Sample Category Title

German Coalition Decision Among Events that May Shake the Euro

The upcoming weekend promises to be an eventful one for European assets. On Sunday, while Italians head to the polls to elect their new leader, Germans will find out whether they have a new government, as the SPD party will announce if its members have approved another "grand coalition" with Merkel's conservatives. The party's decision could have wide-ranging effects for Germany's political stability and by extent, for the common European currency.

Germany has been entangled in political coalition talks for several months now, ever since the election in September did not produce a clear winner. Chancellor Merkel, who's party received the most votes in September but fell short of gaining a majority, has repeatedly rejected the prospect of forming a minority government, signaling that she is comfortable heading for early elections if coalition talks collapse. Her last realistic chance at forming a viable coalition is with the SPD party, her former coalition partners. Meanwhile, the SPD's leadership shied away from agreeing to a partnership directly, and instead opted to put that decision to its members via a postal vote, with the results due to be published on Sunday.

Given the speed at which the euro gained during the early weeks of 2018, one would be forgiven to forget that Europe's largest economy is facing a minor leadership crisis. To be fair, the euro's surge was mostly associated with expectations that the ECB will begin scaling back its massive stimulus program soon, not politics. Still, whether or not Germany acquires a stable and pro-EU government could hold implications for the common currency, as well as European equities. In other words, the euro managed to rally despite looming political risks, and while the ECB's actions may be the biggest driver for the currency, politics still play a significant role.

In case the SPD members finally approve the coalition offer, that would probably lift the cloud of political uncertainty currently hanging over Germany, and perhaps help the euro to resume its broader uptrend. Looking at euro/dollar, it could edge higher in this scenario and aim for a test of the 1.2350 territory, marked by the peaks of February 21, 22, and 26. If buyers manage to overcome that hurdle, the next area that may provide some resistance is 1.2390, identified by the lows of February 19.

A rejection by the SPD, on the other hand, is likely to exert downward pressure on the world's most traded currency pair, as uncertainty heightens and the probability for early elections rises dramatically. An unstable political situation in Germany would also diminish the likelihood that a Franco-German partnership pushes forward with implementing the EU reforms that French President Macron has repeatedly called for over the past year. Euro/dollar may continue to correct lower and test the 1.2205 zone again, the February 9 low. A downward violation of that hurdle could set the stage for declines towards the pair's latest lows, at 1.2150.

As for which is more likely, recent opinion polls generally point to SPD members approving the deal, but by a narrow majority. Considering that such polls carry a considerable margin of error though, and that polling has not been the most reliable predictor of major political events in recent years, it is debatable how much importance one should attach to these surveys.

Besides the German coalition outcome, price action in euro pairs is likely to be affected by how the election in Italy plays out as well. Moreover, the ECB is set to meet next week and thus, market attention may shift back to economics before too long, especially since the Bank is anticipated to tweak its policy language in a more hawkish direction at this gathering.

Sunset Market Commentary

Markets:

Global core bonds lost marginally ground today amid an empty eco calendar. The market move is somewhat remarkable as yesterday's trading themes remained at play. US tariffs on steel and aluminum raised fears of trade wars. President Trump added fuel to the fire by stating that trade wars are a good thing and easy to win. European stock markets lose again up to 2%, but no longer support core bonds. It's an indication that general sentiment towards core bonds is structurally negative. Rising real rates, higher inflation expectations and a hawkish shift in tone by the Fed are the main drivers behind US yields' push higher. Technically, the German 10-yr yield failed to break below 0.62% support. Yields can start a new upleg if worst case scenarios are avoided in this weekend's political events (Italian elections, SPD vote on coalition agreement). The US yield curve bear steepens at the time of writing with yields 1.4 bps (2-yr) to 3.4 bps (30-yr) higher. The German yield curve bull flattens with yields up to 2.4 bps (30-yr) lower. An overnight effect is at play as US yields corrected lower yesterday evening. 10-yr yield spread changes versus Germany widen up to 2 bps with Greece (-7 bps) underperforming.

Yesterday's announcement of US president Trump on import tariffs abruptly aborted a tentative USD rebound. This theme remained the dominant factor for global FX trading today. There were hardly any eco data to guide trading. The USD decline slowed temporary this morning. Markets apparently pondered the seriousness of the consequences. However, the risk-off trade intensified again as US president Trump indicated that he wouldn't backtrack on his intentions, triggering a new USD downleg. EUR/USD jumped back above the 1.23 area. USD/JPY extended its downtrend. The pair dropped below the 105.50 area. The political event risk in Europe (Italian elections and SPD approval of German government coalition) has no negative impact on the euro for now. USD weakness prevails.

Sterling trading was driven by the potential consequences of UK PM May's Brexit speech for the negotiations between the EU and the UK. Over the previous days, it became already clear that the water between the UK and the EU remains very deep. Today's speech didn't bring much progress on the way to a solution. UK PM May put forward five tests for the Brexit negotiations. However, the implementation of those principles, e.g with respect to the Irish boarder, will meet EU objections. Sterling was in the defensive (against the euro) earlier this week and May's speech didn't change that. EUR/GBP tries to regain 0.8930 intermediate resistance. Cable gained marginally ground today, as the dollar and sterling both faced serious headwinds. The pair trades close to, but slightly below 1.38. The UK construction PMI was marginally stronger than expected, but it was no issue for sterling trading.

News Headlines:

The Norwegian government announced that it will lower the Norges Bank's inflation target from 2.5% to 2%. The Norges Bank will adopt a forward-looking and flexible approach toward inflation targeting so the policy can support the economy and counter financial imbalances, according to the statement.

President Donald Trump's planned tariffs prompted angry responses from U.S. allies around the globe Friday, driving down stock prices and generating warnings of a possible international trade war. EU trade commissioner Malmstrom said that the EU will consider imposing its own safeguard tariffs on imports of steel and aluminium.

British PM May called for a deep partnership with the European Union after Brexit, setting out ambitions for a tailor-made deal with independent arbitration and new arrangements for regulation and financial services.

A Ho-Hum End to 2017 for the Canadian Economy

The Canadian economy closed out 2017 on a ho-hum note as GDP rose 1.7% in Q4 (Q/Q, SAAR), roughly matching the previous quarter's revised pace of 1.5%. Healthy gains in export prices led to significant gain in nominal output, which rose a robust 6.5%. Over 2017 as a whole, real GDP expanded by 3.0%, while nominal growth was a brisk 5.3% - the strongest pace since 2011.

Leading growth higher was investment, which climbed 9.6% in aggregate. Investment in residential investment surged ahead, up 13.4%. New construction gained 12.7%, while ownership transfer costs surged 42.8% likely reflecting a recovery from prior quarters as well as the pull-forward of activity ahead of January's changes to mortgage underwriting rules. Non-residential investment also came in strong: non-residential structures investment rose 5.4%, while investment in machinery and equipment rose 12.7%. Government investment was up 10.3%.

Canadian consumers cooled their jets somewhat as household consumption slowed somewhat, to 2.1%. The pace of goods spending ticked down slightly, to 1.6% (Q3: 1.2%), while spending on services slowed to 2.5% from 5.7% previously.

Trade took a significant bite out of headline growth (subtracting 1.1 percentage points) as export growth (+3.0%) failed to keep up with imports (+6.3). Inventories also subtracted from growth (-0.7 percentage points) as firms added slightly less to their stocks.

It was another quarter of solid income gains, as aggregate employment compensation climbed 6.1% - its strongest gain since 2011. This was down largely to a 6% gain in wages and salaries. Household disposable income was up a solid 5.2%, leading to a slight uptick in the household savings rate, to 4.2%, from an upwardly revised rate of 4% previously.

Momentum heading into 2018 is modest. Monthly GDP was up 0.1% month-on-month in December as 13 of 20 major industries expanded. The goods-producing side of the economy pulled back slightly (-0.1%) on weakness in manufacturing (-0.7%) and construction (-0.3%). Services (+0.1%) held up, bringing its run of uninterrupted growth to 21 months as weakness in wholesale and retail trade were offset by gains in nearly all other categories.

Key Implications

Fade the headline on this one. Trade may have led fourth quarter growth to disappoint our earlier expectations, but the story today is one of a still-healthy domestic economy - final domestic demand rose a robust 3.9%, a strong performance to close what has been a strong year. Strength in investment, notably on the non-residential side was an encouraging sign, while government spending also provided a backstop to growth. One quarter is hardly a trend, but the modest slowing of consumer spending towards a more sustainable pace is to be expected in light of high household indebtedness and rising interest rates.

To be sure, headwinds are mounting. The surge in residential investment was almost certainly due to a pull-forward of activity ahead of mortgage underwriting changes. Data received so far for 2018 indicates that this sector will see a big reversal in Q1. Trade also remains a wildcard, with a plethora of near-term headwinds. On the flip side, healthy income gains, a moderately favourable investment environment (at least for domestically-focused firms), and ongoing government stimulus all suggest that growth is likely to continue, albeit at a more sustainable pace.

Turning to the Bank of Canada, the wages and salaries measure of the national accounts, which a January research note notes has the highest weight in their 'wage-common' measure - roared ahead in Q4. This is up 4.9% year-on-year and continues a now six-quarter run of acceleration, marking its fourth straight quarter of gains above 3%. External uncertainties, the impact of past rate hikes and changes to mortgage underwriting rules all suggest that the best approach for now is to 'wait and see.' Still, with Canada in the mature part of the economic cycle and inflation pressures continuing to rise, more rate hikes are likely in store.

Q4 GDP Growth in Canada Remains Moderate

Highlights:

- Canadian Q4 GDP growth rose an annualized 1.7% which was slightly below expectations of a 2.0% gain.

- Monthly December GDP growth rose 0.1% following a 0.4% gain in November. Our expectation is that rising interest rates will keep both monthly and quarterly GDP growth little changed going in 2018 though U.S. trade policy is presenting a growing downside risk.

Our Take:

The 1.7% (annualized) gain in Q4 GDP and the revised 1.5% gain in Q3 are down significantly from the unexpectedly strong average increase of 3.7% from mid-2016 to mid-2017. This earlier strength resulted from a cessation of sizeable declines in energy investment along with consumers continuing to respond to historically low interest rates. The resulting strong pace of activity had the impact of moving the economy to capacity by mid-2017. Thus the slowdown in growth over the second half of last year is not unwanted and will help insure the economy does not move too far into excess demand and stoke inflation pressures. In fact the intent of policy going forward will be to sustain growth close to the economy's potential rate, which is assumed to be around 1.6%. Our forecast assumes that such will be achieved by the Bank of Canada continuing to move the overnight rate gradually higher by 25 basis points per quarter through early next year. Given the hike in January and the Q4 growth coming in slightly below the Bank's projected increase of 2.5%, though, our expectation is that the central bank will remain on the sidelines at the next Wednesday's policy meeting.

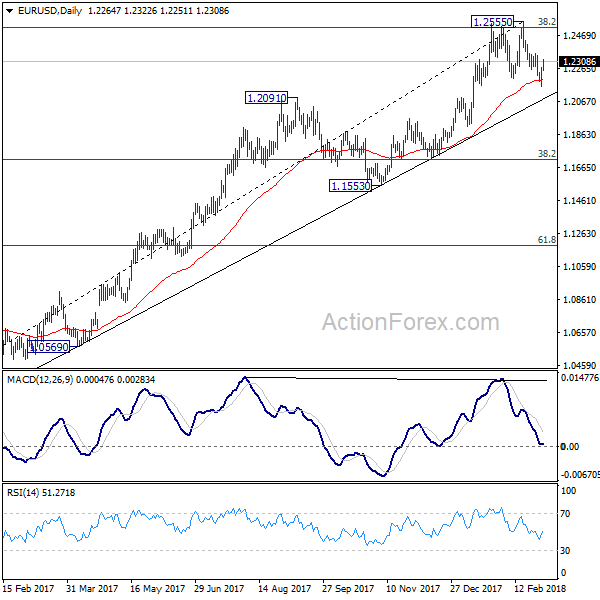

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2173; (P) 1.2207 (R1) 1.2227; More....

EUR/USD's rebound from 1.2154 but stays below 1.2354 minor resistance. Intraday bias remains neutral first. On the upside, break of 1.2354 will indicate that pull back from 1.2555 has completed. In such case, intraday bias will be turned back to the upside for 1.2555 high. Break there will carry larger bullish implication. On the downside, break of 1.2154 will revive the case of trend reversal and turn outlook bearish for 38.2% retracement of 1.0339 to 1.2555 at 1.1708.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.5553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

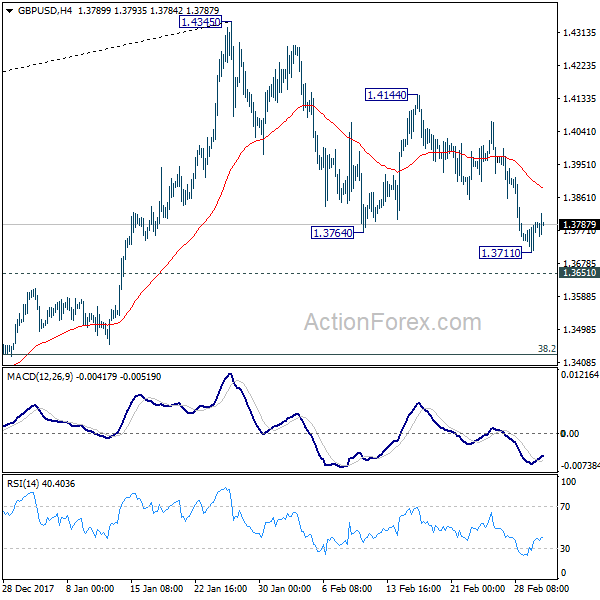

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3729; (P) 1.3756; (R1) 1.3802; More....

Intraday bias in GBP/USD remains neutral at this point. Further fall is still expected as long as 1.4144 resistance holds. Below 1.3711 will target 1.3651 resistance turned support and below. At this point, such fall is viewed as a corrective move. Hence, we'll look for strong support from 38.2% retracement of 1.1946 to 1.4345 at 1.3429 to contain downside and bring rebound.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279) so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

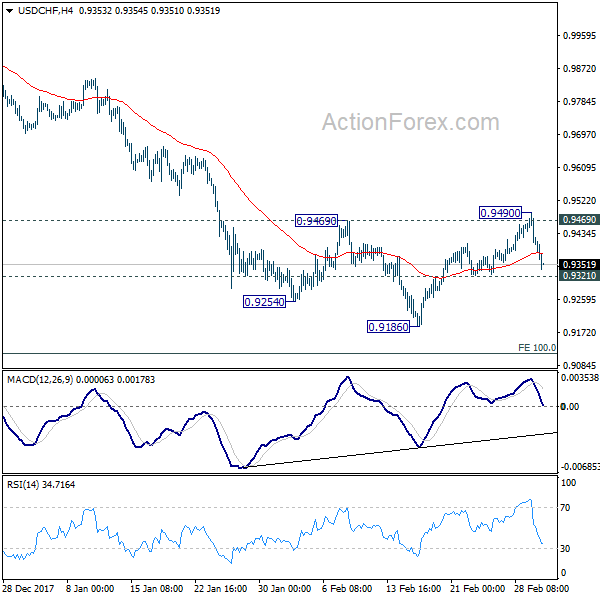

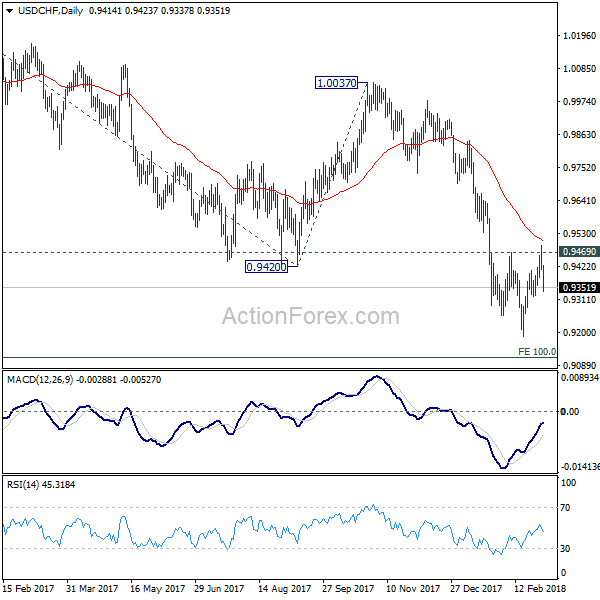

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9388; (P) 0.9439; (R1) 0.9468; More...

USD/CHF's fall from 0.9490 continues but it's staying above 0.9321 minor support. Intraday bias remains neutral first. Rejection from 0.9469 resistance retained near term bearishness. Below 0.9321 will target a test on 0.9186 low. Break will resume larger down trend to 0.9115 medium term projection level next. On the upside, break of 0.9490 should indicate near term trend reversal, on bullish convergence condition in 4 hour MACD.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

Global Markets Tumble Further as Trump Declares Trade Wars are Good, Dollar Pressured

Risk aversion continues to be the main theme today as US President Donald Trump declared that trade wars are good. At the time of writing, German DAX is trading down -2.2%, French CAC down -1.9% and UK FTSE down -1.1%. That follows -2.5% decline in Japanese Nikkei. US futures are pointing to triple digit decline in DOW at open. In the currency markets, Dollar is suffering steep selling against Euro, Yen and Swiss Franc. Nonetheless, commodity currencies are even weaker with Canadian Dollar leading the way down.

Dollar suffers again as Trump said trade wars are good

Fresh selling is seen in Dollar after latest tweet by Trump. He said in early morning that "when a country (USA) is losing many billions of dollars on trade with virtually every country it does business with, trade wars are good, and easy to win." This is a follow up to the news that Trump is going to impose tariffs of 25% on steel and 10% on aluminum. And he plans to announce that formally next week.

It should be noted again that accord to data of IHS Global Trade Atlas, in 2017, Canada was the top supplier of steel to the US, with 16% share. It's followed by Brazil (13%), South Korea (10%), Mexico (9%), Russia (9%), Turkey (7%), Japan (5%), Taiwan (4%), Germany (3%) and India (2%). China is outside of top 10 at 11.

EU to react firmly against Trump's trade war

Response from EU regarding the planned tariff was firm. In a statement, "President of the European Commission, Jean-Claude Juncker said: "We strongly regret this step, which appears to represent a blatant intervention to protect US domestic industry and not to be based on any national security justification." And, "We will not sit idly while our industry is hit with unfair measures that put thousands of European jobs at risk." Juncker pledged "The EU will react firmly and commensurately to defend our interests. The Commission will bring forward in the next few days a proposal for WTO-compatible countermeasures against the US to rebalance the situation."

Data from European steel association Eurofer showed that Turkey was the bloc's biggest steel customer in 2017, with 20% share. The US was just the second with 15% share. Also, that's only around 2% of EU's total steel production.

Canadian Foreign Minister Chrystia Freeland said the country buys more than half of American steel. And the results in a USD 2b surplus for the US. She criticized that it's "entirely inappropriate" for the US to consider Canada a national security threat. Freeland pledged that "we will always stand up for Canadian workers and Canadian businesses." And she warned that "should restrictions be imposed on Canadian steel and aluminum products, Canada will take responsive measures to defend its trade interests and workers."

In China, Foreign Ministry spokeswoman Hua Chunying sounded pedestrian. She warned that "in recent years, the global economy has still recovered slowly and the basis for the global recovery is is still unstable." And she urged all countries to "make concerted efforts to to cooperate to resolve the relevant issues, instead of taking trade restrictive measures unilaterally."

UK PM May to deliver Brexit speech at Mansion House

The markets are awaiting Prime Minister Theresa May's high profile speech regarding post Brexit UK-EU relationship. The speech will take place at Mansion House in London at 1:30pm local time. Accord to the extracts by her office, May would seek "broadest and deepest possible agreement - covering more sectors and co-operating more fully than any Free Trade Agreement anywhere in the world today." And, "rather than having to bring two different systems closer together, the task will be to manage the relationship once we are two separate legal systems."

May is expected to set out five "tests" for the deal with EU. They are:

- That any deal must respect the referendum result

- That any deal must not break down

- That any deal must protect jobs and security

- That any deal must be "consistent with the kind of country we want to be" - modern, outward-looking and tolerant

- That any agreement must bring the country together

On the data front

Canada GDP grew 0.1% mom in December, in line with consensus. Eurozone PPI rose 0.4% mom, 1.5% yoy in January. German import price index rose 0.5% mom in January, retail sales dropped -0.7% mom. UK construction PMI rose to 51.4 in February. New Zealand building permits rose 0.2% mom in January. Japan unemployment rate dropped sharply to 2.4% in January, monetary base rose 9.4% yoy in February, Tokyo CPI rose to 0.9% yoy.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.85; (P) 106.53; (R1) 106.90; More...

USD/JPY's medium term decline from 118.65 resumed by breaking 105.54 and reaches as low as 105.24 so far. Intraday bias remains on the downside for 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. Firm break there will target 98.97 key support level. On the upside, above 106.37 minor resistance will turn bias neutral first. But outlook will remain bearish as long as 107.67 resistance holds.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Jan | 0.20% | -9.60% | -9.50% | |

| 23:30 | JPY | Jobless Rate Jan | 2.40% | 2.80% | 2.80% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Feb | 0.90% | 0.80% | 0.70% | |

| 23:50 | JPY | Monetary Base Y/Y Feb | 9.40% | 9.20% | 9.70% | |

| 07:00 | EUR | German Retail Sales M/M Jan | -0.70% | 0.70% | -1.90% | -1.10% |

| 07:00 | EUR | German Import Price Index M/M Jan | 0.50% | 0.40% | 0.30% | |

| 09:30 | GBP | Construction PMI Feb | 51.4 | 50.5 | 50.2 | |

| 10:00 | EUR | Eurozone PPI M/M Jan | 0.40% | 0.40% | 0.20% | |

| 10:00 | EUR | Eurozone PPI Y/Y Jan | 1.50% | 1.60% | 2.20% | |

| 13:30 | CAD | GDP M/M Dec | 0.10% | 0.10% | 0.40% | |

| 15:00 | USD | U. of Mich. Sentiment Feb F | 99.5 | 99.9 |

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.85; (P) 106.53; (R1) 106.90; More...

USD/JPY's medium term decline from 118.65 resumed by breaking 105.54 and reaches as low as 105.24 so far. Intraday bias remains on the downside for 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. Firm break there will target 98.97 key support level. On the upside, above 106.37 minor resistance will turn bias neutral first. But outlook will remain bearish as long as 107.67 resistance holds.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

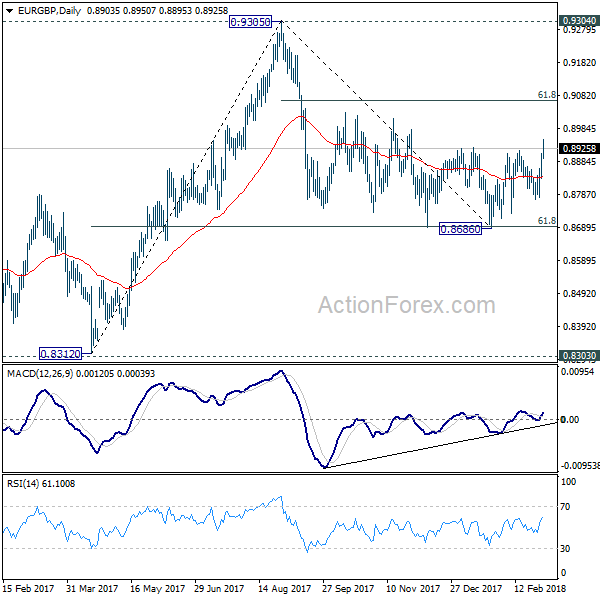

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8857; (P) 0.8883; (R1) 0.8929; More...

EUR/GBP surges to as high as 0.8950 today. The break of 0.8928 resistance now indicates medium term reversal. That is fall from 0.9305 has completed at 0.8868 after drawing support from 61.8% retracement of 0.8312 to 0.9305. Intraday bias is now on the upside for 61.8% retracement of 0.9305 to 0.8686 at 0.9069. Firm break there will target retest of 0.9305 high. On the downside, below 0.8877 minor support will turn intraday bias neutral again.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.