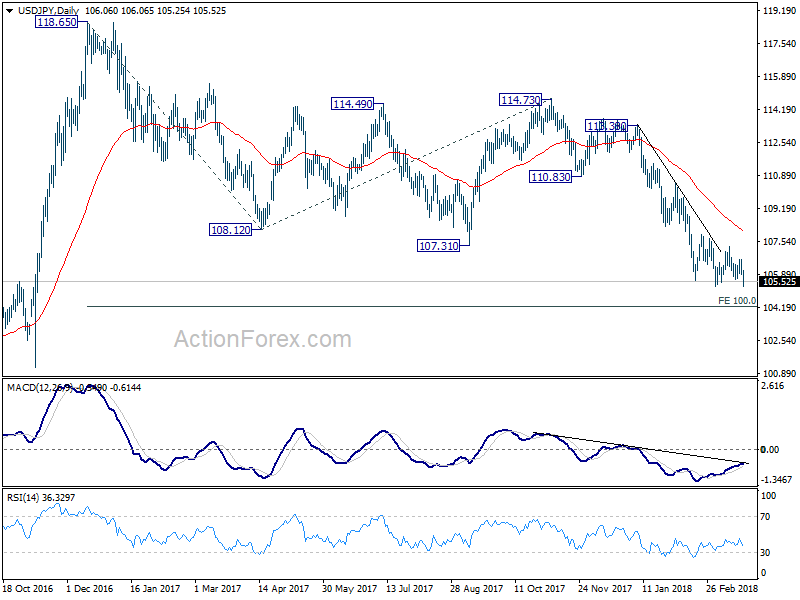

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2268; (P) 1.2309 (R1) 1.2378; More....

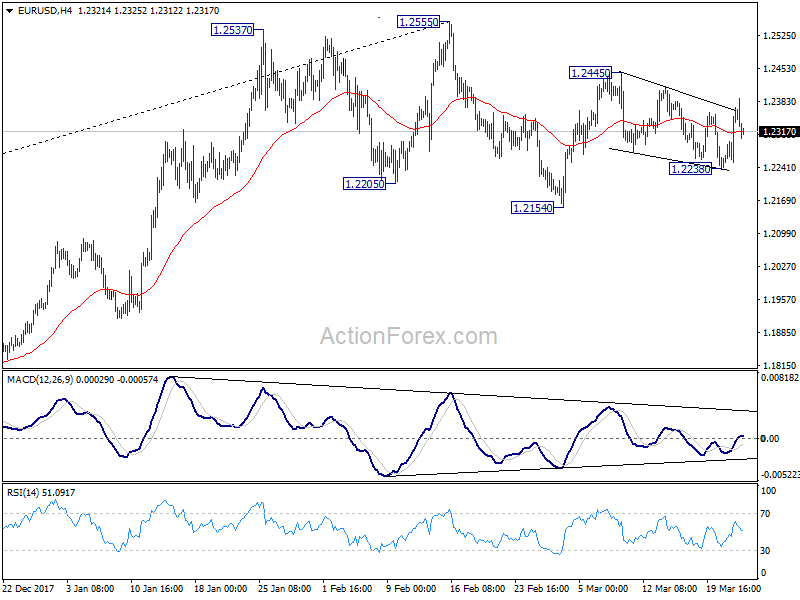

EUR/USD dips sharply after hitting 1.2388 but there is no change in the bullish view. That is, price actions from 1.2445 is a corrective pattern in form of falling wedge. And, it might be completed at 1.2238 already. Further rise should be seen to 1.2445 first. Break will resume whole rebound from 1.2154 and target 1.2555 high, which is close to 1.2516 key long term fibonacci level. On the downside, however, firm break of 1.2238 will turn bias back to the downside, to resume the fall from 1.2555 through 1.2154.

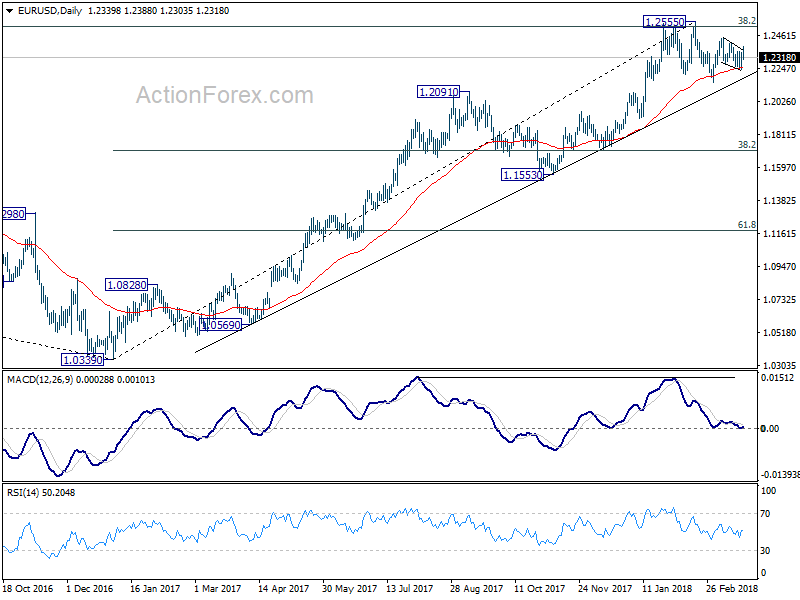

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.