Sample Category Title

FOMC Review: Only Slightly Steeper Rate Path Due To Trumponomics

- The Fed maintained the three rate hikes signal for this year (close call between three and four) and revised the signal for next year up to three hikes, as expected.

- We still expect the Fed to hike twice more this year but risk is skewed towards a third. We expect three hikes next year. While market pricing for this year seems fair, markets are still pricing the Fed too softly next year, in our view.

- The Fed hike is not set to trigger a new course for the dollar, and we still see EUR/USD in the 1.21-1.26 range near term.

Fed maintains three hikes signal for 2018

As expected by everyone, the Fed raised the target range by 25bp to 1.50-1.75%. More interestingly, the Fed maintained the three rate hikes signal for this year, in line with our expectation laid out in our preview, although it was close between three and four hikes (see chart to the bottom-right). This is important given that some of the most outspoken doves like Bullard, Evans and Kashkari are not voting this year. This supports the view that risk is probably skewed towards a total of four hikes this year. Still this was interpreted dovishly with EUR/USD moving higher and US yields lower. Also in line with our expectation, the 2019 dot was raised from slightly more than two hikes to three hikes, taking the Fed funds target range to 2.75%-3.00% by year-end 2019. The Fed now expects the target range to rise 50bp above the natural rate of interest (the rate where monetary policy neither expansionary nor contractionary) by year-end 2020. The reason for the move up in dots is mainly the more expansionary fiscal policy under Trump. We still believe the overall policy mix is going to be more expansionary, as the Fed seems reluctant to offset more expansionary fiscal policy 1:1.

We still expect the Fed to hike twice more this year (June and December) and three times next year (March, June, September). However, the timing of the rate hikes may also depend on whether Powell decides to make every meeting live by having a press conference at every meeting instead of every other. Indeed, it would make it easier for the Fed to spread out the rate hikes (if the number of hikes is uneven).

As expected, there were no major changes to the statement. The Fed repeated risks are “roughly balanced”, it still monitors inflation “closely” and that it expects “further gradual increases” in the target range. The most important change was that it now says that “the economic outlook has strengthened in recent months”.

Powell said very explicitly the Fed is not about to alter its plan to shrink the balance sheet (unless the outlook deteriorates) and it still has not decided what the appropriate target is. Ultimately, it depends on the demand for the Fed’s liabilities (public demand for currencies and banks’ demand for high quality liquid assets due to regulation).

The Fed discussed trade policy but FOMC members have not changed their economic outlook on back of this. We would likely need to see an escalation of the trade war before that is going to happen. There was no question on the higher LIBOR/OIS spread, so we do not know what the Fed might think about the large increases.

FX: dovish Fed hike does not steer new course for EUR/USD

EUR/USD back above 1.23 as Fed delivered a ‘dovish hike’, largely in the way we had expected. While the risk of a fourth hike remains and the somewhat steeper rate path hinted at by the dots suggests potential for USD support from higher US rates further out, the market is not ready for pricing this just yet. Also, we continue to stress that short-term rates are not a key driver of EUR/USD at present. As we wrote in FX Strategy - EUR/USD risks more two-sided over shorter horizons, EUR/USD has been largely unmoved by notably the recent uptick in Libor rates as the short-rate spread fails to set a course for the pair. This hints that the Fed needs to change its course on policy more dramatically for it to impact USD crosses. Rather, we stress that the risk of USD support over shorter horizons from an uptick in US real yields as the issuance of US Treasuries gains traction is a crucial one to watch going forward. In sum, we expect the March hike will not trigger a new course for the dollar, and we still see EUR/USD in the 1.21-1.26 range near term with focus again set to shift to the Trump administration’s next step on protectionist measures

Open Season On The USD ?

Open season on the USD?

On or below the surface, the FOMC statement would suggest its open season on the dollar and greenlights sellers to re-engage as the Fed failed to confirm any of the markets hawkish suspicions. At the end of the day, while the 25 basis point was all but expected, the FOMC is forging a cautious path for the remainder of 2018. Not to mention the board painted a very circumspect path for 2019-2020 dot projections, suggesting this sitting Fed board is going to be no less data dependent than yesteryear which has policy gradualism painted all over it.

Given this more dovish scenario, Dollar bears have the green light after the FOMC failed to embrace a more hawkish tack which should ultimately cap support for USD from policy divergence perspective. Leaving the dollar extremely vulnerable amid ECB or BoJ policy normalisation rhetorics or more profound US political wobbles, particularly around the shifting US trade policies.

Currency Markets

The Dovish Fed outcome should be a green light to sell USD despite the potential for a steeper interest rate path in 2019-20. At this stage, that’s mear conjecture in the face of possible dollar negatives such as trade war escalation, burgeoning US budget deficit, and the political storm clouds that continues to engulf the Trump administration. Markets should view this outcome as a solid signal to re-engage USD short vs EUR and JPY.

The Japanese Yen

Whichever spin you want to put on the FOMC statement, the dovishness is all about not wanting to rock the global equity market boat given the massive geopolitical tail risk facing markets. Also, the market continues to underprice the prospects of the BoJ draining the punch bowl which suggest the downside skews remain intact

The Euro

Speaking of underpricing policy. As the Fed policy matures, the ECB is only entering the early stages of policy debate. With the USD support capped from policy divergence perspective, the opportunity to ride the shifting ECB policy wave should come back in vogue.

The Australian Dollar

The Australian dollar, after trading at bearish extremes, is getting a respite from the overwhelming wave of USD negativity permeating through G-10 markets. But going forward I expect the currency to trade like a canary in the iron ore mine while the shifting narrative on the US-China trade war escalation provides the broader backdrop

The Malaysian Ringgit

Despite yesterday tepid national CPI print lessening the chances for a 2018 BNM followup rate hike, the dulcet FOMC overtones should provide a boost to Ringgit sentiment, even more so more so with Brent Crude tracking towards $70 per barrel. The MYR should be back in the game after a fortnight off the grid.

Equity markets

Equity investors are very restrained suggesting they view the statement as balanced but continue to express concerns about President Trumps protectionist trade policies, particularly towards China While there been some easing in the NAFTA rhetoric; the equity markets remain in limbo as the Whitehouse is expected to announce new trade sanctions directed at China.

Oil Markets

The Energy Information Administration reported a drop in inventories of 2.6 million barrels for the week to March 16 confirm the estimated stockpiles decline from the API earlier in the week. But when factoring in possible supply disruptions from rising middle east tension and concerns about Venesualan supplies, Oil prices are trading firm. The Oil Bulls are revelling this morning with both the fundamental narrative and geopolitical landscapes supporting prices in tandem. Good day to own a piece of the oil patch.

Gold Markets

Gold prices rocketed through the critical $1330 resistance level as the dollar bears are expected to relish this opportunity to re-engage USD short positions.And if you factor in the significant near-term geopolitical concerns and the uncertain equity market fall out from an escalation of a trade war with China, Gold has to be a mainstay component in any investment portfolio which should provide a positive tone for the Gold markets today.

With US interest rates looking lower for longer we could see a pick up in physical demand as many investors were holding off buying for fear of a quicker pace of rising US interest rate

Eco Data 3/22/18

[php_everywhere instance="1"]

The Fed Remains Resolute, Even in the Face of Softer Data

As expected, the Fed hiked the federal funds rate by a quarter percentage point. The FOMC slightly boosted the target range for the funds rate in spite of slightly downgrading its view of recent economic conditions.

The Fed Feels They Finally Have the Wind at Their Back

The Fed's resolve to normalize interest rates clearly trumped any concerns about disappointing first quarter economic data. The opening paragraph of the FOMC policy statement readily acknowledges economic activity has been rising at a moderate rate (as opposed to solid) and "household spending and business fixed investment had moderated from their strong fourth quarter readings." The slight downgrade to recent economic conditions was offset by an upgrade to its assessment of the labor market, where "job gains have been strong" and the "unemployment rate has remained low."

The significance of the Fed's move in the face of this softer data is that the Fed has more confidence in the economy's underlying momentum and appears to be more determined to normalize interest rates. Indeed, the FOMC's median expectations for GDP growth for 2018 and 2019 were increased from 2.5 percent and 2.1 percent to 2.7 percent and 2.4 percent, respectively. Moreover, the median expectations for the unemployment rate were lowered by 0.1 percentage point in 2018, 0.3 percentage points in 2019 and 0.4 percentage points in 2020 to 3.8 percent, 3.6 percent and 3.6 percent, respectively.

Trust the Dots

Jay Powell's first FOMC meeting appears to have a short and concise message for the financial markets: trust the dots. The stronger jobs data and stronger survey data (such as the ISM, regional Fed surveys and consumer confidence surveys) all suggest the economy is growing much more broadly and is more resilient. Moreover, with fiscal policy turning more stimulative, the Fed feels it finally has the wind at its back and appears to be determined to use this opportunity to bring short-term interest rates closer to their new normal. This means it is more likely to follow through with planned rate increases even if the economic data stumble a bit or face some sort of exogenous shock. The gap between the market's expectations for the federal funds rate and the dots laid out in the summary of economic projections should narrow further. One closely watched aspect of the March FOMC meeting was whether a majority of FOMC participants would opt for four rate hikes in 2018 as opposed to the three outlined at the December meeting. Seven of the fifteen dots now have the Fed raising interest rates four or more times this year, which is one more than in December. Eight participants are looking for three or fewer hikes (one of which has already occurred). A majority now sees three hikes in 2019, up from two in December and two participants now see the longer run federal funds rate above 3.0 percent, which had been the upper end of expectations at prior meetings. If economic growth is as strong as the FOMC's current expectations, we would expect the Fed to raise interest rates more than it has currently outlined. We have four rate hikes in our 2018 forecast and expect another dot or two to join us in coming months.

RBNZ kept OCR unchanged at 1.75%, maintains dovish bias

RBNZ kept OCR unchanged at 1.75% as widely expected. It also maintined dovish bias by noting "monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain and policy may need to adjust accordingly."

Here is the full statement:

The Reserve Bank today left the Official Cash Rate (OCR) unchanged at 1.75 percent.

The outlook for global growth continues to gradually improve. While global inflation remains subdued, there are some signs of emerging pressures. Commodity prices have continued to increase and agricultural prices are picking up. Equity markets have been strong, although volatility has increased. Monetary policy remains easy in the advanced economies but is gradually becoming less stimulatory.

GDP was weaker than expected in the fourth quarter, mainly due to weather effects on agricultural production. Growth is expected to strengthen, supported by accommodative monetary policy, a high terms of trade, government spending and population growth. Labour market conditions are projected to tighten further.

Residential construction continues to be hindered by capacity constraints. The Kiwibuild programme is expected to contribute to residential investment growth from 2019. House price inflation remains moderate with restrained credit growth and weak house sales.

CPI inflation is expected to weaken further in the near term due to softness in food and energy prices and adjustments to government charges. Tradables inflation is projected to remain subdued through the forecast period. Non-tradables inflation is moderate but is expected to increase in line with a rise in capacity pressure. Over the medium term, CPI inflation is forecast to trend upwards towards the midpoint of the target range. Longer-term inflation expectations are well anchored at 2 percent.

Monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain and policy may need to adjust accordingly.

(RBNZ) Statement by Reserve Bank Governor Grant Spencer

The Reserve Bank today left the Official Cash Rate (OCR) unchanged at 1.75 percent.

The outlook for global growth continues to gradually improve. While global inflation remains subdued, there are some signs of emerging pressures. Commodity prices have continued to increase and agricultural prices are picking up. Equity markets have been strong, although volatility has increased. Monetary policy remains easy in the advanced economies but is gradually becoming less stimulatory.

GDP was weaker than expected in the fourth quarter, mainly due to weather effects on agricultural production. Growth is expected to strengthen, supported by accommodative monetary policy, a high terms of trade, government spending and population growth. Labour market conditions are projected to tighten further.

Residential construction continues to be hindered by capacity constraints. The Kiwibuild programme is expected to contribute to residential investment growth from 2019. House price inflation remains moderate with restrained credit growth and weak house sales.

CPI inflation is expected to weaken further in the near term due to softness in food and energy prices and adjustments to government charges. Tradables inflation is projected to remain subdued through the forecast period. Non-tradables inflation is moderate but is expected to increase in line with a rise in capacity pressure. Over the medium term, CPI inflation is forecast to trend upwards towards the midpoint of the target range. Longer-term inflation expectations are well anchored at 2 percent.

Monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain and policy may need to adjust accordingly.

FOMC Raises the Fed Funds Rate to 1-1/2 to 1-3/4

As widely expected, the Federal Open Market Committee (FOMC) raised its federal funds target rate range by 25 basis points to 1-1/2 to 1-3/4 percent.

Most notably, the statement noted that "the economic outlook has strengthened in recent months." This was also reflected in upgraded forecasts for real GDP growth in the Survey of Economic Projections (SEP). The median projection for 2018 rose to 2.7% (from 2.5%) and increased to 2.4% (from 2.1%) for 2019.

Alongside faster economic growth, members lowered their expectation for the unemployment rate and nudged up their projections for inflation. The unemployment rate is now expected to trough at just 3.6% in 2019 (from 3.9% previously), where it is expected to stay through 2020 (down from 4.0% previously). The median expected rate over the longer-term edged down to 4.5% (from 4.6%). The median estimate for core PCE inflation rose to 2.1% for 2019 and 2020 (both up from 2.0% previously).

The median expectation for the federal funds rate was unchanged in 2018 at 2.1% (even as the mean moved up 13 basis points), but rose to 2.9% (from 2.7%) in 2019 and to 3.4% (from 3.1%) in 2020. The longer run projection edged up to 2.9% (from 2.8%).

Key Implications

The interest rate increase was the least interesting part of the package delivered today. Given the double-dose of fiscal stimulus delivered by Congress since December, FOMC members had little choice but to raise their expectations for economic growth and the number of rate hikes. Previously, only some included the fiscal stimulus in their projections.

On balance, the unchanged median projection for 2018 suggests a somewhat a dovish lean. The Fed doesn't look to be keen to get too far in front of the expected pickup in economic growth, but is happy to make sure its outlook is realized before draining the punchbowl.

This is also evident in the SEP's median projection for core inflation, which moved above the 2.0% mark in 2019 and 2020. A modest overshoot of inflation following nearly a decade in which it has run under its target should not come as a terrible surprise. But, it speaks volumes to the bias of the current much-changed FOMC not to push too hard or too soon against the rising fiscal tide.

USD Suffers Selloff after FOMC and Powell, Worst against GBP and CAD

Dollar tumbles broadly as bulls are clearly unhappy with what Fed delivered. There are some key take aways from the announce and Jerome Powell's press conference as Fed chair.

Firstly, while Fed raised GDP growth forecasts of 2018 and 2019, it kept 2020 forecast unchanged. Fed is clearly not expectation Trump's tax cut and fiscal policies to have a long lasting effect to the economy. And even at the peak of their impact, Fed only projects 2.7% growth in real GDP in 2018. Powell also said in the press conference that on one on the committee believes that growth will get to 3% and stay there. That's a clear vote of no confidence on what Trump claimed.

Secondly, Powell also said that "the relationship between slack and inflation is not so tight". This echoes the new projections. Unemployment rate forecast is revised sharply lower to 3.6% in 2019 and stay there in 2020. But there is realistically not much impact on inflation. Fed only raised 2019 core PCE forecast by 0.1% to 2.1%, same for 2020. Powell also went further and said that "there is no sense in the data that we are on the cusp of an acceleration of inflation."

Thirdly, this is possibly what disappointed dollar bulls most. Fed will stick with the course of only three rate hike this year. There might be one more hike in 2019 to three in total, thanks to the GDP growth in both 2018 and 2019, as well as the steep improvement in labour market. And, Fed is more confident that there will be another two rate hikes in 2020.

More on the projections here, and the full statement here.

Looking at the 4H heatmap, USD is clearly suffering after the FOMC release.

From volatility chart, it's also rather clear that USD suffers most against CAD and GBP.

From volatility chart, it's also rather clear that USD suffers most against CAD and GBP.

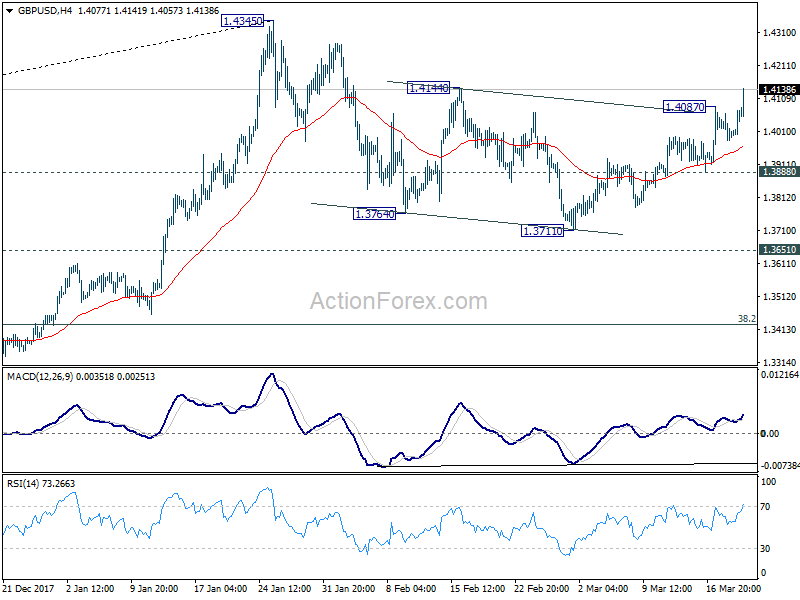

GBP/USD is now on track to take out 1.4144 resistance. 1.4345 will be the next stop, depending on the outcome of tomorrow's BoE rate decision. BoE will stand pat for sure, but voting and the statement might give GBP another boost.

GBP/USD is now on track to take out 1.4144 resistance. 1.4345 will be the next stop, depending on the outcome of tomorrow's BoE rate decision. BoE will stand pat for sure, but voting and the statement might give GBP another boost.

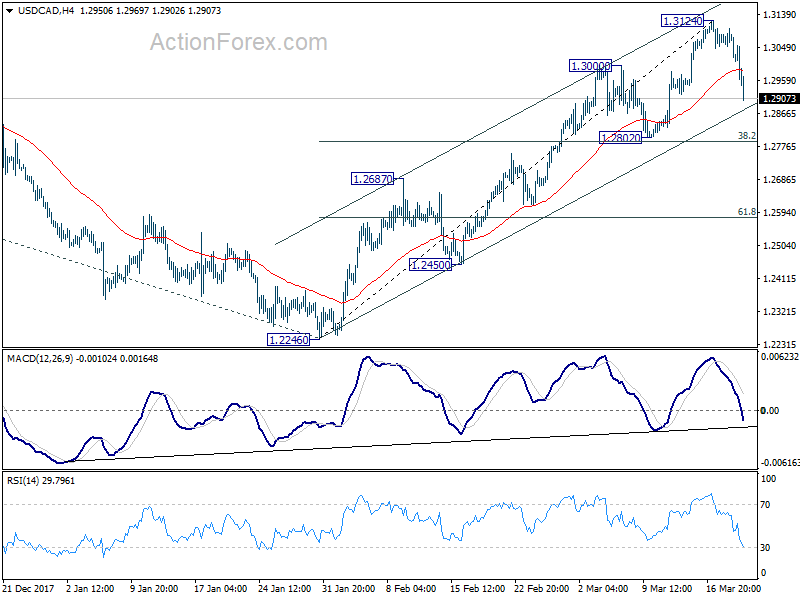

USD/CAD continues to be weighed down by positive NAFTA negotiation development. At this point, we'd still expect strong support from 1.2802 cluster (38.2% retracement of 1.2246 to 1.3124 at 1.2789) to contain downside. But let's see.

USD/CAD continues to be weighed down by positive NAFTA negotiation development. At this point, we'd still expect strong support from 1.2802 cluster (38.2% retracement of 1.2246 to 1.3124 at 1.2789) to contain downside. But let's see.

Fed maintains forecast of three hikes in 2018, expects one extra in 2019

Fed delivered the 25bps rate hike and lifted the federal funds rate to 1.50-1.75% as widely expected. But Dollar bulls are clearly dissatisfied with the updated economic projections. The accompanying statement is nearly a carbon copy of the prior one with balanced changes. It added that "recent data suggest that growth rates of household spending and business fixed investment have moderated from their strong fourth-quarter readings." But at the same time, "economic outlook has strengthened in recent months." The interest rate decision was made with unanimous 8-0 vote.

Going into the projections:

Real GDP forecast for 2018 is raised to 2.7% (up from 2.5%), for 2019 raised to 2.4% (up from 2.1%), for 2020 unchanged at 2.0%.

- Implication is that Fed is expecting slight boost from tax cuts in 2018 and 2019. But the impact won't be long lasting and would fade into 2020.

Unemployment rate forecast for 2018 is lowered to 3.8% (down from 3.9%), for 2019 lowered to 3.6% (down from 3.9%), for 2020 lowered to 3.6% (down from 4.0%).

- The employment market is expected to improve further, with the help of tax cuts and expansive fiscal policy. And the impact would sustain.

PCE inflation forecast for 2018 unchanged at 1.9%, for 2019 unchanged at 2.0%, for 2020 raised to 2.1% (up from 2.0%)

Core PCE inflation forecast for 2018 unchanged at 1.9%, for 2019 raised to 2.1% (up fro 2.0%), for 2020 raised to 2.1% (up from 2.0%).

- While unemployment rate would continue to drop, GDP growth to stay solid, inflation will pressure will remain contained. Fed is seeing the current pattern to continue.

Federal funds rate projection for 2018 unchanged at 2.1%, 2019 raised to 2.9% (up from 2.7%), 2020 raised to 3.4% (up from 3.1%).

- This is possibly what disappointed dollar bulls most. It implies Fed will stick with the course of only three rate hike this year. There might be one more hike in 2019 to three in total, thanks to the GDP growth in both 2018 and 2019, as well as the steep improvement in labour market. And, Fed is more confident that there will be another two rate hikes in 2020.

Fed raised federal fund rates by 25bps to 1.5-1.75%

Fed raised federal fund rates by 25bps to 1.5-1.75%. Statement below.

New economic projections here.

FOMC Statement Mar 21, 2017

Information received since the Federal Open Market Committee met in January indicates that the labor market has continued to strengthen and that economic activity has been rising at a moderate rate. Job gains have been strong in recent months, and the unemployment rate has stayed low. Recent data suggest that growth rates of household spending and business fixed investment have moderated from their strong fourth-quarter readings. On a 12-month basis, both overall inflation and inflation for items other than food and energy have continued to run below 2 percent. Market-based measures of inflation compensation have increased in recent months but remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The economic outlook has strengthened in recent months. The Committee expects that, with further gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace in the medium term and labor market conditions will remain strong. Inflation on a 12-month basis is expected to move up in coming months and to stabilize around the Committee's 2 percent objective over the medium term. Near-term risks to the economic outlook appear roughly balanced, but the Committee is monitoring inflation developments closely.

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 1-1/2 to 1-3/4 percent. The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant further gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

Voting for the FOMC monetary policy action were Jerome H. Powell, Chairman; William C. Dudley, Vice Chairman; Thomas I. Barkin; Raphael W. Bostic; Lael Brainard; Loretta J. Mester; Randal K. Quarles; and John C. Williams.