Sample Category Title

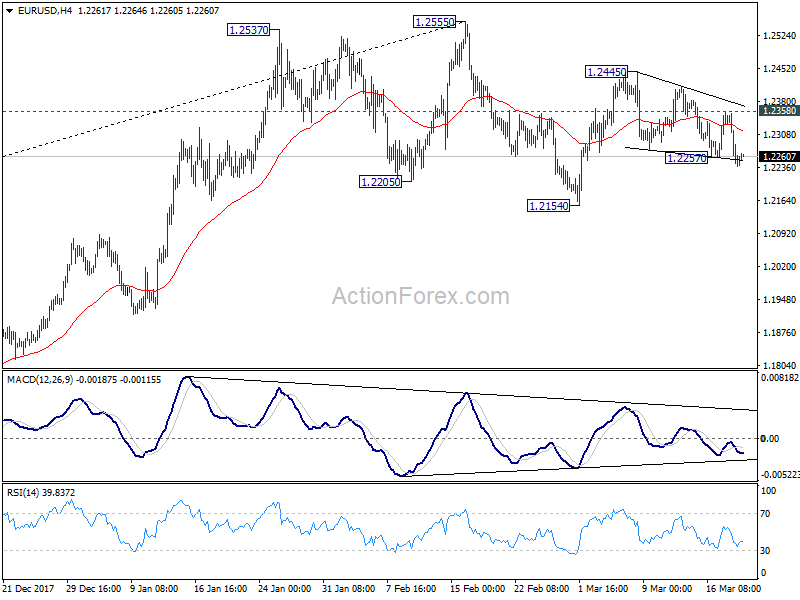

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2202; (P) 1.2278 (R1) 1.2317; More....

Despite breaching 1.2257, EUR/USD recovered without sustaining below. Intraday bias remains neutral first. On the upside, break of 1.2358 resistance will revive the bullish case. That is, pull back from 1.2445 has completed. Intraday bias will be turned back to the upside for 1.2445 and then 1.2555 key resistance. However, sustained break of 1.2257 turned back to the downside, to resume the fall from 1.2555 through 1.2154.

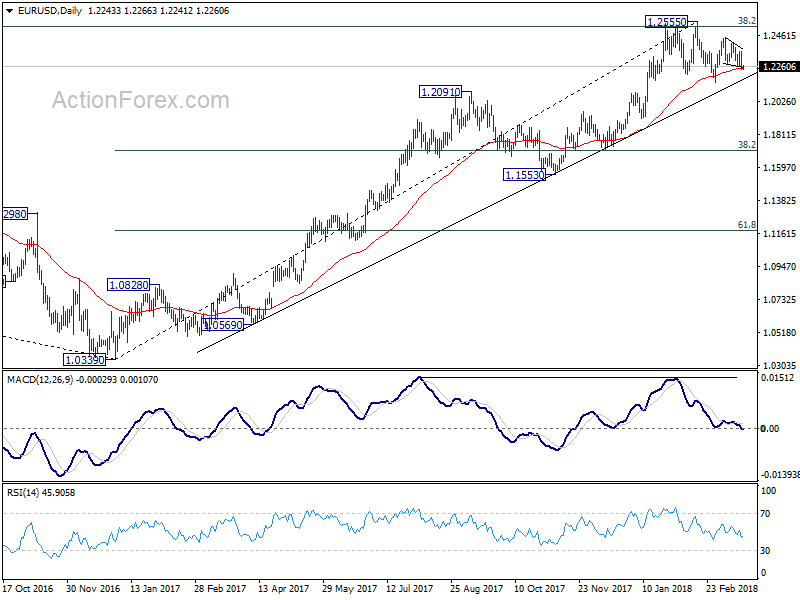

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

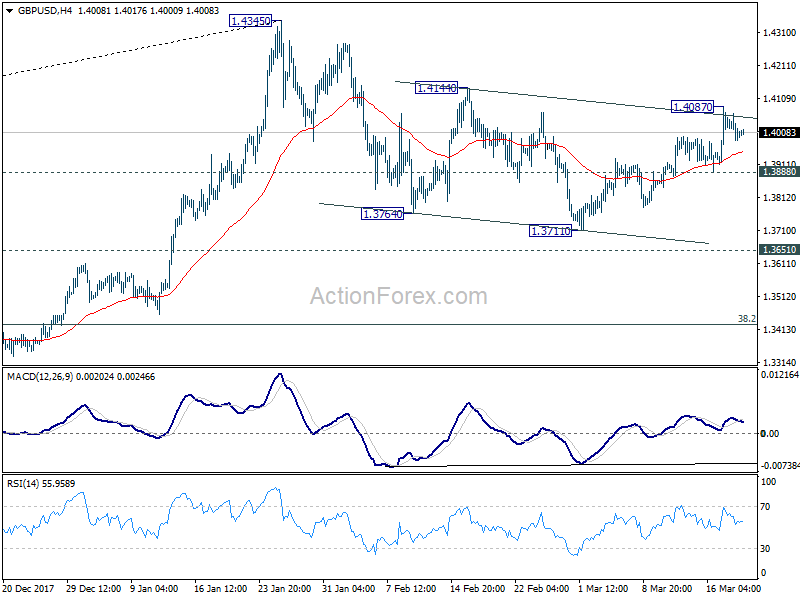

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3964; (P) 1.4015; (R1) 1.4048; More....

Intraday bias in GBP/USD stays neutral for consolidation below 1.4087 temporary top. With 1.3888 minor support intact, further rise is expected in the pair. As noted before, correction from 1.4345 could have completed at 1.3711 already. Above 1.4087 will target 1.4144 resistance first. Firm break there should confirm this bullish view and target 1.4345 and above. On the downside, however, break of 1.3888 minor support will dampen this bullish view. Intraday bias would be turned back to the downside to extend the decline from 1.4345 through 1.3711 instead.

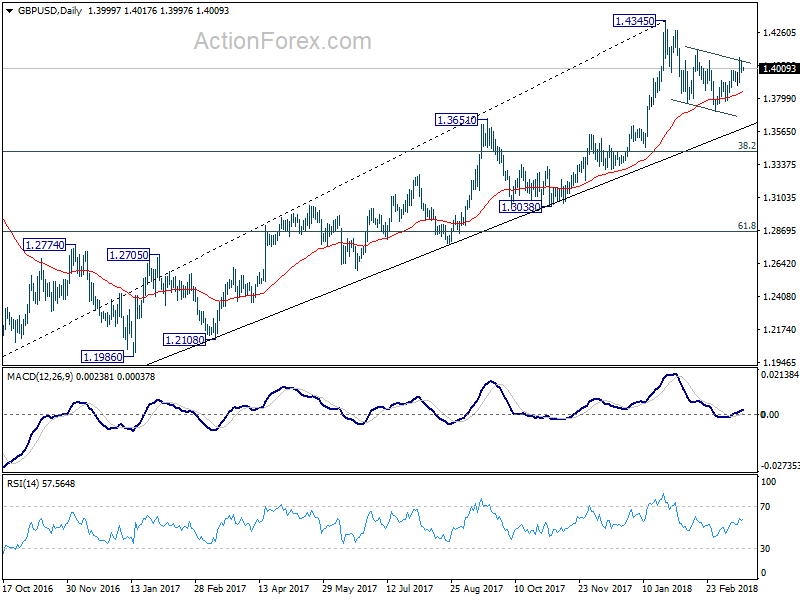

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

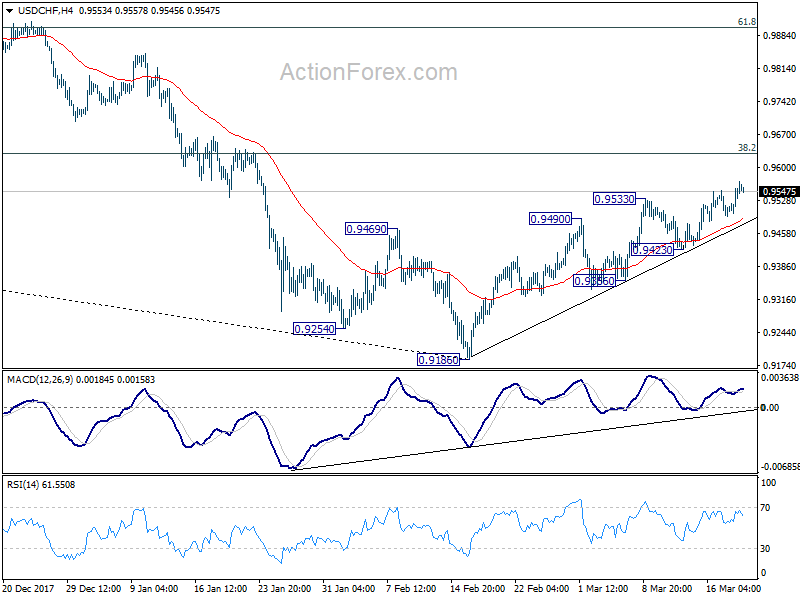

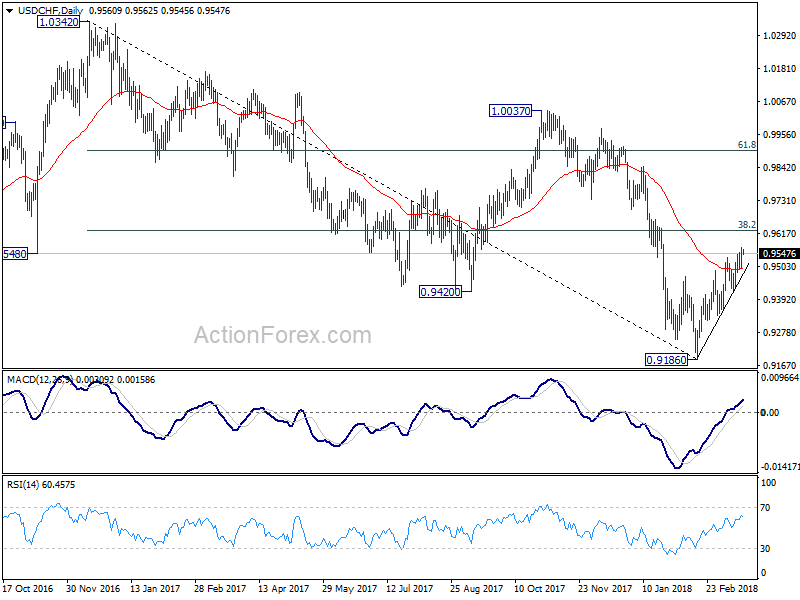

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9520; (P) 0.9544; (R1) 0.9588; More...

Intraday bias in USD/CHF remain son the upside as rebound from 0.9186 is in progress. Further rise should be see to 0.9626 fibonacci level. We'd be cautious on strong resistance from 0.9626 to limit upside. Nonetheless, sustained break of 0.9626 will carry larger bullish implications. On the downside, break of 0.9423 will indicate completion of the rebound from 0.9186. And intraday bias would then be turned back to the downside for 0.9356 support and below.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Current development is raising the chance that it is completed. But there is no confirmation yet. Focus will now be back on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add much credence to the case of trend reversal and target 61.8% retracement at 0.9900 and above. However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

USD/JPY Daily Outlook

Daily Pivots: (S1) 106.10; (P) 106.35; (R1) 106.78; More...

Intraday bias in USD/JPY remains neutral as consolidation from 105.24 is still in progress. With 107.67 resistance intact, near term outlook remains bearish and further decline is expected. On the downside, break of 105.24 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. On the upside, firm break of 107.67 resistance will indicate near term reversal, on bullish convergence condition in 4 hour MACD. In such case, outlook will be turned bullish for 110.47 resistance next.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

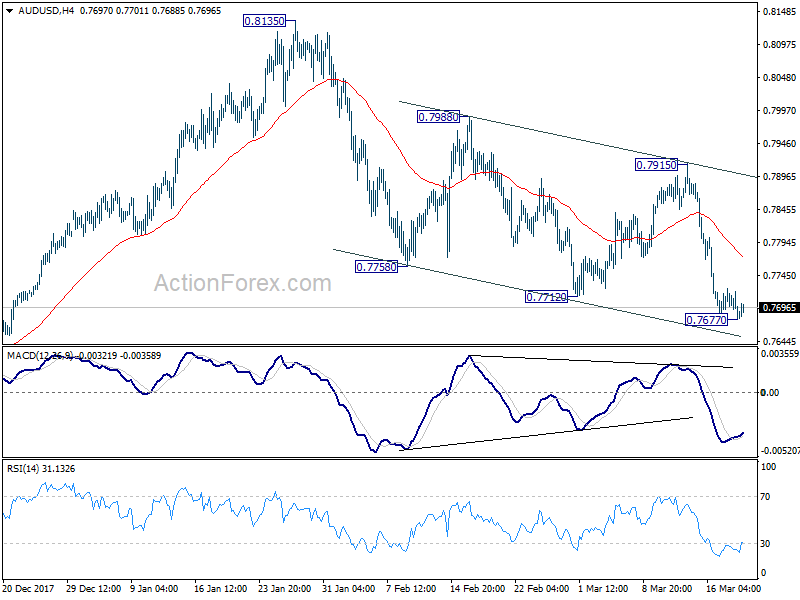

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7667; (P) 0.7693; (R1) 0.7709; More...

Loss of downside momentum as seen in 4 hour MACD suggests temporary bottoming at 0.7677. Intraday bias is turned neutral for consolidation. Stronger recovery could be seen. But upside should be limited well below 0.7915 resistance to bring fall resumption. Below 0.7677 will turn bias back to the downside to extend the decline from 0.8135 to 0.7500 key support.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.

Elliott Wave Analysis: Oil Rallying In Wave 3

Oil (CL_F) Short Term Elliott Wave view suggests that the decline to 59.95 on 3/9 ended Minor wave 2. Minor wave 3 is unfolding as a 5 waves impulse Elliott Wave Structure where Minute wave ((i)) of 3 is currently in progress as a leading diagonal. Up from 59.96, Minutte wave (i) ended at 62.33, Minutte wave (ii) ended at 60.11, and Minutte wave (iii) should end soon. Expect a pullback in Minutte wave (iv) to be followed by another leg higher in Minutte wave (v) before Oil completes Minutte wave (v) and ends cycle from 3/9 low (59.96). The five waves higher from 59.96 should form Minute wave ((i)) of a larger degree as a diagonal. Afterwards, Oil should pullback in Minute wave ((ii)) to correct cycle from 3/9 low in 3, 7, or 11 swing before the rally resumes. As far as pivot at 3/9 low (59.96) stays intact during the pullback, expect Oil to extend higher.

Oil (CL_F) 1 Hour Elliott Wave Chart

UK And EU Reached Transition Deal, Erasing Key Uncertainty Of BOE’s Rate Hike Path

Despite initial rally following the announcement of a Brexit transition deal, British pound has retraced much of its gains. Both UK and EU officials have hailed the agreement. While UK's Brexit negotiator Davis David noted that the deal contains 'a large part of what will make up an international agreement for the ordered withdrawal of the UK', EU's representative Michel Barnier indicated that it marks "decisive step" towards to eventual agreement of the UK-EU relations after Brexit. Yet, the terms of transition agreement reveal that the UK has backed down on various fronts. Over the past meetings, the BOE has suggested that the rate hike pace should be faster than what has been priced in by the market. It also added Brexit uncertainty is a key concern for its monetary policy decision. The transition deal signals soft Brexit is now more likely. We expect the BOE to signal at the meeting later this week that it might increase the Bank rate in May, following a hike in November last year. The disappointing February inflation report (headline CPI eased to +2.7% y/y while core CPI slowed to +2.4% y/y, both missed expectations) should not affect monetary decision making.

As suggested in the UK-EU joint statement, the transition period will last from Brexit day on March 29, 2019 to December 31, 2020. The key terms in the agreement include the followings: EU citizens arriving in the UK between these two dates will enjoy the same rights and guarantees as those who arrive before Brexit. The same will apply to UK expats on the continent; The UK will be able to negotiate, sign and ratify its own trade deals during the transition period; The UK will still be party to existing EU trade deals with other countries The UK's share of fishing catch will be guaranteed during transition but UK will effectively remain part of the Common Fisheries Policy, yet without a direct say in its rules, until the end of 2020; Northern Ireland will effectively stay in parts of the single market and the customs union in the absence of other solutions to avoid a hard border with the Republic of Ireland. Indeed, PM Theresa May has described the arrangement for Northern Ireland as 'unacceptable' as it would effectively shift the existing land border to the Irish Sea and compromise UK sovereignty. Yet, the EU suggested this 'backstop option" was a key part of December's phase one agreement with the UK and this would remain effective "unless and until another solution is found".

Comments from anti-Brexit Labour MP Chuka Umunna – 'In the end the Brexiters have been prepared to compromise and surrender on almost every single point. On the divorce bill, on the primacy of European law, on freedom of movement, on fisheries, the Government has yet again capitulated. We should be in no doubt that this will be the shape of things to come in the negotiations over the future relationship' – are fair enough. The UK has obviously backed down on issues regarding sovereignty and border control. Yet, this does not seem to be a big concern for global investors who focus more on the future trade relations between UK and EU. An increasing likelihood for soft Brexit has diminished uncertainty and should bode well for UK's economic growth outlook. This should facilitate the BOE to proceed with more rate hikes this year.

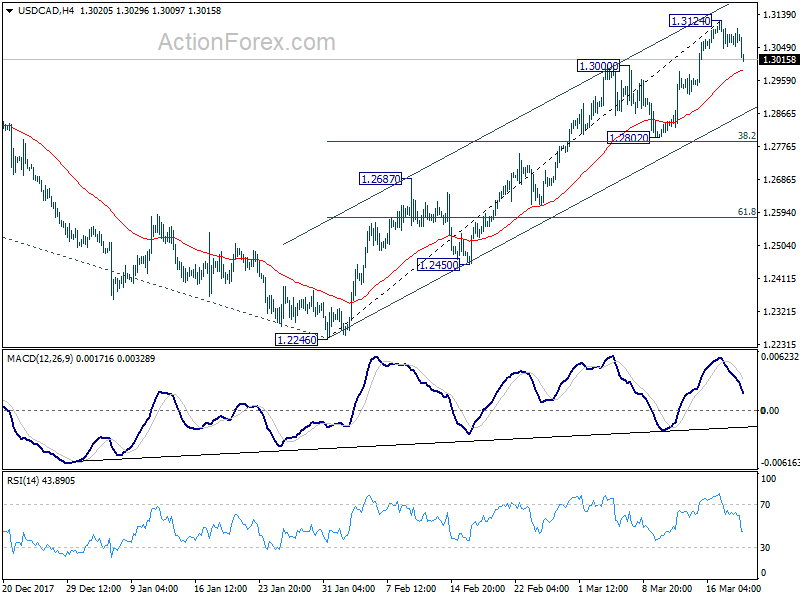

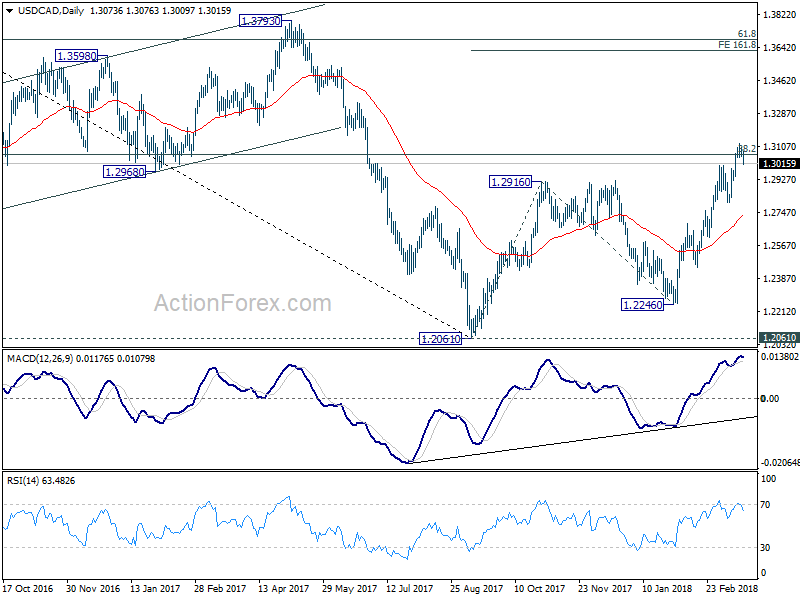

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3047; (P) 1.3075; (R1) 1.3098; More....

USD/CAD's retreat from 1.31214 extends lower today and reaches 1.3009 so far. Deeper fall could be seen to 4 hour 55 EMA (now at 1.2986). But strong support should be seen above 1.2802 cluster (38.2% retracement of 1.2246 to 1.3124 at 1.2789) to contain downside and bring rally resumption. On the upside, break of 1.3124 will extend recent rally to 161.8% projection of 1.2061 to 1.2916 from 1.2246 at 1.3629 next.

In the bigger picture, we're favoring the medium term bullish case. That is larger down trend from 1.4689 has completed at 1.2061 as a correction, drawing support from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Sustained break of 38.2% retracement of 1.4689 to 1.2061 at 1.3065 will pave the way to 61.8% retracement at 1.3685. This will be the preferred case now as long as 1.2802 support holds.

Dollar Turns Soft as Markets Await FOMC Hike, Sterling Looks into Job Data

Dollar trades broadly softer in Asian session today as yesterday's rebound attempt lost steam. Traders are also turning more cautious ahead of FOMC rate decision. While Fed is widely expected to hike, the main question remains on whether there will be three or four hikes this year. Also, Jerome Powell will also make his debut and hold the first post meeting press conference as Fed chair. Elsewhere in the forex markets, while Sterling dipped yesterday following lower than expected CPI, lost was limited. The Pound will look into today's employment data, and then tomorrow's BoE rate decision. Canadian Dollar is notable higher as lifted by news on positive development in NAFTA talks.

In other markets, DOW closed higher by 0.47% overnight while S&P 500 gained 0.15%. NASDAQ also gained 0.27% but stayed below Monday's gap. 10 year yield closed up 0.034 at 2.879 as recent range trading continued between 2.8 and 2.95. Nikkei is trading down -0.47% at the time of writing while HK HSI is up 1.2%.

Fed to hike in Powell's debut

Fed is widely expected to raise federal funds rate by 25bps to 1.50-1.75% today. Fed fund futures are pricing in near 95% chance of that. There is no reason for Fed to give market a surprise. The main question in everybody's mind is whether Fed will hike a total of three times this year, or four. Fed fund futures are pricing more than 80% chance of another hike in June already, and close to 60% chance of another in September. But for now, it's only pricing less than 40% chance of the fourth in December.

As usual with a March FOMC meeting, new economic projections will be released. Given that the Republican's tax cuts were done, there could be upward revisions in growth. Unemployment rate forecast might be left unchanged. PCE core at 1.5% in January, is still way off Fed's median projection of 1.9% in 2018. There is little chance of a change in that figure. Meanwhile, any slight change in the federal funds rate projection would be market moving.

Fed's December projections:

The event also bears additional significance as it's Powell's first press conference as Fed chair. His Congressional testimony was seen by some as more hawkish and upbeat than expected. Recapping that he said "my personal outlook for the economy has strengthened since December." And, "we've seen some data that will in my case add some confidence to my view that inflation is moving up to target." Powell might maintain the tone today and indicate his confidence in continuing the tightening cycle.

The event also bears additional significance as it's Powell's first press conference as Fed chair. His Congressional testimony was seen by some as more hawkish and upbeat than expected. Recapping that he said "my personal outlook for the economy has strengthened since December." And, "we've seen some data that will in my case add some confidence to my view that inflation is moving up to target." Powell might maintain the tone today and indicate his confidence in continuing the tightening cycle.

G20 stressed importance of trade, urged further dialogue, nothing more

G20 finance ministers and central bank governors ended the summit in Buenos Aires with a joint communique that emphasized the importance of international trade. And they urged for the need for "further dialogue and actions". But the communique fell short of anything else to push back protectionism.

The communique noted "International trade and investment are important engines of growth, productivity, innovation, job creation and development." And, "we reaffirm the conclusions of our Leaders on trade at the Hamburg Summit and recognise the need for further dialogue and actions." They pledged to work to "strengthen the contribution of trade to our economies."

Below is the full communique covering areas like technology, infrastructure, global financial system, cross-border capital flow, debts, international tax system and even Cryto-assets. But trade wasn't mentioned beyond the first paragraph.

Trump to announce tariffs on Chinese goods on Thursday, but will seek industry input before finalizing

US President Donald Trump is set to announce the package of tariffs against Chinese goods on Thursday, a day earlier than rumored. It's believed that the total amount of targeted goods adds up to USD 30-60b. We believe that it will be on the higher side on the range. Additionally, there will be new restrictions on Chinese investments in the US. Treasury will be directed to outline the rules regarding Chinese investments.

But, it's reported that the tariffs won't take effect immediately. Instead, businesses are given a chance to comment on the list of tariffed products. The final decision will come after industry input. This is seen as an act of Trump bowing down to pressure from business leaders. Earlier this week, 45 of largest American trade groups wrote an open letter to Trump, warning Trump not to respond to unfair Chinese practices and policies by measures that will "harm U.S. companies, workers, farmers, ranchers, consumers, and investors."

GBP finds footing as UK employment data eyed

For now, Sterling is still trading as the second strongest major currency for the week despite yesterday's post CPI dip. Employment data will be a main focus today. Markets expect claimant counts to dropped -3.1k in February. ILO unemployment rate is expected to stay unchanged at 4.4% in January. A key focus is on wage growth as average weekly earnings is expected to rise 2.6% 3moy in January. Still, with CPI at 2.7% yoy, wage is still playing catch up.

Reaction to the job data could be muted though as the major focus is on tomorrow's BoE rate decision. BoE is widely expected to keep bank rate unchanged at 0.50% and asset purchase target at GBP 435b. No updated economic projections will be delivered as they were published back in February's Inflation Report already. Instead, eyes will be on whether BoE would turn more upbeat in the statement, given that a Brexit transition deal is already done. In addition, known hawks Michael Saunders and Ian McCafferty could come back with a vote on rate hike. All in all, focus in on gauging the chance of a May hike.

Public sector net borrowing will also be released from the UK.

CAD rebounds as US dropped one of the toughest protectionist demand in NAFTA talks

Canadian Dollar rebounds strongly on news that US will drop contentious auto-content proposal in NAFTA talks. It's seen as clearing and important road block in NAFTA renegotiation. The Loonie is trading as the strongest major currency in Asian session. There was a demand for vehicles made in Canada and Mexico for export to the US contain at least 50% US content. But Canada's Globe and Mail reported that this contentious demand was dropped during NAFTA meeting in Washington last week. This is seen by some as one of the US toughest protectionist demand.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3047; (P) 1.3075; (R1) 1.3098; More....

USD/CAD's retreat from 1.31214 extends lower today and reaches 1.3009 so far. Deeper fall could be seen to 4 hour 55 EMA (now at 1.2986). But strong support should be seen above 1.2802 cluster (38.2% retracement of 1.2246 to 1.3124 at 1.2789) to contain downside and bring rally resumption. On the upside, break of 1.3124 will extend recent rally to 161.8% projection of 1.2061 to 1.2916 from 1.2246 at 1.3629 next.

In the bigger picture, we're favoring the medium term bullish case. That is larger down trend from 1.4689 has completed at 1.2061 as a correction, drawing support from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Sustained break of 38.2% retracement of 1.4689 to 1.2061 at 1.3065 will pave the way to 61.8% retracement at 1.3685. This will be the preferred case now as long as 1.2802 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Feb | 0.30% | -0.24% | -0.30% | |

| 09:30 | GBP | Jobless Claims Change Feb | -3.1K | -7.2K | ||

| 09:30 | GBP | Claimant Count Rate Feb | 2.30% | |||

| 09:30 | GBP | Average Weekly Earnings 3M/Y Jan | 2.60% | 2.50% | ||

| 09:30 | GBP | ILO Unemployment Rate 3Mths Jan | 4.40% | 4.40% | ||

| 09:30 | GBP | Public Sector Net Borrowing Feb | -0.4B | -101B | ||

| 14:00 | USD | Existing Home Sales Feb | 5.41M | 5.38M | ||

| 14:30 | USD | Crude Oil Inventories | 5.0M | |||

| 18:00 | USD | FOMC Rate Decision | 1.75% | 1.50% | ||

| 18:30 | USD | FOMC Press Conference | ||||

| 20:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% |

Fed to hike in Powell’s debut

Fed is widely expected to raise federal funds rate by 25bps to 1.50-1.75% today. Fed fund futures are pricing in near 95% chance of that. There is no reason for Fed to give market a surprise. The main question in everybody's mind is whether Fed will hike a total of three times this year, or four. Fed fund futures are pricing more than 80% chance of another hike in June already, and close to 60% chance of another in September. But for now, it's only pricing less than 40% chance of the fourth in December.

As usual with a March FOMC meeting, new economic projections will be released. Given that the Republican's tax cuts were done, there could be upward revisions in growth. Unemployment rate forecast might be left unchanged. PCE core at 1.5% in January, is still way off Fed's median projection of 1.9% in 2018. There is little chance of a change in that figure. Meanwhile, any slight change in the federal funds rate projection would be market moving.

Fed's December projections:

The event also bears additional significance as it's Jerome Powell's first press conference as Fed chair. His Congressional testimony was seen by some as more hawkish and upbeat than expected. Recapping that he said "my personal outlook for the economy has strengthened since December." And, "we've seen some data that will in my case add some confidence to my view that inflation is moving up to target." Powell might maintain the tone today and indicate his confidence in continuing the tightening cycle.