Sample Category Title

Expect The Fed To Dial Up On Rates

Monday March 19: Five things the markets are talking about

This week, the FOMC (Mar 21), the Bank of England and the Reserve Bank of New Zealand (Mar 22) will announce their monetary policy decisions.

Fed officials are expected to weigh whether they will need to raise interest rates more aggressively in the coming months and years because of recent U.S tax cuts and government-spending increases.

Last December, officials expected a gradual path of rate hikes would allow the U.S economy to keep expanding without overheating. Officials penciled in three rate increases for 2018, and two each in 2019 and 2020.

However, fiscal stimulus, coupled with steady growth and low unemployment, is raising questions about how long U.S officials are expected to maintain that approach.

This Fed meeting is also the first to be led by its new Fed chair, Jerome Powell, who has promised “continuity with the gradual rate rise path” charted by former Chair Janet Yellen.

A +25 bps is already priced in for this week’s FOMC meeting ending Wednesday. Officials will also release updated projections showing whether more of them now favour four rate moves this year rather than three.

Elsewhere, flash March PMI’s will be released for Japan, the Eurozone, Germany, France and the U.S.

Japan will post last months merchandise trade along with consumer prices. Key data for the U.K will include consumer and producer prices and the labor market report will be released.

Finally, the E.U leader summit begins on Thursday – E.U leaders are to decide if sufficient progress has been made on the U.K’s Brexit transition period.

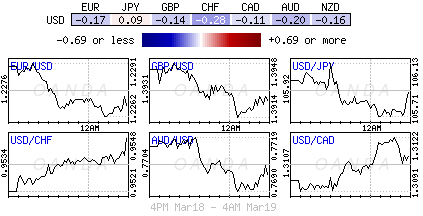

1. Stocks mixed markets

In Japan, the Nikkei share average dropped to a new one-week low overnight as investors responded to opinion polls showing falling support for PM Abe amid a ‘cronyism’ scandal. The Nikkei fell -1.2%, while the broader Topix fell -0.9%.

Down-under, the Aussie S&P/ASX 200 was up +0.2%, with the energy sector bouncing +1.5% following Friday’s near-2% gain in oil prices. In S. Korea, the Kospi was down -0.3%.

In Hong Kong, stocks were little changed as investors await Fed Chair Powell’s first press conference on Wednesday. The market is also digesting a slew of new appointments by Beijing, as China forms its new economic team under the new five-year term of President Xi Jinping. At the close, the Hang Seng index was largely unchanged, while the China Enterprises Index lost -0.1%.

In China, stocks ended higher overnight, with gains led by healthcare firms, after Beijing formed a new economic team. At the close, the Shanghai Composite index was up +0.3%, while the blue-chip CSI300 index gained +0.4%.

In Europe, regional indices have started the week on the back foot, following Asian’s mixed session. The DAX and FTSE are down -1%.

U.S stocks are set to open deep in the ‘red’ (-0.5%).

Indices: Stoxx600 -0.7% at 375.0, FTSE -1.1% at 7086, DAX -1.1% at 12259, CAC-40 -0.8% at 5239, IBEX-35 -0.7% at 9692, FTSE MIB -0.6% at 22717, SMI -0.6% at 8832, S&P 500 Futures -0.5%

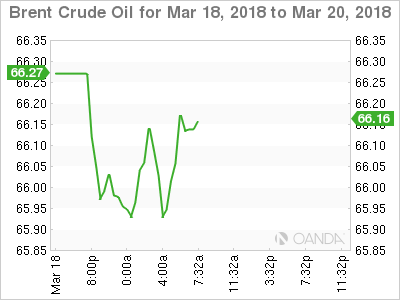

2. Oil prices fall as increased U.S. drilling points to higher output

Oil prices are under pressure as increased drilling in the U.S points to more output, raising concerns about a return of oversupply.

Brent crude futures are at +$65.99 per barrel, down -22c, or -0.3%. U.S West Texas Intermediate (WTI) crude futures are at +$62.14 a barrel, down -20c, or -0.3%, from Friday’s close.

According to Baker Hughes drilling report on Friday, U.S drillers added four oilrigs in the week to March 16, bringing the total count to 800.

The U.S rig count is much higher than a year ago, as energy companies have boosted spending – U.S crude oil production has risen by more than a fifth since mid-2016, to +10.38m bpd, pushing it past top exporter Saudi Arabia.

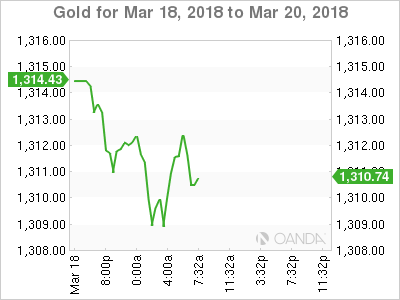

Ahead of the U.S open, gold prices are under pressure for a fourth consecutive session, as the ‘big’ dollar stays firm ahead of Wednesday’s Fed rate announcement. Spot gold is down -0.2% at +$1,310.03 per ounce – prices fell to +$1,307.51 earlier in the session, their lowest since March 1.

3. Central banks take center stage for bonds

The fixed income market will be looking at a series of policy events and data for guidance this week, while sovereign supply is muted.

Bond traders await the U.S Fed’s decision on Wednesday, when a +25 bps rate raise is expected. Thursday sees rate decisions for the U.K, New Zealand, Indonesia and the Philippines.

The BoE is expected to keep interest rates unchanged at +0.5%. The decision is expected to be “unanimous,” but any dissenting vote to raise rates would strengthen ideas of a rate increase in Q2. The market is currently pricing in a little more than +66% chance of a BoE rate increase in May, with the odds drifting higher over the past couple of weeks.

As for bond yields in the eurozone, underlying support from the ECB in the form of asset purchases continues to limit the upside in euro yields. Germany’s 10-year Bund yield trades at +0.57%, while in the U.K, the 10-year Gilt yield has backed up +2bps to +1.429%, the biggest increase in almost two-weeks. The yield on U.S 10’s have advanced +2 bps to +2.87%, the highest in more than a week.

4. Dollar starts the week supported

The USD starts the week on firm footing as the first FOMC meeting under Chair Powell takes place mid-week with expectations that U.S policy makers would hike +25 bps and deliver a ‘hawkish” statement.

This is expected to be a big week for sterling (£1.4000) and Brexit. E.U Leaders gather on Thursday to begin a two-day Summit to decide if sufficient progress has been made on the transition period that the next and last chapter – the new relationship – could be addressed. BoE meets on Thursday and the market will focus on the minutes and the vote of the decision.

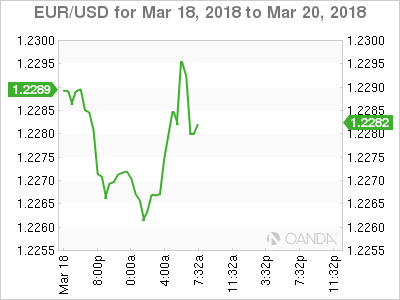

EUR/USD (€1.2291) is holding below the psychological €1.23 print as more ECB members (Weidmann, Knot and Villeroy) over the weekend expressed confidence that the +2% inflation target would be achieved in the medium term.

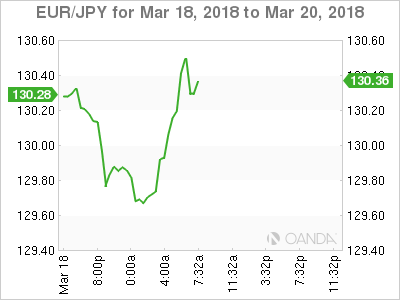

Elsewhere, the yen has climbed +0.1% to ¥105.93, the strongest in more than two-weeks, while South Africa’s rand (ZAR) sank -0.6% to $12.0421, the weakest in more than five-weeks.

5. Eurozone exports slide

Data this morning showed that the eurozone’s exports of goods to the rest of the world fell in January as a strengthening EUR may finally be weakening economic growth.

The E.U statistics agency said that, adjusted for seasonal variations, exports fell -0.7% in January from December, while imports rose by +1.1%. That resulted in a drop in the seasonally adjusted trade surplus to €19.9B from €23.2B in the final month of 2017.

Note: Without seasonal adjustment, the eurozone recorded a surplus of +€3.3B, having recorded a deficit of -€1.4B in January 2017.

Eurostat said the EU’s trade surplus with the U.S widened to +€10.3B from +€9.7B a year earlier.

DAX Down Sharply As European Tech Stocks Slide

The DAX index has posted sharp losses in the Monday session. Currently, the DAX is trading at 12,284, down 0.85% on the day. On the release front, it’s a quiet start to the week. The eurozone trade surplus fell to EUR 19.9 billion, missing the estimate of EUR 22.6 billion. This marked a 3-month low. On Tuesday, Germany releases PPI and ZEW Economic Sentiment.

The DAX has taken a cold shower to start the week, with sharp losses on Monday. European technology stocks are in the red, after Micro Focus, one of Britain’s largest tech firms, saw its shares plunge by 55 percent after it lowered its revenue forecast and its CEO resigned. Investor sentiment has chilled, sending the DAX lower.

The eurozone economy is enjoying a strong first quarter in 2018, with a robust German economy leading the way. A stronger global appetite has boosted exports and the manufacturing sector, while unemployment continues to drop. However, inflation, which has persistently hovered at low levels, continues to pose a problem for policymakers. In fact, Eurozone Final CPI has been dropping in recent months, and this worrisome trend continued on Friday, when the indicator dropped to 1.1%, down from 1.3% a month earlier. This marked the weakest gain since December 2016. ECB President Mario Draghi addressed inflation concerns last week, and sounded cautious. Draghi said that the ECB still needed to see evidence that inflation was gaining strength before there could be any talk about a change in monetary policy. In the meantime, Draghi said the ECB would remain “patient, persistent and prudent”. Stronger economic conditions have led to growing speculation that the ECB will wind up its stimulus program in September. However, there is still plenty of slack in the economy, and coupled with low inflation, Draghi can afford to remain cautious and maintain current monetary policy for some time.

Euro Starts Week Sideways As Investors Search For Cues

EUR/USD has ticked higher in the Monday session. Currently, the pair is trading at 1.2295, up 0.05% on the day. On the release front, the Eurozone trade surplus fell to EUR 19.9 billion, missing the estimate of EUR 22.6 billion. This marked a 3-month low. There are no US events on the schedule. On Tuesday, Germany releases PPI and ZEW Economic Sentiment.

On Friday, US numbers were mixed, and EUR/USD showed limited movement. Construction data disappointed, as Building Permits dropped to 1.30 million, shy of the estimate of 1.30 million. Housing Starts followed a similar trend, falling to 1.24 million and missing the forecast of 1.29 million. There was better news from consumer confidence, as UoM Consumer Sentiment improved to 102.0, beating the estimate of 99.3 points. This marked the first time that the indicator has been over the symbolic 100 level since October 2017.

The eurozone economy is enjoying a solid first quarter in 2018. A stronger global appetite has boosted exports and the manufacturing sector, while unemployment continues to drop. However, inflation, which has persistently hovered at low levels, continues to pose a problem for policymakers. In fact, Eurozone Final CPI has been dropping in recent months, and this worrisome trend continued on Friday, when the indicator dropped to 1.1%, down from 1.3% a month earlier. This marked the weakest gain since December 2016. ECB President Mario Draghi addressed inflation concerns last week, and sounded cautious. Draghi said that the ECB still needed to see evidence that inflation was gaining strength before there could be any talk about a change in monetary policy. In the meantime, Draghi said the ECB would remain “patient, persistent and prudent”. Stronger economic conditions have led to growing speculation that the ECB will wind up its stimulus program in September. However, there is still plenty of slack in the economy, and coupled with low inflation, Draghi can afford to remain cautious and maintain current monetary policy for some time.

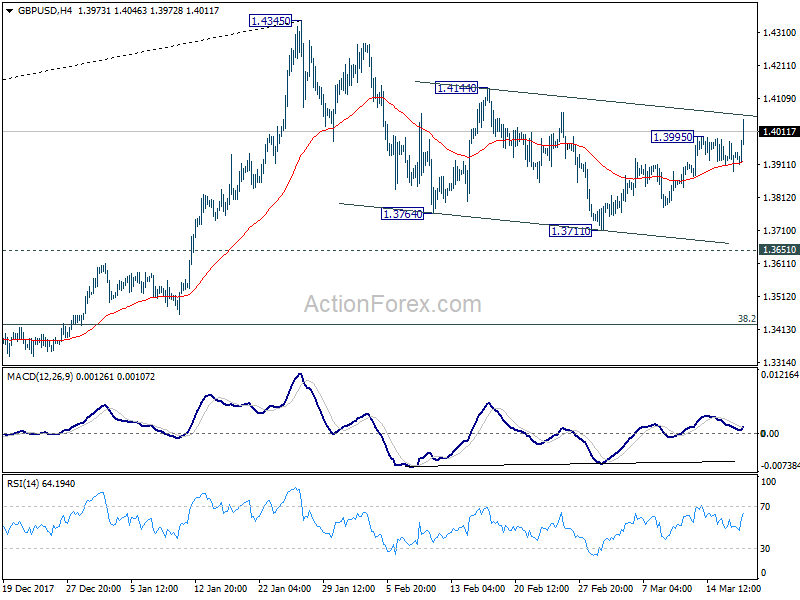

Sterling soars as Brexit transition deal “done”. GBP/USD and EUR/GBP updates

Sterling jumps sharply on news that Brexit transition deal is agreed. And, it's only awaiting sign-off by UK Brexit Secretary David Davis and EU Chief Negotiator Michel Barnier. David and Barnier are meeting in Brussels to hammer out the details today. The legal text of the agreement is expected to be delivered to the EU summit on Thursday and Friday for final approval. Davis and Barnier will hold a joint press conference later today.

It's reported elsewhere that the cut off date for the transition period will be December 2020. And, UK will be allowed to make 3rd party trade deals during the transition.

GBP/USD takes out 1.3995 to resume the rally from 1.3711. It's on course for a test on 1.4144. And, it's getting more convincing that the correction from 1.4345 is completed. And the pair is ready for resuming larger up trend from 2016 low at 1.1946.

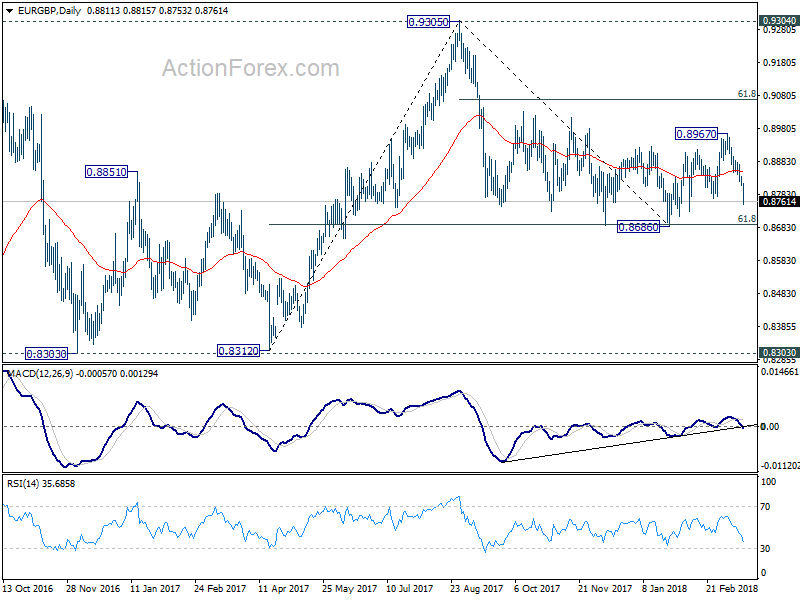

EUR/GBP's break of 0.8871 support also confirm that the corrective rise from 0.8686 has completed at 0.8967. Deeper fall should be seen to retest 0.8686 in near term. It's a bit early to tell if fall from 0.9305 is resuming. But momentum looks promising.

EUR/GBP's break of 0.8871 support also confirm that the corrective rise from 0.8686 has completed at 0.8967. Deeper fall should be seen to retest 0.8686 in near term. It's a bit early to tell if fall from 0.9305 is resuming. But momentum looks promising.

Markets Lower On Trade War Concerns

- US Futures Drop as EU Proposes Counter-Measures;

- GBP Rallies on Brexit Transition Deal Hopes;

- Fed, BoE and UK Data in Focus This Week.

US Futures Drop as EU Proposes Counter-Measures

It’s been a rocky start to trading at the start of the week, as the prospect of a trade war becomes ever more real.

Tariffs are likely to be the main topic of conversation at the G20 meeting at the start of the week after the European Union release details of counter-measures against Donald Trump’s steel and aluminium tariffs. The list totalled around €6.4 billion and will be intended to dissuade Trump from implementing tariffs on the EU, although given what’s been said previously by the US President, further counter-tariffs could be more likely. The question is whether the measures announced by the EU are sufficiently targeted so as to hurt the Republicans in the mid-term elections later this year.

Despite what he says, I’m not sure that a trade war is what Trump actually wants from these tariffs or that he’ll find much support for one within his party. I think the measures were intended to bring certain countries back to the negotiating table and intensify NAFTA negotiations. As yet, it appears other countries are in no mood to be pushed around and if Trump insists on following through on his threats, markets may react more negatively that we’ve seen so far.

GBP Rallies on Brexit Transition Deal Hopes

The pound is up more than half a percent against the dollar, euro and yen this morning, as confidence grows that a deal on the Brexit transition will be agreed this week. There has been reports that a deal has been close for days and David Davis has today flown to Brussels to meet his EU counterpart Michel Barnier. The hope is that a deal can be agreed ahead of a meeting of EU leaders later this week which will enable both sides to begin talks on the future relationship which needs to be wrapped up later this year.

A press conference with Davis and Barnier is believed to have been pencilled in for around midday although this has not yet been confirmed. If this goes ahead, it would suggest a deal has been reached and perhaps it’s the speculation around this that’s leading the pound higher this morning.

Fed, BoE and UK Data in Focus This Week

There may also be an element of caution ahead of another busy week for financial markets. Monday is a little quiet by comparison to the rest of the week, with the Federal Reserve poised to raise interest rates and release new economic projections on Wednesday. The Bank of England will meet on Thursday and while no rate hike is expected from them, markets are expecting at least one this year, with May being well priced in. If that’s to materialise, you would expect some quite strong hints this Thursday.

The UK will be a primary focus for many investors this week, with inflation, retail sales and labour market data also being released. This comes on top of Brexit talk and the ongoing dispute with Russia over the poisoning of an ex-spy in Salisbury a couple of weeks ago. Russia has denied any involvement despite the US, France and Germany joining the UK in accusing the country of carrying out the attack.

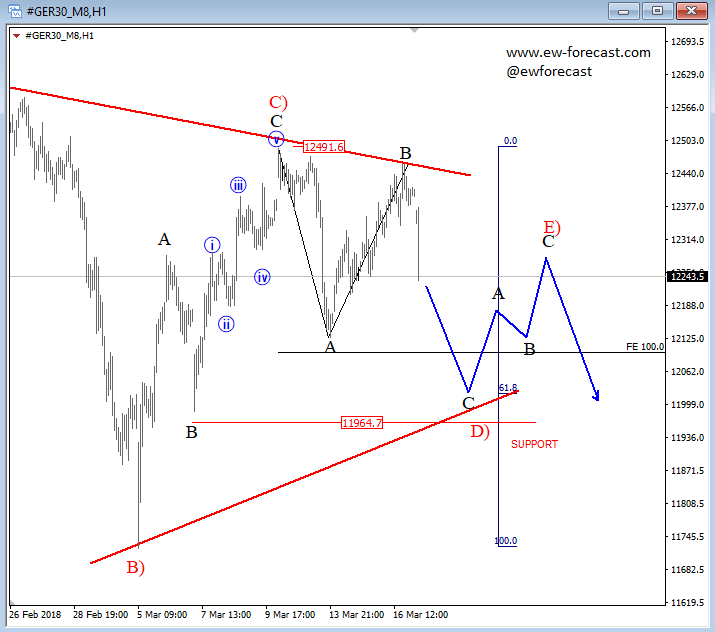

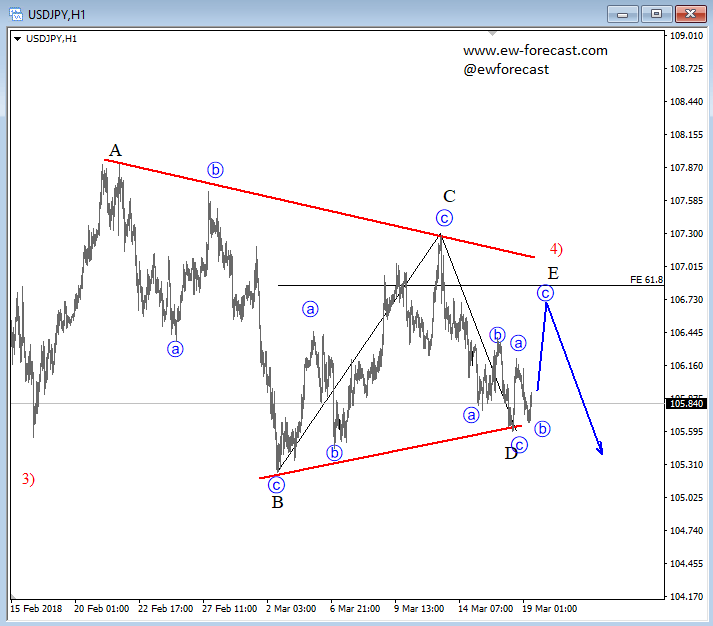

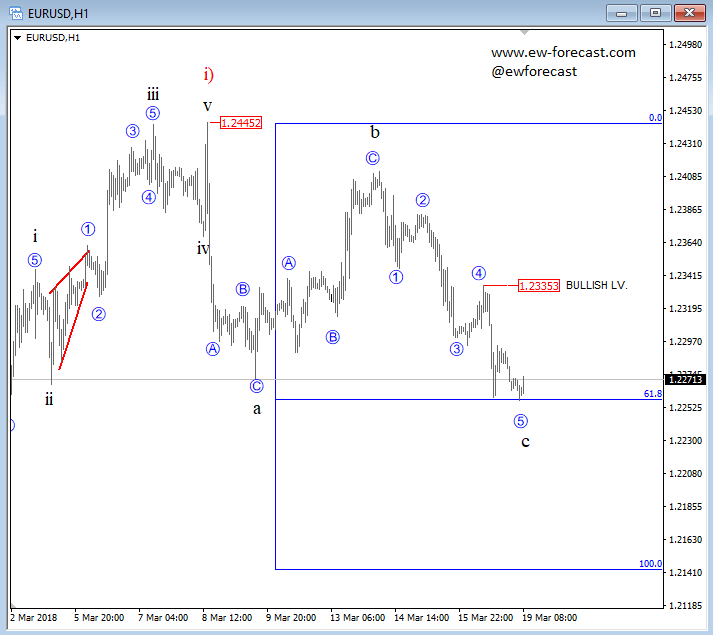

Elliott Wave Analysis: German DAX, USDJPY And EURUSD Update

We can see a nice move down on stocks this morning, with DAX falling away from 12470 where we warned about wave B rally already last week. So current strong leg down can be wave C of D) that is part of a big triangle correction. So despite very strong bearish momentum, do not fall in love with bears just yet, as there can be an interesting support for another three wave rally from 11960-12100 area.

German dax, 1h

If DAX is going to see weakness this week, especially after that completion of wave E) of a triangle, then USDJPY can see more weakness as well, in correlation with other xxx/JPY pairs. On USDJPY we are observing a triangle and would love to try to get on the short side but after a completed wave E rally into 106.50 resistance. At the same time we may see EURUSD turn up after a completed a-b-c drop from 1.2445 high.

USDJPY, 1H

EURUSD, 1H

CRUDE OIL Taking Profits

Crude oil is decreasing following recent rise at 62.54 and heading for the 61.50 range. Hourly support and resistance remain at 59.72 (15/02/2018 low) and 66.33 (25/01/2018 high). The technical structure suggests short-term decline.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being, the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance is located at 77.83 (20/11/2014). Crude oil is trading largely above its 200 DMA.

SILVER Riding Lower

Silver recovery collapses, the currency starts back its consolidation phase following recent high at 16.50, approaching hourly support at 16.18 (09/02/2018 low). Hourly resistance at 16.98 (15/02/2018 high) is distanced. The short-term technical structure suggests further short-term decrease.

In the long-term, the trend remains negative/ sideways. Further downside is very likely. The pair is trading below its 200 DMA. Resistance is located at 21.58 (10/07/2014 high). Strong support can be found at 11.75 (20/04/2009).

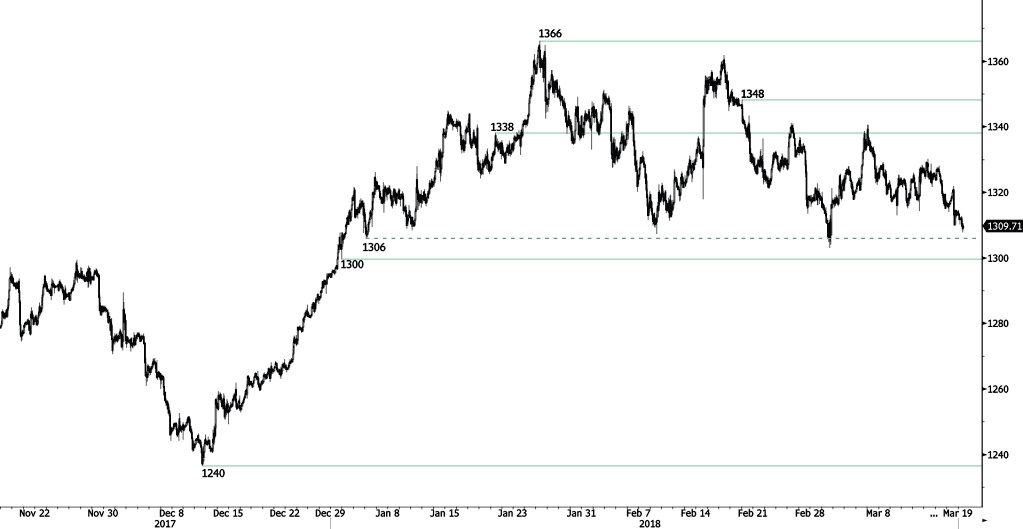

GOLD Bearish Pressures

Gold is decreasing following recent increase at 1323, approaching hourly support at 1300 (29/12/2017 low) and expected to decline at the 1308 range. Hourly resistance at 1338 (19/02/2018 high) is distanced. The technical structure suggests further short-term decrease.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1'392 (17/03/2014) is required to confirm it. A major support can be found at 1'045 (05/02/2010 low).

BITCOIN Further Sideways Consolidation Likely

Bitcoin trades indistinctly at the 8200 range, breaking hourly support at 7614 (02/02/2018 low) and expecting to trade sideway in the shortterm. Hourly support and resistance are given at 6797 (06/02/2018 low) and 12130 (18/01/2018 high).

In the long-term, the digital currency has had an exponential growth but also presented important downturns. There is decent likelihood that the currency could stabilize between 7'000 - 12'000 in 2018. Bitcoin is approaching its 200 DMA (7000 range).