Sample Category Title

UK CPIs the First of Several Risk Events for Sterling this Week

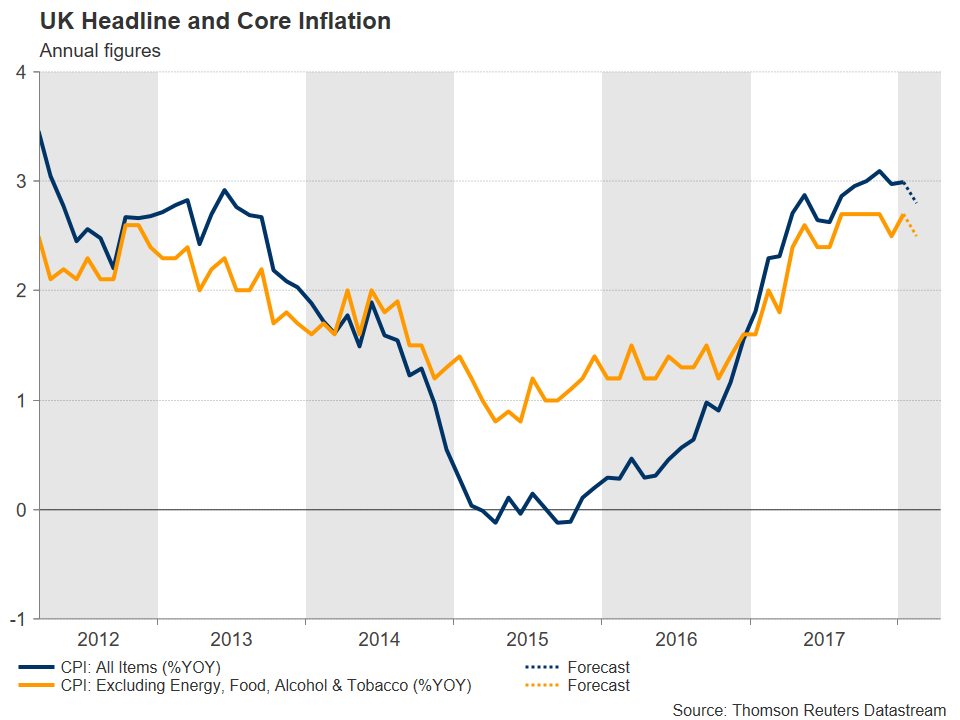

It is going to be a crucial week for the British pound, with a Bank of England (BoE) policy decision on Thursday and an EU summit that will determine whether the UK will finally obtain a transitional Brexit deal. Ahead of these events though, the UK will also release a raft of key economic data that could affect expectations around monetary policy, with the first on the list being the nation’s CPI figures for February, due out on Tuesday at 0930 GMT.

The BoE will announce its rate decision on Thursday, and while no change in policy is expected, markets will be looking for signals regarding the likelihood of a near-term rate hike, perhaps as early as at the May meeting. Whether the Bank will provide such signals though is likely to depend on the quality of incoming data, and the updated inflation numbers are among the most important ones to watch ahead of the gathering.

In February, UK inflation is forecast to have slowed somewhat in yearly terms, but to still remain well-above the BoE’s 2.0% target. The headline CPI rate is projected to have declined to 2.8% from 3.0% previously, while the core rate that excludes food and energy items is anticipated to have eased to 2.5%, from 2.7% in January.

Such prints would likely be encouraging news for the BoE, as they would signify that inflation is moving back down towards its target. What is good news for the BoE though, will probably be bad news for sterling bulls, as such a slowdown in inflation would reduce the pressure on the Bank to hike interest rates soon. Remember that raising interest rates applies downward pressure on inflation, so if inflation is edging lower on its own, the BoE can afford to stay patient for longer and keep rates unchanged. In other words, if inflation is converging towards the target by itself, it makes little sense to hike borrowing costs and risk all the unwanted consequences of higher rates, like slower consumption and economic growth.

Such prints would likely be encouraging news for the BoE, as they would signify that inflation is moving back down towards its target. What is good news for the BoE though, will probably be bad news for sterling bulls, as such a slowdown in inflation would reduce the pressure on the Bank to hike interest rates soon. Remember that raising interest rates applies downward pressure on inflation, so if inflation is edging lower on its own, the BoE can afford to stay patient for longer and keep rates unchanged. In other words, if inflation is converging towards the target by itself, it makes little sense to hike borrowing costs and risk all the unwanted consequences of higher rates, like slower consumption and economic growth.

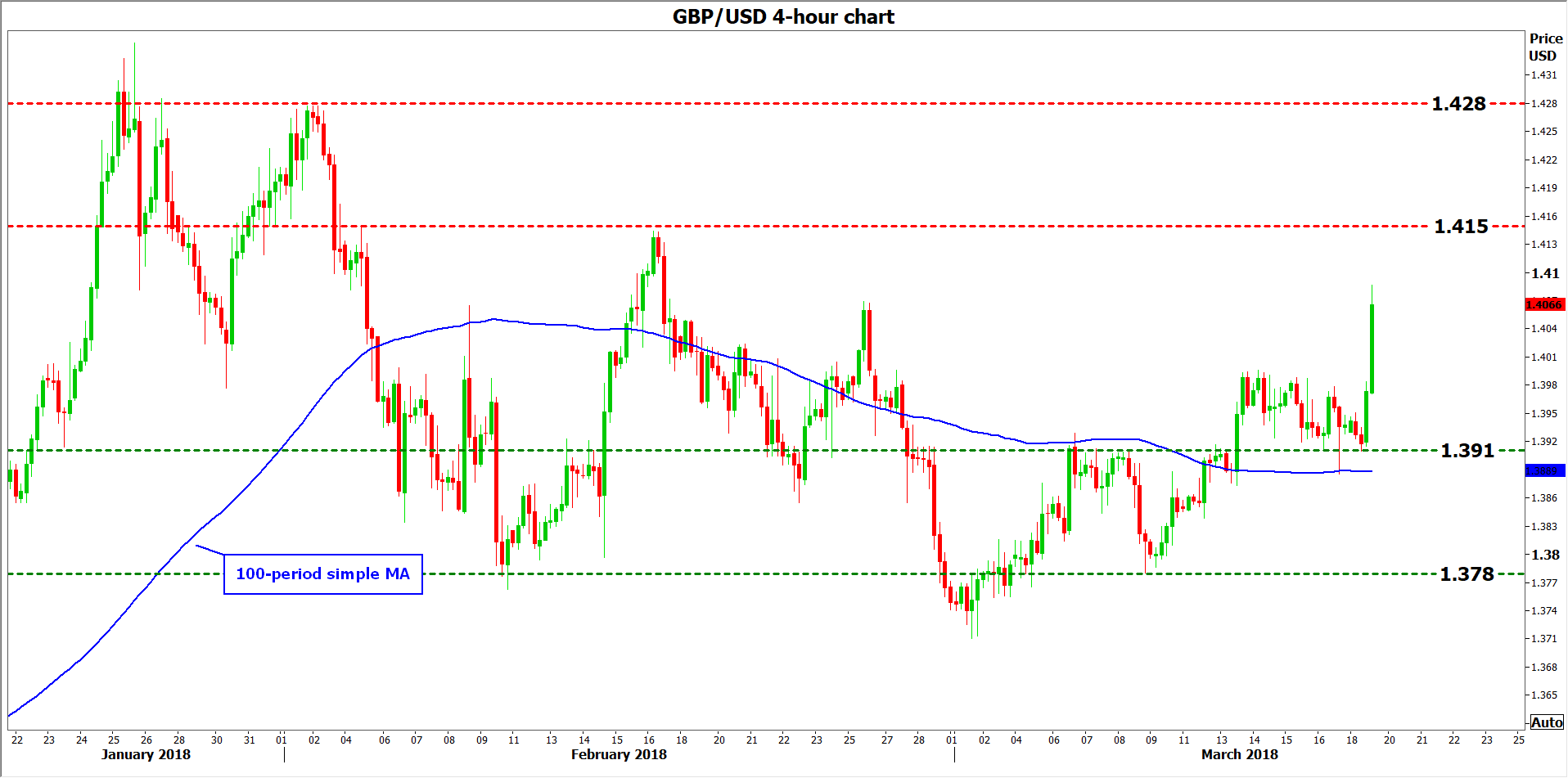

Expectations that the BoE will raise rates by 25bps at its May meeting are currently riding high, with markets attaching a 70% probability to that scenario according to the UK overnight index swaps. Should the UK CPIs – particularly the core rate – decline by more than expected, that could push the probability for a May rate hike lower, and sterling is likely to follow suit. In this scenario, sterling/dollar could edge lower and aim for another test of the 1.3910 territory, marked by the March 19 lows. Further declines after that would bring the 1.3780 zone in play, identified by the troughs of March 9.

A positive surprise in the CPIs on the other hand, for example a smaller-than-anticipated decline in the core rate, could push the probability for a May rate increase higher, and sterling alongside it. In this case, Cable would likely surge and challenge the 1.4150 hurdle, marked by the highs of February 16. If buyers manage to overcome that barrier, then sell orders may be found near 1.4280, the February 2 peak.

As for which scenario is more likely, the UK services PMI for February showed that prices charged by service companies increased at the weakest rate for six months, supporting the forecast for a slowdown in the CPIs. Considering that services account for roughly 80% of UK GDP, this PMI is typically considered a decent gauge of the broader economy.

As for which scenario is more likely, the UK services PMI for February showed that prices charged by service companies increased at the weakest rate for six months, supporting the forecast for a slowdown in the CPIs. Considering that services account for roughly 80% of UK GDP, this PMI is typically considered a decent gauge of the broader economy.

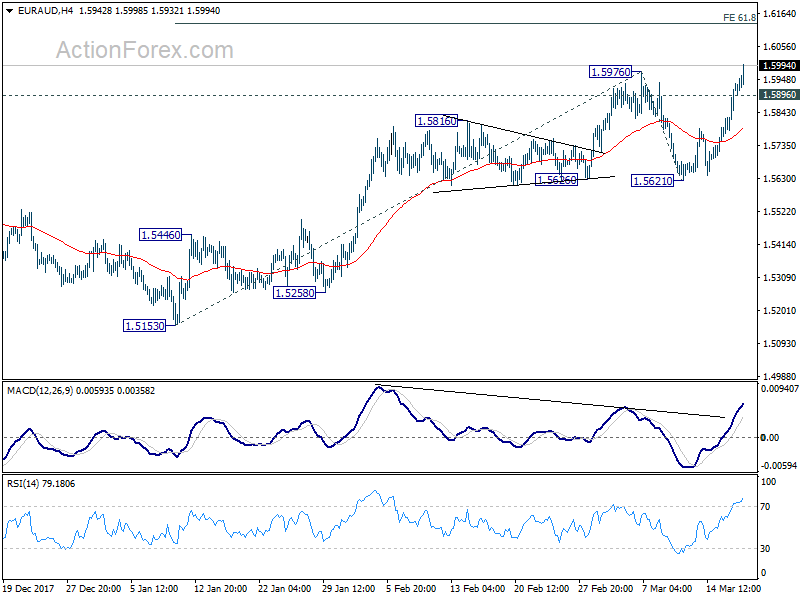

EUR/AUD Mid-Day Outlook

Daily Pivots: (S1) 1.5816; (P) 1.5876; (R1) 1.5982; More....

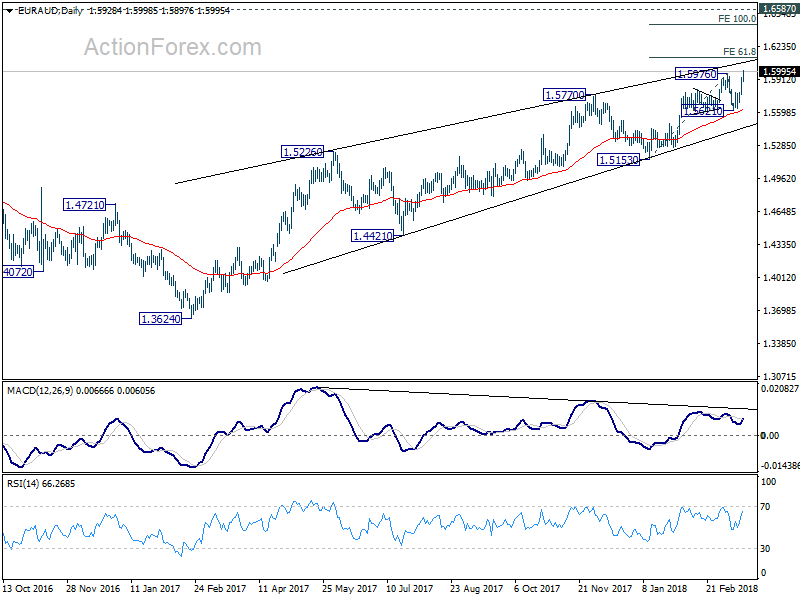

EUR/AUD's rise continues today and reaches as high as 1.5998 so far. The break of 1.5976 high indicates resumption of medium term up trend from 1.3624. Intraday bias stays on the upside for 61.8% projection of 1.5130 to 1.5976 from 1.5621 at 1.6130 first. On the downside, below 1.5896 minor support will turn intraday bias neutral first. But outlook will now remain bullish as long as 1.5621 support holds.

In the bigger picture, current development suggests that rise from 1.3624 is not completed yet. And it's still in progress for 1.6587 key resistance level. We'd be cautious on strong resistance from there to limit upside, on bearish divergence condition in daily MACD. But for now, break of 1.5153 support is needed to indicate medium term reversal. Otherwise, outlook will stays bullish even in case of deep pull back.

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.23; (P) 147.73; (R1) 148.22; More....

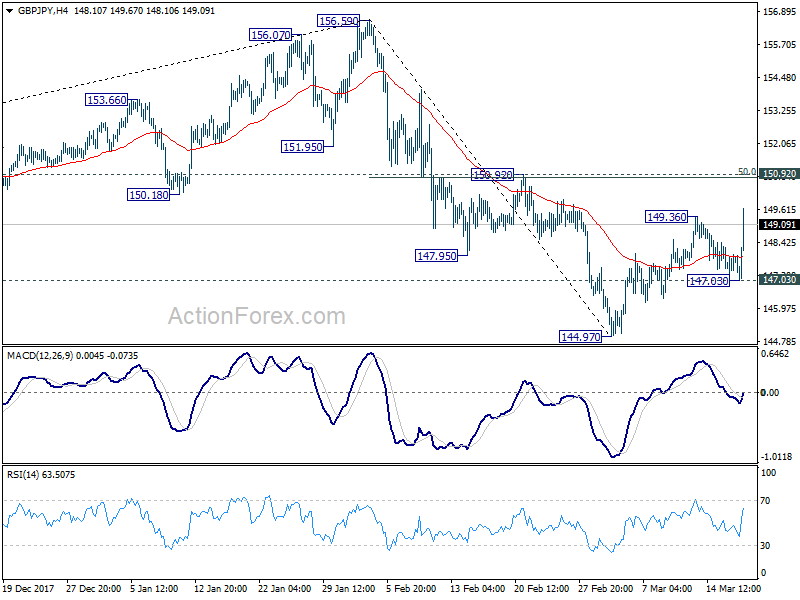

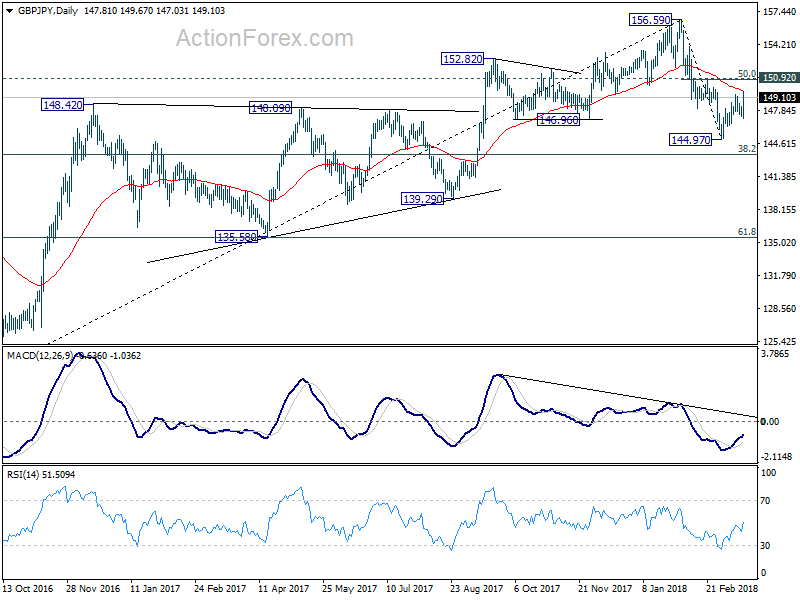

GBP/JPY's rebound from 144.97 resumes today by breaking 149.36 and hits as high as 149.67 so far. Intraday bias is mildly on the upside for further rally. Nonetheless, such rebound is viewed as a corrective move. Hence, we'd expect strong resistance from 150.92 (50% retracement of 156.59 to 144.97 at 150.78) to bring fall resumption. On the downside, below 147.03 will bring retest of 144.97 low first. Break will extend the decline from 156.59 to 143.51 medium term fibonacci level next. However, sustained break of 150.92 will pave the way back to retest 156.69 high.

In the bigger picture, the case for medium term reversal continues to build up. There is bearish divergence condition in daily MACD. 146.96 support was taken out. And GBP/JPY was rejected by 55 month EMA. Break of 38.2% retracement of 122.36 to 156.59 at 143.51 will pave the way to 61.8% retracement at 135.43 and below. This will now be the preferred case as long as 150.92 resistance holds.

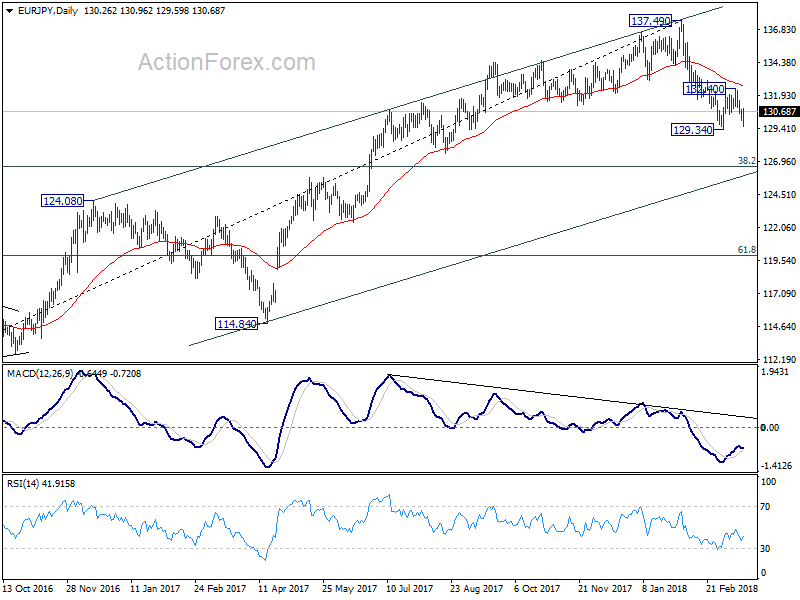

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 129.88; (P) 130.39; (R1) 130.71; More....

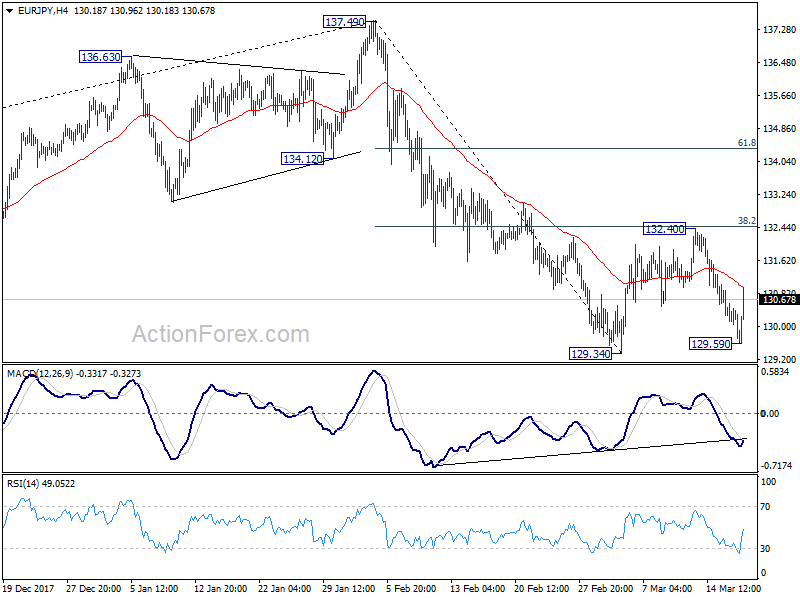

EUR/JPY rebounds strongly ahead of 129.34 low and a temporary bottom is formed at 129.59. Intraday bias is turned neutral first. Consolidation from 129.34 might extend with another up-leg. But upside should be limited by 38.2% retracement of 137.49 to 129.34 at 132.45 to bring fall resumption eventually. On the downside, decisive break of 129.34 will confirm resumption of whole fall 137.49 and target 126.61 medium term fibonacci level.

In the bigger picture, current development argues that rise from 109.03 (2016 low) has completed at 137.49, on bearish divergence condition in weekly MACD. Deeper fall should be seen to 38.2% retracement of 109.03 to 137.49 at 126.61 first. On the upside, break of 137.49 is needed to confirm medium term rise resumption. Otherwise, risk will now stay on the downside even in case of strong rebound.

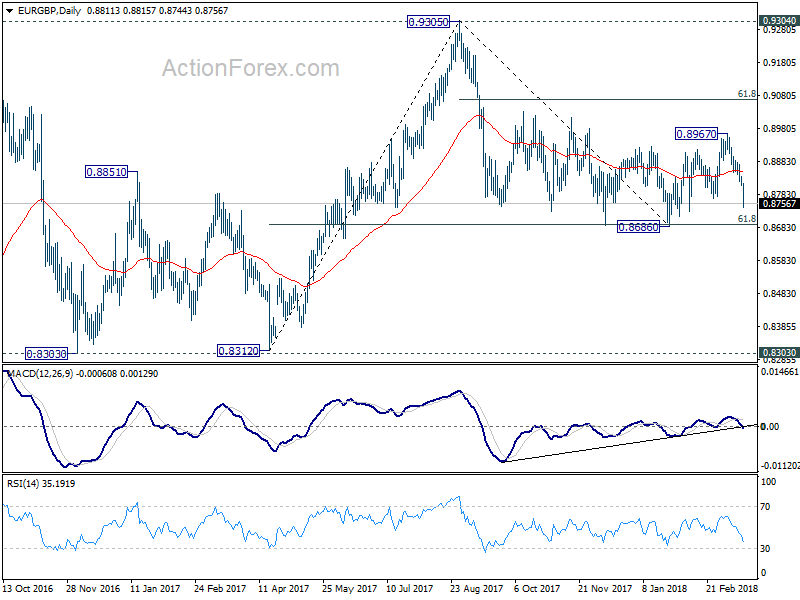

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8797; (P) 0.8817; (R1) 0.8828; More...

EUR/GBP's decline accelerates to as low as 0.8744 so far. Break of 0.8771 support confirms confirm completion of rebound from 0.8686 at 0.8967. Intraday bias stays on the downside on the downside for retesting 0.8686 key near term support. We'd be cautious on strong support from there to bring another rebound. But decisive break of 0.8686 will resume whole fall from 0.9305 and target 0.8303 key support next. On the upside, above 0.8815 minor resistance will turn bias neutral and bring consolidation first, before staging another fall.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.58; (P) 105.97; (R1) 106.34; More...

No change in USD/JPY's outlook. Range trading continues inside 105.24/107.67 and intraday bias remains neutral. With 107.67 resistance holds, near term outlook remains bearish and deeper fall is expected. On the downside, break of 105.24 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. On the upside, firm break of 107.67 resistance will indicate near term reversal, on bullish convergence condition in 4 hour MACD. In such case, outlook will be turned bullish for 110.47 resistance next.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

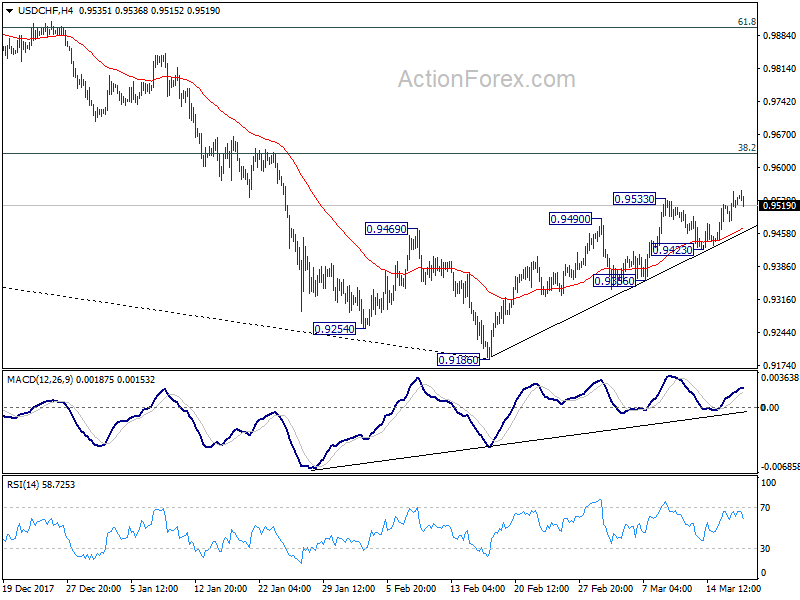

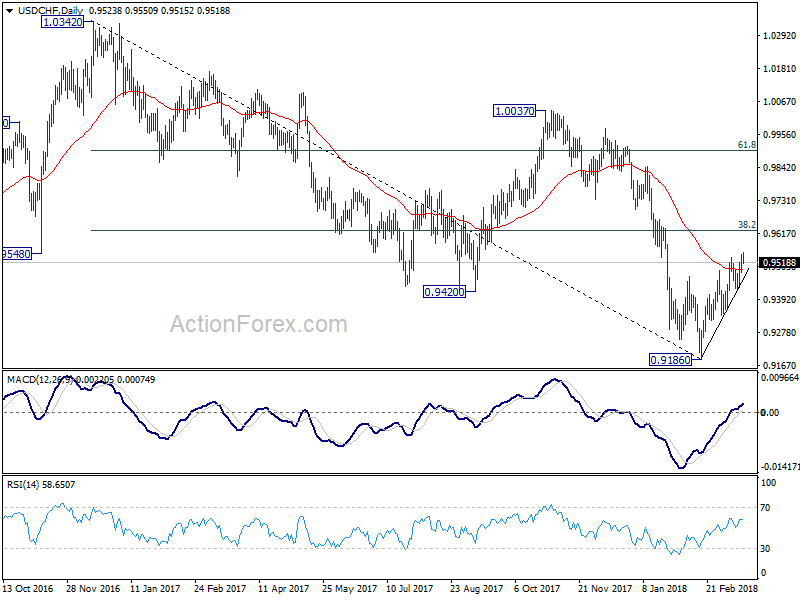

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9484; (P) 0.9516; (R1) 0.9546; More...

USD/CHF lost some momentum after hitting 0.9550. But still intraday bias stays on the upside. The rebound from 0.9186 is in progress for 0.9626 fibonacci level. Firm break there will carry larger bullish implications. On the downside, break of 0.9423 is needed to indicate completion of the rebound. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Current development is raising the chance that it is completed. But there is no confirmation yet. Focus will now be back on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add much credence to the case of trend reversal and target 61.8% retracement at 0.9900 and above. However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

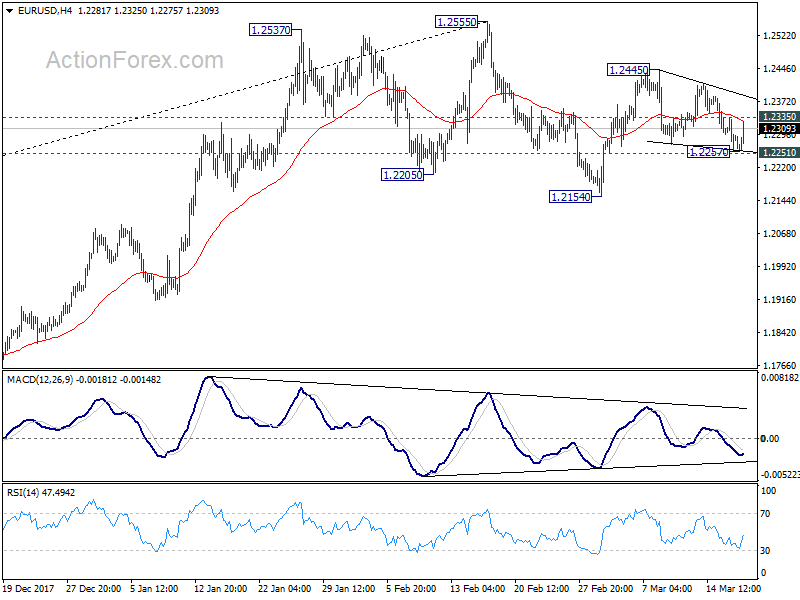

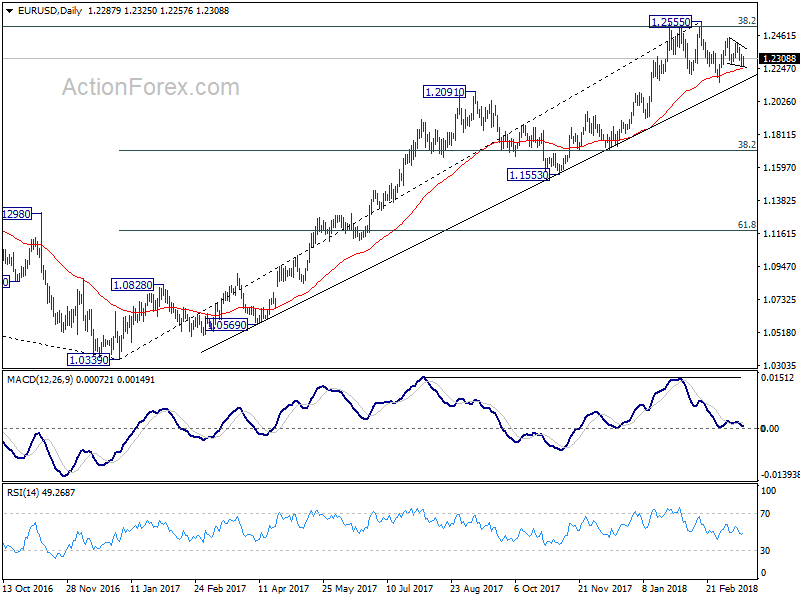

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2252; (P) 1.2294 (R1) 1.2328; More....

EUR/USD recovers strongly ahead of 1.2251 support. But for now it's staying below 1.2335 minor resistance. Intraday bias remains neutral first. Overall, with 1.2251 intact, further rise is expected in the pair. Above 1.2235 will turn bias to the upside for 1.2445 first. Break will confirm resumption of rebound form 1.2154 and target a test on 1.2555 high. But again, on the downside, firm break of 1.2251 will confirm completion of rebound from 1.2154. And intraday bias will be turned to the downside to extend the fall from 1.2555 through 1.2154.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Euro, Pound Post Strong Rally; European Equities Open Lower

Here are the latest developments in global markets:

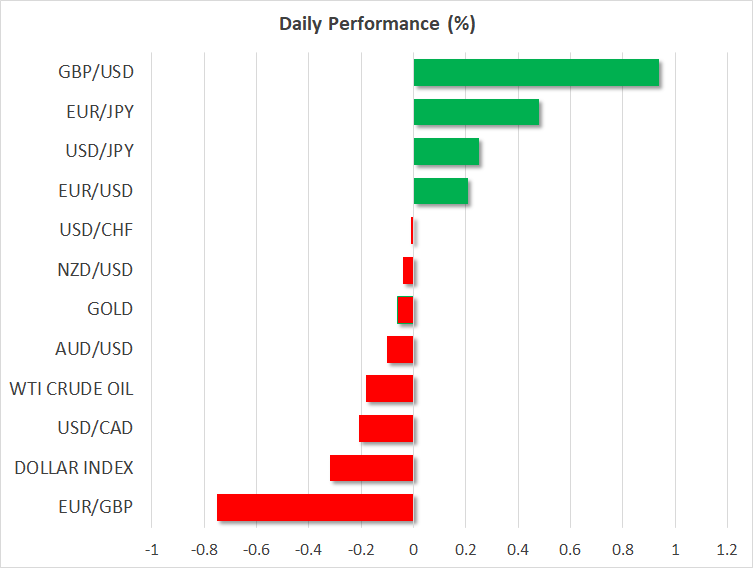

FOREX: The US dollar index outperformed on the day against a basket of currencies, falling to 89.97 (-0.22%) as the euro and the pound strengthened. Dollar/yen was gaining positive momentum in the face of uncertainties surrounding the Japanese finance minister and ahead of the FOMC rate decision on Wednesday, with the pair climbing to 106.30 (+0.21%). Euro/dollar recouped Friday’s losses rallying to 1.2324 (+0.13%) after Reuters sources reported that the ECB has shifted focus from the QE program to the path of interest rates, while pound/dollar and pound/yen hit three-week highs during early European afternoon as sources familiar with Brexit negotiations stated today that the EU and the UK agreed on the broad terms of Britain’s two-year transition deal after leaving the bloc in March 2019. The Canadian dollar was hit the hardest the past week. The loonie came under heavy selling pressure, driving dollar/loonie above the 1.3100 key level early this morning, creating a new 9-month high. Aussie/dollar was trading lower at 0.7695 (-0.27%) despite positive comments from the RBA Assistant Governor Christopher Kent and strong readings on Australia’s consumer confidence in the preceding week.

STOCK: European equities started the day on a softer tone as most of them are completing a red day. Stocks declined globally on Monday as investors awaited some risk events to take place this week, including central banks decisions, a EU summit, and the G20 meeting. The blue-chip Euro Stoxx 50 was down by 0.72%, the German DAX 30 plunged by 0.94% and the British FTSE 100 sank by 1.32% to the lowest level in almost two weeks of 7069.97 at 1030 GMT. The major US indices are poised to open lower today according to US mini stock futures

COMMODITIES: Oil prices were mixed. WTI crude oil was down by 0.08% at $62.29 per barrel, while Brent crude was up by 0.12% at $66.31. Copper plunged by 1.07% near the $3.06 level. Gold was weak at $1311.31 (-0.07%) per ounce.

Day ahead: G20 meeting could wake trade jitters; RBA meeting minutes due in the Asian session

Day ahead: G20 meeting could wake trade jitters; RBA meeting minutes due in the Asian session

The economic calendar will be empty of major data in the remaining of the day, giving some time to investors to prepare their positions ahead of high-spot events this week including three central bank policy meetings, a EU summit and the conclusion of the ongoing G20 meeting where finance ministers are expected to put pressure on the US over its unexpected trade protectionism.

Today, finance ministers from the Group of 20 biggest economies are gathering in Buenos Aires, Argentina, to kick off a two-day meeting, with the representatives expected to discuss on the performance of the global economy and the risks to growth. While such events are not usually attracting attention in foreign exchange markets, this time investors are eagerly anticipating to hear some critics against Trump’s recent import tariffs on steel and aluminum and his intention to take more aggressive steps against China, which have the potential to unleash a global trade war. The US Secretary Steven Mnuchin who will head the US team during the talks and has recently backed Trump’s tariff plans, could be in the defensive probably avoiding any comments that could worsen the negative sentiment around the story. However, if he disappoints his counterparts, supporting the need for further import tariffs on China, the dollar and other currencies linked to China’s economic performance such as the aussie and the kiwi could take a knock, while safe-haven assets could bounce higher.

Dollar bears could also take control if the Fed which starts its two-day policy meeting on Tuesday holds a dovish stance, probably throwing some cold water on speculations that the central bank could raise rates four times this year instead of three currently priced in the markets. Note that, Jerome Powell who will preside over his first meeting as Fed chair is highly expected to announce a 25bps rate hike at the conclusion of the meeting on Wednesday. The Reserve Bank of New Zealand and the Bank of England will follow but no change is expected in their monetary policy.

The EU summit on March 22-23 will be in focus as well for any updates on the Brexit front. If EU leaders manage to achieve a deal on the transition period, the pound could be free to join gains.

Turning to today’s public appearances, the Atlanta Fed President, Raphael Bostic will be speaking at 1340 GMT, while the ECB Executive board member, Yves Mersch will discuss on 2018 monetary policy challenges at 1800 GMT. Earlier, the Norges Bank Governor Oystein Olsen will also make comments at 1600 GMT.

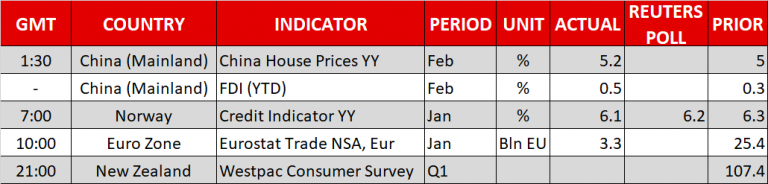

Early on Tuesday, during the Asian session, the Reserve Bank of Australia (RBA) will publish monetary policy meeting minutes (0030 GMT), while at the same time the Australian Bureau of Statistics will be releasing figures on house prices for the final quarter of 2017. Recall that the RBA held interest rates unchanged at record lows for the 17 consecutive month on March 6, as they are waiting for further tightening in labour market to translate into faster wage growth and hence push inflation up towards the RBA’s target.

The Week ahead: FOMC, Trump Tariffs and UK Inflation in Focus

Concerns over the potential for a Trump trade war still seem to be weighing on the minds of investors, with a lack of risk appetite still leading to caution in global stock markets.

Asian stocks were mostly mixed during early trading amid market anxiety, while European equities are currently following the lead from Asia. Trade war fears are lingering in the atmosphere and with political uncertainty in Washington still dominating headlines, stocks could remain under pressure ahead of the highly-anticipated Federal Reserve meeting this week.

Will Powell elevate the Dollar?

The main risk event for the Dollar this week will be the two-day Federal Open Market Committee monetary policy meeting, which is expected to conclude with the central bank raising US interest rates.

With markets heavily pricing in a US rate increase this month, the decision might not have a significant impact on the Dollar. Investors will instead be expected to closely scrutinize the statement for fresh insight into how many times the Fed will raise interest rates in 2018.

Jerome Powell’s optimism over the US economy has encouraged further speculation that the Fed might raise interest rates four times this year. Investors will be paying attention to see if Powell maintains a hawkish stance during his first press conference as Fed Chair. They will also be looking for further indications regarding the potential of four US interest rate increases this year and this would be seen as encouragement for reigniting trader demand for the USD.

Expectations of higher US interest rates are considered as the main catalyst to improve Dollar demand. Political instability in Washington and concerns about Trump’s trade policies negatively impacting the US economy, are seen as the major risks for Dollar demand.

The Dollar is still being driven by conflicting fundamental themes, and there is room for volatility in the Greenback this week.

UK inflation and BoE meeting in focus

This week is a potential busy one for the British Pound. Investors will be tussling with a variety of different economic releases, including inflation, jobs data, retail sales and a Bank of England policy meeting.

Inflation data for February is expected to edge slightly lower which could pressure the Pound. A decline in inflation pressure would be seen as a threat to the Bank of England possibly raising UK interest rates later this year.

The Bank of England is widely expected to leave interest rates unchanged this month.

Attention will be directed to the language of the accompanying statement, in case the wording provides any clues towards the potential timings of a change in UK interest rates.

Sterling not only remains highly sensitive to monetary policy speculation but also to ongoing Brexit developments. Any fresh signs of the Brexit negotiations moving in the right direction could push the British Pound higher.

Gold depressed ahead of FOMC

Gold extended losses on Monday with prices dipping below $1310 as the Dollar remained buoyed by expectations of an interest rate hike by the Fed this week.

Although fears of a trade war and US political uncertainty have stimulated appetite for safe-haven assets, price action suggests that Gold remains pressured due to speculation of higher US interest rates. Taking a look at the technical picture, Gold is under increasing pressure on the daily charts. Prices are trading below the daily 50 SMA while the MACD has crossed to the downside. Sustained weakness under $1314 could encourage a decline towards the psychological $1300 level.