Sample Category Title

(FED) FOMC Statement Mar 21, 2017

Information received since the Federal Open Market Committee met in January indicates that the labor market has continued to strengthen and that economic activity has been rising at a moderate rate. Job gains have been strong in recent months, and the unemployment rate has stayed low. Recent data suggest that growth rates of household spending and business fixed investment have moderated from their strong fourth-quarter readings. On a 12-month basis, both overall inflation and inflation for items other than food and energy have continued to run below 2 percent. Market-based measures of inflation compensation have increased in recent months but remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The economic outlook has strengthened in recent months. The Committee expects that, with further gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace in the medium term and labor market conditions will remain strong. Inflation on a 12-month basis is expected to move up in coming months and to stabilize around the Committee's 2 percent objective over the medium term. Near-term risks to the economic outlook appear roughly balanced, but the Committee is monitoring inflation developments closely.

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 1-1/2 to 1-3/4 percent. The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant further gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

Voting for the FOMC monetary policy action were Jerome H. Powell, Chairman; William C. Dudley, Vice Chairman; Thomas I. Barkin; Raphael W. Bostic; Lael Brainard; Loretta J. Mester; Randal K. Quarles; and John C. Williams.

Will BoE Lay the Foundations For May Rate Hike?

Guidance Key in BoE Minutes on Thursday

Brexit, trade wars, slow economic growth and heightened tensions with Russia, what kind of central bank would consider raising interest rates when the country is facing such challenges? That’s exactly what the Bank of England is doing and on Thursday, they may signal and intention to do so at the next meeting in May.

It is worth pointing out firstly that this is only half the story. The country is also experiencing high inflation, a 43-year low in unemployment and rising wages against a backdrop of strong global growth. The Bank of England is not exactly in an enviable position.

UK Unemployment

UK Average Earnings

UK Average Earnings

UK Inflation

UK Inflation

To make matters more confusing, inflation has fallen from its highs and was lower than expected in February, with the core number only 0.4% above target. Wage growth is improving but from a low base and remains moderate. And finally Brexit talks are progressing, with the transition deal at the start of the week another major hurdle that’s been overcome. It’s no wonder people can’t agree on the correct course of action.

To make matters more confusing, inflation has fallen from its highs and was lower than expected in February, with the core number only 0.4% above target. Wage growth is improving but from a low base and remains moderate. And finally Brexit talks are progressing, with the transition deal at the start of the week another major hurdle that’s been overcome. It’s no wonder people can’t agree on the correct course of action.

Why Are Investors So Confident That Rates Are Rising Then?

The language from policy makers is becoming increasingly hawkish and last month it claimed that tightening (rate hikes) would have to come “somewhat earlier and by a somewhat greater extent” that it expected in November.

It’s because of this that market expectations of a rate hike in May – when the next inflation report is released – are so high. Clearly the central bank is trying to provide clear guidance that interest rates will rise in the near future and May would represent a logical time to do so.

Investors are even looking past small changes in the data that may ordinarily make the BoE question their decision to hike rates – inflation falling more than expected – because the central bank will want to avoid credibility questions arising again if it changes its mind.

What Are We Looking For on Thursday and What Impact Will it Have?

Taking all of the above into consideration, it’s logical then that the Monetary Policy Committee will make clear in Thursday’s minutes its intention to raise interest rates in May, which is what traders will be looking for. Any indication that it may be having doubts could hit the pound, given how priced in a May rate hike now is.

The interesting thing with the charts is that, with all the good Brexit transition news now priced in – subject to sign off by EU leaders later in the week – and a rate hike also priced in, I wonder how much more upside the pound will see and whether we may instead see profit taking shortly after the release. The pound has certainly rallied strongly recently in anticipation of it all, particularly against the euro but I wonder what it has left in the tank.

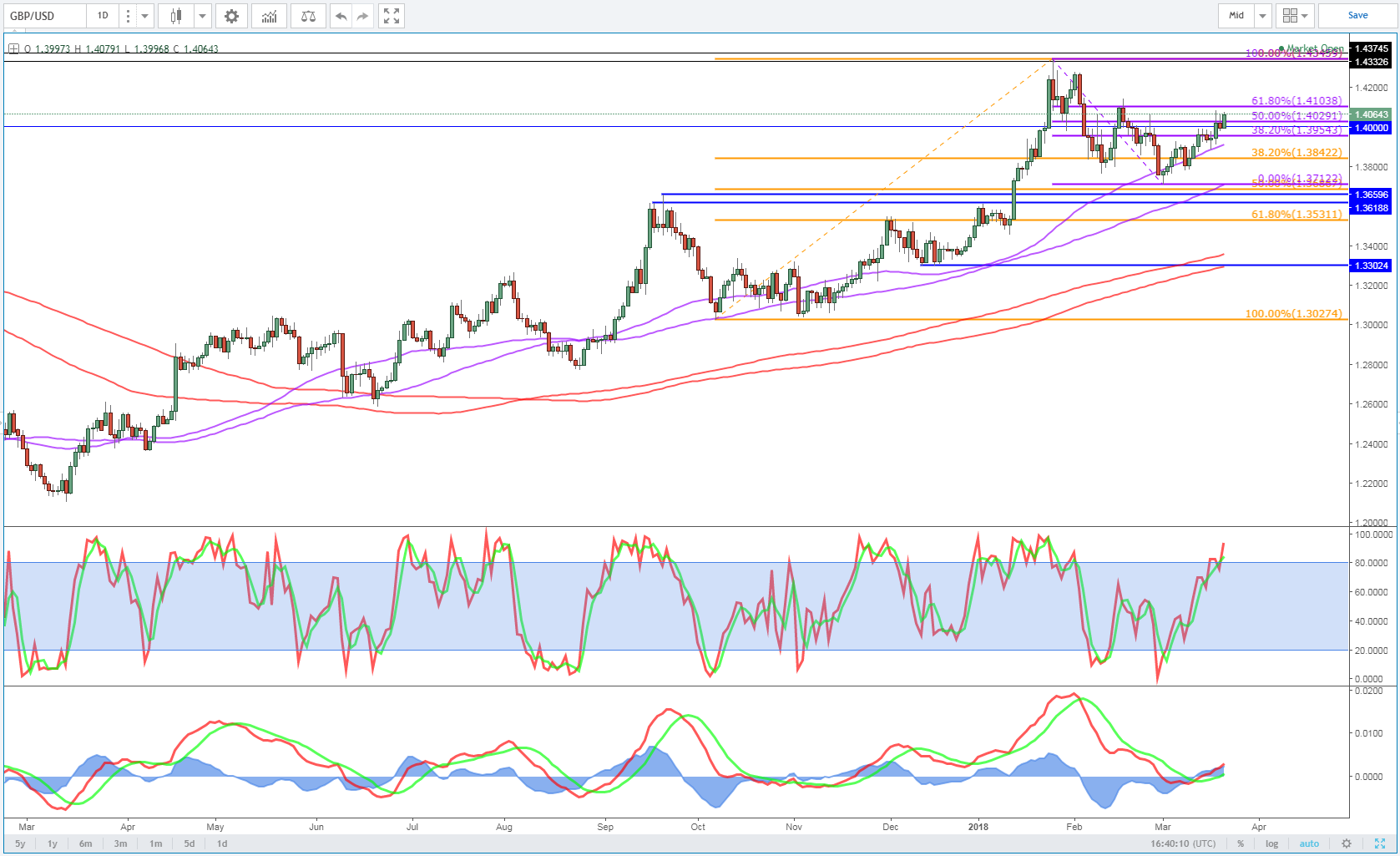

GBPUSD Daily Chart

GBPJPY Daily Chart

GBPJPY Daily Chart

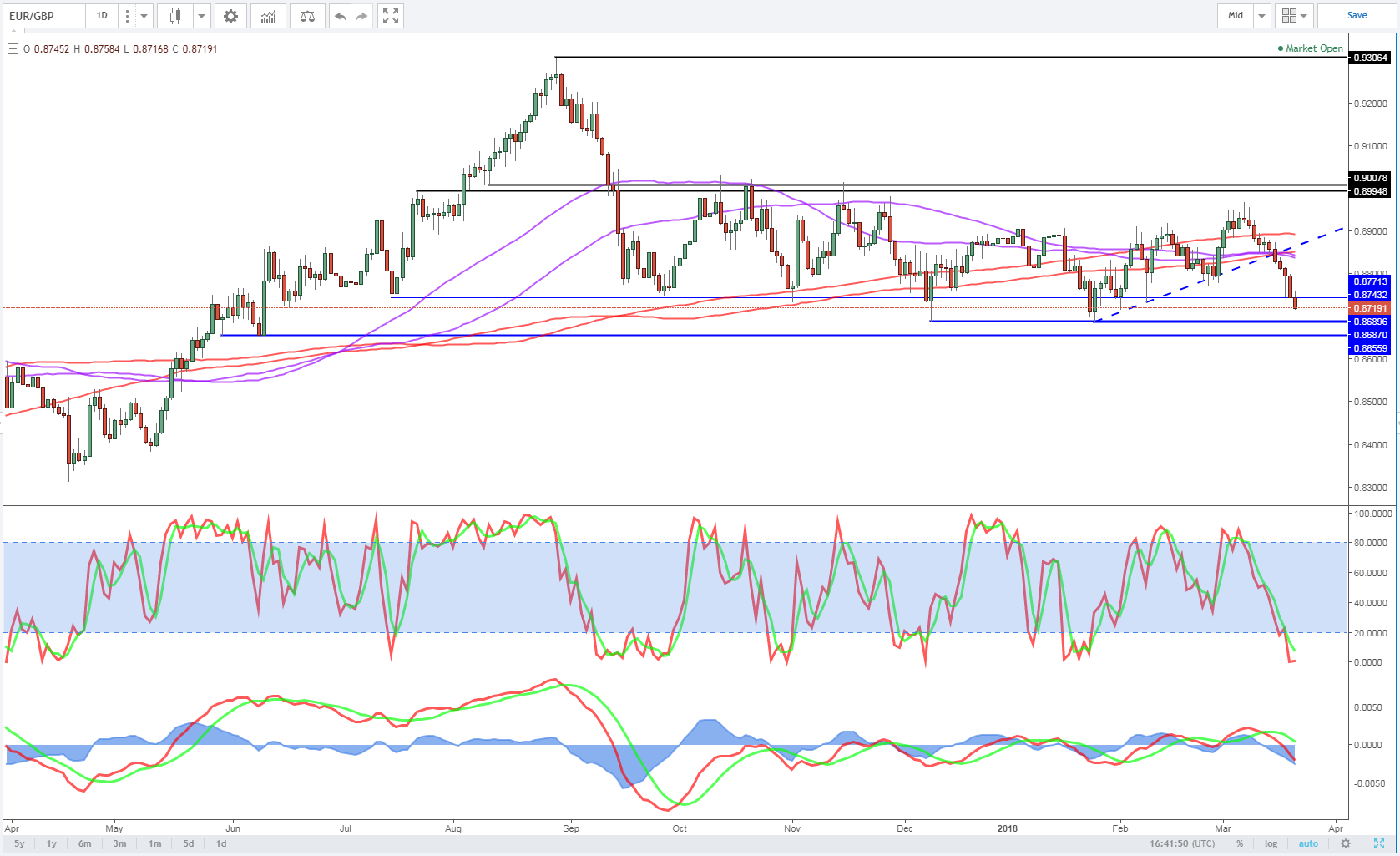

EURGBP Daily Chart

EURGBP Daily Chart

Gold Jumps as Investors Eye Fed Rate Announcement

Gold has posted strong gains in the Wednesday session. In North American trade, the spot price for an ounce of gold is $1324.61, up 1.02% on the day. On the release front, the current account deficit widened to $128 billion, above the estimate of $125 billion. In economic news, the US, the current account deficit widened to $128 billion, above the estimate of $125 billion. On the housing front, Existing Home Sales jumped to 5.54 million, easily beating the estimate of 5.41 million. All eyes are on the Federal Reserve, which is expected to raise the benchmark rate to a range of between 1.50% and 1.75%. On Thursday, the US releases unemployment claims.

Gold prices continue to show movement ahead of the Federal Reserve rate announcement later on Wednesday. The meeting will mark a host of firsts – the Fed is expected to raise rates for the first time in 2018, and Fed Chair Jerome Powell will preside as chair of the FOMC for the first time, followed by Powell’s first post-FMOC press conference. The Fed has sounded marginally more hawkish recently – will this trend continue in the rate statement? The Fed rate projection remains at three rates for 2018, but with the US economy continuing to perform well, this forecast could be revised upwards to four rates. If the rate statement is unexpectedly hawkish, gold could give up some of Wednesday’s gains.

After months of rough rhetoric between Britain and the EU, the two sides announced that there would be a transition period following the UK’s departure from the EU in March 2019. The transition deal will kick in at that time, lasting until December 2020. The deal covers the rights and status of EU citizens in the UK and British citizens in the EU, and allows the UK to pursue new trade agreements during that time. There are still some issues to iron out, such as the Northern Ireland border. The transition period is a major, positive development, in that it will enable Britain to enjoy the benefits of the common market, albeit without a seat at the table. The positive news could raise investor risk appetite and weigh on gold prices.

Japanese Yen Ticks Higher, Fed Decision Looms

The Japanese yen is lower in Tuesday trade. In the North American session, USD/JPY is trading at 106.38, down 0.15% on the day. In Japan, Flash Manufacturing PMI is expected to improve to 54.3 points. In the US, the current account deficit widened to $128 billion, above the estimate of $125 billion. On the housing front, Existing Home Sales is forecast to rise to 5.41 million. All eyes are on the Federal Reserve, which is expected to raise the benchmark rate to a range of between 1.50% and 1.75%. On Thursday, the US releases unemployment claims.

The Bank of Japan has appointed two new deputy governors, Masayoshi Amamiya and Masazumi Wakatabe, to 5-year terms. On Wednesday, Anamiya said that "conceptually and theoretically, we haven't hasn't ruled out the possibility of adjusting the yield curve", leaving the door open to raising rates even if inflation remains shy of the 2 percent target. However, Anamiya added that the Bank has not reached the point of having to make such a decision. In other words, the bank is planning to maintain its ultra-accommodative policy for the foreseeable future.

The markets are keeping a close eye on the Federal Reserve, which will release a rate statement later in the day. The Fed is expected to raise rates for the first time in 2018, and Fed Chair Jerome Powell will preside as chair of the FOMC for the first time, followed by Powell's first post-FMOC press conference. The Fed has sounded marginally more hawkish recently – will this trend continue in the rate statement? The Fed rate projection remains at three rates for 2018, but with the US economy continuing to perform well, this forecast could be revised upwards to four rates. If the rate statement is unexpectedly hawkish, the US dollar could respond with gains.

Sunset Market Commentary

Markets:

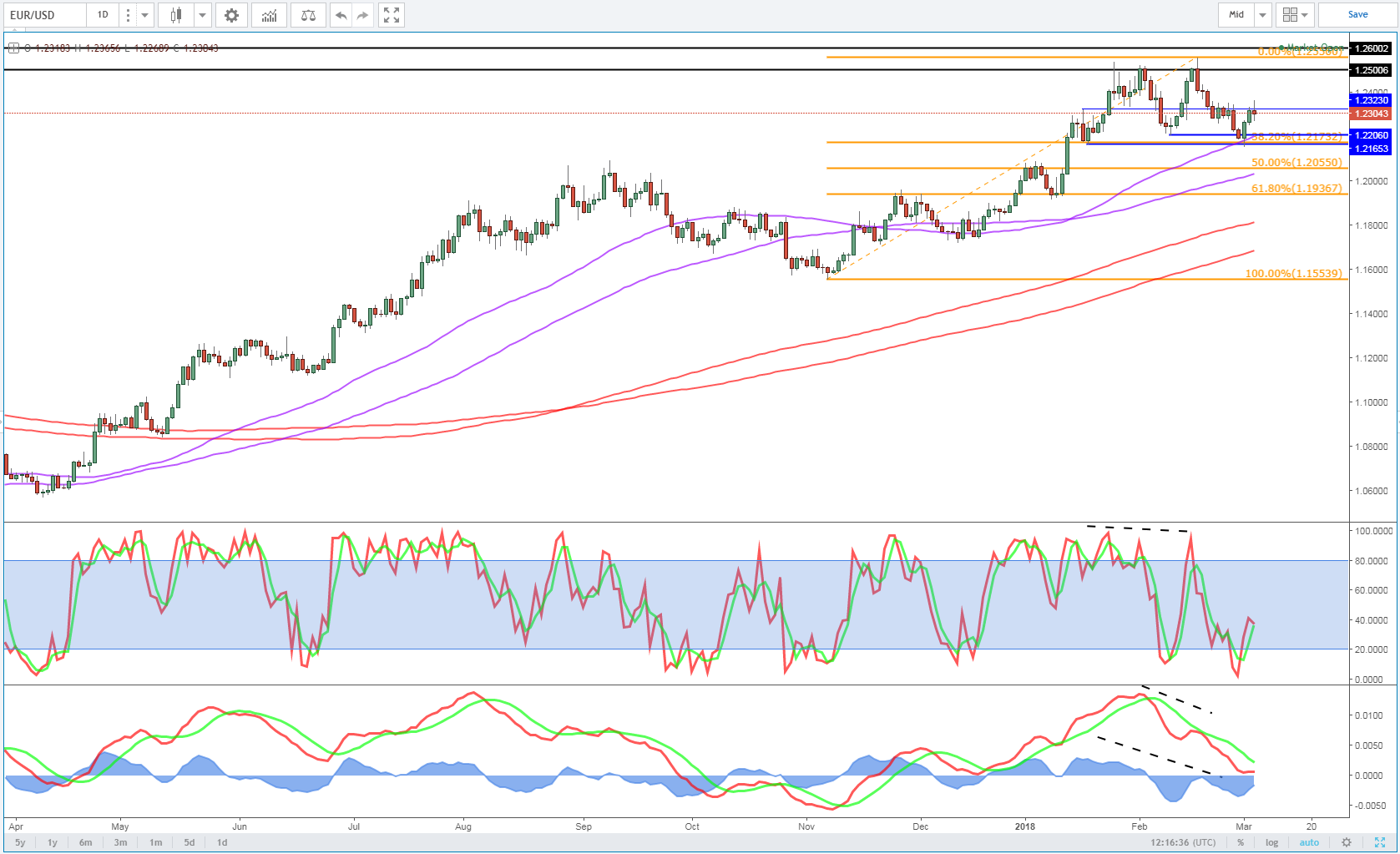

Moves on core bond markets and in EUR/USD was confined to extremely thin ranges ahead of tonight’s FOMC meeting. Bonds had a marginal downward bias (+1 bp in yield terms) via selling pressure in UK Gilts. US yields added another 6 bps across the curve. EUR/USD regained a small part of yesterday’s losses and heads towards 1.23. New weakness on stock markets could be at play as well. Brent crude oil extends its rebound to $68.50/barrel, the highest level since early February. Inventory data and fear about a hawkish shift by the US towards Iran underpin prices.

The Fed will hike its policy rate tonight, but we also expect changes to the dot plot. More specifically, we expect a higher estimation of the neutral rate (3% from 2.75%) and a potential shift already in 2018 (4 from 3) and/or 2019 dots. Markets partly frontrunned on the short term shift, but don’t anticipate a higher neutral rate. Therefore, we mainly expect a sell-off a the longer end of the US yield curve. The Fed’s gradual lowering of its neutral rate from 4.25% in 2012 to 2.75% worked as a cap above the US 10-yr yield. Reversing these dynamics lifts scope for higher long term yields, especially if we add the prospect that the US’ fiscal policy will lead to a significant increase in twin deficits in the longer run. Technically, 3.07% is KEY resistance. A higher neutral rate suggests that we might go for a test in coming days. Medium term, we position for a break higher. If our dots-scenario materializes, there is room for a ST USD rebound. EUR/USD 1.2155 is the first important support. A break opens the way to the 1.20 area. The gain in USD/JPY might be more modest than in USD/EUR.

Sterling maintained its constructive momentum today which started after the EU/UK transition agreement reached earlier this week. Brexit tensions are now moving more the background and the market focus turned to the UK eco data and the BoE. The UK labour market report was stronger than expected with solid job growth. UK average weekly earnings rose to 2.8% Y/Y, better than the 2.6% expected. The data keep the door open for the BoE to raise its policy rate at the May meeting. They might already give some more hints at tomorrow’s policy meeting. Sterling succeeded some further gains against the euro and the dollar. EUR/GBP filled bids in the 0.8725 area. The 0.8700/0.8688 support area is coming within reach. We still assume that more sterling gains below this support area will become more difficult. Cable rebounded north of 1.40.

News Headlines:

British workers' overall pay rose at the fastest pace in more than two years during the three months to January (2.8% Y/Y), bolstering the chances that the BoE will raise borrowing costs in May. Wages excluding bonuses rose by 2.6% Y/Y. The ONS said the number of people in work grew by 168k (+84k expected) in the three months to January. The data also showed the unemployment rate edged back down to its four-decade low of 4.3%. The number of unemployment benefit claimants rose by 9,200 to 838,000 in February.

Former PM Berlusconi wants the centre-right to team up with the 5-Star Movement to form a government with a pre-determined agenda, La Repubblica newspaper reported.

Faced with mounting trade offensives from Washington, China is preparing to hit back with tit-for-tat tariffs aimed at President Trump’s support base, including levies targeting US agricultural exports from Farm Belt states, according to people familiar with the matter.

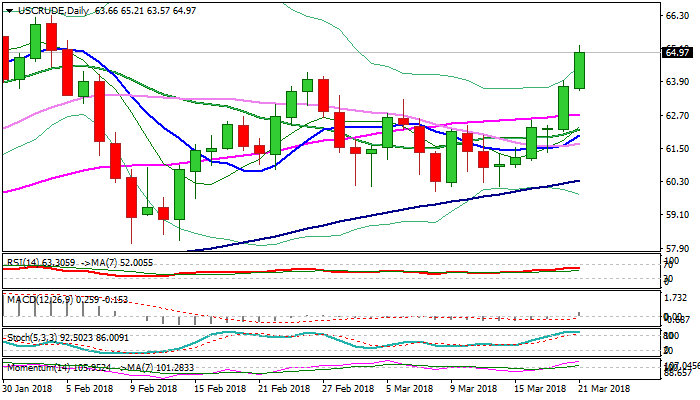

WTI OIL Extends Rally above $65 after Another Unexpected Fall in Oil Inventories

WTI oil hit the highest levels in over six weeks on probe above psychological $65.00 barrier on Wednesday, on fresh bullish acceleration after US crude stocks unexpectedly fell by 2.62 million barrels, compared to forecast for 2.6 million barrels build, EIA report showed.

Oil prices continue to trend higher despite concerns about increasing production of US oil which reached 10.4 million barrels per day, above the output of Saudi Arabia and around levels of oil production in Russia, the biggest oil producer in the world.

Signals of geopolitical tensions in the Middle East and strong falls in crude inventories keep oil prices well supported.

Today’s break above previous high at $64.22, surge through Fibo 76.4% barrier at $64.62 and lift above $65.00, mark an extension of strong Tuesday’s bullish acceleration and continuation of bull-leg from higher base formed at $60.00 zone.

With strong bullish sentiment in play and firmly bullish techs, rally could extend towards next significant barriers at $66.23/28 (01/02 Feb double-top) and key med-term barrier at $66.64 (25 Jan peak), the highest of two-year recovery rally from $26.04 (11 Feb 2016 low).

Consolidative / corrective action could be anticipated in the near-term as slow stochastic is strongly overbought on daily chart, but so far without any stronger bearish signal.

Res: 65.21; 65.38; 65.85; 66.28

Sup: 64.62; 64.22; 63.57; 63.26

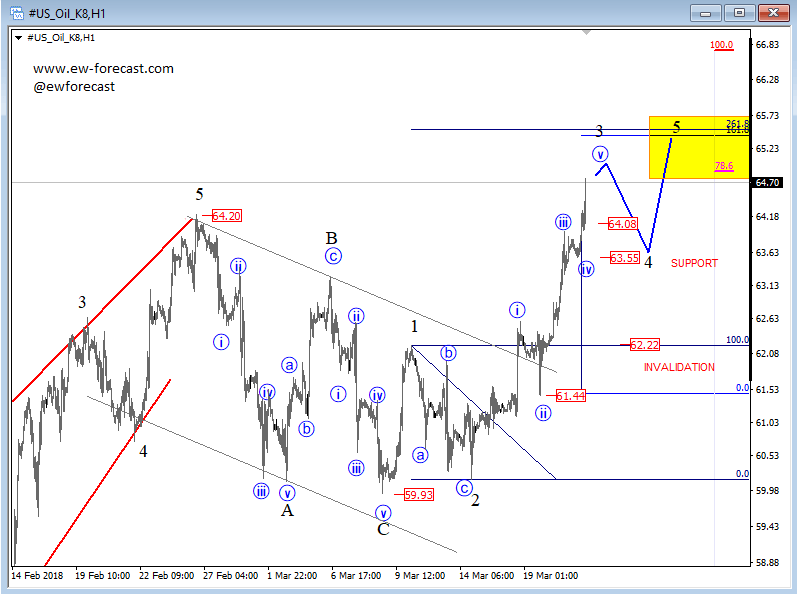

Elliott Wave Analysis: Crude Oil Making A Strong Bullish Run

Crude Oil is making a strong and clear impulsive recovery, which we think is part of a bigger bullish cycle. Specifically, we see price making a five-wave rally within black wave 3, which can see a temporary top and a reversal near the 65.00 area. That being said, once wave 3 fully unfolds, a new temporary pullback as wave 4 may show up, which can later see possible support around the 64.08-63.55 zone. Invalidation level is at 62.22.

Crude oil, 1h

U.S. Existing Home Sales Rise in February, Ending a Two-Month Slump

Existing home sales rose by 3% m/m to 5.54 million units (annualized) in February, exceeding market expectations for a modest gain of 0.4% m/m.

All of the increase and then some was concentrated in the larger single-family segment where sales rose by 4.2% to 4.96 million units. Meanwhile, activity declined in the smaller condo/co-op segment (-6.5% m/m).

Activity was mixed across the country. Sales rebounded quite strongly in the South (+6.6% m/m) and West (+11.4% m/m), helping to offset a large decline in the Northeast (-12.3% m/m) and a modest one in Midwest (-2.4% m/m). Sales in the Northeast have been falling for three consecutive months, and are now 7.3% below their year-ago level.

Median prices remain up comfortably from a year ago. Nationally, the median sales price of an existing home was up 5.9% year-on-year, unchanged from the pace in January.

Rising prices reflect the continued tight supply conditions prevailing in the housing market. While the inventory of homes available for sale rose 4.6% in February, it is down 8.1% relative to a year ago.

Challenging affordability conditions amid rising prices and mortgage rates and low inventory can also be seen in a lower share of first time buyers in the markets. First time buyers accounted for 29% of sales in February, unchanged from last month and down from 32% a year ago.

Key Implications

The spring may have sprung in the U.S. housing market. January's gain ended two months of decline in home sales, suggests that an improvement is on the way. Rising inventory of houses for sale (at least on a monthly basis) is also an encouraging sign and should support moderate improvement in resale activity in the near months.

Broadly speaking, economic conditions are in place for continued improvement in demand for housing: a tight labor market, accelerating wage gains and tax cuts. However, low inventory and deteriorating affordability amid rising home prices and interest rates will weigh on activity, keeping gains modest.

Green shoots did not appear everywhere in February as gains were uneven across the country. The outsized decline in the Northeast is especially disappointing. Unseasonably cold weather and a slew of winter storms are likely to blame for the slowdown. However, changes to MID and SALT deductions as a result of the federal tax reform could have also tempered resale activity in expensive Northeast housing markets, which are expected to be negatively impacted by the changes. For full analysis of the regional impact, please see our latest report.

SNB: Real external value of Swiss franc still at a high level

SNB commented on exchange rate in its latest Quarterly Bulletin. Here are the quotes from section 5.4.

Swiss franc gains against US dollar

Since the monetary policy assessment in December 2017, the Swiss franc has gained in value against the US dollar by around 4% (cf. chart 5.4). This appreciation occurred against a backdrop of general US dollar weakness, which became more pronounced at the end of January following statements by the US Treasury Secretary about the advantages of a weak US dollar for the American economy. At times, the USD/CHF exchange rate declined to its lowest level since mid-2015.

Fluctuations in Swiss franc exchange rate to euro

Initially, the Swiss franc depreciated somewhat against the euro. At times in mid-January, the price of the euro was CHF 1.18, the highest value since the discontinuation of the minimum exchange rate. Thereafter, however, the Swiss franc strengthened again. This appreciation occurred against a backdrop of growing market uncertainty, which was also reflected in share price performance. In mid-March, one euro cost CHF 1.17, which was practically the same level as at the time of the monetary policy assessment in December.

Slight increase in Swiss franc's trade-weighted external value

On a nominal trade-weighted basis, the Swiss franc has increased by more than 1% since mid-December (cf. chart 5.5). This was mainly due to its marked appreciation against the US dollar.

Real external value of Swiss franc still at a high level

Real external value of Swiss franc still at a high level

Since autumn 2017, the real trade-weighted exchange rate index calculated by the SNB has been at roughly the same level as before the discontinuation of the minimum exchange rate. It thereby remains above its long-term average. The same is true for the indices calculated by the Bank for International Settlements (BIS) and the International Monetary Fund (IMF) (cf. chart 5.6).

Basically, there is no indication for a change of SNB's stance on exchange rate. Swiss Franc remains overvalued. And it will stand ready to intervenue if needed.

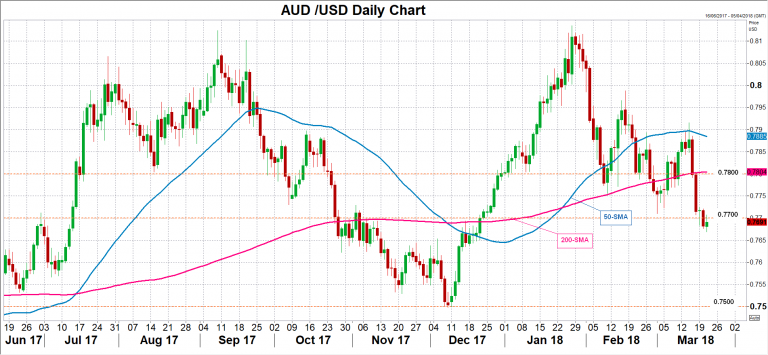

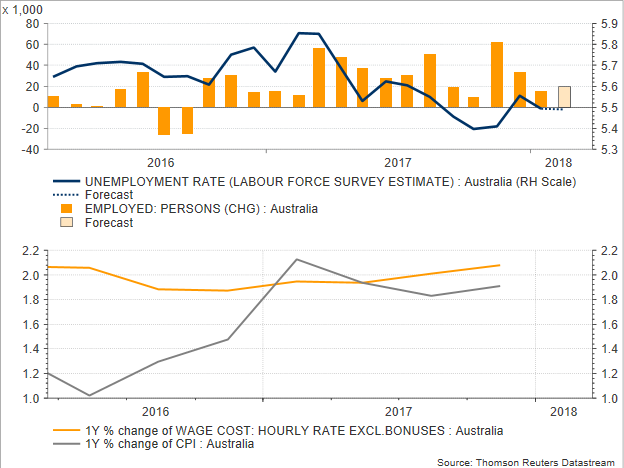

Australia Set to Post Another Record on Jobs Growth But RBA Could be Indifferent

Australia will see the release of employment data this week on Thursday at 0030 GMT, with the figures expected to show that the Australian labor market is in a good shape. Analysts believe that the number of jobs created continued to rise in February, posting the longest streak of employment gains since the Australian Bureau of Statistics began its monthly series in 1978. But once again, this is not what aussie traders want to hear most. The path of the unemployment rate and wage growth is what keeps policymakers cautious since both indicators have shown little progress to reach pre-crisis levels even if interest rates stand at record lows. This comes in contrast to the US example where the aforementioned gauges have already approached levels seen in 2009. Because of that, the RBA is in no rush to hike rates despite maintaining a positive note on Australia’s economic performance.

According to forecasts, the number of jobs added to the economy is expected to have increased by 20,000 in February, overcoming January’s rise of 16,000. If the data confirm expectations, the measure would experience nonstop growth for the 17th month. However, if the expansion appears to be led by rising part-time employment and falling full-time positions, as the previous job report indicated, the news would not be as encouraging to the RBA’s ears but rather another problem added to the list. Regarding the unemployment rate which has eased to 5.5% from 5.6% in the preceding month but overall looks to record a sideway trend (5.4%- 5.9%), forecasts are for the measure to remain steady. Yet this level is above the threshold of 5.0% needed to reach to trigger faster wage growth, hinting that the labor market has still some room for improvement. The participation rate or otherwise the proportion of adults in work or searching for work against the general population is also estimated to remain stable at 65.6%.

The Australian bond yields are currently losing their competitive edge on the back of the Fed’s stimulus reduction measures, with the 10-year Australian bond yields currently standing around 2.70% compared to the US equivalent of 2.85%. Unlike the RBA which drove interest rates to a record low of 1.50% over the past seven years without any hiking, the Fed has delivered five rate hikes since October 2015 and is widely anticipated to announce another one on Wednesday when the FOMC policy meeting concludes. Still, the RBA seems to be ignoring what the Fed is doing as Australia has one more problem to worry about and that is the household debt, with the Swiss-based central bank of central bankers, the Bank for International Settlements, warning that Australia is in a shortlist of countries (Canada, Hong Kong, and mainland China are the others on the list) that are threatened with a mortgage default crisis if their household debt proves unsustainable. The RBA’s meeting minutes published early today also highlighted the risks stemming from the housing sector, reporting that “household debt levels remained high, which contributed to the uncertainty surrounding the outlook for consumption growth”. Besides that, it admitted that despite the improvement in overall conditions and the support of the current accommodative monetary policy which pushed the unemployment rate lower and brought inflation closer to the RBA’s target range of 2-3.0% the progress of these measures is expected to be only gradual.

The Australian bond yields are currently losing their competitive edge on the back of the Fed’s stimulus reduction measures, with the 10-year Australian bond yields currently standing around 2.70% compared to the US equivalent of 2.85%. Unlike the RBA which drove interest rates to a record low of 1.50% over the past seven years without any hiking, the Fed has delivered five rate hikes since October 2015 and is widely anticipated to announce another one on Wednesday when the FOMC policy meeting concludes. Still, the RBA seems to be ignoring what the Fed is doing as Australia has one more problem to worry about and that is the household debt, with the Swiss-based central bank of central bankers, the Bank for International Settlements, warning that Australia is in a shortlist of countries (Canada, Hong Kong, and mainland China are the others on the list) that are threatened with a mortgage default crisis if their household debt proves unsustainable. The RBA’s meeting minutes published early today also highlighted the risks stemming from the housing sector, reporting that “household debt levels remained high, which contributed to the uncertainty surrounding the outlook for consumption growth”. Besides that, it admitted that despite the improvement in overall conditions and the support of the current accommodative monetary policy which pushed the unemployment rate lower and brought inflation closer to the RBA’s target range of 2-3.0% the progress of these measures is expected to be only gradual.

On the trade front, Australia seems to be optimistic that it will get an exemption from Trump’s punitive import tariffs on steel and aluminum after the US president admitted that the US had a trade surplus with its long-term partner. But even if the country does not win an exemption, as Canada and Mexico did – before the tariffs take effect on Friday- Australia is not a big exporter of steel and aluminum. In fact, Australia’s steel and aluminum exports to the US account only about 0.8% and 1.5% respectively of the US import basket. At this point, it is also worth mentioning that the processing of those metals requires Iron ore – mainly on steel production –, a mineral plentiful in Australia (iron ore accounts more than 20.0% of Australia’s exports). Therefore, if US protectionism weighs on iron ore’s demand, the country will definitely feel some economic pain. In addition, the risk could emerge indirectly under the scenario of a potential retaliation from other countries, including China, Australia’s biggest export partner. If a trade war between the US and China begins, harming China’s economic growth, Australia which is sensitive to Chinese economic conditions, could see its terms of trade deteriorating and its job growth narrowing.

Hence, even if Thursday’s jobs report surprises to the upside, the RBA will not change its monetary stance unless it sees job growth translating into faster wage growth which could subsequently help consumers to meet their debt obligations, spend more on goods and services, and therefore push inflation higher. In the forex markets, though, upbeat results could be good news for the aussie. In the wake of better-than-expected readings aussie/dollar could jump above three-month lows reached today, returning to the 0.77 key area. In the best scenario, the pair could crawl above the 200-day simple moving average which currently stands at 0.7800. On the flip side, if the report disappoints, aussie/dollar could extend its downleg towards the 0.7600 handle and even approach December’s low of 0.7500.