Sample Category Title

Markets not too surprised at Gary Cohn’s resignation, DOW ended flat

So it finally happened. White House economic top economic adviser Gary Cohn resigned. It's reported that the decision was made hours after direct confrontation with Trump regarding the steel and aluminum tariffs. Trump requested Cohn to publicly support the tariff plan. But Cohn, as a free trade advocate, didn't answer. The meeting with industry executives, arranged by Cohn for persuading Trump not to impose the tariffs, was also canceled.

Cohn said in a statement that "it has been an honor to serve my country and enact pro-growth economic policies to benefit the American people, in particular the passage of historic tax reform."

Trump said regarding Cohn that "Gary has been my chief economic adviser and did a superb job in driving our agenda, helping to deliver historic tax cuts and reforms and unleashing the American economy once again." And, "he is a rare talent, and I thank him for his dedicated service to the American people."

Stock markets reaction to the news was quiet muted. DOW continued to struggle around 55 H EMA, closed up 0.04% at 24884.12/. Technically, it's also in proximity to 25000 handle, 50% retracement of 25800.35 to 24127.47 at 25008.91. This will a key near term hurdle for DOW to overcome.

S

S

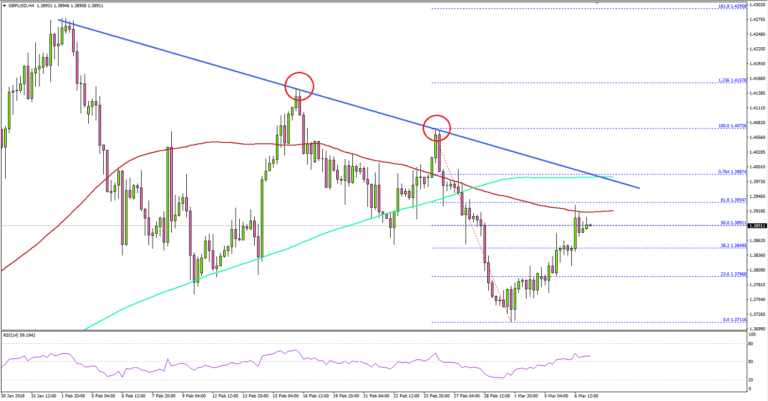

GBP/USD Is Approaching Crucial Resistance

Key Highlights

- The British Pound started a new upside wave and traded above 1.3800 against the US Dollar.

- There is a crucial bearish trend line forming with resistance at 1.3980 on the 4-hours chart of GBP/USD.

- The US Factory orders declined 1.4% in Jan 2018, more than the forecast of -1.3%.

- The US Trade Balance figure for Jan 2018 will be released today, which is forecasted to register a deficit of $-55.1B.

GBPUSD Technical Analysis

The British Pound found a strong support near 1.3700 against the US Dollar, and recovered. The GBP/USD pair traded higher recently and moved above 1.3800.

The current price action is positive above 1.3800, but the pair is facing a major resistance on the upside near 1.3980.

Looking at the 4-hours chart, there was a support base formed at 1.3711 and the pair moved above the 23.6% Fib retracement level of the last decline from the 1.4072 high to 1.3711 low.

The last few candles are positive, but there is a crucial bearish trend line forming with resistance at 1.3980 on the same chart. Moreover, the 76.4% Fib retracement level of the last decline from the 1.4072 high to 1.3711 low is at 1.3987.

Moreover, the 200 simple moving average (green, 4-hour) is also near 1.3980. Therefore, it won’t be easy for buyers to break the 1.3980 resistance area.

On the downside, supports are seen at 1.3820 and 1.3800. Below 1.3800, the pair may retest the 1.3750 support.

Recently, the US Factory orders report for Jan 2018 was released by the US Census Bureau. The market was looking for a decline of 1.3% in orders compared with the previous month.

The result was disappointing, as there was a decline of 1.4% in orders, which was a lot worse than the last revised reading of +1.8%.

Overall, there was a minor increase in the bearish pressure on the US Dollar, which may continue to help pairs such as EUR/USD and GBP/USD.

Economic Releases to Watch Today

- Euro Zone Gross Domestic Product Q4 2017 (QoQ) – Forecast 0.6%, versus 0.6% previous.

- BoC Interest Rate Decision – Forecast 1.25%, versus 1.25% previous.

- US ADP Employment Change Feb 2018 – Forecast 195K, versus 234K previous.

- US Trade Balance Jan 2018 – Forecast $-55.1B, versus $-53.1B previous

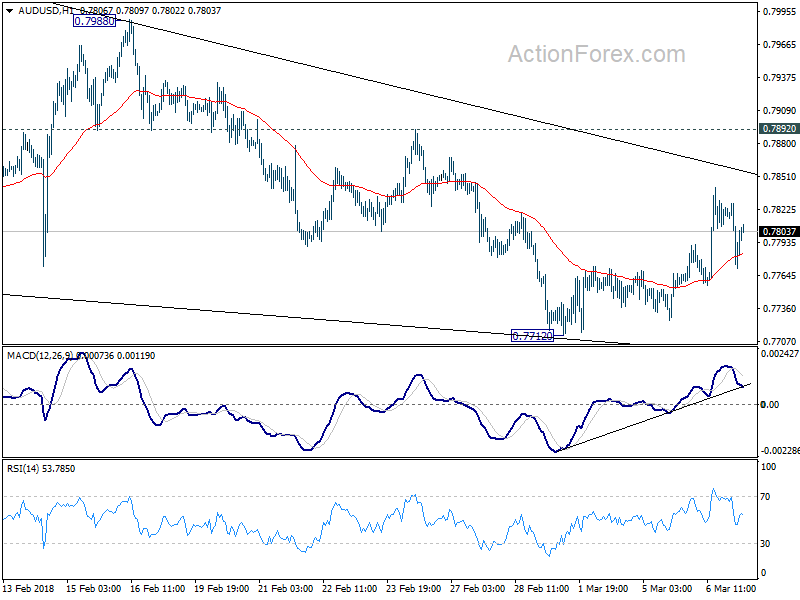

Australia GDP Q4: 0.4% qoq, AUD/USD pressing 55 H EMA

Australia GDP Q4: 0.4% qoq vs exp 0.5% qoq vs prior 0.7% qoq

Australia GDP Q4: 2.4% yoy vs exp 2.5% vs prior 2.9% yoy

From the release: Chief Economist for the ABS, Bruce Hockman, said: "Growth this quarter was driven by the household sector, with continued strength in household income matched by growth in household consumption."

AUD/USD struggling to break 55 day EMA and topped at 0.7814. Rebound from 0.7712 is corrective looking. Focus back on whether 55 H EMA could hold.

Cohn Shocker

Cohn Shocker

The morning Whitehouse shocker is that Gary Cohn is resigning as head of the White House’s National Economic Council. His resignation increased the risk tenfold that President Trump will follow through with far-reaching trade tariffs given that Cohn was said to be remaining in his role to convince Trump to reverse his trade policy views, or at least temper them.

Predictably USDJPY is wearing the initial brunt of the move, and in general, the Cohn announcement is reversing the positive risk sentiment from the unexpected news from North Korea after reports that North Korea is open to denuclearisation if the safety of its regime is guaranteed.

While the world appears to be in a safer place this morning due to the denuclearisation olive branch offered by North Korea, the market is no less safe from the wrath of Trump’s trade policies.

Gold Prices

Gold was trading positively overnight on the back of the softer USD trend BS continues to perform exceptionally well on that narrative. But prices will remain firmly supported on the tariff tail risks from Cohn departure as the tariff gambit hits the market again with blunt force.

Oil Prices

What goes up must come down or the opposite in the case of US oil inventories data. The American Petroleum Institute (API) reported a considerable build of 5.661 million barrels for the week ending March 2, e doubling up analysts expectations. Early trade WTI prices remain tentatively supported by the weaker dollar. But with the overhang from the Cohn resignation yet to filter through market’s, risk aversion could see OIl prices move lower during today session.

Overnight long USD hedges were unwound as on the news from South Korea that North Korea was willing to hold talks with the United States on denuclearisation

Currency Markets

Japanese Yen

A bit of a topsy-turvy 24 hours for USDJPY spiked on the Korea headlines from 105.90 towards 106.40, which was pips shy of the significant 106.50 support. But is back plumbing the depths this morning as Tariffs are back in play on the back of Cohn’s resignation.

US politics is an absolute mess inspiring little confidence in the President, and this real-life political melodrama unfolds it hard to avoid parallels with Tumps for TV show The Apprentice.

The Malaysian Ringgit

Decision day for the BNM but the market is expecting few if any fireworks. Regional currency sentiment received a boost after surprising news that North Korea is open to denuclearisation if the safety of its regime is guaranteed.

The prospect of trade tariffs is raising their ugly head again, but when all is said and done, these tit-for-tat tariffs are not significant enough factor to weigh on MYR sentiment let alone derail the buoyant global growth narrative.

Dollar Awaits US Jobs Data As Trade Uncertainty Remains

The USD was lower against most major pairs as trade fears receded and sparked a sell off of the American currency. The ADP will mark the first release of February employment data in the US at 8:15 am EST on Wednesday, March 7. Strong gains are expected from private payrolls with the market looking ahead to the U.S. non farm payrolls (NFP) on Friday with a special attention paid to the wages component seeking signs of higher inflation. The Bank of Canada (BoC) will release its rate statement at 10:00 am EST with no press conference to follow the release of the statement. Weekly crude inventories will be published at 10:30 am EST with the results guiding prices that are caught in a tight trading range.

- BOC expected to keep rates unchanged at 1.25%

- ADP payrolls report forecasted to show gain of 194,000 US jobs

- Weekly US crude inventories expected to increase buildup putting downward pressure on prices

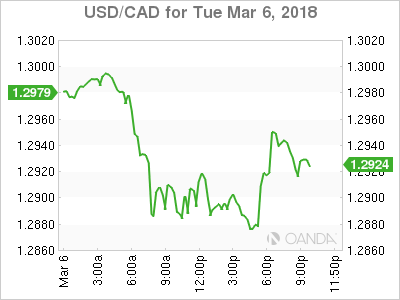

Canadian dollar rebounds despite US tough trade talk

The USD/CAD lost 0.52 percent in the last 24 hours. The currency pair is trading at 1.2898 ahead of the Bank of Canada (BoC) rate statement. The BoC will publish its statement on Wednesday, March 7 at 10:00 am. The central bank is not expected to make changes to the benchmark interest rate, keeping it unchanged at 1.25 percent. Canadian fundamentals have slowed down since the BoC hiked rates two times in 2017. The uncertain fate of NAFTA has also keep the loonie under pressure as Donald Trump’s words on trade are not reassuring investors the trade deal can be renegotiated.

The USD/CAD lost 0.52 percent in the last 24 hours. The currency pair is trading at 1.2898 ahead of the Bank of Canada (BoC) rate statement. The BoC will publish its statement on Wednesday, March 7 at 10:00 am. The central bank is not expected to make changes to the benchmark interest rate, keeping it unchanged at 1.25 percent. Canadian fundamentals have slowed down since the BoC hiked rates two times in 2017. The uncertain fate of NAFTA has also keep the loonie under pressure as Donald Trump’s words on trade are not reassuring investors the trade deal can be renegotiated.

The BoC is still expected to raise rates three more times in 2018 to keep up with the U.S. Federal Reserve. The US central bank is anticipated to hike three or four times this year as the economy keeps growing at steady pace, with the biggest question mark being the slow path of inflation. The fourth quarter of 2017 marked a slowdown of Canadian indicators after a strong Q3, but the close relationship it has with the US and the White House’s tough talk on trade are keeping the USD/CAD near 1.30 despite the market selling off the USD to seek higher returns. The lonnie recovered ahead of the BoC but all eyes will be on the U.S. jobs data this week looking for signs of US inflation and validating four rate hikes from the Fed this year.

The CAD and the MXN recovered from earlier setback as the anti-trade rhetoric from Washington has moved to the background, but with the NAFTA renegotiations talks leaving very little to show for seven rounds it would apear it could be a short lived respite. Mid term elections in the US and presidential elections in Mexico will make the team of negotiators harder as the trade agreement will become a political target.

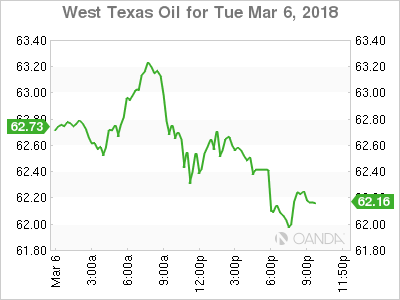

The price of energy is close to its opening price on Tuesday. West Texas Intermediate is trading at $62.60 after opening in Asia at 62.73. Crude is trading in a tight range oil ahead of the weekly US crude inventories release on Wednesday, March 7 at 10:30 am EST. The Organization of the Petroleum Exporting Countries (OPEC) partnered with other major producers to limit oil production but the stage is set for the US and other nations who did not join the agreement to start ramping up supply. The International Energy Agency released today a report forecasting that 80 percent of global demand will be met by non-OPEC producers.

The softness of the USD after trade talks and North Korea closer to a historic summit with North Korea have kept the price of energy from falling ahead of the release of crude stocks in the US. The market is forecasting a rise of 2.5 million barrels in crude inventories.

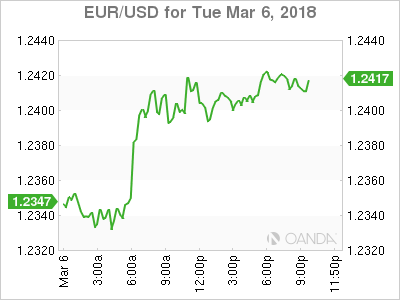

The EUR/USD gained 0.57 percent on Tuesday. The single currency is trading at 1.2406 after the EUR has recovered from the political anxiety going into the previous weekend. Italian election results came in as predicted with a hung parliament as the most likely outcome but noting a rise of anti Europe representation. The German coalition formed a new government with the SDP once again teaming up with Merkel’s CDU/CSU to form a grand coalition despite their initial reluctance. In Germany like in Italy nationalist parties are on the rise making it harder for pro European parties to stay in power without coalition partners. The political hurdles behind the euro rose against the US dollar and is looking ahead at the European Central Bank (ECB) monetary policy meeting on Thursday.

The ECB is not expected to announce any major changes but could continue playing its neutral card as economic indicators have not been impressive of late, added to that is the rise of anti-trade rhetoric in the US but the central bank could still remove key language in its statement clearing the way for an end of quantitive easing in Europe. The rhetoric form the ECB will be measured to avoid sounding too hawkish, while at the same time avoiding a rise in the currency. The ECB is due to release its economic forecasts, but economists do not expect major deviations from previous targets.

Market events to watch this week:

Wednesday, March 7

8:15am USD ADP Non-Farm Employment Change

8:30am CAD Trade Balance

10:00am CAD BOC Rate Statement

10:00am CAD Overnight Rate

10:30am USD Crude Oil Inventories

7:30pm AUD Trade Balance

Thursday, March 8

7:45am EUR Minimum Bid Rate

8:30am EUR ECB Press Conference

Midnight JPY BOJ Policy Rate

Midnight JPY Monetary Policy Statement

Friday, March 9

JPY BOJ Press Conference

4:30am GBP

Manufacturing Production m/m

8:30am CAD Employment Change

8:30am USD Average Hourly Earnings m/m

8:30am USD Non-Farm Employment Change

Gold Jumps As Tensions Over Trump Tariffs Weighing On Dollar

Gold has posted sharp gains in the Tuesday session. In North American trade, the spot price for an ounce of gold is $1336.39 up 1.19% on the day. In economic news, there are no major US events. Factory Orders were unexpectedly soft, with a decline of 1.4%. This was well short of the estimate of -0.4%. On Wednesday, the US releases ADP Nonfarm Employment Change.

In the US, tensions over proposed tariffs on steel imports continue to hurt the US dollar, which has been a boon for gold prices on Tuesday. President Trump appears set on applying stiff tariffs of 25% on steel, much to the consternation of the European Union and other US trading partners. However, there is plenty of domestic opposition to Trump's plan, as Republican lawmakers, including House Speaker Paul Ryan, have come out strongly against the move. If Trump doesn't back down, the Republicans could even resort to legislation to limit Trump's authority on tariffs. The announcement of the tariffs last week sent the dollar broadly lower, and if the tariffs are introduced, negative investor sentiment could keep the gold rally going. Until this dispute is resolved, traders should be prepared for continuing volatility in gold prices.

Gold prices often climb in response to geopolitical tensions, and Britain's exit out of the European Union seems to be getting bumpier each day. Tensions are growing between London and Brussels as the Brexit deadline of March 2019 looms ever closer. Last week, there were sharp exchanges between the two sides after the EU releases a draft of the legal framework of the Brexit agreement. On Friday, Prime Minister May outlined her vision of relations between the EU and Britain after Brexit. May sought to lower the recent sharp rhetoric surrounding Brexit, saying that both sides needed to show flexibility in order to reach an agreement. May said that she was seeking a free trade agreement with the EU that included financial services. The response from Brussels has been lukewarm, with some policymakers saying that Britain continues to operate under the illusion that it can leave the club but still enjoy the benefits.

Cohn Out, USD Tumbles, Futures Shaken

Equity index futures are down sharply (S&P minis -33 pts or -1.2%) after the announced resignation of White House top economic advisor Gary Cohn, long regarded as the remaining "adult in the room" when it came to economic/fiscal policy was instrumental in shaping up Trump's tax reform. Cohn's sharp disagreement with Trump's trade war approach is widely attributed to his departure. A new Premium trade has been issued earlier today. There are 10 Premium trades in progress; 8 in the green, 1 flat and 1 at a loss.

The twists and turns of tariff talk gave the loonie some relief on Tuesday. Trump tied them to a new NAFTA deal and, at the same time, Congress and business lobbies have rallied to head off a trade war. USD/CAD touched just above 1.3000 before sinking down to 1.2875.

The drop erases Monday's gain and leave some uncertainty about a break above the late-2017 highs. That's likely to be resolved with the Bank of Canada rate decision on Wednesday. The OIS market is pricing in a 13% chance of a hike but even that number is too high with virtually no economist is predicting a move.

The latest round of economic data in Canada sharply deteriorated and that's compounded by the trade talk. The previous BOC statement included the line "recent data have been strong" and that's almost certain to be downgraded.

Guidance, however, is likely to remain largely intact so the risks to the loonie are probably modest. That said, the BOC certainly has a flair for the dramatic and officials will tread cautiously on trade.

The bigger current question for the loonie is about the uncertainty between any implementation of tariffs and a NAFTA agreement. It's unclear if the White House will give Mexico and Canada a waiver while NAFTA negotiations continue. If not, that would provoke a kneejerk lower in CAD and MXN.

One indicator that can't be overlooked on Wednesday is trade data from the US and Canada. We've written recently about the rising US trade deficit and corresponding risks of clumsy policies to counteract it. The US trade deficit is expected at $55 billion per month in January.

Eco Data 3/7/18

[php_everywhere instance="1"]

British Pound Edges Higher, Investors Eye ADP Employment Report

The British pound has posted gains on Tuesday, continuing the upward movement seen on Monday. In North American trade, GBP/USD is trading at 1.3884, up 0.26% on the day. In economic news, there are no major indicators in the US or the UK. In the US, Factory Orders were unexpectedly soft, with a decline of 1.4%. This was well short of the estimate of -0.4%. On Wednesday, the US releases ADP Nonfarm Employment Change.

Tensions are growing between London and Brussels as the Brexit deadline of March 2019 looms ever closer. Last week, there were sharp exchanges between the two sides after the EU releases a draft of the legal framework of the Brexit agreement. On Friday, Prime Minister May outlined her vision of relations between the EU and Britain after Brexit. May sought to lower the recent sharp rhetoric surrounding Brexit, saying that both sides needed to show flexibility in order to reach an agreement. May said that she was seeking a free trade agreement with the EU that included financial services. The response from Brussels has been lukewarm, with some policymakers saying that Britain continues to operate under the illusion that it can leave the club but still enjoy the benefits.

Over in the US, the “tariff tussle” shows no sign of being resolved anytime soon. US President Trump appears set on applying stiff tariffs on steel imports, much to the consternation of the European Union and other US trading partners. However, there is plenty of domestic opposition to Trump’s plan, as Republican lawmakers, including House Speaker Paul Ryan, have come out strongly against the move. If Trump doesn’t back down, the Republicans could even resort to legislation to limit Trump’s authority on tariffs. The announcement of the tariffs last week sent the dollar broadly lower, and if the tariffs are introduced, negative investor sentiment could send the greenback to lower levels.

25000 too much for DOW? Mnuchin backs tariffs

25000 proves to be too much for DOW? It opened higher and hit as high as 24995.24. But stocks seem to response negatively to Treasurer Steve Mnuchin's backing on steel and aluminum tariffs. Mnuchin said in House:

- Regarding Trump's tariffs - "I am supportive of them and I am supportive of the mechanisms that the president has announced,"

- “To the extent that we’re successful in renegotiating Nafta, those tariffs won’t apply to Mexico and Canada.” (same position as Trump)

- "We're not looking to get into trade wars."

- "We're looking to make sure that U.S. companies can compete fairly around the world."

- He brought up China too. (?!) "President Trump has been very clear: We want to make sure U.S. companies have the same ability to do business in China as Chinese companies have here."

- And, "our priority at the moment is to renegotiate NAFTA and to focus on our trade relationships with China and have fair and balanced trade with China."

Facts: China is the 11th imports of steel to US in 2017. India ranked 10 with contribution merely 2%. Canada was top at 16%, Mexico 4th at 9%.